Management Accounting Report: PC Clothing Limited Case Study Analysis

VerifiedAdded on 2021/02/18

|18

|3831

|117

Report

AI Summary

This report delves into the realm of management accounting, exploring its various types, including financial, cost, and management accounting systems. It examines different methods used for management accounting reporting, such as account receivable aging reports, cost accounting reports, and inventory reports, alongside the purpose of financial statements like profit and loss accounts and balance sheets. The report then analyzes different management accounting systems, like price optimization and inventory management systems. Furthermore, it compares and contrasts absorption costing and marginal costing methods through case studies, preparing income statements for each. Finally, it explores the limitations and profits of planning tools, such as budgetary control and zero-based budgeting, providing a comprehensive overview of management accounting principles and practices, using PC Clothing Limited as a case study to illustrate real-world applications.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of content

INTRODUCTION

The MA is a kind of accounting which is associated with process of recording monetary

and non monetary activities of a business in a systematic way (Zarzycka, Dobroszek, Circa and

Almasan, 2017). Main purpose of recording these transactions is to prepare internal reports

which are essential for management department of companies. In current scenario, the role of

this accounting is becoming wider because it includes different accounting systems and reports

that play a significant part in activities of business. In report, variety of MAS and MA techniques

are demonstrated. As well as types of planning tools and role of MA in order to sort financial

problems are also mentioned. For better understanding of these aspects of MA PC clothing

limited company is chosen which is located at London, United Kingdom. The organisation deals

in manufacturing of vital range of cloths.

TASK 1

P1. Management accounting and its types.

The MA is a way of collecting and analysing monetary and non monetary information for

producing internal report.

Functions of management accounting systems -

Provide data – This is key function of management accounting that is related to gathering

all kind of data that occurs in businesses due to transaction.

Modify data – Another function of this accounting is to modifying the gathered data. In

other words, ignoring those information which is not linked with business activities.

Analyse and interprets data – In the management accounting, modified data is being used

to produce reports and statements which is being interpreted to take important decisions

(Evans and Tucker, 2015).

Qualitative and quantitative information- Under this accounting systems, qualitative and

quantitative information is included that are beneficial for companies in making plans &

policies.

Various kind of accounting systems -

The MA is a kind of accounting which is associated with process of recording monetary

and non monetary activities of a business in a systematic way (Zarzycka, Dobroszek, Circa and

Almasan, 2017). Main purpose of recording these transactions is to prepare internal reports

which are essential for management department of companies. In current scenario, the role of

this accounting is becoming wider because it includes different accounting systems and reports

that play a significant part in activities of business. In report, variety of MAS and MA techniques

are demonstrated. As well as types of planning tools and role of MA in order to sort financial

problems are also mentioned. For better understanding of these aspects of MA PC clothing

limited company is chosen which is located at London, United Kingdom. The organisation deals

in manufacturing of vital range of cloths.

TASK 1

P1. Management accounting and its types.

The MA is a way of collecting and analysing monetary and non monetary information for

producing internal report.

Functions of management accounting systems -

Provide data – This is key function of management accounting that is related to gathering

all kind of data that occurs in businesses due to transaction.

Modify data – Another function of this accounting is to modifying the gathered data. In

other words, ignoring those information which is not linked with business activities.

Analyse and interprets data – In the management accounting, modified data is being used

to produce reports and statements which is being interpreted to take important decisions

(Evans and Tucker, 2015).

Qualitative and quantitative information- Under this accounting systems, qualitative and

quantitative information is included that are beneficial for companies in making plans &

policies.

Various kind of accounting systems -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial accounting system – This is a systematic process of analysing financial

transaction of a business in order to prepare different financial statements. The prepared

financial statements are being presented to internal and external stakeholders. In this

accounting system, it is necessary to conduct auditing of all produced financial

statements so that their efficiency can be evaluated. In the above selected company, their

accountant prepare financial statements which are audited by auditor as per this

accounting. For example PC clothing company prepare the income statements to evaluate

their profitability and loss in end of year as accordance of this accounting.

Cost accounting system – This is a process of projection of futuristic cost and allocating

funds accordingly (Cohen, Karatzimas and Naoum, 2015). It helps to finance department

because they need it for proper use of available financial resources in a better way. Thus,

it is essentially needed in companies for controlling and reducing expenditure of different

kind of activities. For example in, PC clothing limited they are using this accounting

system for minimising the overall cost of activities and operations of clothing production.

Management accounting system – This is an accounting system which assists companies’

financial information and create reports for managers to take decisions. It is needed for

supporting in decision-making. It is so because prepared reports consist monetary and

non monetary information that are needed by managers. Like in above company, the

MAS supports them in taking decision about different activities and operations regards to

cloth manufacturing. For example use of price optimisation system of management

accounting leads to effectively price setting.

Tax accounting system – It is an accounting whose main objective is to managing overall

taxation activities. In this accounting, it is essential that companies must follow

prescribed rules and regulations when computing tax return. For example, there are

international taxations rules which are essential for companies to apply in process of

calculating tax rate. As well as the PC clothing limited computes tax at the end of year by

help of this accounting.

P2. Different methods used for management accounting reporting.

MA reporting – It can be defined as a process of preparing internal reports in order to

help board of directors in decision-making.

transaction of a business in order to prepare different financial statements. The prepared

financial statements are being presented to internal and external stakeholders. In this

accounting system, it is necessary to conduct auditing of all produced financial

statements so that their efficiency can be evaluated. In the above selected company, their

accountant prepare financial statements which are audited by auditor as per this

accounting. For example PC clothing company prepare the income statements to evaluate

their profitability and loss in end of year as accordance of this accounting.

