Management Accounting Report: Roles, Systems, and Budgets

VerifiedAdded on 2020/10/05

|13

|2987

|90

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its critical role in business decision-making and strategic planning. It differentiates management accounting from financial accounting, highlighting their distinct objectives, applications, and reporting structures. The report delves into various management accounting systems, including balance scorecards and budgeting, detailing their advantages and disadvantages. It includes practical applications such as break-even analysis under different scenarios, calculating contribution per unit, and determining the impact of price changes on sales and profits. Furthermore, the report examines different types of budgets – static, zero-based, rolling, and incremental – discussing their merits and demerits, and emphasizing the importance of preparing budgets for financial control and goal achievement. The report also covers inventory valuation methods.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Section 1...........................................................................................................................................1

QUESTION 1..............................................................................................................................1

QUESTION 2..............................................................................................................................4

SECTION 2......................................................................................................................................6

QUESTION 3..............................................................................................................................6

QUESTION 4..............................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

Section 1...........................................................................................................................................1

QUESTION 1..............................................................................................................................1

QUESTION 2..............................................................................................................................4

SECTION 2......................................................................................................................................6

QUESTION 3..............................................................................................................................6

QUESTION 4..............................................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management Accounting is the branch of accounting that helps in decision making of

managers. This report presents various role of management accounting in day to day business

and also presents differences in different form of accounting that are financial and management.

This project report also discusses about management accounting systems. In this report there is

calculation of Break Even sales in different scenarios that are provided by client. This reports

also explains about different types of budgets and the importance of preparing budgets. The

different methods of inventory valuations are been described and also there is discussion about

the use of both the methods.

Section 1

QUESTION 1

(a)Role of Management Accounting in Business Organisation

Management accounting is any profession which involves decision making of

management, planning and performance of all management systems and it also provides in

expertise in reporting of financial statement in assisting the management of organisation for

implementation and formulation of organisational strategy(Renz, 2016). It can also be defined as

it is process of analysing all the cost that are related to business and different operations that are

needed to prepare financial reports which helps in decision making for the achievement of

organisation goals.

The following are the roles of management accounting in any business organisation-:

1. It helps in designing the structure of cost and report preparation for routine decision

making for managers of a business organisation.

2. This type of accounting plays an important role for forecasting the economic events that

may occur in future and also helps in making the long term plans for an business

organisation(Parker, and Fleischman, 2017).

3. The major role of management accounting can be said as it helps in defining capital

structure and to know from where to raise fund for an business organisation. The role of

an management accountant is to decide about the proper mixture between debt and equity

and maintains there debt equity ratio.

4. It helps in analysing accounts and preparing different reports such as cash and fund flow

analysis, performance evaluation reports, liquidity management etc.

1

Management Accounting is the branch of accounting that helps in decision making of

managers. This report presents various role of management accounting in day to day business

and also presents differences in different form of accounting that are financial and management.

This project report also discusses about management accounting systems. In this report there is

calculation of Break Even sales in different scenarios that are provided by client. This reports

also explains about different types of budgets and the importance of preparing budgets. The

different methods of inventory valuations are been described and also there is discussion about

the use of both the methods.

Section 1

QUESTION 1

(a)Role of Management Accounting in Business Organisation

Management accounting is any profession which involves decision making of

management, planning and performance of all management systems and it also provides in

expertise in reporting of financial statement in assisting the management of organisation for

implementation and formulation of organisational strategy(Renz, 2016). It can also be defined as

it is process of analysing all the cost that are related to business and different operations that are

needed to prepare financial reports which helps in decision making for the achievement of

organisation goals.

The following are the roles of management accounting in any business organisation-:

1. It helps in designing the structure of cost and report preparation for routine decision

making for managers of a business organisation.

2. This type of accounting plays an important role for forecasting the economic events that

may occur in future and also helps in making the long term plans for an business

organisation(Parker, and Fleischman, 2017).

3. The major role of management accounting can be said as it helps in defining capital

structure and to know from where to raise fund for an business organisation. The role of

an management accountant is to decide about the proper mixture between debt and equity

and maintains there debt equity ratio.

4. It helps in analysing accounts and preparing different reports such as cash and fund flow

analysis, performance evaluation reports, liquidity management etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

