Management Accounting Report: Decision Making for Oshodi PLC Success

VerifiedAdded on 2021/02/21

|16

|4987

|38

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Oshodi PLC, a small manufacturing company. It explores various management accounting systems, including price optimization, cost accounting, inventory management, and job costing, and their benefits. The report details different types of management accounting reporting, such as budget reports, account receivable reports, performance reports, and job cost reports. It then produces income statements using both marginal and absorption costing methods for November and December, demonstrating how these techniques aid in financial reporting. Furthermore, the report examines planning tools for budgetary control and defines financial problems, comparing different organizations through the lens of management accounting, ultimately emphasizing the role of management accounting in achieving sustainable success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different kind of management accounting system............1

P2: Different types of management accounting reporting.....................................................3

M1: Benefits of management accounting systems.................................................................5

TASK 2............................................................................................................................................6

P3: Produce income statement by using marginal or absorption costing method..................6

M2: Apply accounting techniques to produce financial reporting documents.......................8

TASK 3............................................................................................................................................8

P4. Planning tools for budgetary control................................................................................8

M3: Application of planning tools for preparing and forecasting budgets..........................10

TASK 4..........................................................................................................................................10

P5: Define financial problem and comparison different organisation by masking the use of

management accounting system...........................................................................................10

M4: Management accounting in response to solve financial issue that can lead to the

sustainable success...............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different kind of management accounting system............1

P2: Different types of management accounting reporting.....................................................3

M1: Benefits of management accounting systems.................................................................5

TASK 2............................................................................................................................................6

P3: Produce income statement by using marginal or absorption costing method..................6

M2: Apply accounting techniques to produce financial reporting documents.......................8

TASK 3............................................................................................................................................8

P4. Planning tools for budgetary control................................................................................8

M3: Application of planning tools for preparing and forecasting budgets..........................10

TASK 4..........................................................................................................................................10

P5: Define financial problem and comparison different organisation by masking the use of

management accounting system...........................................................................................10

M4: Management accounting in response to solve financial issue that can lead to the

sustainable success...............................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

In the business world, there is a urge need of an effective and systematic approach which

enable management to control and manage different operation and activities in appropriate

manner and take decision to maximise output. Management accounting is refereed to be an

impressive approach that includes valid collection of financial information, making of

appropriate plans, taking useful decision that will help to increase the profit margin so easily

objective are accomplished (Alenius, Lind and Strömsten, 2015). To better understand the

importance of management accounting Oshodi plc have been selected that is a small

manufacturing company.

In this report, several management accounting system are discussed that help to make

decision and resolve financial issues, management report the analyse the internal performance

are elaborated. Costing techniques are used to prepare income statements which help in

determining the net profit for the year. In this report, planning tools are implemented in order to

prepare budgets and make effective solution to problems faced by company.

