Management Accounting Report: Oshodi PLC, Decision Making, and Systems

VerifiedAdded on 2021/02/19

|19

|6045

|219

Report

AI Summary

This report provides a detailed analysis of management accounting practices within the context of Oshodi PLC, a manufacturing company specializing in JOJO fruit juice. The report explores the significance of management accounting in decision-making, covering various management accounting systems such as inventory management, job costing, cost accounting, and price optimization systems. It examines different methods used for management accounting reporting, including budgeting reports, cost accounting reports, inventory management reports, job costing reports, and accounts receivable reports. The report also delves into the advantages and disadvantages of planning tools for budgetary control, and it compares how organizations are adopting management accounting systems to respond to financial problems. The integration of these systems and reporting methods, and their impact on organizational success are evaluated, providing a comprehensive understanding of how management accounting contributes to financial success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting System......................................................................................3

P2. Different Methods used for Management Accounting Reporting....................................5

M1. Benefits of Management Accounting System and their Application..............................6

D1. Integration of Management Accounting Systems and Management Accounting Reporting

in Organisational Context.......................................................................................................7

TASK 2 ...........................................................................................................................................7

P3) Cost analysis through income statement..........................................................................7

M2: Range of management accounting techniques ...............................................................9

D2: Interpretation of data ....................................................................................................10

TASK 3..........................................................................................................................................10

P4: Advantages and Disadvantages of Planning tools for budgetary control .....................10

M3: Analysation of planning tools.......................................................................................12

TASK 4..........................................................................................................................................12

P5: Comparison on how organisations are adopting management accounting system........12

M4: Management accounting lead to organisation to financial success .............................14

D3: Evaluation of planning tools and its significance in organisational success.................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION ..........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Management accounting System......................................................................................3

P2. Different Methods used for Management Accounting Reporting....................................5

M1. Benefits of Management Accounting System and their Application..............................6

D1. Integration of Management Accounting Systems and Management Accounting Reporting

in Organisational Context.......................................................................................................7

TASK 2 ...........................................................................................................................................7

P3) Cost analysis through income statement..........................................................................7

M2: Range of management accounting techniques ...............................................................9

D2: Interpretation of data ....................................................................................................10

TASK 3..........................................................................................................................................10

P4: Advantages and Disadvantages of Planning tools for budgetary control .....................10

M3: Analysation of planning tools.......................................................................................12

TASK 4..........................................................................................................................................12

P5: Comparison on how organisations are adopting management accounting system........12

M4: Management accounting lead to organisation to financial success .............................14

D3: Evaluation of planning tools and its significance in organisational success.................15

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting refers to a tool or technique which is utilised by managers of

various business entities for measuring, monitoring, analysing, planning, and controlling all the

tasks and activities for acquiring sustainable success. It helps members of management team to

develop strategic decisions to accomplish specific tasks on time and achieve predetermined

objectives of an organisation (Usenko and et. al., 2018). It helps internal shareholders to analyse

performance of company and form decision making. Oshodi PLC is a manufacturing company

which is specialised in production of JOJO fruit juice that covers all age bracket. This report

covers the importance of management accounting in decision making process and the need of

different types of management accounting system. It also covers various processes that is used

for management accounting reporting. In this project, cost is calculated by using appropriate

tools of cost analysis for preparing an income statement with the help of marginal and absorption

costs is covered. Further it covers advantages and disadvantages of various kinds of planning

tools that is used for budgetary control in production of JOJO fruit juice. The way in which

organisations is adapting and using management accounting system for responding to various

financial problems is also covered in this project.

TASK 1

P1: Management accounting System

Management Accounting- It can defined as a tool and technique that is adopted by

managers of different organisations in order to monitor, analyse, control, measure and plan

performance of a company for the purpose of generating higher profits in future. With the help of

management accounting, managers utilises provision of information related to accounting for

attaining better performance of certain control functions (Management Accounting – Meaning,

2019.). It helps members of an organisation to take strategic decisions for accomplishing

different tasks and activities.

Management Accounting System- These are the tools that is used to analyse actual

status of an organisation for attaining its predetermined objectives. It helps in guiding internal

shareholders to determine probability of a company which will enhance overall performance of

an enterprise. Oshodi PLC firm that is specialise in producing JOJO fruit juice should keep an

Management accounting refers to a tool or technique which is utilised by managers of

various business entities for measuring, monitoring, analysing, planning, and controlling all the

tasks and activities for acquiring sustainable success. It helps members of management team to

develop strategic decisions to accomplish specific tasks on time and achieve predetermined

objectives of an organisation (Usenko and et. al., 2018). It helps internal shareholders to analyse

performance of company and form decision making. Oshodi PLC is a manufacturing company

which is specialised in production of JOJO fruit juice that covers all age bracket. This report

covers the importance of management accounting in decision making process and the need of

different types of management accounting system. It also covers various processes that is used

for management accounting reporting. In this project, cost is calculated by using appropriate

tools of cost analysis for preparing an income statement with the help of marginal and absorption

costs is covered. Further it covers advantages and disadvantages of various kinds of planning

tools that is used for budgetary control in production of JOJO fruit juice. The way in which

organisations is adapting and using management accounting system for responding to various

financial problems is also covered in this project.