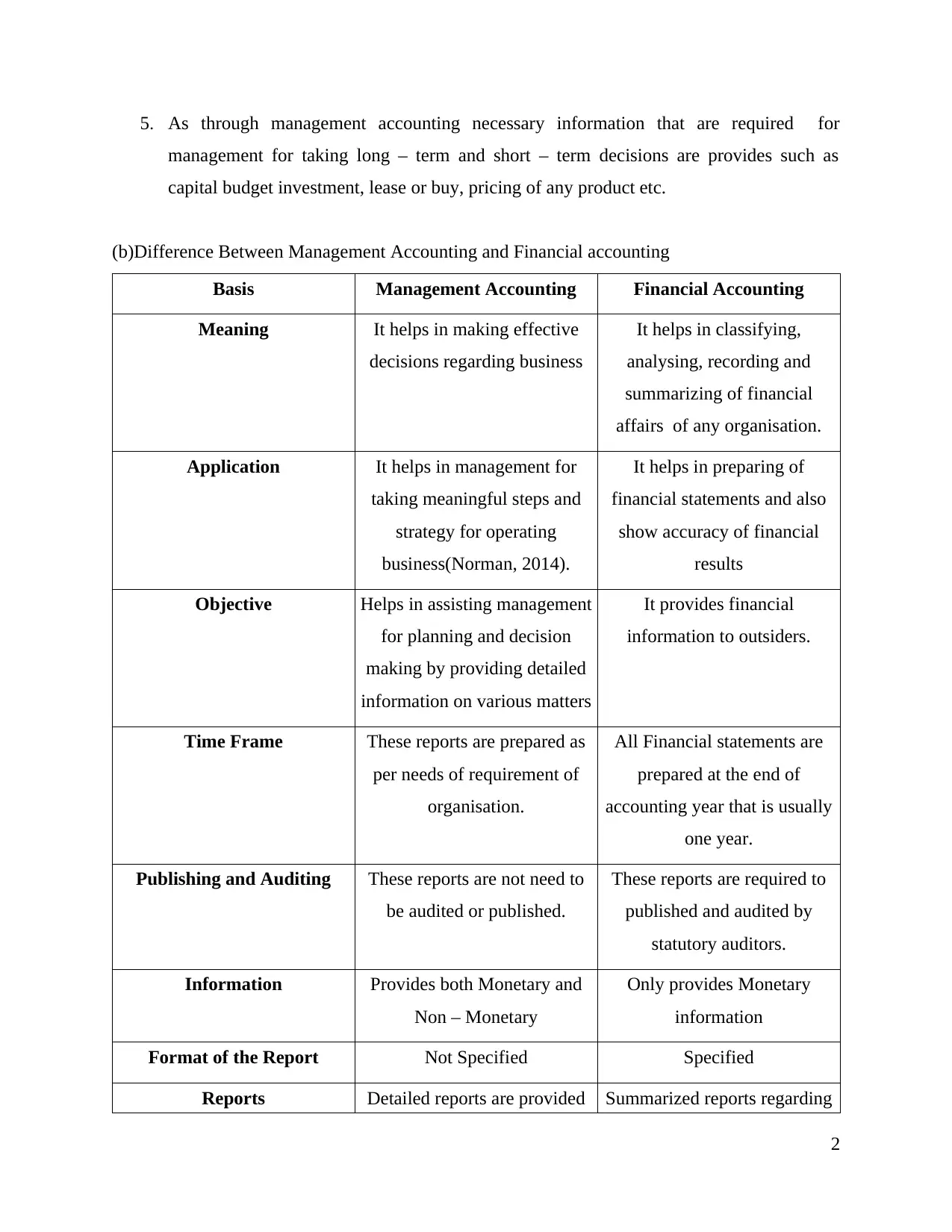

5. As through management accounting necessary information that are required for

management for taking long – term and short – term decisions are provides such as

capital budget investment, lease or buy, pricing of any product etc.