TASK 1

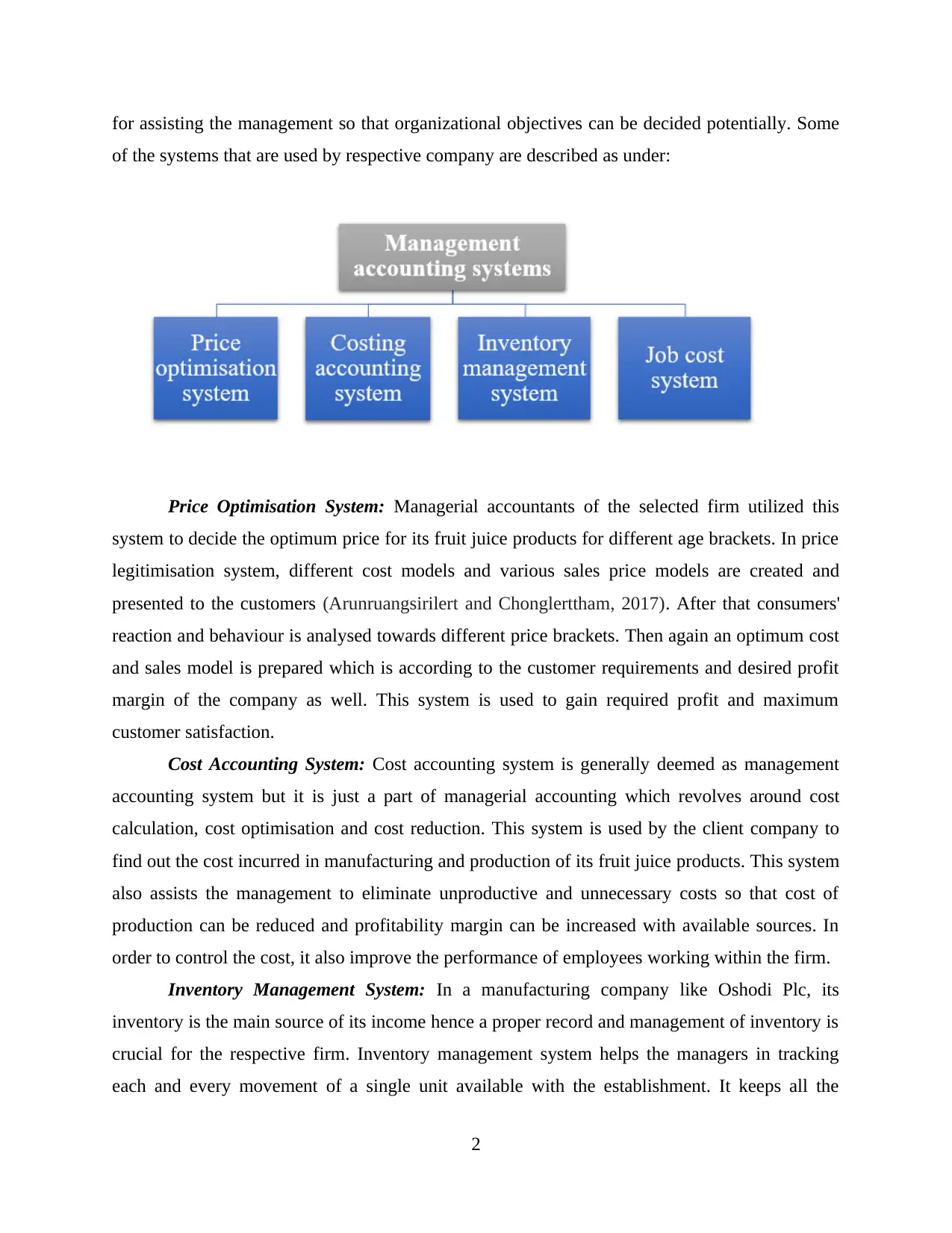

P1: Management accounting and different kind of management accounting system.

Management Accounting: It is also known as managerial accounting is a method which

prepare and present the historical and current financial and non-financial data in such a

professional way that it may assist the top administration in effective planning and decision

making process. The data and information provides by management accountant is used by

internal stakeholder specially the managers in order to strategic planning, risk management,

performance evaluation, etc. This accounting method uses various systems to help it in achieving

its objectives.

Management Accounting Systems: In order to provide information and content to

managerial accounting process, management accounting system has been evolved. With the help

of data provided by this system, managers are able to generate various accounts, reports, budgets

and strategies which eventually help the management in taking appropriate decisions and co-

ordination between revenue and expenses. The administration of Oshodi Plc. Uses different types

of this system so that impressive and effectively helpful accounts and statements can be created

1

In the business world, there is a urge need of an effective and systematic approach which

enable management to control and manage different operation and activities in appropriate

manner and take decision to maximise output. Management accounting is refereed to be an

impressive approach that includes valid collection of financial information, making of

appropriate plans, taking useful decision that will help to increase the profit margin so easily

objective are accomplished (Alenius, Lind and Strömsten, 2015). To better understand the

importance of management accounting Oshodi plc have been selected that is a small

manufacturing company.

In this report, several management accounting system are discussed that help to make

decision and resolve financial issues, management report the analyse the internal performance

are elaborated. Costing techniques are used to prepare income statements which help in

determining the net profit for the year. In this report, planning tools are implemented in order to

prepare budgets and make effective solution to problems faced by company.

TASK 1

P1: Management accounting and different kind of management accounting system.

Management Accounting: It is also known as managerial accounting is a method which

prepare and present the historical and current financial and non-financial data in such a

professional way that it may assist the top administration in effective planning and decision

making process. The data and information provides by management accountant is used by

internal stakeholder specially the managers in order to strategic planning, risk management,

performance evaluation, etc. This accounting method uses various systems to help it in achieving

its objectives.

Management Accounting Systems: In order to provide information and content to

managerial accounting process, management accounting system has been evolved. With the help

of data provided by this system, managers are able to generate various accounts, reports, budgets

and strategies which eventually help the management in taking appropriate decisions and co-

ordination between revenue and expenses. The administration of Oshodi Plc. Uses different types

of this system so that impressive and effectively helpful accounts and statements can be created

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for assisting the management so that organizational objectives can be decided potentially. Some

of the systems that are used by respective company are described as under:

Price Optimisation System: Managerial accountants of the selected firm utilized this

system to decide the optimum price for its fruit juice products for different age brackets. In price

legitimisation system, different cost models and various sales price models are created and

presented to the customers (Arunruangsirilert and Chonglerttham, 2017). After that consumers'

reaction and behaviour is analysed towards different price brackets. Then again an optimum cost

and sales model is prepared which is according to the customer requirements and desired profit

margin of the company as well. This system is used to gain required profit and maximum

customer satisfaction.

