Management Accounting Report: Systems, Methods, and Income Statements

VerifiedAdded on 2020/07/23

|19

|5069

|63

Report

AI Summary

This report provides a comprehensive overview of management accounting practices within R.L. Maynard Limited, a construction company. It begins by explaining different management accounting systems such as cost accounting, price optimization, stock management, and job costing, and their significance for the company. The report then describes various methods used for management accounting reporting, including accounts receivables ageing, budget reports, stock and manufacturing reports, and job cost reports. Furthermore, the report includes the preparation of an income statement using both marginal and absorption costing methods, highlighting the differences between the two. It also explores the advantages and disadvantages of planning tools under budgetary control and discusses how the organization can respond to financial problems by adopting a management accounting system. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in making informed business decisions and ensuring sustainable growth.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining different systems of MA considered by accountant of R.L. Maynard Limited...1

P2 Describing several methods which are taken into account for MA reporting at the

workplace of R.L. Maynard Limited...........................................................................................3

TASK 2............................................................................................................................................6

P3 Preparation of income statement on the basis of marginal as well as absorption costing.....6

Difference between both the MA techniques which are marginal and absorption.....................7

TASK 3............................................................................................................................................8

P4. Explaining advantages and disadvantages of different types of planning tools under

budgetary control........................................................................................................................8

TASK 4..........................................................................................................................................12

P5. Different ways by which organisation can respond to financial problems by adopting

management accounting system................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Explaining different systems of MA considered by accountant of R.L. Maynard Limited...1

P2 Describing several methods which are taken into account for MA reporting at the

workplace of R.L. Maynard Limited...........................................................................................3

TASK 2............................................................................................................................................6

P3 Preparation of income statement on the basis of marginal as well as absorption costing.....6

Difference between both the MA techniques which are marginal and absorption.....................7

TASK 3............................................................................................................................................8

P4. Explaining advantages and disadvantages of different types of planning tools under

budgetary control........................................................................................................................8

TASK 4..........................................................................................................................................12

P5. Different ways by which organisation can respond to financial problems by adopting

management accounting system................................................................................................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management Accounting or Managerial accounting is a management tool that provides

basis to small business owners and managers for the preparation of management reports and

accounts. It helps in providing accurate band timely internal information to managers about the

organisation that in turns enable them in taking various future economic decisions along with

evaluating performance of the company.

Unlike financial accounting, management accounting does not provide annual reports.

Instead, it provides interim reports that are for the use of internal users only and not for external

users. However, reports of managerial accounting facilitates annual reports of business. Present

report discusses management accounting system and its benefits to R.L. Maynard Limited. It is a

small sized company from construction industry. Different types of systems and reports that can

be used by cited firm are explained along with producing its income statement using two

different techniques of costing.

Both the techniques treat costs differently that is also explained. Further, management

can use different planning tools under budgetary control and so the same are discussed with their

advantages and disadvantages. An organisation faces different financial problems in its day to

day activities, in order to respond to such problems, it can also use management accounting

system and can lead to sustainable growth.

Management Accounting or Managerial accounting is a management tool that provides

basis to small business owners and managers for the preparation of management reports and

accounts. It helps in providing accurate band timely internal information to managers about the

organisation that in turns enable them in taking various future economic decisions along with

evaluating performance of the company.

Unlike financial accounting, management accounting does not provide annual reports.

Instead, it provides interim reports that are for the use of internal users only and not for external

users. However, reports of managerial accounting facilitates annual reports of business. Present

report discusses management accounting system and its benefits to R.L. Maynard Limited. It is a

small sized company from construction industry. Different types of systems and reports that can

be used by cited firm are explained along with producing its income statement using two

different techniques of costing.

Both the techniques treat costs differently that is also explained. Further, management

can use different planning tools under budgetary control and so the same are discussed with their

advantages and disadvantages. An organisation faces different financial problems in its day to

day activities, in order to respond to such problems, it can also use management accounting

system and can lead to sustainable growth.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 1