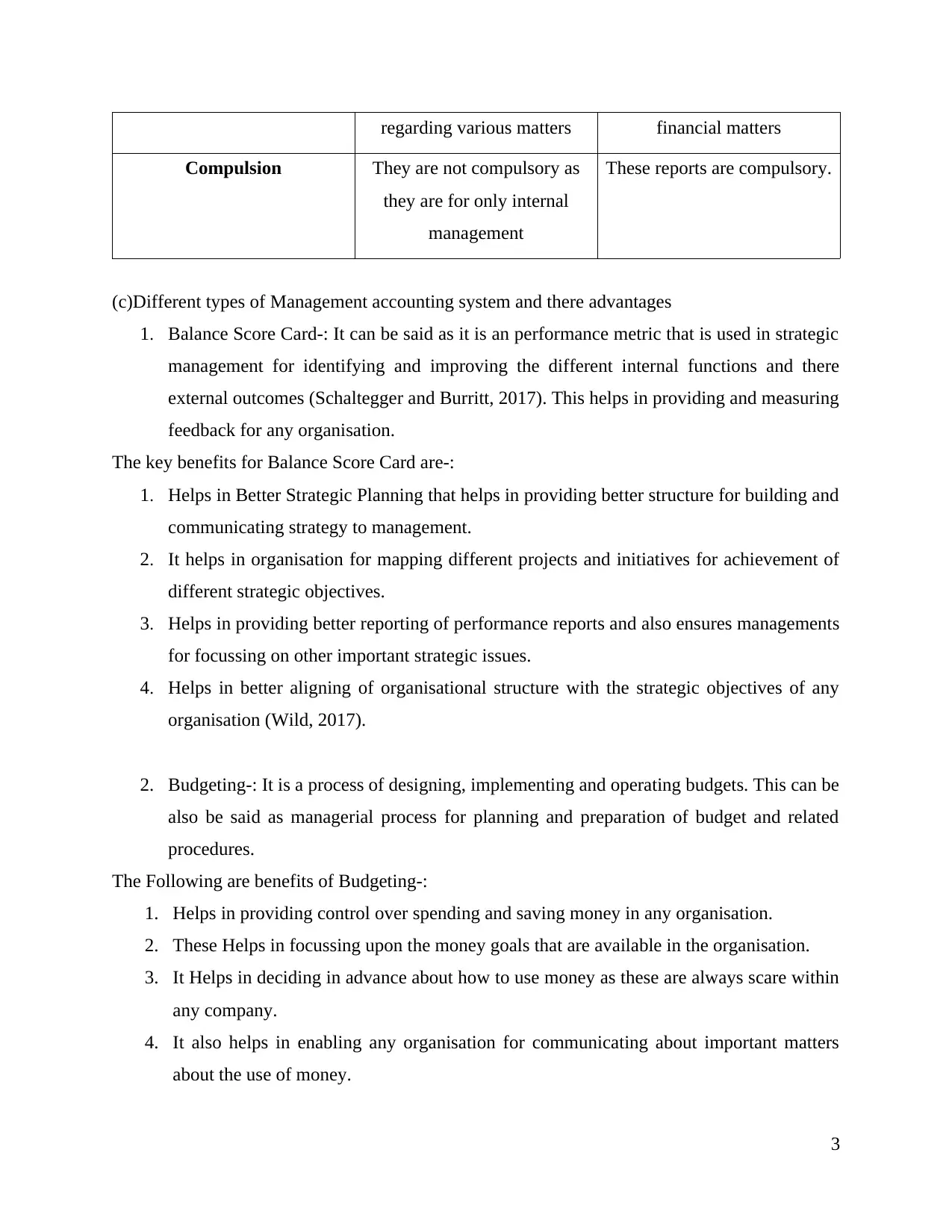

(b)Difference Between Management Accounting and Financial accounting

Basis Management Accounting Financial Accounting

Meaning It helps in making effective

decisions regarding business

It helps in classifying,

analysing, recording and

summarizing of financial

affairs of any organisation.

Application It helps in management for

taking meaningful steps and

strategy for operating

business(Norman, 2014).

It helps in preparing of

financial statements and also

show accuracy of financial

results

Objective Helps in assisting management

for planning and decision

making by providing detailed

information on various matters

It provides financial

information to outsiders.

Time Frame These reports are prepared as

per needs of requirement of

organisation.

All Financial statements are

prepared at the end of

accounting year that is usually

one year.

Publishing and Auditing These reports are not need to

be audited or published.

These reports are required to

published and audited by

statutory auditors.

Information Provides both Monetary and

Non – Monetary

Only provides Monetary

information

Format of the Report Not Specified Specified

Reports Detailed reports are provided Summarized reports regarding

2

management for taking long – term and short – term decisions are provides such as

capital budget investment, lease or buy, pricing of any product etc.

(b)Difference Between Management Accounting and Financial accounting

Basis Management Accounting Financial Accounting

Meaning It helps in making effective

decisions regarding business

It helps in classifying,

analysing, recording and

summarizing of financial

affairs of any organisation.

Application It helps in management for

taking meaningful steps and

strategy for operating

business(Norman, 2014).

It helps in preparing of

financial statements and also

show accuracy of financial

results

Objective Helps in assisting management

for planning and decision

making by providing detailed

information on various matters

It provides financial

information to outsiders.

Time Frame These reports are prepared as

per needs of requirement of

organisation.

All Financial statements are

prepared at the end of

accounting year that is usually

one year.

Publishing and Auditing These reports are not need to

be audited or published.

These reports are required to

published and audited by

statutory auditors.

Information Provides both Monetary and

Non – Monetary

Only provides Monetary

information

Format of the Report Not Specified Specified

Reports Detailed reports are provided Summarized reports regarding

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

regarding various matters financial matters

Compulsion They are not compulsory as

they are for only internal

management

These reports are compulsory.

(c)Different types of Management accounting system and there advantages

1. Balance Score Card-: It can be said as it is an performance metric that is used in strategic

management for identifying and improving the different internal functions and there

external outcomes (Schaltegger and Burritt, 2017). This helps in providing and measuring

feedback for any organisation.

The key benefits for Balance Score Card are-:

1. Helps in Better Strategic Planning that helps in providing better structure for building and

communicating strategy to management.

2. It helps in organisation for mapping different projects and initiatives for achievement of

different strategic objectives.

3. Helps in providing better reporting of performance reports and also ensures managements

for focussing on other important strategic issues.

4. Helps in better aligning of organisational structure with the strategic objectives of any

organisation (Wild, 2017).

2. Budgeting-: It is a process of designing, implementing and operating budgets. This can be

also be said as managerial process for planning and preparation of budget and related

procedures.

The Following are benefits of Budgeting-:

1. Helps in providing control over spending and saving money in any organisation.

2. These Helps in focussing upon the money goals that are available in the organisation.

3. It Helps in deciding in advance about how to use money as these are always scare within

any company.

4. It also helps in enabling any organisation for communicating about important matters

about the use of money.

3

Compulsion They are not compulsory as

they are for only internal

management

These reports are compulsory.

(c)Different types of Management accounting system and there advantages

1. Balance Score Card-: It can be said as it is an performance metric that is used in strategic

management for identifying and improving the different internal functions and there

external outcomes (Schaltegger and Burritt, 2017). This helps in providing and measuring

feedback for any organisation.

The key benefits for Balance Score Card are-:

1. Helps in Better Strategic Planning that helps in providing better structure for building and

communicating strategy to management.

2. It helps in organisation for mapping different projects and initiatives for achievement of

different strategic objectives.

3. Helps in providing better reporting of performance reports and also ensures managements

for focussing on other important strategic issues.

4. Helps in better aligning of organisational structure with the strategic objectives of any

organisation (Wild, 2017).

2. Budgeting-: It is a process of designing, implementing and operating budgets. This can be

also be said as managerial process for planning and preparation of budget and related

procedures.

