Management Accounting Report: Costing, Reporting, and Systems Analysis

VerifiedAdded on 2020/01/28

|20

|4826

|31

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, focusing on their application within R.L. Maynard Limited, a UK-based property construction company. It explores various management accounting systems, including traditional cost accounting, lean accounting, transfer pricing, and inventory management, highlighting their benefits and requirements. The report delves into different reporting methods, such as cost reports, job cost reports, sales reports, payroll reports, budget reports, and accounts receivable reports, explaining their significance in financial management and decision-making. Furthermore, the study includes the preparation of financial gain statements using both marginal and absorption costing methods, comparing their outcomes and emphasizing the impact of different cost considerations on profitability. The report underscores the importance of management accounting in reducing expenses, aiding business decisions, and increasing return on investments, offering a practical perspective on financial management within a business context.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REPORT

From: Management accounting

To: General Manager

R. L. Maynard Limited

Date: 20th April 2017

Subject: Management accounting and its systems along with various costing as well as reporting

methods implementation in the workplace.

INTRODUCTION

In the business environment, it is very necessary to manage financial resources in order to

make the firm more profitable within industry. In context to this in the accounting and financial

world, there are different types of methods, tools and techniques which are helpful for

entrepreneur for manage accoutring transactions in proper manner. In the present report R.L.

Maynard Limited company is chosen which is located in UK and operates in property

construction segment. The company has 24 employees in the organisation and generates sales

worth 10.00 GBP. The report shows different methods and importance of management

accounting informations which helps to the firm up to greater extent. Along with this it shows

income statement as per the absorption and marginal costing methods as well as difference

between both the methods. Further, the study emphasises on benefits and limitations of various

kinds of planning tools uses in management accounting along with examples. At the last, current

report describes about management accounting systems by which the firm able to resolve

financial obstacles or problems.

TASK 1

P1 Different types of management accounting systems which are require for R.L. Maynard

Limited

Accounts which are made for managerial purpose are comes under management

accounting. These are used for internal affairs which provides timely information regarding

financial status of the company on daily basis. This helps in decision making by the

departmental managers for short term. Management accounting is a combination of accounts,

From: Management accounting

To: General Manager

R. L. Maynard Limited

Date: 20th April 2017

Subject: Management accounting and its systems along with various costing as well as reporting

methods implementation in the workplace.

INTRODUCTION

In the business environment, it is very necessary to manage financial resources in order to

make the firm more profitable within industry. In context to this in the accounting and financial

world, there are different types of methods, tools and techniques which are helpful for

entrepreneur for manage accoutring transactions in proper manner. In the present report R.L.

Maynard Limited company is chosen which is located in UK and operates in property

construction segment. The company has 24 employees in the organisation and generates sales

worth 10.00 GBP. The report shows different methods and importance of management

accounting informations which helps to the firm up to greater extent. Along with this it shows

income statement as per the absorption and marginal costing methods as well as difference

between both the methods. Further, the study emphasises on benefits and limitations of various

kinds of planning tools uses in management accounting along with examples. At the last, current

report describes about management accounting systems by which the firm able to resolve

financial obstacles or problems.

TASK 1

P1 Different types of management accounting systems which are require for R.L. Maynard

Limited

Accounts which are made for managerial purpose are comes under management

accounting. These are used for internal affairs which provides timely information regarding

financial status of the company on daily basis. This helps in decision making by the

departmental managers for short term. Management accounting is a combination of accounts,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

finance and management (Kaplan and Atkinson, 2015). It contains all kind of information

related to each subject or activity like strategy of business, financial accounts, etc. It is very

helpful for small businesses.

Benefits of management accounting:

Reduce expenses:It is considered as essential firms to reduces their expenses on operation by

analysing the cost of economic resources.

Help in making business decisions: it provides a quantitative analysis to the owners about the

cost of goods and services that helps in making effective decisions to enhance profitability.

Increase in return on investments: It provides forecast to the firms about the consumer

demand, potential sales and effects of prices on customers by which they can take effective

measures to increase their profitability.

R.L. Maynard Ltd. which is a property construction company, it follows management

accounting system in their company. Through this they are running their company very

effectively and efficiently. Management accounting is to be done on daily, weekly or monthly

basis for the company's internal people like functional or departmental heads, board of directors,

operational officers.

