Management Accounting Report: Strategies for 4com plc Improvement

VerifiedAdded on 2020/06/05

|16

|5267

|109

Report

AI Summary

This report, prepared for 4com plc's General Manager by a Management Accounting Officer, explores the application of various management accounting tools to improve the company's operations. The introduction highlights the role of management accounting in collecting and utilizing financial and non-financial information for decision-making, emphasizing its importance for sustainable development and competitive advantage. The report delves into specific tools such as cost accounting systems, inventory management, and job costing, detailing their functions and advantages. It also examines different reporting systems, including performance, operational, job cost, inventory management, and accounts receivable reports, highlighting their significance in strategic planning and performance evaluation. The report emphasizes the importance of understanding both the advantages and limitations of these tools for effective implementation, and it concludes by reinforcing the importance of financial data and reporting in achieving organizational goals. The report also presents various costing methods like absorption costing and marginal costing, with a comparison between them.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

From: Management account officer.................................................................................................1

To: General Manager.......................................................................................................................1

Subject: For improving the management operations of the 4com plc. ...........................................1

INTRODUCTION...........................................................................................................................1

P1.................................................................................................................................................1

P2.................................................................................................................................................4

M1...............................................................................................................................................5

D1................................................................................................................................................5

P3.................................................................................................................................................5

M2...............................................................................................................................................7

D2................................................................................................................................................7

P4.................................................................................................................................................8

M3...............................................................................................................................................9

D3................................................................................................................................................9

P5...............................................................................................................................................10

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

From: Management account officer.................................................................................................1

To: General Manager.......................................................................................................................1

Subject: For improving the management operations of the 4com plc. ...........................................1

INTRODUCTION...........................................................................................................................1

P1.................................................................................................................................................1

P2.................................................................................................................................................4

M1...............................................................................................................................................5

D1................................................................................................................................................5

P3.................................................................................................................................................5

M2...............................................................................................................................................7

D2................................................................................................................................................7

P4.................................................................................................................................................8

M3...............................................................................................................................................9

D3................................................................................................................................................9

P5...............................................................................................................................................10

M4.............................................................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

From: Management account officer

To: General Manager

Subject: For improving the management operations of the 4com plc.

INTRODUCTION

Management accounting used by the managers of company to collect accounting

information and decisions are taken by them according to that. This helps the management of

company to improve the performance of company and control different functions. Management

accounting is the provision used by company for financial and non-financial decision making.

Management accounting is the main tool which is used by the firm in order to get sustainable

development. with the help of management accounting tools, 4com plc can processed their input

in an effective manner. Under this report, diverse management accounting tools, and their reports

are used in order gain the competitive advantages over the rivals (Management Accounting,

2017). Various budgetary tools are used under this and their uses for gaining firm’s pre-set

objectives. Although, various financial problems are addressed in an effective manner so that the

management can overcome these problems by applying various management accounting tools.

But, before going to implement MA tools, there is a need to know about their advantages and

limitations so that management account officer can take optimum benefits.

P1

Management accounting is the process which is used by each organization in order to

attain its pre-set targets. However, for applying such tools, each company needs to appoint

skilled staff so that they could implement in an organization. This will provides the different

types of data to the mangers of company so, they can manage the different departments and

employees of company according to that. This helps the managers of company to improve the

performance of different departments by use effective methods and strategies which helps in

optimum utilisation of given resources (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). This

helps the manger of company to make the budgets for different departments according to their

1

To: General Manager

Subject: For improving the management operations of the 4com plc.

INTRODUCTION

Management accounting used by the managers of company to collect accounting

information and decisions are taken by them according to that. This helps the management of

company to improve the performance of company and control different functions. Management

accounting is the provision used by company for financial and non-financial decision making.

Management accounting is the main tool which is used by the firm in order to get sustainable

development. with the help of management accounting tools, 4com plc can processed their input

in an effective manner. Under this report, diverse management accounting tools, and their reports

are used in order gain the competitive advantages over the rivals (Management Accounting,

2017). Various budgetary tools are used under this and their uses for gaining firm’s pre-set

objectives. Although, various financial problems are addressed in an effective manner so that the

management can overcome these problems by applying various management accounting tools.

But, before going to implement MA tools, there is a need to know about their advantages and

limitations so that management account officer can take optimum benefits.