TASK 1

P1: Management accounting System

Management Accounting- It can defined as a tool and technique that is adopted by

managers of different organisations in order to monitor, analyse, control, measure and plan

performance of a company for the purpose of generating higher profits in future. With the help of

management accounting, managers utilises provision of information related to accounting for

attaining better performance of certain control functions (Management Accounting – Meaning,

2019.). It helps members of an organisation to take strategic decisions for accomplishing

different tasks and activities.

Management Accounting System- These are the tools that is used to analyse actual

status of an organisation for attaining its predetermined objectives. It helps in guiding internal

shareholders to determine probability of a company which will enhance overall performance of

an enterprise. Oshodi PLC firm that is specialise in producing JOJO fruit juice should keep an

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

eye on each activity and will use different types of management accounting system tools which

are-

Inventory management system- It can be defined as an method that is used to control,

oversee ordering, and storing of certain components which is applied by corporation in

production procedure of goods sold by it. This system is usually utilised in companies that are

related to engineering and manufacturing procedures (Adler, 2018). It is a combination of

application of barcode printers, scanners, mobile devices, and desktop software to streamline this

system like consumables, supplies, stock, and goods. It can be defined as an practice to control

and oversee quantities of finished goods for the purpose of sale. It will help managers to have

insight and make them capable to make sufficient decisions of inventory. This method is used by

managers Oshodi for controlling and overseeing ordering of JOJO fruit juice.

Job Costing System- It can be defined as an system that is used for allocating

manufacturing costs to an individual item of product. It applies for a purpose of checking if

products of an organisation are different from each other or not. It includes practice of

accumulating data upon costs that is related to a particular job. The information that is needed in

order to submit cost data towards consumer under a contract under which costs are refunded.

This method can be used by Oshodi in order to allocate manufacturing costs to JOJO fruit juice

to determine cost of every job separately.

Cost Accounting System- It can be defined as a framework which is applied by

corporation for approximating cost of different products for controlling costs, inventory

valuation, and profitability analysis (Phang, Siti-Nabiha and Jalaludin, 2019). In this system,

allocation of cost is performed which is based upon traditional accounting system and activity

based costing system. Its basic aim and purpose is to capture production cost of company. It

helps to measure and record costs individually and then compare inputs results to actual output

for assisting management of an organisation in measuring and evaluating overall financial

position of a company. Oshodi PLC can utilise cost accounting system to determine current

financial position of it.

Price Optimisation System- This system of management accounting is used by many

organisations for setting up adequate pricing for its products and services in order to attract large

number of customers towards an enterprise. This model is used to alter pricing for segmenting

customers by stimulating the way in which targeted customers respond to changes in price. It

are-

Inventory management system- It can be defined as an method that is used to control,

oversee ordering, and storing of certain components which is applied by corporation in

production procedure of goods sold by it. This system is usually utilised in companies that are

related to engineering and manufacturing procedures (Adler, 2018). It is a combination of

application of barcode printers, scanners, mobile devices, and desktop software to streamline this

system like consumables, supplies, stock, and goods. It can be defined as an practice to control

and oversee quantities of finished goods for the purpose of sale. It will help managers to have

insight and make them capable to make sufficient decisions of inventory. This method is used by

managers Oshodi for controlling and overseeing ordering of JOJO fruit juice.

Job Costing System- It can be defined as an system that is used for allocating

manufacturing costs to an individual item of product. It applies for a purpose of checking if

products of an organisation are different from each other or not. It includes practice of

accumulating data upon costs that is related to a particular job. The information that is needed in

order to submit cost data towards consumer under a contract under which costs are refunded.

This method can be used by Oshodi in order to allocate manufacturing costs to JOJO fruit juice

to determine cost of every job separately.

Cost Accounting System- It can be defined as a framework which is applied by

corporation for approximating cost of different products for controlling costs, inventory

valuation, and profitability analysis (Phang, Siti-Nabiha and Jalaludin, 2019). In this system,

allocation of cost is performed which is based upon traditional accounting system and activity

based costing system. Its basic aim and purpose is to capture production cost of company. It

helps to measure and record costs individually and then compare inputs results to actual output

for assisting management of an organisation in measuring and evaluating overall financial

position of a company. Oshodi PLC can utilise cost accounting system to determine current

financial position of it.

Price Optimisation System- This system of management accounting is used by many

organisations for setting up adequate pricing for its products and services in order to attract large

number of customers towards an enterprise. This model is used to alter pricing for segmenting

customers by stimulating the way in which targeted customers respond to changes in price. It

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

helps in demand forecasting, developing pricing and promotional strategies, controlling

inventory levels and result in customer satisfaction. Oshodi PLC can take this model into action

to meet overall expectations of customers by setting appropriate prices to its various juices of

JOJO fruit juice and by providing juice of good quality.

