Management Accounting Report: Excite Entertainment Case Study

VerifiedAdded on 2020/12/18

|15

|3782

|300

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of Excite Entertainment, a UK-based entertainment company. It begins by defining management accounting and contrasting it with financial accounting, emphasizing the importance of various systems such as cost accounting, inventory management, and job costing. The report then delves into different reporting methods used in management accounting, including budget reports, accounts receivable reports, job costing reports, inventory reports, and performance reports, highlighting their significance in assessing business performance and aiding in strategic decision-making. Furthermore, it evaluates the advantages and applications of management accounting systems, specifically focusing on cost accounting, inventory management, and job costing. The report also includes calculations of net profit using both marginal and absorption costing techniques. Finally, it explores the benefits and limitations of budgetary control and compares different management accounting systems for resolving financial problems and achieving sustainable organizational success. The report concludes by summarizing key findings and offering insights into the practical implications of management accounting for businesses like Excite Entertainment.

MANAGEMENT

ACCOUNTING

INTRODUCTION 3

LO1..................................................................................................................................................3

P1. Explaining the concept of management accounting and the importance of its various

systems.........................................................................................................................................3

P2. Explaining several methods for reporting under management accounting...........................5

M3. Evaluating the advantages and the application of the system of management accounting..6

LO2..................................................................................................................................................7

P3. Calculation of the net profit by using the marginal and the absorption costing technique...7

LO3..................................................................................................................................................8

P4&M3. Explaining the benefits and the limitations of the different planning tools of

budgetary control.........................................................................................................................8

LO4................................................................................................................................................10

P5&M4. Comparing the adaptation of the different management accounting system for

resolving the financial problems and which leads to sustainable success of the organization..10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

ACCOUNTING

INTRODUCTION 3

LO1..................................................................................................................................................3

P1. Explaining the concept of management accounting and the importance of its various

systems.........................................................................................................................................3

P2. Explaining several methods for reporting under management accounting...........................5

M3. Evaluating the advantages and the application of the system of management accounting..6

LO2..................................................................................................................................................7

P3. Calculation of the net profit by using the marginal and the absorption costing technique...7

LO3..................................................................................................................................................8

P4&M3. Explaining the benefits and the limitations of the different planning tools of

budgetary control.........................................................................................................................8

LO4................................................................................................................................................10

P5&M4. Comparing the adaptation of the different management accounting system for

resolving the financial problems and which leads to sustainable success of the organization..10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

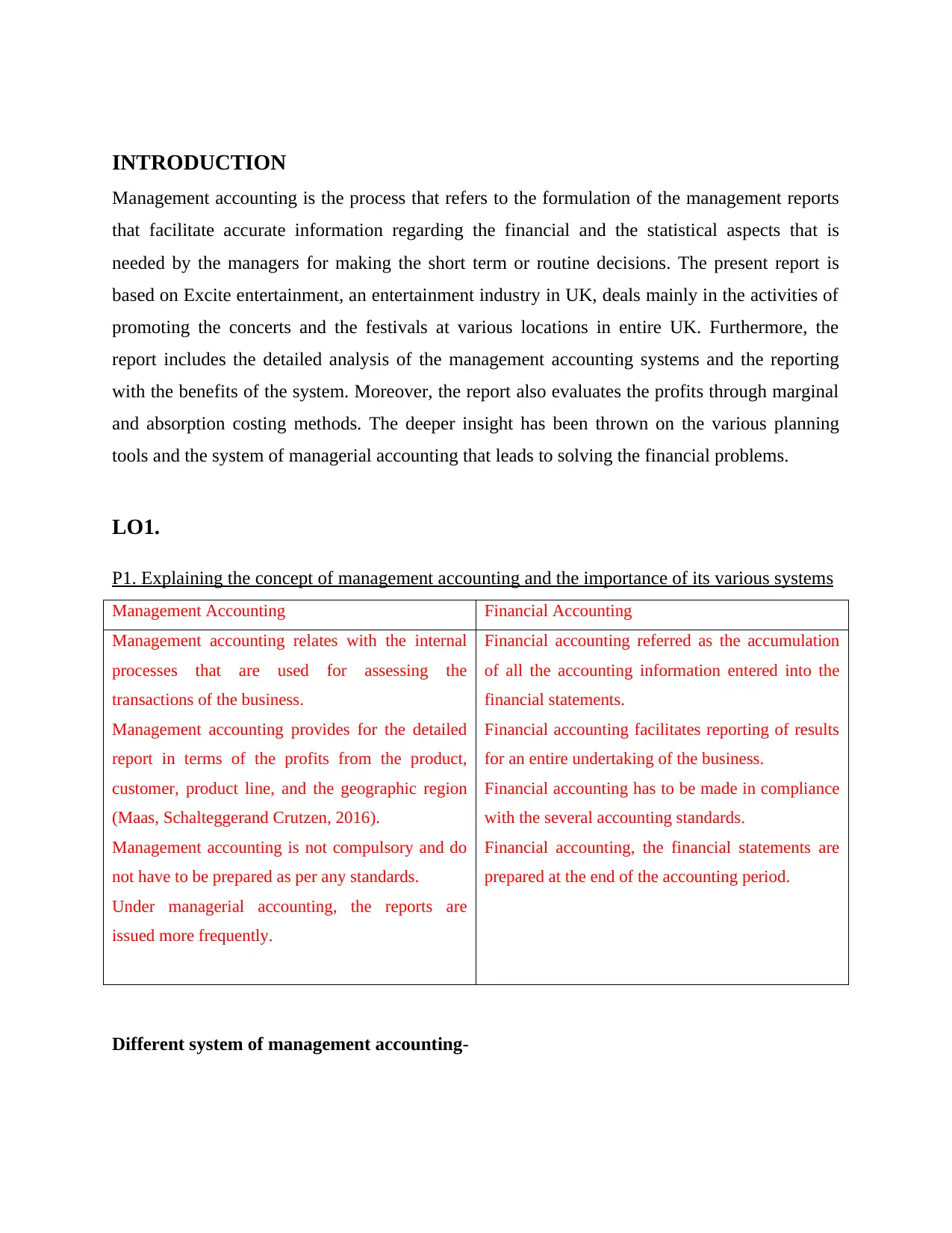

INTRODUCTION

Management accounting is the process that refers to the formulation of the management reports

that facilitate accurate information regarding the financial and the statistical aspects that is

needed by the managers for making the short term or routine decisions. The present report is

based on Excite entertainment, an entertainment industry in UK, deals mainly in the activities of

promoting the concerts and the festivals at various locations in entire UK. Furthermore, the

report includes the detailed analysis of the management accounting systems and the reporting

with the benefits of the system. Moreover, the report also evaluates the profits through marginal

and absorption costing methods. The deeper insight has been thrown on the various planning

tools and the system of managerial accounting that leads to solving the financial problems.

LO1.

P1. Explaining the concept of management accounting and the importance of its various systems

Management Accounting Financial Accounting

Management accounting relates with the internal

processes that are used for assessing the

transactions of the business.

Management accounting provides for the detailed

report in terms of the profits from the product,

customer, product line, and the geographic region

(Maas, Schalteggerand Crutzen, 2016).

Management accounting is not compulsory and do

not have to be prepared as per any standards.

Under managerial accounting, the reports are

issued more frequently.

Financial accounting referred as the accumulation

of all the accounting information entered into the

financial statements.

