Management Accounting Report: Tools, Techniques and Applications

VerifiedAdded on 2020/06/05

|26

|6243

|107

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its role in organizational performance and decision-making. It begins by defining management accounting and contrasting it with financial accounting, highlighting the different users, data sources, and regulatory frameworks. The report then delves into the importance of management accounting information as a decision-making tool for departmental managers, emphasizing its role in supporting strategic goals and integrating sustainability considerations. Various costing systems, including actual, normal, and standard costing, are examined, along with their applications in cost control and product costing. The report also discusses inventory management systems, job costing systems, and activity-based costing, providing insights into how these tools can be used to optimize resource allocation, improve efficiency, and support informed business decisions. Overall, the report offers a practical guide to management accounting principles and techniques, illustrating their significance in enhancing organizational performance and achieving sustainable success.

MANAGEMENT

ACCOUTING

ACCOUTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A). ...............................................................................................................................................1

b).................................................................................................................................................6

M1...............................................................................................................................................8

D1................................................................................................................................................8

TASK 2............................................................................................................................................9

M2 ............................................................................................................................................10

D2..............................................................................................................................................10

TASK 3..........................................................................................................................................10

M3.............................................................................................................................................14

TASK 4..........................................................................................................................................14

M4.............................................................................................................................................14

D3..............................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A). ...............................................................................................................................................1

b).................................................................................................................................................6

M1...............................................................................................................................................8

D1................................................................................................................................................8

TASK 2............................................................................................................................................9

M2 ............................................................................................................................................10

D2..............................................................................................................................................10

TASK 3..........................................................................................................................................10

M3.............................................................................................................................................14

TASK 4..........................................................................................................................................14

M4.............................................................................................................................................14

D3..............................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting systems are the most effective tools which assist the firm for

gaining the business in an effective manner. This report states that an important discussion about

the management accounting and its tools and techniques which is used in measurement and

planning for the organization to assess its overall performance and also involves the meaningful

explanations regarding the various management accounting system and they are necessary for the

sound organization activities to be coordinated with the management accounting reporting (King,

Clarkson and Wallace, 2010). This will help to make an understanding in regards to the

management accounting system. It involves the preparation of statement of income on the basis

of absorption and marginal costing. The reports will also talk about the usage of many tools of

planning which are mainly used in budgetary control as an evaluation of organization

performance appraisal.

TASK 1

A).

Management Accounting: It is also known as managerial accounting. Management

accounting is a well-defined process to recognizing, analysing, measuring, explaining and

communicating information for the chasing of an organization’s goals. This accounting covers

all the accounting fields aimed at advising management of business operations (Fullerton,

Kennedy and Widener, 2014). Management accountant uses information relating to the costs of

goods or services purchased by the organization. With the help of management accounting, the

manager formulates the policies, decisions, and strategies for day-to-day business operations of

an organization.

Implementation areas of management accounting:

Performance evaluation: It helps out the organization in evaluating the performance and

productivity of an employee. The performance evaluation can be done with the help of

comparing the actual performance with the planned performance which shows the

deviations on which needful steps can be taken and applied.

Risk appraisal: Another advantage of the management accounting is that it determines

and appraise the risk factors within the organization which can be eliminated with the

help of the well-defined organization management.

1

Management accounting systems are the most effective tools which assist the firm for

gaining the business in an effective manner. This report states that an important discussion about

the management accounting and its tools and techniques which is used in measurement and

planning for the organization to assess its overall performance and also involves the meaningful

explanations regarding the various management accounting system and they are necessary for the

sound organization activities to be coordinated with the management accounting reporting (King,

Clarkson and Wallace, 2010). This will help to make an understanding in regards to the

management accounting system. It involves the preparation of statement of income on the basis

of absorption and marginal costing. The reports will also talk about the usage of many tools of

planning which are mainly used in budgetary control as an evaluation of organization

performance appraisal.

TASK 1

A).