The necessary requirements of various management accounting systems which are

followed by the R.L. Maynard Ltd.:

The cost which is related to the manufacturing of goods and services of the organization

covers in the management accounting (Ward, 2012). The most commonly systems of

management accounting involves are as follows:

Traditional cost accounting

Lean accounting

Turnout accounting

Transfer pricing

Price optimisation system

Cost accounting system

Inventory management system

Job costing system

related to each subject or activity like strategy of business, financial accounts, etc. It is very

helpful for small businesses.

Benefits of management accounting:

Reduce expenses:It is considered as essential firms to reduces their expenses on operation by

analysing the cost of economic resources.

Help in making business decisions: it provides a quantitative analysis to the owners about the

cost of goods and services that helps in making effective decisions to enhance profitability.

Increase in return on investments: It provides forecast to the firms about the consumer

demand, potential sales and effects of prices on customers by which they can take effective

measures to increase their profitability.

R.L. Maynard Ltd. which is a property construction company, it follows management

accounting system in their company. Through this they are running their company very

effectively and efficiently. Management accounting is to be done on daily, weekly or monthly

basis for the company's internal people like functional or departmental heads, board of directors,

operational officers.

The necessary requirements of various management accounting systems which are

followed by the R.L. Maynard Ltd.:

The cost which is related to the manufacturing of goods and services of the organization

covers in the management accounting (Ward, 2012). The most commonly systems of

management accounting involves are as follows:

Traditional cost accounting

Lean accounting

Turnout accounting

Transfer pricing

Price optimisation system

Cost accounting system

Inventory management system

Job costing system

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The description of the above mentioned accounting systems are discussed below: Traditional cost accounting: In the traditional cost accounting system, the cost of

production overhead is to be allocated to the products which has manufactured in the

company. This traditional method also called as Conventional method. Mostly

traditional method of cost accounting is to be adopted by the manufacturing companies

like RL Maynard Ltd. It distributes the indirect costs of the manufacturing unit on the

produced units. This is to be done on the criteria of quantity or volume of the produced

units, direct labour over-head, production over-head. Traditional method of cost

accounting includes Job order costing and Process costing. This costing is applicable

where cost can be easily identified for individual project in case of big or large projects

(Strumickas and Valanciene, 2015). Since the homogeneous products are move on

various processes, so it become difficult to allocate cost individually on them. Process

costing is used for allocating cost on the basis of number of processes on which the

homogeneous products have gone through.

Transfer pricing: Transfer pricing generates when goods are transferring from one

department to another department and from ownership organization to the subsidiary

firm. The moving or transfer of goods from one place to another added little part of cost

to it with each and every step for transferring. Generally the costs which are to be

generated in transfer pricing are variable cost and opportunity cost. Variable cost

depends on the production unit. And opportunity cost shows the amount of money that

the company would bear in case of outsourcing of products to the outside firm. The

benefit of transfer pricing is its flexibility in the system (Suomala and Lyly-Yrjänäinen,

2012).

Price optimisation system: It is considered as a mathematical analysis, which is used

by business firms to understand response of customers in different possible prices. It is

also used by firms to adopt the best possible prices for their products to influence more

customers.

Cost accounting system:Suitable framework utilized by entities to analyse the cost their

products to determine the profitability (Melnyk and et.al., 2014). Also, considered as

effective method to control the cost, expenses to increase the profitability of firm.

Inventory management system:Continuous process of handling the parts and products

production overhead is to be allocated to the products which has manufactured in the

company. This traditional method also called as Conventional method. Mostly

traditional method of cost accounting is to be adopted by the manufacturing companies

like RL Maynard Ltd. It distributes the indirect costs of the manufacturing unit on the

produced units. This is to be done on the criteria of quantity or volume of the produced

units, direct labour over-head, production over-head. Traditional method of cost

accounting includes Job order costing and Process costing. This costing is applicable

where cost can be easily identified for individual project in case of big or large projects

(Strumickas and Valanciene, 2015). Since the homogeneous products are move on

various processes, so it become difficult to allocate cost individually on them. Process

costing is used for allocating cost on the basis of number of processes on which the

homogeneous products have gone through.

Transfer pricing: Transfer pricing generates when goods are transferring from one

department to another department and from ownership organization to the subsidiary

firm. The moving or transfer of goods from one place to another added little part of cost

to it with each and every step for transferring. Generally the costs which are to be

generated in transfer pricing are variable cost and opportunity cost. Variable cost

depends on the production unit. And opportunity cost shows the amount of money that

the company would bear in case of outsourcing of products to the outside firm. The

benefit of transfer pricing is its flexibility in the system (Suomala and Lyly-Yrjänäinen,

2012).

