Management Accounting Report: Oak Cash and Carry Case Study Analysis

VerifiedAdded on 2021/01/01

|14

|4557

|261

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within the retail sector, specifically using Oak Cash and Carry as a case study. It delves into the definition and importance of management accounting, contrasting it with financial accounting and highlighting various management accounting systems like cost accounting and price optimization. The report then explores different types of management accounting reports, such as performance and inventory management reports, and their significance in decision-making. A key section analyzes cost determination techniques, including marginal and absorption costing, with calculations and comparisons. Furthermore, the report examines various planning tools used for budgetary control, discussing their advantages and disadvantages. Finally, it includes a comparison of how different companies adapt their management accounting systems to address financial problems, offering valuable insights for students and professionals alike. The report concludes with a summary of the findings and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................4

TASK 1...........................................................................................................................................4

P1 Management accounting and requirement of its systems......................................................4

P2:Different types of management accounting reports...............................................................6

TASK 2............................................................................................................................................7

P3: Techniques used to analyse cost with marginal and absorption costs..................................7

TASK 3 .........................................................................................................................................11

P4. The advantages and disadvantages for different types of planning tools used for budgetary

control:......................................................................................................................................11

P5. Comparison on how companies are adapting management accounting systems to respond

to financial problems:................................................................................................................13

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION ..........................................................................................................................4

TASK 1...........................................................................................................................................4

P1 Management accounting and requirement of its systems......................................................4

P2:Different types of management accounting reports...............................................................6

TASK 2............................................................................................................................................7

P3: Techniques used to analyse cost with marginal and absorption costs..................................7

TASK 3 .........................................................................................................................................11

P4. The advantages and disadvantages for different types of planning tools used for budgetary

control:......................................................................................................................................11

P5. Comparison on how companies are adapting management accounting systems to respond

to financial problems:................................................................................................................13

CONCLUSION .............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting could be described as the process of identifying, analysing,

interpreting and communication of financial information and data that aids management to plan,

evaluate and handle a firm (Management accounting, 2018). It includes preparation of various

reports and accounts that assist managers in making short and long term financial decisions and

to present it to people inside as well as outside firm. The report is based on the case study of Oak

cash and carry that belongs to retail industry and provide offers wide variety of products to

retailers, local business, caterers, offices and other customers. The project will discuss the

concept of management accounting, its various systems and different reports that could be

prepared by firm. Further it includes cost determination by using various cost analysis

techniques. Moreover, various planning tools with their merits and demerits are to be discussed

to over come the financial problems that a firm faces. Lastly a comparison between two leading

companies will be provided.

TASK 1

P1 Management accounting and requirement of its systems

Definition of Management Accounting : According to National Association of

Accountants management accounting could be described as “analytical framework for

identifying,measuring, collecting, examining and presentation of financial information so as to

take appropriate decisions for ensuring optimum use of and accountability for its resources.”

Management accounting involves making use of various methods, techniques, planning tools and

systems that assist managers in formulating policies, plan and handling its varies operations

effectively (Carlsson-Wall, Kraus and Lind, 2015). By providing means to track down its

internal costs incurred on various processes it further acts a tool for taking authentic and relevant

decisions in regard to manufacturing, operations and business investments. Management

accounting in general mixed with financial accounting although both differs with each other in

mentioned below ways:

Difference between management accounting and financial accounting:

Basis of

comparison

Management accounting Financial accounting

Management accounting could be described as the process of identifying, analysing,

interpreting and communication of financial information and data that aids management to plan,

evaluate and handle a firm (Management accounting, 2018). It includes preparation of various

reports and accounts that assist managers in making short and long term financial decisions and

to present it to people inside as well as outside firm. The report is based on the case study of Oak

cash and carry that belongs to retail industry and provide offers wide variety of products to

retailers, local business, caterers, offices and other customers. The project will discuss the

concept of management accounting, its various systems and different reports that could be

prepared by firm. Further it includes cost determination by using various cost analysis

techniques. Moreover, various planning tools with their merits and demerits are to be discussed

to over come the financial problems that a firm faces. Lastly a comparison between two leading

companies will be provided.

TASK 1

P1 Management accounting and requirement of its systems

Definition of Management Accounting : According to National Association of

Accountants management accounting could be described as “analytical framework for

identifying,measuring, collecting, examining and presentation of financial information so as to

take appropriate decisions for ensuring optimum use of and accountability for its resources.”

Management accounting involves making use of various methods, techniques, planning tools and

systems that assist managers in formulating policies, plan and handling its varies operations

effectively (Carlsson-Wall, Kraus and Lind, 2015). By providing means to track down its

internal costs incurred on various processes it further acts a tool for taking authentic and relevant

decisions in regard to manufacturing, operations and business investments. Management

accounting in general mixed with financial accounting although both differs with each other in

mentioned below ways:

Difference between management accounting and financial accounting:

Basis of

comparison

Management accounting Financial accounting

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Meaning Management accounting provides

information and data that is been

utilized by the people within the

company such as managers for

decision making purpose. It is as this

accounting includes information

related to specific products, cost

centres etc.

Financial accounting majorly give

information that is primary used by

those from outside organization such as

stakeholders. It includes data and

statistics related to entire company and

its various operations.

Mandatory Management accounting is optional

to be implemented by any firm.

