Management Accounting Report: TPG Processing, Financial Analysis

VerifiedAdded on 2021/02/21

|21

|4634

|40

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its tools, techniques, and applications within the context of TPG processing. It begins by defining management accounting, differentiating it from financial accounting, and highlighting its crucial roles in organizational development, including cost analysis, budgeting, and financial management. The report then delves into various management accounting tools such as cost accounting systems, inventory management systems, job costing systems, and price optimization systems. Furthermore, it examines different types of management accounting reports, including performance management, inventory management, cost accounting, and accounts receivable reports. The report also discusses marginal costing and absorption costing approaches, providing insights into their methodologies and applications. Overall, the report offers a detailed analysis of management accounting practices, emphasizing their importance in financial decision-making and organizational performance.

Management accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

MA refers to the chain of various kinds of applications to grab professional knowledge,

tools and techniques and kinds of concepts for prepare the information to get desirable goals and

objectives that helps in formulating plans and policies in context of organisation. In other words,

it helps in devising meaning of information and data related to cost accounting to get useful

knowledge and information to remain always relevant into marketplace. That assignment rely on

TPG processing that a service provider to the general public to provide best services to consumer

base. This assignment rely on kinds of management tools and their techniques with their

relevance in marketplace. With it added methods of management accounting reporting with help

of tools that helps in plan and coordinate each and every activity with their advantages and

disadvantages. It includes systems to resolving financial problems to get right kinds of outputs.

TASK 1

P1

As per view of R.N. Anthony “MA defines about accounting information that proved

useful for management.” Management accounting helps to management in major decision

making by giving them direction to get most important insights and knowledge that are relevant

for organisation.

As per the view of Batty “Management accounting described as an accounting methods,

techniques and systems that associated with knowledge and capabilities that helps to

management to gain maximum profit by minimizing losses. It mixed with the coherent whole,

financial accounting, cost accounting and whole concept of financial accounting” As per the

batty management accounting helps to acknowledge the useful knowledge and capabilities that

gives important insights that ultimately useful for major decision-making in context of

organisation.

Management accounting proved useful by using all kinds of tools and techniques such as

financial accounting, cost accounting and various kinds of statistics to collect and process

information that available before management that helps in taking important kinds of decisions.

Comparison:

Management accounting is differ from the financial accounting that it focuses on building

and preparation of financial statement for an organisation (Banerjee, 2012.. On other hand

MA refers to the chain of various kinds of applications to grab professional knowledge,

tools and techniques and kinds of concepts for prepare the information to get desirable goals and

objectives that helps in formulating plans and policies in context of organisation. In other words,

it helps in devising meaning of information and data related to cost accounting to get useful

knowledge and information to remain always relevant into marketplace. That assignment rely on

TPG processing that a service provider to the general public to provide best services to consumer

base. This assignment rely on kinds of management tools and their techniques with their

relevance in marketplace. With it added methods of management accounting reporting with help

of tools that helps in plan and coordinate each and every activity with their advantages and

disadvantages. It includes systems to resolving financial problems to get right kinds of outputs.

TASK 1

P1

As per view of R.N. Anthony “MA defines about accounting information that proved

useful for management.” Management accounting helps to management in major decision

making by giving them direction to get most important insights and knowledge that are relevant

for organisation.

As per the view of Batty “Management accounting described as an accounting methods,

techniques and systems that associated with knowledge and capabilities that helps to

management to gain maximum profit by minimizing losses. It mixed with the coherent whole,

financial accounting, cost accounting and whole concept of financial accounting” As per the

batty management accounting helps to acknowledge the useful knowledge and capabilities that

gives important insights that ultimately useful for major decision-making in context of

organisation.

Management accounting proved useful by using all kinds of tools and techniques such as

financial accounting, cost accounting and various kinds of statistics to collect and process

information that available before management that helps in taking important kinds of decisions.

Comparison:

Management accounting is differ from the financial accounting that it focuses on building

and preparation of financial statement for an organisation (Banerjee, 2012.. On other hand

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting system give necessary and relevant information for managers for building policies,

plans and tactics.