Price optimisation system: It is considered as a mathematical analysis, which is used

by business firms to understand response of customers in different possible prices. It is

also used by firms to adopt the best possible prices for their products to influence more

customers.

Cost accounting system:Suitable framework utilized by entities to analyse the cost their

products to determine the profitability (Melnyk and et.al., 2014). Also, considered as

effective method to control the cost, expenses to increase the profitability of firm.

Inventory management system:Continuous process of handling the parts and products

of company. System used to manage the inventory of firm and providing information

about the availability of products within the firm.

Job costing system: Most effective system that is used to calculate the manufacturing

cots of each products. Firms that are regulating in production of goods and services

utilize this method to determine the overall cost of manufacturing products (Chenhall,

2012).

P2 Explanation of various methods which are useful for the reporting of management accounting

Cost report: It is a process in which they provide the cost related information to the

management that helps in controlling the cost in future. Thus, it also assist in making

decisions as they provide the internal report system and it is used to determine the unit

cost of those products that are manufacture. This will facilitate them to report the cost of

goods on the firm's balance sheet as well as Cost of goods sold on the P/ L account. Thus,

these accounting will helps the management by provide them transfer pricing, variance

analysis, standard costing and activity based costing etc.

Job cost reports: The job cost report in which there is a overall statement of a firm's in

terms of profit and loss that are specifically given for each job that are assigned to

individuals. It helps the R.L. Maynard Ltd to make changes in the future with proper job

cost report and it is easier to get cost data relate to job that provides greater efficiency for

the long period of time (Kokubu and Kitada, 2015). Along with that, direct cost and

allocate overheads cost relate to the job all these are record in the ledger a/c and it is

summarise in the trail balance that also help the management to prepare the batch

manufacturing statement.

Sales report: The report indicate the company's sales increase or decrease that helps the

manager to know those areas where the market opportunity to increase the sales. The

report that shows the firm's actual sales made by over some specific time period this will

also help the management that time framework is more significant for them. Therefore,

management required these type of management report to know the customer's buying

behaviour relate to product or any services as they not analyse the firm's turnover but also

the discount offer of the clients.

about the availability of products within the firm.

Job costing system: Most effective system that is used to calculate the manufacturing

cots of each products. Firms that are regulating in production of goods and services

utilize this method to determine the overall cost of manufacturing products (Chenhall,

2012).

P2 Explanation of various methods which are useful for the reporting of management accounting

Cost report: It is a process in which they provide the cost related information to the

management that helps in controlling the cost in future. Thus, it also assist in making

decisions as they provide the internal report system and it is used to determine the unit

cost of those products that are manufacture. This will facilitate them to report the cost of

goods on the firm's balance sheet as well as Cost of goods sold on the P/ L account. Thus,

these accounting will helps the management by provide them transfer pricing, variance

analysis, standard costing and activity based costing etc.

Job cost reports: The job cost report in which there is a overall statement of a firm's in

terms of profit and loss that are specifically given for each job that are assigned to

individuals. It helps the R.L. Maynard Ltd to make changes in the future with proper job

cost report and it is easier to get cost data relate to job that provides greater efficiency for

the long period of time (Kokubu and Kitada, 2015). Along with that, direct cost and

allocate overheads cost relate to the job all these are record in the ledger a/c and it is

summarise in the trail balance that also help the management to prepare the batch

manufacturing statement.

Sales report: The report indicate the company's sales increase or decrease that helps the

manager to know those areas where the market opportunity to increase the sales. The

report that shows the firm's actual sales made by over some specific time period this will

also help the management that time framework is more significant for them. Therefore,

management required these type of management report to know the customer's buying

behaviour relate to product or any services as they not analyse the firm's turnover but also

the discount offer of the clients.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Payroll report: The report is regard to employee's compensation salary that show the

management to know the financial position of the organization (Klychova, Faskhutdinova

and Sadrieva, 2014). Thus, it show the company reputation and it help the manager to

evaluate the individual's performance through the increase in the number of bonus and

increment in the salary. Therefore, the report are generate automatically through the

software that are update with the legislative changes as it also save cost for a long time

period to the organization.

Budget report: The report is a internal part that are used by the firm's management to

make comparison the estimate performance with the actual to know the achievements

over the period. The R.L. Maynard Ltd helps in make comparison on those sales data so,

they can make various decisions regard to the firm. It is important for the to control the

activities and also make relevant decisions regard to financial resources so, they can run

the functions smoothly and effectively. The management can make out the deviation

through the budget report and also find out the cause and effects.