Essentials requirements of management accounting system

Management accounting plays a key role in helping management of a business in

controlling the entity. It helps the organisation by providing them financial decisions by

appropriate planning, controlling and analysing business conditions. There are some necessary

requirements of management accounting system which can be discussed as follows-

Management Style- The management style followed by an organisation affects its

overall management accounting system as it determines how the data and information is

processed to achieve business objectives. It can use autocratic style, in which information

obtained is delivered to those people who take decisions. It can also use democratic style,

in which information is passed to those people who are involved in decision making

procedure.

Organisation Structure- It determines range of information needed by manager and

their extent to which information is provided by them. Organisation can use either

functional or flat structured. By using functional structure, manager uses financial

information up to the extent of its own functions. When enterprise uses flat structure,

managers are given wide report range on basis of which decisions are taken.

Information- These are vital requirement for management accounting system as it is the

lifeblood of important managerial decisions. Management need to take decisions

regarding what information is required for taking business decisions. It should be taken

into consideration that from which sources information should be collected from internal

or external.

P2. Different Methods used for Management Accounting Reporting

Management Accounting Reporting means analysing and recording of business activities

for internal company use in order to increase productivity and efficiency. Management

Accounting Reporting includes the details of company's available cash, the present state of

company's accounts payable , receivable and also the recent generation of sales revenue. The

inventory levels and result in customer satisfaction. Oshodi PLC can take this model into action

to meet overall expectations of customers by setting appropriate prices to its various juices of

JOJO fruit juice and by providing juice of good quality.

Essentials requirements of management accounting system

Management accounting plays a key role in helping management of a business in

controlling the entity. It helps the organisation by providing them financial decisions by

appropriate planning, controlling and analysing business conditions. There are some necessary

requirements of management accounting system which can be discussed as follows-

Management Style- The management style followed by an organisation affects its

overall management accounting system as it determines how the data and information is

processed to achieve business objectives. It can use autocratic style, in which information

obtained is delivered to those people who take decisions. It can also use democratic style,

in which information is passed to those people who are involved in decision making

procedure.

Organisation Structure- It determines range of information needed by manager and

their extent to which information is provided by them. Organisation can use either

functional or flat structured. By using functional structure, manager uses financial

information up to the extent of its own functions. When enterprise uses flat structure,

managers are given wide report range on basis of which decisions are taken.

Information- These are vital requirement for management accounting system as it is the

lifeblood of important managerial decisions. Management need to take decisions

regarding what information is required for taking business decisions. It should be taken

into consideration that from which sources information should be collected from internal

or external.

P2. Different Methods used for Management Accounting Reporting

Management Accounting Reporting means analysing and recording of business activities

for internal company use in order to increase productivity and efficiency. Management

Accounting Reporting includes the details of company's available cash, the present state of

company's accounts payable , receivable and also the recent generation of sales revenue. The

management accounting reports are confidential and used for the internal purposes only which

helps the enterprises to run more effectively (Hoozée and Mitchel, 2018).

The different methods used in preparation of Management Accounting Reporting are mentioned

below :

Budgeting Reports – A budget report is an internal report used by management to

compare the estimated projections with the actual performance for a certain period of time.

Budgeting reports helps Oshodi PLC manufacturing business owners to understand and control

the costs across the organization. By evaluating the expenses in prior years for the production of

JOJO fruit juice , it becomes possible to estimate the budgets for manufacturing JOJO fruit juice

for the following year and with the help of those budget reports the company can find places to

cut costs. The budget reports are also used by Oshodi PLC to provide incentives to their

employees which motivates them to achieve the set objectives.

Cost Accounting Reports - Cost accounting report is a statement of all the costs like raw

material, labour , overhead and any additional costs that is involved in manufacturing process.

The profit margins can be estimated and monitored by Oshodi PLC through cost accounting

reports which helps them to get a clear picture of all the costs that is indulged in the production

of JOJO fruit juice (Booth, 2018)(Alamri, 2019). For the better optimization of resources among

all the departments , Cost accounting reports provides an exact understanding of all the expenses

included in manufacturing of JOJO fruit juice and also distinct the fixed cost and variable cost.

Inventory Management Reports – This type of reports provide a encompassing account

of the stock in hand or supply of various goods in the organisation. These reports can track the

accurate stock holdings of the Oshodi PLC which can help them to take accurate business

decisions. The organization can loose the power over profits if they don't have good control over

the stocks because it is essential for the survival in the market. The detailed information of all

raw materials, semi finished goods and finished products can control the wastage of extra

production or procurement of materials.