Cost Accounting System: Cost accounting system is generally deemed as management

accounting system but it is just a part of managerial accounting which revolves around cost

calculation, cost optimisation and cost reduction. This system is used by the client company to

find out the cost incurred in manufacturing and production of its fruit juice products. This system

also assists the management to eliminate unproductive and unnecessary costs so that cost of

production can be reduced and profitability margin can be increased with available sources. In

order to control the cost, it also improve the performance of employees working within the firm.

Inventory Management System: In a manufacturing company like Oshodi Plc, its

inventory is the main source of its income hence a proper record and management of inventory is

crucial for the respective firm. Inventory management system helps the managers in tracking

each and every movement of a single unit available with the establishment. It keeps all the

2

of the systems that are used by respective company are described as under:

Price Optimisation System: Managerial accountants of the selected firm utilized this

system to decide the optimum price for its fruit juice products for different age brackets. In price

legitimisation system, different cost models and various sales price models are created and

presented to the customers (Arunruangsirilert and Chonglerttham, 2017). After that consumers'

reaction and behaviour is analysed towards different price brackets. Then again an optimum cost

and sales model is prepared which is according to the customer requirements and desired profit

margin of the company as well. This system is used to gain required profit and maximum

customer satisfaction.

Cost Accounting System: Cost accounting system is generally deemed as management

accounting system but it is just a part of managerial accounting which revolves around cost

calculation, cost optimisation and cost reduction. This system is used by the client company to

find out the cost incurred in manufacturing and production of its fruit juice products. This system

also assists the management to eliminate unproductive and unnecessary costs so that cost of

production can be reduced and profitability margin can be increased with available sources. In

order to control the cost, it also improve the performance of employees working within the firm.

Inventory Management System: In a manufacturing company like Oshodi Plc, its

inventory is the main source of its income hence a proper record and management of inventory is

crucial for the respective firm. Inventory management system helps the managers in tracking

each and every movement of a single unit available with the establishment. It keeps all the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

information from purchase of raw material to dispatch of finished goods and goods returned as

well. Further this method also helps in choosing optimum method to evaluate the value of

inventory. For better operations of inventory, the client company uses inventory management

software which also helps in solving customers' queries regarding products.

Job Costing System: This costing method is used when every unit of the manufactured

product is sufficiently different from the other units. In case of Selected company, different type

of juices differ from each other because of the age brackets hence job costing system is used by

the managers to find out the cost of every batch so that prices of the products can be decided

accordingly. Job costing system is also helpful in examining the performance of the employees

and rewarding them according to their efficiency (Sugahara, Daidj and Ushio, 2017).

P2: Different types of management accounting reporting.

These are internal reports made for the Oshodi PLC management body to take hard

decisions for the future based on the insights received from the reports. These reports help

management by giving them quantitative data needed (Chandler, 2017). This data is inferred by

the executives of the organisation to identify future growth potential of the firm, product

feasibility analysis, cost benefit modelling of the ideas and other tough managerial decisions.

Management accounting reports are of more importance to small business owners need critical

financial data to design its short term as well as long terms objectives and decide the longevity

line of the business. These are various kind of reports which are used by managers at Oshodi

PLC to gain business segment knowledge. Some of them are as described :

3

well. Further this method also helps in choosing optimum method to evaluate the value of

inventory. For better operations of inventory, the client company uses inventory management

software which also helps in solving customers' queries regarding products.

Job Costing System: This costing method is used when every unit of the manufactured

product is sufficiently different from the other units. In case of Selected company, different type

of juices differ from each other because of the age brackets hence job costing system is used by

the managers to find out the cost of every batch so that prices of the products can be decided

accordingly. Job costing system is also helpful in examining the performance of the employees

and rewarding them according to their efficiency (Sugahara, Daidj and Ushio, 2017).

P2: Different types of management accounting reporting.

These are internal reports made for the Oshodi PLC management body to take hard

decisions for the future based on the insights received from the reports. These reports help

management by giving them quantitative data needed (Chandler, 2017). This data is inferred by

the executives of the organisation to identify future growth potential of the firm, product

feasibility analysis, cost benefit modelling of the ideas and other tough managerial decisions.

Management accounting reports are of more importance to small business owners need critical

financial data to design its short term as well as long terms objectives and decide the longevity

line of the business. These are various kind of reports which are used by managers at Oshodi

PLC to gain business segment knowledge. Some of them are as described :

3

Budget report: This report gives a brief knowledge about the budgets allocated to

different business activities in Oshodi plc. It gives the management an idea about the budgeted

targets for each department. This helps the management in monitoring the performance of each

unit by tracking their skewness from budgeted position to the actual outcome. Budget reports

also helps in checking the profitability of the business and measuring cost centre for cost

allocation to individual unit engaged in production and by product activities. Budget reports also

depends on the size of the organisation. In Oshodi plc. annual budgets report are prepared by

manager on a big scale so that monthly sales projections can be done and entire team member are

communicated regarding these targets.