Financial management is obligatory by

law for every enterprise to applied in its

company as per set standards.

Thus for a small scale firm like Oak cash and carry it becomes critically important to

implement an effective management accounting that will aid company to monitor its transactions

related to various departments. Further implementation and integration of management

accounting with company will also assist managers to determine efficiency of costs of its various

business activities, budgets, financial performance and then accordingly allocate its limitedly

available resources in various segments comprising production, sales and investments.

Various Management Accounting Systems

Management accounting involves certain internal systems that enables an enterprise to

determine, measure and analyse effectiveness as well as efficacy of its various functions.

Mentioned below are various management accounting systems that are been consider by Oak

cash and carry :

Cost accounting System: It is also called as product costing system that involves

framework for ascertaining cost of goods for determining its profitability, product valuation and

administrating expenses (Granlund, 2011). It counts in one of the most prominent management

accounting system that when applied by Oak cash and carry will aid in track down those

products that are generating high profits for the company and ones that are not much in demand.

Besides, this it will enables managers of Oak cash and carry to compute value of its raw

materials, work in progress and finished goods. This, it make it easy for managers to prepare

authentic financial statements that helps top management in formulating realistic and effective

financial strategies. Thus, as company is related to retail sector this system will help managers to

information and data that is been

utilized by the people within the

company such as managers for

decision making purpose. It is as this

accounting includes information

related to specific products, cost

centres etc.

Financial accounting majorly give

information that is primary used by

those from outside organization such as

stakeholders. It includes data and

statistics related to entire company and

its various operations.

Mandatory Management accounting is optional

to be implemented by any firm.

Financial management is obligatory by

law for every enterprise to applied in its

company as per set standards.

Thus for a small scale firm like Oak cash and carry it becomes critically important to

implement an effective management accounting that will aid company to monitor its transactions

related to various departments. Further implementation and integration of management

accounting with company will also assist managers to determine efficiency of costs of its various

business activities, budgets, financial performance and then accordingly allocate its limitedly

available resources in various segments comprising production, sales and investments.

Various Management Accounting Systems

Management accounting involves certain internal systems that enables an enterprise to

determine, measure and analyse effectiveness as well as efficacy of its various functions.

Mentioned below are various management accounting systems that are been consider by Oak

cash and carry :

Cost accounting System: It is also called as product costing system that involves

framework for ascertaining cost of goods for determining its profitability, product valuation and

administrating expenses (Granlund, 2011). It counts in one of the most prominent management

accounting system that when applied by Oak cash and carry will aid in track down those

products that are generating high profits for the company and ones that are not much in demand.

Besides, this it will enables managers of Oak cash and carry to compute value of its raw

materials, work in progress and finished goods. This, it make it easy for managers to prepare

authentic financial statements that helps top management in formulating realistic and effective

financial strategies. Thus, as company is related to retail sector this system will help managers to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

monitor its fund flow that is been invested in its various departments and also to prepare budgets.

It includes two types of costs:

Direct Cost : It is associated with production and manufacturing of a specific good and

includes costs related to direct labour, direct raw materials, commissions, fright out expenses etc.

Standard Cost: It involves substituting an expected expense for the actual one in

accounts and then determining, recording the deviation between the two. It includes making cost

assumptions for a specific business operations within a firm.

Price optimisation System: This management accounting system is associated with

evaluating and calculation of product prices that are having high probability of generating best

outcome and to add on to profitability of company. This system not only focus on fixing prices

but also to attain those revenue and margin targets through high sales volumes. For Oak cash and

carry adoption of this system will help in implementing best pricing strategy for its products that

besides maximizing its profits will have no negative impact in the demand of its products by

customers.

Job Costing System : It is generally used as technique for a particular good or group of

products. For Oak cash and carry that manufactures various products that are different from one

other this forms to be one of the most effective system to be implemented (Johnson, 2013). This

system creates record of job cost for all products that are been manufactures and take into

consideration three types of costs i.e. direct labour, direct material and overhead expenses.

Therefore adoption and application of these system by Oak cash and carry into its

business management will reap various benefits for the firm including preparing reliable and

realistic forecasts related to its cash flows, sales etc. Further it will also help in gaining proper

understanding about its performance variances, to determine rate of return of a particular product

or project and to improve its decision making process regarding quality, quantity, product ,price

and so on.

P2:Different types of management accounting reports

Management accounting includes representation of accounting information that are

processed within a company and are presented in certain standardize or non standardize manner

in the form of reports. preparation of these financial reports forms critical part that provided the

actual picture of business performance during a specific time period. These reports in context to

Oak cash and carry could assist managers in taking short term decisions and those related to

It includes two types of costs:

Direct Cost : It is associated with production and manufacturing of a specific good and

includes costs related to direct labour, direct raw materials, commissions, fright out expenses etc.

Standard Cost: It involves substituting an expected expense for the actual one in

accounts and then determining, recording the deviation between the two. It includes making cost

assumptions for a specific business operations within a firm.

Price optimisation System: This management accounting system is associated with

evaluating and calculation of product prices that are having high probability of generating best

outcome and to add on to profitability of company. This system not only focus on fixing prices

but also to attain those revenue and margin targets through high sales volumes. For Oak cash and

carry adoption of this system will help in implementing best pricing strategy for its products that

besides maximizing its profits will have no negative impact in the demand of its products by

customers.