P1

Management accounting is the process which is used by each organization in order to

attain its pre-set targets. However, for applying such tools, each company needs to appoint

skilled staff so that they could implement in an organization. This will provides the different

types of data to the mangers of company so, they can manage the different departments and

employees of company according to that. This helps the managers of company to improve the

performance of different departments by use effective methods and strategies which helps in

optimum utilisation of given resources (Jalaludin, Sulaiman and Nazli Nik Ahmad, 2011). This

helps the manger of company to make the budgets for different departments according to their

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

needs and provides the resource as per actual requirement. Management accounting is the

process of measuring, knowing, assessing and communicating finance related information in the

pursuit of the firm’s objectives. This is also known as the cost accounting.

The major difference between the management accounting and financial accounting is

that the information of MA is used in the firm for help managers in a firm so that they could take

decisions in an effective manner. While on the other hand, financial accounting information is

relevant to the diverse stakeholders who are directly or indirectly concerned to the firm’s

performance. The management accounting information helsp the manager and the top level

authority to regulate the expenditures and able to optimize the firm performance. The process of

making management accounting reports are that this offers to the firm accurate and timely

information to the external parties and also satiate the needs of manager. There are so many tools

of management accounting few of them are discussed as follows:

Cost accounting system: This is the system which is implemented by the firm to know

cost of its goods for stock valuation, profitability evaluation, and cost control. Under cost

accounting system, allocation of cost is executed either on the basis of ABC system or

traditional costing approach. This is the costing system which determines the cost as per

the pre-set costing methods. By using this method, company can lower the costs by

eliminating wastage of costs from the cost of production (Carenzo and Turolla, 2010).

This can be said that the company can attain the pre-set targets in an effective manner by

applying this technique. This system would separately assess and record the costs and

after assessing the costs compare inputs results to the actual outcomes to support

management of the firm. the managers are totally depends such costing data in common

and specific on cost as any task of the firm might be elaborated through its costs. This

2

process of measuring, knowing, assessing and communicating finance related information in the

pursuit of the firm’s objectives. This is also known as the cost accounting.

The major difference between the management accounting and financial accounting is

that the information of MA is used in the firm for help managers in a firm so that they could take

decisions in an effective manner. While on the other hand, financial accounting information is

relevant to the diverse stakeholders who are directly or indirectly concerned to the firm’s

performance. The management accounting information helsp the manager and the top level

authority to regulate the expenditures and able to optimize the firm performance. The process of

making management accounting reports are that this offers to the firm accurate and timely

information to the external parties and also satiate the needs of manager. There are so many tools

of management accounting few of them are discussed as follows:

Cost accounting system: This is the system which is implemented by the firm to know

cost of its goods for stock valuation, profitability evaluation, and cost control. Under cost

accounting system, allocation of cost is executed either on the basis of ABC system or

traditional costing approach. This is the costing system which determines the cost as per

the pre-set costing methods. By using this method, company can lower the costs by

eliminating wastage of costs from the cost of production (Carenzo and Turolla, 2010).

This can be said that the company can attain the pre-set targets in an effective manner by

applying this technique. This system would separately assess and record the costs and

after assessing the costs compare inputs results to the actual outcomes to support

management of the firm. the managers are totally depends such costing data in common

and specific on cost as any task of the firm might be elaborated through its costs. This

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system is observed that the management accounting offers the analytical tools such as

budgetary control, marginal costing, operational related costing, standard costing,

inventory control and others which are implemented by the management for discharging

their operations in an effective manner.

Inventory management: This is the inventory management tool which is used by the

firm specially by the manufacturing firms for controlling and overseeing the ordering, use

and storage of stocks which are going to be implemented for making the final outcome by

the firm. this system is used by the firm for effective application of inventory (Gates, and

Germain, 2010). Although, this can be said that the company needs to apply this so

effective within the firm so that the working capital can be used by the firm so

effectively. By implementing this, management of the cited firm could have effective

tracking of quantities throughout the stocking location, manager would have detailed and

be capable of forming effective inventory inventory decisions. As, this is rightly stated

that inventory is one of the crucial assets in the firm.