Roles of MA:

MA are very much crucial for organisational development and enhancement by some

factors its importance and roles should be understood that are as follows:

Fewer numbers to crunch:

MA enables to understand the technical aspect of knowledge and information. It enables

to giving hidden facts and figures by reading the net income, contingent liability, accounts

receivable and payable (Contrafatto and Burns, 2013. ). Managerial accounting not follow the

standard financial accounting principles to get right kind of outputs. By giving accurate

knowledge and information it helps to managers in taking crucial decisions. In respective

organisation they use management accounting to get gist of financial accounting tools and

techniques so that better results should be accomplished.

Looking to the future:

Management accounting proved beneficial by build projections for the future but their

main focus is on the performance in past year or in quarter. It majorly focus on what is coming in

future so that better plans should be prepared to get right kind of objectives.

Follow the money:

Management accounting helps in looking and observing projections of system. It is the

responsibility of a manager to observe about the performance level to take correct course of

action. In respective organisation they enables to management accounting evaluate the financial

condition of their respective organisation.

Ready when they need it:

In an organisation financial statements should be prepared on the regular basis such as

every month, quarterly or yearly basis. It enables to system can be able to get update about cash

flow position that helps in deal with the critical situations to remain always competitive in

marketplace (DRURY, 2013. ). In respective organisation by financial statements firm measure

or assess their performance on fixed duration.

Margin analysis:

Management accounting proved beneficial in determining the amount of profit or ratio of

cash that created or generated by using specific product or services with a particular state or

plans and tactics.

Roles of MA:

MA are very much crucial for organisational development and enhancement by some

factors its importance and roles should be understood that are as follows:

Fewer numbers to crunch:

MA enables to understand the technical aspect of knowledge and information. It enables

to giving hidden facts and figures by reading the net income, contingent liability, accounts

receivable and payable (Contrafatto and Burns, 2013. ). Managerial accounting not follow the

standard financial accounting principles to get right kind of outputs. By giving accurate

knowledge and information it helps to managers in taking crucial decisions. In respective

organisation they use management accounting to get gist of financial accounting tools and

techniques so that better results should be accomplished.

Looking to the future:

Management accounting proved beneficial by build projections for the future but their

main focus is on the performance in past year or in quarter. It majorly focus on what is coming in

future so that better plans should be prepared to get right kind of objectives.

Follow the money:

Management accounting helps in looking and observing projections of system. It is the

responsibility of a manager to observe about the performance level to take correct course of

action. In respective organisation they enables to management accounting evaluate the financial

condition of their respective organisation.

Ready when they need it:

In an organisation financial statements should be prepared on the regular basis such as

every month, quarterly or yearly basis. It enables to system can be able to get update about cash

flow position that helps in deal with the critical situations to remain always competitive in

marketplace (DRURY, 2013. ). In respective organisation by financial statements firm measure

or assess their performance on fixed duration.

Margin analysis:

Management accounting proved beneficial in determining the amount of profit or ratio of

cash that created or generated by using specific product or services with a particular state or

region. In context of TPG processing they get important outcomes by analysing the margin in

standards set by them.

Auditing:

Auditing is one of major role of management accounting that are responsible for the

performing audits, reviews and compilations of various kinds of financial statements to achieve

better decision making. It is one of major role of management accounting to get important

insights and knowledge to remain always competitive in marketplace.

Financial management:

This is one of most important kind of role of management accounting in which financial

fuel information and regular and efficient functioning to ensuring that should be provided to

remain always relevant in the marketplace. Role of management accounting is to accumulate

necessary knowledge and information regarding the finance and resources to get desirable

objectives in better manner. In context of TPG processing by using the management accounting

tools and techniques they predict in better manner about future projections.

Cost analysis:

The most important role of management accounting is to analyse the cost associated with

producing the products and services by predicting the existing expenses of an organisation as per

the future activities. In context of TPG processing by using that tool organisation can be evaluate

the incurred cost and various measures associated with it.