Job Costing System : It is generally used as technique for a particular good or group of

products. For Oak cash and carry that manufactures various products that are different from one

other this forms to be one of the most effective system to be implemented (Johnson, 2013). This

system creates record of job cost for all products that are been manufactures and take into

consideration three types of costs i.e. direct labour, direct material and overhead expenses.

Therefore adoption and application of these system by Oak cash and carry into its

business management will reap various benefits for the firm including preparing reliable and

realistic forecasts related to its cash flows, sales etc. Further it will also help in gaining proper

understanding about its performance variances, to determine rate of return of a particular product

or project and to improve its decision making process regarding quality, quantity, product ,price

and so on.

P2:Different types of management accounting reports

Management accounting includes representation of accounting information that are

processed within a company and are presented in certain standardize or non standardize manner

in the form of reports. preparation of these financial reports forms critical part that provided the

actual picture of business performance during a specific time period. These reports in context to

Oak cash and carry could assist managers in taking short term decisions and those related to

routine business operations. Further these reports could also assist in tracking down, calculating

and recording all expenses that are been incurred by firm in its process of production and in

ascertaining profits that are been generated out of sales. Mentioned below are some most

prominent reports that could aid managers of Oak cash and carry to determine its current

financial position for a particular time period.

Performance Report: This report includes a in depth analysis of performance of

employees against set benchmarks and a comparative study about the actual and expected level

of their performance (JOSHI and et. al., 2011). This is one of most elaborative financial

statement that measure and determines the actual output of a particular activity in reference to its

allotted budget within a specific time frame. For instance for Oak cash and carry theses reports

could be formulated in regard to employee annual performance, success report of a particular

product, project etc. Further manager could utilize its staff annual performance report to

ascertain their overall performance that can aid them in taking decisions regarding promotion,

training, transfers etc.

Inventory Management Report : This report includes information related with the

opening and closing stock of an organization. In context to Oak cash and carry these reports

could assist managers to review current status of their inventory, to ascertain reorder quantity

and time period etc. Further various techniques that Oak cash and carry could implement are just

in time, EOQ, turnover ratio etc. that could assist management to ascertain its actual profitability,

demand of its products, total turnovers etc.

Thus Oak cash and carry applies management accounting system that reveals out

important information regarding the financial position of firm, current status of its

investors,stakeholders, demand and sales records etc.

TASK 2

P3: Techniques used to analyse cost with marginal and absorption costs.

Cost : it could be described as the amount that is been paid by a firm to procurer its raw

materials, resources, utilities for production and final delivery of its finished products and

services (Klychova, Faskhutdinova and Sadrieva., 2014). Management accounting involves

computation of two types of cost that is generally incurred by a firm i.e. fixed cost and variable

cost. Fixed cost is the set amount that firm is liable to incurred even at zero production as it

and recording all expenses that are been incurred by firm in its process of production and in

ascertaining profits that are been generated out of sales. Mentioned below are some most

prominent reports that could aid managers of Oak cash and carry to determine its current

financial position for a particular time period.

Performance Report: This report includes a in depth analysis of performance of

employees against set benchmarks and a comparative study about the actual and expected level

of their performance (JOSHI and et. al., 2011). This is one of most elaborative financial

statement that measure and determines the actual output of a particular activity in reference to its

allotted budget within a specific time frame. For instance for Oak cash and carry theses reports

could be formulated in regard to employee annual performance, success report of a particular

product, project etc. Further manager could utilize its staff annual performance report to

ascertain their overall performance that can aid them in taking decisions regarding promotion,

training, transfers etc.

Inventory Management Report : This report includes information related with the

opening and closing stock of an organization. In context to Oak cash and carry these reports

could assist managers to review current status of their inventory, to ascertain reorder quantity

and time period etc. Further various techniques that Oak cash and carry could implement are just

in time, EOQ, turnover ratio etc. that could assist management to ascertain its actual profitability,

demand of its products, total turnovers etc.

Thus Oak cash and carry applies management accounting system that reveals out

important information regarding the financial position of firm, current status of its

investors,stakeholders, demand and sales records etc.

TASK 2

P3: Techniques used to analyse cost with marginal and absorption costs.

Cost : it could be described as the amount that is been paid by a firm to procurer its raw

materials, resources, utilities for production and final delivery of its finished products and

services (Klychova, Faskhutdinova and Sadrieva., 2014). Management accounting involves

computation of two types of cost that is generally incurred by a firm i.e. fixed cost and variable

cost. Fixed cost is the set amount that firm is liable to incurred even at zero production as it

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

includes expenses related to rent, electricity, salary of employees etc. Variable cost varies as per

the level of production. Marginal Cost: It is a variable cost that involves expenses related to material and

labour. It is cost incurred by Oak cash and carry in producing one extra unit of a product.

At initial level this cost seems to be quiet high for a Oak cash and carry as it involves

expense related to raw material, promotion, selling, administration etc.

Absorption Cost : Manufacturing costs which are engrossed by the production of quantity

are included in this cost. Absorption cost us covers the overall cost of finished goods.