The Following are benefits of Budgeting-:

1. Helps in providing control over spending and saving money in any organisation.

2. These Helps in focussing upon the money goals that are available in the organisation.

3. It Helps in deciding in advance about how to use money as these are always scare within

any company.

4. It also helps in enabling any organisation for communicating about important matters

about the use of money.

3

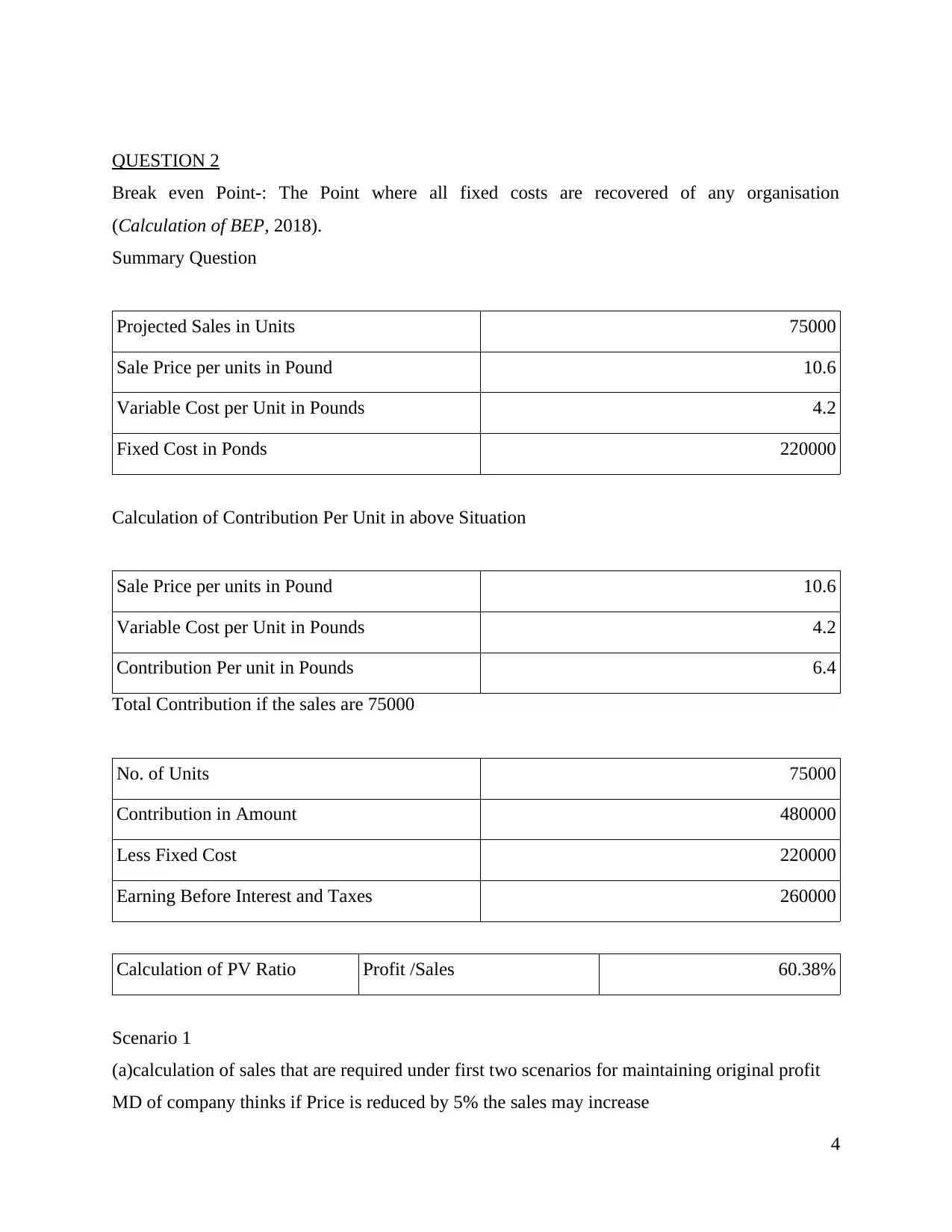

QUESTION 2

Break even Point-: The Point where all fixed costs are recovered of any organisation

(Calculation of BEP, 2018).

Summary Question

Projected Sales in Units 75000

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.2

Fixed Cost in Ponds 220000

Calculation of Contribution Per Unit in above Situation

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.2

Contribution Per unit in Pounds 6.4

Total Contribution if the sales are 75000

No. of Units 75000

Contribution in Amount 480000

Less Fixed Cost 220000

Earning Before Interest and Taxes 260000

Calculation of PV Ratio Profit /Sales 60.38%

Scenario 1

(a)calculation of sales that are required under first two scenarios for maintaining original profit

MD of company thinks if Price is reduced by 5% the sales may increase

4

Break even Point-: The Point where all fixed costs are recovered of any organisation

(Calculation of BEP, 2018).