Cost accounting system – This is a process of projection of futuristic cost and allocating

funds accordingly (Cohen, Karatzimas and Naoum, 2015). It helps to finance department

because they need it for proper use of available financial resources in a better way. Thus,

it is essentially needed in companies for controlling and reducing expenditure of different

kind of activities. For example in, PC clothing limited they are using this accounting

system for minimising the overall cost of activities and operations of clothing production.

Management accounting system – This is an accounting system which assists companies’

financial information and create reports for managers to take decisions. It is needed for

supporting in decision-making. It is so because prepared reports consist monetary and

non monetary information that are needed by managers. Like in above company, the

MAS supports them in taking decision about different activities and operations regards to

cloth manufacturing. For example use of price optimisation system of management

accounting leads to effectively price setting.

Tax accounting system – It is an accounting whose main objective is to managing overall

taxation activities. In this accounting, it is essential that companies must follow

prescribed rules and regulations when computing tax return. For example, there are

international taxations rules which are essential for companies to apply in process of

calculating tax rate. As well as the PC clothing limited computes tax at the end of year by

help of this accounting.

P2. Different methods used for management accounting reporting.

MA reporting – It can be defined as a process of preparing internal reports in order to

help board of directors in decision-making.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Types of MA reports :

Account receivable ageing report – This can be defined as a kind of report which contains

information about credit transaction made by company with customers or other parties

(Krause and Tse, 2016). By using this report, companies get aware about how much

amount is needed to be collect from debtors in market. The above PC clothing limited is

preparing this report with an objective to find out those debtors who are making delay in

payment even after pre-set date of payment.

Cost accounting report – In this, information about each and every activities cost is

included. By using this report, companies can estimate further time period cost. As well

as it becomes easy to assess which activities are resulting in higher cost in compare to last

accounting period. PC clothing company's accountant is preparing this report to aware

overall expenditure in an accounting time period.

Inventory report – In it, information of quantity of stored commodities in stores. With

the use of this report, production department becomes able to take corrective decisions

regards to manufacturing and purchasing. The above company is preparing this report in

order to produce cloths as per the stored quantity in warehouse.

Purpose of financial statements :

Profit and loss account – The main purpose of preparing profit and loss account by

companies to know about net profit at the end of financial year. By help of measured net

profit, rate of dividend is computed.

Balance sheet – Companies prepare balance sheet for checking the amount of net assets

and liabilities at the end of year.

Cash flow statement – This statement is prepared by companies with an objective of

assessing cash position. Under it, cash position is evaluated by help of three activities:

operating, financing and investing (Becker, Wald, Gessner and Gleich, 2015).

Cost of goods sold – It helps in providing information about total cost incurred in process

of selling products.

Types of MAS -

Account receivable ageing report – This can be defined as a kind of report which contains

information about credit transaction made by company with customers or other parties

(Krause and Tse, 2016). By using this report, companies get aware about how much

amount is needed to be collect from debtors in market. The above PC clothing limited is

preparing this report with an objective to find out those debtors who are making delay in

payment even after pre-set date of payment.

Cost accounting report – In this, information about each and every activities cost is

included. By using this report, companies can estimate further time period cost. As well

as it becomes easy to assess which activities are resulting in higher cost in compare to last

accounting period. PC clothing company's accountant is preparing this report to aware

overall expenditure in an accounting time period.

Inventory report – In it, information of quantity of stored commodities in stores. With

the use of this report, production department becomes able to take corrective decisions

regards to manufacturing and purchasing. The above company is preparing this report in

order to produce cloths as per the stored quantity in warehouse.

Purpose of financial statements :

Profit and loss account – The main purpose of preparing profit and loss account by

companies to know about net profit at the end of financial year. By help of measured net

profit, rate of dividend is computed.

Balance sheet – Companies prepare balance sheet for checking the amount of net assets

and liabilities at the end of year.

Cash flow statement – This statement is prepared by companies with an objective of

assessing cash position. Under it, cash position is evaluated by help of three activities:

operating, financing and investing (Becker, Wald, Gessner and Gleich, 2015).

Cost of goods sold – It helps in providing information about total cost incurred in process

of selling products.

Types of MAS -

Price optimisation system - This is a system which is assigned with process of guiding

companies' managers in order to set the price of products and services. Under this

accounting system, prices are set by gathering customers feedback on alternative prices

and demand in market. Hence, the price optimisation system is needed in companies for

keeping prices of products at level which is acceptable by all customers as well as

beneficial for company. Under the chosen company, PC clothing limited they implement

this accounting system which is helping them for setting price of their manufactured

cloths as per analysis of customers' feedback.

Inventory management system – This is a system which is applied by companies for

evaluating quantitative aspect of unprocessed material and prepared products (Khan and

Jain, 2018). This accounting system is being enabled in companies by coordination of

production department. It is so, as the production department acquires key information

from this accounting which becomes a basis for taking decision for operational activities.

In the aspect of PC clothing limited company, they are using this accounting system that

is helping them in effective management of processed and unprocessed material of cloth

manufacturing such as fibre, cotton, wool and many more. The above company is using

LIFO method for managing inventories in an effective manner.

Job costing system – This is an accounting system which is linked with process of

allocating and compile production cost of a particular unit. Basically, this accounting is

suitable for those business entities wherein wide range of products are produced. In

computes each produced unit's cost individually and becomes possible only by checking

number of job assigned in different operations.

