Analysis of Management Accounting Systems at Sollatek

VerifiedAdded on 2020/10/22

|15

|5225

|491

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and their applications within Sollatek, a manufacturer of valves and tubes. It examines various aspects, including cost accounting, inventory management, price optimization, and job costing, highlighting their roles in planning, organizing, controlling, and decision-making. The report delves into the benefits of different management accounting systems, such as cost accounting's role in profitability analysis and inventory management's contribution to efficient stock control. Furthermore, it analyzes different reporting methods like performance reporting, inventory management reporting, account receivable reporting, and job cost reporting. The report showcases how Sollatek utilizes these systems and reporting methods to improve its financial performance and respond to financial problems, including the calculation of costs using marginal and absorption costing techniques. Finally, the report highlights the advantages and disadvantages of budgetary control and planning tools used in budgetary control and planning tools used in budgetary control.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Management accounting reporting and its types..................................................................3

M1. Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................5

TASK 2............................................................................................................................................5

P3. Calculation of cost using an appropriate technique..............................................................5

D2: Data interpretation................................................................................................................7

TASK 3............................................................................................................................................7

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages..............................................................................................................................7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and its types of management accounting systems........................1

P2. Management accounting reporting and its types..................................................................3

M1. Evaluate the benefits of management accounting system and its applications...................4

D1. Management accounting system and its reporting within organisation process..................5

TASK 2............................................................................................................................................5

P3. Calculation of cost using an appropriate technique..............................................................5

D2: Data interpretation................................................................................................................7

TASK 3............................................................................................................................................7

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages..............................................................................................................................7

M3: Uses and applications of planning tools for preparing and forecasting budgets.................9

TASK 4..........................................................................................................................................10

P5: Responses of management accounting system to deal with financial problems................10

M4: Management accounting lead organisation to sustainable success in responding to

financial problems.....................................................................................................................12

D3: Planning tools respond appropriately to resolve financial problems.................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an approach of analysing accounting information and set

guidelines that are useful in recording financial transaction of the company. The main objective

of management accounting is assistance in planning and future policies formulation. Sollatek is a

manufacturer of valves and tubes situated in Slough, United Kingdom. Company manufacture a

large range of voltage protection, solar products and LED lights.

In this report, company follows various management accounting systems and methods

used for reporting. Cost and profit of product is determine using costing techniques which helps

in preparing income statement. Company evaluate various planning tools used for budgetary

control. It also adopt management accounting systems to respond to financial problems (rabner,

and Moers, 2013).

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting plays a vital role in managerial functions like planning,

organising, controlling and decision making that are performed by managers. It is a core process

where employers manage with their subordinates by introducing a set of specific objectives.

These goals are important for both the company and employee strive to achieve in coming future.

Management accounting systems are confidential internal statements that assist managers

in decision making and identifying ways to run the company more efficiently. Sollatek use

management accounting system such as cost accounting, inventory management, price

optimisation and job costing for evaluating its process of working. The information of these

systems used in all departments of a company such as finance, information technology, HR,

marketing, operations and sales. Various management accounting systems are explained below:

Cost Accounting System: It is a framework used by company in estimating their product

cost for profitability analysis, cost control and product valuation (Padovani, Orelli and Young,

2014). Cost of raw material, work in progress and finished goods are estimated under this system

for the purpose of preparing income statement. Sollatek use this method for calculating the

accurate cost of synthetic rubber which is necessary for profitability operations. Company must

know that their products are profitable or not. This is only possible when it estimate correct cost

of it's product in manufacturing process.

1

Management accounting is an approach of analysing accounting information and set

guidelines that are useful in recording financial transaction of the company. The main objective

of management accounting is assistance in planning and future policies formulation. Sollatek is a

manufacturer of valves and tubes situated in Slough, United Kingdom. Company manufacture a

large range of voltage protection, solar products and LED lights.

In this report, company follows various management accounting systems and methods

used for reporting. Cost and profit of product is determine using costing techniques which helps

in preparing income statement. Company evaluate various planning tools used for budgetary

control. It also adopt management accounting systems to respond to financial problems (rabner,

and Moers, 2013).

TASK 1

P1. Management accounting and its types of management accounting systems

Management accounting plays a vital role in managerial functions like planning,

organising, controlling and decision making that are performed by managers. It is a core process

where employers manage with their subordinates by introducing a set of specific objectives.

These goals are important for both the company and employee strive to achieve in coming future.