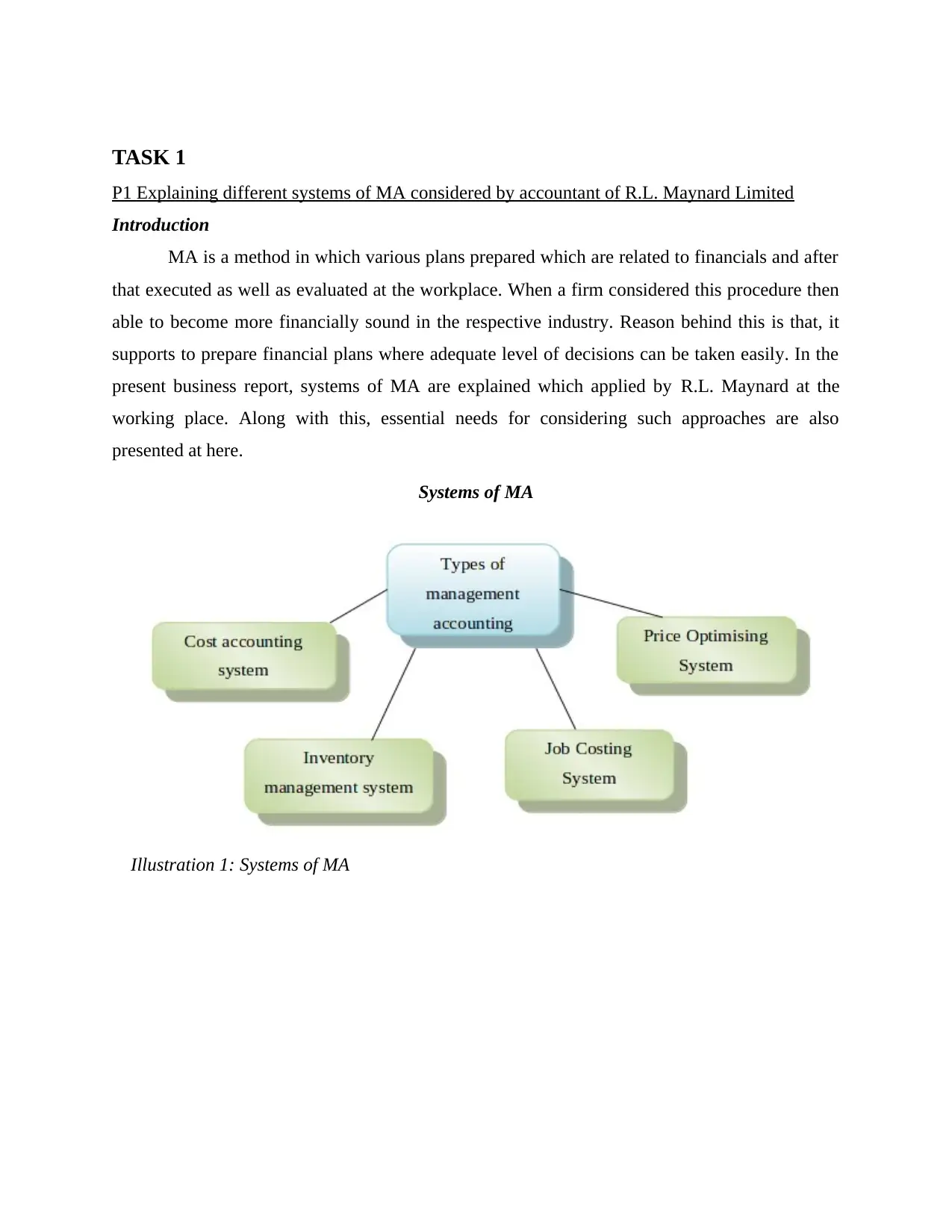

P1 Explaining different systems of MA considered by accountant of R.L. Maynard Limited

Introduction

MA is a method in which various plans prepared which are related to financials and after

that executed as well as evaluated at the workplace. When a firm considered this procedure then

able to become more financially sound in the respective industry. Reason behind this is that, it

supports to prepare financial plans where adequate level of decisions can be taken easily. In the

present business report, systems of MA are explained which applied by R.L. Maynard at the

working place. Along with this, essential needs for considering such approaches are also

presented at here.

Systems of MA

Illustration 1: Systems of MA

(Source: Jansen, 2011)

P1 Explaining different systems of MA considered by accountant of R.L. Maynard Limited

Introduction

MA is a method in which various plans prepared which are related to financials and after

that executed as well as evaluated at the workplace. When a firm considered this procedure then

able to become more financially sound in the respective industry. Reason behind this is that, it

supports to prepare financial plans where adequate level of decisions can be taken easily. In the

present business report, systems of MA are explained which applied by R.L. Maynard at the

working place. Along with this, essential needs for considering such approaches are also

presented at here.

Systems of MA

Illustration 1: Systems of MA

(Source: Jansen, 2011)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting: For every company of any sector, cost is one of the crucial part which must be

lower at the workplace. To manage as well as reduce total expenses, it is necessary to know

overall cost incurred for constructing the buildings. With the help of this particular system of

MA, accountant of R.L. Maynard Limited able to determine costs associated with the business

for constructing the buildings as well as houses. Once this required data derived at the working

environment then management easily able to make pricing decisions in fruitful manner. Further,

it is basically needed for assessing costs which is occurred in production, administration and

selling the products (Baldvinsdottir, Mitchell and Nørreklit, 2010). Another requirement to

consider this system is that, R.L. Maynard able to identify costs by classifying in different parts

like fixed, variable and semi-variable. In addition to this, it consists of target, standard,

throughput, activity based costing etc. by which the manager able to take effectual level of

business decisions.

Price optimisation: Apart from the costs, pricing factor also has pivotal role at the workplace of

each organisation. The reason is that, attraction level of customers and profitability position of

business both depended on this specific element. If higher prices charges by R.L. Maynard, then

buying behaviour of people towards it will be declining where capability of construction firm for

generating income will be affected negatively. While operating in the cited industry, the

company charges different price level from people within specific period of time. Further, with

the help of price optimisation system, manager of cited firm able to decide one particular price at

where huge numbers of customers purchased products and services from it (Jansen, 2011).

Therefore, able to maintain and improve profit of the entire firm and market share as well in

construction sector of UK.

Stock management: In the business of R.L. Maynard it is necessary to manage stock available in

the business. The reason is that, when inventory is not managed as well as declined from the

company then create negative impact on sales revenue generation capacity up to a higher level.

This stated system is supportive for managing along with utilising inventory in proper and

optimum manner respectively. Once the available stock is utilised effectually then enhance

efficiency as well as productivity of the selected organisation. Further, it is essentially needed for

manage stock and boost up inventory turnover ratio at the end of accounting period (Inventory

lower at the workplace. To manage as well as reduce total expenses, it is necessary to know

overall cost incurred for constructing the buildings. With the help of this particular system of

MA, accountant of R.L. Maynard Limited able to determine costs associated with the business

for constructing the buildings as well as houses. Once this required data derived at the working

environment then management easily able to make pricing decisions in fruitful manner. Further,

it is basically needed for assessing costs which is occurred in production, administration and

selling the products (Baldvinsdottir, Mitchell and Nørreklit, 2010). Another requirement to

consider this system is that, R.L. Maynard able to identify costs by classifying in different parts

like fixed, variable and semi-variable. In addition to this, it consists of target, standard,

throughput, activity based costing etc. by which the manager able to take effectual level of

business decisions.