Account receivable report: This report is prepared to ensure that the flow of cash

inwards and outwards be maintained at Oshodi plc. This report contains details about the bills

receivables, cash invoices, interest receivables, with due date and details of the debtors. It helps

the organisation in not missing any payment from receiving. This report also provides summary

of the total inflow and outflow of cash during a period which helps in conducting liquidity

analysis (Cooper, 2017). This report provides broad framework to manager of Oshodi plc that

helps them to make decision related to credit & cash management system. So that co0mpanmy

have enough funds which support to run other business operating profitable manner. This report

is used for 'ageing' the information for successive years. This report helps in establishing a

centralised data management system which is been built to track the funds processing via fluent

mediums.

4

different business activities in Oshodi plc. It gives the management an idea about the budgeted

targets for each department. This helps the management in monitoring the performance of each

unit by tracking their skewness from budgeted position to the actual outcome. Budget reports

also helps in checking the profitability of the business and measuring cost centre for cost

allocation to individual unit engaged in production and by product activities. Budget reports also

depends on the size of the organisation. In Oshodi plc. annual budgets report are prepared by

manager on a big scale so that monthly sales projections can be done and entire team member are

communicated regarding these targets.

Account receivable report: This report is prepared to ensure that the flow of cash

inwards and outwards be maintained at Oshodi plc. This report contains details about the bills

receivables, cash invoices, interest receivables, with due date and details of the debtors. It helps

the organisation in not missing any payment from receiving. This report also provides summary

of the total inflow and outflow of cash during a period which helps in conducting liquidity

analysis (Cooper, 2017). This report provides broad framework to manager of Oshodi plc that

helps them to make decision related to credit & cash management system. So that co0mpanmy

have enough funds which support to run other business operating profitable manner. This report

is used for 'ageing' the information for successive years. This report helps in establishing a

centralised data management system which is been built to track the funds processing via fluent

mediums.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Performance report: This report is based on the key performance indicators which

provide quantifiable data set to discover the performance standards for evaluation. This report

helps Oshodi plc's management in restructuring or redesigning work related systems into more

precisely designed scientific system to ensure that they turn out to be more productive for the

firm. This report evaluates the total variation from the budgeted position to the actual position.

In Oshodi plc's this reports ascertain the imbalance in the performance parameters of each factor

of production and labour working on different production activities. This report ensures that all

financial and non financial benchmarks are met and the degree of non compliance owing to the

standards set.

Job cost report : This report helps the business in identifying the costs assigned to each

job factor and the conversion rate of the job into profit. This report defines the profit making,

cost effective and revenue enhancing capacity of each individual unit of production. This report

also helps the management in ascertaining the cost to profit conversion capacity of each project

which helps the organisation in prioritising the most profit making projects to least profitable

one's (De Loo, Cooper and Manochin, 2015). This reports helps in conducting each job category

accordingly in respective firm so that overall cost involved different jobs within specific time

period are determined. Job cost report also support to make better decision related to reduction

of cost that directly increase the profit margin.

M1: Benefits of management accounting systems.

Price Optimisation System It is the mechanism that helps the Oshodi plc's to select

the appropriate price in order to increase the

company's general profit margin.

In Oshodi plc's, in order to gather the information

regarding customer expectation related to product

price this system is most beneficial.

Inventory Management

System

This can readily decrease the stock-keeping issue

within the Oshodi plc's that is beneficial to increase

revenue.

It support to reduces the Oshodi plc's time, money and

even energy that is further used on other operating

5

provide quantifiable data set to discover the performance standards for evaluation. This report

helps Oshodi plc's management in restructuring or redesigning work related systems into more

precisely designed scientific system to ensure that they turn out to be more productive for the

firm. This report evaluates the total variation from the budgeted position to the actual position.

In Oshodi plc's this reports ascertain the imbalance in the performance parameters of each factor

of production and labour working on different production activities. This report ensures that all

financial and non financial benchmarks are met and the degree of non compliance owing to the

standards set.

Job cost report : This report helps the business in identifying the costs assigned to each

job factor and the conversion rate of the job into profit. This report defines the profit making,

cost effective and revenue enhancing capacity of each individual unit of production. This report

also helps the management in ascertaining the cost to profit conversion capacity of each project

which helps the organisation in prioritising the most profit making projects to least profitable

one's (De Loo, Cooper and Manochin, 2015). This reports helps in conducting each job category

accordingly in respective firm so that overall cost involved different jobs within specific time

period are determined. Job cost report also support to make better decision related to reduction

of cost that directly increase the profit margin.

M1: Benefits of management accounting systems.

Price Optimisation System It is the mechanism that helps the Oshodi plc's to select

the appropriate price in order to increase the

company's general profit margin.

