Management Accounting Report: Costing, Budgeting, and Analysis

VerifiedAdded on 2020/10/23

|19

|5435

|172

Report

AI Summary

This report provides a detailed analysis of management accounting principles and techniques, focusing on their application within R. Robson & Son Ltd. It begins with an introduction to management accounting, its different types, and their importance, including cost accounting, inventory management, and job costing systems. The report then delves into specific management accounting reports such as budget reports, accounts receivable aging reports, job cost reports, and inventory and manufacturing reports. The benefits of management accounting systems, including increased efficiency, profit maximization, goal setting, planning, and organizing, are also discussed. The report critically evaluates the integration of management accounting systems and reporting within R. Robson Ltd., highlighting its strengths and weaknesses. Furthermore, the report explores costing methods, including absorption and marginal costing, with calculations of net income using each method. It also includes break-even analysis and a financial report on management accounting techniques. Finally, the report examines planning tools for budgetary control, their advantages and disadvantages, and their application in preparing, forecasting, and analyzing budgets. It concludes with a comparison of R. Robson's management accounting system with other companies in the same industry and addresses planning tools to resolve financial problems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management Accounting .................................................................................................1

B) Types of management accounting reports and importance ..............................................2

C) Benefits of Management Accounting Systems..................................................................3

D) Critical evaluation of the integration of management accounting system and reporting in R.

Robson Ltd.............................................................................................................................4

TASK 2............................................................................................................................................5

A1. Absorption Costing and Marginal Costing Methods.......................................................5

A2. Calculation of net income as per abortion and marginal costing method.......................5

B & D. Calculation on Break-even analysis...........................................................................7

C. Financial report on management accounting techniques to General Manager..................9

TASK 3............................................................................................................................................9

A. The advantage and disadvantage of planning tools of budgetary control.........................9

B. The application of planning tools for preparing, forecasting and analysing budgets......11

C. Comparing the management accounting system of R. Robson with other company in same

industry.................................................................................................................................12

D. Management Accounting Techniques.............................................................................13

E. Planning tools in order to resolve financial problems in business..................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A) Management Accounting .................................................................................................1

B) Types of management accounting reports and importance ..............................................2

C) Benefits of Management Accounting Systems..................................................................3

D) Critical evaluation of the integration of management accounting system and reporting in R.

Robson Ltd.............................................................................................................................4

TASK 2............................................................................................................................................5

A1. Absorption Costing and Marginal Costing Methods.......................................................5

A2. Calculation of net income as per abortion and marginal costing method.......................5

B & D. Calculation on Break-even analysis...........................................................................7

C. Financial report on management accounting techniques to General Manager..................9

TASK 3............................................................................................................................................9

A. The advantage and disadvantage of planning tools of budgetary control.........................9

B. The application of planning tools for preparing, forecasting and analysing budgets......11

C. Comparing the management accounting system of R. Robson with other company in same

industry.................................................................................................................................12

D. Management Accounting Techniques.............................................................................13

E. Planning tools in order to resolve financial problems in business..................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

1

INTRODUCTION

Management accounting plays a significant role in the survival and growth of a business

organisation. In today's competitive business environment, organisation needs to have a proper

management accounting system to ensure efficient running of the financial needs of company.

An effective management accounting information system will provide accurate financial

information to the management to make planning and decisions regarding investment and

enhancing organisational performance. The present report will help in understanding different

management accounting systems and techniques. Further, the importance of different

management accounting reports will be discussed. Study will help to understand different

systems of costing including absorption and marginal by calculating net income through each

method. A financial report is also included in the report.

The report will also address cost volume profit analysis. Present study will demonstrate

the planning tools for budgetary control. Report will also address the significance of planning

tools to solve financial problem of organisation to sustainable success.

TASK 1

A) Management Accounting

To,

The General Manager

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

Management accounting is the process of examining costs and operations of business for

preparing financial report, records and account that help managers to make decisions for

achieving R ROBSON & SON LIMITED's goals. It helps management in performing functions

like planning, organising, staffing, directing and controlling. In other words, it relates to make

financial and costing data with translating the same into useful information for management

within an organization (Otley, 2016).

1

Management accounting plays a significant role in the survival and growth of a business

organisation. In today's competitive business environment, organisation needs to have a proper

management accounting system to ensure efficient running of the financial needs of company.

An effective management accounting information system will provide accurate financial

information to the management to make planning and decisions regarding investment and

enhancing organisational performance. The present report will help in understanding different

management accounting systems and techniques. Further, the importance of different

management accounting reports will be discussed. Study will help to understand different

systems of costing including absorption and marginal by calculating net income through each

method. A financial report is also included in the report.

The report will also address cost volume profit analysis. Present study will demonstrate

the planning tools for budgetary control. Report will also address the significance of planning

tools to solve financial problem of organisation to sustainable success.