Price optimisation: Apart from the costs, pricing factor also has pivotal role at the workplace of

each organisation. The reason is that, attraction level of customers and profitability position of

business both depended on this specific element. If higher prices charges by R.L. Maynard, then

buying behaviour of people towards it will be declining where capability of construction firm for

generating income will be affected negatively. While operating in the cited industry, the

company charges different price level from people within specific period of time. Further, with

the help of price optimisation system, manager of cited firm able to decide one particular price at

where huge numbers of customers purchased products and services from it (Jansen, 2011).

Therefore, able to maintain and improve profit of the entire firm and market share as well in

construction sector of UK.

Stock management: In the business of R.L. Maynard it is necessary to manage stock available in

the business. The reason is that, when inventory is not managed as well as declined from the

company then create negative impact on sales revenue generation capacity up to a higher level.

This stated system is supportive for managing along with utilising inventory in proper and

optimum manner respectively. Once the available stock is utilised effectually then enhance

efficiency as well as productivity of the selected organisation. Further, it is essentially needed for

manage stock and boost up inventory turnover ratio at the end of accounting period (Inventory

Management, 2013). For performing valuation of stock basically three methods are considered

by R.L. Maynard which include LIFO, FIFO and weighted average.

Job costing: The company producing or constructing different kinds of products like houses,

offices, buildings, bungalows etc. Further, it is mandatory to determine that in which kind of

products how much level of costing is incurred. On the basis of thus, decisions for charging

prices are easily taken by manager of R.L. Maynard. In short, this system is considered by the

firm for calculating expenses associated with different goods constructed in each job. It is

beneficial to assess costs and take pricing decisions so that, huge customers will be attracting

towards it.

Conclusion

Hereby, it can be pertained that R.L. Maynard uses basically four aspects of management

accounting for making several internal business decisions. Cost accounting and price

optimisation systems are used to assess total cost of production and opt profitable or attractive

price of buildings respectively. Apart from this, stock management is supportive to boost up

inventory turnover ratio while job costing is undertaken for determining cost of products

produced under each job.

P2 Describing several methods which are taken into account for MA reporting at the workplace

of R.L. Maynard Limited

Introduction

A method under which small reports considering financial transactions are prepared and then

formulated final accounts at the end of fiscal period is known as MA reporting. Under the current

report of business presented to general manager of R.L. Maynard, method of this reporting are

described. Apart from this, importance of such reports is also discussed through the present

report.

Significance of management activity reports

Documents prepared related to management activity shows about the incomes as well as

expenses occurred within one year in the company. On the basis of this, company can determine

by R.L. Maynard which include LIFO, FIFO and weighted average.

Job costing: The company producing or constructing different kinds of products like houses,

offices, buildings, bungalows etc. Further, it is mandatory to determine that in which kind of

products how much level of costing is incurred. On the basis of thus, decisions for charging

prices are easily taken by manager of R.L. Maynard. In short, this system is considered by the

firm for calculating expenses associated with different goods constructed in each job. It is

beneficial to assess costs and take pricing decisions so that, huge customers will be attracting

towards it.

Conclusion

Hereby, it can be pertained that R.L. Maynard uses basically four aspects of management

accounting for making several internal business decisions. Cost accounting and price

optimisation systems are used to assess total cost of production and opt profitable or attractive

price of buildings respectively. Apart from this, stock management is supportive to boost up

inventory turnover ratio while job costing is undertaken for determining cost of products

produced under each job.

P2 Describing several methods which are taken into account for MA reporting at the workplace

of R.L. Maynard Limited

Introduction

A method under which small reports considering financial transactions are prepared and then

formulated final accounts at the end of fiscal period is known as MA reporting. Under the current

report of business presented to general manager of R.L. Maynard, method of this reporting are

described. Apart from this, importance of such reports is also discussed through the present

report.

Significance of management activity reports

Documents prepared related to management activity shows about the incomes as well as

expenses occurred within one year in the company. On the basis of this, company can determine

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

that firm able to generate revenue and profit up to which extent (Cooper, Ezzamel and Qu,

2017). Apart from this, such reports are important to make proper record of all the financial

transactions come into consideration within R.L. Maynard. So that, financial statements like I/S,

B/S, cash flows etc. will be formulated easily as well as appropriately.