Financial accounting facilitates reporting of results

for an entire undertaking of the business.

Financial accounting has to be made in compliance

with the several accounting standards.

Financial accounting, the financial statements are

prepared at the end of the accounting period.

Different system of management accounting-

Management accounting is the process that refers to the formulation of the management reports

that facilitate accurate information regarding the financial and the statistical aspects that is

needed by the managers for making the short term or routine decisions. The present report is

based on Excite entertainment, an entertainment industry in UK, deals mainly in the activities of

promoting the concerts and the festivals at various locations in entire UK. Furthermore, the

report includes the detailed analysis of the management accounting systems and the reporting

with the benefits of the system. Moreover, the report also evaluates the profits through marginal

and absorption costing methods. The deeper insight has been thrown on the various planning

tools and the system of managerial accounting that leads to solving the financial problems.

LO1.

P1. Explaining the concept of management accounting and the importance of its various systems

Management Accounting Financial Accounting

Management accounting relates with the internal

processes that are used for assessing the

transactions of the business.

Management accounting provides for the detailed

report in terms of the profits from the product,

customer, product line, and the geographic region

(Maas, Schalteggerand Crutzen, 2016).

Management accounting is not compulsory and do

not have to be prepared as per any standards.

Under managerial accounting, the reports are

issued more frequently.

Financial accounting referred as the accumulation

of all the accounting information entered into the

financial statements.

Financial accounting facilitates reporting of results

for an entire undertaking of the business.

Financial accounting has to be made in compliance

with the several accounting standards.

Financial accounting, the financial statements are

prepared at the end of the accounting period.

Different system of management accounting-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

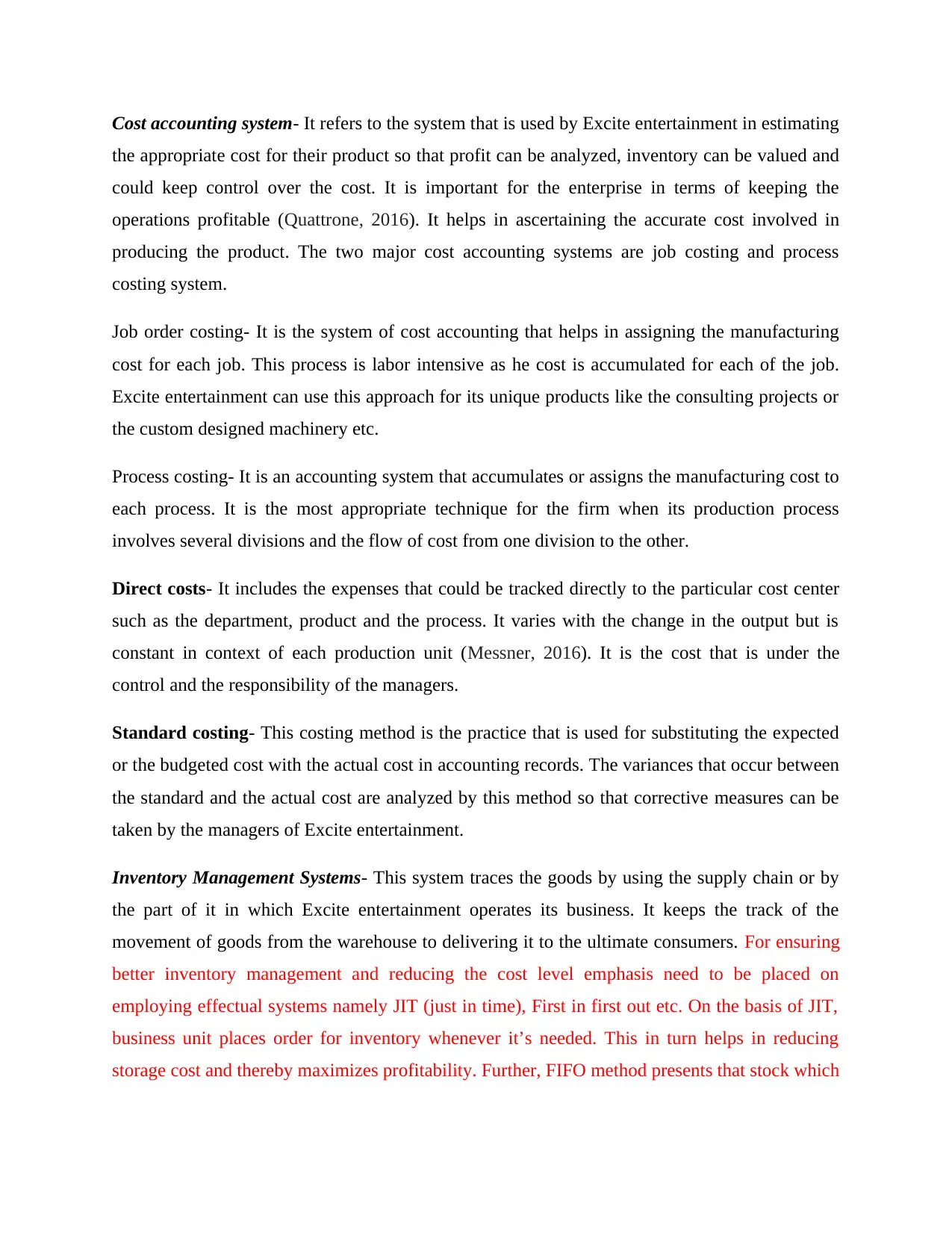

Cost accounting system- It refers to the system that is used by Excite entertainment in estimating

the appropriate cost for their product so that profit can be analyzed, inventory can be valued and

could keep control over the cost. It is important for the enterprise in terms of keeping the

operations profitable (Quattrone, 2016). It helps in ascertaining the accurate cost involved in

producing the product. The two major cost accounting systems are job costing and process

costing system.

Job order costing- It is the system of cost accounting that helps in assigning the manufacturing

cost for each job. This process is labor intensive as he cost is accumulated for each of the job.

Excite entertainment can use this approach for its unique products like the consulting projects or

the custom designed machinery etc.

Process costing- It is an accounting system that accumulates or assigns the manufacturing cost to

each process. It is the most appropriate technique for the firm when its production process

involves several divisions and the flow of cost from one division to the other.

Direct costs- It includes the expenses that could be tracked directly to the particular cost center

such as the department, product and the process. It varies with the change in the output but is

constant in context of each production unit (Messner, 2016). It is the cost that is under the

control and the responsibility of the managers.

Standard costing- This costing method is the practice that is used for substituting the expected

or the budgeted cost with the actual cost in accounting records. The variances that occur between

the standard and the actual cost are analyzed by this method so that corrective measures can be

taken by the managers of Excite entertainment.

Inventory Management Systems- This system traces the goods by using the supply chain or by

the part of it in which Excite entertainment operates its business. It keeps the track of the

movement of goods from the warehouse to delivering it to the ultimate consumers. For ensuring

better inventory management and reducing the cost level emphasis need to be placed on

employing effectual systems namely JIT (just in time), First in first out etc. On the basis of JIT,

business unit places order for inventory whenever it’s needed. This in turn helps in reducing

storage cost and thereby maximizes profitability. Further, FIFO method presents that stock which

the appropriate cost for their product so that profit can be analyzed, inventory can be valued and

could keep control over the cost. It is important for the enterprise in terms of keeping the

operations profitable (Quattrone, 2016). It helps in ascertaining the accurate cost involved in

producing the product. The two major cost accounting systems are job costing and process

costing system.