TASK 1

A) Management Accounting

To,

The General Manager

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

Management accounting is the process of examining costs and operations of business for

preparing financial report, records and account that help managers to make decisions for

achieving R ROBSON & SON LIMITED's goals. It helps management in performing functions

like planning, organising, staffing, directing and controlling. In other words, it relates to make

financial and costing data with translating the same into useful information for management

within an organization (Otley, 2016).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The different types of management accounting systems are as follows:-

Cost Accounting System: It is a framework that is used by the firms in order to estimate

value of their products for analysing its profitability, inventory valuation and cost control.

Cost accounting is a key concept of management accounting because it offers various

analytical tools such as marginal, operating, standard and budgetary and inventory

control. The two main cost accounting systems are job order and process costing. Thus,

having a proper cost accounting helps the company to analyse the profitability of the

individual products and services or jobs and different departments as well as operations

of R ROBSON & SON LIMITED. Hence, cost accounting helps the selected company to

cover the cost and generate the level of profit accepted.

Inventory Management System: It combines the application of consumables, stock,

goods and supplies. Its goal and objective is to know current inventory level and it

minimizes the situation of overstock and under stock. Its benefits are improvement of R

ROBSON & SON LIMITED's bottom line, workflow and inventory accuracy. Thus, this

system aims to provide an efficient interface and calculates the amount of usage for

specific set days. The user of the selected company do not have to calculate the usage

manually but the system does everything.

Job Costing System: It is a process of accumulating information about costs associated

with the service job (Fullerton, Kennedy and Widener, 2014). It is applied when goods

processed are different from each other. It is required to accumulate information related

to direct labour, materials and overhead costs. Thus, job costing is suitable in deriving the

cost of constructing the custom machine, the software programme designed or

manufacturing limited batch of products.

Price Optimising System: It refers to the mathematical programs that are used to

calculate variations in demand at different levels of price by combining that data with

information on costs and inventory level to improve profits. Thus, this system helps the

quoted company to determine initial pricing, promotional and discount pricing and helps

to set the temporary prices to increase the sales of the items.

Thanks and Regards

Management Accounting Officer

2

Cost Accounting System: It is a framework that is used by the firms in order to estimate

value of their products for analysing its profitability, inventory valuation and cost control.

Cost accounting is a key concept of management accounting because it offers various

analytical tools such as marginal, operating, standard and budgetary and inventory

control. The two main cost accounting systems are job order and process costing. Thus,

having a proper cost accounting helps the company to analyse the profitability of the

individual products and services or jobs and different departments as well as operations

of R ROBSON & SON LIMITED. Hence, cost accounting helps the selected company to

cover the cost and generate the level of profit accepted.

Inventory Management System: It combines the application of consumables, stock,

goods and supplies. Its goal and objective is to know current inventory level and it

minimizes the situation of overstock and under stock. Its benefits are improvement of R

ROBSON & SON LIMITED's bottom line, workflow and inventory accuracy. Thus, this

system aims to provide an efficient interface and calculates the amount of usage for

specific set days. The user of the selected company do not have to calculate the usage

manually but the system does everything.

Job Costing System: It is a process of accumulating information about costs associated

with the service job (Fullerton, Kennedy and Widener, 2014). It is applied when goods

processed are different from each other. It is required to accumulate information related

to direct labour, materials and overhead costs. Thus, job costing is suitable in deriving the

cost of constructing the custom machine, the software programme designed or

manufacturing limited batch of products.

Price Optimising System: It refers to the mathematical programs that are used to

calculate variations in demand at different levels of price by combining that data with

information on costs and inventory level to improve profits. Thus, this system helps the

quoted company to determine initial pricing, promotional and discount pricing and helps

to set the temporary prices to increase the sales of the items.

Thanks and Regards

Management Accounting Officer

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B) Types of management accounting reports and importance

To,

The General Manager

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

Hereby enclosing the details about different management accounting reports that

company can use along with their importance.

Budget Report: It is one of the most important reports of management accounting as it

helps small business owners in analysing performance of their company and managers in

examining performance of their department for controlling costs. Budget report is

important to R ROBSON & SON LIMITED as it is used by both; manager as well as

owner for providing incentives and bonuses to its employees (Cooper, Ezzamel and Qu,

2017). Budget report is important to rectify errors, revise budget and for taking remedial

action without any delay.

Accounts Receivable Aging Report: It is a critical tool that is used in managing the flow

of cash. It also includes separate columns for those items that are 30, 60 and 90 days late.

This report is used by the managers in order to find problems that are related to collection

procedure followed by R ROBSON & SON LIMITED. Its importance is that customers

come to know that late payment is not accepted (Suomala, Lyly-Yrjänäinen and Lukka,

2014). Thus, aging report helps company to understand the outstanding receivables and

their quality and it is also used to determine the value of receivable portfolio.