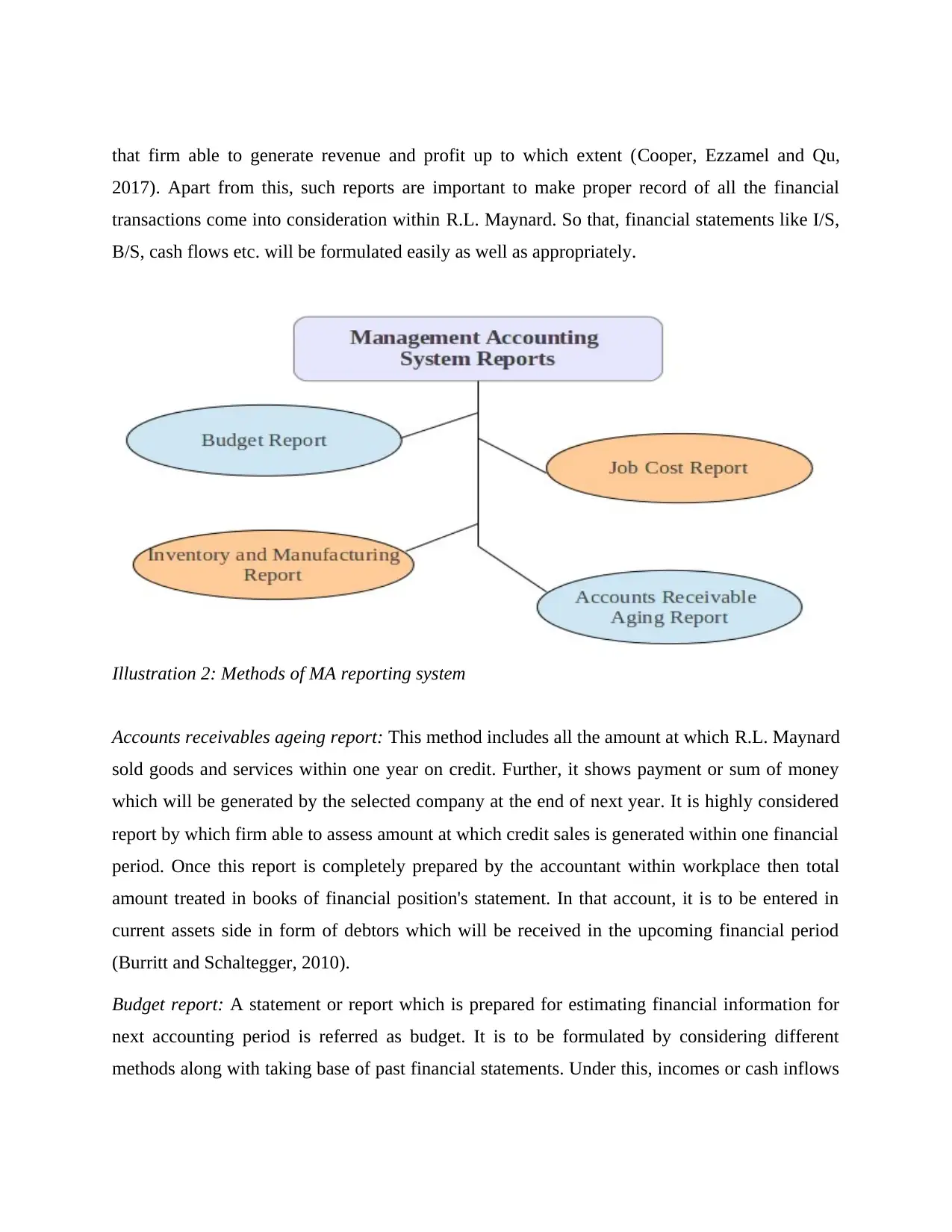

Illustration 2: Methods of MA reporting system

(Source: Otley and Emmanuel, 2013)

Accounts receivables ageing report: This method includes all the amount at which R.L. Maynard

sold goods and services within one year on credit. Further, it shows payment or sum of money

which will be generated by the selected company at the end of next year. It is highly considered

report by which firm able to assess amount at which credit sales is generated within one financial

period. Once this report is completely prepared by the accountant within workplace then total

amount treated in books of financial position's statement. In that account, it is to be entered in

current assets side in form of debtors which will be received in the upcoming financial period

(Burritt and Schaltegger, 2010).

Budget report: A statement or report which is prepared for estimating financial information for

next accounting period is referred as budget. It is to be formulated by considering different

methods along with taking base of past financial statements. Under this, incomes or cash inflows

2017). Apart from this, such reports are important to make proper record of all the financial

transactions come into consideration within R.L. Maynard. So that, financial statements like I/S,

B/S, cash flows etc. will be formulated easily as well as appropriately.

Illustration 2: Methods of MA reporting system

(Source: Otley and Emmanuel, 2013)

Accounts receivables ageing report: This method includes all the amount at which R.L. Maynard

sold goods and services within one year on credit. Further, it shows payment or sum of money

which will be generated by the selected company at the end of next year. It is highly considered

report by which firm able to assess amount at which credit sales is generated within one financial

period. Once this report is completely prepared by the accountant within workplace then total

amount treated in books of financial position's statement. In that account, it is to be entered in

current assets side in form of debtors which will be received in the upcoming financial period

(Burritt and Schaltegger, 2010).

Budget report: A statement or report which is prepared for estimating financial information for

next accounting period is referred as budget. It is to be formulated by considering different

methods along with taking base of past financial statements. Under this, incomes or cash inflows

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

as well as payments or cash outflows are estimated for upcoming year. So that, cash position is

to be determined in current accounting period where corrective actions and strategies are applied

in R.L. Maynard, if needed. This report or method is basically considered in order to assess

business performance and make targets of financials. At the end of next year, actual data

compared with budgeted which supports to assess performance.

Stock and manufacturing report: Another method is stock where information related to this

specific aspect are recorded in an effectual direction. This is helpful for accountant of R.L.

Maynard in order to know stock remained at the end of year. On the basis of this, decisions for

producing or constructing buildings are taken that how many goods are required to construct in

next year (Otley and Emmanuel, 2013). In addition to this, another report i.e. manufacturing

reflects, how much production is completed at the end of year and how much is needed to

construct in next period.