Management accounting systems are confidential internal statements that assist managers

in decision making and identifying ways to run the company more efficiently. Sollatek use

management accounting system such as cost accounting, inventory management, price

optimisation and job costing for evaluating its process of working. The information of these

systems used in all departments of a company such as finance, information technology, HR,

marketing, operations and sales. Various management accounting systems are explained below:

Cost Accounting System: It is a framework used by company in estimating their product

cost for profitability analysis, cost control and product valuation (Padovani, Orelli and Young,

2014). Cost of raw material, work in progress and finished goods are estimated under this system

for the purpose of preparing income statement. Sollatek use this method for calculating the

accurate cost of synthetic rubber which is necessary for profitability operations. Company must

know that their products are profitable or not. This is only possible when it estimate correct cost

of it's product in manufacturing process.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price Optimisation System: It is a system used to tailor product pricing for customers of

different segments that evaluate how targeted customers will respond to variation in price. This

system assist in accumulating the demand of product at various level of prices. Sollatek use price

optimisation system to identify the best price of its product that customers are willingness to pay.

Company set a price of its product which it supply to clients. These price strategies are reviewed

from time to time to make an improvement in pricing policies which helps in achieving

maximum efficiency and decision making.

Inventory Management System: This system is designed for manufacturers that track

the flows of inventory at different stages of production and distribution. This system includes a

detailed information about inventory in opening stock, work in process and finished goods or in

storage warehouse. The features of this system are asset tracking, service management, product

identification, inventory optimization etc. Sollatek use this system for tracking the inflow or

outflow of raw material that management wants to supply their product as per the demand of

suppliers and customers. Inventory management system also reduces the improper management

of inventory by controlling and managing product future demand. It increases product efficiency

and helps in inventory optimisation and demand forecasting (Ball, 2013).

Job cost System: This system is used to determine costs at a small unit level where

company record the costs of manufacturing instead of process. Cost of direct raw material,

labour, applied overhead combines to find a total job cost. Sollatek is valves & tubes

manufacturer and distributor to clients. It follows job cost system to accumulate the cost of each

job, maintaining information that is much related to its operations. Company identify the costs

and revenues of its products at different levels of manufacturing and distributing. Each job is

different and company wants to perform its job as per the requirement of customers and

suppliers. This system also assist in evaluating the actual cost and performance of each jobs.

2

different segments that evaluate how targeted customers will respond to variation in price. This

system assist in accumulating the demand of product at various level of prices. Sollatek use price

optimisation system to identify the best price of its product that customers are willingness to pay.

Company set a price of its product which it supply to clients. These price strategies are reviewed

from time to time to make an improvement in pricing policies which helps in achieving

maximum efficiency and decision making.

Inventory Management System: This system is designed for manufacturers that track

the flows of inventory at different stages of production and distribution. This system includes a

detailed information about inventory in opening stock, work in process and finished goods or in

storage warehouse. The features of this system are asset tracking, service management, product

identification, inventory optimization etc. Sollatek use this system for tracking the inflow or

outflow of raw material that management wants to supply their product as per the demand of

suppliers and customers. Inventory management system also reduces the improper management

of inventory by controlling and managing product future demand. It increases product efficiency

and helps in inventory optimisation and demand forecasting (Ball, 2013).

Job cost System: This system is used to determine costs at a small unit level where

company record the costs of manufacturing instead of process. Cost of direct raw material,

labour, applied overhead combines to find a total job cost. Sollatek is valves & tubes

manufacturer and distributor to clients. It follows job cost system to accumulate the cost of each

job, maintaining information that is much related to its operations. Company identify the costs

and revenues of its products at different levels of manufacturing and distributing. Each job is

different and company wants to perform its job as per the requirement of customers and

suppliers. This system also assist in evaluating the actual cost and performance of each jobs.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Management accounting reporting and its types

Management accounting reporting is a tool used for understanding the current status of

company i.e. what is going on in business activities quantitatively (Mahesha and Akash, 2013.).

It includes collection of data which give useful information about company's operations. The

various mode of reporting are written statements, graphical and oral reports. A good reporting

system carries information to different levels of administration. It assist in qualitative decision

making which consist of quality of informations that are useful for stakeholders. Performance,

inventory management, account receivables and job cost reporting are the various methods of

management accounting reporting that are follow by Sollatek Information of these reporting

systems must be clear and easily understand by both internal and external stakeholders. It also

help in preparing effective management accounting reports for the company. Various types of

management accounting reporting are described below:

Performance Reporting: This reporting method consist of periodic performance which

is essential for each stakeholder. It is a report on the performance of something which is

routinely made by company. It shows the amount management is spending on activities to make

its performance more effective and useful. It is a detailed statement includes project information

about collection and distribution of product (Performance Reporting, 2018). This reporting

system set certain guidelines that managers must follow in determining defaults and resolves

them on time. Sollatek use this reporting system for evaluating its continuous progress by

comparing present performance with past. Analyse the variation, if any in production and

distribution of its present performance. It also help in future progress of company at various level

of management and prepare a attractive performance report for Sollatek

Inventory Management Reporting: This method improves the management of

inventory by showing proper stock movement in an organisation. Company use this reporting

method for tracking its cost of goods sold, avoid under and overselling and even prepare custom

reports. Sollatek follow inventory management reporting technique for evaluating the status of

raw material, analyse and integrate product at different levels of production and distribution.