In Oshodi plc's, in order to gather the information

regarding customer expectation related to product

price this system is most beneficial.

Inventory Management

System

This can readily decrease the stock-keeping issue

within the Oshodi plc's that is beneficial to increase

revenue.

It support to reduces the Oshodi plc's time, money and

even energy that is further used on other operating

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

activities.

Cost Accounting System In Oshodi plc's this system helps to determine the

actual cost incurred on different activities and remove

unwanted expenses.

It help manager of Oshodi plc's in order to find

adjustments in the price trend within the organization

readily (Elmassri, Harris and Carter, 2016).

Job Costing System Manager of Oshodi plc's can easily estimation costs by

measuring previous outcomes acquired by costing

jobs.

This system in Oshodi plc's is effective to rise profit by

eliminating unprofitable activity and adding

professional jobs within

TASK 2

P3: Produce income statement by using marginal or absorption costing method.

Marginal costing:It relates to an approach to calculate income which specifically

classifies costs and expenses as variable and fixed.

Income statement by marginal costing for month of November and December.

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

6

Cost Accounting System In Oshodi plc's this system helps to determine the

actual cost incurred on different activities and remove

unwanted expenses.

It help manager of Oshodi plc's in order to find

adjustments in the price trend within the organization

readily (Elmassri, Harris and Carter, 2016).

Job Costing System Manager of Oshodi plc's can easily estimation costs by

measuring previous outcomes acquired by costing

jobs.

This system in Oshodi plc's is effective to rise profit by

eliminating unprofitable activity and adding

professional jobs within

TASK 2

P3: Produce income statement by using marginal or absorption costing method.

Marginal costing:It relates to an approach to calculate income which specifically

classifies costs and expenses as variable and fixed.

Income statement by marginal costing for month of November and December.