Account receivables report: Most important tool used by the firms to keep record of

invoices of unpaid customers and unused credit memos. It is most important for firms to

identity the amount which the firm has to take from debtors. It also used by the

management to determine the collections functions and credit.

Job cost report:From the analysis, it has been analysed that this report involves the

accumulation of expenses made by the firm on raw materials, labour and overhead for

manufacturing specific product. It utilized by firms to analyse and control the cost of

manufacturing products and services for increasing the profitability of firm.

TASK 2

2.1 Preparation of financial gain statement on the basis of costing method such as marginal and

absorption costing

Income statement is one of the most and widely used statement form all the financial

statements which shows firm's profitable situation at the end of specific period of time. In

context to this, the statement is prepared on the basis of two methods such as marginal as well as

absorption costing method (Drury, 2013). On the basis of both the methods and income

statement is prepared and stated below:

management to know the financial position of the organization (Klychova, Faskhutdinova

and Sadrieva, 2014). Thus, it show the company reputation and it help the manager to

evaluate the individual's performance through the increase in the number of bonus and

increment in the salary. Therefore, the report are generate automatically through the

software that are update with the legislative changes as it also save cost for a long time

period to the organization.

Budget report: The report is a internal part that are used by the firm's management to

make comparison the estimate performance with the actual to know the achievements

over the period. The R.L. Maynard Ltd helps in make comparison on those sales data so,

they can make various decisions regard to the firm. It is important for the to control the

activities and also make relevant decisions regard to financial resources so, they can run

the functions smoothly and effectively. The management can make out the deviation

through the budget report and also find out the cause and effects.

Account receivables report: Most important tool used by the firms to keep record of

invoices of unpaid customers and unused credit memos. It is most important for firms to

identity the amount which the firm has to take from debtors. It also used by the

management to determine the collections functions and credit.

Job cost report:From the analysis, it has been analysed that this report involves the

accumulation of expenses made by the firm on raw materials, labour and overhead for

manufacturing specific product. It utilized by firms to analyse and control the cost of

manufacturing products and services for increasing the profitability of firm.

TASK 2

2.1 Preparation of financial gain statement on the basis of costing method such as marginal and

absorption costing

Income statement is one of the most and widely used statement form all the financial

statements which shows firm's profitable situation at the end of specific period of time. In

context to this, the statement is prepared on the basis of two methods such as marginal as well as

absorption costing method (Drury, 2013). On the basis of both the methods and income

statement is prepared and stated below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