Fixed cost and variable cost along with labour cost and direct material are included in

these costs. Oak Cash & Carry uses absorption cost when they recognise the company's

financial account for all its expenditures (Mistry, Sharma and Low, 2014). This

managerial accounting method is used to determine complete cost of production of

manufacturing goods. Relation of absorption cost and net income is negative. Whenever

absorption cost of Oak Cash & Carry would decrease, it would result in rising of its net

income and vice versa.

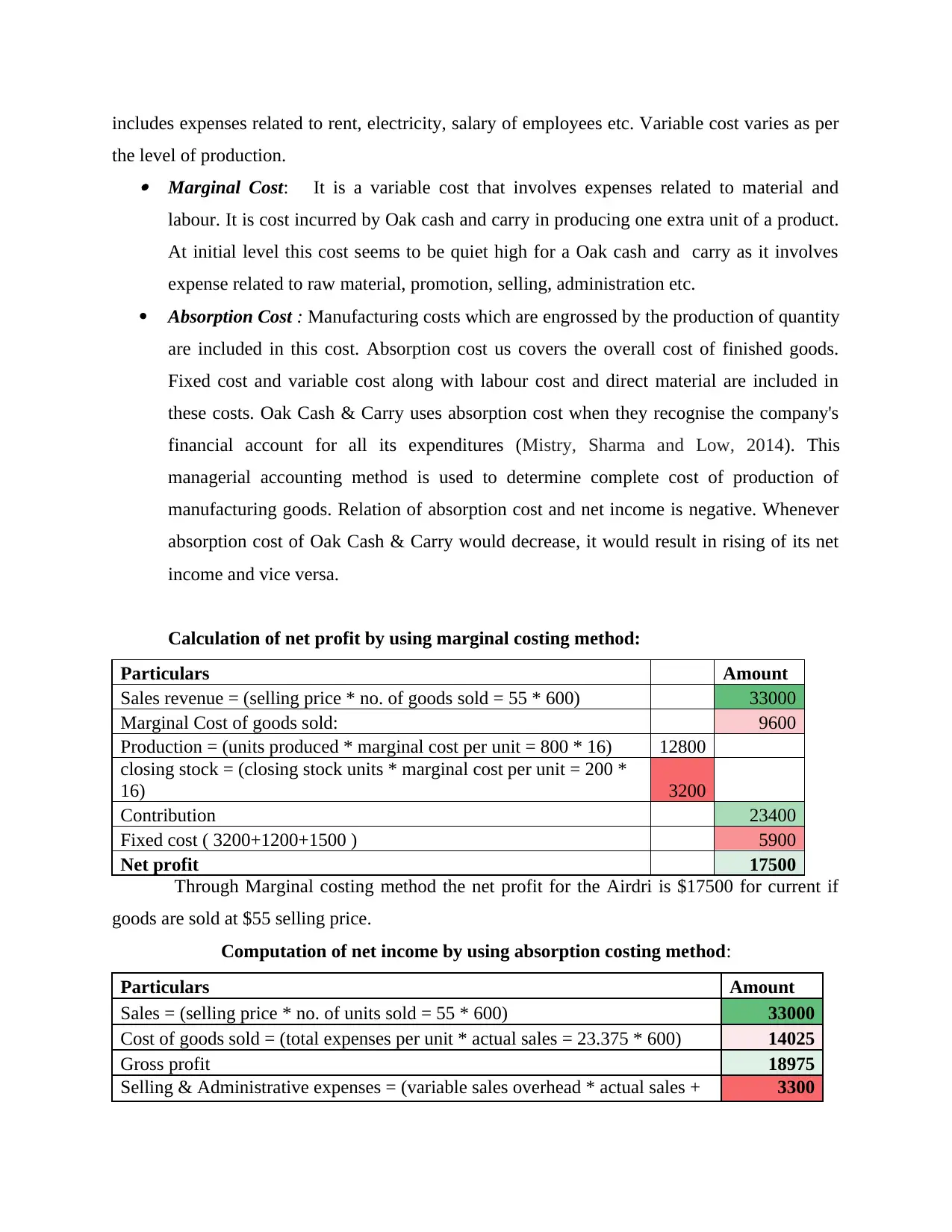

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Through Marginal costing method the net profit for the Airdri is $17500 for current if

goods are sold at $55 selling price.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales + 3300

the level of production. Marginal Cost: It is a variable cost that involves expenses related to material and

labour. It is cost incurred by Oak cash and carry in producing one extra unit of a product.

At initial level this cost seems to be quiet high for a Oak cash and carry as it involves

expense related to raw material, promotion, selling, administration etc.

Absorption Cost : Manufacturing costs which are engrossed by the production of quantity

are included in this cost. Absorption cost us covers the overall cost of finished goods.

Fixed cost and variable cost along with labour cost and direct material are included in

these costs. Oak Cash & Carry uses absorption cost when they recognise the company's

financial account for all its expenditures (Mistry, Sharma and Low, 2014). This

managerial accounting method is used to determine complete cost of production of

manufacturing goods. Relation of absorption cost and net income is negative. Whenever

absorption cost of Oak Cash & Carry would decrease, it would result in rising of its net

income and vice versa.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Through Marginal costing method the net profit for the Airdri is $17500 for current if

goods are sold at $55 selling price.

