Management Accounting Report: Stubbing Group Analysis and Strategies

VerifiedAdded on 2021/01/01

|16

|5107

|155

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on the application of these principles within the Stubbing Group, a retail sector company. The report delves into the essential requirements of management accounting systems, including MIS, cost accounting, inventory management, and price optimization. It explores various methods used for management accounting reporting, such as accounts receivable, cash flow, financial, job cost, performance, sales, and stock management reports. The report further examines the effectiveness of different management accounting systems and their integration with management accounting reporting, emphasizing the importance of accurate financial data for effective business strategies. Cost analysis techniques, including marginal costing, are applied to prepare an income statement. The report also discusses the advantages and disadvantages of different planning tools for budgetary control and evaluates how management accounting helps organizations respond to financial problems. The report concludes with an overview of how organizations adapt their management accounting systems to meet evolving business needs.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and the essential requirements of types of MA systems................1

P2 Various methods used for management accounting reporting...............................................3

M1 effectiveness of management accounting systems and their application in organisation.....5

D1 integration of management accounting system and management accounting reporting.......5

TASK 2............................................................................................................................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement.....................................................................................................................................5

M2 Apply of range of cost accounting techniques and produce financial reports......................8

D2 financial reports which are accurately applied and interpret data for a range of business....8

TASK 3 ...........................................................................................................................................8

P4 The advantages and disadvantages of different type of planning tools used for budgetary

control.........................................................................................................................................8

M3 Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................10

D3 Planning tools for accounting respond financial problems to lead association...................10

TASK 4..........................................................................................................................................10

P5 Ways in which organisations are adapting management accounting system.......................10

M4 Evaluate how management accounting helps to respond financial problems....................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting and the essential requirements of types of MA systems................1

P2 Various methods used for management accounting reporting...............................................3

M1 effectiveness of management accounting systems and their application in organisation.....5

D1 integration of management accounting system and management accounting reporting.......5

TASK 2............................................................................................................................................5

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income

statement.....................................................................................................................................5

M2 Apply of range of cost accounting techniques and produce financial reports......................8

D2 financial reports which are accurately applied and interpret data for a range of business....8

TASK 3 ...........................................................................................................................................8

P4 The advantages and disadvantages of different type of planning tools used for budgetary

control.........................................................................................................................................8

M3 Use of different planning tools and their application for preparing and forecasting budgets

...................................................................................................................................................10

D3 Planning tools for accounting respond financial problems to lead association...................10

TASK 4..........................................................................................................................................10

P5 Ways in which organisations are adapting management accounting system.......................10

M4 Evaluate how management accounting helps to respond financial problems....................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a terminology of managing records, information and

accounting reports are considered in this context. The process of preparing management reports

and maintaining records which provides a clear information regarding the performance of

organisation to managers are considered in management accounting (Bradbard, Alvis and

Morris,2014). Financial information, departmental information, statistical information which

remain essential in terms of determining the performance of organisations are included in

management accounting.

This report is prepared to defined the meaning of management accounting, and

management accounting systems are defined in this context. various methods used for

management accounting reporting are illustrated in this context. Techniques are used subject to

measure the profitability of organisation defined in this context. This is one of the essential

aspect in terms of analysing the profitability and managing the operations of association. Use of

budgetary control and role of planning tools to assist budgetary control process defined in this

context. Ways are compared in terms of adapting the management accounting system with in

organisation are defined in this context. Stubbing group of retail sector is chosen organisation

under which management accounting is illustrated.

TASK 1

P1 Management accounting and the essential requirements of types of MA systems

Management accounting

Management accounting provides a structure to use of type of information and data

related to analyse the day to day transactions and records for better management and control with

in business. It allows managers to evaluate 360 dimensions of business from lower level to upper

level. Different perspective and assumptions are made in terms of managing the operations and

functions of business. Anthers and writers have their own perspective in terms of management

accounting. Management accounting is not only a tool used for effective management and

control but also it is a process of nourishing the organisation's functions and management

operations in more significant manner (Bruynseels and Cardinaels, 2013).

As per IMA (Institute of Management Accounts) “management accounting is a

profession that involves partnering in managerial decisions making, addressing plans,

1

Management accounting is a terminology of managing records, information and

accounting reports are considered in this context. The process of preparing management reports

and maintaining records which provides a clear information regarding the performance of

organisation to managers are considered in management accounting (Bradbard, Alvis and

Morris,2014). Financial information, departmental information, statistical information which

remain essential in terms of determining the performance of organisations are included in

management accounting.

This report is prepared to defined the meaning of management accounting, and

management accounting systems are defined in this context. various methods used for

management accounting reporting are illustrated in this context. Techniques are used subject to

measure the profitability of organisation defined in this context. This is one of the essential

aspect in terms of analysing the profitability and managing the operations of association. Use of

budgetary control and role of planning tools to assist budgetary control process defined in this

context. Ways are compared in terms of adapting the management accounting system with in

organisation are defined in this context. Stubbing group of retail sector is chosen organisation

under which management accounting is illustrated.