Summary Question

Projected Sales in Units 75000

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.2

Fixed Cost in Ponds 220000

Calculation of Contribution Per Unit in above Situation

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.2

Contribution Per unit in Pounds 6.4

Total Contribution if the sales are 75000

No. of Units 75000

Contribution in Amount 480000

Less Fixed Cost 220000

Earning Before Interest and Taxes 260000

Calculation of PV Ratio Profit /Sales 60.38%

Scenario 1

(a)calculation of sales that are required under first two scenarios for maintaining original profit

MD of company thinks if Price is reduced by 5% the sales may increase

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

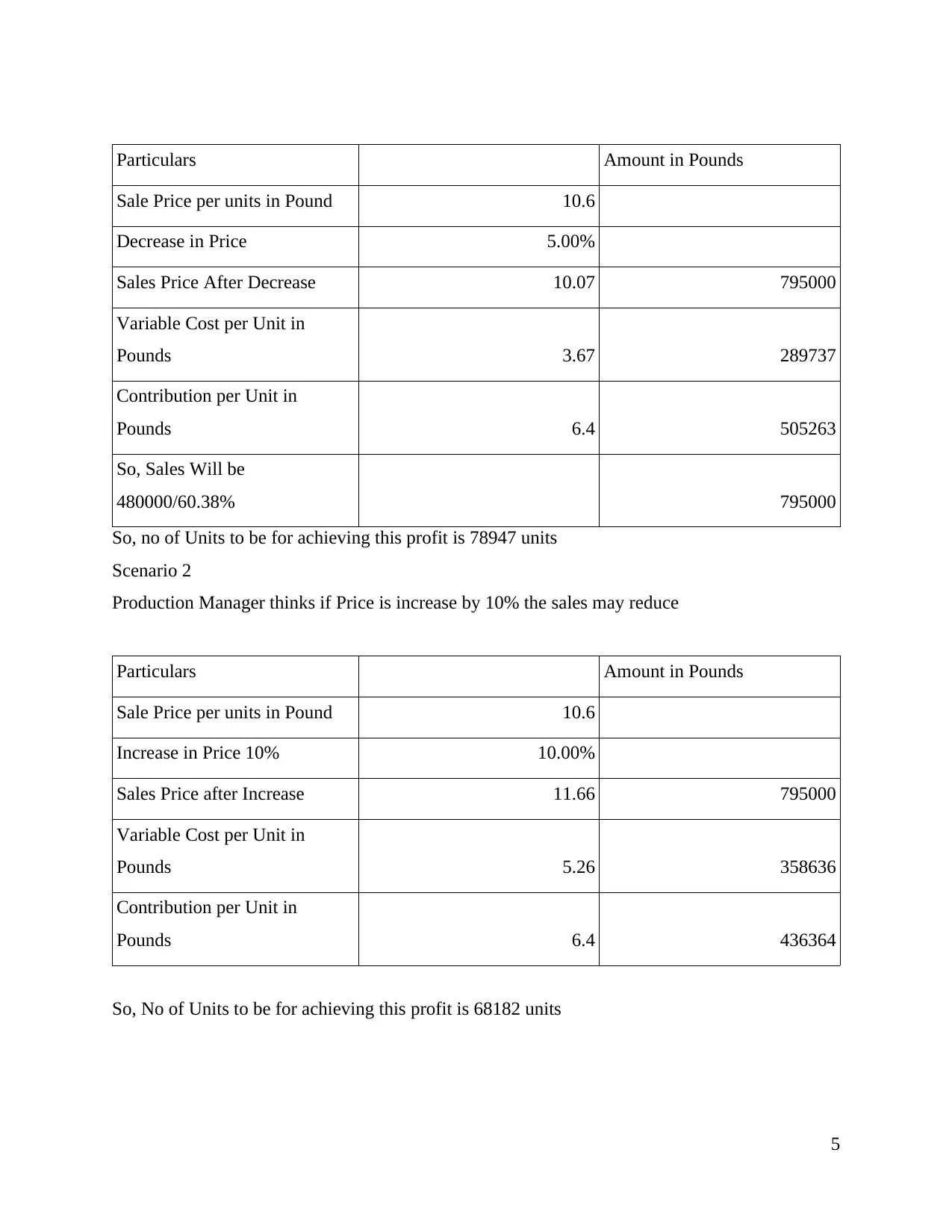

Particulars Amount in Pounds

Sale Price per units in Pound 10.6

Decrease in Price 5.00%

Sales Price After Decrease 10.07 795000

Variable Cost per Unit in

Pounds 3.67 289737

Contribution per Unit in

Pounds 6.4 505263

So, Sales Will be

480000/60.38% 795000

So, no of Units to be for achieving this profit is 78947 units

Scenario 2

Production Manager thinks if Price is increase by 10% the sales may reduce

Particulars Amount in Pounds

Sale Price per units in Pound 10.6

Increase in Price 10% 10.00%

Sales Price after Increase 11.66 795000

Variable Cost per Unit in

Pounds 5.26 358636

Contribution per Unit in

Pounds 6.4 436364

So, No of Units to be for achieving this profit is 68182 units

5

Sale Price per units in Pound 10.6

Decrease in Price 5.00%

Sales Price After Decrease 10.07 795000

Variable Cost per Unit in

Pounds 3.67 289737

Contribution per Unit in

Pounds 6.4 505263

So, Sales Will be

480000/60.38% 795000

So, no of Units to be for achieving this profit is 78947 units

Scenario 2

Production Manager thinks if Price is increase by 10% the sales may reduce

Particulars Amount in Pounds

Sale Price per units in Pound 10.6

Increase in Price 10% 10.00%

Sales Price after Increase 11.66 795000

Variable Cost per Unit in

Pounds 5.26 358636

Contribution per Unit in

Pounds 6.4 436364

So, No of Units to be for achieving this profit is 68182 units

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