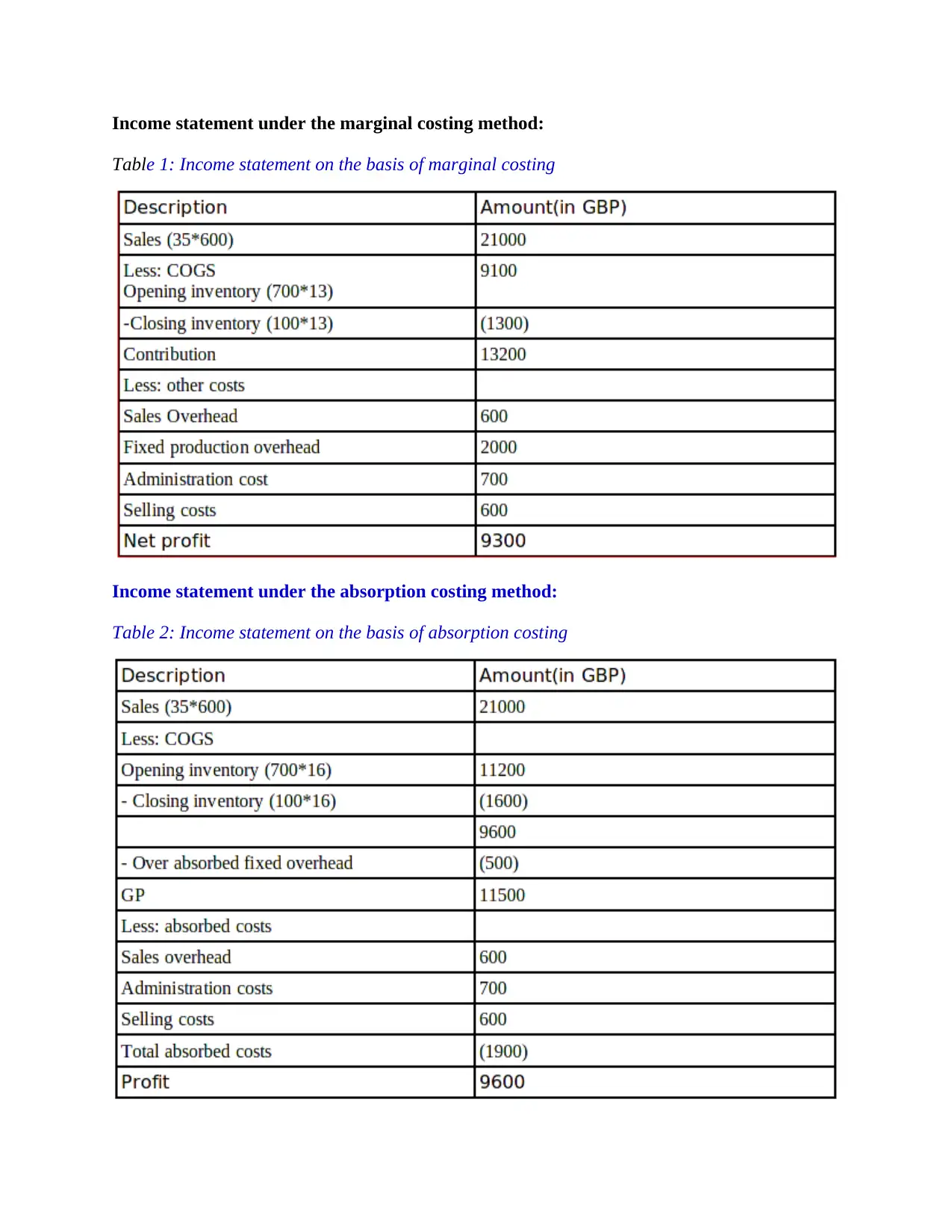

Income statement under the marginal costing method:

Table 1: Income statement on the basis of marginal costing

Income statement under the absorption costing method:

Table 2: Income statement on the basis of absorption costing

Table 1: Income statement on the basis of marginal costing

Income statement under the absorption costing method:

Table 2: Income statement on the basis of absorption costing

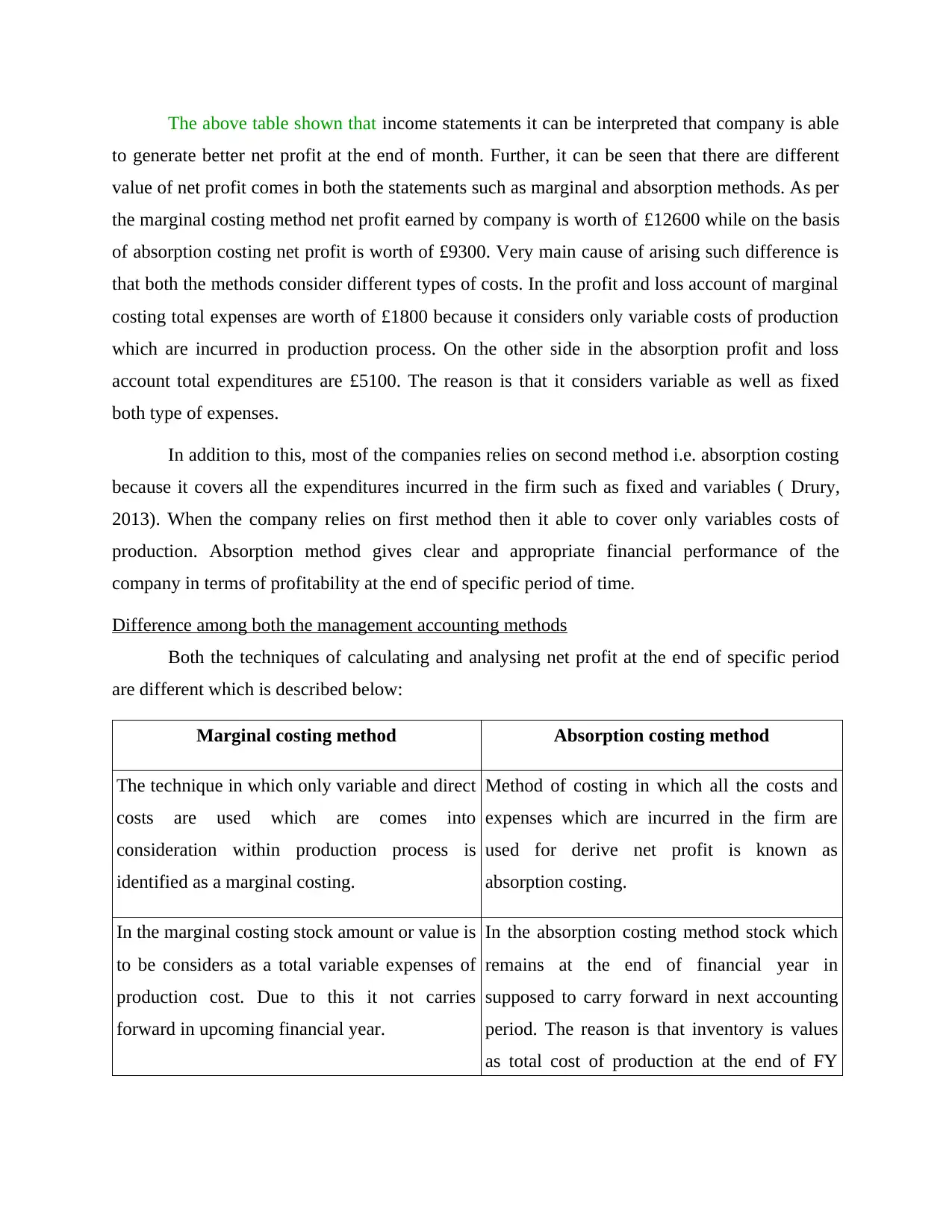

The above table shown that income statements it can be interpreted that company is able

to generate better net profit at the end of month. Further, it can be seen that there are different

value of net profit comes in both the statements such as marginal and absorption methods. As per

the marginal costing method net profit earned by company is worth of £12600 while on the basis

of absorption costing net profit is worth of £9300. Very main cause of arising such difference is

that both the methods consider different types of costs. In the profit and loss account of marginal

costing total expenses are worth of £1800 because it considers only variable costs of production

which are incurred in production process. On the other side in the absorption profit and loss

account total expenditures are £5100. The reason is that it considers variable as well as fixed

both type of expenses.

In addition to this, most of the companies relies on second method i.e. absorption costing

because it covers all the expenditures incurred in the firm such as fixed and variables ( Drury,

2013). When the company relies on first method then it able to cover only variables costs of

production. Absorption method gives clear and appropriate financial performance of the

company in terms of profitability at the end of specific period of time.

Difference among both the management accounting methods

Both the techniques of calculating and analysing net profit at the end of specific period

are different which is described below:

Marginal costing method Absorption costing method

The technique in which only variable and direct

costs are used which are comes into

consideration within production process is

identified as a marginal costing.

Method of costing in which all the costs and

expenses which are incurred in the firm are

used for derive net profit is known as

absorption costing.

In the marginal costing stock amount or value is

to be considers as a total variable expenses of

production cost. Due to this it not carries

forward in upcoming financial year.

In the absorption costing method stock which

remains at the end of financial year in

supposed to carry forward in next accounting

period. The reason is that inventory is values

as total cost of production at the end of FY

to generate better net profit at the end of month. Further, it can be seen that there are different

value of net profit comes in both the statements such as marginal and absorption methods. As per

the marginal costing method net profit earned by company is worth of £12600 while on the basis

of absorption costing net profit is worth of £9300. Very main cause of arising such difference is

that both the methods consider different types of costs. In the profit and loss account of marginal

costing total expenses are worth of £1800 because it considers only variable costs of production

which are incurred in production process. On the other side in the absorption profit and loss

account total expenditures are £5100. The reason is that it considers variable as well as fixed

both type of expenses.

In addition to this, most of the companies relies on second method i.e. absorption costing

because it covers all the expenditures incurred in the firm such as fixed and variables ( Drury,

2013). When the company relies on first method then it able to cover only variables costs of

production. Absorption method gives clear and appropriate financial performance of the

company in terms of profitability at the end of specific period of time.

Difference among both the management accounting methods

Both the techniques of calculating and analysing net profit at the end of specific period

are different which is described below:

Marginal costing method Absorption costing method

The technique in which only variable and direct

costs are used which are comes into

consideration within production process is

identified as a marginal costing.

Method of costing in which all the costs and

expenses which are incurred in the firm are

used for derive net profit is known as

absorption costing.

In the marginal costing stock amount or value is

to be considers as a total variable expenses of

production cost. Due to this it not carries

forward in upcoming financial year.

In the absorption costing method stock which

remains at the end of financial year in

supposed to carry forward in next accounting

period. The reason is that inventory is values

as total cost of production at the end of FY

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(Manohar, M., 2012).

When the level or amount of stock will be

decrease then the net profit will be increase in

the marginal costing method because here such

amount is not carry forward.

In this when amount of stock enhances then

net profit as well at the end of FY due to carry

forward.