TASK 2

P3 Income statement under absorption and marginal costing.

Absorption costing – This can be defined as a costing technique in that fixed and variable

costs are assigned as unit cost during preparation of income statement.

Marginal costing- Under this, fixed cost is taken as period cost and variable cost as per

unit cost in process of preparing income statement (da Silva, Llewellyn and Anderson-Gough,

2017).

companies' managers in order to set the price of products and services. Under this

accounting system, prices are set by gathering customers feedback on alternative prices

and demand in market. Hence, the price optimisation system is needed in companies for

keeping prices of products at level which is acceptable by all customers as well as

beneficial for company. Under the chosen company, PC clothing limited they implement

this accounting system which is helping them for setting price of their manufactured

cloths as per analysis of customers' feedback.

Inventory management system – This is a system which is applied by companies for

evaluating quantitative aspect of unprocessed material and prepared products (Khan and

Jain, 2018). This accounting system is being enabled in companies by coordination of

production department. It is so, as the production department acquires key information

from this accounting which becomes a basis for taking decision for operational activities.

In the aspect of PC clothing limited company, they are using this accounting system that

is helping them in effective management of processed and unprocessed material of cloth

manufacturing such as fibre, cotton, wool and many more. The above company is using

LIFO method for managing inventories in an effective manner.

Job costing system – This is an accounting system which is linked with process of

allocating and compile production cost of a particular unit. Basically, this accounting is

suitable for those business entities wherein wide range of products are produced. In

computes each produced unit's cost individually and becomes possible only by checking

number of job assigned in different operations.

TASK 2

P3 Income statement under absorption and marginal costing.

Absorption costing – This can be defined as a costing technique in that fixed and variable

costs are assigned as unit cost during preparation of income statement.

Marginal costing- Under this, fixed cost is taken as period cost and variable cost as per

unit cost in process of preparing income statement (da Silva, Llewellyn and Anderson-Gough,

2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

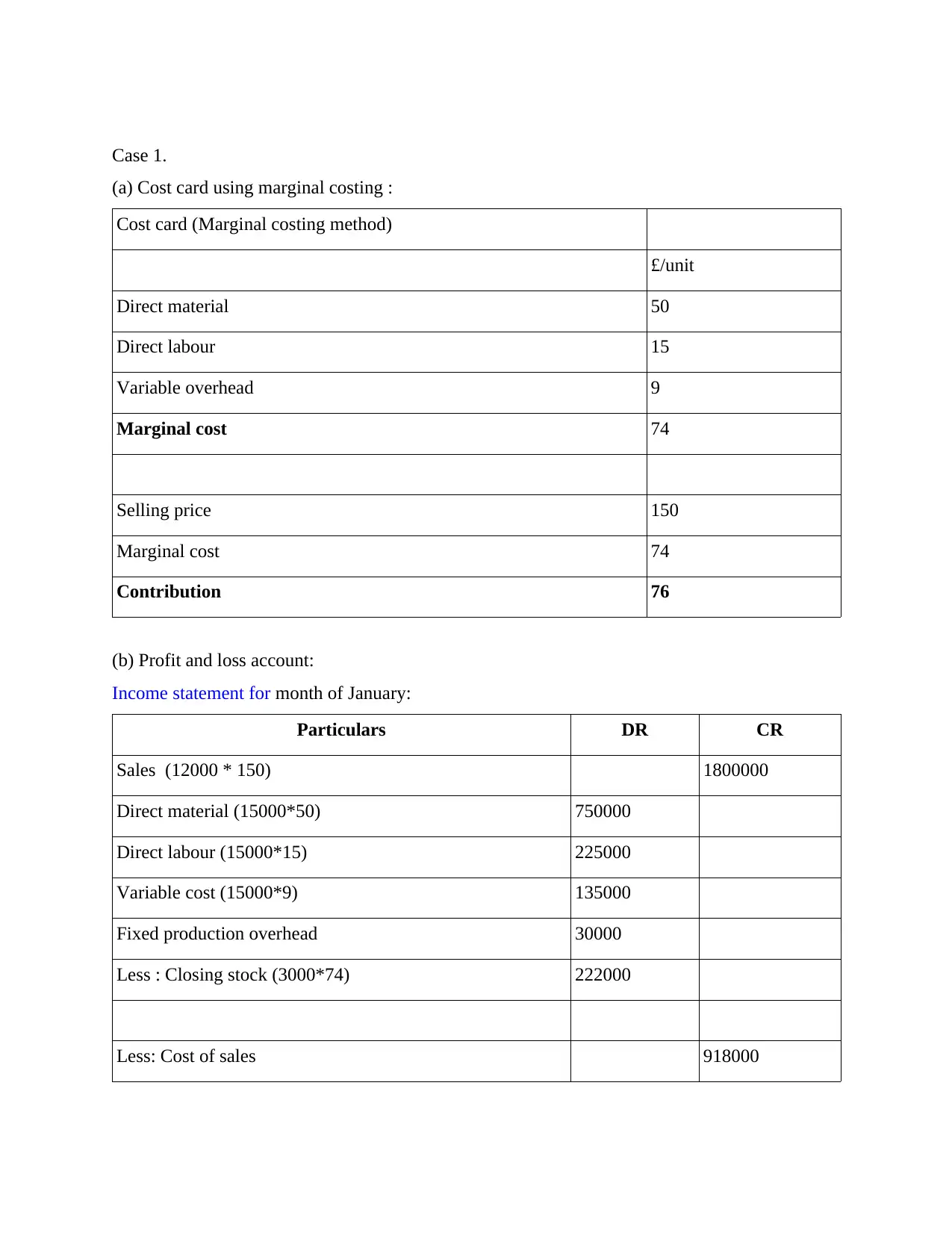

Case 1.