Job Cost Report: It shows the total cost incurred by a single project as compared to their

expectations to evaluate the profitability of job by estimating its revenue. It is also

essential for examining the expenses when project is in progress so that waste can be

controlled. With the help of this report, leaders can evaluate various financial gains of

3

To,

The General Manager

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

Hereby enclosing the details about different management accounting reports that

company can use along with their importance.

Budget Report: It is one of the most important reports of management accounting as it

helps small business owners in analysing performance of their company and managers in

examining performance of their department for controlling costs. Budget report is

important to R ROBSON & SON LIMITED as it is used by both; manager as well as

owner for providing incentives and bonuses to its employees (Cooper, Ezzamel and Qu,

2017). Budget report is important to rectify errors, revise budget and for taking remedial

action without any delay.

Accounts Receivable Aging Report: It is a critical tool that is used in managing the flow

of cash. It also includes separate columns for those items that are 30, 60 and 90 days late.

This report is used by the managers in order to find problems that are related to collection

procedure followed by R ROBSON & SON LIMITED. Its importance is that customers

come to know that late payment is not accepted (Suomala, Lyly-Yrjänäinen and Lukka,

2014). Thus, aging report helps company to understand the outstanding receivables and

their quality and it is also used to determine the value of receivable portfolio.

Job Cost Report: It shows the total cost incurred by a single project as compared to their

expectations to evaluate the profitability of job by estimating its revenue. It is also

essential for examining the expenses when project is in progress so that waste can be

controlled. With the help of this report, leaders can evaluate various financial gains of

3

jobs and focus on those jobs which are the most profitable. It leads to profitability, proper

management decision and financial reporting (Melnyk and et.al, 2014). This report helps

the management to provide information about each and every job so that review can be

made about greater transparency

Inventory and Manufacturing Report: It includes items such as inventory waste,

labour and per-unit overheads costs involved in the process of production. This report is

useful for those companies which maintain physical products or inventory (Types of

Managerial Accounting Reports, 2018). It is important for highlighting the areas of

improvement and offering bonuses to the best one. The importance of inventory and

manufacturing report is to keep records of various things like inventory change, purchase

order, multi stock location, etc. (Gibassier, 2017). This report is important for the

manager as it includes accurate record of cost of goods sold and the cost involved for

manufacturing goods.

Thanks and Regards

Management Accounting Officer

C) Benefits of Management Accounting Systems

Management accounting system is helpful for business, advantage of this are given as below:

Increases efficiency: Management accounting systems helps R ROBSON & SON

LIMITED in increasing its efficiency for performing various operations by eliminating

various kinds of wastages and defectives. It motivates employees to give better

performance and receive rewards in the form of promotions.

Maximization of profits: Management accounting helps to compare actual performance

with standard budgets to analyse deviations. If deviations are found then management is

required to take corrective actions for maximising profits (Flamholtz and et.al, 2016).

Goal setting: Management accounting helps managers at the time of setting goals and

making adjustments in order to motivate employees for achieving the ultimate goal. It

helps in improving relationship between management and labour.

Planning: Management accounting focuses on planning for future which includes

information of specific products, market reach and regional information. These

information are obtained from budgets, surveys and competitor analysis. For proper

4

management decision and financial reporting (Melnyk and et.al, 2014). This report helps

the management to provide information about each and every job so that review can be

made about greater transparency

Inventory and Manufacturing Report: It includes items such as inventory waste,

labour and per-unit overheads costs involved in the process of production. This report is

useful for those companies which maintain physical products or inventory (Types of

Managerial Accounting Reports, 2018). It is important for highlighting the areas of

improvement and offering bonuses to the best one. The importance of inventory and

manufacturing report is to keep records of various things like inventory change, purchase

order, multi stock location, etc. (Gibassier, 2017). This report is important for the

manager as it includes accurate record of cost of goods sold and the cost involved for

manufacturing goods.

Thanks and Regards

Management Accounting Officer

C) Benefits of Management Accounting Systems

Management accounting system is helpful for business, advantage of this are given as below:

Increases efficiency: Management accounting systems helps R ROBSON & SON

LIMITED in increasing its efficiency for performing various operations by eliminating

various kinds of wastages and defectives. It motivates employees to give better

performance and receive rewards in the form of promotions.

Maximization of profits: Management accounting helps to compare actual performance

with standard budgets to analyse deviations. If deviations are found then management is

required to take corrective actions for maximising profits (Flamholtz and et.al, 2016).

Goal setting: Management accounting helps managers at the time of setting goals and

making adjustments in order to motivate employees for achieving the ultimate goal. It

helps in improving relationship between management and labour.

Planning: Management accounting focuses on planning for future which includes

information of specific products, market reach and regional information. These

information are obtained from budgets, surveys and competitor analysis. For proper

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

planning, the information are rearranged in accordance with departments, products and

sections (Macinati and Anessi-Pessina, 2014).

Organizing: Management accounting plays an essential role in organizing business. It

assist management with help of internal audit and internal control, performance appraisal

and executing overall control of business activities. It helps for proper organizing the

work in R ROBSON & SON LIMITED.