Job order costing- It is the system of cost accounting that helps in assigning the manufacturing

cost for each job. This process is labor intensive as he cost is accumulated for each of the job.

Excite entertainment can use this approach for its unique products like the consulting projects or

the custom designed machinery etc.

Process costing- It is an accounting system that accumulates or assigns the manufacturing cost to

each process. It is the most appropriate technique for the firm when its production process

involves several divisions and the flow of cost from one division to the other.

Direct costs- It includes the expenses that could be tracked directly to the particular cost center

such as the department, product and the process. It varies with the change in the output but is

constant in context of each production unit (Messner, 2016). It is the cost that is under the

control and the responsibility of the managers.

Standard costing- This costing method is the practice that is used for substituting the expected

or the budgeted cost with the actual cost in accounting records. The variances that occur between

the standard and the actual cost are analyzed by this method so that corrective measures can be

taken by the managers of Excite entertainment.

Inventory Management Systems- This system traces the goods by using the supply chain or by

the part of it in which Excite entertainment operates its business. It keeps the track of the

movement of goods from the warehouse to delivering it to the ultimate consumers. For ensuring

better inventory management and reducing the cost level emphasis need to be placed on

employing effectual systems namely JIT (just in time), First in first out etc. On the basis of JIT,

business unit places order for inventory whenever it’s needed. This in turn helps in reducing

storage cost and thereby maximizes profitability. Further, FIFO method presents that stock which

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

purchased earlier need to be sold first. This in turn reduces problem in relation to outdated

stockand thereby helps in maintaining profitability.

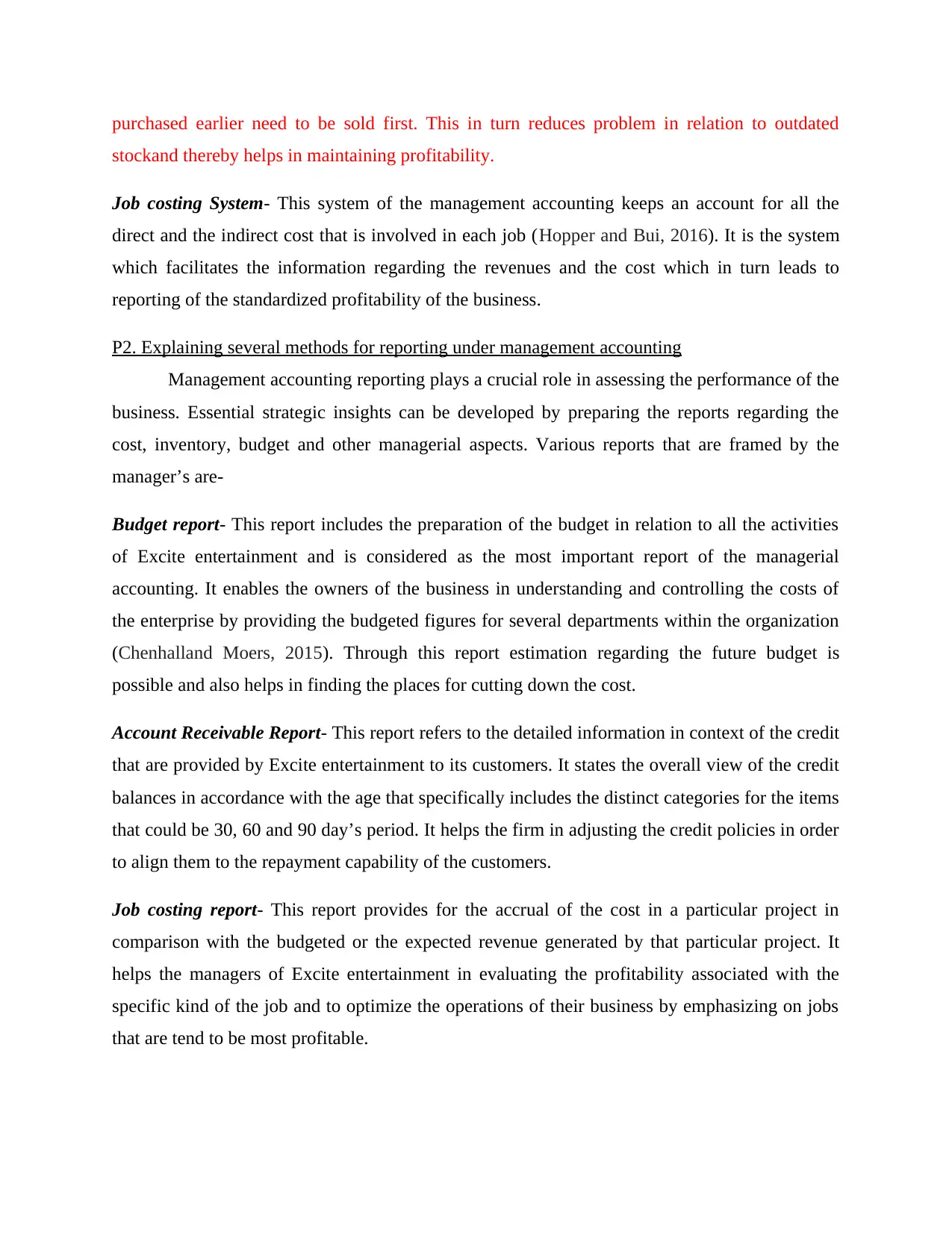

Job costing System- This system of the management accounting keeps an account for all the

direct and the indirect cost that is involved in each job (Hopper and Bui, 2016). It is the system

which facilitates the information regarding the revenues and the cost which in turn leads to

reporting of the standardized profitability of the business.

P2. Explaining several methods for reporting under management accounting

Management accounting reporting plays a crucial role in assessing the performance of the

business. Essential strategic insights can be developed by preparing the reports regarding the

cost, inventory, budget and other managerial aspects. Various reports that are framed by the

manager’s are-

Budget report- This report includes the preparation of the budget in relation to all the activities

of Excite entertainment and is considered as the most important report of the managerial

accounting. It enables the owners of the business in understanding and controlling the costs of

the enterprise by providing the budgeted figures for several departments within the organization

(Chenhalland Moers, 2015). Through this report estimation regarding the future budget is

possible and also helps in finding the places for cutting down the cost.

Account Receivable Report- This report refers to the detailed information in context of the credit

that are provided by Excite entertainment to its customers. It states the overall view of the credit

balances in accordance with the age that specifically includes the distinct categories for the items

that could be 30, 60 and 90 day’s period. It helps the firm in adjusting the credit policies in order

to align them to the repayment capability of the customers.

Job costing report- This report provides for the accrual of the cost in a particular project in

comparison with the budgeted or the expected revenue generated by that particular project. It

helps the managers of Excite entertainment in evaluating the profitability associated with the

specific kind of the job and to optimize the operations of their business by emphasizing on jobs

that are tend to be most profitable.

stockand thereby helps in maintaining profitability.

Job costing System- This system of the management accounting keeps an account for all the

direct and the indirect cost that is involved in each job (Hopper and Bui, 2016). It is the system

which facilitates the information regarding the revenues and the cost which in turn leads to

reporting of the standardized profitability of the business.