Job cost report: According to this method of MA reporting, costs as well as expenses incurred at

the time of producing products in each job are to be recorded. Along with this, transactions

related to incomes generated by goods sold of every job are also mentioned in this particular

report. On the basis of this, R.L. Maynard able to determine total expenditures come into

consideration for manufacturing such items. Therefore, easily able to determine that, which job

products are highly effective and help to generate huge profits. Under this report, if it has been

found that particular product incurring more costs as compared to incomes, then corrective

actions are to be taken into account (Van der Stede, 2011).

Conclusion

Considering to the above analysis it has been articulated that, R.L. Maynard implements

some important and key methods in order to complete process of MA reporting. It uses accounts

receivables ageing report which reflects amount of debtors which will be gained in next year.

Apart from this, stock, manufacturing, job cost as well as budget reports are also prepared by

accountant of the construction company

to be determined in current accounting period where corrective actions and strategies are applied

in R.L. Maynard, if needed. This report or method is basically considered in order to assess

business performance and make targets of financials. At the end of next year, actual data

compared with budgeted which supports to assess performance.

Stock and manufacturing report: Another method is stock where information related to this

specific aspect are recorded in an effectual direction. This is helpful for accountant of R.L.

Maynard in order to know stock remained at the end of year. On the basis of this, decisions for

producing or constructing buildings are taken that how many goods are required to construct in

next year (Otley and Emmanuel, 2013). In addition to this, another report i.e. manufacturing

reflects, how much production is completed at the end of year and how much is needed to

construct in next period.

Job cost report: According to this method of MA reporting, costs as well as expenses incurred at

the time of producing products in each job are to be recorded. Along with this, transactions

related to incomes generated by goods sold of every job are also mentioned in this particular

report. On the basis of this, R.L. Maynard able to determine total expenditures come into

consideration for manufacturing such items. Therefore, easily able to determine that, which job

products are highly effective and help to generate huge profits. Under this report, if it has been

found that particular product incurring more costs as compared to incomes, then corrective

actions are to be taken into account (Van der Stede, 2011).

Conclusion

Considering to the above analysis it has been articulated that, R.L. Maynard implements

some important and key methods in order to complete process of MA reporting. It uses accounts

receivables ageing report which reflects amount of debtors which will be gained in next year.

Apart from this, stock, manufacturing, job cost as well as budget reports are also prepared by

accountant of the construction company

TASK 2

P3 Preparation of income statement on the basis of marginal as well as absorption costing

An account which shows sales revenue as well as profit generated within one financial

year is referred as income statement. It is one of the widely considered method which gives clear

outline of profit situations. Further, to prepare this account R.L. Maynard considered two

methods i.e. marginal and absorption. Moreover, such statements are stated below:

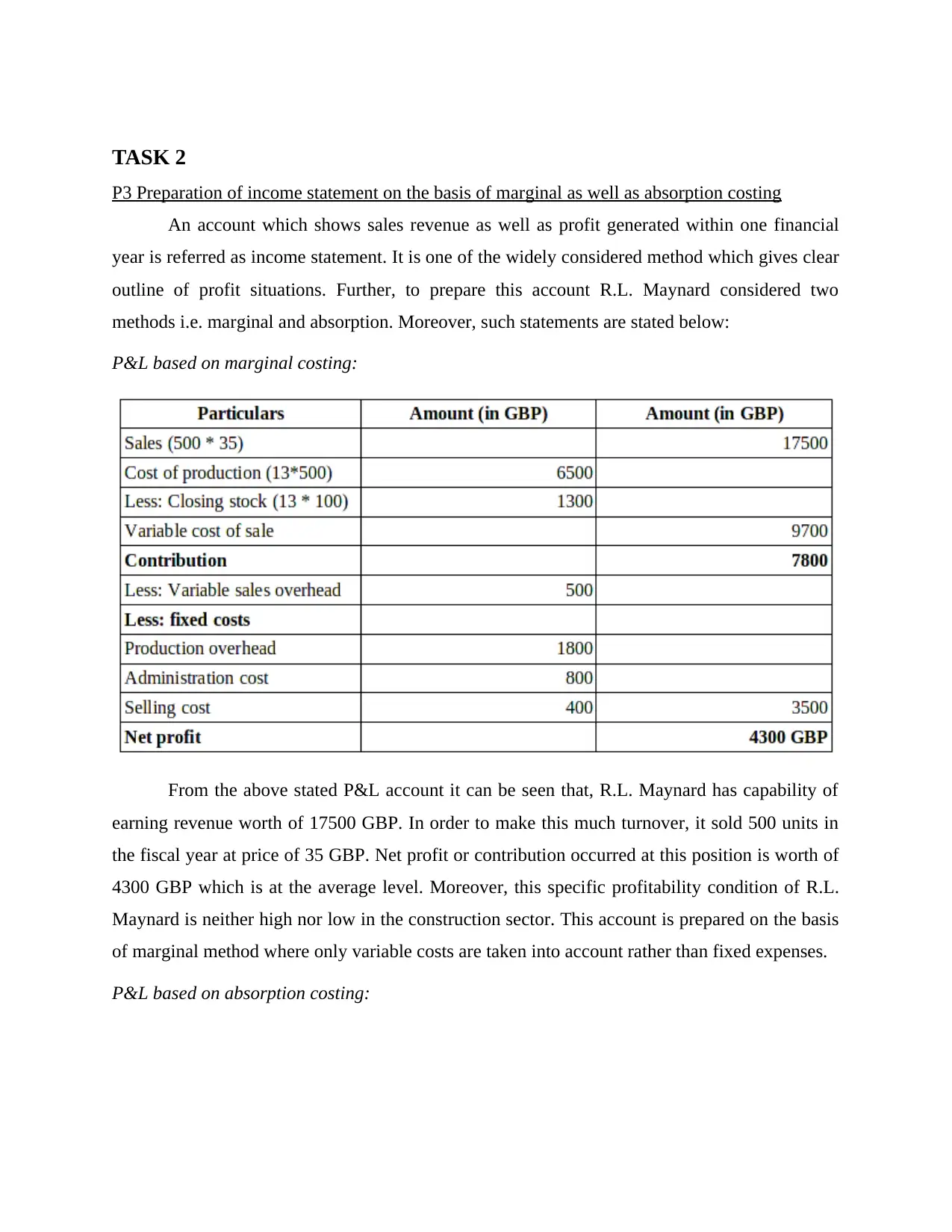

P&L based on marginal costing:

From the above stated P&L account it can be seen that, R.L. Maynard has capability of

earning revenue worth of 17500 GBP. In order to make this much turnover, it sold 500 units in

the fiscal year at price of 35 GBP. Net profit or contribution occurred at this position is worth of

4300 GBP which is at the average level. Moreover, this specific profitability condition of R.L.

Maynard is neither high nor low in the construction sector. This account is prepared on the basis

of marginal method where only variable costs are taken into account rather than fixed expenses.

P&L based on absorption costing:

P3 Preparation of income statement on the basis of marginal as well as absorption costing

An account which shows sales revenue as well as profit generated within one financial

year is referred as income statement. It is one of the widely considered method which gives clear

outline of profit situations. Further, to prepare this account R.L. Maynard considered two

methods i.e. marginal and absorption. Moreover, such statements are stated below:

P&L based on marginal costing:

From the above stated P&L account it can be seen that, R.L. Maynard has capability of

earning revenue worth of 17500 GBP. In order to make this much turnover, it sold 500 units in

the fiscal year at price of 35 GBP. Net profit or contribution occurred at this position is worth of

4300 GBP which is at the average level. Moreover, this specific profitability condition of R.L.

Maynard is neither high nor low in the construction sector. This account is prepared on the basis

of marginal method where only variable costs are taken into account rather than fixed expenses.

P&L based on absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

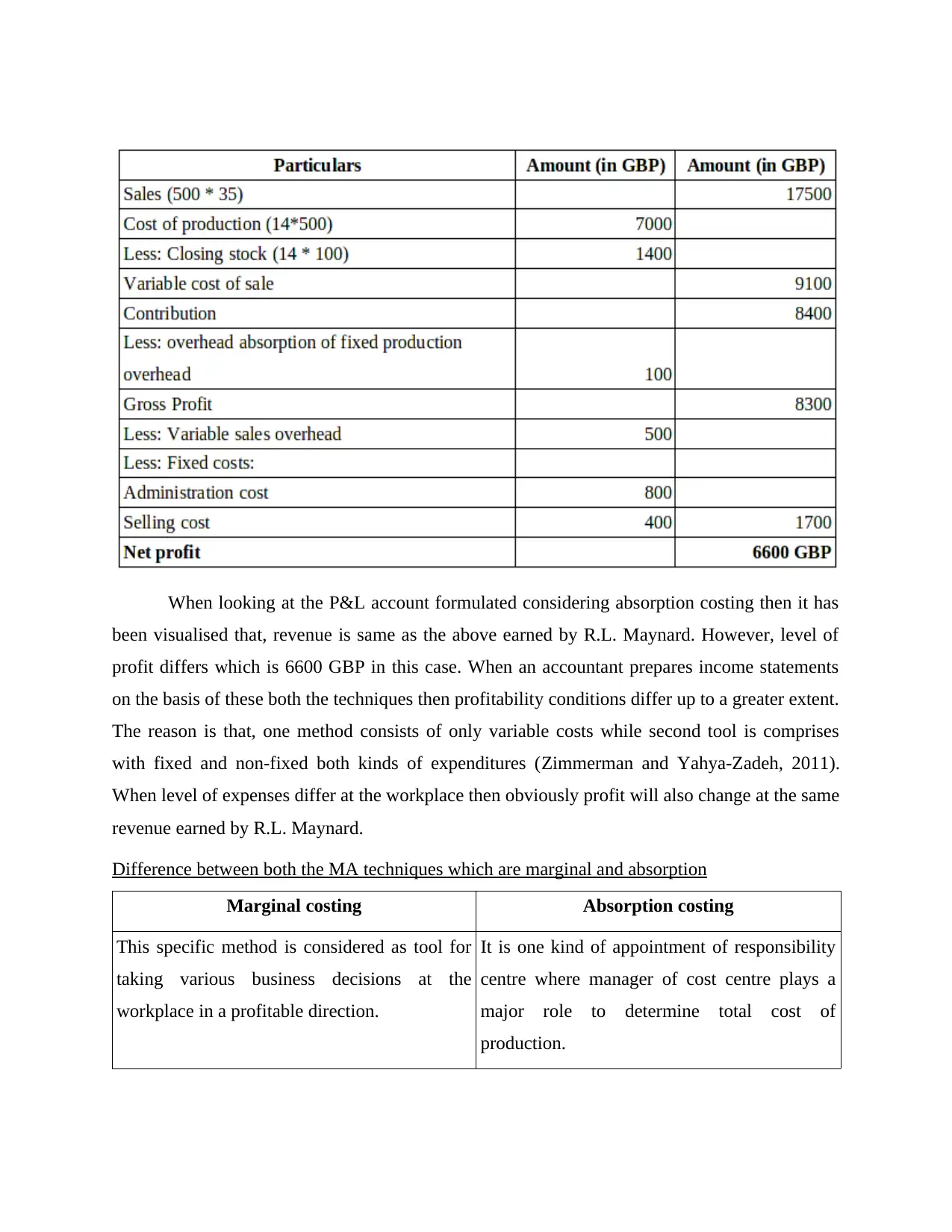

When looking at the P&L account formulated considering absorption costing then it has

been visualised that, revenue is same as the above earned by R.L. Maynard. However, level of

profit differs which is 6600 GBP in this case. When an accountant prepares income statements

on the basis of these both the techniques then profitability conditions differ up to a greater extent.