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

6

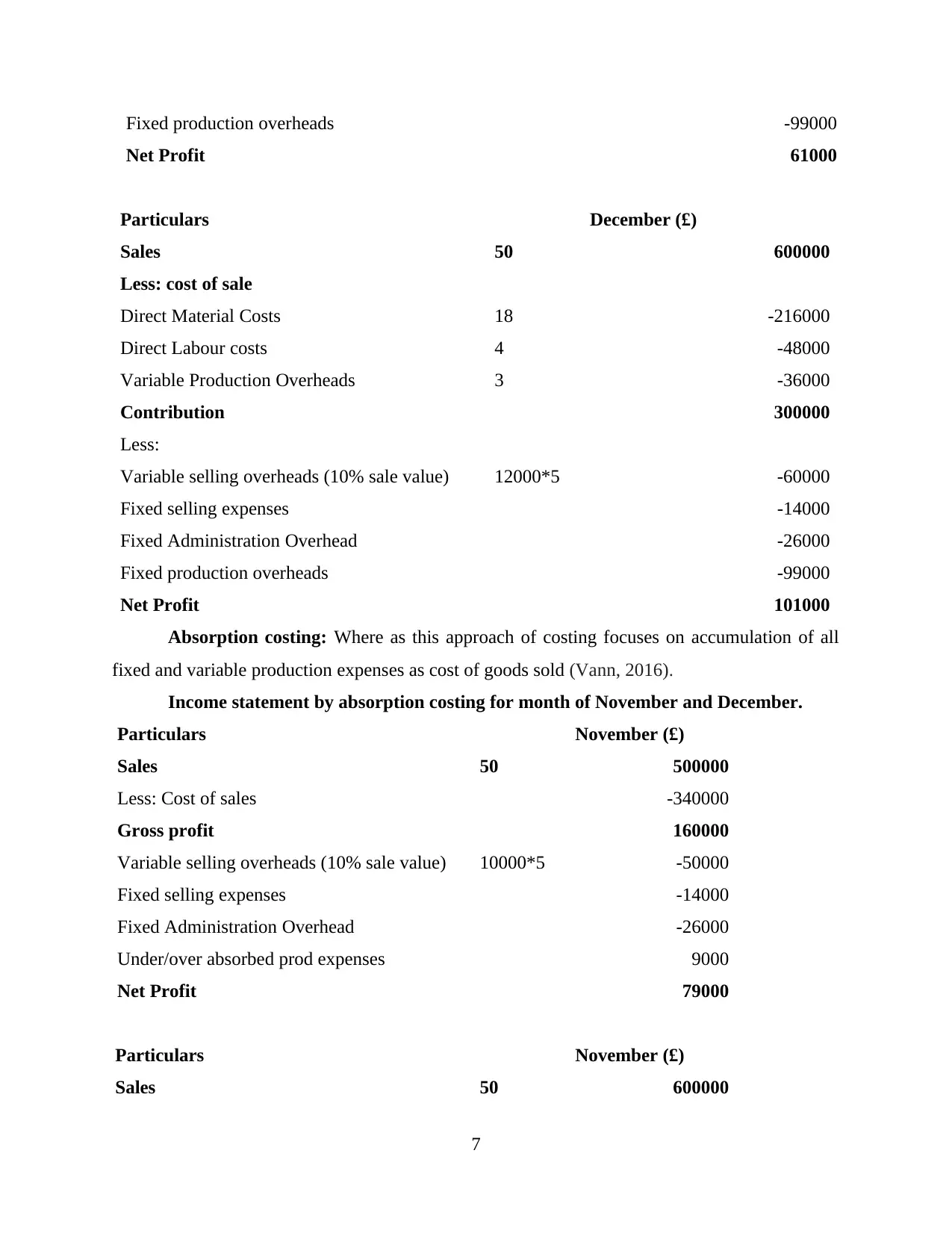

Fixed production overheads -99000

Net Profit 61000

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing: Where as this approach of costing focuses on accumulation of all

fixed and variable production expenses as cost of goods sold (Vann, 2016).

Income statement by absorption costing for month of November and December.

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars November (£)

Sales 50 600000

7

Net Profit 61000

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing: Where as this approach of costing focuses on accumulation of all

fixed and variable production expenses as cost of goods sold (Vann, 2016).

Income statement by absorption costing for month of November and December.

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars November (£)

Sales 50 600000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

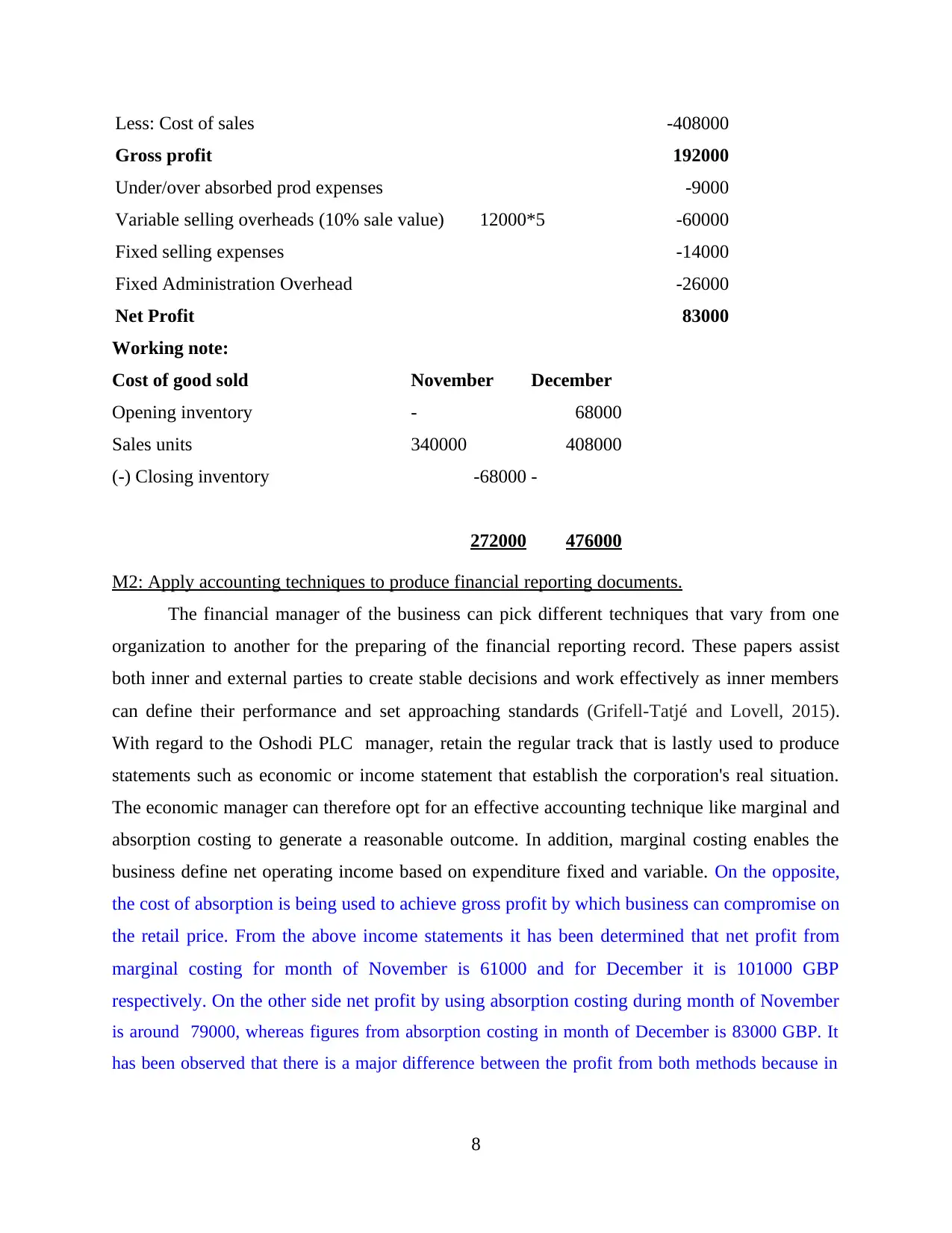

Less: Cost of sales -408000

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working note:

Cost of good sold November December

Opening inventory - 68000

Sales units 340000 408000

(-) Closing inventory -68000 -

272000 476000

M2: Apply accounting techniques to produce financial reporting documents.