Make or buy evaluations:

Management accounting helps in taking the make or buy evaluations, for an organisation

produce a product is one of most expensive possession so it helps to make sure about the chosen

option suits with needs of an organisation. In that regards management accounting helps to

evaluate the best option for them to remain always competitive in marketplace.

Define budgets:

the main role of management accounting is to give important insights to taken budget

related decisions by complying with sales history and marketing database. By analysing the

former activities and defining actions for the future activities they take important decisions.

Controlling:

standards set by them.

Auditing:

Auditing is one of major role of management accounting that are responsible for the

performing audits, reviews and compilations of various kinds of financial statements to achieve

better decision making. It is one of major role of management accounting to get important

insights and knowledge to remain always competitive in marketplace.

Financial management:

This is one of most important kind of role of management accounting in which financial

fuel information and regular and efficient functioning to ensuring that should be provided to

remain always relevant in the marketplace. Role of management accounting is to accumulate

necessary knowledge and information regarding the finance and resources to get desirable

objectives in better manner. In context of TPG processing by using the management accounting

tools and techniques they predict in better manner about future projections.

Cost analysis:

The most important role of management accounting is to analyse the cost associated with

producing the products and services by predicting the existing expenses of an organisation as per

the future activities. In context of TPG processing by using that tool organisation can be evaluate

the incurred cost and various measures associated with it.

Make or buy evaluations:

Management accounting helps in taking the make or buy evaluations, for an organisation

produce a product is one of most expensive possession so it helps to make sure about the chosen

option suits with needs of an organisation. In that regards management accounting helps to

evaluate the best option for them to remain always competitive in marketplace.

Define budgets:

the main role of management accounting is to give important insights to taken budget

related decisions by complying with sales history and marketing database. By analysing the

former activities and defining actions for the future activities they take important decisions.

Controlling:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Controlling is one of major role that played by management accounting by evaluating the

work of all major units of an organisation with conclusions concerned with financial

performance.

Break even analysis:

By calculating the contribution margin with help of management accounting and volume

of unit that shows the break even of an organisation. In respective organisation that It enables to

Management accounting determine the price points.

Cost accounting system:

Cost accounting system that proved helpful by tracking raw material while proceed

towards the production stage and gradually convert into finished goods and services. The two

kinds of cost accounting systems are job order costing and processing costing (Herbert and Seal,

2012.). In respective organisation It enables to firm can be able to determine about the prices of

their products and services. It enables to organisation to track and record each and every activity

in an organisation to forecast demand in future. Cost accounting system is very much important

for organisation to analyse the profitability by individual products, services or by job and by

sales of various departments or operational units. The essential requirements of this system is to

compute the cost of whole process and services and also evaluate the actual profit of firm

through comparing the total gained amount with incurred cost.

Inventory management system:

that kind of management accounting system that obsessed with oversight and

administration of stock of goods and non capitalised possession of an organisation. That system

helps to reach effective rate of ware in a firm to remain always relevant in market. Inventory

management system is very much potential for organisation to track goods and services across

the supply chain to get optimum outputs. With it is essential to optimise the spectrum for order

placements. The crucial needs of this particular system is to keep the accurate records whole

stock levels within respective firm. With the assistance of this they can able to know about the

availability of stock and products effectively and efficiently. As by managing the inventory,

company can meet the consumers requirements, deliver the quality product on time as well as

also reduce the various costs related with holding stocks.

Job costing system:

work of all major units of an organisation with conclusions concerned with financial

performance.

Break even analysis:

By calculating the contribution margin with help of management accounting and volume

of unit that shows the break even of an organisation. In respective organisation that It enables to

Management accounting determine the price points.

Cost accounting system:

Cost accounting system that proved helpful by tracking raw material while proceed

towards the production stage and gradually convert into finished goods and services. The two

kinds of cost accounting systems are job order costing and processing costing (Herbert and Seal,

2012.). In respective organisation It enables to firm can be able to determine about the prices of

their products and services. It enables to organisation to track and record each and every activity

in an organisation to forecast demand in future. Cost accounting system is very much important

for organisation to analyse the profitability by individual products, services or by job and by

sales of various departments or operational units. The essential requirements of this system is to

compute the cost of whole process and services and also evaluate the actual profit of firm

through comparing the total gained amount with incurred cost.