Management Accounting: It is also known as managerial accounting. Management

accounting is a well-defined process to recognizing, analysing, measuring, explaining and

communicating information for the chasing of an organization’s goals. This accounting covers

all the accounting fields aimed at advising management of business operations (Fullerton,

Kennedy and Widener, 2014). Management accountant uses information relating to the costs of

goods or services purchased by the organization. With the help of management accounting, the

manager formulates the policies, decisions, and strategies for day-to-day business operations of

an organization.

Implementation areas of management accounting:

Performance evaluation: It helps out the organization in evaluating the performance and

productivity of an employee. The performance evaluation can be done with the help of

comparing the actual performance with the planned performance which shows the

deviations on which needful steps can be taken and applied.

Risk appraisal: Another advantage of the management accounting is that it determines

and appraise the risk factors within the organization which can be eliminated with the

help of the well-defined organization management.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Presentation of the financial statement: Management accounting provides a proper

manner to present organization financial position with the help of necessary useful data

and information. Various data helps and make an easy way for the organization to

prepare the reports for strategies and decisions- making.

Apportionment of resources: An organization becomes capable to achieve the

utilization of resources in an effective and efficient manner with the help of allocation of

resources in a proper way to various divisions and departments within the organization.

This makes sure that the organization achieves its objectives and goals for a long-term

period.

1. Management Accounting vs. Financial Accounting:

There are so many differences between the management and financial accounting are

discussed as below:

Users of both accounting: - The management accounting mainly uses in internal by the

managers and employees of an organization whereas external users or outsiders of an

organization uses the financial accounting for decision-making that whether they invest their

money or not. External users include creditors, shareholders, and financial institutions.

Sources of data: - The management accounting uses the financial and non- financial data

in an organization whereas the financial accounting uses only the financial data which are based

on the accounting system of an organization.

Set of rules and regulations: - In management accounting, no standards or external rules

is applied whereas in the financial accounting various set of rules and regulations are applicable

to the organization.

Nature of both accounting: - The nature and source of information in the financial

accounting are historical which was related to the past performance of an organization whereas

the nature of information in the management accounting is primarily past, present and future-

oriented.

Reporting: - The management accounting provides information in an efficient and

effective manner to the management of an organization whereas the financial accounting gives

information regarding income and profit earning of the organization and also tells the sound

position of the organization.

2

manner to present organization financial position with the help of necessary useful data

and information. Various data helps and make an easy way for the organization to

prepare the reports for strategies and decisions- making.

Apportionment of resources: An organization becomes capable to achieve the

utilization of resources in an effective and efficient manner with the help of allocation of

resources in a proper way to various divisions and departments within the organization.

This makes sure that the organization achieves its objectives and goals for a long-term

period.

1. Management Accounting vs. Financial Accounting:

There are so many differences between the management and financial accounting are

discussed as below:

Users of both accounting: - The management accounting mainly uses in internal by the

managers and employees of an organization whereas external users or outsiders of an

organization uses the financial accounting for decision-making that whether they invest their

money or not. External users include creditors, shareholders, and financial institutions.

Sources of data: - The management accounting uses the financial and non- financial data

in an organization whereas the financial accounting uses only the financial data which are based

on the accounting system of an organization.

Set of rules and regulations: - In management accounting, no standards or external rules

is applied whereas in the financial accounting various set of rules and regulations are applicable

to the organization.

Nature of both accounting: - The nature and source of information in the financial

accounting are historical which was related to the past performance of an organization whereas

the nature of information in the management accounting is primarily past, present and future-

oriented.

Reporting: - The management accounting provides information in an efficient and

effective manner to the management of an organization whereas the financial accounting gives

information regarding income and profit earning of the organization and also tells the sound

position of the organization.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Audit and publication: - The audit and publication of the management accounting

statements and reports are not required, because these are used in the internally whereas in the

financial accounting the financial statements of the organization are published for the use of

general public and they are audited by the professional persons having qualified degree.

Following are the importance of the management accounting information as a decision-making

tool for department managers.

2. Importance of MA information as a decision-making tools for departmental managers:

Management accounting is the most effective tool which helps the organisation for

gaining the sustainability in an effective manner. Here are some of the benefits of the MA

systems. The management accounting role in the sustainable success of the organization business

can be explained and summarized in below:

The manager of the organization will need to support the sustainable and strategic goals

with the policies and strategies which are previously developed.