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales + 3300

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

selling and administrative cost = 1 * 600 + 2700)

Net profit/ operating income 15675

Management uses absorption costing method to calculate net profit and result is $15675

that is $1875 less than marginal costing method. So Manger of Airdri must adopt the marginal

costing to calculate their net profit.

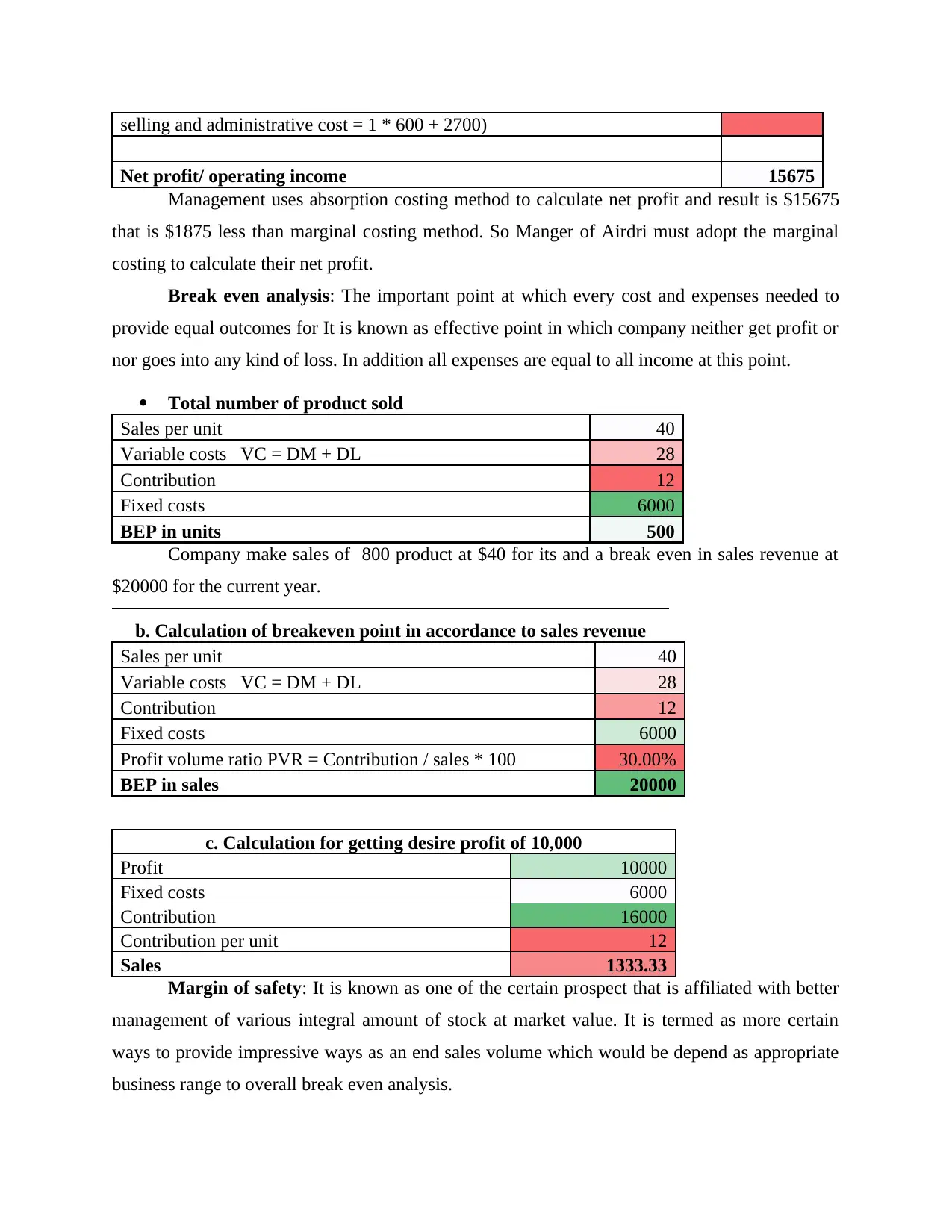

Break even analysis: The important point at which every cost and expenses needed to

provide equal outcomes for It is known as effective point in which company neither get profit or

nor goes into any kind of loss. In addition all expenses are equal to all income at this point.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Company make sales of 800 product at $40 for its and a break even in sales revenue at

$20000 for the current year.

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is known as one of the certain prospect that is affiliated with better

management of various integral amount of stock at market value. It is termed as more certain

ways to provide impressive ways as an end sales volume which would be depend as appropriate

business range to overall break even analysis.

Net profit/ operating income 15675

Management uses absorption costing method to calculate net profit and result is $15675

that is $1875 less than marginal costing method. So Manger of Airdri must adopt the marginal

costing to calculate their net profit.

Break even analysis: The important point at which every cost and expenses needed to

provide equal outcomes for It is known as effective point in which company neither get profit or

nor goes into any kind of loss. In addition all expenses are equal to all income at this point.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

Company make sales of 800 product at $40 for its and a break even in sales revenue at

$20000 for the current year.

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It is known as one of the certain prospect that is affiliated with better

management of various integral amount of stock at market value. It is termed as more certain

ways to provide impressive ways as an end sales volume which would be depend as appropriate

business range to overall break even analysis.