P2. Explaining several methods for reporting under management accounting

Management accounting reporting plays a crucial role in assessing the performance of the

business. Essential strategic insights can be developed by preparing the reports regarding the

cost, inventory, budget and other managerial aspects. Various reports that are framed by the

manager’s are-

Budget report- This report includes the preparation of the budget in relation to all the activities

of Excite entertainment and is considered as the most important report of the managerial

accounting. It enables the owners of the business in understanding and controlling the costs of

the enterprise by providing the budgeted figures for several departments within the organization

(Chenhalland Moers, 2015). Through this report estimation regarding the future budget is

possible and also helps in finding the places for cutting down the cost.

Account Receivable Report- This report refers to the detailed information in context of the credit

that are provided by Excite entertainment to its customers. It states the overall view of the credit

balances in accordance with the age that specifically includes the distinct categories for the items

that could be 30, 60 and 90 day’s period. It helps the firm in adjusting the credit policies in order

to align them to the repayment capability of the customers.

Job costing report- This report provides for the accrual of the cost in a particular project in

comparison with the budgeted or the expected revenue generated by that particular project. It

helps the managers of Excite entertainment in evaluating the profitability associated with the

specific kind of the job and to optimize the operations of their business by emphasizing on jobs

that are tend to be most profitable.

Inventory report- In this report the records relating to the inventory of the enterprise are

maintained and the combination of technology is used for managing the inventory (Latan and

et.al., 2018). This report helps in centralizing the data on the cost of the inventory, labor cost and

other overhead cost that is involved in production process, facilitates the raw data for optimizing

the machining or the assembly.

Performance report-This report of management accounting is created for reviewing the

performance of Excite entertainment as well as the performance of its employees in performing

the task as per the standard set. Performance report is used by the managers in making the

strategic decisions relating to the future needs of the enterprise. This report plays a vital role in

keeping a relevant measure of the strategy towards the mission and the vision of Excite

entertainment.

Thus, it is important for Excite entertainment to choose the right type of the report which helps in

achieving the goals more effectively and efficiently. Through these reports, deeper insights can

be attained in capturing the opportunities in the overall marketplace.

Stating reasons behind having accurate managerial accounting report

By doing assessment, it has identified that managerial accounting reports provide high

level of assistance to the managers in decision making. Referringreports, manager makes

evaluation of departmental performance and thereby take further measures for improvement.

Further, report also gives indication to the firm in relation to maintenance of stock within the

firm. Hence, considering all such aspects it can be stated that information contained in

managerial reports should be accurate and reliable in nature.

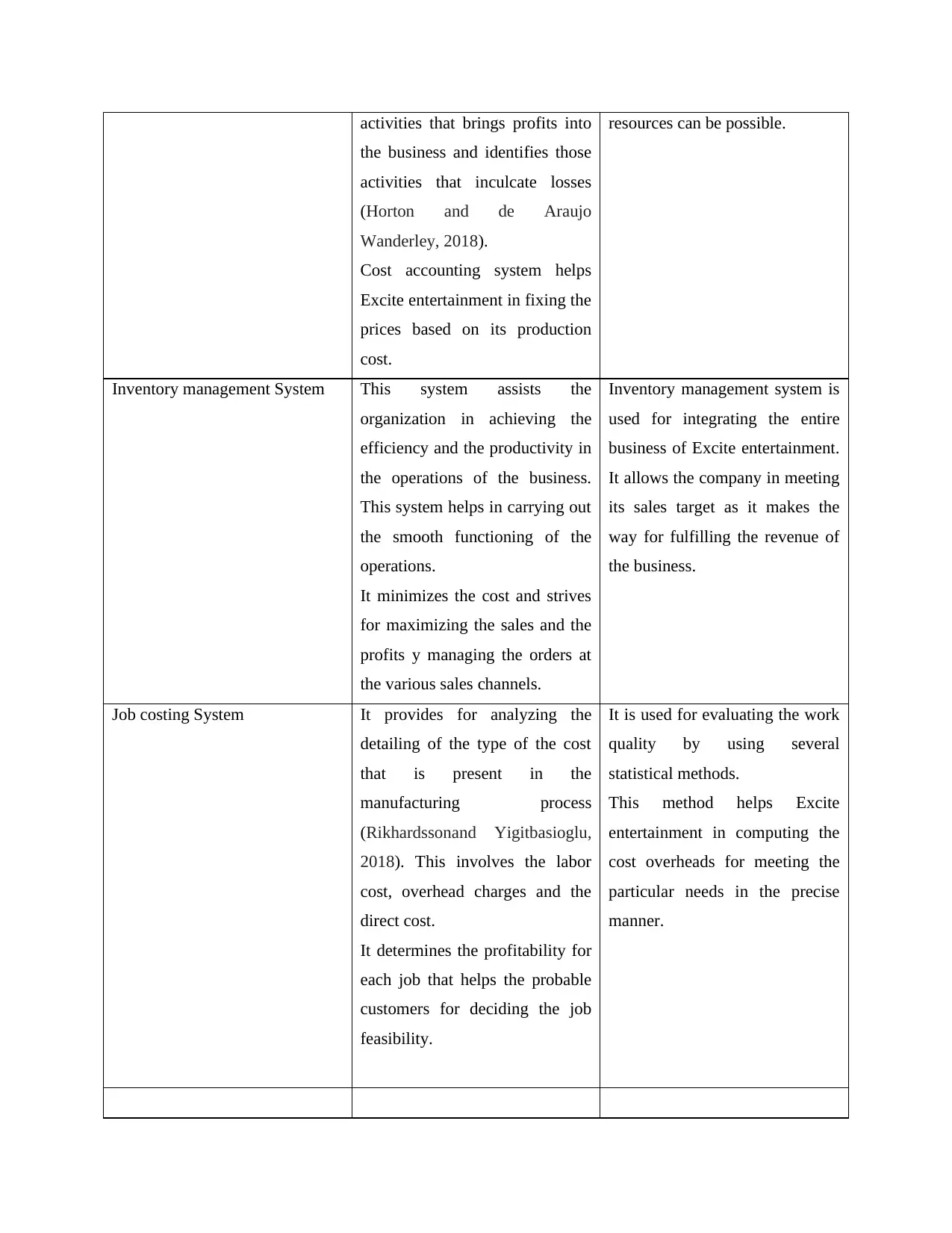

M3. Evaluating the advantages and the application of the system of management accounting

Management accounting systems Benefits Application

Cost Accounting System This system helps in measuring

and continuous improvement in

the efficiency of Excite

entertainment.

It throws the highlights on the

Cost accounting system is used

by Excite entertainment in

ascertaining the cost involved

and reducing the unnecessary

cost so that optimum use of the

maintained and the combination of technology is used for managing the inventory (Latan and

et.al., 2018). This report helps in centralizing the data on the cost of the inventory, labor cost and

other overhead cost that is involved in production process, facilitates the raw data for optimizing

the machining or the assembly.

Performance report-This report of management accounting is created for reviewing the

performance of Excite entertainment as well as the performance of its employees in performing

the task as per the standard set. Performance report is used by the managers in making the

strategic decisions relating to the future needs of the enterprise. This report plays a vital role in

keeping a relevant measure of the strategy towards the mission and the vision of Excite

entertainment.

Thus, it is important for Excite entertainment to choose the right type of the report which helps in

achieving the goals more effectively and efficiently. Through these reports, deeper insights can

be attained in capturing the opportunities in the overall marketplace.