The respective method is used by the company

in order to take better and effective business

decisions (Drury, 2013 ).

Here the company is able to take better

business decisions as well as treatment of

inventory is to be done on the basis of

international accounting standards 2.

The technique or costing method is used by

management for the purpose of internal

reporting system.

The absorption costing method is used by

management for the purpose of external

reporting system.

In this method amount of net profit is higher

compare to another costing method.

As per the respective costing system net profit

is comparatively low due to considering all the

expenses and costs.

TASK 3

P4 Explanation of advantages and drawbacks of different kinds of planning tools

In the accounting systems there are various types of tools and techniques are available by

which management able to control over the disposals. Further, by such tools the firm helpful up

to greater level in the budgetary control systems. The organisation such as R.L. Maynard using

several planning tools to generate high amount of profit at the end of accounting period in overall

construction industry of UK (R.L. Maynard Limited, 2016). Among various tools the firm uses

mainly three methods or techniques which are such as budget, capital budgeting methods as well

as ratio analysis. Benefits and limitations of such tools are describes as below:

Budget: It is one of the most important technique used in the firm for managing accounts

and financial resources as well. As per the budget the R.L. Maynard able to know future

accounting and financial performance of business. Here the management forecasts that within

When the level or amount of stock will be

decrease then the net profit will be increase in

the marginal costing method because here such

amount is not carry forward.

In this when amount of stock enhances then

net profit as well at the end of FY due to carry

forward.

The respective method is used by the company

in order to take better and effective business

decisions (Drury, 2013 ).

Here the company is able to take better

business decisions as well as treatment of

inventory is to be done on the basis of

international accounting standards 2.

The technique or costing method is used by

management for the purpose of internal

reporting system.

The absorption costing method is used by

management for the purpose of external

reporting system.

In this method amount of net profit is higher

compare to another costing method.

As per the respective costing system net profit

is comparatively low due to considering all the

expenses and costs.

TASK 3

P4 Explanation of advantages and drawbacks of different kinds of planning tools

In the accounting systems there are various types of tools and techniques are available by

which management able to control over the disposals. Further, by such tools the firm helpful up

to greater level in the budgetary control systems. The organisation such as R.L. Maynard using

several planning tools to generate high amount of profit at the end of accounting period in overall

construction industry of UK (R.L. Maynard Limited, 2016). Among various tools the firm uses

mainly three methods or techniques which are such as budget, capital budgeting methods as well

as ratio analysis. Benefits and limitations of such tools are describes as below:

Budget: It is one of the most important technique used in the firm for managing accounts

and financial resources as well. As per the budget the R.L. Maynard able to know future

accounting and financial performance of business. Here the management forecasts that within