TASK 1

P1 Management accounting and the essential requirements of types of MA systems

Management accounting

Management accounting provides a structure to use of type of information and data

related to analyse the day to day transactions and records for better management and control with

in business. It allows managers to evaluate 360 dimensions of business from lower level to upper

level. Different perspective and assumptions are made in terms of managing the operations and

functions of business. Anthers and writers have their own perspective in terms of management

accounting. Management accounting is not only a tool used for effective management and

control but also it is a process of nourishing the organisation's functions and management

operations in more significant manner (Bruynseels and Cardinaels, 2013).

As per IMA (Institute of Management Accounts) “management accounting is a

profession that involves partnering in managerial decisions making, addressing plans,

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

performance management system, providing skills and knowledge subject to financial reporting

and control to assist management and formulating and implementing of business policies and

strategies.

As per business environment organisational needs and priorities also gee changed. There

are type of management accounting systems has been formed in terms of providing the path of

effective working and management. There are type of management accounting systems are

defined below which are commonly used by organisation in present organisational environment:

MIS (Management Information System) system: a system based information is

provided in terms of managing the business operations and managements are defined in this

context. System generated information are used to elaborate the context operations and

management of organisation. It is one of the essential aspect in terms of elaborating the

information and system for better used and effective management. In large organisations MIS is

widely used for sorting out the complex business circumstances and challenges. In organisational

context the information and details and information are associated with departmental issues and

problems (Chapman, Kern and Laguecir, 2014).

Cost accounting system: this accounting system Marjory used in large production and

manufacturing industries. To abolish the production and manufacturing issues and conflicts cost

accounting is being used by organisations rapidly. This mainly associated with defining the

budget requirements and preparing cost plans for effective management and plans. This provides

different type of methods and analysis approaches in terms of managing the operations and

functions with optimum use of financial resources.

Inventory management system: this is a system which helps to control and manage the

flow of inventories and stocks with in storage departments and sections. This mainly associated

with identifying the requirement of raw stock to continue the manufacturing and production

process with and resolving the production and manufacturing issues. As the Stubbing group of

retail deals in day to day retail products and the raw stocks materials are the essential aspects

considered in this inventory management system. EOQ, ABC are the methods are used to

manage the flow of inventories with in organisation. FIFO, LIFO, Weighted average methods are

the valuation techniques used for determining the price of inventories.

Price optimisation system: this is an accounting system which is used to elaborate the

concept of determining the price of products and services by utilising the cost of resources. This

2

and control to assist management and formulating and implementing of business policies and

strategies.

As per business environment organisational needs and priorities also gee changed. There

are type of management accounting systems has been formed in terms of providing the path of

effective working and management. There are type of management accounting systems are

defined below which are commonly used by organisation in present organisational environment:

MIS (Management Information System) system: a system based information is

provided in terms of managing the business operations and managements are defined in this

context. System generated information are used to elaborate the context operations and

management of organisation. It is one of the essential aspect in terms of elaborating the

information and system for better used and effective management. In large organisations MIS is

widely used for sorting out the complex business circumstances and challenges. In organisational

context the information and details and information are associated with departmental issues and

problems (Chapman, Kern and Laguecir, 2014).

Cost accounting system: this accounting system Marjory used in large production and

manufacturing industries. To abolish the production and manufacturing issues and conflicts cost

accounting is being used by organisations rapidly. This mainly associated with defining the

budget requirements and preparing cost plans for effective management and plans. This provides

different type of methods and analysis approaches in terms of managing the operations and

functions with optimum use of financial resources.

Inventory management system: this is a system which helps to control and manage the

flow of inventories and stocks with in storage departments and sections. This mainly associated

with identifying the requirement of raw stock to continue the manufacturing and production

process with and resolving the production and manufacturing issues. As the Stubbing group of

retail deals in day to day retail products and the raw stocks materials are the essential aspects

considered in this inventory management system. EOQ, ABC are the methods are used to

manage the flow of inventories with in organisation. FIFO, LIFO, Weighted average methods are

the valuation techniques used for determining the price of inventories.

Price optimisation system: this is an accounting system which is used to elaborate the

concept of determining the price of products and services by utilising the cost of resources. This

2

system helps to explain the essential aspect which remain associated with analysing the price of

per product and services by compressing the cost of allocated resources. Stubbing group of retail

mainly associated with providing retail products as home appliances, grocery products. This

system would help to centralised the cost of applied resources and allocation of resources with in

the organisation.

P2 Various methods used for management accounting reporting

There are numerous reports which can be readied like monetary and costing reports yet

not at all like administration bookkeeping report they cannot present a correct impression of the

association's money related and administrative position. Administration bookkeeping reports are

the administrative archives which mirror the genuine and reasonable photo of an association's

budgetary position, planning of these administration bookkeeping reports are a vital assignment

to execute as it requires high aptitudes (Goodman and et. Al., 2013).