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 9

Marginal cost 74

Selling price 150

Marginal cost 74

Contribution 76

(b) Profit and loss account:

Income statement for month of January:

Particulars DR CR

Sales (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*9) 135000

Fixed production overhead 30000

Less : Closing stock (3000*74) 222000

Less: Cost of sales 918000

(a) Cost card using marginal costing :

Cost card (Marginal costing method)

£/unit

Direct material 50

Direct labour 15

Variable overhead 9

Marginal cost 74

Selling price 150

Marginal cost 74

Contribution 76

(b) Profit and loss account:

Income statement for month of January:

Particulars DR CR

Sales (12000 * 150) 1800000

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Variable cost (15000*9) 135000

Fixed production overhead 30000

Less : Closing stock (3000*74) 222000

Less: Cost of sales 918000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

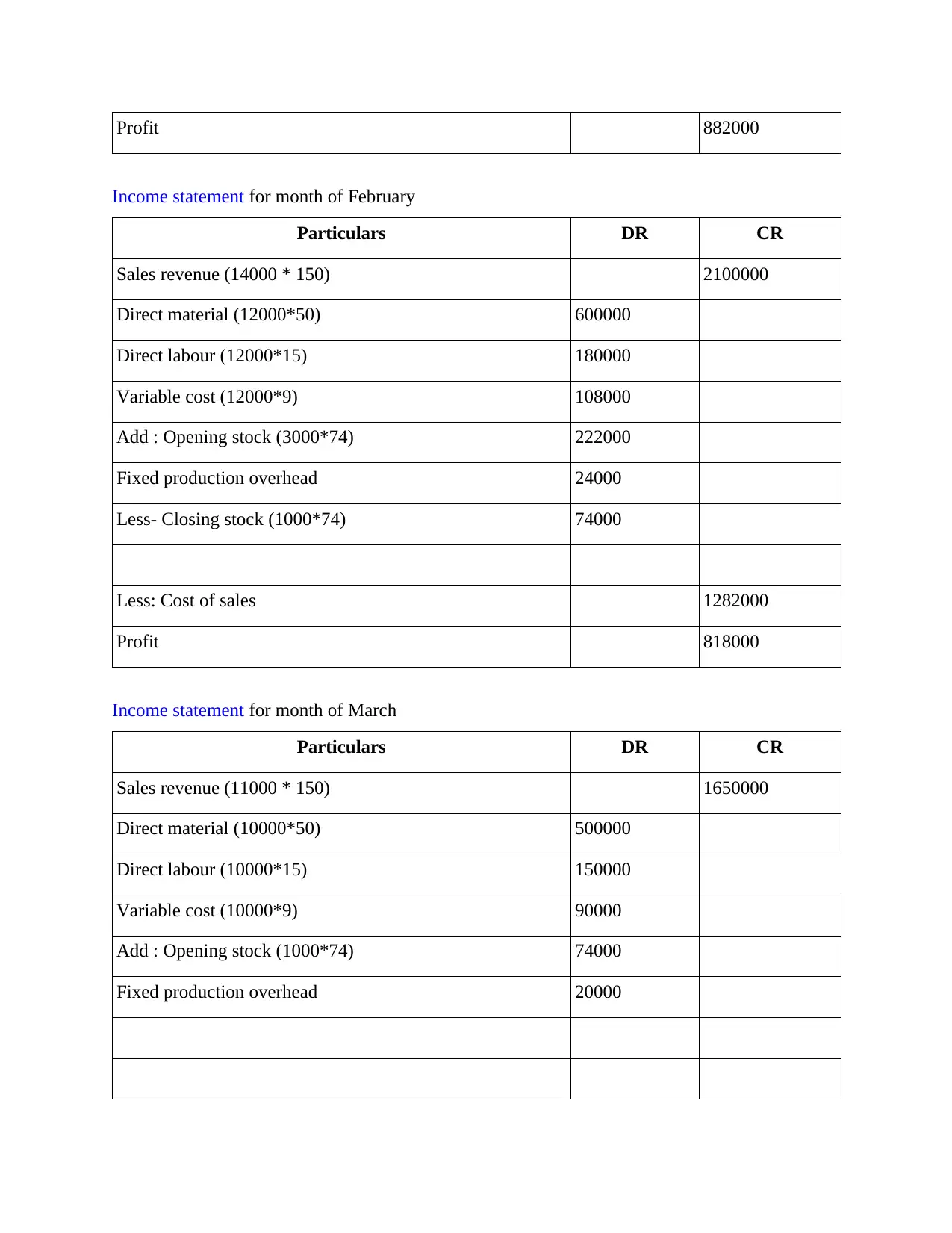

Profit 882000

Income statement for month of February

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*9) 108000

Add : Opening stock (3000*74) 222000

Fixed production overhead 24000

Less- Closing stock (1000*74) 74000

Less: Cost of sales 1282000

Profit 818000

Income statement for month of March

Particulars DR CR

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*9) 90000

Add : Opening stock (1000*74) 74000

Fixed production overhead 20000

Income statement for month of February

Particulars DR CR

Sales revenue (14000 * 150) 2100000

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Variable cost (12000*9) 108000