Stating reasons behind having accurate managerial accounting report

By doing assessment, it has identified that managerial accounting reports provide high

level of assistance to the managers in decision making. Referringreports, manager makes

evaluation of departmental performance and thereby take further measures for improvement.

Further, report also gives indication to the firm in relation to maintenance of stock within the

firm. Hence, considering all such aspects it can be stated that information contained in

managerial reports should be accurate and reliable in nature.

M3. Evaluating the advantages and the application of the system of management accounting

Management accounting systems Benefits Application

Cost Accounting System This system helps in measuring

and continuous improvement in

the efficiency of Excite

entertainment.

It throws the highlights on the

Cost accounting system is used

by Excite entertainment in

ascertaining the cost involved

and reducing the unnecessary

cost so that optimum use of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

activities that brings profits into

the business and identifies those

activities that inculcate losses

(Horton and de Araujo

Wanderley, 2018).

Cost accounting system helps

Excite entertainment in fixing the

prices based on its production

cost.

resources can be possible.

Inventory management System This system assists the

organization in achieving the

efficiency and the productivity in

the operations of the business.

This system helps in carrying out

the smooth functioning of the

operations.

It minimizes the cost and strives

for maximizing the sales and the

profits y managing the orders at

the various sales channels.

Inventory management system is

used for integrating the entire

business of Excite entertainment.

It allows the company in meeting

its sales target as it makes the

way for fulfilling the revenue of

the business.

Job costing System It provides for analyzing the

detailing of the type of the cost

that is present in the

manufacturing process

(Rikhardssonand Yigitbasioglu,

2018). This involves the labor

cost, overhead charges and the

direct cost.

It determines the profitability for

each job that helps the probable

customers for deciding the job

feasibility.

It is used for evaluating the work

quality by using several

statistical methods.

This method helps Excite

entertainment in computing the

cost overheads for meeting the

particular needs in the precise

manner.

the business and identifies those

activities that inculcate losses

(Horton and de Araujo

Wanderley, 2018).

Cost accounting system helps

Excite entertainment in fixing the

prices based on its production

cost.

resources can be possible.

Inventory management System This system assists the

organization in achieving the

efficiency and the productivity in

the operations of the business.

This system helps in carrying out

the smooth functioning of the

operations.

It minimizes the cost and strives

for maximizing the sales and the

profits y managing the orders at

the various sales channels.

Inventory management system is

used for integrating the entire

business of Excite entertainment.

It allows the company in meeting

its sales target as it makes the

way for fulfilling the revenue of

the business.

Job costing System It provides for analyzing the

detailing of the type of the cost

that is present in the

manufacturing process

(Rikhardssonand Yigitbasioglu,

2018). This involves the labor

cost, overhead charges and the

direct cost.

It determines the profitability for

each job that helps the probable

customers for deciding the job

feasibility.

It is used for evaluating the work

quality by using several

statistical methods.

This method helps Excite

entertainment in computing the

cost overheads for meeting the

particular needs in the precise

manner.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO2.

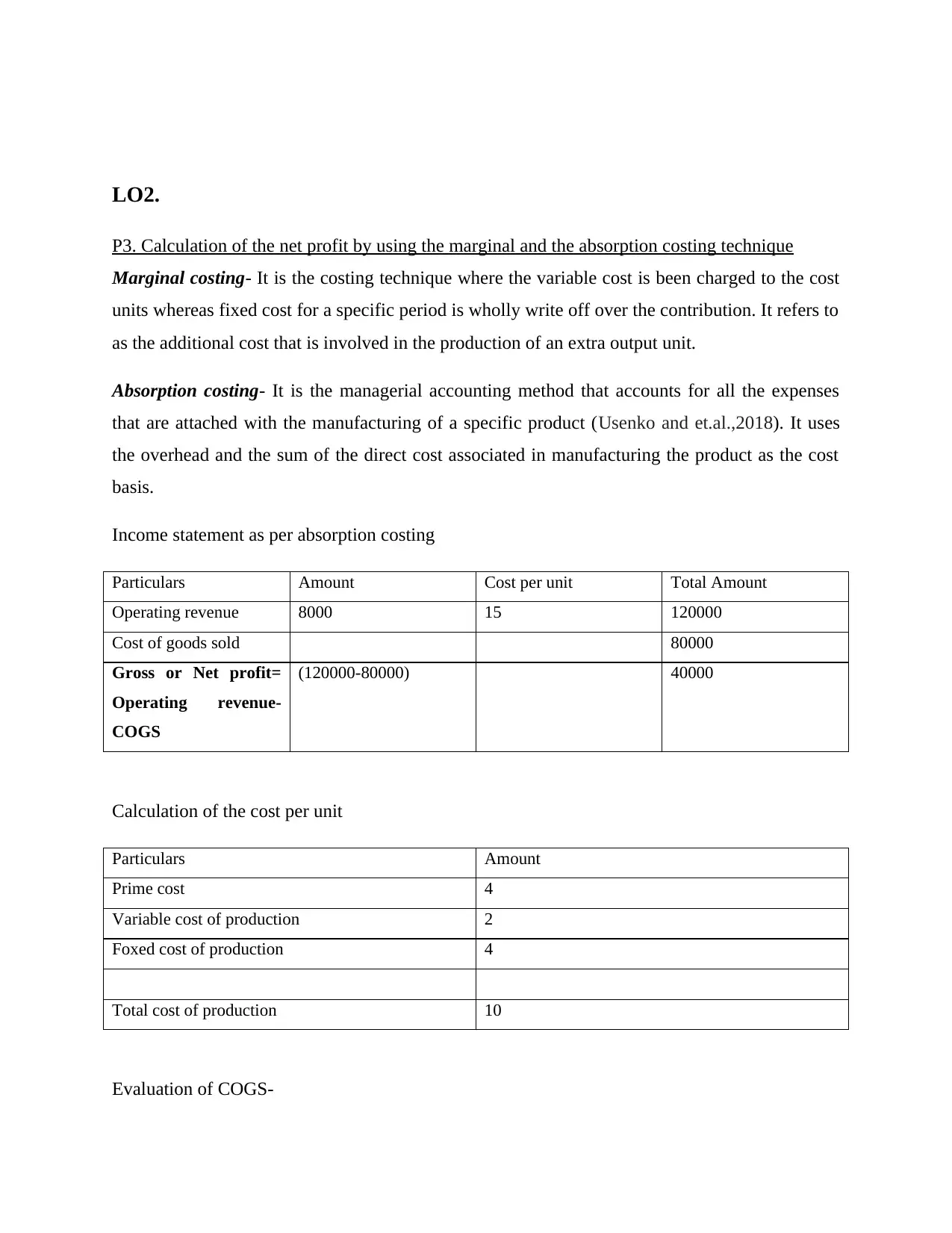

P3. Calculation of the net profit by using the marginal and the absorption costing technique

Marginal costing- It is the costing technique where the variable cost is been charged to the cost

units whereas fixed cost for a specific period is wholly write off over the contribution. It refers to

as the additional cost that is involved in the production of an extra output unit.

Absorption costing- It is the managerial accounting method that accounts for all the expenses

that are attached with the manufacturing of a specific product (Usenko and et.al.,2018). It uses

the overhead and the sum of the direct cost associated in manufacturing the product as the cost

basis.