Job Costing system: This is one of the management accounting system which is used by

the firm for allocating production costs to the individual costs for the individual product

or batch of the goods. This is implemented if the products processed are diverse from

each other. This contains the practice of gathering data on the costs connected to a

specific product. The information could be required to be submit cost data to a consumer

within the costs could be refunded. In addition to this, these information are crucial for

assessing the adequacy of forecasting system of the company which must be capable of

quoting prices which enables for a reasonable income. Such information might likewise

be implemented to assigning inventorial costs to processed goods. This approach of

3

budgetary control, marginal costing, operational related costing, standard costing,

inventory control and others which are implemented by the management for discharging

their operations in an effective manner.

Inventory management: This is the inventory management tool which is used by the

firm specially by the manufacturing firms for controlling and overseeing the ordering, use

and storage of stocks which are going to be implemented for making the final outcome by

the firm. this system is used by the firm for effective application of inventory (Gates, and

Germain, 2010). Although, this can be said that the company needs to apply this so

effective within the firm so that the working capital can be used by the firm so

effectively. By implementing this, management of the cited firm could have effective

tracking of quantities throughout the stocking location, manager would have detailed and

be capable of forming effective inventory inventory decisions. As, this is rightly stated

that inventory is one of the crucial assets in the firm.

Job Costing system: This is one of the management accounting system which is used by

the firm for allocating production costs to the individual costs for the individual product

or batch of the goods. This is implemented if the products processed are diverse from

each other. This contains the practice of gathering data on the costs connected to a

specific product. The information could be required to be submit cost data to a consumer

within the costs could be refunded. In addition to this, these information are crucial for

assessing the adequacy of forecasting system of the company which must be capable of

quoting prices which enables for a reasonable income. Such information might likewise

be implemented to assigning inventorial costs to processed goods. This approach of

3

management accounting needs gathering of labour, direct materials and overheads

(Carenzo and Turolla, 2010).

P2

There are so many ways or methods which are used by the firm for enhancing the

profitability. However, this can be observed that the company needs a sound reporting system

that could records its each at every transaction done by the firm at that time. This is formed by

getting support direction from financial statements. With the help of this, company could use

effective available resources in an effective manner so that the business can get the maximum

advantages in an effective manner. The management of the 4com plc needs to make certain

decisions so that the management of the cited firm can effectively utilise their resources. With

the help of management accounting reports, firm can make strategies regarding to the

performance appraisal. The data gathered for the aim of making reports are collected from the

financial and the non-financial resources. After gathering the data, they are firstly assessed by

implementing adequate tools prior posting it to the books of accounts. This is essentially

required to do so as this overcomes the mistakes and frauds. Data is required to gathered from

diverse department which are working for the similar objectives (Nielsen, Mitchell and Nørreklit,

2015). For getting the more information, then the company's manager is required to have more

reports so that sustainable development can be done. The future investment is relied upon these

reporting system under which brand vale of the firm is totally relied. There are so many reporting

system which could be implemented by the firm. Few of them are as follow:

Performance reporting system: as per this reporting, this is essential

information about firm past and existing year performances are recorded. This can

be seen that by implementing diverse statements. This is crucial report as future

investment decisions are interpreted if performance of firm is sound enough in a

past few years.

Operational reporting: This is the kind of report which is used by the firm in the

manufacturing process (Bagautdinova, Kundakchyan and Malakhov, 2013).

However, this can be said that the company needs to identify actual costs occurred

by the firm at the time of period. This is mostly connected with inner reporting.

4

(Carenzo and Turolla, 2010).

P2

There are so many ways or methods which are used by the firm for enhancing the

profitability. However, this can be observed that the company needs a sound reporting system

that could records its each at every transaction done by the firm at that time. This is formed by

getting support direction from financial statements. With the help of this, company could use

effective available resources in an effective manner so that the business can get the maximum

advantages in an effective manner. The management of the 4com plc needs to make certain

decisions so that the management of the cited firm can effectively utilise their resources. With

the help of management accounting reports, firm can make strategies regarding to the

performance appraisal. The data gathered for the aim of making reports are collected from the

financial and the non-financial resources. After gathering the data, they are firstly assessed by

implementing adequate tools prior posting it to the books of accounts. This is essentially

required to do so as this overcomes the mistakes and frauds. Data is required to gathered from

diverse department which are working for the similar objectives (Nielsen, Mitchell and Nørreklit,

2015). For getting the more information, then the company's manager is required to have more

reports so that sustainable development can be done. The future investment is relied upon these

reporting system under which brand vale of the firm is totally relied. There are so many reporting

system which could be implemented by the firm. Few of them are as follow:

Performance reporting system: as per this reporting, this is essential

information about firm past and existing year performances are recorded. This can

be seen that by implementing diverse statements. This is crucial report as future

investment decisions are interpreted if performance of firm is sound enough in a

past few years.