The management accounting assists in the manufacturing and production reports that

involves sustainability information, which helps the managers in understanding the

pricing and decisions regarding the budgets and planning of essential strategies (DRURY,

2013).

The management accounting techniques and useful tools like standard costing, ABC,

marginal and absorption costing etc, will assist in the integration of matters in the

sustainable which involves various processes of decision-making.

Assists the organization in the development of a reporting strategy that will consolidate

with the issues of sustainability which in turn will allow accessing the non-financial and

financial useful information.

Activity-based costing method: - It allocates the overhead to those items which are

actually produced and use it. The ABC can be used to minimize the targeted overhead costs. It

best works in an environment which is complex, where there are so many products and machines

are used to manufacturing. It helps in identifying the activities that an organization performs and

then assign indirect costs to products which are produced. It helps the organization to make and

develop a much better way focus on corporate and strategy regarding the costs (Dillard and

Roslender, 2011).

3

statements and reports are not required, because these are used in the internally whereas in the

financial accounting the financial statements of the organization are published for the use of

general public and they are audited by the professional persons having qualified degree.

Following are the importance of the management accounting information as a decision-making

tool for department managers.

2. Importance of MA information as a decision-making tools for departmental managers:

Management accounting is the most effective tool which helps the organisation for

gaining the sustainability in an effective manner. Here are some of the benefits of the MA

systems. The management accounting role in the sustainable success of the organization business

can be explained and summarized in below:

The manager of the organization will need to support the sustainable and strategic goals

with the policies and strategies which are previously developed.

The management accounting assists in the manufacturing and production reports that

involves sustainability information, which helps the managers in understanding the

pricing and decisions regarding the budgets and planning of essential strategies (DRURY,

2013).

The management accounting techniques and useful tools like standard costing, ABC,

marginal and absorption costing etc, will assist in the integration of matters in the

sustainable which involves various processes of decision-making.

Assists the organization in the development of a reporting strategy that will consolidate

with the issues of sustainability which in turn will allow accessing the non-financial and

financial useful information.

Activity-based costing method: - It allocates the overhead to those items which are

actually produced and use it. The ABC can be used to minimize the targeted overhead costs. It

best works in an environment which is complex, where there are so many products and machines

are used to manufacturing. It helps in identifying the activities that an organization performs and

then assign indirect costs to products which are produced. It helps the organization to make and

develop a much better way focus on corporate and strategy regarding the costs (Dillard and

Roslender, 2011).

3

Make or buy decisions: - The main use of management accounting information is to

render useful information which is used in manufacturing the products. A make or buy decisions

is the action of selecting in between manufacturing a product or purchasing it from the outsider

or external suppliers.

Utilization of useful and relevant data: - The management accounting information

gives a data which is useful to make a strategy and decisions for the growth of an organization

business..

3. Cost Accounting Systems (actual, normal and standard costing): -

The cost accounting system helps the organization to forecast the cost of the product

which they want to produce. The managers of the organization make the analysis of profitability,

inventory and cost control of the products. Cost accounting is the major concept of the

management accounting which offers the useful tools and techniques of budgetary control,

standard and marginal costing and inventory control which are used by the management of the

organization to improve their productivity in the product (Contrafatto and Burns, 2013).

Actual costing: it records the costs of the product on the basis of following factors:

The actual cost of materials

The actual cost of labor

The actual overhead costs incurred and allocated using the actual quantity.

The main point in an actual costing system is that it uses only the actual costs incurred

and allocated using the actual quantity produced. It does not use any budgeted or

standards. It is very simplest costing which is not required any pre-planning of standard

costs.

Normal costing: It is used to derive the product costs. It includes the following factors:

The actual cost of materials

The actual cost of labour

The standard overhead rate that is applied by using the actual usage of the product of

whatsoever allocation base is being used (machine hours or direct labour hours)

The normal costing is different from the standard costing, in the standard costing, the

standards cost is pre-determined, while in the normal costing the actual costs are used for

the materials and labour.