Income statement as per absorption costing

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Cost of goods sold 80000

Gross or Net profit=

Operating revenue-

COGS

(120000-80000) 40000

Calculation of the cost per unit

Particulars Amount

Prime cost 4

Variable cost of production 2

Foxed cost of production 4

Total cost of production 10

Evaluation of COGS-

P3. Calculation of the net profit by using the marginal and the absorption costing technique

Marginal costing- It is the costing technique where the variable cost is been charged to the cost

units whereas fixed cost for a specific period is wholly write off over the contribution. It refers to

as the additional cost that is involved in the production of an extra output unit.

Absorption costing- It is the managerial accounting method that accounts for all the expenses

that are attached with the manufacturing of a specific product (Usenko and et.al.,2018). It uses

the overhead and the sum of the direct cost associated in manufacturing the product as the cost

basis.

Income statement as per absorption costing

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Cost of goods sold 80000

Gross or Net profit=

Operating revenue-

COGS

(120000-80000) 40000

Calculation of the cost per unit

Particulars Amount

Prime cost 4

Variable cost of production 2

Foxed cost of production 4

Total cost of production 10

Evaluation of COGS-

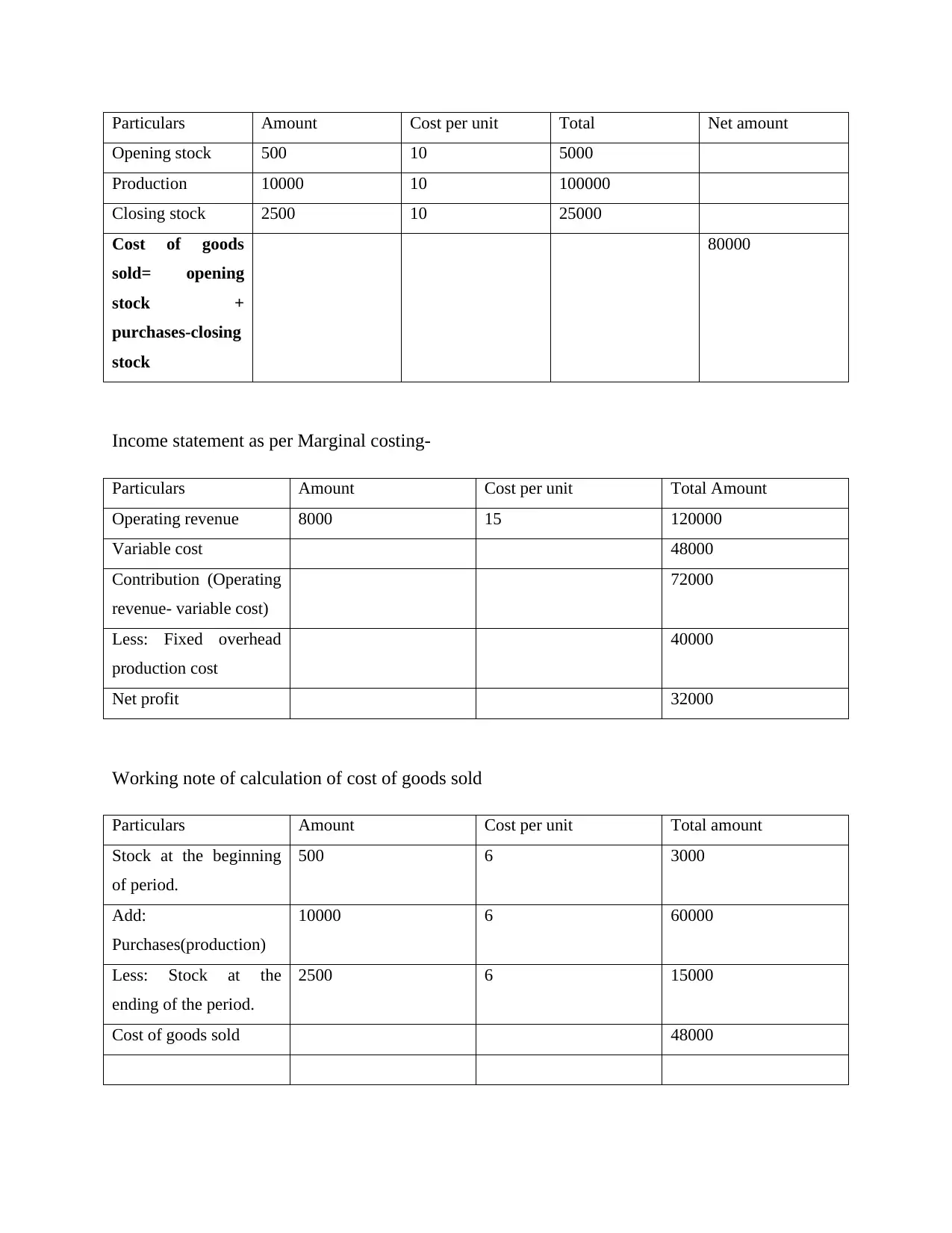

Particulars Amount Cost per unit Total Net amount

Opening stock 500 10 5000

Production 10000 10 100000

Closing stock 2500 10 25000

Cost of goods

sold= opening

stock +

purchases-closing

stock

80000

Income statement as per Marginal costing-

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Variable cost 48000

Contribution (Operating

revenue- variable cost)

72000

Less: Fixed overhead

production cost

40000

Net profit 32000

Working note of calculation of cost of goods sold

Particulars Amount Cost per unit Total amount

Stock at the beginning

of period.

500 6 3000

Add:

Purchases(production)

10000 6 60000

Less: Stock at the

ending of the period.

2500 6 15000

Cost of goods sold 48000

Opening stock 500 10 5000

Production 10000 10 100000

Closing stock 2500 10 25000

Cost of goods

sold= opening

stock +

purchases-closing

stock

80000

Income statement as per Marginal costing-

Particulars Amount Cost per unit Total Amount

Operating revenue 8000 15 120000

Variable cost 48000

Contribution (Operating

revenue- variable cost)

72000

Less: Fixed overhead

production cost

40000

Net profit 32000

Working note of calculation of cost of goods sold

Particulars Amount Cost per unit Total amount

Stock at the beginning

of period.

500 6 3000

Add:

Purchases(production)

10000 6 60000

Less: Stock at the

ending of the period.

2500 6 15000

Cost of goods sold 48000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculating the cost per unit by using the marginal costing

Particulars Amount

Prime cost 4

Variable cost of production 2

Total cost of production 6

Interpretation- From the above analysis it can be interpreted that net profit resulted as 40000 by

applying the absorption costing method where it includes both variable and the fixed cost of

production. On the other hand, the profits ascertained by using the marginal costing equates to

32000 which does account for the fixed overhead production cost. Absorption costing is more

suitable technique as compared to marginal costing as it provides for the realistic evaluation of

the profits because it calculates the profits after considering both the costs that is variable and the

fixed cost.

LO3.

P4&M3. Explaining the benefits and the limitations of the different planning tools of budgetary

control

Activity based budget- It is the method of budgeting in which the budgets are prepared after

considering an overhead cost. It is the tool that does not accounts for the previous budget for

arriving at the preset year budget.

Advantages/uses Disadvantages

Evaluation- This method helps in evaluating every

cost driver. It takes into account all the steps that

are involved in the activity.

Competitive edge- This system eliminates

irrelevant activities which results in cost saving.