Operational reporting: This is the kind of report which is used by the firm in the

manufacturing process (Bagautdinova, Kundakchyan and Malakhov, 2013).

However, this can be said that the company needs to identify actual costs occurred

by the firm at the time of period. This is mostly connected with inner reporting.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost reporting: Such reporting system covers of those costs that are charged

over the material, labour, and other manufacturing overheads. This is an efficient

tools which are used by the firm to track actual costs incurred on a particular jobs

and assess to critically, if these costs could be managed in a job activity.

Inventory management reporting: This is required to be known as an efficient

elements of supply chain which indicates flow of goods from producer to ultimate

consumer. With the help of inventory management system, company's manager

implement its resources in an effective manner so that the business can get its pre-

set objectives. This is concerned to the tracking of products, billing records,

supplier information and delivering data.

Account receivable report: This is known as list of non-paying consumers

invoice. With the help of this, manager could track their debtors and effectively

used their resources. This is the main tool which is used for gathering of due

amount.

M1

Management accounting tools have various advantages which are going to be applied by

the firm in order to assess the performance of the firm. This assist the firm's managers to gain the

positive outcomes by using the available resources (Jalaludin, Sulaiman and Nazli Nik Ahmad,

2011). For such aim, they are required to implement diverse management accounting tools which

would assist them to meet out their long term objectives. As these management accounting tools

helps the firm to maximise their profits in an effective manner.

D1

An effective outcome is achieved by implementing adequate financial data which could

assist the firm to plan their future targets. For such purpose, reporting is said to be the useful

tools under which firm's decisions is based. Financial reports are made by implementing

essential information which are based on the existing and previous year performance. This is

implemented by investors for making effective capital investment plans.

P3

Costing is the term use to evaluate aggregate sum of capital contributed on the generation

of merchandise and ventures. It is straightforwardly related with material, work and overheads

5

over the material, labour, and other manufacturing overheads. This is an efficient

tools which are used by the firm to track actual costs incurred on a particular jobs

and assess to critically, if these costs could be managed in a job activity.

Inventory management reporting: This is required to be known as an efficient

elements of supply chain which indicates flow of goods from producer to ultimate

consumer. With the help of inventory management system, company's manager

implement its resources in an effective manner so that the business can get its pre-

set objectives. This is concerned to the tracking of products, billing records,

supplier information and delivering data.

Account receivable report: This is known as list of non-paying consumers

invoice. With the help of this, manager could track their debtors and effectively

used their resources. This is the main tool which is used for gathering of due

amount.

M1

Management accounting tools have various advantages which are going to be applied by

the firm in order to assess the performance of the firm. This assist the firm's managers to gain the

positive outcomes by using the available resources (Jalaludin, Sulaiman and Nazli Nik Ahmad,

2011). For such aim, they are required to implement diverse management accounting tools which

would assist them to meet out their long term objectives. As these management accounting tools

helps the firm to maximise their profits in an effective manner.

D1

An effective outcome is achieved by implementing adequate financial data which could

assist the firm to plan their future targets. For such purpose, reporting is said to be the useful

tools under which firm's decisions is based. Financial reports are made by implementing

essential information which are based on the existing and previous year performance. This is

implemented by investors for making effective capital investment plans.

P3

Costing is the term use to evaluate aggregate sum of capital contributed on the generation

of merchandise and ventures. It is straightforwardly related with material, work and overheads

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

that are utilized while creation. It is for the most part known as monitory esteem that compress

with endeavours and assets use by chiefs so as to convey quality items to its clients ( Gates,

Nicolas and Walker, 2012). It comprises of variable costs that adjust with every unit create.

These are prompted as immediate cost. In monetary bookkeeping there are different costing

techniques are utilized as a part of request to acquire most extreme benefit and manage a

splendid future for the organization.

Absorption costing: Under this the whole the cost which are related to the production of

goods irrespective of fixed or variable costs. All the cost which are related to the manufacturing

of goods are covered under this. And this is presumes to be the most effective tool for calculating

the profits of the firm.