Inventory management system:

that kind of management accounting system that obsessed with oversight and

administration of stock of goods and non capitalised possession of an organisation. That system

helps to reach effective rate of ware in a firm to remain always relevant in market. Inventory

management system is very much potential for organisation to track goods and services across

the supply chain to get optimum outputs. With it is essential to optimise the spectrum for order

placements. The crucial needs of this particular system is to keep the accurate records whole

stock levels within respective firm. With the assistance of this they can able to know about the

availability of stock and products effectively and efficiently. As by managing the inventory,

company can meet the consumers requirements, deliver the quality product on time as well as

also reduce the various costs related with holding stocks.

Job costing system:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Job costing method enables to give price or commercial enterprise cost for an each and

every individual product simultaneously track their expenses (Hilton and Platt, 2013). With the

help of it organisation can determine the price of their products and services to reach at large no.

of consumer base. In context of TPG processing by fixing some factors that directly related with

price that ultimately proved beneficial for them to determine the prices. It is require to track the

cost while creating or developing the new product or services in the marketplace. It is also useful

to track or measure associated cost with production system, custom, bespoke and many more.

Price optimising system:

That helps to regulate cost of various kinds of sources that organisation have. It enables

to determining the pricing of multiple products at at time. In respective organisation with using

diverse factors for fulfilling organisational goals and objectives. The main requirements of that

system is to find out the pricing sweet spot that easily consumers willing to pay. In that aspect it

is very much potential to use that system to get desirable goals and objectives. This type of

management accounting system is required through respective company for setting the prices of

their services at advantageous level. Moreover, through this they can able to ascertain the prices

of their various process and services that aids them to grab the attention of more clients.

P2

MAR is very much decisive for an organisation deal in systematic way about

performance of firm to lead in market. There are diverse types of costing so that sustainability

should be maintained.

There are four kinds of management accounting reports that are as follows:

Performance management report:

The main purpose of that reports to review the performance of the organisation as well as

a whole of a employee. In which departmental vies performance reports should be build that

helps to eliminate the gaps in performance.

Contents: the major content of that report is to evaluate the performance of an each and every

individual on the kinds of duration such as on monthly basis, quarterly and yearly basis.

every individual product simultaneously track their expenses (Hilton and Platt, 2013). With the

help of it organisation can determine the price of their products and services to reach at large no.

of consumer base. In context of TPG processing by fixing some factors that directly related with

price that ultimately proved beneficial for them to determine the prices. It is require to track the

cost while creating or developing the new product or services in the marketplace. It is also useful

to track or measure associated cost with production system, custom, bespoke and many more.

Price optimising system:

That helps to regulate cost of various kinds of sources that organisation have. It enables

to determining the pricing of multiple products at at time. In respective organisation with using

diverse factors for fulfilling organisational goals and objectives. The main requirements of that

system is to find out the pricing sweet spot that easily consumers willing to pay. In that aspect it

is very much potential to use that system to get desirable goals and objectives. This type of

management accounting system is required through respective company for setting the prices of

their services at advantageous level. Moreover, through this they can able to ascertain the prices

of their various process and services that aids them to grab the attention of more clients.

P2

MAR is very much decisive for an organisation deal in systematic way about

performance of firm to lead in market. There are diverse types of costing so that sustainability

should be maintained.

There are four kinds of management accounting reports that are as follows:

Performance management report:

The main purpose of that reports to review the performance of the organisation as well as

a whole of a employee. In which departmental vies performance reports should be build that

helps to eliminate the gaps in performance.

Contents: the major content of that report is to evaluate the performance of an each and every

individual on the kinds of duration such as on monthly basis, quarterly and yearly basis.