The financial manager of the business can pick different techniques that vary from one

organization to another for the preparing of the financial reporting record. These papers assist

both inner and external parties to create stable decisions and work effectively as inner members

can define their performance and set approaching standards (Grifell-Tatjé and Lovell, 2015).

With regard to the Oshodi PLC manager, retain the regular track that is lastly used to produce

statements such as economic or income statement that establish the corporation's real situation.

The economic manager can therefore opt for an effective accounting technique like marginal and

absorption costing to generate a reasonable outcome. In addition, marginal costing enables the

business define net operating income based on expenditure fixed and variable. On the opposite,

the cost of absorption is being used to achieve gross profit by which business can compromise on

the retail price. From the above income statements it has been determined that net profit from

marginal costing for month of November is 61000 and for December it is 101000 GBP

respectively. On the other side net profit by using absorption costing during month of November

is around 79000, whereas figures from absorption costing in month of December is 83000 GBP. It

has been observed that there is a major difference between the profit from both methods because in

8

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working note:

Cost of good sold November December

Opening inventory - 68000

Sales units 340000 408000

(-) Closing inventory -68000 -

272000 476000

M2: Apply accounting techniques to produce financial reporting documents.

The financial manager of the business can pick different techniques that vary from one

organization to another for the preparing of the financial reporting record. These papers assist

both inner and external parties to create stable decisions and work effectively as inner members

can define their performance and set approaching standards (Grifell-Tatjé and Lovell, 2015).

With regard to the Oshodi PLC manager, retain the regular track that is lastly used to produce

statements such as economic or income statement that establish the corporation's real situation.

The economic manager can therefore opt for an effective accounting technique like marginal and

absorption costing to generate a reasonable outcome. In addition, marginal costing enables the

business define net operating income based on expenditure fixed and variable. On the opposite,

the cost of absorption is being used to achieve gross profit by which business can compromise on

the retail price. From the above income statements it has been determined that net profit from

marginal costing for month of November is 61000 and for December it is 101000 GBP

respectively. On the other side net profit by using absorption costing during month of November

is around 79000, whereas figures from absorption costing in month of December is 83000 GBP. It

has been observed that there is a major difference between the profit from both methods because in

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

marginal costing fixed production overheads are considered while calculating net profit. In

absorption costing fixed production overheads are absorbed under cost of good sold.

TASK 3

P4. Planning tools for budgetary control

Controlling budgetary expenditure is an important measure which every organisation

must pursue in order to be cost effective along with being profitable. The Oshodi plc's

management has designed a system of planning tools which contains various budgets which all

together help the organisation in saving costs. These tools have different significance. Planning

tools assist the managers in planning for the big turns in pursuit of which an organisation

prepares a budget. Some major planning tools are as follows :

Operating budget: This budget contains operational costs of the business activities.

Costs like production cost, manufacturing cost, overheads, labour cost, administration cost etc.

form part of this budget. This budget satisfies the fund requirements of day to day operational

activities of the business. This budget can be formed as per the requirements which can be

monthly , quarterly, bi-annually or yearly. This budget creates a boundary line on the scope of

business activities of each budgeted functional unit to carry out its targets within the budgeted

amount for the period defined (Ionescu, 2016).

Advantages

In Oshodi PLC this budget helps in managing costs in short run in order to oblige to long

run financial obligations. That helps to maintain a systematic control on each activity that

are beneficial to grow profit.

This budget keeps the financial information in Oshodi PLC very accurately and precisely

and in regulated format which ensures better tax compliances for the organisation.

Disadvantages

In Oshodi PLC it decides the scope of each function, sometimes departments gets choked

due to low availability of funds than actually required. This could lead to slow production

of valuables goods that will impact the overall image.

It is sometimes difficult to assign costs to each factor of production in Oshodi PLC due to

variability of roles. As employees gets impacted and overall performance gets influenced

due to low productivity hours.

9

absorption costing fixed production overheads are absorbed under cost of good sold.