4

render useful information which is used in manufacturing the products. A make or buy decisions

is the action of selecting in between manufacturing a product or purchasing it from the outsider

or external suppliers.

Utilization of useful and relevant data: - The management accounting information

gives a data which is useful to make a strategy and decisions for the growth of an organization

business..

3. Cost Accounting Systems (actual, normal and standard costing): -

The cost accounting system helps the organization to forecast the cost of the product

which they want to produce. The managers of the organization make the analysis of profitability,

inventory and cost control of the products. Cost accounting is the major concept of the

management accounting which offers the useful tools and techniques of budgetary control,

standard and marginal costing and inventory control which are used by the management of the

organization to improve their productivity in the product (Contrafatto and Burns, 2013).

Actual costing: it records the costs of the product on the basis of following factors:

The actual cost of materials

The actual cost of labor

The actual overhead costs incurred and allocated using the actual quantity.

The main point in an actual costing system is that it uses only the actual costs incurred

and allocated using the actual quantity produced. It does not use any budgeted or

standards. It is very simplest costing which is not required any pre-planning of standard

costs.

Normal costing: It is used to derive the product costs. It includes the following factors:

The actual cost of materials

The actual cost of labour

The standard overhead rate that is applied by using the actual usage of the product of

whatsoever allocation base is being used (machine hours or direct labour hours)

The normal costing is different from the standard costing, in the standard costing, the

standards cost is pre-determined, while in the normal costing the actual costs are used for

the materials and labour.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The normal costing means a manner to find out the cost of a manufactured item using the

product costs.

Standard costing: It involves the creation of estimated or standard costs for some or all

the activities of the manufacturing company. The standard costs are a close approximation of

actual costs. The cost accountant of the company calculates the variances. It also changes the

standard costs to bring closer alignment with the actual cost.

The following elements used by the accountant in the standard costing are:

The standard cost of materials

The standard cost of labour

The standard overhead rate

It is the most effective and important method available for the controlling the costs and

the performance.

4. Inventory management system: - This method of management accounting system is

concerned with the management and supervision of inventory of the organization. This system

track goods and raw materials through the entire supply chain or the portion which are used in

the manufacturing operations. It covers almost everything from production to retail and all

movements of inventory. The process of TECH (UK) LTD. can be mixed with this type of

system to attain effective and efficient flow of stock inside the organization and at the time of

sale. The organization must have an effective inventory control system to control the wastage of

the inventory and the essentials elements are: -

Identification and classification of inventories.

Setting minimum and maximum limits for each and every part of the inventory in the

organization.

Economic order quantity.

There should be adequate storage facilities.

Adequate reports and records.

Coordination, budgeting, and internal check.

Inventory management system is optimum used after knowing the final inventory in an

effective manner. But the problem is that, inventory management system is effectively used by

using FIFO, LIFO AVCO method which would ultimately assist the organization in order to

assist the organization for making the business sustainability

5

product costs.

Standard costing: It involves the creation of estimated or standard costs for some or all

the activities of the manufacturing company. The standard costs are a close approximation of

actual costs. The cost accountant of the company calculates the variances. It also changes the

standard costs to bring closer alignment with the actual cost.

The following elements used by the accountant in the standard costing are:

The standard cost of materials

The standard cost of labour

The standard overhead rate

It is the most effective and important method available for the controlling the costs and

the performance.

4. Inventory management system: - This method of management accounting system is

concerned with the management and supervision of inventory of the organization. This system

track goods and raw materials through the entire supply chain or the portion which are used in

the manufacturing operations. It covers almost everything from production to retail and all

movements of inventory. The process of TECH (UK) LTD. can be mixed with this type of

system to attain effective and efficient flow of stock inside the organization and at the time of

sale. The organization must have an effective inventory control system to control the wastage of

the inventory and the essentials elements are: -

Identification and classification of inventories.

Setting minimum and maximum limits for each and every part of the inventory in the

organization.

Economic order quantity.

There should be adequate storage facilities.

Adequate reports and records.

Coordination, budgeting, and internal check.