Marginal cost: the marginal cost is the tool which is used by the firm for ascertaining the

profits. However this can be said that under this costing tool, only variable cost is to be

considered for calculating the contribution of the firm. This is the most effective tool for

calculating the profits of the firm. Although, this can be seen that the company can attain the pre-

set targets by maximising the cost of the firm. There is a need to make certain

there are few of the differences. Which are mentioned as under:

Absorption costing Marginal costing

Fixed costs are also covered in the cost of

production of the product.

Assessment of fixed costs are measured via

period costs.

Cost data is reflected by implemented

conventional pattern. Net profit is measured

after reducing fixed costs from variable costs

(Bennett, Schaltegger and Zvezdov, 2011).

As per this method, contribution per units is

determined.

If there is any deviation in opening and closing

of stock which would impact the costs of

production.

If any deviation occurred in opening and

closing of inventory which does not impact the

units of production.

Costing overheads covers at the time of

calculation of absorption costs.

Expenses which are related to selling and

distribution are taken as critical part.

Calculation by using marginal costing

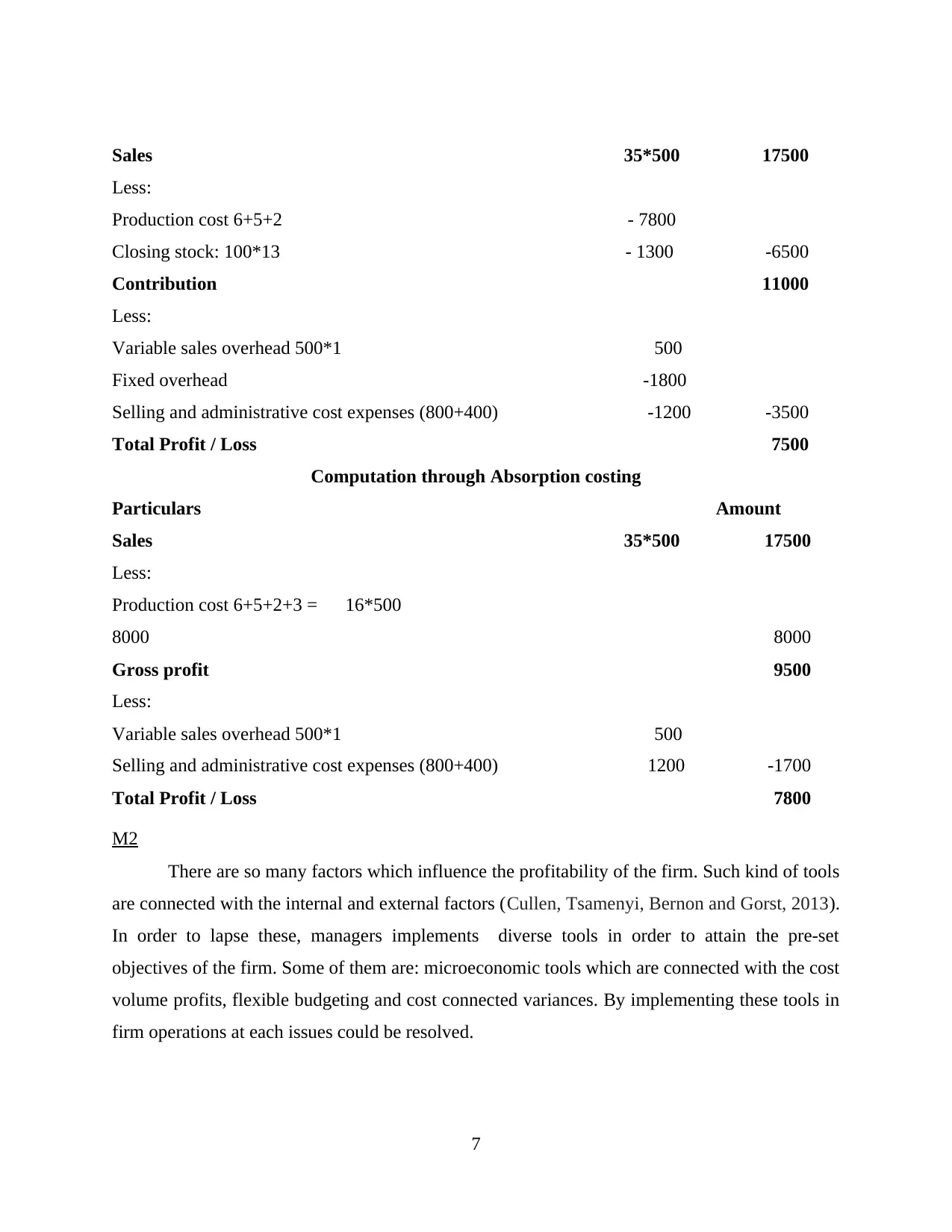

Particulars Amount

6

with endeavours and assets use by chiefs so as to convey quality items to its clients ( Gates,