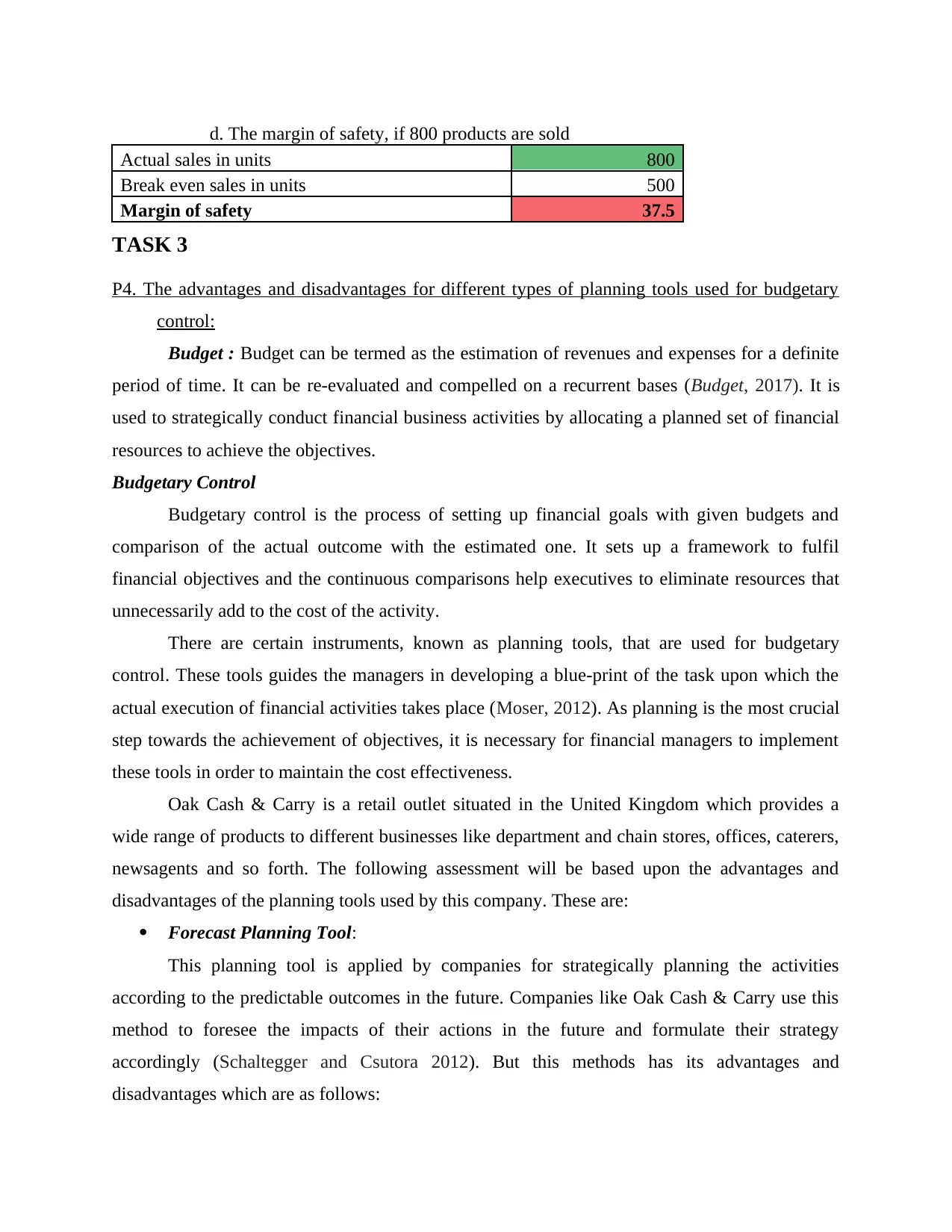

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

TASK 3

P4. The advantages and disadvantages for different types of planning tools used for budgetary

control:

Budget : Budget can be termed as the estimation of revenues and expenses for a definite

period of time. It can be re-evaluated and compelled on a recurrent bases (Budget, 2017). It is

used to strategically conduct financial business activities by allocating a planned set of financial

resources to achieve the objectives.

Budgetary Control

Budgetary control is the process of setting up financial goals with given budgets and

comparison of the actual outcome with the estimated one. It sets up a framework to fulfil

financial objectives and the continuous comparisons help executives to eliminate resources that

unnecessarily add to the cost of the activity.

There are certain instruments, known as planning tools, that are used for budgetary

control. These tools guides the managers in developing a blue-print of the task upon which the

actual execution of financial activities takes place (Moser, 2012). As planning is the most crucial

step towards the achievement of objectives, it is necessary for financial managers to implement

these tools in order to maintain the cost effectiveness.

Oak Cash & Carry is a retail outlet situated in the United Kingdom which provides a

wide range of products to different businesses like department and chain stores, offices, caterers,

newsagents and so forth. The following assessment will be based upon the advantages and

disadvantages of the planning tools used by this company. These are:

Forecast Planning Tool:

This planning tool is applied by companies for strategically planning the activities

according to the predictable outcomes in the future. Companies like Oak Cash & Carry use this

method to foresee the impacts of their actions in the future and formulate their strategy

accordingly (Schaltegger and Csutora 2012). But this methods has its advantages and

disadvantages which are as follows:

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

TASK 3

P4. The advantages and disadvantages for different types of planning tools used for budgetary

control:

Budget : Budget can be termed as the estimation of revenues and expenses for a definite

period of time. It can be re-evaluated and compelled on a recurrent bases (Budget, 2017). It is

used to strategically conduct financial business activities by allocating a planned set of financial

resources to achieve the objectives.