This technique helps in identifying product demand, profitability, sales etc. and assess the

difference between accounting and product information. This reporting tool help in dealing with

under and overselling of product. It also create a effective report with details information about

current inventory levels and amount of stock committed to sales order.

3

Management accounting reporting is a tool used for understanding the current status of

company i.e. what is going on in business activities quantitatively (Mahesha and Akash, 2013.).

It includes collection of data which give useful information about company's operations. The

various mode of reporting are written statements, graphical and oral reports. A good reporting

system carries information to different levels of administration. It assist in qualitative decision

making which consist of quality of informations that are useful for stakeholders. Performance,

inventory management, account receivables and job cost reporting are the various methods of

management accounting reporting that are follow by Sollatek Information of these reporting

systems must be clear and easily understand by both internal and external stakeholders. It also

help in preparing effective management accounting reports for the company. Various types of

management accounting reporting are described below:

Performance Reporting: This reporting method consist of periodic performance which

is essential for each stakeholder. It is a report on the performance of something which is

routinely made by company. It shows the amount management is spending on activities to make

its performance more effective and useful. It is a detailed statement includes project information

about collection and distribution of product (Performance Reporting, 2018). This reporting

system set certain guidelines that managers must follow in determining defaults and resolves

them on time. Sollatek use this reporting system for evaluating its continuous progress by

comparing present performance with past. Analyse the variation, if any in production and

distribution of its present performance. It also help in future progress of company at various level

of management and prepare a attractive performance report for Sollatek

Inventory Management Reporting: This method improves the management of

inventory by showing proper stock movement in an organisation. Company use this reporting

method for tracking its cost of goods sold, avoid under and overselling and even prepare custom

reports. Sollatek follow inventory management reporting technique for evaluating the status of

raw material, analyse and integrate product at different levels of production and distribution.

This technique helps in identifying product demand, profitability, sales etc. and assess the

difference between accounting and product information. This reporting tool help in dealing with

under and overselling of product. It also create a effective report with details information about

current inventory levels and amount of stock committed to sales order.

3

Account Receivable Reporting: In this reporting technique includes a date wise lists of

due customer invoices and unaccustomed credit memos. Account receivable report is the main

tool used by collections person of the department to determine invoices which are overdue for

payments. The aging report is used as a technique for estimating possible bad debts, that are then

used to revise the portion for doubtful accounts. Sollatek use this reporting tool for summarizing

and creating the list of customer's past or present dues. Company use this account receivable as a

collection tool which provide detailed information about average collection period. With the help

of this reporting system Sollatek determine the effectiveness in credit and collection process

(Chiarini, 2012).

Job Cost reporting: In this reporting technique company gets detailed information about

the total cost incurred in each job within a specific time period. Cost of material, labour and

overhead are included in job cost. Sollatek use job costing reporting because a proper job begins

with perfect cost estimates. With the help of this reporting technique company evaluate its raw

material, labour and overheads costs at various job levels. These costs appears clearly in this

reports. This is important to display accurate cost each job like manufacturing and distributing.

M1. Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It assist in identifying the production

cost at a specific volume of units.

Effective controlling technique helps

the management to achieve overall

profit (Gullkvist, 2013).

Price optimisation system It allocates resources efficiently.

With the help of effective pricing

policies company attracts more and

more customers.

Inventory management system It assist in determining the exact

amount of inventory that Sollatek need.

This system help in evaluating higher

4

due customer invoices and unaccustomed credit memos. Account receivable report is the main

tool used by collections person of the department to determine invoices which are overdue for

payments. The aging report is used as a technique for estimating possible bad debts, that are then

used to revise the portion for doubtful accounts. Sollatek use this reporting tool for summarizing

and creating the list of customer's past or present dues. Company use this account receivable as a

collection tool which provide detailed information about average collection period. With the help

of this reporting system Sollatek determine the effectiveness in credit and collection process

(Chiarini, 2012).