It provides both qualitative as well as quantitative information for measuring operational

and financial performance. Management accounting is used by managers, employees and owners

within R ROBSON & SON LIMITED. Continuous improvement helps in improving the

effectiveness of process, systems and quality of various goods and services. Also it helps in

reducing the wastage of time, efforts and materials which ultimately helps in increasing its

productivity.

D) Critical evaluation of the integration of management accounting system and reporting in R.

Robson Ltd.

Management accounting system is an integral part of R. Robson ltd. Management

accounting helps to guide and advice management at every step. It helps in increasing the

efficiency of company. Management accounting system helps management of R. Robson Ltd. In

making efficient decisions for achieving sustainable success of organisation. Several techniques

in management accounting system like budgetary control helps in analysing the performance of

R. Robson Ltd. Management Accounting System helps R. Robson Ltd. in tracking cost and

expenses that involves in manufacturing processes and product sale. These accounting systems

have made it easier for R. Robson Ltd. to conduct day to day business activities in effective

manner.

Management Accounting Reports enabled R. Robson ltd to analyse business performance

and to estimate yearly budgets of company. Implementing accounting reports in R. Robson Ltd.

is able to make manufacturing processes more efficiently. Management Accounting Reports

helped R. Robson Ltd. in providing information about various levels of management, which

helps the management to make effective decisions regarding budgeting and operations of

organisations. Management accounting reports helps in providing information to the higher

authorities of R. Robson Ltd.

5

sections (Macinati and Anessi-Pessina, 2014).

Organizing: Management accounting plays an essential role in organizing business. It

assist management with help of internal audit and internal control, performance appraisal

and executing overall control of business activities. It helps for proper organizing the

work in R ROBSON & SON LIMITED.

It provides both qualitative as well as quantitative information for measuring operational

and financial performance. Management accounting is used by managers, employees and owners

within R ROBSON & SON LIMITED. Continuous improvement helps in improving the

effectiveness of process, systems and quality of various goods and services. Also it helps in

reducing the wastage of time, efforts and materials which ultimately helps in increasing its

productivity.

D) Critical evaluation of the integration of management accounting system and reporting in R.

Robson Ltd.

Management accounting system is an integral part of R. Robson ltd. Management

accounting helps to guide and advice management at every step. It helps in increasing the

efficiency of company. Management accounting system helps management of R. Robson Ltd. In

making efficient decisions for achieving sustainable success of organisation. Several techniques

in management accounting system like budgetary control helps in analysing the performance of

R. Robson Ltd. Management Accounting System helps R. Robson Ltd. in tracking cost and

expenses that involves in manufacturing processes and product sale. These accounting systems

have made it easier for R. Robson Ltd. to conduct day to day business activities in effective

manner.

Management Accounting Reports enabled R. Robson ltd to analyse business performance

and to estimate yearly budgets of company. Implementing accounting reports in R. Robson Ltd.

is able to make manufacturing processes more efficiently. Management Accounting Reports

helped R. Robson Ltd. in providing information about various levels of management, which

helps the management to make effective decisions regarding budgeting and operations of

organisations. Management accounting reports helps in providing information to the higher

authorities of R. Robson Ltd.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, there are some criticism on management accounting system as both financial

and cost accounting information are used in the management accounting system. The accuracy is

dependent on the accuracy of financial and cost record and these records determine weaknesses

and strengths of management accounting (Suomala, Lyly-Yrjänäinen and Lukka, 2014). So, it

would require by Nisa to maintain accuracy of these records in order to maintain management

accounting systems. Personal prejudices and bias of an individual can also affect the objectivity

and effectiveness of the conclusions and recommendations. These systems will only be providing

Nisa with data to solve the problem before the management.

TASK 2

A1. Absorption Costing and Marginal Costing Methods

Absorption Costing: It is a technique which assumes both fixed and variable costs as the

product costs. Costs per unit gets affected by changes in opening and closing stock. It is used for

determining cost of each unit. It shows the accuracy and fair treatment of product cost. In this

profits gets reduced since fixed costs are considered in product costs. It is required to be

presented or used for the purpose of financial as well as tax reporting. Under absorption costing,

the expenses or overheads are divided into production, administration and selling and

distribution. Fixed costs are included in product costs as compared to variable costs. Also cost

data is presented in a traditional way and profit is determined after deducting fixed costs with

their variable costs (Otley, 2016). The differences between opening stock and closing stock will

show effects by either increasing or decreasing the cost per unit. As we take all the cost in

absorption costing then our profit will increase but if fixed or variable costs is not considered

then it will result in reduced profit.