The reason is that, one method consists of only variable costs while second tool is comprises

with fixed and non-fixed both kinds of expenditures (Zimmerman and Yahya-Zadeh, 2011).

When level of expenses differ at the workplace then obviously profit will also change at the same

revenue earned by R.L. Maynard.

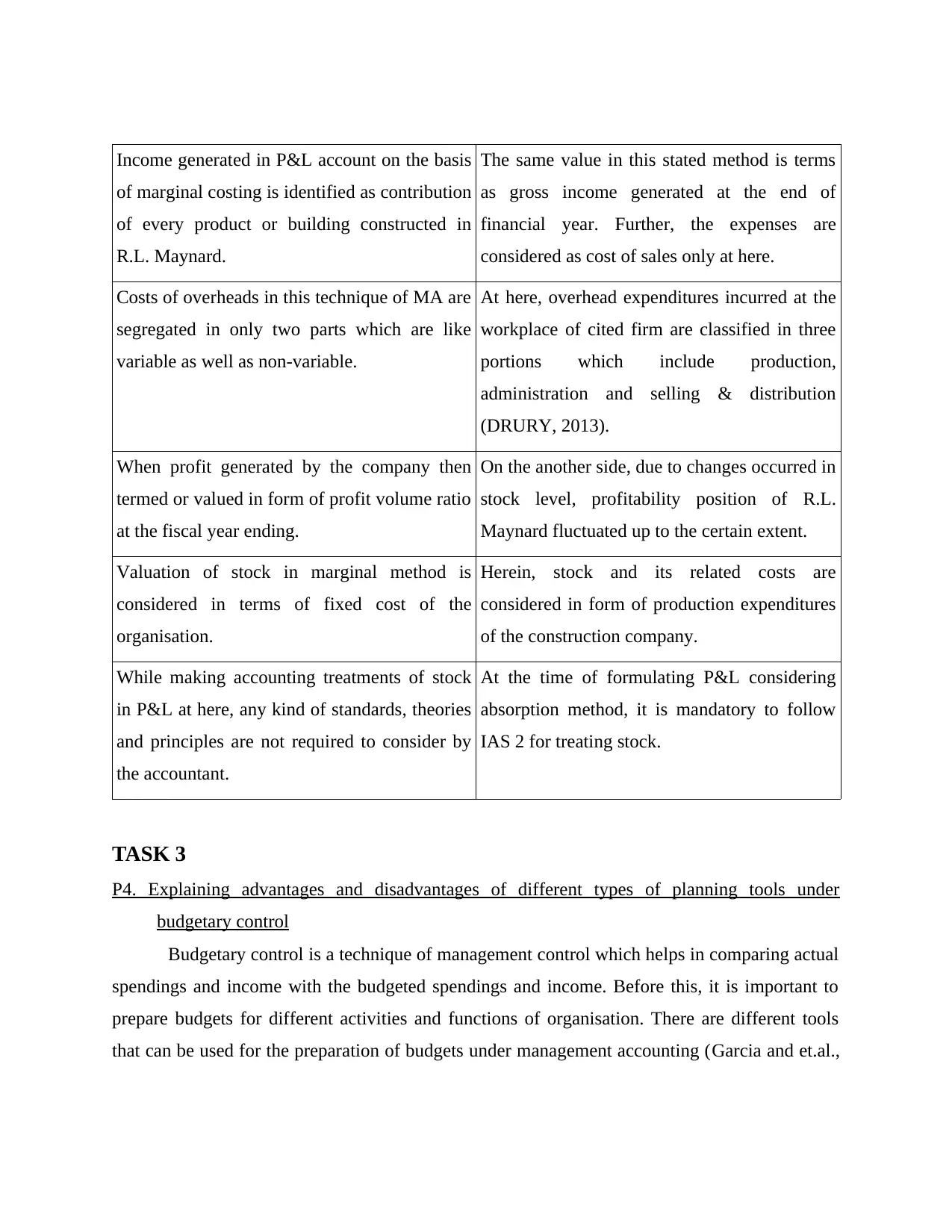

Difference between both the MA techniques which are marginal and absorption

Marginal costing Absorption costing

This specific method is considered as tool for

taking various business decisions at the

workplace in a profitable direction.

It is one kind of appointment of responsibility

centre where manager of cost centre plays a

major role to determine total cost of

production.

been visualised that, revenue is same as the above earned by R.L. Maynard. However, level of

profit differs which is 6600 GBP in this case. When an accountant prepares income statements

on the basis of these both the techniques then profitability conditions differ up to a greater extent.

The reason is that, one method consists of only variable costs while second tool is comprises

with fixed and non-fixed both kinds of expenditures (Zimmerman and Yahya-Zadeh, 2011).

When level of expenses differ at the workplace then obviously profit will also change at the same

revenue earned by R.L. Maynard.

Difference between both the MA techniques which are marginal and absorption

Marginal costing Absorption costing

This specific method is considered as tool for

taking various business decisions at the

workplace in a profitable direction.