Job Costing Reports – These reports are preoccupied with identifying the costs,

expenditure , and profits included in each activity separately. Job cost reports can help Oshodi

PLC to evaluate the most profitable areas of the business which is contributing maximum of all

tasks (Scott, 2019). Job Costing reports help company to correct the areas of wastage before

those expenditures go out of control. Oshodi PLC Company is using job costing processes to

helps the enterprises to run more effectively (Hoozée and Mitchel, 2018).

The different methods used in preparation of Management Accounting Reporting are mentioned

below :

Budgeting Reports – A budget report is an internal report used by management to

compare the estimated projections with the actual performance for a certain period of time.

Budgeting reports helps Oshodi PLC manufacturing business owners to understand and control

the costs across the organization. By evaluating the expenses in prior years for the production of

JOJO fruit juice , it becomes possible to estimate the budgets for manufacturing JOJO fruit juice

for the following year and with the help of those budget reports the company can find places to

cut costs. The budget reports are also used by Oshodi PLC to provide incentives to their

employees which motivates them to achieve the set objectives.

Cost Accounting Reports - Cost accounting report is a statement of all the costs like raw

material, labour , overhead and any additional costs that is involved in manufacturing process.

The profit margins can be estimated and monitored by Oshodi PLC through cost accounting

reports which helps them to get a clear picture of all the costs that is indulged in the production

of JOJO fruit juice (Booth, 2018)(Alamri, 2019). For the better optimization of resources among

all the departments , Cost accounting reports provides an exact understanding of all the expenses

included in manufacturing of JOJO fruit juice and also distinct the fixed cost and variable cost.

Inventory Management Reports – This type of reports provide a encompassing account

of the stock in hand or supply of various goods in the organisation. These reports can track the

accurate stock holdings of the Oshodi PLC which can help them to take accurate business

decisions. The organization can loose the power over profits if they don't have good control over

the stocks because it is essential for the survival in the market. The detailed information of all

raw materials, semi finished goods and finished products can control the wastage of extra

production or procurement of materials.

Job Costing Reports – These reports are preoccupied with identifying the costs,

expenditure , and profits included in each activity separately. Job cost reports can help Oshodi

PLC to evaluate the most profitable areas of the business which is contributing maximum of all

tasks (Scott, 2019). Job Costing reports help company to correct the areas of wastage before

those expenditures go out of control. Oshodi PLC Company is using job costing processes to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

track the right costs to deliver a job, so they can charge right prices to achieve the profit margins

targeted. This reporting gives insight to manufactures that their JOJO fruit juice is the most

profitable area among all the other businesses.

Account Receivable Reports – This type of reports includes all details including

collection period of money, credit policies or terms & conditions of credits that company has

given. The company should monitored their collection period time to time for its flexibility and

accuracy. It also allocates the difficulties associated with the Oshodi PLC credit process. Also,

account receivable reports helps to tighten the credit policies of company as to maintain a good

liquidity for the production process. This reports ensure that Oshodi PLC can minimise their bad

debts and keep required liquidity for the shortcomings.

M1. Benefits of Management Accounting System and their Application

Management Accounting

System

Benefits Application

Inventory Management System It helps Oshodi to provide

knowledge of flow of materials,

equipments to effectively

coordinate the internal activities

(Quinn and Oliveira, 2018).

Oshodi can make good

decisions for ordering of raw

materials used for producing

JOJO fruit juice.

Job Costing System Oshodi PLC can measure the

profitability of each job

individually using job costing

system.

The company can determine

cost of each task separately in

manufacturing of JOJO fruit

juice.

Cost Accounting System It separates all fixed costs and

variable costs.

The company can determine

current situation of funds using

Cost Accounting System.

Price Optimisation System The large number of customers

can be attracted due to

satisfactory pricing.

Oshodi can attract large number

of customers by offering good

quality Juices at affordable

targeted. This reporting gives insight to manufactures that their JOJO fruit juice is the most

profitable area among all the other businesses.

Account Receivable Reports – This type of reports includes all details including

collection period of money, credit policies or terms & conditions of credits that company has

given. The company should monitored their collection period time to time for its flexibility and

accuracy. It also allocates the difficulties associated with the Oshodi PLC credit process. Also,

account receivable reports helps to tighten the credit policies of company as to maintain a good

liquidity for the production process. This reports ensure that Oshodi PLC can minimise their bad

debts and keep required liquidity for the shortcomings.

M1. Benefits of Management Accounting System and their Application

Management Accounting

System

Benefits Application

Inventory Management System It helps Oshodi to provide

knowledge of flow of materials,

equipments to effectively

coordinate the internal activities

(Quinn and Oliveira, 2018).

Oshodi can make good

decisions for ordering of raw

materials used for producing

JOJO fruit juice.

Job Costing System Oshodi PLC can measure the

profitability of each job

individually using job costing

system.

The company can determine

cost of each task separately in

manufacturing of JOJO fruit

juice.

Cost Accounting System It separates all fixed costs and

variable costs.