Job Cost reporting: In this reporting technique company gets detailed information about

the total cost incurred in each job within a specific time period. Cost of material, labour and

overhead are included in job cost. Sollatek use job costing reporting because a proper job begins

with perfect cost estimates. With the help of this reporting technique company evaluate its raw

material, labour and overheads costs at various job levels. These costs appears clearly in this

reports. This is important to display accurate cost each job like manufacturing and distributing.

M1. Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It assist in identifying the production

cost at a specific volume of units.

Effective controlling technique helps

the management to achieve overall

profit (Gullkvist, 2013).

Price optimisation system It allocates resources efficiently.

With the help of effective pricing

policies company attracts more and

more customers.

Inventory management system It assist in determining the exact

amount of inventory that Sollatek need.

This system help in evaluating higher

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

inventory turnover ratio.

Job costing system It provides information related to costs

in each job.

It is proper reporting tool which lead to

good results in the form of less costly

and more profitable.

D1. Management accounting system and its reporting within organisation process

Sollatek uses various management accounting systems and reporting methods that aid to

increase profit and improve its overall performance. It follow cost accounting system for

evaluating the accurate cost of rubber at time of manufacturing (Ahmad, 2012). Company set

certain rules and regulations regarding pricing policies to target new and existing customers

under price optimisation system. In inventory management system company track the flow of

inventory at different levels of production and this system helps in creating effective inventory

reports. Account receivable reporting system helps in identifying the amount due with customers

and collection tool aid in preparing correct report. With the help of job costing system company

create a detail report regarding job cost at each level of manufacturing and distribution.

TASK 2

P3. Calculation of cost using an appropriate technique

Cost: A monetary value that is needed to buy or make a particular product. In

accounting, the amount spend on raw material consumed, product production, labour hours,

equipments purchase etc. are costs of business activities. Sollatek want to fix correct cost of its

product in order to attract large scale of customers. The cost must be supportable by both

company and customers.

Marginal costing: This costing technique includes marginal cost i.e. change in total cost

of production for creating one extra unit of an item. It is the accounting system where variable

costs are charged to fixed costs and cost units of the period that are deducted against

contribution. Sollatek use marginal costing for determining marginal cost that charge to

additional unit of production.

Absorption costing: This costing tool refers to method of calculating product cost by

considering its indirect expenses as well as direct costs. Here all the manufacturing costs are

5

Job costing system It provides information related to costs

in each job.

It is proper reporting tool which lead to

good results in the form of less costly

and more profitable.

D1. Management accounting system and its reporting within organisation process

Sollatek uses various management accounting systems and reporting methods that aid to

increase profit and improve its overall performance. It follow cost accounting system for

evaluating the accurate cost of rubber at time of manufacturing (Ahmad, 2012). Company set

certain rules and regulations regarding pricing policies to target new and existing customers

under price optimisation system. In inventory management system company track the flow of

inventory at different levels of production and this system helps in creating effective inventory

reports. Account receivable reporting system helps in identifying the amount due with customers

and collection tool aid in preparing correct report. With the help of job costing system company

create a detail report regarding job cost at each level of manufacturing and distribution.

TASK 2

P3. Calculation of cost using an appropriate technique

Cost: A monetary value that is needed to buy or make a particular product. In

accounting, the amount spend on raw material consumed, product production, labour hours,

equipments purchase etc. are costs of business activities. Sollatek want to fix correct cost of its

product in order to attract large scale of customers. The cost must be supportable by both

company and customers.

Marginal costing: This costing technique includes marginal cost i.e. change in total cost

of production for creating one extra unit of an item. It is the accounting system where variable

costs are charged to fixed costs and cost units of the period that are deducted against

contribution. Sollatek use marginal costing for determining marginal cost that charge to

additional unit of production.

Absorption costing: This costing tool refers to method of calculating product cost by

considering its indirect expenses as well as direct costs. Here all the manufacturing costs are