Inventory management system is optimum used after knowing the final inventory in an

effective manner. But the problem is that, inventory management system is effectively used by

using FIFO, LIFO AVCO method which would ultimately assist the organization in order to

assist the organization for making the business sustainability

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FIFO method: This stands for “first in first out”, which simply means that the raw

material which comes at the beginning of the year would ultimately release firstly.

LIFO method: This stands for “last in first out” which simply means that the goods

which comes at last is ultimately released firstly.

AVCO method: This stands for average inventory costs during a certain period of time.

This is calculated by dividing cost of goods in stock by number of goods in the inventory level at

any point of time.

5. Job costing system: This system of costing includes the process of collecting information

about the costs which is associated with the particular production job. A job costing system

accumulates the following three types of information:

Direct materials

Direct labour

Overheads

Job costing system customized the requirements of the customer. Some customers only

permit certain costs to be charged to their jobs (Cinquini and Tenucci, 2010). The TECH (UK)

LTD. uses this costing system when the products are identical or customized according to the

customers need and keep track expenses on these jobs. It consists the following procedures are:

Receiving inquiry from the customers about the price, quality of the materials are used to

complete the job.

Keeping the tastes and preferences of the customers in the mind while manufacturing the

products.

The order will be placed to the customer when the price is assured by him.

Each and every cost related to the production process is to be recorded (Christ and

Burritt, 2013).

Once the job is complete, a report is given to the cost department of the organization for

finalizing the job costing. The comparison is done with the help of estimated cost which

was already prepared by the cost accountant.

Job costing systems are of various types. Some of them are: Batch Costing, Contract Costing,

process costing, and service costing. These are defined in details:

6

material which comes at the beginning of the year would ultimately release firstly.

LIFO method: This stands for “last in first out” which simply means that the goods

which comes at last is ultimately released firstly.

AVCO method: This stands for average inventory costs during a certain period of time.

This is calculated by dividing cost of goods in stock by number of goods in the inventory level at

any point of time.

5. Job costing system: This system of costing includes the process of collecting information

about the costs which is associated with the particular production job. A job costing system

accumulates the following three types of information:

Direct materials

Direct labour

Overheads

Job costing system customized the requirements of the customer. Some customers only

permit certain costs to be charged to their jobs (Cinquini and Tenucci, 2010). The TECH (UK)

LTD. uses this costing system when the products are identical or customized according to the

customers need and keep track expenses on these jobs. It consists the following procedures are:

Receiving inquiry from the customers about the price, quality of the materials are used to

complete the job.

Keeping the tastes and preferences of the customers in the mind while manufacturing the

products.

The order will be placed to the customer when the price is assured by him.

Each and every cost related to the production process is to be recorded (Christ and

Burritt, 2013).

Once the job is complete, a report is given to the cost department of the organization for

finalizing the job costing. The comparison is done with the help of estimated cost which

was already prepared by the cost accountant.

Job costing systems are of various types. Some of them are: Batch Costing, Contract Costing,

process costing, and service costing. These are defined in details:

6

Batch costing: Under this, cost of a particular batch is calculated. This is a kind of

particular order costing. Within each batch, a number of identical units are comprised but

each batch would be different.

Contract Costing: This is a kind of knowing of the costs which are linked to particular

contract with a consumer. For instance, an organization bids for a huge construction

project along with the prospective consumer, and two parties have decided in a contract

for a particular kind of reimbursement to the organization.

b).

1. Different types of management accounting reports are: -

The management accounting uses different kinds of reports to help the organization

management in preparing the accurate management reports and also help to make the decisions

regarding in critical business situations. They also give the reliable and accurate data and

information of the financial position of the organization to the managers. The various reports are

prepared by the management accountant and their advantages are discussed as below: -

Reports on budgets: - The budgets are prepared to analyse the company performance in

all aspects. With the help of budgets, the managers of the organization review and analysis each

department performance and the related cost which is incurred. The estimated budgets are

usually depending upon the actual costs from the previous years (Østergren and Stensaker,

2011). With the help of this estimation, the actual figure is compared with the budgeted figure

and then analyses it in an efficient and effective manner. The TECH (UK) LTD. uses budget

reports to control the unexpected costs and expenses and also compare the actual outcomes with

the budgeted. If the variances or differences incurred are favourable to the organization, then it

reflects the good performance of each and every department. But if, variances incurred are

negative or adverse, then the managers will overcome these adverse issues more efficient way.