Stubbing group has procured a group of experts who take care of their administrative

records and reports to ensure that speculators and different gatherings can get to precise reports

and other administrative archives.

Sorts of administration bookkeeping reports

Administration bookkeeping report is an authoritative administration archive which is set

up by the directors for the outsiders with the goal that they can get to a genuine and reasonable

photo of the association, few of those administration bookkeeping reports are:

Accounts receivable report – Bookkeeping receivable report is set up to account the

records of every unpaid purchaser to ensure that all sum is gotten properly, if any unpaid

purchaser neglects to pay the sum than it will be recorded in terrible obligations report

independently or in the area of awful obligations in money due report as it were. Account

receivable report is an archive which contains arrangements of all unpaid client alongside their

sums, dates and bookkeeping periods.

Cash flow report – It incorporates all inflow and outpouring money exchange happened

from working, contributing and financing exercises, Stubbing group plans income articulation

for brief periods which can be valuable for them to get to month to month appraisals of costs and

which can refresh effortlessly. Cash stream articulation or report incorporates all money

exchanges of the association which influences an association's execution (Guthrie and Parker,

2014).

3

per product and services by compressing the cost of allocated resources. Stubbing group of retail

mainly associated with providing retail products as home appliances, grocery products. This

system would help to centralised the cost of applied resources and allocation of resources with in

the organisation.

P2 Various methods used for management accounting reporting

There are numerous reports which can be readied like monetary and costing reports yet

not at all like administration bookkeeping report they cannot present a correct impression of the

association's money related and administrative position. Administration bookkeeping reports are

the administrative archives which mirror the genuine and reasonable photo of an association's

budgetary position, planning of these administration bookkeeping reports are a vital assignment

to execute as it requires high aptitudes (Goodman and et. Al., 2013).

Stubbing group has procured a group of experts who take care of their administrative

records and reports to ensure that speculators and different gatherings can get to precise reports

and other administrative archives.

Sorts of administration bookkeeping reports

Administration bookkeeping report is an authoritative administration archive which is set

up by the directors for the outsiders with the goal that they can get to a genuine and reasonable

photo of the association, few of those administration bookkeeping reports are:

Accounts receivable report – Bookkeeping receivable report is set up to account the

records of every unpaid purchaser to ensure that all sum is gotten properly, if any unpaid

purchaser neglects to pay the sum than it will be recorded in terrible obligations report

independently or in the area of awful obligations in money due report as it were. Account

receivable report is an archive which contains arrangements of all unpaid client alongside their

sums, dates and bookkeeping periods.

Cash flow report – It incorporates all inflow and outpouring money exchange happened

from working, contributing and financing exercises, Stubbing group plans income articulation

for brief periods which can be valuable for them to get to month to month appraisals of costs and

which can refresh effortlessly. Cash stream articulation or report incorporates all money

exchanges of the association which influences an association's execution (Guthrie and Parker,

2014).

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial reports – Monetary reports of an association for the most part incorporates

exchanging record, benefit and misfortune proclamation and accounting report. Usually

monetary reports are incorporated into budgetary bookkeeping however to recognize a precise

administration position of an association. Stubbing group readies their money related report by

including their benefit and misfortune proclamation which demonstrates all incomes and

consumptions of the association and accounting report which is the confirmation of the

advantages and liabilities. It is critical for the managers to incorporate budgetary report while

getting ready administrative bookkeeping report as it reflect figures and correct quantities of the

association's productivity, costs and so on (Myers, 2013).

Job cost report – Occupation cost report enables associations to like Stubbing group to

assesses and recognize the benefit making capacity of different employment exercises, with the

goal that manager can centre around most productive employment movement. Job cost report is

a sort of administration bookkeeping report which decides the costs associated with different

occupations performed in an association.

Performance report – Performance report are set up to check general execution of an

association including each representative of each division, administrators of an association break

down and assesses exhibitions of workers and think about it from different pre settled guidelines

and benchmarks. Stubbing group readies their execution answer to have precise outcomes for

advancement of their systems which can lead them towards accomplishment of their objectives.

Sales report – Sales report incorporates deals done in a money related year which can

help an association breaking down what sources are more beneficial and distinguishes those

business people who produces generally salary. Stubbing group sets up their business report by

deciding all deals made in multi year, and investigations which dispersion channel is producing

more income that is retail appropriation channel or discount dissemination channel.

Stock administration report – This bookkeeping report is vital as associations like

Stubbing group which decent variety in their items and inventories are in much need of a

successful stock administration report framework, with the goal that every single supplied stock

can be utilized proficiently. Inventory administration report is a bookkeeping archive where all

inventories of an association are recorded paying little respect to its tendency like crude material,

merchandise occupied with work in advance or last items.