This lower cost helps in achieving the competitive

edge against the competitors of Excite

entertainment.

Requires understanding- It requires the deep

understanding relating to the several functional

areas within the business (Curry, 2019).

Incapability of the managers in understanding the

areas lead to the inaccurate budget.

Complex-This technique of budgetary control is

very complex as it needs research of the various

factors.

Short term approach- Activity based budget

Particulars Amount

Prime cost 4

Variable cost of production 2

Total cost of production 6

Interpretation- From the above analysis it can be interpreted that net profit resulted as 40000 by

applying the absorption costing method where it includes both variable and the fixed cost of

production. On the other hand, the profits ascertained by using the marginal costing equates to

32000 which does account for the fixed overhead production cost. Absorption costing is more

suitable technique as compared to marginal costing as it provides for the realistic evaluation of

the profits because it calculates the profits after considering both the costs that is variable and the

fixed cost.

LO3.

P4&M3. Explaining the benefits and the limitations of the different planning tools of budgetary

control

Activity based budget- It is the method of budgeting in which the budgets are prepared after

considering an overhead cost. It is the tool that does not accounts for the previous budget for

arriving at the preset year budget.

Advantages/uses Disadvantages

Evaluation- This method helps in evaluating every

cost driver. It takes into account all the steps that

are involved in the activity.

Competitive edge- This system eliminates

irrelevant activities which results in cost saving.

This lower cost helps in achieving the competitive

edge against the competitors of Excite

entertainment.

Requires understanding- It requires the deep

understanding relating to the several functional

areas within the business (Curry, 2019).

Incapability of the managers in understanding the

areas lead to the inaccurate budget.

Complex-This technique of budgetary control is

very complex as it needs research of the various

factors.

Short term approach- Activity based budget

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

emphasize on the short term objectives of business.

It does not focus on long term objectives which can

prove fatal for Excite entertainment.

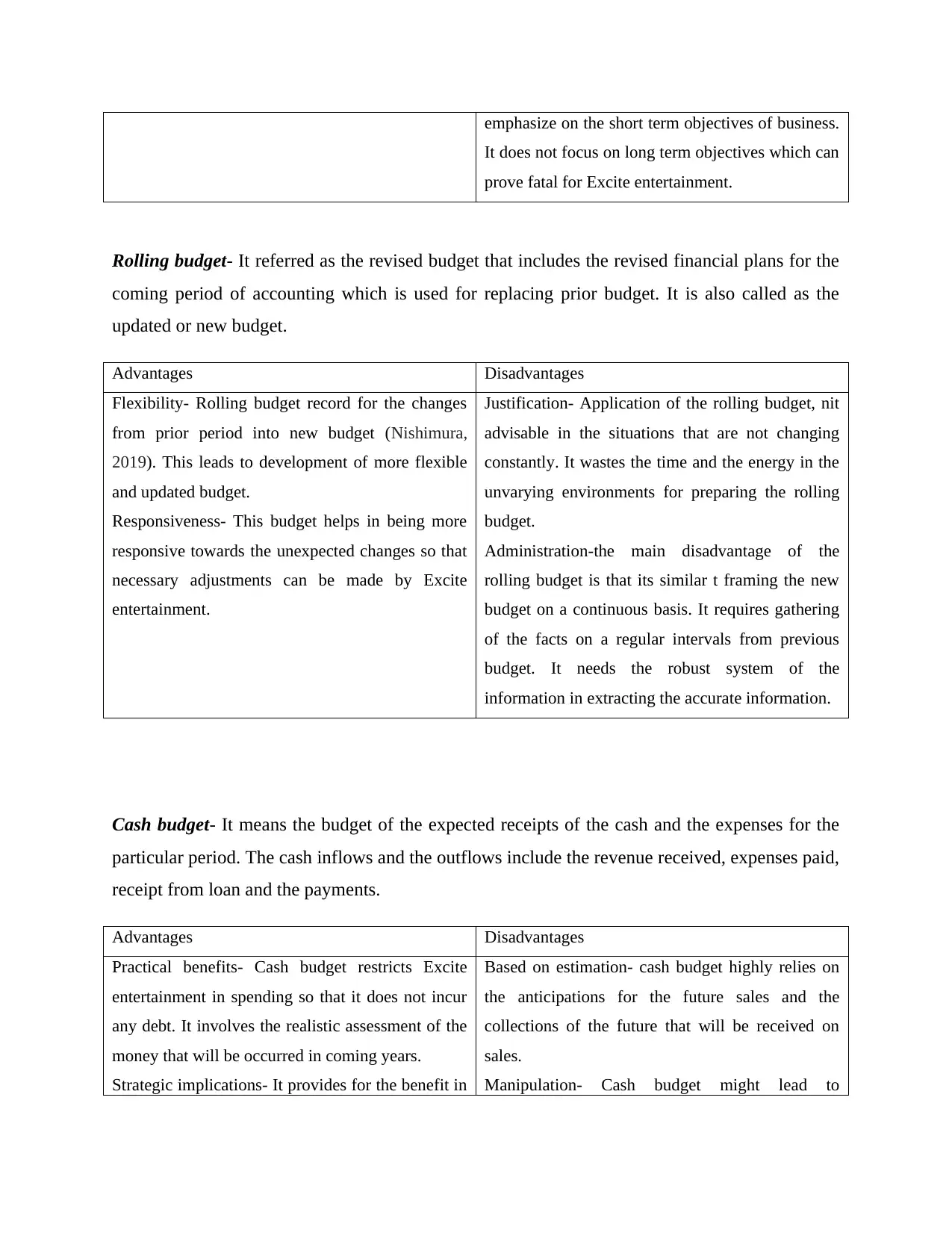

Rolling budget- It referred as the revised budget that includes the revised financial plans for the

coming period of accounting which is used for replacing prior budget. It is also called as the

updated or new budget.

Advantages Disadvantages

Flexibility- Rolling budget record for the changes

from prior period into new budget (Nishimura,

2019). This leads to development of more flexible

and updated budget.

Responsiveness- This budget helps in being more

responsive towards the unexpected changes so that

necessary adjustments can be made by Excite

entertainment.

Justification- Application of the rolling budget, nit

advisable in the situations that are not changing

constantly. It wastes the time and the energy in the

unvarying environments for preparing the rolling

budget.

Administration-the main disadvantage of the

rolling budget is that its similar t framing the new

budget on a continuous basis. It requires gathering

of the facts on a regular intervals from previous

budget. It needs the robust system of the

information in extracting the accurate information.

Cash budget- It means the budget of the expected receipts of the cash and the expenses for the

particular period. The cash inflows and the outflows include the revenue received, expenses paid,

receipt from loan and the payments.

Advantages Disadvantages

Practical benefits- Cash budget restricts Excite

entertainment in spending so that it does not incur

any debt. It involves the realistic assessment of the

money that will be occurred in coming years.

Strategic implications- It provides for the benefit in

Based on estimation- cash budget highly relies on

the anticipations for the future sales and the

collections of the future that will be received on

sales.

Manipulation- Cash budget might lead to

It does not focus on long term objectives which can

prove fatal for Excite entertainment.

Rolling budget- It referred as the revised budget that includes the revised financial plans for the

coming period of accounting which is used for replacing prior budget. It is also called as the

updated or new budget.

Advantages Disadvantages

Flexibility- Rolling budget record for the changes

from prior period into new budget (Nishimura,

2019). This leads to development of more flexible

and updated budget.