Accounting receivable report: - This type of report is basically concerned with the

receivables for those organizations which want to extend the credit policies to their loyal

customers. Under this accounting receivable reports, all the earnings which are arises or assumed

that earnings which are received in the future, are to recorded properly (Parker, 2012.). This

report helps the organization to analysis the credit policy and at what point they need to tighten

the policy of the credit. This assures minimizing the old bad debts and liquidity of the

organization should be maintained.

7

particular order costing. Within each batch, a number of identical units are comprised but

each batch would be different.

Contract Costing: This is a kind of knowing of the costs which are linked to particular

contract with a consumer. For instance, an organization bids for a huge construction

project along with the prospective consumer, and two parties have decided in a contract

for a particular kind of reimbursement to the organization.

b).

1. Different types of management accounting reports are: -

The management accounting uses different kinds of reports to help the organization

management in preparing the accurate management reports and also help to make the decisions

regarding in critical business situations. They also give the reliable and accurate data and

information of the financial position of the organization to the managers. The various reports are

prepared by the management accountant and their advantages are discussed as below: -

Reports on budgets: - The budgets are prepared to analyse the company performance in

all aspects. With the help of budgets, the managers of the organization review and analysis each

department performance and the related cost which is incurred. The estimated budgets are

usually depending upon the actual costs from the previous years (Østergren and Stensaker,

2011). With the help of this estimation, the actual figure is compared with the budgeted figure

and then analyses it in an efficient and effective manner. The TECH (UK) LTD. uses budget

reports to control the unexpected costs and expenses and also compare the actual outcomes with

the budgeted. If the variances or differences incurred are favourable to the organization, then it

reflects the good performance of each and every department. But if, variances incurred are

negative or adverse, then the managers will overcome these adverse issues more efficient way.

Accounting receivable report: - This type of report is basically concerned with the

receivables for those organizations which want to extend the credit policies to their loyal

customers. Under this accounting receivable reports, all the earnings which are arises or assumed

that earnings which are received in the future, are to recorded properly (Parker, 2012.). This

report helps the organization to analysis the credit policy and at what point they need to tighten

the policy of the credit. This assures minimizing the old bad debts and liquidity of the

organization should be maintained.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job cost report: - Job cost reports show the costs or expenses and profitability of the

specific job. It helps the organization to determines the more profitable areas so that they could

fully concentrate on these areas rather than wasting the time and other resources on jobs which

are less profitable. It is used to review the costs and other expenses at the time when the products

are manufacturing which helps the managers to reduce the unwanted waste before the costs

maximize.

Inventory Management report: - When the organization doing the manufacturing

process they have to prepare this kind of reports so that the inventory utilized in the more

appropriate manner in the manufacturing process. This report helps the organization, to track the

inventory level whether it is maximum or minimum and in danger level. With this report, the

managers take the accurate decisions regarding the inventory. This report includes the various

cost related to the labour and overhead per unit and wastages concerned with the inventory.

Performance report: - In this report, the information regarding the performance of the

organization is recorded, after analysing the actual performance with the planned performance.

The performance report is prepared annually. With the help of this report, the managers make the

effective and productive strategy which helps the organization to earn more benefits in the

future. Various stakeholders use this performance report to analyse the performance and after

that, they invest in the organization (Frezatti, Aguiar, Guerreiro and Gouvea, 2011).

2. Importance of implementing accounting reporting systems:

It is crucial for the management accounting reporting which provides assistance to the

organisation to identify the organisation entire crucial financial transactions in the elaborated

structure. By using of all the above mentioned report, company could assess the organisation for

assessing their performance level, lowering the wastage of the resources, limiting the unwanted

costs, enhances their productivity and much more. These kinds of report assisting to make

strategies, goals and pre-set objectives for the future period of time.