TASK 3

P4. Planning tools for budgetary control

Controlling budgetary expenditure is an important measure which every organisation

must pursue in order to be cost effective along with being profitable. The Oshodi plc's

management has designed a system of planning tools which contains various budgets which all

together help the organisation in saving costs. These tools have different significance. Planning

tools assist the managers in planning for the big turns in pursuit of which an organisation

prepares a budget. Some major planning tools are as follows :

Operating budget: This budget contains operational costs of the business activities.

Costs like production cost, manufacturing cost, overheads, labour cost, administration cost etc.

form part of this budget. This budget satisfies the fund requirements of day to day operational

activities of the business. This budget can be formed as per the requirements which can be

monthly , quarterly, bi-annually or yearly. This budget creates a boundary line on the scope of

business activities of each budgeted functional unit to carry out its targets within the budgeted

amount for the period defined (Ionescu, 2016).

Advantages

In Oshodi PLC this budget helps in managing costs in short run in order to oblige to long

run financial obligations. That helps to maintain a systematic control on each activity that

are beneficial to grow profit.

This budget keeps the financial information in Oshodi PLC very accurately and precisely

and in regulated format which ensures better tax compliances for the organisation.

Disadvantages

In Oshodi PLC it decides the scope of each function, sometimes departments gets choked

due to low availability of funds than actually required. This could lead to slow production

of valuables goods that will impact the overall image.

It is sometimes difficult to assign costs to each factor of production in Oshodi PLC due to

variability of roles. As employees gets impacted and overall performance gets influenced

due to low productivity hours.

9

Master budget: It summarises all the departmental budgets prepared within the Oshodi

plc premises. This budget is prepared after preparing all departmental budgets. All functional

units gives their recommendations about their funding needs, the areas they want to explore with

the funds and modification ideas in the main budget according to the timely needs. After this all

budgets are merged into a single budget which provides a broader picture of the organisational

objectives known as Master budget (Nuhu, Baird and Bala Appuhamilage, 2017). This budget is

also used to measure the deviation from the budgeted targets. If the deviation is much higher

than expected than management applies control mechanism to reduce the impact.

Advantages

In Oshodi PLC this budgets is consider to be the most powerful budget which shows

total targets to be achieved in a given period which helps employee motivation and a

value to be realised with efforts.

This budget helps the management of respective firm to make proactive plans and take

valuable decisions because it identifies possible problems in advance by showing total

figures.

Disadvantages

By nature the master budget Oshodi PLC also faces major problem as this budget not

flexible and rigid in nature which makes it hard to alter.

Being a big budget its figures and values can sometimes be inaccurate to the manager of

Oshodi PLC as they need more time and effort to make understand these changes.

Flexible budget: This budget is very lucrative in nature and can be changed according to

the movement of cost and volume. This budget is opposite of static budget or fixed budget. This

budget has a variable rate per unit system instead of fixed rate system which would flex itself it

the costs vary according tot he volume of production. This budget is very helpful in evaluation of

efficiency of the management (Advantages and disadvantage of flexible budget, 2019).

Advantages

It is good for Oshodi PLC because manager can easily manipulate these budgets

according to there needs and requirements. This will bring more stability in business

operation as specific time can be given to important activity.

In Oshodi PLC this budget is helpful to saves costs for the business by reducing the extra

costs which are not required for the time being.

10

plc premises. This budget is prepared after preparing all departmental budgets. All functional

units gives their recommendations about their funding needs, the areas they want to explore with

the funds and modification ideas in the main budget according to the timely needs. After this all

budgets are merged into a single budget which provides a broader picture of the organisational

objectives known as Master budget (Nuhu, Baird and Bala Appuhamilage, 2017). This budget is

also used to measure the deviation from the budgeted targets. If the deviation is much higher

than expected than management applies control mechanism to reduce the impact.

Advantages

In Oshodi PLC this budgets is consider to be the most powerful budget which shows

total targets to be achieved in a given period which helps employee motivation and a

value to be realised with efforts.

This budget helps the management of respective firm to make proactive plans and take

valuable decisions because it identifies possible problems in advance by showing total

figures.

Disadvantages

By nature the master budget Oshodi PLC also faces major problem as this budget not

flexible and rigid in nature which makes it hard to alter.

Being a big budget its figures and values can sometimes be inaccurate to the manager of

Oshodi PLC as they need more time and effort to make understand these changes.

Flexible budget: This budget is very lucrative in nature and can be changed according to

the movement of cost and volume. This budget is opposite of static budget or fixed budget. This

budget has a variable rate per unit system instead of fixed rate system which would flex itself it

the costs vary according tot he volume of production. This budget is very helpful in evaluation of

efficiency of the management (Advantages and disadvantage of flexible budget, 2019).

Advantages

It is good for Oshodi PLC because manager can easily manipulate these budgets

according to there needs and requirements. This will bring more stability in business

operation as specific time can be given to important activity.

In Oshodi PLC this budget is helpful to saves costs for the business by reducing the extra

costs which are not required for the time being.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.