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

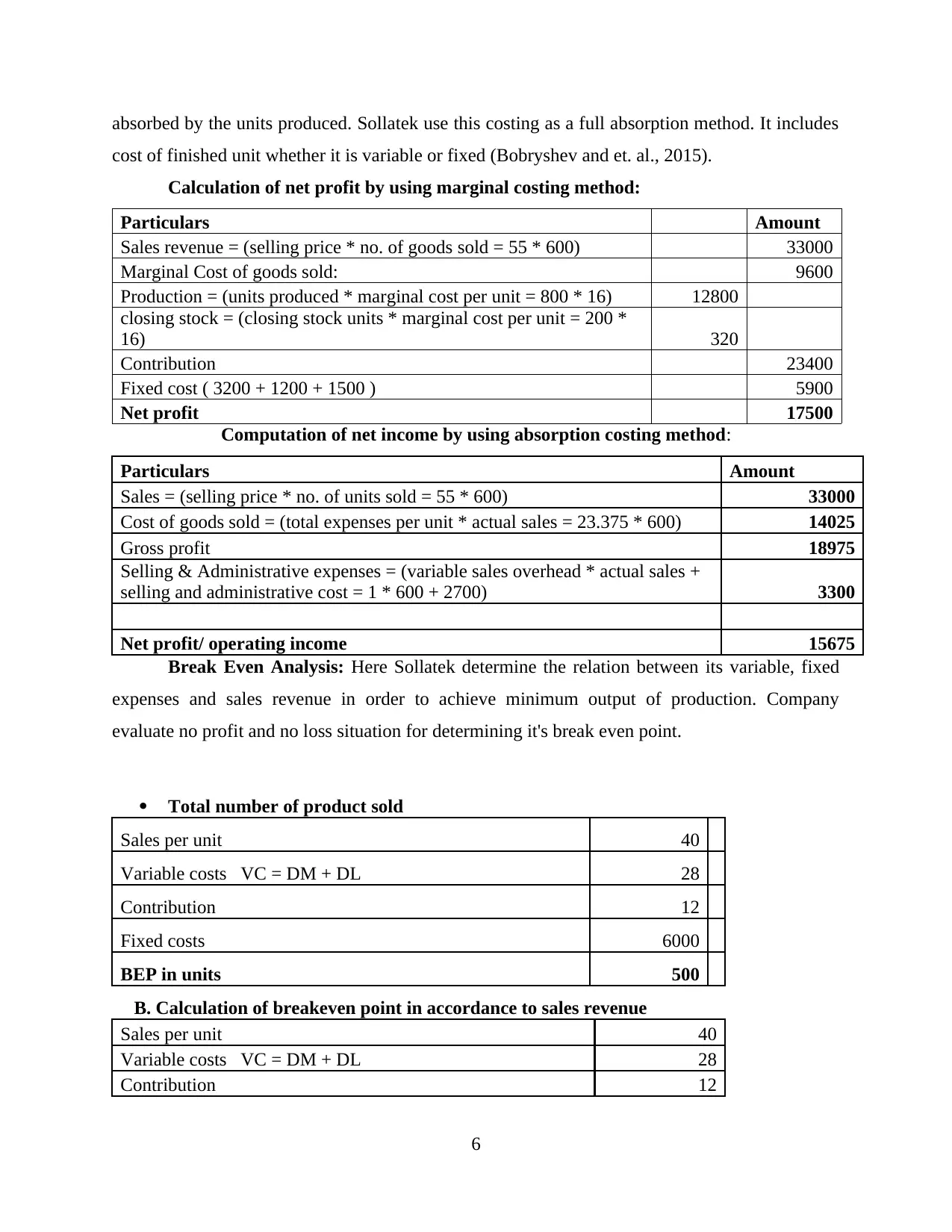

absorbed by the units produced. Sollatek use this costing as a full absorption method. It includes

cost of finished unit whether it is variable or fixed (Bobryshev and et. al., 2015).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 320

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break Even Analysis: Here Sollatek determine the relation between its variable, fixed

expenses and sales revenue in order to achieve minimum output of production. Company

evaluate no profit and no loss situation for determining it's break even point.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

