Management Accounting Report: Job Order Costing and ABC Analysis

VerifiedAdded on 2020/05/28

|14

|2050

|33

Report

AI Summary

This report examines management accounting principles, focusing on job order costing and activity-based costing (ABC) within the context of Turramurra Furniture. The report begins by defining job order costing and identifying suitable applications, followed by an analysis of work-in-process balances and the calculation of costs for finished goods. It then delves into the computation of over or under-applied overhead, explores different adjustment treatments, and addresses the application of activity-based costing. The report highlights the importance of accurate overhead allocation and the benefits of ABC in improving cost information and strategic decision-making. The conclusion summarizes the key findings and emphasizes the efficiency of job order costing for differentiated products and the advantages of ABC in optimizing overhead allocation.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Management Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Body:..........................................................................................................................................3

Suitable Circumstances for Job Order Costing System.........................................................3

Introduction........................................................................................................................3

Body:..................................................................................................................................3

Work-in-Process Balance.......................................................................................................4

Introduction........................................................................................................................4

Work-in-Process Balance:..................................................................................................4

Cost of Chairs in Finished Goods Inventory:.........................................................................5

Introduction........................................................................................................................5

Computation of Over or Under Applied Overhead................................................................6

Introduction........................................................................................................................6

Different Treatments for Adjusting Over Applied Overheads:..............................................7

Introduction........................................................................................................................7

Different Treatments for Adjusting Over Applied Overheads:..........................................7

Approach for Adjusting Over Applied Material Cost............................................................8

Activity Based Costing..........................................................................................................9

Introduction........................................................................................................................9

Activity Based Costing......................................................................................................9

Conclusion................................................................................................................................11

Reference List..........................................................................................................................12

MANAGEMENT ACCOUNTING

Table of Contents

Introduction................................................................................................................................2

Body:..........................................................................................................................................3

Suitable Circumstances for Job Order Costing System.........................................................3

Introduction........................................................................................................................3

Body:..................................................................................................................................3

Work-in-Process Balance.......................................................................................................4

Introduction........................................................................................................................4

Work-in-Process Balance:..................................................................................................4

Cost of Chairs in Finished Goods Inventory:.........................................................................5

Introduction........................................................................................................................5

Computation of Over or Under Applied Overhead................................................................6

Introduction........................................................................................................................6

Different Treatments for Adjusting Over Applied Overheads:..............................................7

Introduction........................................................................................................................7

Different Treatments for Adjusting Over Applied Overheads:..........................................7

Approach for Adjusting Over Applied Material Cost............................................................8

Activity Based Costing..........................................................................................................9

Introduction........................................................................................................................9

Activity Based Costing......................................................................................................9

Conclusion................................................................................................................................11

Reference List..........................................................................................................................12

2

MANAGEMENT ACCOUNTING

Introduction

The company that is under consideration in this paper is Turramurra Furniture, which

is a specialised organization for making use of the computer. There are numerous kinds of

furniture that are manufactured under variant job numbers. This report is constructed to

ascertain the cost of every kind of the furniture and explains the method of cost assumption

under the process of job order costing.

MANAGEMENT ACCOUNTING

Introduction

The company that is under consideration in this paper is Turramurra Furniture, which

is a specialised organization for making use of the computer. There are numerous kinds of

furniture that are manufactured under variant job numbers. This report is constructed to

ascertain the cost of every kind of the furniture and explains the method of cost assumption

under the process of job order costing.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT ACCOUNTING

Body:

Suitable Circumstances for Job Order Costing System

Introduction

Job Order Costing System is a kind of costing method that is generally used by the

manufacturing industries in order to keep track about the manufacturing process and the

number of products that have been produced in a day or a batch. This part would therefore

determine the appropriate situations that can be used for the purpose of Job Order Costing

System

Body:

There are several scenarios within which the method of job order costing process can

be utilised by the firms and even individuals. The process of job order costing is generally

exploited by the organizations that have the capability of manufacturing various kinds of and

number of products that are way different from each other. It is a kind of costing process that

is used extensively in the manufacturing process along with the industries that are related to

the service sector (Weygandt, Kimmel and Kieso 2015). The manufacturing units and

organizations that are exploiting the process of job costing usually attain the orders for their

tailored products and services. These orders that have been tailored by nature are called the

jobs and the batches. When a company permits the orders and the jobs for different products,

the allotment of the cost towards the product become a tough job. In this respect, the record

for every expense for every distinct job is maintained due to the reason that each of the jobs

have several products and services associated with it (Edmonds et al. 2016). The expense per

unit of a distinct task is computed by dividing the total allocated cost to that job by the

MANAGEMENT ACCOUNTING

Body:

Suitable Circumstances for Job Order Costing System

Introduction

Job Order Costing System is a kind of costing method that is generally used by the

manufacturing industries in order to keep track about the manufacturing process and the

number of products that have been produced in a day or a batch. This part would therefore

determine the appropriate situations that can be used for the purpose of Job Order Costing

System

Body:

There are several scenarios within which the method of job order costing process can

be utilised by the firms and even individuals. The process of job order costing is generally

exploited by the organizations that have the capability of manufacturing various kinds of and

number of products that are way different from each other. It is a kind of costing process that

is used extensively in the manufacturing process along with the industries that are related to

the service sector (Weygandt, Kimmel and Kieso 2015). The manufacturing units and

organizations that are exploiting the process of job costing usually attain the orders for their

tailored products and services. These orders that have been tailored by nature are called the

jobs and the batches. When a company permits the orders and the jobs for different products,

the allotment of the cost towards the product become a tough job. In this respect, the record

for every expense for every distinct job is maintained due to the reason that each of the jobs

have several products and services associated with it (Edmonds et al. 2016). The expense per

unit of a distinct task is computed by dividing the total allocated cost to that job by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT ACCOUNTING

number of the distinct units related to the job. The three basic aspects of job order costing

process is inclusive of the cost of labour, materials and the factory overhead cost.

Work-in-Process Balance

Introduction

The work-in-process balance is even known as the balance for the work-in-progress,

which is the sum of all the expenses that has been put in the process of manufacturing the

product that have been concluded partially (Schönsleben 2016). This even addresses the

labour, overhead expenses and the raw materials that have been incurred for the products that

are available at several stages of the manufacturing process. The balance for Turramurra

Furniture has been depicted in the table below:

Work-in-Process Balance:

Particulars SE523 PS612 CH421 DS174 Total

Opening WIP 20000 25000 15000 0

Quantity Completed 20000 0 15000 5000

Closing WIP Units 0 25000 0 0

Opening Value of Work-in-Process $ 3,00,000 $ 3,00,000

Raw Material $ 2,21,000 $ 2,21,000

Labor Cost $ 2,00,500 $ 2,00,500

Manufacturing Overhead $ 97,500 $ 97,500

Closing Value of Work-in-Process $ 0 $ 8,19,000 $ 0 $ 0 $ 8,19,000

MANAGEMENT ACCOUNTING

number of the distinct units related to the job. The three basic aspects of job order costing

process is inclusive of the cost of labour, materials and the factory overhead cost.

Work-in-Process Balance

Introduction

The work-in-process balance is even known as the balance for the work-in-progress,

which is the sum of all the expenses that has been put in the process of manufacturing the

product that have been concluded partially (Schönsleben 2016). This even addresses the

labour, overhead expenses and the raw materials that have been incurred for the products that

are available at several stages of the manufacturing process. The balance for Turramurra

Furniture has been depicted in the table below:

Work-in-Process Balance:

Particulars SE523 PS612 CH421 DS174 Total

Opening WIP 20000 25000 15000 0

Quantity Completed 20000 0 15000 5000

Closing WIP Units 0 25000 0 0

Opening Value of Work-in-Process $ 3,00,000 $ 3,00,000

Raw Material $ 2,21,000 $ 2,21,000

Labor Cost $ 2,00,500 $ 2,00,500

Manufacturing Overhead $ 97,500 $ 97,500

Closing Value of Work-in-Process $ 0 $ 8,19,000 $ 0 $ 0 $ 8,19,000

5

MANAGEMENT ACCOUNTING

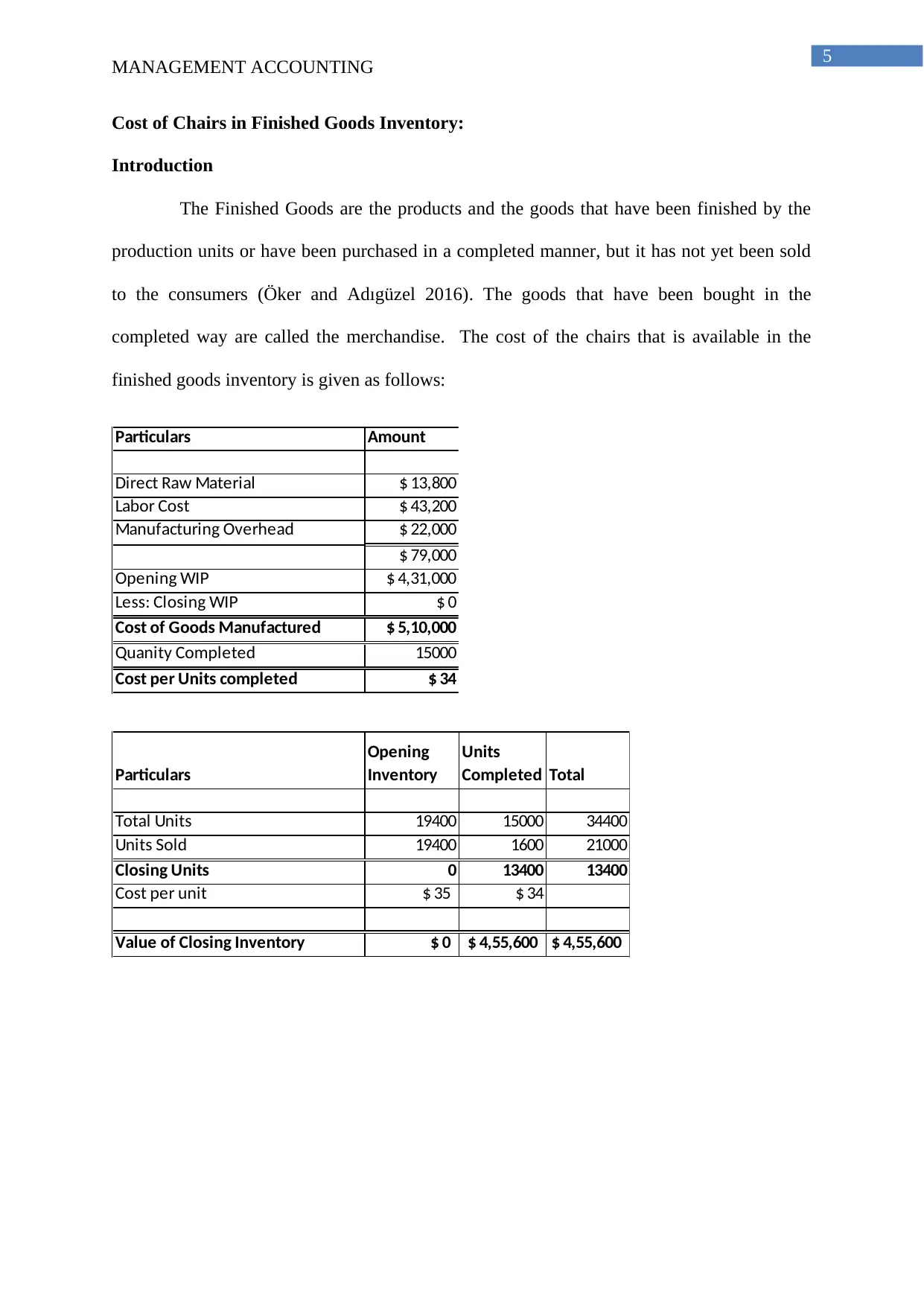

Cost of Chairs in Finished Goods Inventory:

Introduction

The Finished Goods are the products and the goods that have been finished by the

production units or have been purchased in a completed manner, but it has not yet been sold

to the consumers (Öker and Adıgüzel 2016). The goods that have been bought in the

completed way are called the merchandise. The cost of the chairs that is available in the

finished goods inventory is given as follows:

Particulars Amount

Direct Raw Material $ 13,800

Labor Cost $ 43,200

Manufacturing Overhead $ 22,000

$ 79,000

Opening WIP $ 4,31,000

Less: Closing WIP $ 0

Cost of Goods Manufactured $ 5,10,000

Quanity Completed 15000

Cost per Units completed $ 34

Particulars

Opening

Inventory

Units

Completed Total

Total Units 19400 15000 34400

Units Sold 19400 1600 21000

Closing Units 0 13400 13400

Cost per unit $ 35 $ 34

Value of Closing Inventory $ 0 $ 4,55,600 $ 4,55,600

MANAGEMENT ACCOUNTING

Cost of Chairs in Finished Goods Inventory:

Introduction

The Finished Goods are the products and the goods that have been finished by the

production units or have been purchased in a completed manner, but it has not yet been sold

to the consumers (Öker and Adıgüzel 2016). The goods that have been bought in the

completed way are called the merchandise. The cost of the chairs that is available in the

finished goods inventory is given as follows:

Particulars Amount

Direct Raw Material $ 13,800

Labor Cost $ 43,200

Manufacturing Overhead $ 22,000

$ 79,000

Opening WIP $ 4,31,000

Less: Closing WIP $ 0

Cost of Goods Manufactured $ 5,10,000

Quanity Completed 15000

Cost per Units completed $ 34

Particulars

Opening

Inventory

Units

Completed Total

Total Units 19400 15000 34400

Units Sold 19400 1600 21000

Closing Units 0 13400 13400

Cost per unit $ 35 $ 34

Value of Closing Inventory $ 0 $ 4,55,600 $ 4,55,600

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT ACCOUNTING

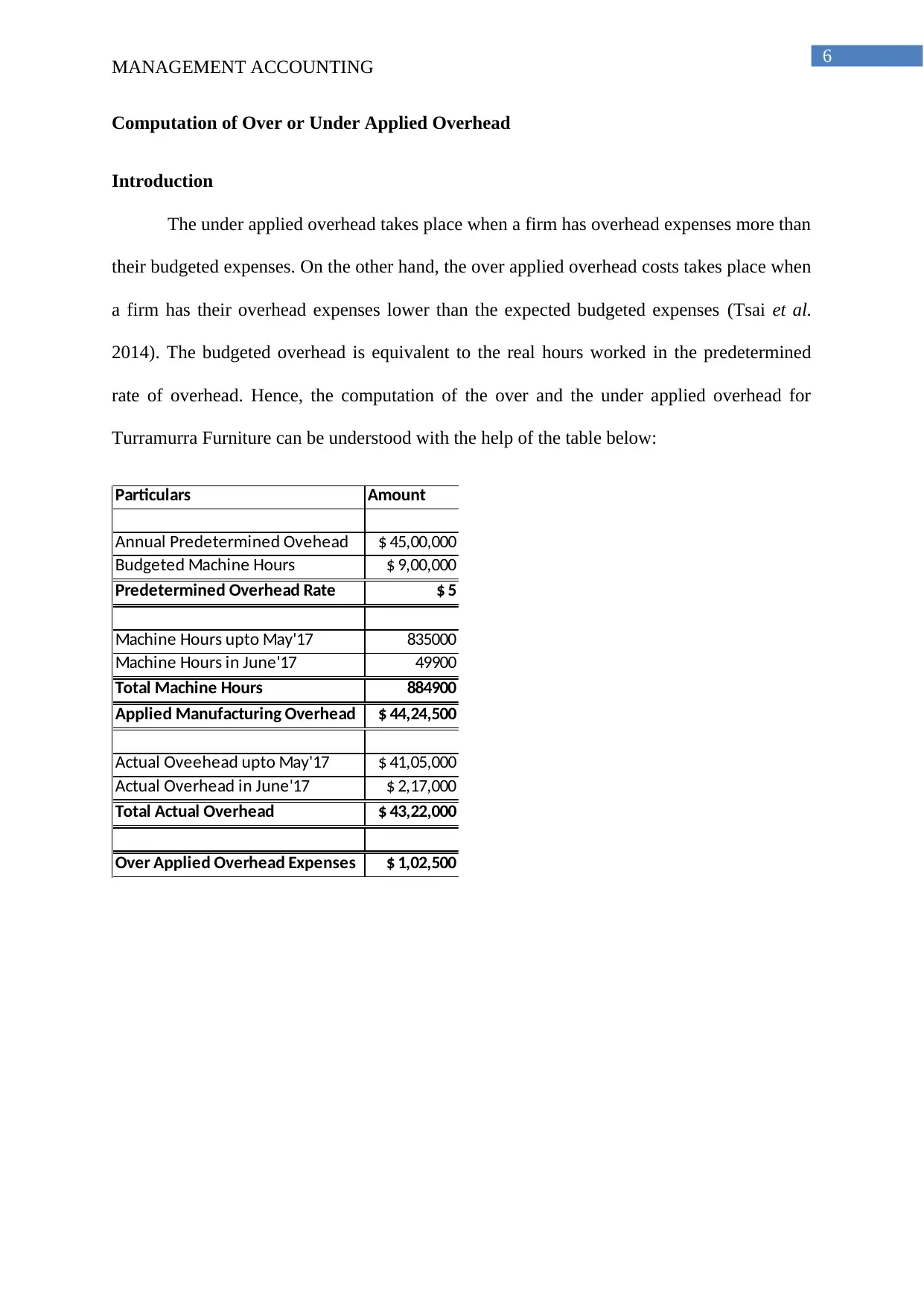

Computation of Over or Under Applied Overhead

Introduction

The under applied overhead takes place when a firm has overhead expenses more than

their budgeted expenses. On the other hand, the over applied overhead costs takes place when

a firm has their overhead expenses lower than the expected budgeted expenses (Tsai et al.

2014). The budgeted overhead is equivalent to the real hours worked in the predetermined

rate of overhead. Hence, the computation of the over and the under applied overhead for

Turramurra Furniture can be understood with the help of the table below:

Particulars Amount

Annual Predetermined Ovehead $ 45,00,000

Budgeted Machine Hours $ 9,00,000

Predetermined Overhead Rate $ 5

Machine Hours upto May'17 835000

Machine Hours in June'17 49900

Total Machine Hours 884900

Applied Manufacturing Overhead $ 44,24,500

Actual Oveehead upto May'17 $ 41,05,000

Actual Overhead in June'17 $ 2,17,000

Total Actual Overhead $ 43,22,000

Over Applied Overhead Expenses $ 1,02,500

MANAGEMENT ACCOUNTING

Computation of Over or Under Applied Overhead

Introduction

The under applied overhead takes place when a firm has overhead expenses more than

their budgeted expenses. On the other hand, the over applied overhead costs takes place when

a firm has their overhead expenses lower than the expected budgeted expenses (Tsai et al.