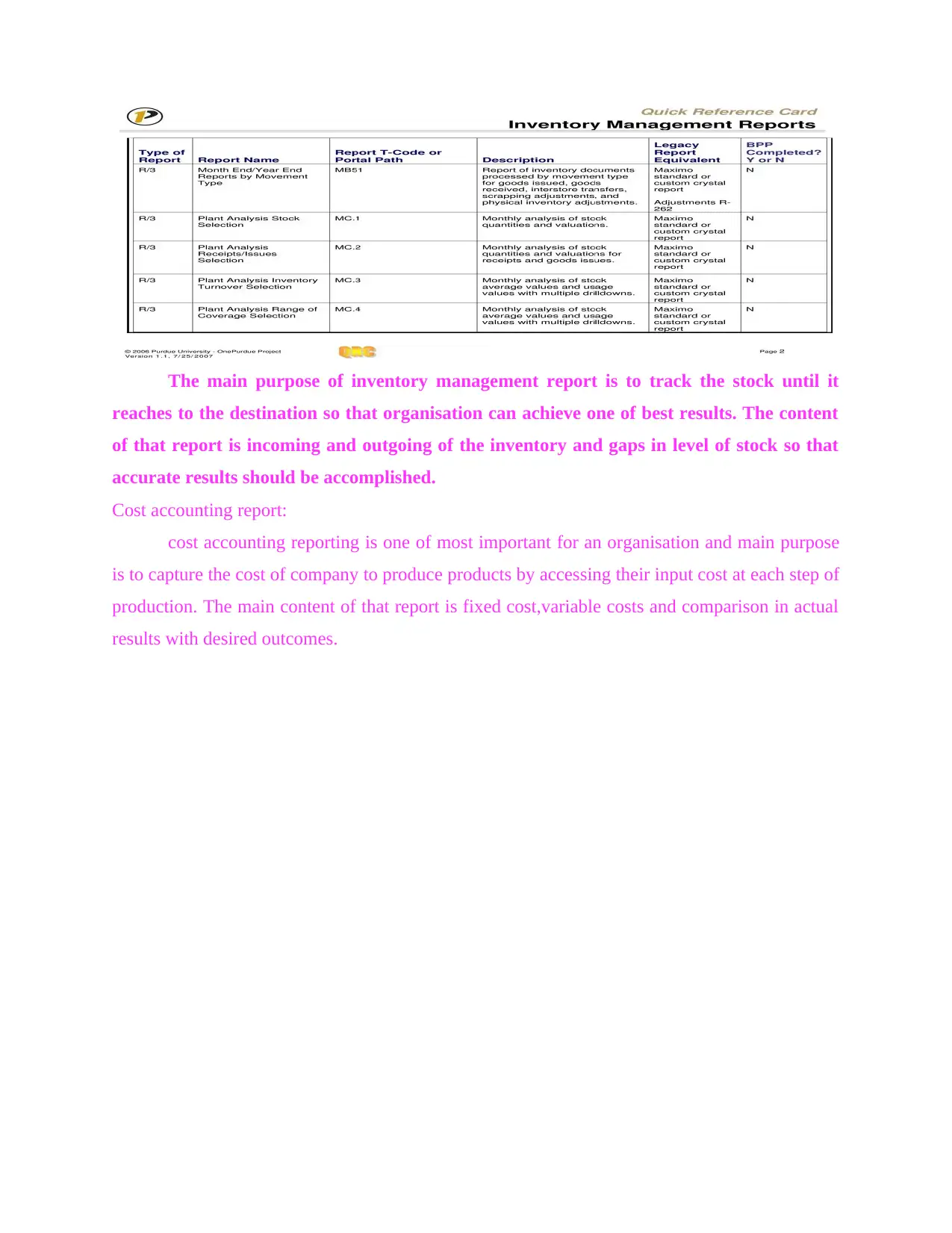

Inventory management report:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The main purpose of inventory management report is to track the stock until it

reaches to the destination so that organisation can achieve one of best results. The content

of that report is incoming and outgoing of the inventory and gaps in level of stock so that

accurate results should be accomplished.