M1

By using management accounting systems, cited company could implement an effective

strategy that could implement in an effective manner. As Job costing system will assist the

TECH (UK) LTD. in the approximation of all kinds of expenses or costs related to the

manufacturing the products. It also helps in overall check on the quality performance done by the

labour.

8

specific job. It helps the organization to determines the more profitable areas so that they could

fully concentrate on these areas rather than wasting the time and other resources on jobs which

are less profitable. It is used to review the costs and other expenses at the time when the products

are manufacturing which helps the managers to reduce the unwanted waste before the costs

maximize.

Inventory Management report: - When the organization doing the manufacturing

process they have to prepare this kind of reports so that the inventory utilized in the more

appropriate manner in the manufacturing process. This report helps the organization, to track the

inventory level whether it is maximum or minimum and in danger level. With this report, the

managers take the accurate decisions regarding the inventory. This report includes the various

cost related to the labour and overhead per unit and wastages concerned with the inventory.

Performance report: - In this report, the information regarding the performance of the

organization is recorded, after analysing the actual performance with the planned performance.

The performance report is prepared annually. With the help of this report, the managers make the

effective and productive strategy which helps the organization to earn more benefits in the

future. Various stakeholders use this performance report to analyse the performance and after

that, they invest in the organization (Frezatti, Aguiar, Guerreiro and Gouvea, 2011).

2. Importance of implementing accounting reporting systems:

It is crucial for the management accounting reporting which provides assistance to the

organisation to identify the organisation entire crucial financial transactions in the elaborated

structure. By using of all the above mentioned report, company could assess the organisation for

assessing their performance level, lowering the wastage of the resources, limiting the unwanted

costs, enhances their productivity and much more. These kinds of report assisting to make

strategies, goals and pre-set objectives for the future period of time.

M1

By using management accounting systems, cited company could implement an effective

strategy that could implement in an effective manner. As Job costing system will assist the

TECH (UK) LTD. in the approximation of all kinds of expenses or costs related to the

manufacturing the products. It also helps in overall check on the quality performance done by the

labour.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounting systems Benefits

Cost accounting system It is vital for the company to evaluate total cost for estimating the

cost of their product for increasing the productivity of the company.

Inventory management

system

According to this system, it has been seen that overall management

and control of stock those are kept by the company can be determine

effectively under this report.

Job costing system It is used to deliver various unique advantage those are set as

important process in costing methods.

D1

Budget reports: The integration in between the process of TECH (UK) LTD and the

budget reports make a way for the company activities and the managers can concentrate on the

objectives and targeted results in a proper manner.

Accounts receivable report: The integration between both of them, helps the managers

to collects the receivables on the time and also helps to create the proper collection policy that

should be analysed on daily basis for the accuracy and its flexibility.

Job cost reports: The TECH (UK) LTD. activities should be oriented towards the cost

objectives achievement and the job cost reports which make easier to finalize the strategy

regarding the price and minimizing the whole cost regarding the products (Baldvinsdottir,

Mitchell and Nørreklit, 2010).

There is certain other reporting method which will be helpful in recording all essential

transaction that are done during an accounting period of time. Inventory management report can

be used to record opening and closing stocks of the company. while in case of performance

report that consists of specific information about company’s current year performance to the with

past one.

9

Cost accounting system It is vital for the company to evaluate total cost for estimating the

cost of their product for increasing the productivity of the company.

Inventory management

system

According to this system, it has been seen that overall management

and control of stock those are kept by the company can be determine

effectively under this report.

Job costing system It is used to deliver various unique advantage those are set as

important process in costing methods.

D1

Budget reports: The integration in between the process of TECH (UK) LTD and the

budget reports make a way for the company activities and the managers can concentrate on the

objectives and targeted results in a proper manner.

Accounts receivable report: The integration between both of them, helps the managers

to collects the receivables on the time and also helps to create the proper collection policy that

should be analysed on daily basis for the accuracy and its flexibility.

Job cost reports: The TECH (UK) LTD. activities should be oriented towards the cost

objectives achievement and the job cost reports which make easier to finalize the strategy

regarding the price and minimizing the whole cost regarding the products (Baldvinsdottir,

Mitchell and Nørreklit, 2010).