4

exchanging record, benefit and misfortune proclamation and accounting report. Usually

monetary reports are incorporated into budgetary bookkeeping however to recognize a precise

administration position of an association. Stubbing group readies their money related report by

including their benefit and misfortune proclamation which demonstrates all incomes and

consumptions of the association and accounting report which is the confirmation of the

advantages and liabilities. It is critical for the managers to incorporate budgetary report while

getting ready administrative bookkeeping report as it reflect figures and correct quantities of the

association's productivity, costs and so on (Myers, 2013).

Job cost report – Occupation cost report enables associations to like Stubbing group to

assesses and recognize the benefit making capacity of different employment exercises, with the

goal that manager can centre around most productive employment movement. Job cost report is

a sort of administration bookkeeping report which decides the costs associated with different

occupations performed in an association.

Performance report – Performance report are set up to check general execution of an

association including each representative of each division, administrators of an association break

down and assesses exhibitions of workers and think about it from different pre settled guidelines

and benchmarks. Stubbing group readies their execution answer to have precise outcomes for

advancement of their systems which can lead them towards accomplishment of their objectives.

Sales report – Sales report incorporates deals done in a money related year which can

help an association breaking down what sources are more beneficial and distinguishes those

business people who produces generally salary. Stubbing group sets up their business report by

deciding all deals made in multi year, and investigations which dispersion channel is producing

more income that is retail appropriation channel or discount dissemination channel.

Stock administration report – This bookkeeping report is vital as associations like

Stubbing group which decent variety in their items and inventories are in much need of a

successful stock administration report framework, with the goal that every single supplied stock

can be utilized proficiently. Inventory administration report is a bookkeeping archive where all

inventories of an association are recorded paying little respect to its tendency like crude material,

merchandise occupied with work in advance or last items.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M1 effectiveness of management accounting systems and their application in organisation

There are options and mediums defined below that which management accounting

system is suitable for organisations.

Price optimising system: this system is suitable for those organisation which deals in

multiple products and services. Products and services can be divided as per allocation of

resources. Price is calculated on the basis of utilisation of resources at per product.

Inventory management system: this system will be able to manage the systems related

to Inventory management and control. Organisation which deals in large quantities and

inventories use these inventory management system (Otley, 2016).

Cost accounting system: to evaluate profitability and cost of production and operations

are considered in this system. Manufacturing and production organisations which production

departments remain bifurcated in various sections use this accounting system.

D1 integration of management accounting system and management accounting reporting

Management accounting reports are produced with the help of management accounting

systems. There is a direct relation found in terms of managing accounting systems and the

management accounting reports. Effective business strategies remain based upon accurate

accounting reports and management this is the main aspect in terms of preparing the accounting

reports. As per above analysis it is considered that the management accounting is a process of

containing the records and information in such an manner so that effective management and

process be able to correlate the information in significant manner (Tucker and Lowe, 2014).

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

Marginal costing – this is one of the cost evaluating and profit measurement technique

which helps to make effective decision making strategies and plans. This costing technique

contains all the variable cost as direct material, direct labour and direct expenses in terms of

evaluating the marginal effect upon evaluating the profitability and maximising the profitability.

All other expenditures and cost as fixed cost are charged on periodic basis. This cost mainly

helps to determine the price and strategies for better understanding and analysis. This mainly

associated with deploying strategies and plans for better understanding of direct cost concepts

and manufacturing cost.

5

There are options and mediums defined below that which management accounting

system is suitable for organisations.

Price optimising system: this system is suitable for those organisation which deals in

multiple products and services. Products and services can be divided as per allocation of

resources. Price is calculated on the basis of utilisation of resources at per product.

Inventory management system: this system will be able to manage the systems related

to Inventory management and control. Organisation which deals in large quantities and

inventories use these inventory management system (Otley, 2016).

Cost accounting system: to evaluate profitability and cost of production and operations

are considered in this system. Manufacturing and production organisations which production

departments remain bifurcated in various sections use this accounting system.

D1 integration of management accounting system and management accounting reporting

Management accounting reports are produced with the help of management accounting

systems. There is a direct relation found in terms of managing accounting systems and the

management accounting reports. Effective business strategies remain based upon accurate

accounting reports and management this is the main aspect in terms of preparing the accounting

reports. As per above analysis it is considered that the management accounting is a process of

containing the records and information in such an manner so that effective management and

process be able to correlate the information in significant manner (Tucker and Lowe, 2014).

TASK 2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an income statement

Marginal costing – this is one of the cost evaluating and profit measurement technique

which helps to make effective decision making strategies and plans. This costing technique

contains all the variable cost as direct material, direct labour and direct expenses in terms of

evaluating the marginal effect upon evaluating the profitability and maximising the profitability.