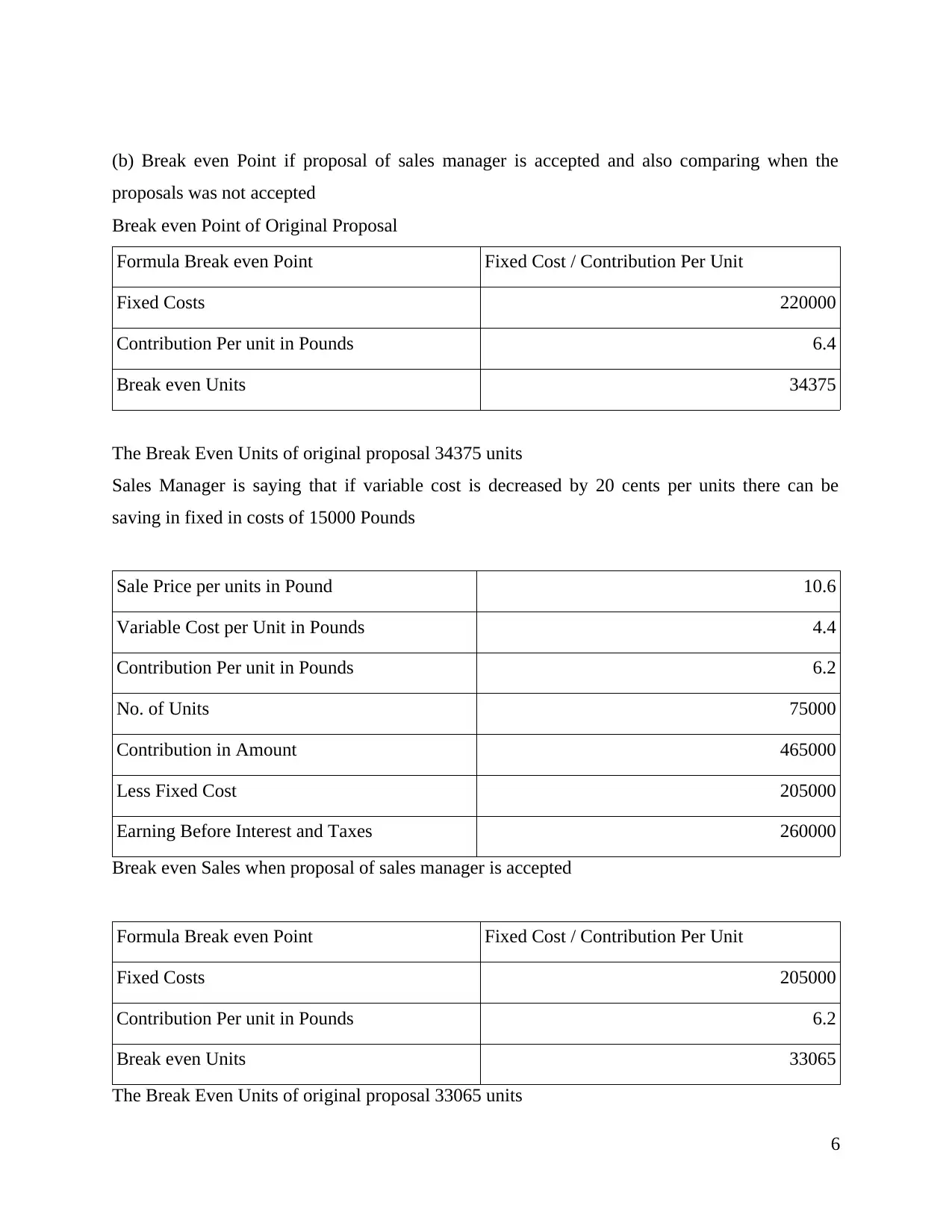

(b) Break even Point if proposal of sales manager is accepted and also comparing when the

proposals was not accepted

Break even Point of Original Proposal

Formula Break even Point Fixed Cost / Contribution Per Unit

Fixed Costs 220000

Contribution Per unit in Pounds 6.4

Break even Units 34375

The Break Even Units of original proposal 34375 units

Sales Manager is saying that if variable cost is decreased by 20 cents per units there can be

saving in fixed in costs of 15000 Pounds

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.4

Contribution Per unit in Pounds 6.2

No. of Units 75000

Contribution in Amount 465000

Less Fixed Cost 205000

Earning Before Interest and Taxes 260000

Break even Sales when proposal of sales manager is accepted

Formula Break even Point Fixed Cost / Contribution Per Unit

Fixed Costs 205000

Contribution Per unit in Pounds 6.2

Break even Units 33065

The Break Even Units of original proposal 33065 units

6

proposals was not accepted

Break even Point of Original Proposal

Formula Break even Point Fixed Cost / Contribution Per Unit

Fixed Costs 220000

Contribution Per unit in Pounds 6.4

Break even Units 34375

The Break Even Units of original proposal 34375 units

Sales Manager is saying that if variable cost is decreased by 20 cents per units there can be

saving in fixed in costs of 15000 Pounds

Sale Price per units in Pound 10.6

Variable Cost per Unit in Pounds 4.4

Contribution Per unit in Pounds 6.2

No. of Units 75000

Contribution in Amount 465000

Less Fixed Cost 205000

Earning Before Interest and Taxes 260000

Break even Sales when proposal of sales manager is accepted

Formula Break even Point Fixed Cost / Contribution Per Unit

Fixed Costs 205000

Contribution Per unit in Pounds 6.2

Break even Units 33065

The Break Even Units of original proposal 33065 units

6

SECTION 2

QUESTION 3

Following Types of Budgets including their Pros and Cons

1. Static Budget-: It is a type of Budget which incorporates different values regarding input

and output that had been calculated before the period had been started. These when

compared to actual results are quite different (Types of Budgets, 2018).