Marginal Costing: It is a technique of decision making which assumes variable costs as

product costs and fixed cost is assumed as cost of product. It is used to determine the cost of next

unit. The cost per unit does not get affected by changes in opening and closing stock since its

emphasis is on next unit (Suomala, Lyly-Yrjänäinen and Lukka, 2014). It emphasis of

contribution is shown in product cost. It is useful in decision making process and simple to

operate. The cost data is presented in order to outline total contribution of each product. The cost

per unit of output is not influenced by the variations in opening and closing stock. It

distinguishes overheads as fixed overheads and variable overheads. The fixed costs are charged

6

and cost accounting information are used in the management accounting system. The accuracy is

dependent on the accuracy of financial and cost record and these records determine weaknesses

and strengths of management accounting (Suomala, Lyly-Yrjänäinen and Lukka, 2014). So, it

would require by Nisa to maintain accuracy of these records in order to maintain management

accounting systems. Personal prejudices and bias of an individual can also affect the objectivity

and effectiveness of the conclusions and recommendations. These systems will only be providing

Nisa with data to solve the problem before the management.

TASK 2

A1. Absorption Costing and Marginal Costing Methods

Absorption Costing: It is a technique which assumes both fixed and variable costs as the

product costs. Costs per unit gets affected by changes in opening and closing stock. It is used for

determining cost of each unit. It shows the accuracy and fair treatment of product cost. In this

profits gets reduced since fixed costs are considered in product costs. It is required to be

presented or used for the purpose of financial as well as tax reporting. Under absorption costing,

the expenses or overheads are divided into production, administration and selling and

distribution. Fixed costs are included in product costs as compared to variable costs. Also cost

data is presented in a traditional way and profit is determined after deducting fixed costs with

their variable costs (Otley, 2016). The differences between opening stock and closing stock will

show effects by either increasing or decreasing the cost per unit. As we take all the cost in

absorption costing then our profit will increase but if fixed or variable costs is not considered

then it will result in reduced profit.

Marginal Costing: It is a technique of decision making which assumes variable costs as

product costs and fixed cost is assumed as cost of product. It is used to determine the cost of next

unit. The cost per unit does not get affected by changes in opening and closing stock since its

emphasis is on next unit (Suomala, Lyly-Yrjänäinen and Lukka, 2014). It emphasis of

contribution is shown in product cost. It is useful in decision making process and simple to

operate. The cost data is presented in order to outline total contribution of each product. The cost

per unit of output is not influenced by the variations in opening and closing stock. It

distinguishes overheads as fixed overheads and variable overheads. The fixed costs are charged

6

against the profits of the year in R ROBSON & SON LIMITED. It can be expressed as

contribution per unit.