All other expenditures and cost as fixed cost are charged on periodic basis. This cost mainly

helps to determine the price and strategies for better understanding and analysis. This mainly

associated with deploying strategies and plans for better understanding of direct cost concepts

and manufacturing cost.

5

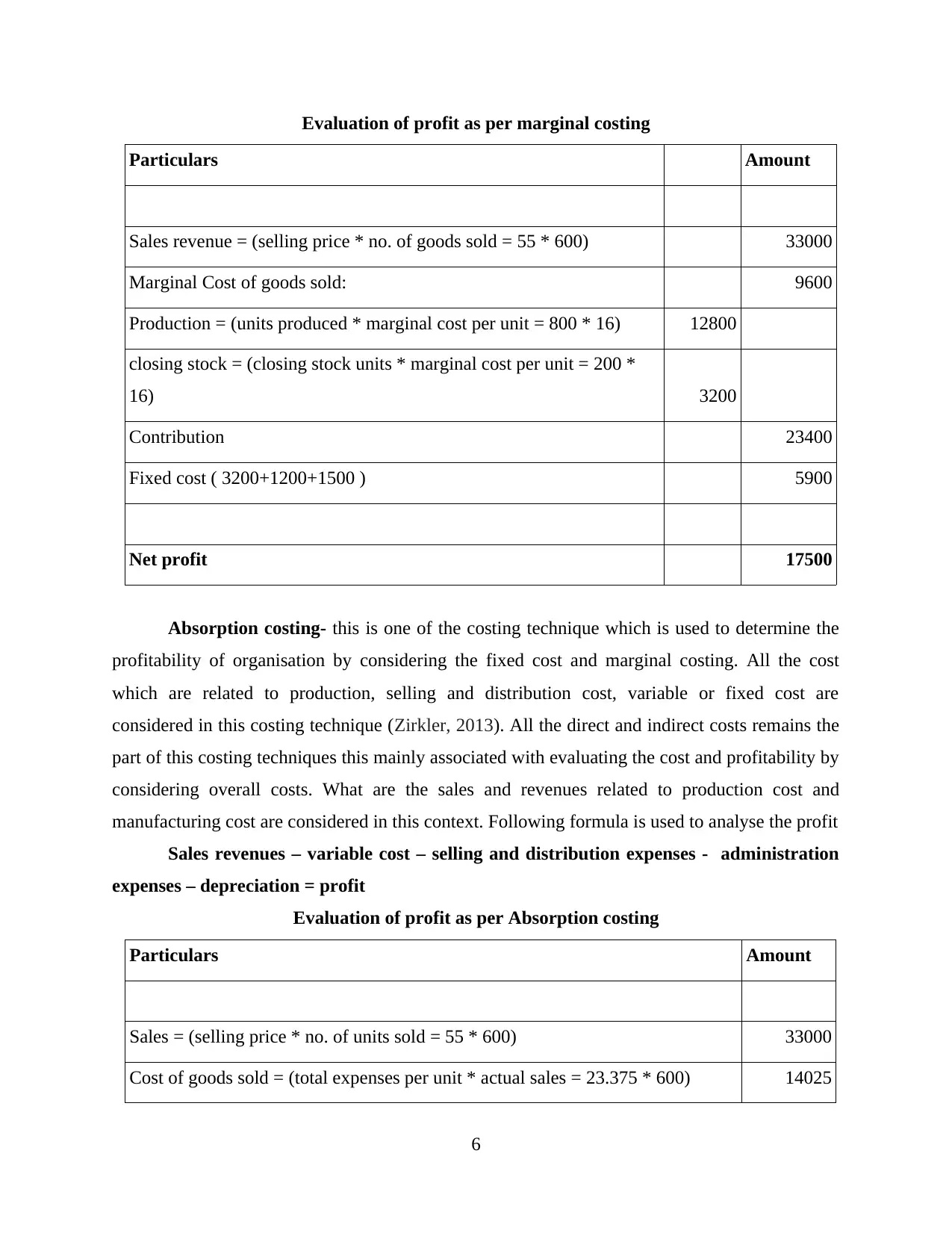

Evaluation of profit as per marginal costing

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing- this is one of the costing technique which is used to determine the

profitability of organisation by considering the fixed cost and marginal costing. All the cost

which are related to production, selling and distribution cost, variable or fixed cost are

considered in this costing technique (Zirkler, 2013). All the direct and indirect costs remains the

part of this costing techniques this mainly associated with evaluating the cost and profitability by

considering overall costs. What are the sales and revenues related to production cost and

manufacturing cost are considered in this context. Following formula is used to analyse the profit

Sales revenues – variable cost – selling and distribution expenses - administration

expenses – depreciation = profit

Evaluation of profit as per Absorption costing

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

6

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Absorption costing- this is one of the costing technique which is used to determine the

profitability of organisation by considering the fixed cost and marginal costing. All the cost

which are related to production, selling and distribution cost, variable or fixed cost are

considered in this costing technique (Zirkler, 2013). All the direct and indirect costs remains the

part of this costing techniques this mainly associated with evaluating the cost and profitability by

considering overall costs. What are the sales and revenues related to production cost and

manufacturing cost are considered in this context. Following formula is used to analyse the profit