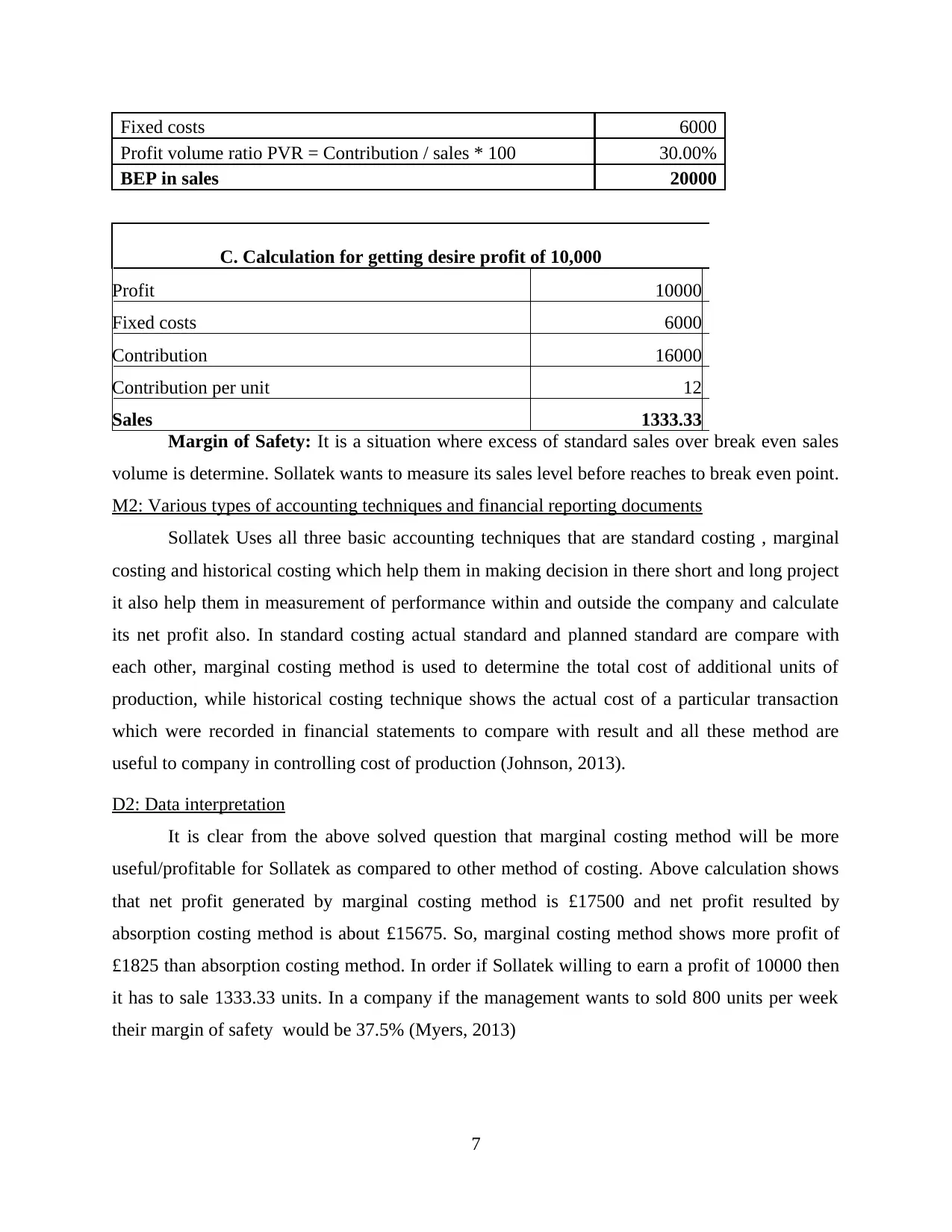

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

6

cost of finished unit whether it is variable or fixed (Bobryshev and et. al., 2015).

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 320

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break Even Analysis: Here Sollatek determine the relation between its variable, fixed

expenses and sales revenue in order to achieve minimum output of production. Company

evaluate no profit and no loss situation for determining it's break even point.

Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

6

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is a situation where excess of standard sales over break even sales

volume is determine. Sollatek wants to measure its sales level before reaches to break even point.

M2: Various types of accounting techniques and financial reporting documents

Sollatek Uses all three basic accounting techniques that are standard costing , marginal

costing and historical costing which help them in making decision in there short and long project

it also help them in measurement of performance within and outside the company and calculate

its net profit also. In standard costing actual standard and planned standard are compare with

each other, marginal costing method is used to determine the total cost of additional units of

production, while historical costing technique shows the actual cost of a particular transaction

which were recorded in financial statements to compare with result and all these method are

useful to company in controlling cost of production (Johnson, 2013).

D2: Data interpretation

It is clear from the above solved question that marginal costing method will be more

useful/profitable for Sollatek as compared to other method of costing. Above calculation shows

that net profit generated by marginal costing method is £17500 and net profit resulted by

absorption costing method is about £15675. So, marginal costing method shows more profit of

£1825 than absorption costing method. In order if Sollatek willing to earn a profit of 10000 then

it has to sale 1333.33 units. In a company if the management wants to sold 800 units per week

their margin of safety would be 37.5% (Myers, 2013)

7

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

C. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of Safety: It is a situation where excess of standard sales over break even sales

volume is determine. Sollatek wants to measure its sales level before reaches to break even point.

M2: Various types of accounting techniques and financial reporting documents

Sollatek Uses all three basic accounting techniques that are standard costing , marginal

costing and historical costing which help them in making decision in there short and long project

it also help them in measurement of performance within and outside the company and calculate

its net profit also. In standard costing actual standard and planned standard are compare with

each other, marginal costing method is used to determine the total cost of additional units of

production, while historical costing technique shows the actual cost of a particular transaction

which were recorded in financial statements to compare with result and all these method are

useful to company in controlling cost of production (Johnson, 2013).