Nicolas and Walker, 2012). It comprises of variable costs that adjust with every unit create.

These are prompted as immediate cost. In monetary bookkeeping there are different costing

techniques are utilized as a part of request to acquire most extreme benefit and manage a

splendid future for the organization.

Absorption costing: Under this the whole the cost which are related to the production of

goods irrespective of fixed or variable costs. All the cost which are related to the manufacturing

of goods are covered under this. And this is presumes to be the most effective tool for calculating

the profits of the firm.

Marginal cost: the marginal cost is the tool which is used by the firm for ascertaining the

profits. However this can be said that under this costing tool, only variable cost is to be

considered for calculating the contribution of the firm. This is the most effective tool for

calculating the profits of the firm. Although, this can be seen that the company can attain the pre-

set targets by maximising the cost of the firm. There is a need to make certain

there are few of the differences. Which are mentioned as under:

Absorption costing Marginal costing

Fixed costs are also covered in the cost of

production of the product.

Assessment of fixed costs are measured via

period costs.

Cost data is reflected by implemented

conventional pattern. Net profit is measured

after reducing fixed costs from variable costs

(Bennett, Schaltegger and Zvezdov, 2011).

As per this method, contribution per units is

determined.

If there is any deviation in opening and closing

of stock which would impact the costs of

production.

If any deviation occurred in opening and

closing of inventory which does not impact the

units of production.

Costing overheads covers at the time of

calculation of absorption costs.

Expenses which are related to selling and

distribution are taken as critical part.

Calculation by using marginal costing

Particulars Amount

6

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2

There are so many factors which influence the profitability of the firm. Such kind of tools

are connected with the internal and external factors (Cullen, Tsamenyi, Bernon and Gorst, 2013).

In order to lapse these, managers implements diverse tools in order to attain the pre-set

objectives of the firm. Some of them are: microeconomic tools which are connected with the cost

volume profits, flexible budgeting and cost connected variances. By implementing these tools in

firm operations at each issues could be resolved.

7

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2

There are so many factors which influence the profitability of the firm. Such kind of tools

are connected with the internal and external factors (Cullen, Tsamenyi, Bernon and Gorst, 2013).

In order to lapse these, managers implements diverse tools in order to attain the pre-set

objectives of the firm. Some of them are: microeconomic tools which are connected with the cost

volume profits, flexible budgeting and cost connected variances. By implementing these tools in

firm operations at each issues could be resolved.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D2

From the above-mentioned financial information is taken as on assumption basis. This is

required to identify net profits for the firm by implementing diverse costing tools. The cited firm

is having two major tools. Like- absorption and marginal costing. If they are implementing

absorption costing, then the profits will come to 7800. while on the other hand, by using

marginal costing, company earns 7500. which is less than the profits which is calculated by using

absorption costing.

P4

A budget is forecasting of revenue and expenses over a particular future period of time.

This is made and assessed on a periodic basis. Budgets can be formed for an individual, a family,

a group, a firm, a government, a nation, a multinational firm or just about anything else which

forms and spends amount. In a firm, a budget is the most powerful internal tool which is used by

the management and most probably not needed for reporting by the external parties.

Budget is a planned tool which is used by the firm in order to make certain tools and then

compare with this with the actual figures. The cited company needs to make certain tools which

are used in order to get the certain tools. Although, budgetary plans are made by the firm for a

specified period of time (Hansen, 2011). There are various types of budgets which are used by

the firm. Some of them are as follows:

Static budget: This is also known as the static budget which does not change and the

change in the production unit. This plays a crucial role in assisting firms track their finances,

assess their expenses, and determines manner to optimise the performance of the firm.

Advantages:

This can be likewise be supportable if firm continuously spend beyond the amount what

company earns. This is mandatorily supportable if firm's keep efforts with debt due to the past

financial crisis.