Sales revenues – variable cost – selling and distribution expenses - administration

expenses – depreciation = profit

Evaluation of profit as per Absorption costing

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

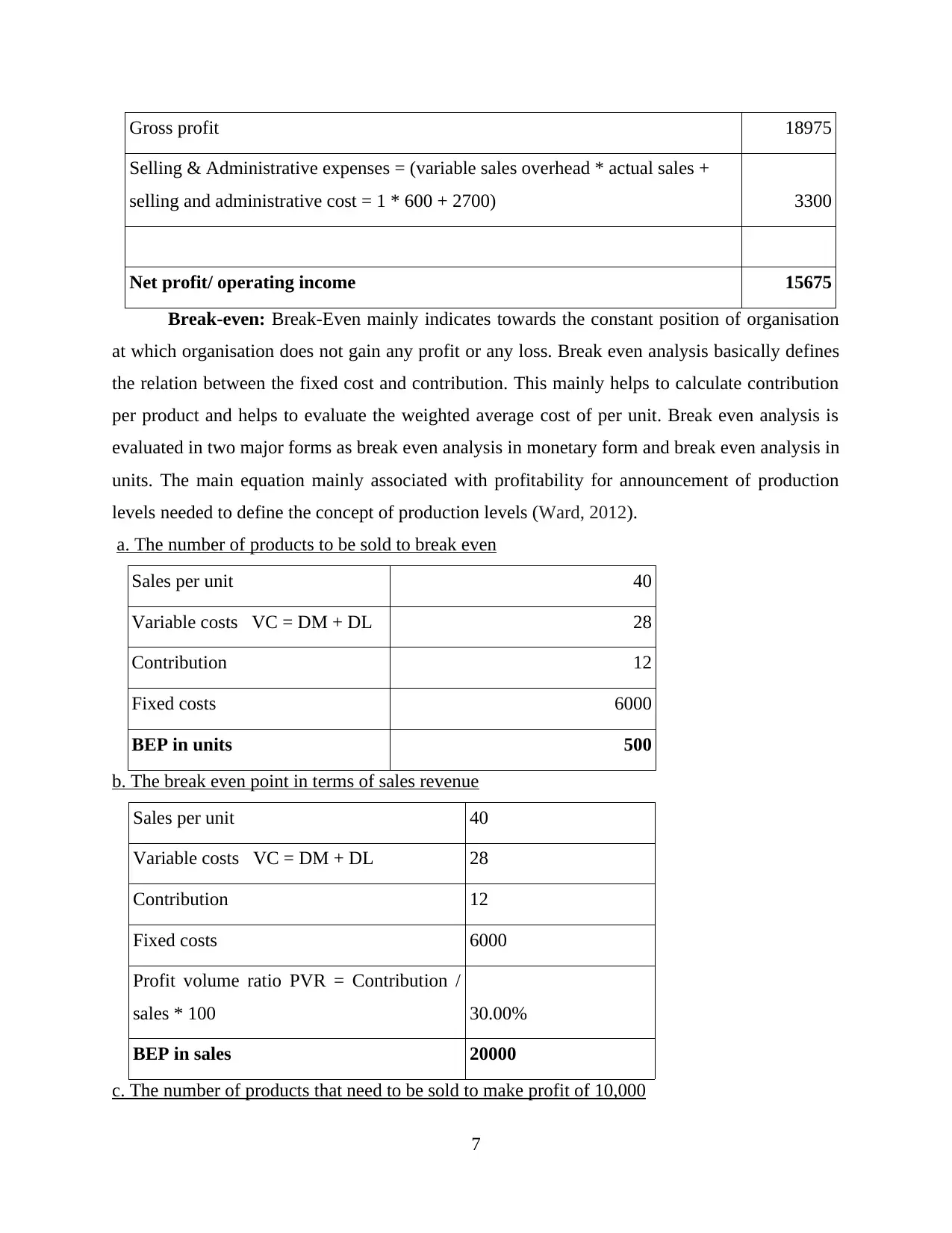

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-even: Break-Even mainly indicates towards the constant position of organisation

at which organisation does not gain any profit or any loss. Break even analysis basically defines

the relation between the fixed cost and contribution. This mainly helps to calculate contribution

per product and helps to evaluate the weighted average cost of per unit. Break even analysis is

evaluated in two major forms as break even analysis in monetary form and break even analysis in

units. The main equation mainly associated with profitability for announcement of production

levels needed to define the concept of production levels (Ward, 2012).