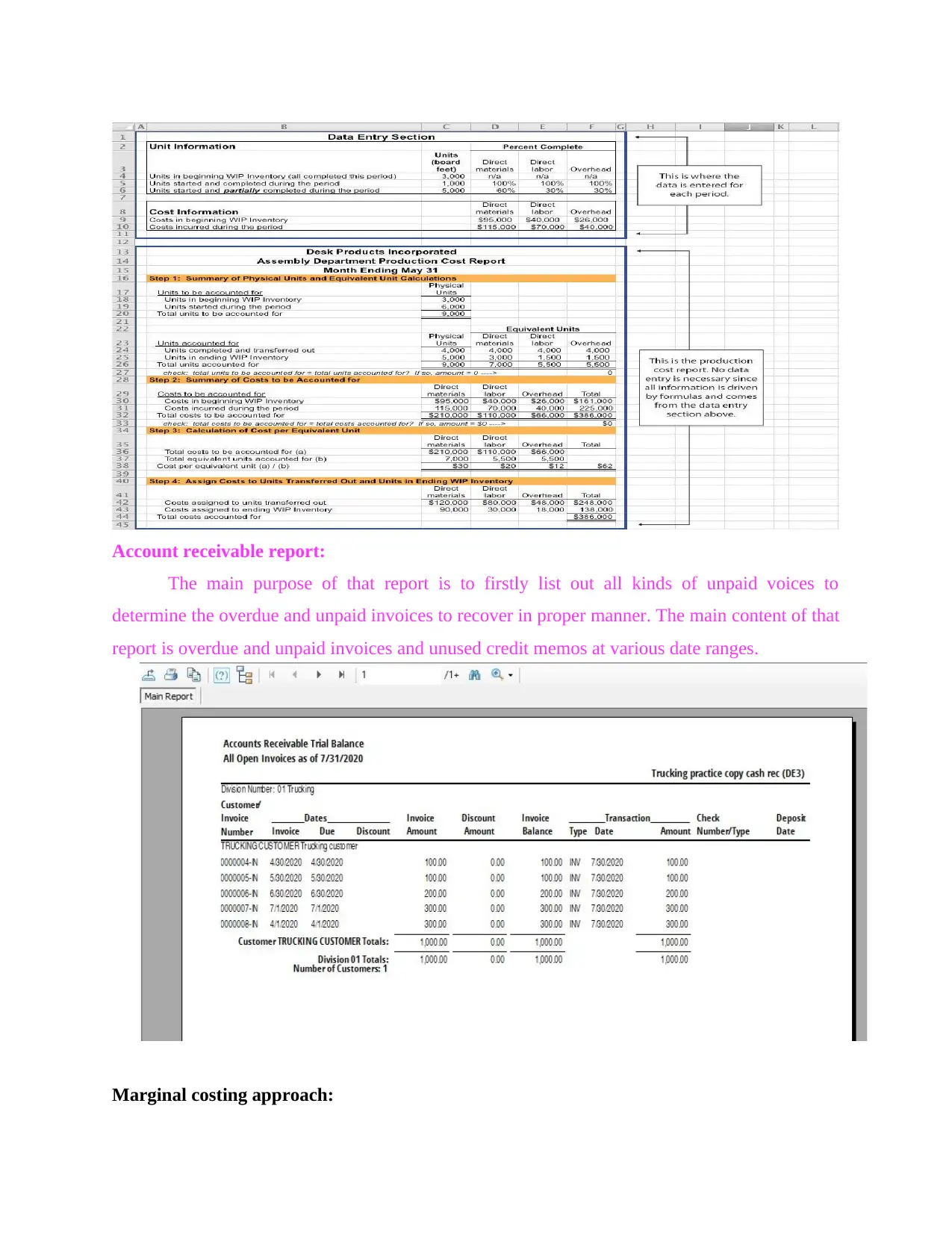

Cost accounting report:

cost accounting reporting is one of most important for an organisation and main purpose

is to capture the cost of company to produce products by accessing their input cost at each step of

production. The main content of that report is fixed cost,variable costs and comparison in actual

results with desired outcomes.

reaches to the destination so that organisation can achieve one of best results. The content

of that report is incoming and outgoing of the inventory and gaps in level of stock so that

accurate results should be accomplished.