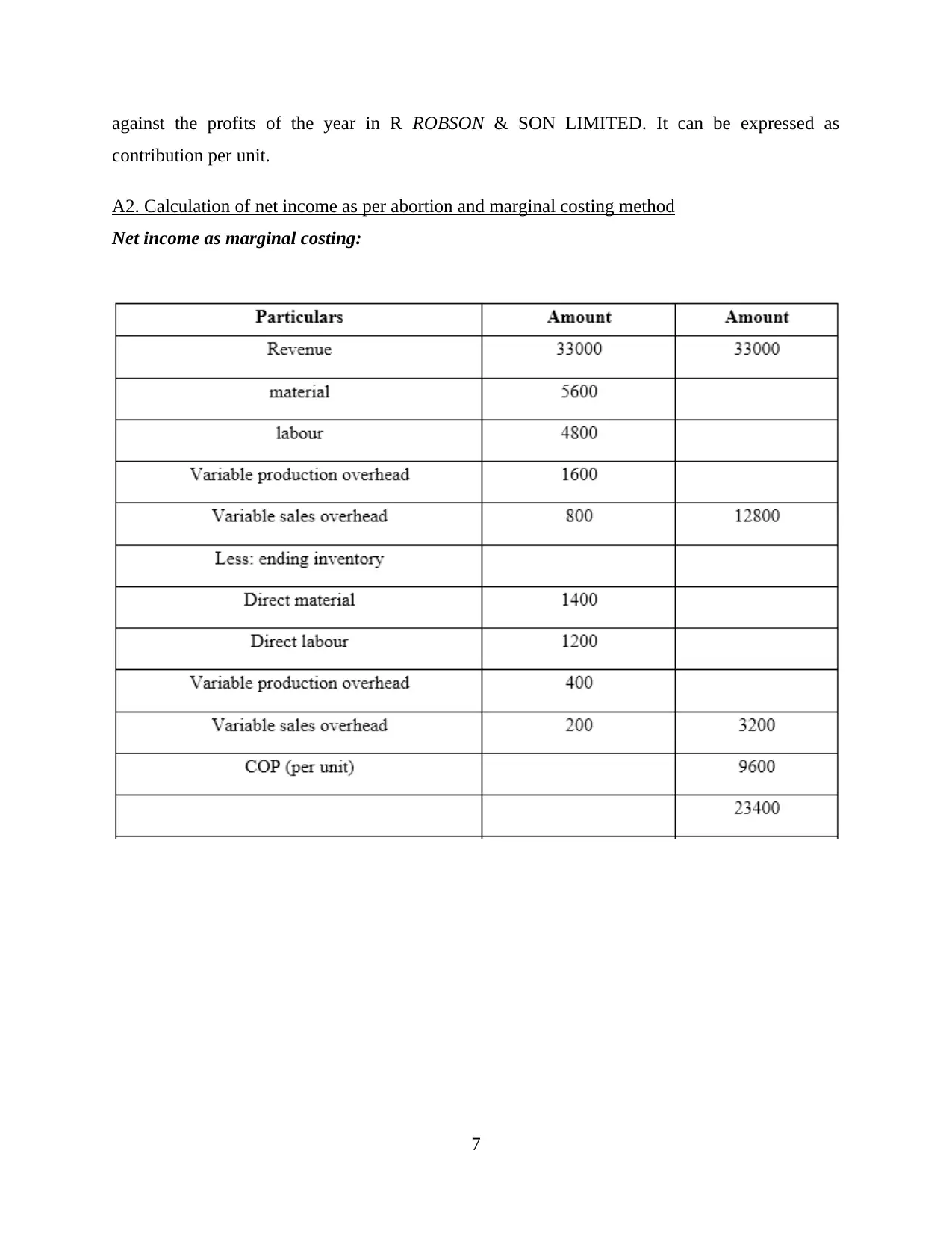

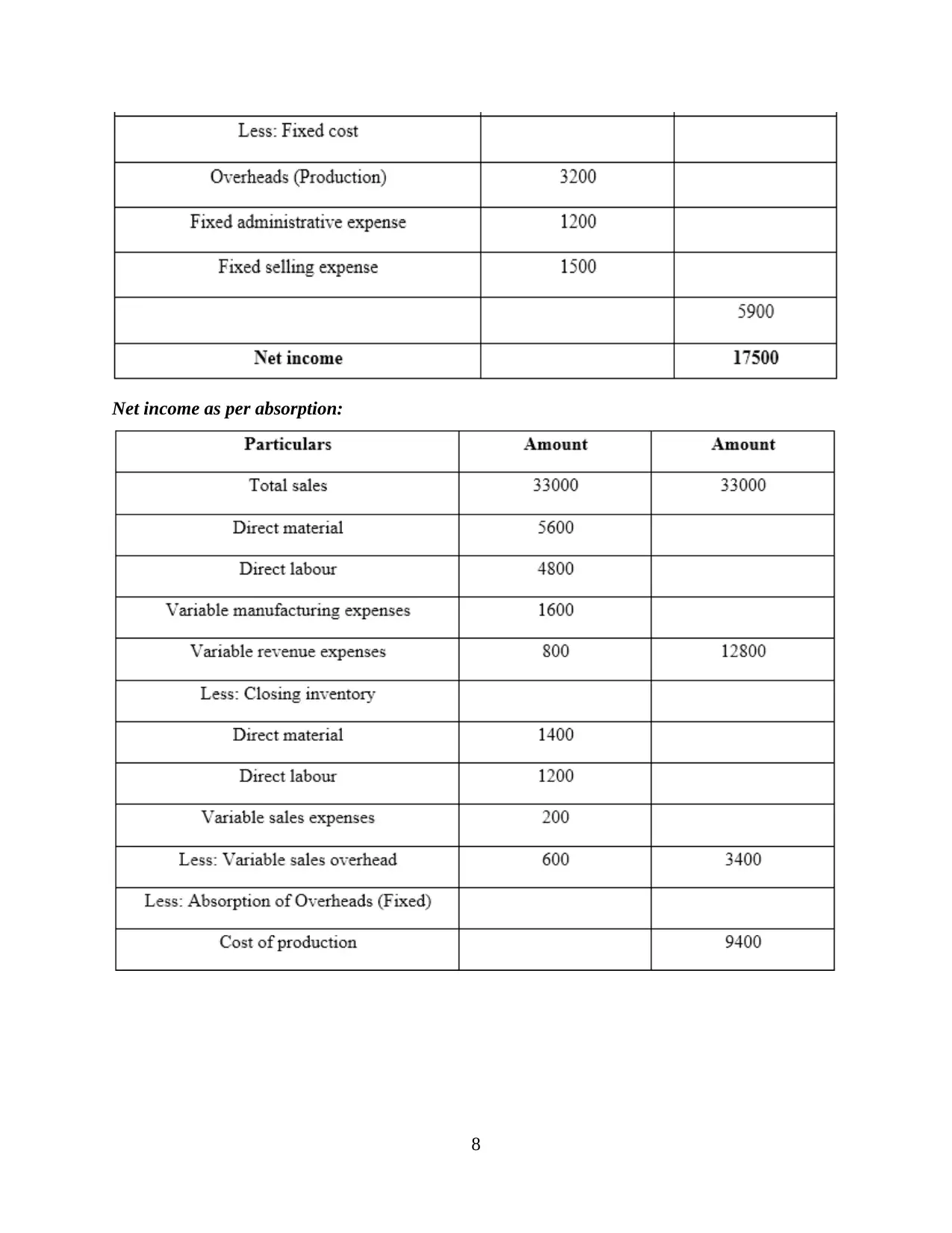

A2. Calculation of net income as per abortion and marginal costing method

Net income as marginal costing:

7

contribution per unit.