D2: Data interpretation

It is clear from the above solved question that marginal costing method will be more

useful/profitable for Sollatek as compared to other method of costing. Above calculation shows

that net profit generated by marginal costing method is £17500 and net profit resulted by

absorption costing method is about £15675. So, marginal costing method shows more profit of

£1825 than absorption costing method. In order if Sollatek willing to earn a profit of 10000 then

it has to sale 1333.33 units. In a company if the management wants to sold 800 units per week

their margin of safety would be 37.5% (Myers, 2013)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages

Budgetary control : The process under which financial and performance based goal are

set in references with the budget. This system of management help Sollatek managers to

compare all income and expenditure for a year with the budgeted income and expenditure,it help

to compare the actual performance of their employee with the budgeted performance. Budgetary-

control help company to identify that predefined plans/budget are being followed or not and if

there is any alteration required in those budget. Basically, it is used by Sollatek to plan and

control budgets related to production and sales.

Sollatek is a valves and tubes manufacturer and seller, so budgetary-control in these

company includes following like objective for sales and production are set at first, actual result

are recorded for sales and production then these record are compared with budgeted norms and if

required changes are done to increase sales and production of company (Schaltegger and Burritt,

2017). It help company in an advance planning of the money related function of the organisation.

Sollatek uses three planning tools for budgetary-control, that are as follows :

Forecasting tool: These tools are consider very useful in company, as it help to fore cast

future condition of the business or get the idea about future that how its business look like.

Sollatek use forecasting tool to predict future of its business depending upon its past

activities,past result and its current position in the market. Manager on their experience,

knowledge use these business tool to predict sales, form budget and study market. This tool has

many advantages and disadvantage to a company like Sollatek.

Advantages Disadvantages

Provides valuable informations to work

efficiently in condition, like increase in

demand , drop in sales.

It helps company to be more prepared

for any uncertainty happen in the

future.

It is a time consuming activity as

prediction involve accurate study of

data.

As these prediction are based on past

event it may led to outdated result.

8

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages

Budgetary control : The process under which financial and performance based goal are

set in references with the budget. This system of management help Sollatek managers to

compare all income and expenditure for a year with the budgeted income and expenditure,it help

to compare the actual performance of their employee with the budgeted performance. Budgetary-

control help company to identify that predefined plans/budget are being followed or not and if

there is any alteration required in those budget. Basically, it is used by Sollatek to plan and

control budgets related to production and sales.

Sollatek is a valves and tubes manufacturer and seller, so budgetary-control in these

company includes following like objective for sales and production are set at first, actual result

are recorded for sales and production then these record are compared with budgeted norms and if

required changes are done to increase sales and production of company (Schaltegger and Burritt,

2017). It help company in an advance planning of the money related function of the organisation.

Sollatek uses three planning tools for budgetary-control, that are as follows :

Forecasting tool: These tools are consider very useful in company, as it help to fore cast

future condition of the business or get the idea about future that how its business look like.

Sollatek use forecasting tool to predict future of its business depending upon its past

activities,past result and its current position in the market. Manager on their experience,

knowledge use these business tool to predict sales, form budget and study market. This tool has

many advantages and disadvantage to a company like Sollatek.

Advantages Disadvantages

Provides valuable informations to work

efficiently in condition, like increase in

demand , drop in sales.

It helps company to be more prepared

for any uncertainty happen in the

future.

It is a time consuming activity as

prediction involve accurate study of

data.

As these prediction are based on past

event it may led to outdated result.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contingency tools: These tools have a main aim to minimise the impact of a unexpected

and unwelcome events and develop a plan that how the business will run its normal operation

after those events (Innes and Mitchell, 1995) Sollatek use this tool to study the current market

trends, changes in the market trends, customer demand that might affect their business and form

a perfect “Plan B” to overcome this problem. It identify key risk, rank those risk and create a

proper contingency plan to resolve those risk to increase the efficiency of business. These tools

have many advantages and disadvantage to the company like:

Advantages Disadvantages

It helps to identify unwelcome events

and develop “Plan B” to solve those

events.

Play a key role to identify all possible

contingency that have an impact on

business.

It require lot of amount to be involved

on extensive planning.

It led to wrong formation of plan which

are never going to be used as those are

based on outdated result.

Scenario tools: It is consider one of the perfect tool in today's increasingly uncertain and

changing world. These tools are are largely focused on answering two question like, what could

happen in future and what would be the impact of event on business. It also analysis the changes

in the performance of business and its monetary factors. Sollatek uses these scenario to study the

efficiency of strategies and make plan under a range of favourable as well as unfavourable events

that might occur in future.

It develop the understanding of market

among the management, that what is to

be produced and how to sell (Reid and

Smith 2000).