Responsiveness- This budget helps in being more

responsive towards the unexpected changes so that

necessary adjustments can be made by Excite

entertainment.

Justification- Application of the rolling budget, nit

advisable in the situations that are not changing

constantly. It wastes the time and the energy in the

unvarying environments for preparing the rolling

budget.

Administration-the main disadvantage of the

rolling budget is that its similar t framing the new

budget on a continuous basis. It requires gathering

of the facts on a regular intervals from previous

budget. It needs the robust system of the

information in extracting the accurate information.

Cash budget- It means the budget of the expected receipts of the cash and the expenses for the

particular period. The cash inflows and the outflows include the revenue received, expenses paid,

receipt from loan and the payments.

Advantages Disadvantages

Practical benefits- Cash budget restricts Excite

entertainment in spending so that it does not incur

any debt. It involves the realistic assessment of the

money that will be occurred in coming years.

Strategic implications- It provides for the benefit in

Based on estimation- cash budget highly relies on

the anticipations for the future sales and the

collections of the future that will be received on

sales.

Manipulation- Cash budget might lead to

making strategic decisions relating to the cash

requirements in the future.

underestimation of the expenses over the period of

budget (Alamri, 2019). The actual expenses that

incurred may not match with the budgeted figures

due to the manipulation in the budget.

LO4.

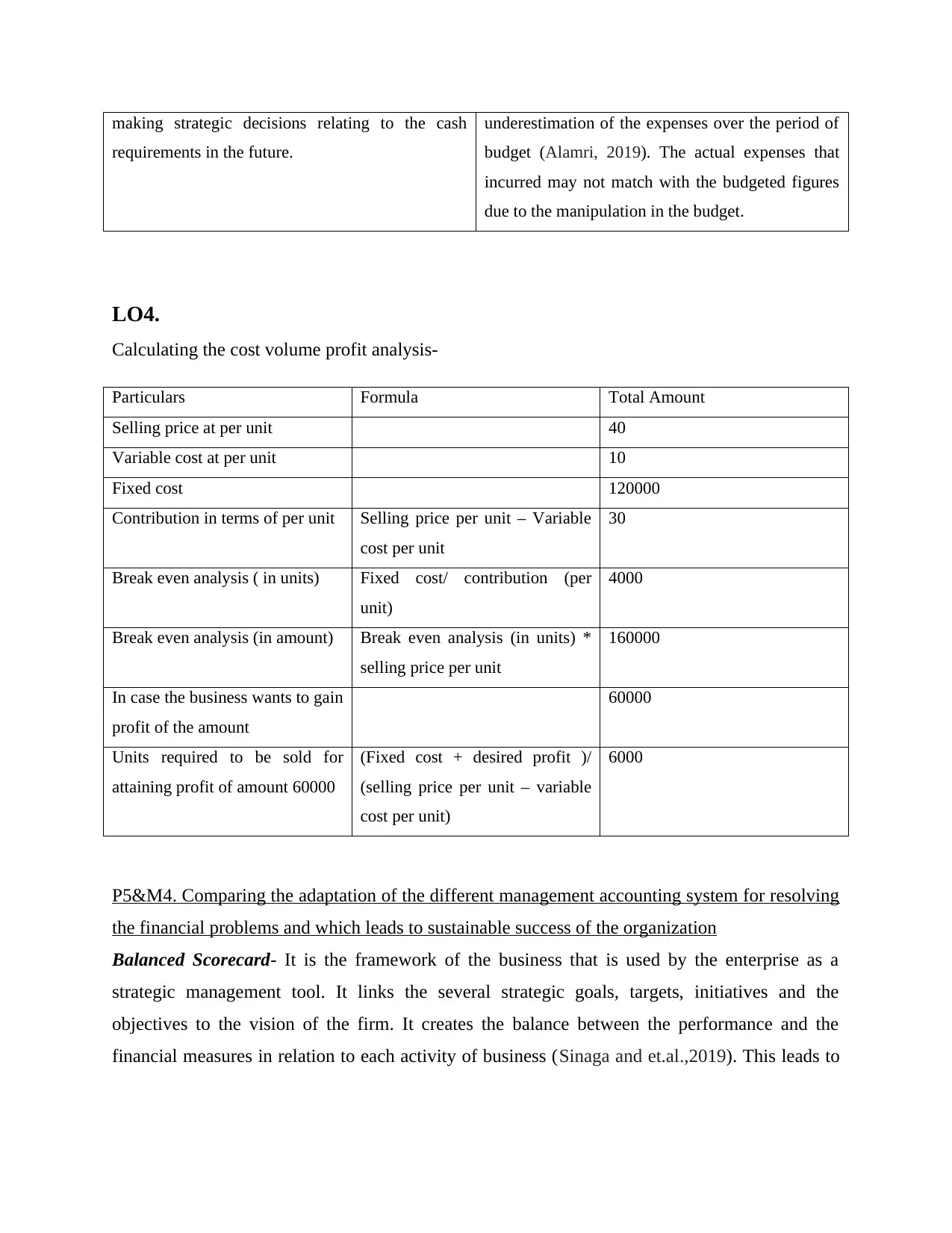

Calculating the cost volume profit analysis-

Particulars Formula Total Amount

Selling price at per unit 40

Variable cost at per unit 10

Fixed cost 120000

Contribution in terms of per unit Selling price per unit – Variable

cost per unit

30

Break even analysis ( in units) Fixed cost/ contribution (per

unit)

4000

Break even analysis (in amount) Break even analysis (in units) *

selling price per unit

160000

In case the business wants to gain

profit of the amount

60000

Units required to be sold for

attaining profit of amount 60000

(Fixed cost + desired profit )/

(selling price per unit – variable

cost per unit)

6000

P5&M4. Comparing the adaptation of the different management accounting system for resolving

the financial problems and which leads to sustainable success of the organization

Balanced Scorecard- It is the framework of the business that is used by the enterprise as a

strategic management tool. It links the several strategic goals, targets, initiatives and the

objectives to the vision of the firm. It creates the balance between the performance and the

financial measures in relation to each activity of business (Sinaga and et.al.,2019). This leads to

requirements in the future.

underestimation of the expenses over the period of

budget (Alamri, 2019). The actual expenses that

incurred may not match with the budgeted figures

due to the manipulation in the budget.

LO4.

Calculating the cost volume profit analysis-

Particulars Formula Total Amount

Selling price at per unit 40

Variable cost at per unit 10

Fixed cost 120000

Contribution in terms of per unit Selling price per unit – Variable

cost per unit

30

Break even analysis ( in units) Fixed cost/ contribution (per

unit)

4000

Break even analysis (in amount) Break even analysis (in units) *

selling price per unit

160000

In case the business wants to gain

profit of the amount

60000

Units required to be sold for

attaining profit of amount 60000

(Fixed cost + desired profit )/

(selling price per unit – variable

cost per unit)

6000

P5&M4. Comparing the adaptation of the different management accounting system for resolving

the financial problems and which leads to sustainable success of the organization

Balanced Scorecard- It is the framework of the business that is used by the enterprise as a

strategic management tool. It links the several strategic goals, targets, initiatives and the

objectives to the vision of the firm. It creates the balance between the performance and the

financial measures in relation to each activity of business (Sinaga and et.al.,2019). This leads to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.