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. The break even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

7

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break-even: Break-Even mainly indicates towards the constant position of organisation

at which organisation does not gain any profit or any loss. Break even analysis basically defines

the relation between the fixed cost and contribution. This mainly helps to calculate contribution

per product and helps to evaluate the weighted average cost of per unit. Break even analysis is

evaluated in two major forms as break even analysis in monetary form and break even analysis in

units. The main equation mainly associated with profitability for announcement of production

levels needed to define the concept of production levels (Ward, 2012).

a. The number of products to be sold to break even

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

b. The break even point in terms of sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution /

sales * 100 30.00%

BEP in sales 20000

c. The number of products that need to be sold to make profit of 10,000

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

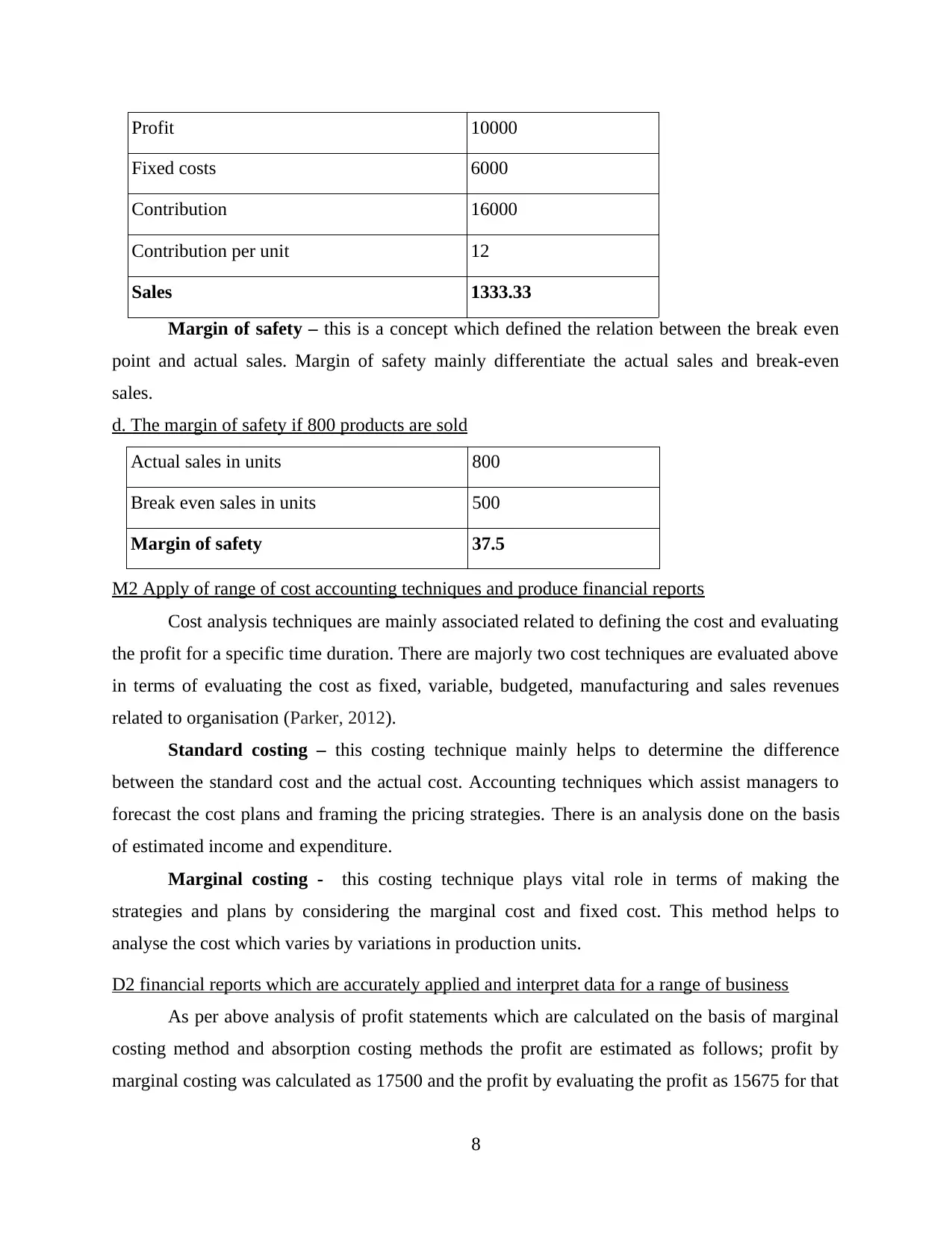

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – this is a concept which defined the relation between the break even

point and actual sales. Margin of safety mainly differentiate the actual sales and break-even

sales.

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Apply of range of cost accounting techniques and produce financial reports

Cost analysis techniques are mainly associated related to defining the cost and evaluating

the profit for a specific time duration. There are majorly two cost techniques are evaluated above

in terms of evaluating the cost as fixed, variable, budgeted, manufacturing and sales revenues

related to organisation (Parker, 2012).