Budgetary Control

Budgetary control is the process of setting up financial goals with given budgets and

comparison of the actual outcome with the estimated one. It sets up a framework to fulfil

financial objectives and the continuous comparisons help executives to eliminate resources that

unnecessarily add to the cost of the activity.

There are certain instruments, known as planning tools, that are used for budgetary

control. These tools guides the managers in developing a blue-print of the task upon which the

actual execution of financial activities takes place (Moser, 2012). As planning is the most crucial

step towards the achievement of objectives, it is necessary for financial managers to implement

these tools in order to maintain the cost effectiveness.

Oak Cash & Carry is a retail outlet situated in the United Kingdom which provides a

wide range of products to different businesses like department and chain stores, offices, caterers,

newsagents and so forth. The following assessment will be based upon the advantages and

disadvantages of the planning tools used by this company. These are:

Forecast Planning Tool:

This planning tool is applied by companies for strategically planning the activities

according to the predictable outcomes in the future. Companies like Oak Cash & Carry use this

method to foresee the impacts of their actions in the future and formulate their strategy

accordingly (Schaltegger and Csutora 2012). But this methods has its advantages and

disadvantages which are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages:

Usually, companies depend on the data and the information they receive through their

analysis. Forecasting planning tool would help them predict the market conditions of the future,

how to gain competitive advantage from rising competition, how to innovate their resources to

better satisfy customer demands and how to expand their business activities.

Disadvantages:

This tool is qualitative in nature. Seeing this, this can be said that it is just not possible to

predict the future accurately. As business environment is dynamic, Oak Cash & Carry can face

any situation in future that they are unprepared for. Scenario Planning:

In this tool, the financial manager takes limited future outcomes into account and

accordingly work its strategy towards each outcome. This method is helpful where alternate

strategies are needed to developed to execute a single task. There are certain advantages as well

as disadvantages associated with it. These are

Advantages:

Since there are not many factors in this tool that are taken into account, managers of Oak

Carry & Cash can accurately predict the future outcomes and develop apt strategies for each

outcome (Ward, 2012). This tool serves best where a long range planning is needed if any

uncertain situation arise.

Disadvantages:

Using this tool can be time-consuming as a deep knowledge of various factors are

required to assess those and managers will not be able to use this where spontaneous decision-

making is required. Contingency Planning Tool:

Managers at Oak Cash & Carry use this tool to derive outcomes of situations not-likely to

arise during the usual planning, i.e., during contingency.

Advantages:

This tool is beneficial as it reassures the employees that the company considers their

safety as its priority.

Disadvantages:

However, this tool need modifications as the nature of contingencies changes overtime.

Usually, companies depend on the data and the information they receive through their

analysis. Forecasting planning tool would help them predict the market conditions of the future,

how to gain competitive advantage from rising competition, how to innovate their resources to

better satisfy customer demands and how to expand their business activities.

Disadvantages:

This tool is qualitative in nature. Seeing this, this can be said that it is just not possible to

predict the future accurately. As business environment is dynamic, Oak Cash & Carry can face

any situation in future that they are unprepared for. Scenario Planning:

In this tool, the financial manager takes limited future outcomes into account and

accordingly work its strategy towards each outcome. This method is helpful where alternate

strategies are needed to developed to execute a single task. There are certain advantages as well

as disadvantages associated with it. These are

Advantages:

Since there are not many factors in this tool that are taken into account, managers of Oak

Carry & Cash can accurately predict the future outcomes and develop apt strategies for each

outcome (Ward, 2012). This tool serves best where a long range planning is needed if any

uncertain situation arise.

Disadvantages:

Using this tool can be time-consuming as a deep knowledge of various factors are

required to assess those and managers will not be able to use this where spontaneous decision-

making is required. Contingency Planning Tool:

Managers at Oak Cash & Carry use this tool to derive outcomes of situations not-likely to

arise during the usual planning, i.e., during contingency.

Advantages:

This tool is beneficial as it reassures the employees that the company considers their

safety as its priority.

Disadvantages:

However, this tool need modifications as the nature of contingencies changes overtime.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

P5. Comparison on how companies are adapting management accounting systems to respond to

financial problems:

The financial aspect of any business is subject to various problems. Companies find it

difficult to deal with these issues as they hinder the financial goals and optimisation of financial

resources of the companies (Wickramasinghe and Alawattage, 2012). Oak Carry & Cash also

faced many financial problems in the recent past seeing the local country's scenario. But, there

are different management accounting systems that help a firm in responding to such financial

issues and in achieving its financial targets. These tools are: Financial Governance:

This system relates with how a company manages its financial information. It includes

how a company collects financial data, manages the performance and controls all the information

related to finance. These are important for a company like Oak Cash & Carry as it would help

the firm in developing to be financially strong internally. It would help reduce the material errors

and penalties of the firm, building its trust with the stakeholders. A good control on the financial

resources of a company assures the optimisation of company's financial resources. Oak Cash &

Carry can take steps towards ensuring a good financial governance in their firm, such as

It can develop or purchase software to record and manage all their financial data.