Disadvantage:

the main problem with this budget is that this does not account for life's uncertain events. While

on the other hand, this can be said that fixed bills like- mortgage or car payments are easy to

forecast, but variable costs can not forecasted. As a final outcome, exceeding the budget would

cause the problems for the firm. This is not an exact way to track expenses.

8

From the above-mentioned financial information is taken as on assumption basis. This is

required to identify net profits for the firm by implementing diverse costing tools. The cited firm

is having two major tools. Like- absorption and marginal costing. If they are implementing

absorption costing, then the profits will come to 7800. while on the other hand, by using

marginal costing, company earns 7500. which is less than the profits which is calculated by using

absorption costing.

P4

A budget is forecasting of revenue and expenses over a particular future period of time.

This is made and assessed on a periodic basis. Budgets can be formed for an individual, a family,

a group, a firm, a government, a nation, a multinational firm or just about anything else which

forms and spends amount. In a firm, a budget is the most powerful internal tool which is used by

the management and most probably not needed for reporting by the external parties.

Budget is a planned tool which is used by the firm in order to make certain tools and then

compare with this with the actual figures. The cited company needs to make certain tools which

are used in order to get the certain tools. Although, budgetary plans are made by the firm for a

specified period of time (Hansen, 2011). There are various types of budgets which are used by

the firm. Some of them are as follows:

Static budget: This is also known as the static budget which does not change and the

change in the production unit. This plays a crucial role in assisting firms track their finances,

assess their expenses, and determines manner to optimise the performance of the firm.

Advantages:

This can be likewise be supportable if firm continuously spend beyond the amount what

company earns. This is mandatorily supportable if firm's keep efforts with debt due to the past

financial crisis.

Disadvantage:

the main problem with this budget is that this does not account for life's uncertain events. While

on the other hand, this can be said that fixed bills like- mortgage or car payments are easy to

forecast, but variable costs can not forecasted. As a final outcome, exceeding the budget would

cause the problems for the firm. This is not an exact way to track expenses.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Sales budget: this is the budget which forecasts the sales for the forthcoming year of the

firm. With the help of this, the company can try to optimise the sales and also provides the

managers a clue about the sales related strategies. However, the company needs to make certain

tools which are used by the manager for getting the certain sustainable development.

Advantages:

The sales budget helps the firm to make strategies related to the sales expenditures and also

trying to limit these by way of implementing this in an effective manner (Chiwamit, Modell and

Yang, 2014). However, this can be said that the company needs to make certain gain which are

useful for the firm to attain their pre-set targets. The mangers with the help of sales budget, can

find out the variances which occurs in the firm and tries to eliminate them effectively. There are

certain tools which are used by the firm so that the company can get the advantages in an

effective..

Disadvantage:

Sales budget does not always renders an accurate benefits for the firm. However, this can be seen

that the sales budget is rigid and does not change as per the change in the production. This would

make the firm to limit its performance.

Operational budget:

This is the budget which is related to the firm's operations. However, all the expenses and

income which are related to the firm's operations for a particular period of time, are covered into

this. This is the forecasting of firm's operations related expenses and earnings for a certain period

of time (.Setthasakko, 2010).

Advantage:

This is the planning tool which is used by the firm in order to achieve its pre-set targets.

However, this can be observed that the operational budget helps the firm to optimise their

revenues and limits the costs so that the competitive advantage over the firm could get.

Disadvantage:

There are certain tools that can be used by the firm which will not reflects the true image. Hence,

firm cannot get the competitive advantage and also make wrong strategies that could lead to

spoil the performance of the firm.

9

firm. With the help of this, the company can try to optimise the sales and also provides the

managers a clue about the sales related strategies. However, the company needs to make certain

tools which are used by the manager for getting the certain sustainable development.

Advantages:

The sales budget helps the firm to make strategies related to the sales expenditures and also

trying to limit these by way of implementing this in an effective manner (Chiwamit, Modell and

Yang, 2014). However, this can be said that the company needs to make certain gain which are

useful for the firm to attain their pre-set targets. The mangers with the help of sales budget, can

find out the variances which occurs in the firm and tries to eliminate them effectively. There are

certain tools which are used by the firm so that the company can get the advantages in an

effective..