The company can determine

current situation of funds using

Cost Accounting System.

Price Optimisation System The large number of customers

can be attracted due to

satisfactory pricing.

Oshodi can attract large number

of customers by offering good

quality Juices at affordable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

prices.

D1. Integration of Management Accounting Systems and Management Accounting Reporting in

Organisational Context

Management Accounting system is used to analyse the real situation of company due to

which they can achieve its present objectives. Management Accounting Reporting are based on

these systems which helps to convince the investors on the sustainability of the business. The

interrelationship between management accounting systems and accounting management

reporting can make a path for Oshodi PLC to focus on targeted results and objectives in a better

way (Pavlatos and Kostakis, 2018). The process of accounting reports and accounting systems

has becomes a routine that sticks throughout the lifetime of organization.

TASK 2

P3) Cost analysis through income statement

Marginal costing – under this method of costing, fixed cost for a completely period of

time is written off against the contribution and only the variable cost is charged to units of cost.

Marginal cost refer to additional cost involved in manufacturing an extra unit of output. Under

this method variable cost is taken as product cost and fixed cost is assumed as period cost which

remain unaffected by level of activity (Lawson, 2018). The income statement of Oshodi

organisation to ascertain profit through marginal coasting is provided below:

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

D1. Integration of Management Accounting Systems and Management Accounting Reporting in

Organisational Context

Management Accounting system is used to analyse the real situation of company due to

which they can achieve its present objectives. Management Accounting Reporting are based on

these systems which helps to convince the investors on the sustainability of the business. The

interrelationship between management accounting systems and accounting management

reporting can make a path for Oshodi PLC to focus on targeted results and objectives in a better

way (Pavlatos and Kostakis, 2018). The process of accounting reports and accounting systems

has becomes a routine that sticks throughout the lifetime of organization.

TASK 2

P3) Cost analysis through income statement

Marginal costing – under this method of costing, fixed cost for a completely period of

time is written off against the contribution and only the variable cost is charged to units of cost.

Marginal cost refer to additional cost involved in manufacturing an extra unit of output. Under

this method variable cost is taken as product cost and fixed cost is assumed as period cost which

remain unaffected by level of activity (Lawson, 2018). The income statement of Oshodi

organisation to ascertain profit through marginal coasting is provided below:

Particulars November (£)

Sales 50 500000

Less: Cost of sales

Direct Material Costs 18 -180000

Direct Labour costs 4 -40000

Variable Production Overheads 3 -30000

Contribution 250000

Less:

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing – under this method all manufacturing costs are absorbed or assigned

to units produced. Cost of direct materials, direct labour, variable manufacturing cost and fixed

manufacturing cost all make a part of cost of finished product (Walker, Johnson and Fleischman,

2018). It is mainly required to meet the needs of external financial reporting and also for income

tax reporting. Ascertainment of profit and income statement of Oshodi organisation through

absorption costing method is given below:

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 61000

Particulars December (£)

Sales 50 600000

Less: cost of sale

Direct Material Costs 18 -216000

Direct Labour costs 4 -48000

Variable Production Overheads 3 -36000

Contribution 300000

Less:

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Fixed production overheads -99000

Net Profit 101000

Absorption costing – under this method all manufacturing costs are absorbed or assigned

to units produced. Cost of direct materials, direct labour, variable manufacturing cost and fixed

manufacturing cost all make a part of cost of finished product (Walker, Johnson and Fleischman,

2018). It is mainly required to meet the needs of external financial reporting and also for income

tax reporting. Ascertainment of profit and income statement of Oshodi organisation through

absorption costing method is given below:

Particulars November (£)