It ease the work of manager to adopt

the best plan to overcome any

unfavourable event.

Scenario are totally based on

assumption and correlation that may be

wrong.

Time consuming tool as most of the

time management are involved

predicting future events.

9

and unwelcome events and develop a plan that how the business will run its normal operation

after those events (Innes and Mitchell, 1995) Sollatek use this tool to study the current market

trends, changes in the market trends, customer demand that might affect their business and form

a perfect “Plan B” to overcome this problem. It identify key risk, rank those risk and create a

proper contingency plan to resolve those risk to increase the efficiency of business. These tools

have many advantages and disadvantage to the company like:

Advantages Disadvantages

It helps to identify unwelcome events

and develop “Plan B” to solve those

events.

Play a key role to identify all possible

contingency that have an impact on

business.

It require lot of amount to be involved

on extensive planning.

It led to wrong formation of plan which

are never going to be used as those are

based on outdated result.

Scenario tools: It is consider one of the perfect tool in today's increasingly uncertain and

changing world. These tools are are largely focused on answering two question like, what could

happen in future and what would be the impact of event on business. It also analysis the changes

in the performance of business and its monetary factors. Sollatek uses these scenario to study the

efficiency of strategies and make plan under a range of favourable as well as unfavourable events

that might occur in future.

It develop the understanding of market

among the management, that what is to

be produced and how to sell (Reid and

Smith 2000).

It ease the work of manager to adopt

the best plan to overcome any

unfavourable event.

Scenario are totally based on

assumption and correlation that may be

wrong.

Time consuming tool as most of the

time management are involved

predicting future events.

9

M3: Uses and applications of planning tools for preparing and forecasting budgets

Planning tools are very useful for Sollatek which help them in formation of budget,

compare its performance and predict all possible risk that might effect its business. Company

uses all three planning tool, like forecasting tool that is useful in estimating future conditions like

demand of customer's towards their product, future risk etc. (Ter Bogt and Van Helden, 2000).

Contingency tool to analyse change in the market trends, prediction of unwelcome events and

develop plan B which is implemented to resolve these situations and maximize profit. Scenario

tool helps manager to get prepare for any risk that might occur in future. All these planning tool

help management of Sollatek to get straight information about the uncertain and it help manager

in formation of policies and decision making.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problem are consider to be a situation under which there is lack of enough

monetary resources in a company to run its business and day-to-day activities. They may also

not able to produce its product, pay salary to its employee's etc. Sollatek faces these financial

problem:

High debt level: Regular sales on credit basis may led to increase in debt level. Sollatek

faces these problem as many of its customer do not pay payment of time and it increase their

debt level.

Lack of budgeting and money management skills: Management of Sollatek is not able

to maintain proper amount of money to run their business as the lack the skill of money

management and budgeting.

Improper maintenance of records: Main reason of financial problem for Sollatek is

improper book keeping. Record handling department is not able to record all its transaction

related to income and expenditure.

More spending on promotion and coupons: To attract more number of customer

Sollatek spend lots of its income on promotion activity. As a result these activities are no able to

increase sale for the company and it face financial problem (Foster and Gupta, 1994).

10

Planning tools are very useful for Sollatek which help them in formation of budget,

compare its performance and predict all possible risk that might effect its business. Company

uses all three planning tool, like forecasting tool that is useful in estimating future conditions like

demand of customer's towards their product, future risk etc. (Ter Bogt and Van Helden, 2000).

Contingency tool to analyse change in the market trends, prediction of unwelcome events and

develop plan B which is implemented to resolve these situations and maximize profit. Scenario

tool helps manager to get prepare for any risk that might occur in future. All these planning tool

help management of Sollatek to get straight information about the uncertain and it help manager

in formation of policies and decision making.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problem are consider to be a situation under which there is lack of enough

monetary resources in a company to run its business and day-to-day activities. They may also

not able to produce its product, pay salary to its employee's etc. Sollatek faces these financial

problem:

High debt level: Regular sales on credit basis may led to increase in debt level. Sollatek

faces these problem as many of its customer do not pay payment of time and it increase their

debt level.

Lack of budgeting and money management skills: Management of Sollatek is not able

to maintain proper amount of money to run their business as the lack the skill of money

management and budgeting.

Improper maintenance of records: Main reason of financial problem for Sollatek is

improper book keeping. Record handling department is not able to record all its transaction

related to income and expenditure.

More spending on promotion and coupons: To attract more number of customer

Sollatek spend lots of its income on promotion activity. As a result these activities are no able to

increase sale for the company and it face financial problem (Foster and Gupta, 1994).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.