A2. Calculation of net income as per abortion and marginal costing method

Net income as marginal costing:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

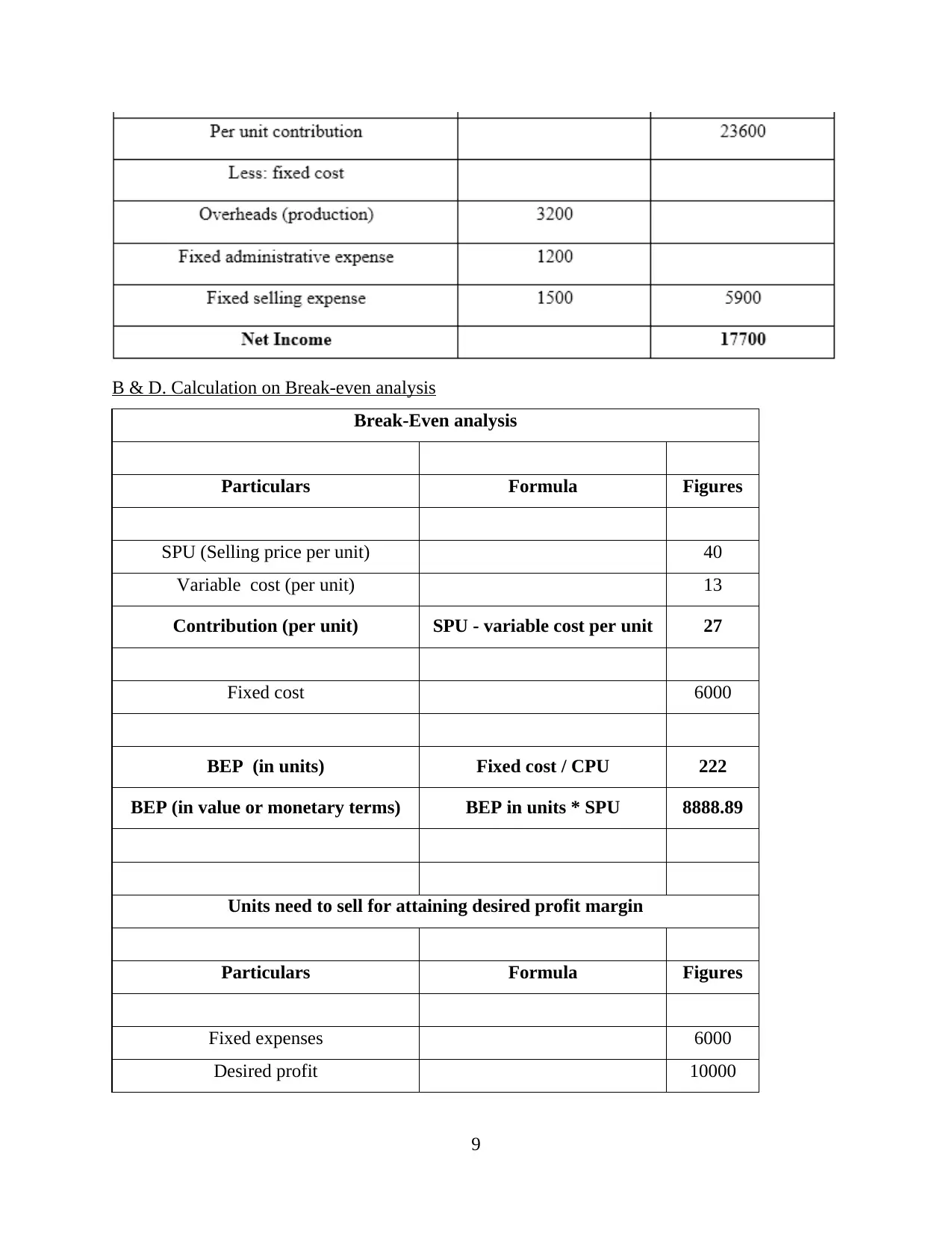

Net income as per absorption:

8

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B & D. Calculation on Break-even analysis