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

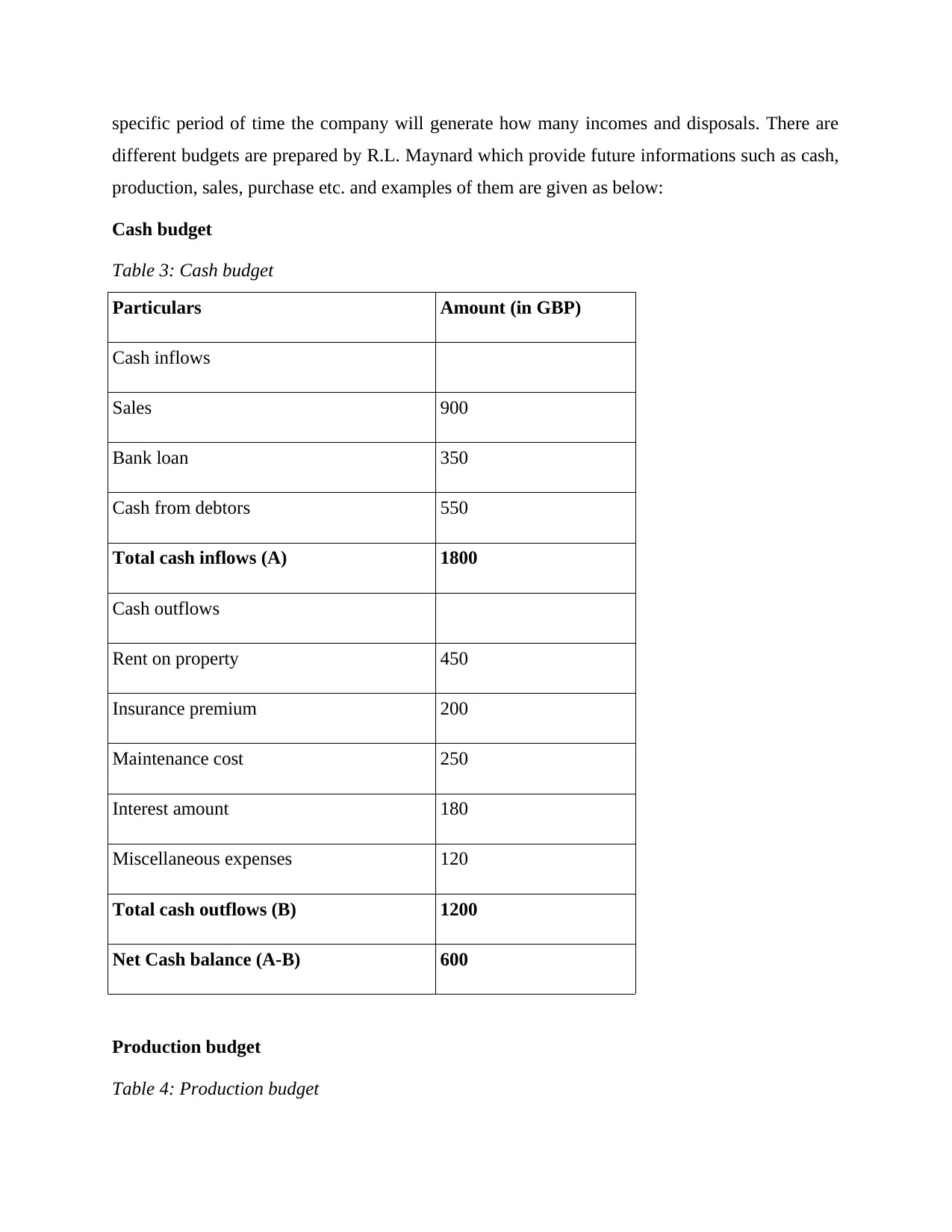

specific period of time the company will generate how many incomes and disposals. There are

different budgets are prepared by R.L. Maynard which provide future informations such as cash,

production, sales, purchase etc. and examples of them are given as below:

Cash budget

Table 3: Cash budget

Particulars Amount (in GBP)

Cash inflows

Sales 900

Bank loan 350

Cash from debtors 550

Total cash inflows (A) 1800

Cash outflows

Rent on property 450

Insurance premium 200

Maintenance cost 250

Interest amount 180

Miscellaneous expenses 120

Total cash outflows (B) 1200

Net Cash balance (A-B) 600

Production budget

Table 4: Production budget

different budgets are prepared by R.L. Maynard which provide future informations such as cash,

production, sales, purchase etc. and examples of them are given as below:

Cash budget

Table 3: Cash budget

Particulars Amount (in GBP)

Cash inflows

Sales 900

Bank loan 350

Cash from debtors 550

Total cash inflows (A) 1800

Cash outflows

Rent on property 450

Insurance premium 200

Maintenance cost 250

Interest amount 180

Miscellaneous expenses 120

Total cash outflows (B) 1200

Net Cash balance (A-B) 600

Production budget

Table 4: Production budget

Particulars Product Z

Estimated sales items 1350

Add: Desired stock at the end of month 130

Number of items required 1480

Less: Stock available at the beginning of month 50

Items required to produce 1430

Sales budget

Table 5: Sales budget

Particulars Product Z

Estimated sales items 1350

Selling price of each item 20

Total sales for next month 27000

Various advantages and limitations are given as below:

Advantages:

The R.L. Maynard able to make effective financial plan on the basis of monthly,

quarterly or yearly.

It helps to allocate financial resources to every organisational function in an adequate

manner.

By this management prepare effective business strategies for attract more number of

customers (Agarwal, R., 2016).

In addition to this, R.L. Maynard can know that which activity takes higher cost and

expenses.

Estimated sales items 1350

Add: Desired stock at the end of month 130

Number of items required 1480

Less: Stock available at the beginning of month 50

Items required to produce 1430

Sales budget

Table 5: Sales budget

Particulars Product Z

Estimated sales items 1350

Selling price of each item 20

Total sales for next month 27000

Various advantages and limitations are given as below:

Advantages:

The R.L. Maynard able to make effective financial plan on the basis of monthly,

quarterly or yearly.

It helps to allocate financial resources to every organisational function in an adequate

manner.

By this management prepare effective business strategies for attract more number of

customers (Agarwal, R., 2016).

In addition to this, R.L. Maynard can know that which activity takes higher cost and

expenses.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.