2014). The budgeted overhead is equivalent to the real hours worked in the predetermined

rate of overhead. Hence, the computation of the over and the under applied overhead for

Turramurra Furniture can be understood with the help of the table below:

Particulars Amount

Annual Predetermined Ovehead $ 45,00,000

Budgeted Machine Hours $ 9,00,000

Predetermined Overhead Rate $ 5

Machine Hours upto May'17 835000

Machine Hours in June'17 49900

Total Machine Hours 884900

Applied Manufacturing Overhead $ 44,24,500

Actual Oveehead upto May'17 $ 41,05,000

Actual Overhead in June'17 $ 2,17,000

Total Actual Overhead $ 43,22,000

Over Applied Overhead Expenses $ 1,02,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT ACCOUNTING

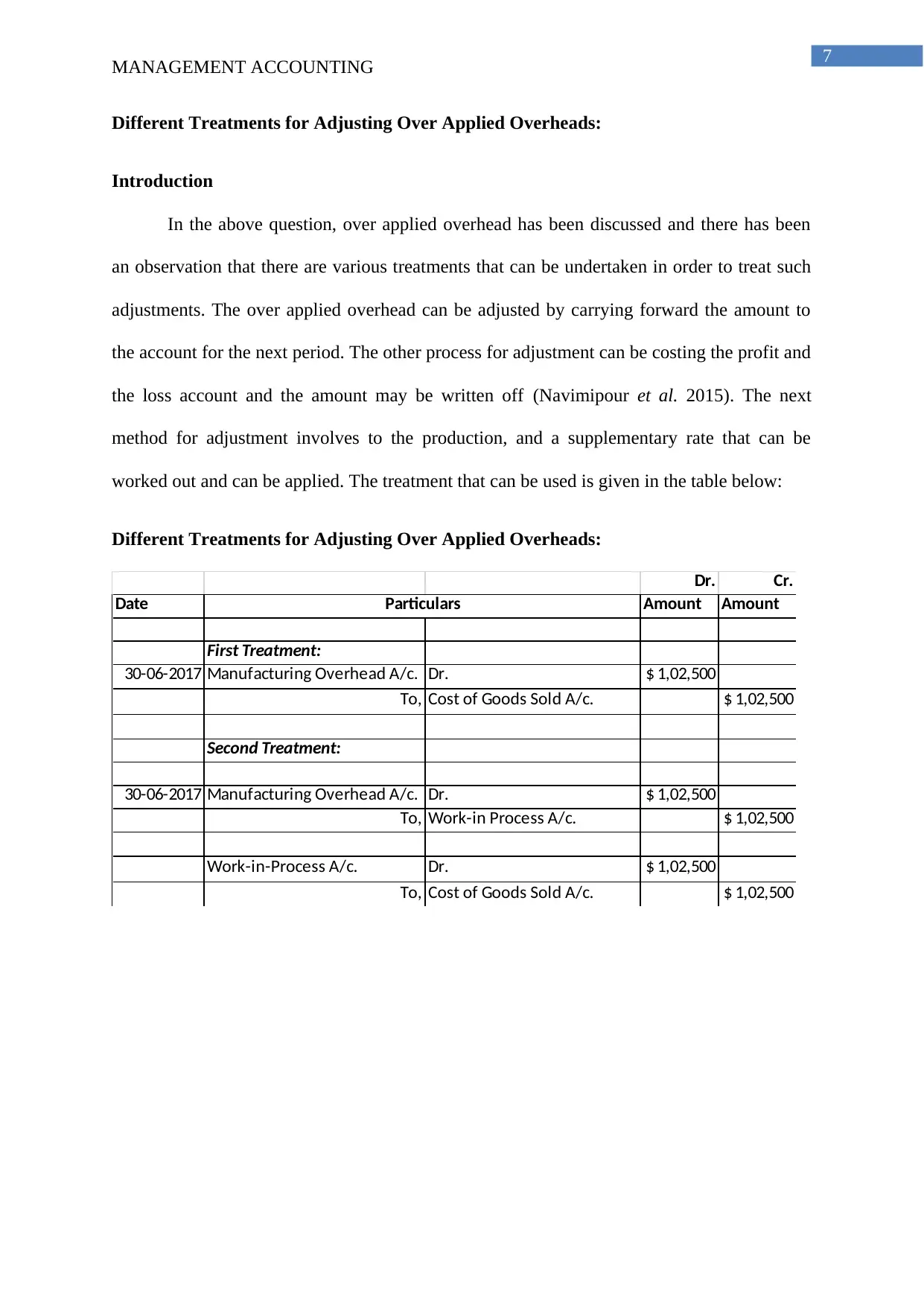

Different Treatments for Adjusting Over Applied Overheads:

Introduction

In the above question, over applied overhead has been discussed and there has been

an observation that there are various treatments that can be undertaken in order to treat such

adjustments. The over applied overhead can be adjusted by carrying forward the amount to

the account for the next period. The other process for adjustment can be costing the profit and

the loss account and the amount may be written off (Navimipour et al. 2015). The next

method for adjustment involves to the production, and a supplementary rate that can be

worked out and can be applied. The treatment that can be used is given in the table below:

Different Treatments for Adjusting Over Applied Overheads:

Dr. Cr.

Date Amount Amount

First Treatment:

30-06-2017 Manufacturing Overhead A/c. Dr. $ 1,02,500

To, Cost of Goods Sold A/c. $ 1,02,500

Second Treatment:

30-06-2017 Manufacturing Overhead A/c. Dr. $ 1,02,500

To, Work-in Process A/c. $ 1,02,500

Work-in-Process A/c. Dr. $ 1,02,500

To, Cost of Goods Sold A/c. $ 1,02,500

Particulars

MANAGEMENT ACCOUNTING

Different Treatments for Adjusting Over Applied Overheads:

Introduction

In the above question, over applied overhead has been discussed and there has been

an observation that there are various treatments that can be undertaken in order to treat such

adjustments. The over applied overhead can be adjusted by carrying forward the amount to

the account for the next period. The other process for adjustment can be costing the profit and

the loss account and the amount may be written off (Navimipour et al. 2015). The next

method for adjustment involves to the production, and a supplementary rate that can be

worked out and can be applied. The treatment that can be used is given in the table below:

Different Treatments for Adjusting Over Applied Overheads:

Dr. Cr.

Date Amount Amount

First Treatment:

30-06-2017 Manufacturing Overhead A/c. Dr. $ 1,02,500

To, Cost of Goods Sold A/c. $ 1,02,500

Second Treatment:

30-06-2017 Manufacturing Overhead A/c. Dr. $ 1,02,500

To, Work-in Process A/c. $ 1,02,500

Work-in-Process A/c. Dr. $ 1,02,500

To, Cost of Goods Sold A/c. $ 1,02,500

Particulars

8

MANAGEMENT ACCOUNTING

Approach for Adjusting Over Applied Material Cost

In order to resolve the issues that is related to the under and over utilisation of the

overhead products, Turramurra Furniture Company has looked to debit the manufacturing

overhead and the provide a credit to the cost of goods sold and the next adjustment of the

production overhead has been debiting cost of the manufacturing overhead with the work in

progress and then debit the work in progress along with the cost of goods sold (Kim,

Schmidgall and Damitio 2017). These adjustments would be able to resolve the problems that

is existent in the under and over application of the manufacturing overhead.

MANAGEMENT ACCOUNTING

Approach for Adjusting Over Applied Material Cost

In order to resolve the issues that is related to the under and over utilisation of the

overhead products, Turramurra Furniture Company has looked to debit the manufacturing

overhead and the provide a credit to the cost of goods sold and the next adjustment of the

production overhead has been debiting cost of the manufacturing overhead with the work in

progress and then debit the work in progress along with the cost of goods sold (Kim,

Schmidgall and Damitio 2017). These adjustments would be able to resolve the problems that

is existent in the under and over application of the manufacturing overhead.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT ACCOUNTING

Activity Based Costing

Introduction

The process of activity based costing is one of the key accounting practices that have

been exploited by the product and service industries and even by individuals. Hence, this

section of the paper would explain this costing method.