Cost accounting report:

cost accounting reporting is one of most important for an organisation and main purpose

is to capture the cost of company to produce products by accessing their input cost at each step of

production. The main content of that report is fixed cost,variable costs and comparison in actual

results with desired outcomes.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

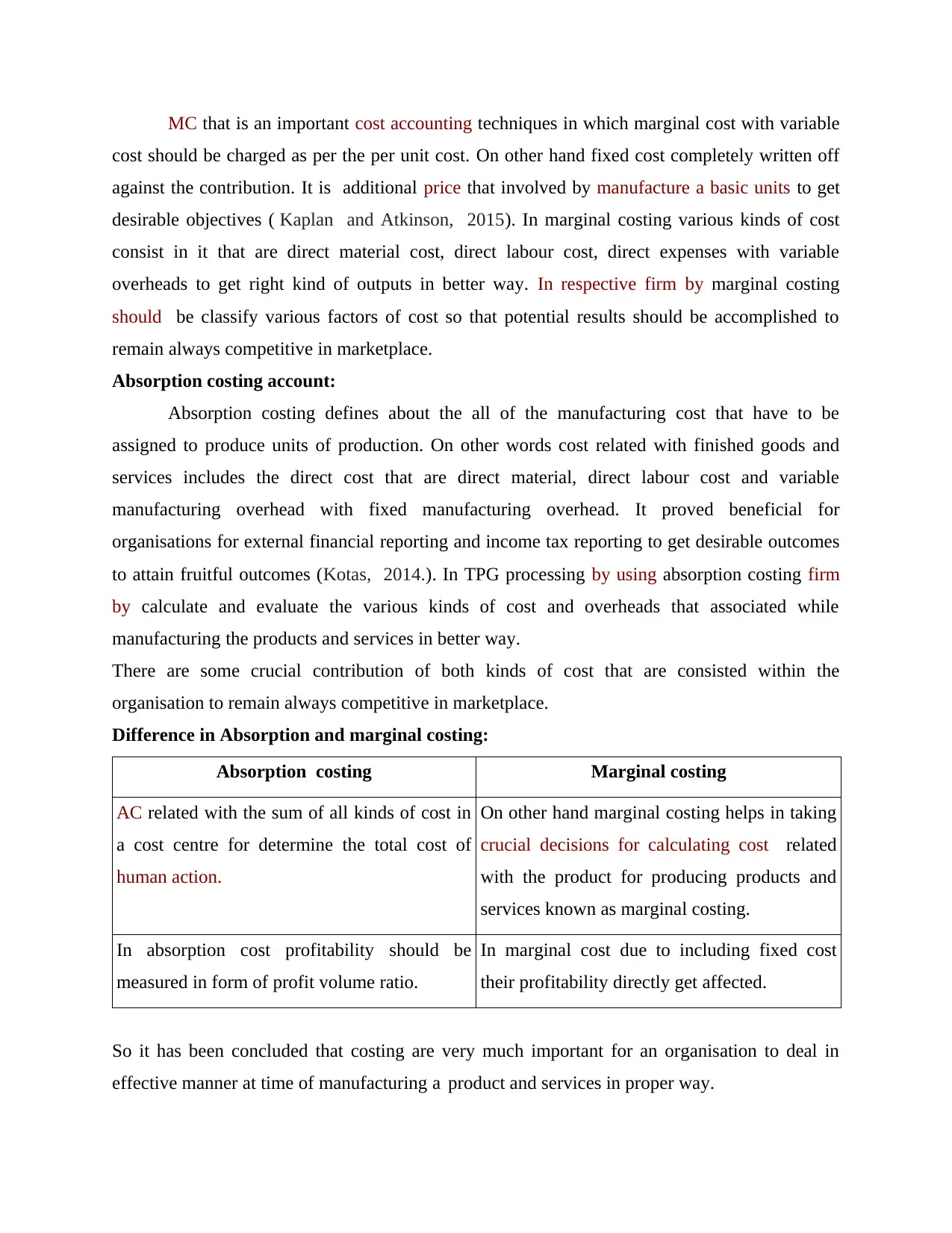

Account receivable report:

The main purpose of that report is to firstly list out all kinds of unpaid voices to

determine the overdue and unpaid invoices to recover in proper manner. The main content of that

report is overdue and unpaid invoices and unused credit memos at various date ranges.