Sales 50 500000

Less: Cost of sales -340000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

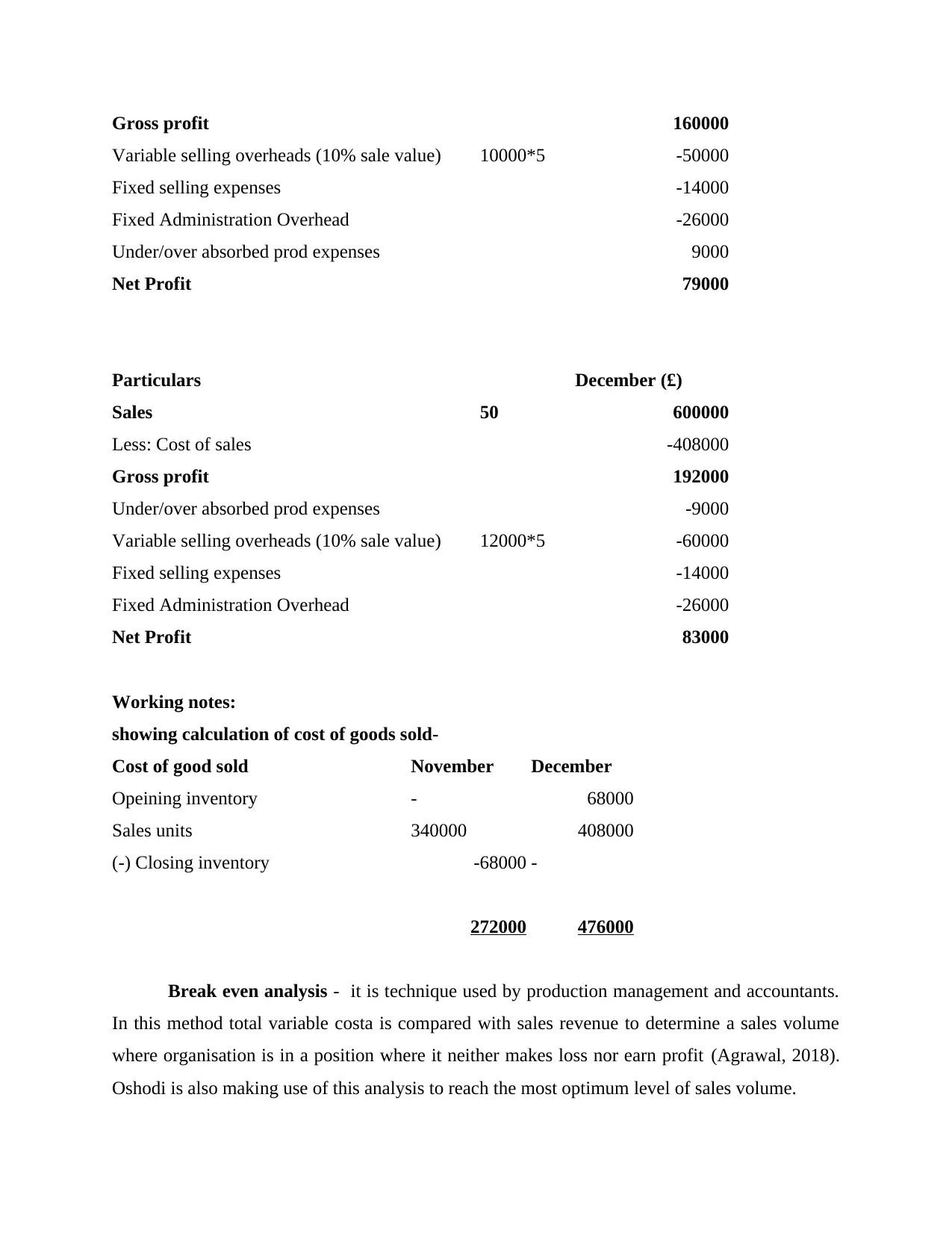

Gross profit 160000

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars December (£)

Sales 50 600000

Less: Cost of sales -408000

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working notes:

showing calculation of cost of goods sold-

Cost of good sold November December

Opeining inventory - 68000

Sales units 340000 408000

(-) Closing inventory -68000 -

272000 476000

Break even analysis - it is technique used by production management and accountants.

In this method total variable costa is compared with sales revenue to determine a sales volume

where organisation is in a position where it neither makes loss nor earn profit (Agrawal, 2018).

Oshodi is also making use of this analysis to reach the most optimum level of sales volume.

Variable selling overheads (10% sale value) 10000*5 -50000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Under/over absorbed prod expenses 9000

Net Profit 79000

Particulars December (£)

Sales 50 600000

Less: Cost of sales -408000

Gross profit 192000

Under/over absorbed prod expenses -9000

Variable selling overheads (10% sale value) 12000*5 -60000

Fixed selling expenses -14000

Fixed Administration Overhead -26000

Net Profit 83000

Working notes:

showing calculation of cost of goods sold-

Cost of good sold November December

Opeining inventory - 68000

Sales units 340000 408000

(-) Closing inventory -68000 -

272000 476000

Break even analysis - it is technique used by production management and accountants.

In this method total variable costa is compared with sales revenue to determine a sales volume

where organisation is in a position where it neither makes loss nor earn profit (Agrawal, 2018).

Oshodi is also making use of this analysis to reach the most optimum level of sales volume.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M2: Range of management accounting techniques

There are many management accounting techniques which are issued for preparing and

producing financial reporting documents some are explained below which can also be used by

Oshodi organisation for better presentation and recording of its document :

Standard costing – it is mainly used by manufacturer to calculate different variances

between actual cost of goods and the cost that is estimated as actual cost of goods produced. This

estimated cost of production is termed as standard cost which is integrated in manufacturer's

budget.

Historical cost – it this accounting system price of asset in balance sheet is based on its

nominal or original cost. This is used for calculation of value of assets under Generally Accepted

Accounting Principal (GAAP).

D2: Interpretation of data

From the above numericals and calumniation it is clear that net profit earned by Oshodi

organisation under Marginal costing is more as compared with absorption costing (Monden,

2019). Marginal costing is better for Oshodi organisation as it helps in more clear determination

and calculation of price and assist manger in taking very critical and vital decisions.