Add : Opening stock (3000*74) 222000

Fixed production overhead 24000

Less- Closing stock (1000*74) 74000

Less: Cost of sales 1282000

Profit 818000

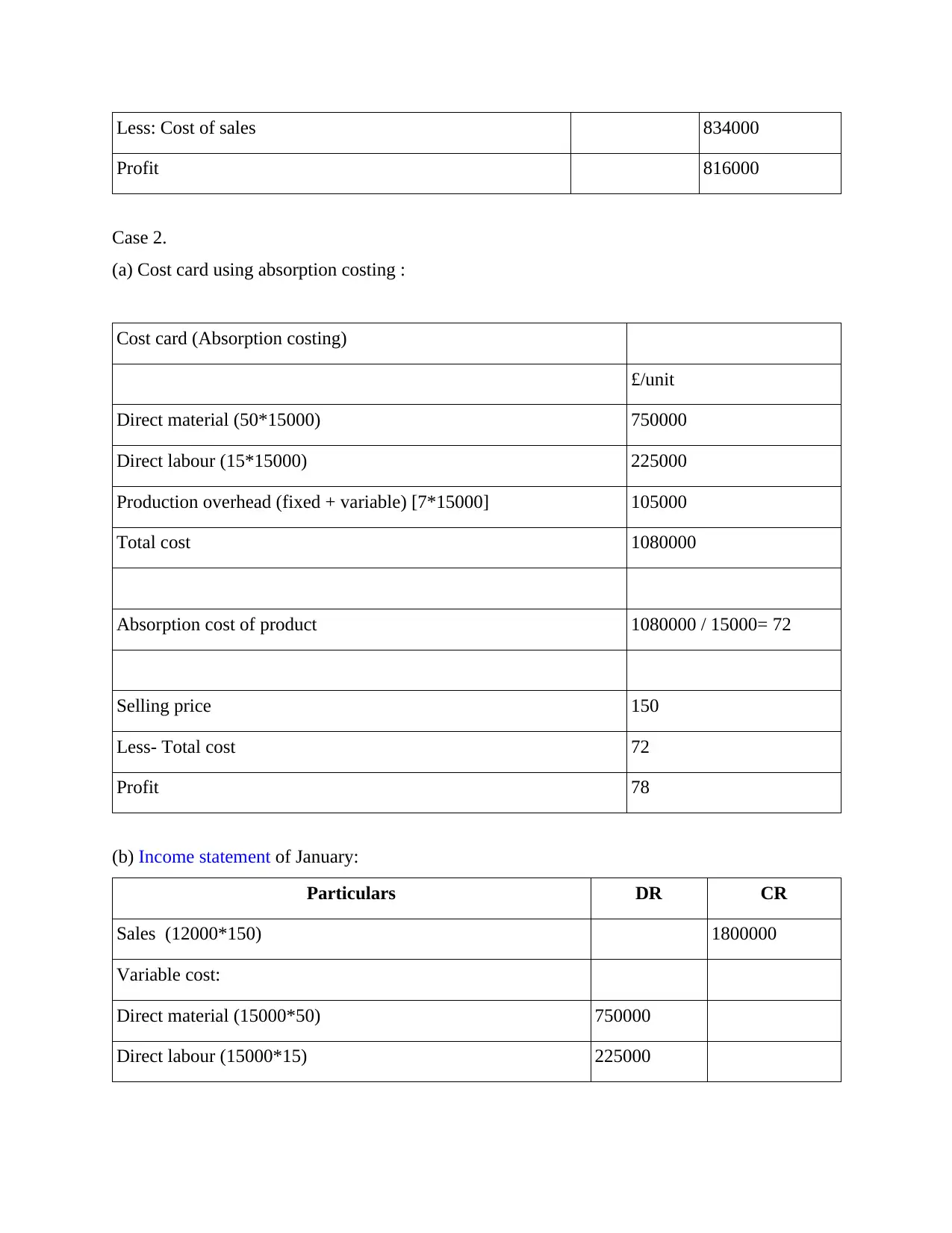

Income statement for month of March

Particulars DR CR

Sales revenue (11000 * 150) 1650000

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Variable cost (10000*9) 90000