It can ensure a detailed summarisation of company's information which includes the data

from every part of the firm, historic as well as real-time

A system that gives detailed information on all the data processes required to finish

financial tasks.

Taking these steps, our firm can facilitate easy data processing which will make the task

time efficient.

Benchmarking:

This management accounting system is used to identify areas which are underperforming

by comparing their tasks with those of other departments (Windolph and Moelle, 2012). It may

or may not include the whole organisation at once and rather few departments. Benchmarking

can be done in two different ways, either it can be result-oriented, where comparisons are made

on the basis of end result achieved or, performance-oriented, where comparisons are made on the

P5. Comparison on how companies are adapting management accounting systems to respond to

financial problems:

The financial aspect of any business is subject to various problems. Companies find it

difficult to deal with these issues as they hinder the financial goals and optimisation of financial

resources of the companies (Wickramasinghe and Alawattage, 2012). Oak Carry & Cash also

faced many financial problems in the recent past seeing the local country's scenario. But, there

are different management accounting systems that help a firm in responding to such financial

issues and in achieving its financial targets. These tools are: Financial Governance:

This system relates with how a company manages its financial information. It includes

how a company collects financial data, manages the performance and controls all the information

related to finance. These are important for a company like Oak Cash & Carry as it would help

the firm in developing to be financially strong internally. It would help reduce the material errors

and penalties of the firm, building its trust with the stakeholders. A good control on the financial

resources of a company assures the optimisation of company's financial resources. Oak Cash &

Carry can take steps towards ensuring a good financial governance in their firm, such as

It can develop or purchase software to record and manage all their financial data.

It can ensure a detailed summarisation of company's information which includes the data

from every part of the firm, historic as well as real-time

A system that gives detailed information on all the data processes required to finish

financial tasks.

Taking these steps, our firm can facilitate easy data processing which will make the task

time efficient.

Benchmarking:

This management accounting system is used to identify areas which are underperforming

by comparing their tasks with those of other departments (Windolph and Moelle, 2012). It may

or may not include the whole organisation at once and rather few departments. Benchmarking

can be done in two different ways, either it can be result-oriented, where comparisons are made

on the basis of end result achieved or, performance-oriented, where comparisons are made on the

basis of the process by which the outcome was achieved. Oak Carry & Cash can use this system

to compare the performance of its various departments which in end, would help them focus on

areas that need attention. Also, benchmarking would help the companies maintain a close look at

the internal as well as external environment, that would help the company to ensure effective

performance.

Key Performance Indicator:

This system compares organisation's or it's employee's performance in a particular

objective. These are quantifiable aspects that companies use to determine their financial health

by applying various metrics. Oak Cash & Carry can introduce this system as it would give the

company a quantified outcome by which the company can compare its success rate. The

managers of the firm can set operational goals that can be measured in quantifiable terms, which

can link to the performance goals of the employee(Zainun, Tuanmat and Smith, 2011). Then the

managers can provide a process to achieve these operational goals. And once the employees

achieve the outcome, these results can be evaluated. This would help increase the productivity of

its employees as well as company can try innovative and cost effective ways to accomplish their

internal tasks.

Comparison between Oak Cash & Carry & A David & Co

OAK CASH & CARRY A DAVID & CO

1) The firm uses financial governance which is

considered as one of the best technique

which helps firm to increase its stakeholders

confidence along with reduction in

regulatory penalties and better decision-

making (Kuula, Putkiranta and Toivanen,

2012)

This company uses benchmarking tool which

is has a vast concept and is meant for

companies larger in size. This results in under

utilisation of this technique and poor

measurement of performance.

2) This company uses Key Performance

Indicators to compare performance of its

This company uses the tool to evaluate its

financial health and is yet to use it effectively

to compare the performance of its various departments which in end, would help them focus on

areas that need attention. Also, benchmarking would help the companies maintain a close look at

the internal as well as external environment, that would help the company to ensure effective

performance.

Key Performance Indicator:

This system compares organisation's or it's employee's performance in a particular

objective. These are quantifiable aspects that companies use to determine their financial health

by applying various metrics. Oak Cash & Carry can introduce this system as it would give the

company a quantified outcome by which the company can compare its success rate. The

managers of the firm can set operational goals that can be measured in quantifiable terms, which

can link to the performance goals of the employee(Zainun, Tuanmat and Smith, 2011). Then the

managers can provide a process to achieve these operational goals. And once the employees

achieve the outcome, these results can be evaluated. This would help increase the productivity of

its employees as well as company can try innovative and cost effective ways to accomplish their

internal tasks.

Comparison between Oak Cash & Carry & A David & Co

OAK CASH & CARRY A DAVID & CO

1) The firm uses financial governance which is

considered as one of the best technique

which helps firm to increase its stakeholders

confidence along with reduction in

regulatory penalties and better decision-

making (Kuula, Putkiranta and Toivanen,

2012)

This company uses benchmarking tool which

is has a vast concept and is meant for

companies larger in size. This results in under

utilisation of this technique and poor

measurement of performance.

2) This company uses Key Performance

Indicators to compare performance of its

This company uses the tool to evaluate its

financial health and is yet to use it effectively

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.