There is certain other reporting method which will be helpful in recording all essential

transaction that are done during an accounting period of time. Inventory management report can

be used to record opening and closing stocks of the company. while in case of performance

report that consists of specific information about company’s current year performance to the with

past one.

9

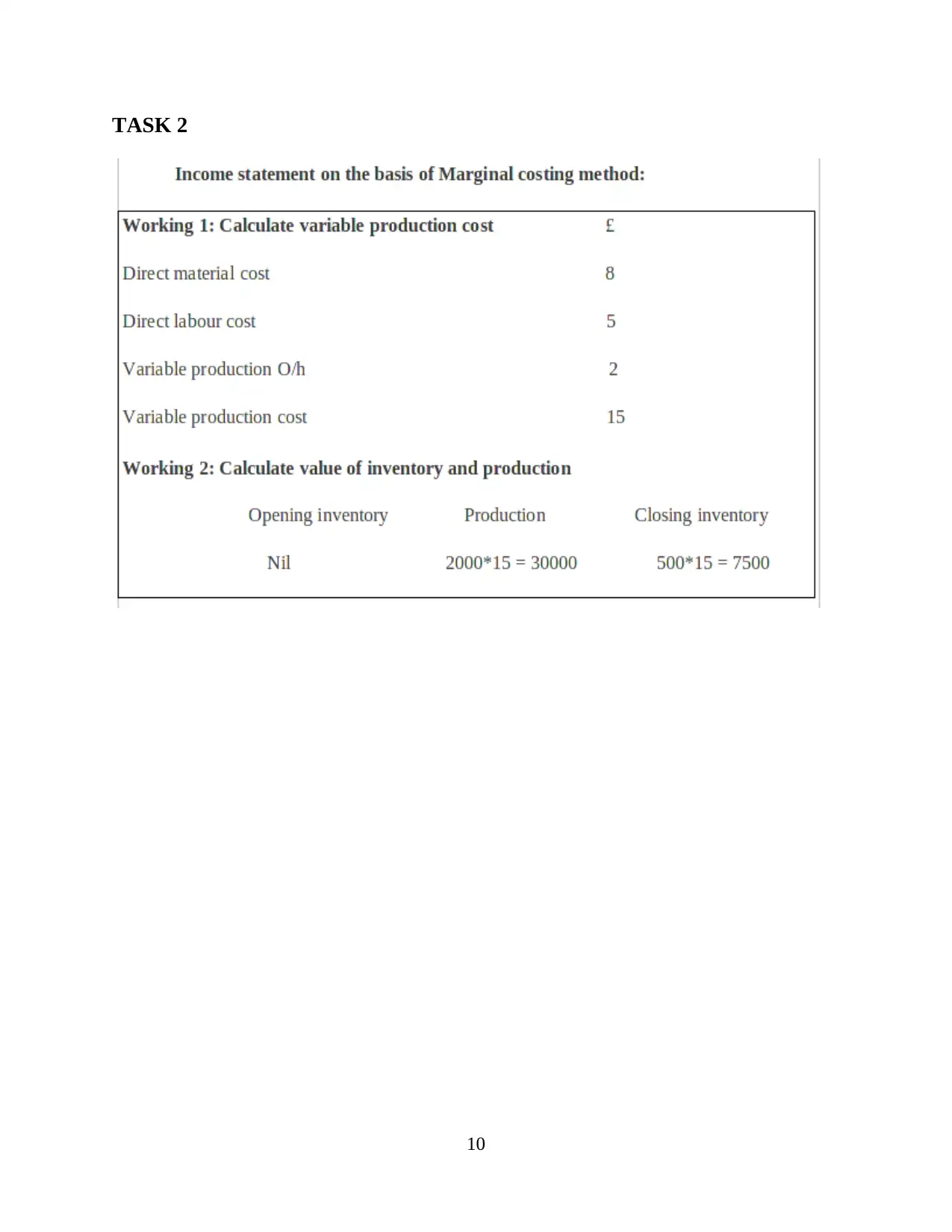

TASK 2

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 26

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.