Disadvantage:

Sales budget does not always renders an accurate benefits for the firm. However, this can be seen

that the sales budget is rigid and does not change as per the change in the production. This would

make the firm to limit its performance.

Operational budget:

This is the budget which is related to the firm's operations. However, all the expenses and

income which are related to the firm's operations for a particular period of time, are covered into

this. This is the forecasting of firm's operations related expenses and earnings for a certain period

of time (.Setthasakko, 2010).

Advantage:

This is the planning tool which is used by the firm in order to achieve its pre-set targets.

However, this can be observed that the operational budget helps the firm to optimise their

revenues and limits the costs so that the competitive advantage over the firm could get.

Disadvantage:

There are certain tools that can be used by the firm which will not reflects the true image. Hence,

firm cannot get the competitive advantage and also make wrong strategies that could lead to

spoil the performance of the firm.

9

M3

From this report, this has been analysed that the company needs to adopt diverse planning

tools so that it can attain its pre-set objectives. However, this is the most important tool for

gaining the sustainable development. With the help of diverse planning tools, firm’s are assessed

by forecasting budget in an effective manner.

D3

With the help of planning tools, firm could resolve the financial related problems in an

effective manner. This can also be said about these above mentioned planning tools are useable

in order to solve the financial problems so that the 4com plc could get sustainable development.

P5

In a firm, this is observed that profitability could enhanced by implementing an adequate

tools and techniques. There are certain tools which can be used by the firm in order to enhance

the profitability of the firm (Hoque, 2011). Although, earnings could be influenced by financial

issues. There are some of the examples which have been quoted that are: lack of cash availability

in order to meet out the short term debts. The financial distress is required to be resolved by the

management accounting officer before the business operations started so that the firm

performance can-not be affected. This is rightly stated that such kind of issues arises due to not

properly utilizing of available resources which creates a vast impacts over the firm performance

of the firm. Henceforth, this is the great responsibility of both managers and firms to overcome

the financial constraints as soon as possible. There are so many tools which can be used by the

firm in order to assist the firm for maximising the performance. Few of them are as follow:

Key performance indicators: This is known as the solid tool which is used by the firm

in order to assess the employee and firm performance at the time of past few years. This

can be said that the company can resolve these financial distress by using key

performance indicators and also providers essential indicators by which firm can attain its

pre-set targets. However, this is the business metrics which is applied by the corporate

executives and other managers to know and assess the factors which are most imperative

to the success of the firm (Tucker and Parker, 2014). A sound KPI's is intended on the

firm's processes and functions which top level authorities overviews as the most crucial

for assessing the progress towards attain the strategic targets and performance goals.

10

From this report, this has been analysed that the company needs to adopt diverse planning

tools so that it can attain its pre-set objectives. However, this is the most important tool for

gaining the sustainable development. With the help of diverse planning tools, firm’s are assessed

by forecasting budget in an effective manner.

D3

With the help of planning tools, firm could resolve the financial related problems in an

effective manner. This can also be said about these above mentioned planning tools are useable

in order to solve the financial problems so that the 4com plc could get sustainable development.

P5

In a firm, this is observed that profitability could enhanced by implementing an adequate

tools and techniques. There are certain tools which can be used by the firm in order to enhance

the profitability of the firm (Hoque, 2011). Although, earnings could be influenced by financial

issues. There are some of the examples which have been quoted that are: lack of cash availability

in order to meet out the short term debts. The financial distress is required to be resolved by the

management accounting officer before the business operations started so that the firm

performance can-not be affected. This is rightly stated that such kind of issues arises due to not

properly utilizing of available resources which creates a vast impacts over the firm performance

of the firm. Henceforth, this is the great responsibility of both managers and firms to overcome

the financial constraints as soon as possible. There are so many tools which can be used by the

firm in order to assist the firm for maximising the performance. Few of them are as follow:

Key performance indicators: This is known as the solid tool which is used by the firm

in order to assess the employee and firm performance at the time of past few years. This

can be said that the company can resolve these financial distress by using key

performance indicators and also providers essential indicators by which firm can attain its

pre-set targets. However, this is the business metrics which is applied by the corporate

executives and other managers to know and assess the factors which are most imperative

to the success of the firm (Tucker and Parker, 2014). A sound KPI's is intended on the

firm's processes and functions which top level authorities overviews as the most crucial

for assessing the progress towards attain the strategic targets and performance goals.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.