TASK 3

P4: Advantages and Disadvantages of Planning tools for budgetary control

Budget- For the purpose of recording estimated incomes and expenses, business

enterprises generates budgets for a specific period of time. By using budget, managers compare

actual and budgeted figures for analysing whether company is performing in a good manner or

not. It is also helpful to formulate financial objectives for making information available related to

actual funds and their availability for determining business activities. Oshodi PLC can use

budget to make estimates about its performance and to maintain a summary of planned revenues

for future. It aims at reducing inappropriate allocation of of budgets to different departments to

reduce the possibility of financial challenges.

Budgetary Control- This method is utilised for controlling overspending and excess of

budget. It can be defined as an process for setting up financial and performance objectives with

budgets, compare it with actual results, and adjust the performance in accordance. In Oshodi

PLC, budgetary control can be used by this enterprise to allocate specific monetary funds and

There are many management accounting techniques which are issued for preparing and

producing financial reporting documents some are explained below which can also be used by

Oshodi organisation for better presentation and recording of its document :

Standard costing – it is mainly used by manufacturer to calculate different variances

between actual cost of goods and the cost that is estimated as actual cost of goods produced. This

estimated cost of production is termed as standard cost which is integrated in manufacturer's

budget.

Historical cost – it this accounting system price of asset in balance sheet is based on its

nominal or original cost. This is used for calculation of value of assets under Generally Accepted

Accounting Principal (GAAP).

D2: Interpretation of data

From the above numericals and calumniation it is clear that net profit earned by Oshodi

organisation under Marginal costing is more as compared with absorption costing (Monden,

2019). Marginal costing is better for Oshodi organisation as it helps in more clear determination

and calculation of price and assist manger in taking very critical and vital decisions.

TASK 3

P4: Advantages and Disadvantages of Planning tools for budgetary control

Budget- For the purpose of recording estimated incomes and expenses, business

enterprises generates budgets for a specific period of time. By using budget, managers compare

actual and budgeted figures for analysing whether company is performing in a good manner or

not. It is also helpful to formulate financial objectives for making information available related to

actual funds and their availability for determining business activities. Oshodi PLC can use

budget to make estimates about its performance and to maintain a summary of planned revenues

for future. It aims at reducing inappropriate allocation of of budgets to different departments to

reduce the possibility of financial challenges.

Budgetary Control- This method is utilised for controlling overspending and excess of

budget. It can be defined as an process for setting up financial and performance objectives with

budgets, compare it with actual results, and adjust the performance in accordance. In Oshodi

PLC, budgetary control can be used by this enterprise to allocate specific monetary funds and

resources towards different functional and operational departments in accordance with its

requirements so that company can achieve its overall objectives (Zheng and Feng, 2018).