It is one kind of appointment of responsibility

centre where manager of cost centre plays a

major role to determine total cost of

production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income generated in P&L account on the basis

of marginal costing is identified as contribution

of every product or building constructed in

R.L. Maynard.

The same value in this stated method is terms

as gross income generated at the end of

financial year. Further, the expenses are

considered as cost of sales only at here.

Costs of overheads in this technique of MA are

segregated in only two parts which are like

variable as well as non-variable.

At here, overhead expenditures incurred at the

workplace of cited firm are classified in three

portions which include production,

administration and selling & distribution

(DRURY, 2013).

When profit generated by the company then

termed or valued in form of profit volume ratio

at the fiscal year ending.

On the another side, due to changes occurred in

stock level, profitability position of R.L.

Maynard fluctuated up to the certain extent.

Valuation of stock in marginal method is

considered in terms of fixed cost of the

organisation.

Herein, stock and its related costs are

considered in form of production expenditures

of the construction company.

While making accounting treatments of stock

in P&L at here, any kind of standards, theories

and principles are not required to consider by

the accountant.

At the time of formulating P&L considering

absorption method, it is mandatory to follow

IAS 2 for treating stock.

TASK 3

P4. Explaining advantages and disadvantages of different types of planning tools under

budgetary control

Budgetary control is a technique of management control which helps in comparing actual

spendings and income with the budgeted spendings and income. Before this, it is important to

prepare budgets for different activities and functions of organisation. There are different tools

that can be used for the preparation of budgets under management accounting (Garcia and et.al.,

of marginal costing is identified as contribution

of every product or building constructed in

R.L. Maynard.

The same value in this stated method is terms

as gross income generated at the end of

financial year. Further, the expenses are

considered as cost of sales only at here.

Costs of overheads in this technique of MA are

segregated in only two parts which are like

variable as well as non-variable.

At here, overhead expenditures incurred at the

workplace of cited firm are classified in three

portions which include production,

administration and selling & distribution

(DRURY, 2013).

When profit generated by the company then

termed or valued in form of profit volume ratio

at the fiscal year ending.

On the another side, due to changes occurred in

stock level, profitability position of R.L.

Maynard fluctuated up to the certain extent.

Valuation of stock in marginal method is

considered in terms of fixed cost of the

organisation.

Herein, stock and its related costs are

considered in form of production expenditures

of the construction company.

While making accounting treatments of stock

in P&L at here, any kind of standards, theories

and principles are not required to consider by

the accountant.

At the time of formulating P&L considering

absorption method, it is mandatory to follow

IAS 2 for treating stock.

TASK 3

P4. Explaining advantages and disadvantages of different types of planning tools under

budgetary control

Budgetary control is a technique of management control which helps in comparing actual

spendings and income with the budgeted spendings and income. Before this, it is important to

prepare budgets for different activities and functions of organisation. There are different tools

that can be used for the preparation of budgets under management accounting (Garcia and et.al.,

2016). These tools helps in planning for future events which includes taking decision regarding

how many resources are to be allocated to various functions to achieve desired targets. R.L.

Maynard Limited can use following planning tools for the purpose of preparing budgets and

planning for future events:

Incremental Budgeting:

This is a traditional method of budget preparation. Under this method current years

budget are used for making budgets for next year by adding a certain percentage or increment in

order to arrive at new budget (Groot and Selto, 2013). It is the easiest method among all the

budgeting methods. For example, if the monthly budget of small business is $5000 and allowing

for inflation and other business expenses means there is a need to add another 5% to respective

budget and then new budget will be $5250. This method does not evaluate business activities

and just provide further resources to the existing ones whenever required.

Advantages:

It is a stable budget and changes under this are gradual.

Highly skilled professionals are not required to undertake the process of incremental budgeting

as this can be done by any employee with nominal knowledge of accounting.

The impact of change can be seen instantly just after providing incremented resources.

It is am economical method of budgeting as preparation costs are low (Hickman, 2016.).

Since all the departments have same amount of money to spend and which reduces employee

conflicts.

Disadvantages:

Using this method may not provide correct resources to departments as it cannot be said entirely

accurate method.

It is rigid in nature and does not allow changes whenever needed.

Incentives are not provided to employees for reducing cost and increasing profit and productivity

of organisation.

how many resources are to be allocated to various functions to achieve desired targets. R.L.

Maynard Limited can use following planning tools for the purpose of preparing budgets and

planning for future events:

Incremental Budgeting:

This is a traditional method of budget preparation. Under this method current years

budget are used for making budgets for next year by adding a certain percentage or increment in

order to arrive at new budget (Groot and Selto, 2013). It is the easiest method among all the

budgeting methods. For example, if the monthly budget of small business is $5000 and allowing

for inflation and other business expenses means there is a need to add another 5% to respective

budget and then new budget will be $5250. This method does not evaluate business activities

and just provide further resources to the existing ones whenever required.

Advantages:

It is a stable budget and changes under this are gradual.

Highly skilled professionals are not required to undertake the process of incremental budgeting

as this can be done by any employee with nominal knowledge of accounting.

The impact of change can be seen instantly just after providing incremented resources.

It is am economical method of budgeting as preparation costs are low (Hickman, 2016.).

Since all the departments have same amount of money to spend and which reduces employee

conflicts.

Disadvantages:

Using this method may not provide correct resources to departments as it cannot be said entirely

accurate method.

It is rigid in nature and does not allow changes whenever needed.

Incentives are not provided to employees for reducing cost and increasing profit and productivity

of organisation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.