Merits

1. It is very easy to implement and prepare

2. They are not needed to be updated regularly

3. They can offer strong insight about the cost and profits of company.

Demerits

1. This budget lacks flexibility

2. As this budget is made on previous year figures there is more difficulty in implementing

and establishing them.

3. This budget cannot be used where there are more fluctuations.

2. Zero based Budget-: It is a part of management accounting system that helps in

preparing the budget from starting by having Zero as a base. It can also be said as a

method of budget where all expenses of new period are calculated on the basis of actual

expenses that had to be incurred (Types of Budgets, 2018).

Merits

1. Accurate-: as per the regular methods this budgeting involves by making some needed

changes from previous year actual expenses.

2. Effective and Efficient-: This budget helps in effective and efficiently distribute the

resources that the organisations have as they are made after the requirements of every

department (Barr and McClellan, 2018).

3. Communication and Coordination-: It helps in improving communication and co-

ordination that are there within the organisation as it leads to involvement in decision

making of organisation.

Demerits

1. Time Consuming-: This budget is very time consuming as expenses are to determined

communicating and co-ordination with different departments which takes time.

7

QUESTION 3

Following Types of Budgets including their Pros and Cons

1. Static Budget-: It is a type of Budget which incorporates different values regarding input

and output that had been calculated before the period had been started. These when

compared to actual results are quite different (Types of Budgets, 2018).

Merits

1. It is very easy to implement and prepare

2. They are not needed to be updated regularly

3. They can offer strong insight about the cost and profits of company.

Demerits

1. This budget lacks flexibility

2. As this budget is made on previous year figures there is more difficulty in implementing

and establishing them.

3. This budget cannot be used where there are more fluctuations.

2. Zero based Budget-: It is a part of management accounting system that helps in

preparing the budget from starting by having Zero as a base. It can also be said as a

method of budget where all expenses of new period are calculated on the basis of actual

expenses that had to be incurred (Types of Budgets, 2018).

Merits

1. Accurate-: as per the regular methods this budgeting involves by making some needed

changes from previous year actual expenses.

2. Effective and Efficient-: This budget helps in effective and efficiently distribute the

resources that the organisations have as they are made after the requirements of every

department (Barr and McClellan, 2018).

3. Communication and Coordination-: It helps in improving communication and co-

ordination that are there within the organisation as it leads to involvement in decision

making of organisation.

Demerits

1. Time Consuming-: This budget is very time consuming as expenses are to determined

communicating and co-ordination with different departments which takes time.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Lack of Expertise-: As to explain each and every time is difficult and also requires

expertise in the field

3. Rolling Budgets-: It is a new budget and revised set of financial plan for the next

accounting period which is used to replace the older one in a continuous budget system

(Types of Budgets, 2018). In Simple words this budget is updated budget that had been

taken place when the older version expires.

Merits-:

1. This budget helps in planning and controlling more accurate as they reduce the

uncertainty of budget.

2. Spending can be wisely-: As there some places where managers spends more but actually

they are not required. So this budget helps them in guiding spending of money with more

intelligence

Demerits-:

1. Time Consuming-: This budget needs more efforts, time and money as they are mad eon

periodic basis.

2. Uneven Updates-: This can be the main problem with this type of budget as there is no

updating of budget during entire period.

4. Incremental Budget-: This type of budget are been prepared by using the previous year

budgeted or actual performance with some incremental amounts for current period (Types

of Budgets, 2018). In simple words it can be said as by making some small changes in

previous year budget the incremental budget is prepared.

Merits-:

1. It is very easy to implement and there are no complexity in calculations.

2. They ensure for providing funds for the department without making detailed analysis.

3. Impact of this type of budget can be seen immediately (Horngren and et.al., 2014).

Demerits-:

1. As this budget is of incremental it assumes that without have any analysis that the funds

will be required more in the next year from previous period.

8

expertise in the field

3. Rolling Budgets-: It is a new budget and revised set of financial plan for the next

accounting period which is used to replace the older one in a continuous budget system

(Types of Budgets, 2018). In Simple words this budget is updated budget that had been

taken place when the older version expires.

Merits-:

1. This budget helps in planning and controlling more accurate as they reduce the

uncertainty of budget.

2. Spending can be wisely-: As there some places where managers spends more but actually

they are not required. So this budget helps them in guiding spending of money with more

intelligence

Demerits-:

1. Time Consuming-: This budget needs more efforts, time and money as they are mad eon

periodic basis.

2. Uneven Updates-: This can be the main problem with this type of budget as there is no

updating of budget during entire period.

4. Incremental Budget-: This type of budget are been prepared by using the previous year

budgeted or actual performance with some incremental amounts for current period (Types

of Budgets, 2018). In simple words it can be said as by making some small changes in

previous year budget the incremental budget is prepared.