Marginal costing approach:

The main purpose of that report is to firstly list out all kinds of unpaid voices to

determine the overdue and unpaid invoices to recover in proper manner. The main content of that

report is overdue and unpaid invoices and unused credit memos at various date ranges.

Marginal costing approach:

MC that is an important cost accounting techniques in which marginal cost with variable

cost should be charged as per the per unit cost. On other hand fixed cost completely written off

against the contribution. It is additional price that involved by manufacture a basic units to get

desirable objectives ( Kaplan and Atkinson, 2015). In marginal costing various kinds of cost

consist in it that are direct material cost, direct labour cost, direct expenses with variable

overheads to get right kind of outputs in better way. In respective firm by marginal costing

should be classify various factors of cost so that potential results should be accomplished to

remain always competitive in marketplace.

Absorption costing account:

Absorption costing defines about the all of the manufacturing cost that have to be

assigned to produce units of production. On other words cost related with finished goods and

services includes the direct cost that are direct material, direct labour cost and variable

manufacturing overhead with fixed manufacturing overhead. It proved beneficial for

organisations for external financial reporting and income tax reporting to get desirable outcomes

to attain fruitful outcomes (Kotas, 2014.). In TPG processing by using absorption costing firm

by calculate and evaluate the various kinds of cost and overheads that associated while

manufacturing the products and services in better way.

There are some crucial contribution of both kinds of cost that are consisted within the

organisation to remain always competitive in marketplace.

Difference in Absorption and marginal costing:

Absorption costing Marginal costing

AC related with the sum of all kinds of cost in

a cost centre for determine the total cost of

human action.

On other hand marginal costing helps in taking

crucial decisions for calculating cost related

with the product for producing products and

services known as marginal costing.

In absorption cost profitability should be

measured in form of profit volume ratio.

In marginal cost due to including fixed cost

their profitability directly get affected.

So it has been concluded that costing are very much important for an organisation to deal in

effective manner at time of manufacturing a product and services in proper way.

cost should be charged as per the per unit cost. On other hand fixed cost completely written off

against the contribution. It is additional price that involved by manufacture a basic units to get

desirable objectives ( Kaplan and Atkinson, 2015). In marginal costing various kinds of cost

consist in it that are direct material cost, direct labour cost, direct expenses with variable

overheads to get right kind of outputs in better way. In respective firm by marginal costing

should be classify various factors of cost so that potential results should be accomplished to

remain always competitive in marketplace.

Absorption costing account:

Absorption costing defines about the all of the manufacturing cost that have to be

assigned to produce units of production. On other words cost related with finished goods and

services includes the direct cost that are direct material, direct labour cost and variable

manufacturing overhead with fixed manufacturing overhead. It proved beneficial for

organisations for external financial reporting and income tax reporting to get desirable outcomes

to attain fruitful outcomes (Kotas, 2014.). In TPG processing by using absorption costing firm

by calculate and evaluate the various kinds of cost and overheads that associated while

manufacturing the products and services in better way.

There are some crucial contribution of both kinds of cost that are consisted within the

organisation to remain always competitive in marketplace.

Difference in Absorption and marginal costing:

Absorption costing Marginal costing

AC related with the sum of all kinds of cost in

a cost centre for determine the total cost of

human action.

On other hand marginal costing helps in taking

crucial decisions for calculating cost related

with the product for producing products and

services known as marginal costing.

In absorption cost profitability should be

measured in form of profit volume ratio.

In marginal cost due to including fixed cost

their profitability directly get affected.

So it has been concluded that costing are very much important for an organisation to deal in

effective manner at time of manufacturing a product and services in proper way.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.