Standard costing – this costing technique mainly helps to determine the difference

between the standard cost and the actual cost. Accounting techniques which assist managers to

forecast the cost plans and framing the pricing strategies. There is an analysis done on the basis

of estimated income and expenditure.

Marginal costing - this costing technique plays vital role in terms of making the

strategies and plans by considering the marginal cost and fixed cost. This method helps to

analyse the cost which varies by variations in production units.

D2 financial reports which are accurately applied and interpret data for a range of business

As per above analysis of profit statements which are calculated on the basis of marginal

costing method and absorption costing methods the profit are estimated as follows; profit by

marginal costing was calculated as 17500 and the profit by evaluating the profit as 15675 for that

8

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety – this is a concept which defined the relation between the break even

point and actual sales. Margin of safety mainly differentiate the actual sales and break-even

sales.

d. The margin of safety if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Apply of range of cost accounting techniques and produce financial reports

Cost analysis techniques are mainly associated related to defining the cost and evaluating

the profit for a specific time duration. There are majorly two cost techniques are evaluated above

in terms of evaluating the cost as fixed, variable, budgeted, manufacturing and sales revenues

related to organisation (Parker, 2012).

Standard costing – this costing technique mainly helps to determine the difference

between the standard cost and the actual cost. Accounting techniques which assist managers to

forecast the cost plans and framing the pricing strategies. There is an analysis done on the basis

of estimated income and expenditure.

Marginal costing - this costing technique plays vital role in terms of making the

strategies and plans by considering the marginal cost and fixed cost. This method helps to

analyse the cost which varies by variations in production units.

D2 financial reports which are accurately applied and interpret data for a range of business

As per above analysis of profit statements which are calculated on the basis of marginal

costing method and absorption costing methods the profit are estimated as follows; profit by

marginal costing was calculated as 17500 and the profit by evaluating the profit as 15675 for that

8

period (Quinn, Strauss and Kristandl, 2014). As per the break-even analysis it is calculated that if

organisation produce at least 500 units that it would be able to maintain the constant position of

no profit and no loss. The margin of safety was calculated as 37.5.

TASK 3

P4 The advantages and disadvantages of different type of planning tools used for budgetary

control

Budgetary control is considered as a process of analysing the information and details for

future forecast and analysing the related aspects to performance and growth of organisation. In

legal terms management and departments of organisation keep align in making financial forecast

and preparing information to assist the budgeting process. There are type of information related

to sales budget, cash budget and fixed budgets are prepared in terms of effective control and

management.

There are type of planning tools are used in organisational context to assist the decision

making process which are discussed as follows;

Contingency tool

Possibility arranging incorporates noting the inquiries concerning what will happen, how

administration will manage it and what steps ought to be taken to manage such crises.

Contingency is an arranging device which empowers an association to be set up for future

vulnerabilities and crises, possibility arranging incorporates propel basic leadership about the

money related assets and stock administration (Van der Stede, 2011).

Merits: Contingency design goes about as a go down arrangement which is enacted when

there is any crisis circumstances which decreases misfortune.

Demerits: Contingency design is a move down arrangement for future crises, yet in the

event that none of the crisis circumstances happen than all the cash and assets utilized as a part of

readiness of alternate course of action is resultant to be squandered.

Forecasting tool

It encourages administration to find out the vulnerabilities without bounds by considering

past encounters and pattern investigation. Forecasting is an arranging instrument that ventures

future occasions and conditions.

9

organisation produce at least 500 units that it would be able to maintain the constant position of

no profit and no loss. The margin of safety was calculated as 37.5.

TASK 3

P4 The advantages and disadvantages of different type of planning tools used for budgetary

control

Budgetary control is considered as a process of analysing the information and details for

future forecast and analysing the related aspects to performance and growth of organisation. In

legal terms management and departments of organisation keep align in making financial forecast

and preparing information to assist the budgeting process. There are type of information related

to sales budget, cash budget and fixed budgets are prepared in terms of effective control and

management.

There are type of planning tools are used in organisational context to assist the decision

making process which are discussed as follows;

Contingency tool

Possibility arranging incorporates noting the inquiries concerning what will happen, how

administration will manage it and what steps ought to be taken to manage such crises.

Contingency is an arranging device which empowers an association to be set up for future

vulnerabilities and crises, possibility arranging incorporates propel basic leadership about the

money related assets and stock administration (Van der Stede, 2011).

Merits: Contingency design goes about as a go down arrangement which is enacted when

there is any crisis circumstances which decreases misfortune.

Demerits: Contingency design is a move down arrangement for future crises, yet in the

event that none of the crisis circumstances happen than all the cash and assets utilized as a part of

readiness of alternate course of action is resultant to be squandered.

Forecasting tool

It encourages administration to find out the vulnerabilities without bounds by considering

past encounters and pattern investigation. Forecasting is an arranging instrument that ventures

future occasions and conditions.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.