Merits-:

1. It is very easy to implement and there are no complexity in calculations.

2. They ensure for providing funds for the department without making detailed analysis.

3. Impact of this type of budget can be seen immediately (Horngren and et.al., 2014).

Demerits-:

1. As this budget is of incremental it assumes that without have any analysis that the funds

will be required more in the next year from previous period.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. As the approach of budget is of incremental nature it tends managers to spend more as the

organisation is automatically increasing their budget.

(b)The importance of Preparing Budgets-:

1. It helps in figuring out the long term goals of the organisation and by which any manager

must know where and when to spend as the resources are limited.

2. It helps in effective communication of and co-ordination between different departments

of any organisation regarding the spending of money (Hansen, Mowen and Guan, 2017).

3. It helps in forecasting the future cash expenses and receipts to meet future needs and

arrangement of finance.

4. Through Budget the amount is distributed in efficient manner to divisions and

departments as per there requirements.

5. Budget helps in maximising the profits as to achieve the goals the resources are allocated

accordingly so that the utilisation is optimum.

6. Uniform policy is adopted to all divisions and departments so that the budget is allocated

without favouring any branch or divisions.

QUESTION 4

As All-Ace Limited is using perpetual inventory management system it means they are

recording and accounting inventory immediately after sales and purchase through computerized

environment. It immediately shows detailed view off inventory and also provides stock statement

whenever required. They are valuing there inventory as per FIFO method of valuation and now

want to shift to LIFO System. So here are the merits and demerits of both the methods.

FIFO Method

First In First out Method of valuation means that earliest the goods are purchased will be

removed first from Stock Account (Norman, 2014.). This results that with the remaining stock

which is there, all cost that are incurred to kept them will be charged to them.

Merits

1. This method saves time for calculation of exact cost of inventory as it is depended upon

the last purchases of stock.

2. This concept is very easy to understand.

9

organisation is automatically increasing their budget.

(b)The importance of Preparing Budgets-:

1. It helps in figuring out the long term goals of the organisation and by which any manager

must know where and when to spend as the resources are limited.

2. It helps in effective communication of and co-ordination between different departments

of any organisation regarding the spending of money (Hansen, Mowen and Guan, 2017).

3. It helps in forecasting the future cash expenses and receipts to meet future needs and

arrangement of finance.

4. Through Budget the amount is distributed in efficient manner to divisions and

departments as per there requirements.

5. Budget helps in maximising the profits as to achieve the goals the resources are allocated

accordingly so that the utilisation is optimum.

6. Uniform policy is adopted to all divisions and departments so that the budget is allocated

without favouring any branch or divisions.

QUESTION 4

As All-Ace Limited is using perpetual inventory management system it means they are

recording and accounting inventory immediately after sales and purchase through computerized

environment. It immediately shows detailed view off inventory and also provides stock statement

whenever required. They are valuing there inventory as per FIFO method of valuation and now

want to shift to LIFO System. So here are the merits and demerits of both the methods.

FIFO Method

First In First out Method of valuation means that earliest the goods are purchased will be

removed first from Stock Account (Norman, 2014.). This results that with the remaining stock

which is there, all cost that are incurred to kept them will be charged to them.

Merits

1. This method saves time for calculation of exact cost of inventory as it is depended upon

the last purchases of stock.

2. This concept is very easy to understand.

9

3. As it widely used approach it increases comparability and consistency.

Demerits

1. The Biggest disadvantages is that when the inflation rates are high it will show more

profits.

2. This method may not be appropriate measure to calculate inventory when prices of

products are more fluctuating.

LIFO Method

Last in First Out method operates under assumption that inventory that is purchase last

will be sold first (Renz, 2016). If this approach is accepted than there are chances when that the

valuation may be higher than cost of earlier purchase of products.

Merits

1. As in the period of inflation, profits can be understated which can result in tax benefits.

2. It provides better measurements of current earnings by matching all the relevant costs of

the same.

Demerits

1. Inventory is understated as they are based on the older costs.

2. Easily manipulation of records can be done by making changes in purchase pattern.

CONCLUSION

By Summing up this report it states that Management accounting is very much helpful in

decision making of managers. It provides all the information by which they can take better

decisions for effective utilization of resources. This project report also concludes that making of

budget is very important for forecasting of revenue and expenditures in the organisation. It also

concludes that better inventory valuation techniques in FIFO method of Valuation as they are

generally acceptable.

10

Demerits

1. The Biggest disadvantages is that when the inflation rates are high it will show more

profits.

2. This method may not be appropriate measure to calculate inventory when prices of

products are more fluctuating.

LIFO Method

Last in First Out method operates under assumption that inventory that is purchase last

will be sold first (Renz, 2016). If this approach is accepted than there are chances when that the

valuation may be higher than cost of earlier purchase of products.

Merits

1. As in the period of inflation, profits can be understated which can result in tax benefits.

2. It provides better measurements of current earnings by matching all the relevant costs of

the same.

Demerits

1. Inventory is understated as they are based on the older costs.

2. Easily manipulation of records can be done by making changes in purchase pattern.

CONCLUSION

By Summing up this report it states that Management accounting is very much helpful in

decision making of managers. It provides all the information by which they can take better

decisions for effective utilization of resources. This project report also concludes that making of

budget is very important for forecasting of revenue and expenditures in the organisation. It also

concludes that better inventory valuation techniques in FIFO method of Valuation as they are

generally acceptable.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.