Activity Based Costing

The company is worried about their computation and the incorporation of the

overhead and has the intention of making use of the Activity Based Costing as it has the

intention of developing their range of products and is even worried about the application of

the overheads. The Activity Based Costing is usually exploited by the production firms as it

enhances the dependability of the cost information and hence the firms come close to the

authentic and true expenses and improved classification of the costs that have been gained by

the company during the process of manufacturing (Braun et al. 2014). The method of costing

is utilised in the product costing, profitability of the customers, target costing and assessment

of profitability and service pricing. This has been widely popular as the firms can construct

an effective corporate strategy and the focus if the expenses are attained efficiently. The

method of Activity Based Costing exploits various pools of costing controlled by the

operations in order to assign overhead expenses (Joseph 2014). The knowledge has been that

the operations are required to produce the products and assessing the finished products and

accumulating the product. These operations can be costly and hence the costs of the

operations require to be assigned to the product dependent on the use of the product activities.

An activity is a process that looks to make use of the overhead costs. The goal is to

have knowledge about all the operations that is needed to produce the product for the firm.

This process needs the overhead costs associated with each operation that is to be allocated to

MANAGEMENT ACCOUNTING

Activity Based Costing

Introduction

The process of activity based costing is one of the key accounting practices that have

been exploited by the product and service industries and even by individuals. Hence, this

section of the paper would explain this costing method.

Activity Based Costing

The company is worried about their computation and the incorporation of the

overhead and has the intention of making use of the Activity Based Costing as it has the

intention of developing their range of products and is even worried about the application of

the overheads. The Activity Based Costing is usually exploited by the production firms as it

enhances the dependability of the cost information and hence the firms come close to the

authentic and true expenses and improved classification of the costs that have been gained by

the company during the process of manufacturing (Braun et al. 2014). The method of costing

is utilised in the product costing, profitability of the customers, target costing and assessment

of profitability and service pricing. This has been widely popular as the firms can construct

an effective corporate strategy and the focus if the expenses are attained efficiently. The

method of Activity Based Costing exploits various pools of costing controlled by the

operations in order to assign overhead expenses (Joseph 2014). The knowledge has been that

the operations are required to produce the products and assessing the finished products and

accumulating the product. These operations can be costly and hence the costs of the

operations require to be assigned to the product dependent on the use of the product activities.

An activity is a process that looks to make use of the overhead costs. The goal is to

have knowledge about all the operations that is needed to produce the product for the firm.

This process needs the overhead costs associated with each operation that is to be allocated to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT ACCOUNTING

the operations (Gigler et al. 2014). Therefore, Activity Based Costing is useful for looking at

the overhead applications and range of the products.

MANAGEMENT ACCOUNTING

the operations (Gigler et al. 2014). Therefore, Activity Based Costing is useful for looking at

the overhead applications and range of the products.

11

MANAGEMENT ACCOUNTING

Conclusion

It can be addressed by looking at the discussion that have been made earlier that Job

Order Costing is an efficient process of ascertaining the cost of various differentiated

products. The administration has assigned the overhead to the expense of the product at an

increased rate than the real rate of overhead. Conversely, the management can even make

alterations on the over applied overhead in the various processes and under each of the

processes, there would be a reduction in the cost of goods sold.

The organization can even optimise the issues associated to the allocation of the

overhead by incorporating the Activity Based Costing process. It would assist the firm to

assign the overheads according to the benefits attained by every product and even to ascertain

the cost more effectively.

MANAGEMENT ACCOUNTING

Conclusion

It can be addressed by looking at the discussion that have been made earlier that Job

Order Costing is an efficient process of ascertaining the cost of various differentiated

products. The administration has assigned the overhead to the expense of the product at an

increased rate than the real rate of overhead. Conversely, the management can even make

alterations on the over applied overhead in the various processes and under each of the

processes, there would be a reduction in the cost of goods sold.

The organization can even optimise the issues associated to the allocation of the

overhead by incorporating the Activity Based Costing process. It would assist the firm to

assign the overheads according to the benefits attained by every product and even to ascertain

the cost more effectively.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.