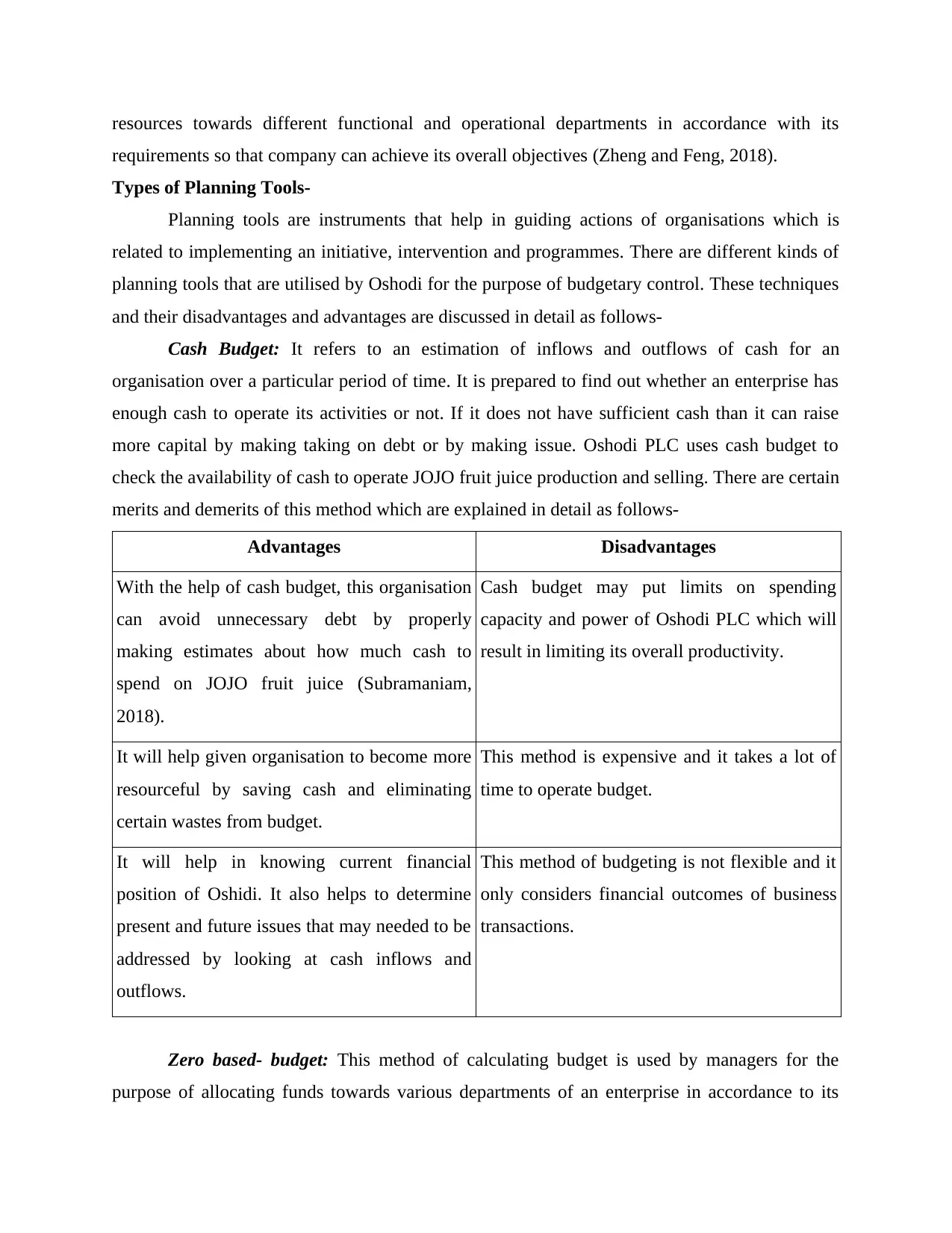

Types of Planning Tools-

Planning tools are instruments that help in guiding actions of organisations which is

related to implementing an initiative, intervention and programmes. There are different kinds of

planning tools that are utilised by Oshodi for the purpose of budgetary control. These techniques

and their disadvantages and advantages are discussed in detail as follows-

Cash Budget: It refers to an estimation of inflows and outflows of cash for an

organisation over a particular period of time. It is prepared to find out whether an enterprise has

enough cash to operate its activities or not. If it does not have sufficient cash than it can raise

more capital by making taking on debt or by making issue. Oshodi PLC uses cash budget to

check the availability of cash to operate JOJO fruit juice production and selling. There are certain

merits and demerits of this method which are explained in detail as follows-

Advantages Disadvantages

With the help of cash budget, this organisation

can avoid unnecessary debt by properly

making estimates about how much cash to

spend on JOJO fruit juice (Subramaniam,

2018).

Cash budget may put limits on spending

capacity and power of Oshodi PLC which will

result in limiting its overall productivity.

It will help given organisation to become more

resourceful by saving cash and eliminating

certain wastes from budget.

This method is expensive and it takes a lot of

time to operate budget.

It will help in knowing current financial

position of Oshidi. It also helps to determine

present and future issues that may needed to be

addressed by looking at cash inflows and

outflows.

This method of budgeting is not flexible and it

only considers financial outcomes of business

transactions.

Zero based- budget: This method of calculating budget is used by managers for the

purpose of allocating funds towards various departments of an enterprise in accordance to its

requirements so that company can achieve its overall objectives (Zheng and Feng, 2018).

Types of Planning Tools-

Planning tools are instruments that help in guiding actions of organisations which is

related to implementing an initiative, intervention and programmes. There are different kinds of

planning tools that are utilised by Oshodi for the purpose of budgetary control. These techniques

and their disadvantages and advantages are discussed in detail as follows-

Cash Budget: It refers to an estimation of inflows and outflows of cash for an

organisation over a particular period of time. It is prepared to find out whether an enterprise has

enough cash to operate its activities or not. If it does not have sufficient cash than it can raise

more capital by making taking on debt or by making issue. Oshodi PLC uses cash budget to

check the availability of cash to operate JOJO fruit juice production and selling. There are certain

merits and demerits of this method which are explained in detail as follows-

Advantages Disadvantages

With the help of cash budget, this organisation

can avoid unnecessary debt by properly

making estimates about how much cash to

spend on JOJO fruit juice (Subramaniam,

2018).

Cash budget may put limits on spending

capacity and power of Oshodi PLC which will

result in limiting its overall productivity.

It will help given organisation to become more

resourceful by saving cash and eliminating

certain wastes from budget.

This method is expensive and it takes a lot of

time to operate budget.

It will help in knowing current financial

position of Oshidi. It also helps to determine

present and future issues that may needed to be

addressed by looking at cash inflows and

outflows.

This method of budgeting is not flexible and it

only considers financial outcomes of business

transactions.

Zero based- budget: This method of calculating budget is used by managers for the

purpose of allocating funds towards various departments of an enterprise in accordance to its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.