Add : Opening stock (1000*74) 74000

Fixed production overhead 20000

Less: Cost of sales 834000

Profit 816000

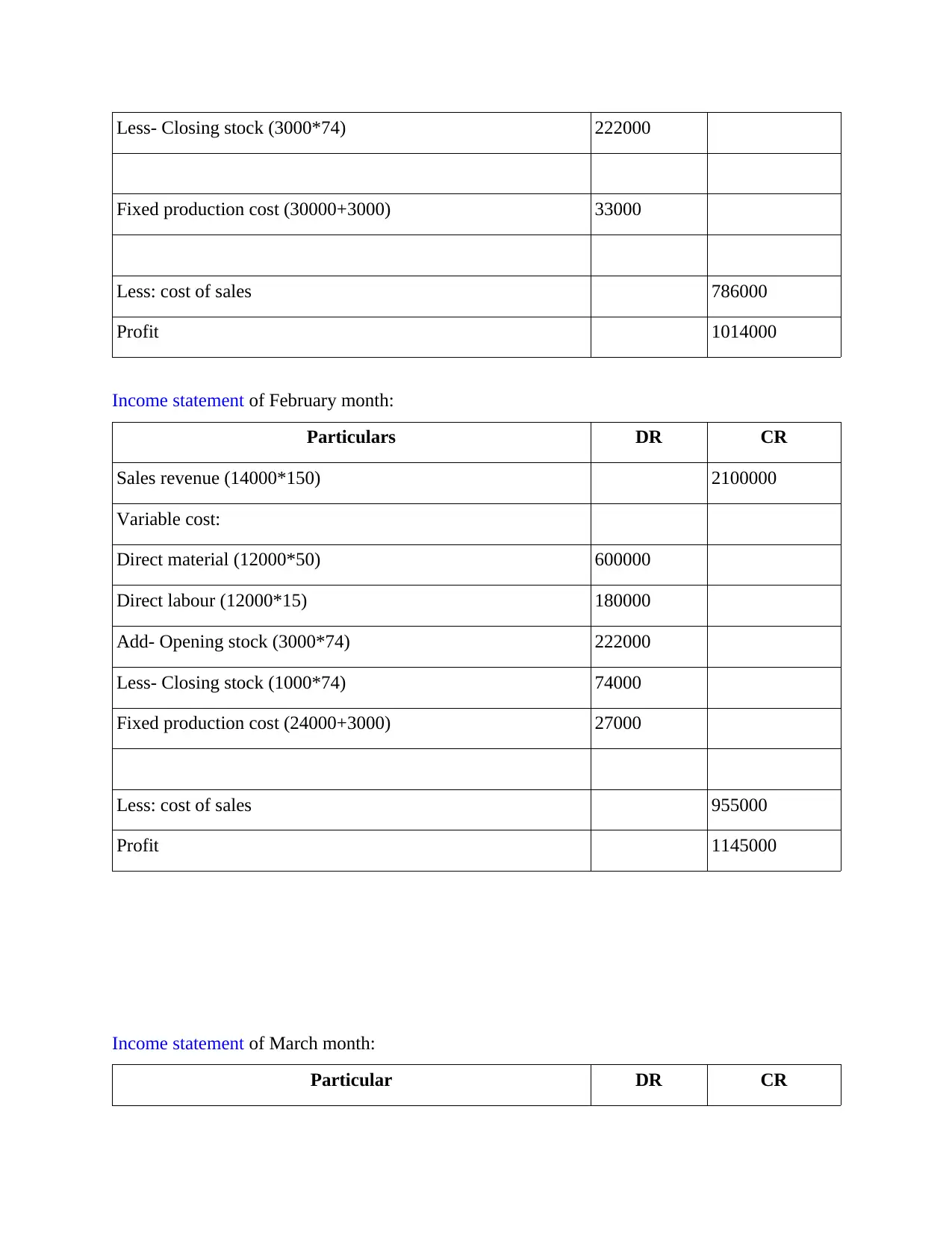

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing)

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

Selling price 150

Less- Total cost 72

Profit 78

(b) Income statement of January:

Particulars DR CR

Sales (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

Profit 816000

Case 2.

(a) Cost card using absorption costing :

Cost card (Absorption costing)

£/unit

Direct material (50*15000) 750000

Direct labour (15*15000) 225000

Production overhead (fixed + variable) [7*15000] 105000

Total cost 1080000

Absorption cost of product 1080000 / 15000= 72

Selling price 150

Less- Total cost 72

Profit 78

(b) Income statement of January:

Particulars DR CR

Sales (12000*150) 1800000

Variable cost:

Direct material (15000*50) 750000

Direct labour (15000*15) 225000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

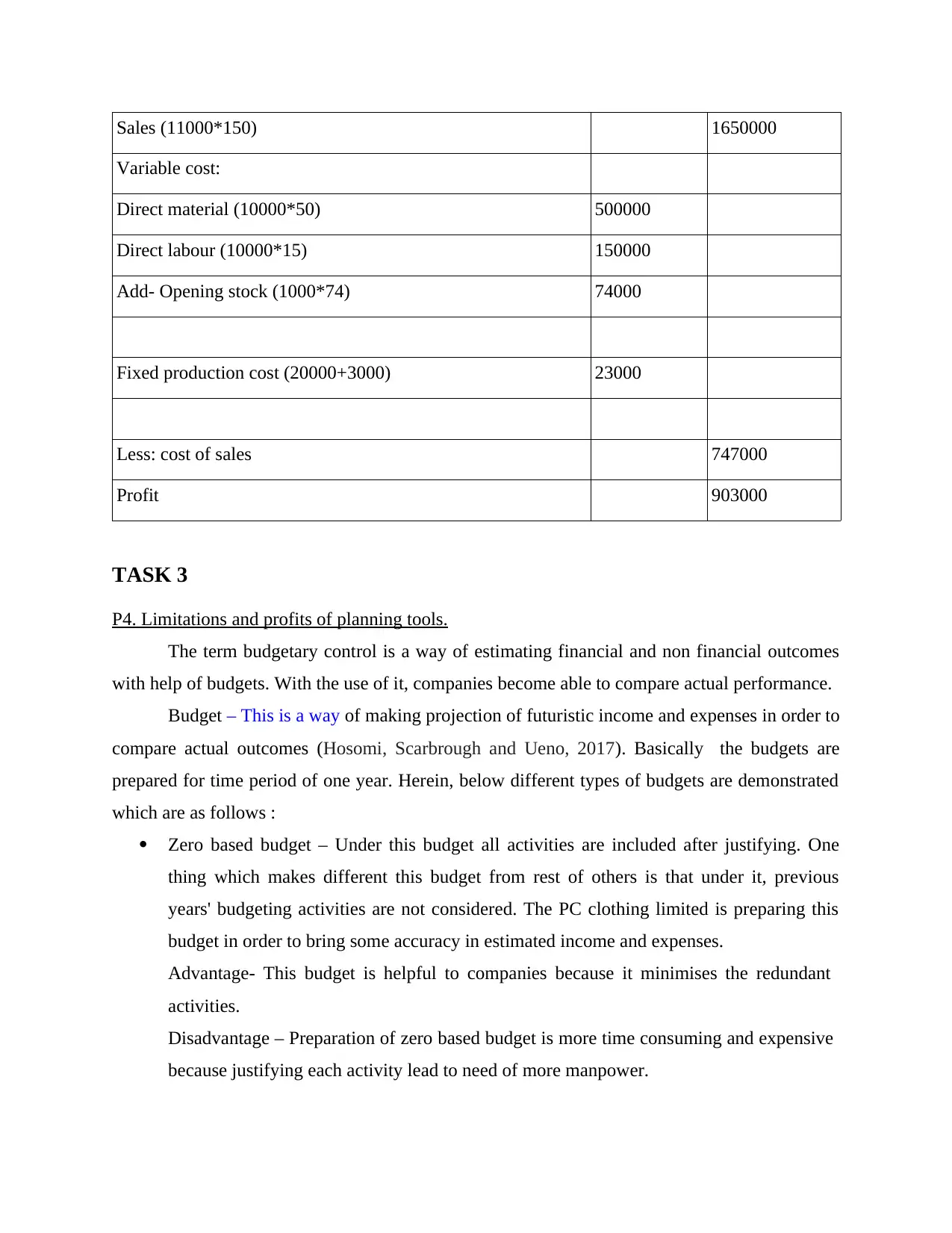

Less- Closing stock (3000*74) 222000

Fixed production cost (30000+3000) 33000

Less: cost of sales 786000

Profit 1014000

Income statement of February month:

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*74) 222000

Less- Closing stock (1000*74) 74000

Fixed production cost (24000+3000) 27000

Less: cost of sales 955000

Profit 1145000

Income statement of March month:

Particular DR CR

Fixed production cost (30000+3000) 33000

Less: cost of sales 786000

Profit 1014000

Income statement of February month:

Particulars DR CR

Sales revenue (14000*150) 2100000

Variable cost:

Direct material (12000*50) 600000

Direct labour (12000*15) 180000

Add- Opening stock (3000*74) 222000

Less- Closing stock (1000*74) 74000

Fixed production cost (24000+3000) 27000

Less: cost of sales 955000

Profit 1145000

Income statement of March month:

Particular DR CR

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

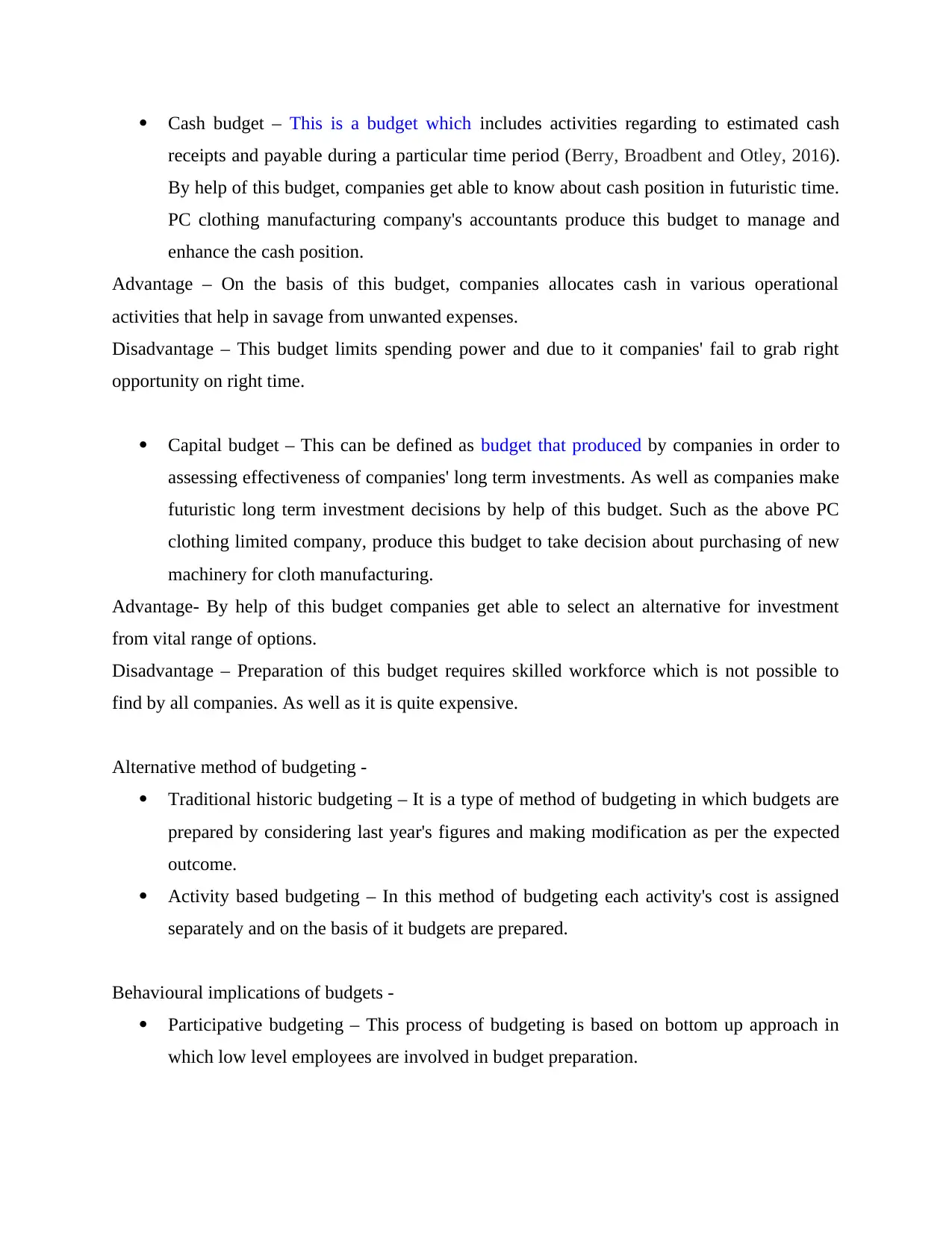

Sales (11000*150) 1650000

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*74) 74000

Fixed production cost (20000+3000) 23000

Less: cost of sales 747000

Profit 903000

TASK 3

P4. Limitations and profits of planning tools.

The term budgetary control is a way of estimating financial and non financial outcomes

with help of budgets. With the use of it, companies become able to compare actual performance.

Budget – This is a way of making projection of futuristic income and expenses in order to

compare actual outcomes (Hosomi, Scarbrough and Ueno, 2017). Basically the budgets are

prepared for time period of one year. Herein, below different types of budgets are demonstrated

which are as follows :

Zero based budget – Under this budget all activities are included after justifying. One

thing which makes different this budget from rest of others is that under it, previous

years' budgeting activities are not considered. The PC clothing limited is preparing this

budget in order to bring some accuracy in estimated income and expenses.

Advantage- This budget is helpful to companies because it minimises the redundant

activities.

Disadvantage – Preparation of zero based budget is more time consuming and expensive

because justifying each activity lead to need of more manpower.

Variable cost:

Direct material (10000*50) 500000

Direct labour (10000*15) 150000

Add- Opening stock (1000*74) 74000

Fixed production cost (20000+3000) 23000

Less: cost of sales 747000

Profit 903000

TASK 3

P4. Limitations and profits of planning tools.

The term budgetary control is a way of estimating financial and non financial outcomes

with help of budgets. With the use of it, companies become able to compare actual performance.

Budget – This is a way of making projection of futuristic income and expenses in order to

compare actual outcomes (Hosomi, Scarbrough and Ueno, 2017). Basically the budgets are

prepared for time period of one year. Herein, below different types of budgets are demonstrated

which are as follows :

Zero based budget – Under this budget all activities are included after justifying. One

thing which makes different this budget from rest of others is that under it, previous

years' budgeting activities are not considered. The PC clothing limited is preparing this

budget in order to bring some accuracy in estimated income and expenses.

Advantage- This budget is helpful to companies because it minimises the redundant

activities.

Disadvantage – Preparation of zero based budget is more time consuming and expensive

because justifying each activity lead to need of more manpower.

Cash budget – This is a budget which includes activities regarding to estimated cash

receipts and payable during a particular time period (Berry, Broadbent and Otley, 2016).

By help of this budget, companies get able to know about cash position in futuristic time.

PC clothing manufacturing company's accountants produce this budget to manage and

enhance the cash position.

Advantage – On the basis of this budget, companies allocates cash in various operational

activities that help in savage from unwanted expenses.

Disadvantage – This budget limits spending power and due to it companies' fail to grab right

opportunity on right time.

Capital budget – This can be defined as budget that produced by companies in order to

assessing effectiveness of companies' long term investments. As well as companies make

futuristic long term investment decisions by help of this budget. Such as the above PC

clothing limited company, produce this budget to take decision about purchasing of new

machinery for cloth manufacturing.

Advantage- By help of this budget companies get able to select an alternative for investment

from vital range of options.

Disadvantage – Preparation of this budget requires skilled workforce which is not possible to

find by all companies. As well as it is quite expensive.

Alternative method of budgeting -

Traditional historic budgeting – It is a type of method of budgeting in which budgets are

prepared by considering last year's figures and making modification as per the expected

outcome.

Activity based budgeting – In this method of budgeting each activity's cost is assigned

separately and on the basis of it budgets are prepared.

Behavioural implications of budgets -

Participative budgeting – This process of budgeting is based on bottom up approach in

which low level employees are involved in budget preparation.

receipts and payable during a particular time period (Berry, Broadbent and Otley, 2016).

By help of this budget, companies get able to know about cash position in futuristic time.

PC clothing manufacturing company's accountants produce this budget to manage and

enhance the cash position.

Advantage – On the basis of this budget, companies allocates cash in various operational

activities that help in savage from unwanted expenses.

Disadvantage – This budget limits spending power and due to it companies' fail to grab right

opportunity on right time.

Capital budget – This can be defined as budget that produced by companies in order to

assessing effectiveness of companies' long term investments. As well as companies make

futuristic long term investment decisions by help of this budget. Such as the above PC

clothing limited company, produce this budget to take decision about purchasing of new

machinery for cloth manufacturing.

Advantage- By help of this budget companies get able to select an alternative for investment

from vital range of options.

Disadvantage – Preparation of this budget requires skilled workforce which is not possible to

find by all companies. As well as it is quite expensive.

Alternative method of budgeting -

Traditional historic budgeting – It is a type of method of budgeting in which budgets are

prepared by considering last year's figures and making modification as per the expected

outcome.

Activity based budgeting – In this method of budgeting each activity's cost is assigned

separately and on the basis of it budgets are prepared.

Behavioural implications of budgets -

Participative budgeting – This process of budgeting is based on bottom up approach in

which low level employees are involved in budget preparation.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.