Break-Even analysis

Particulars Formula Figures

SPU (Selling price per unit) 40

Variable cost (per unit) 13

Contribution (per unit) SPU - variable cost per unit 27

Fixed cost 6000

BEP (in units) Fixed cost / CPU 222

BEP (in value or monetary terms) BEP in units * SPU 8888.89

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

Desired profit 10000

9

Break-Even analysis

Particulars Formula Figures

SPU (Selling price per unit) 40

Variable cost (per unit) 13

Contribution (per unit) SPU - variable cost per unit 27

Fixed cost 6000

BEP (in units) Fixed cost / CPU 222

BEP (in value or monetary terms) BEP in units * SPU 8888.89

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed expenses 6000

Desired profit 10000

9

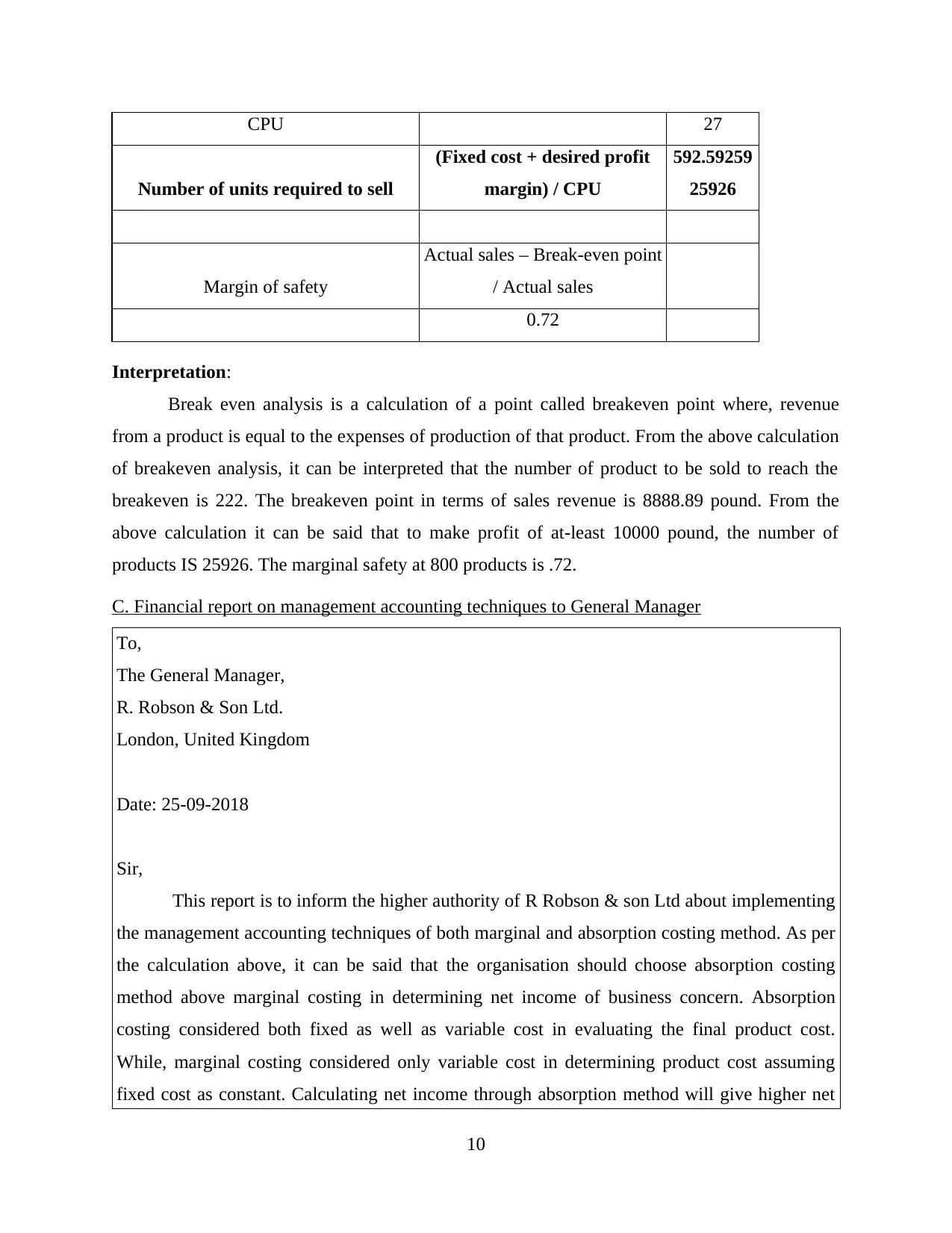

CPU 27

Number of units required to sell

(Fixed cost + desired profit

margin) / CPU

592.59259

25926

Margin of safety

Actual sales – Break-even point

/ Actual sales

0.72

Interpretation:

Break even analysis is a calculation of a point called breakeven point where, revenue

from a product is equal to the expenses of production of that product. From the above calculation

of breakeven analysis, it can be interpreted that the number of product to be sold to reach the

breakeven is 222. The breakeven point in terms of sales revenue is 8888.89 pound. From the

above calculation it can be said that to make profit of at-least 10000 pound, the number of

products IS 25926. The marginal safety at 800 products is .72.

C. Financial report on management accounting techniques to General Manager

To,

The General Manager,

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

This report is to inform the higher authority of R Robson & son Ltd about implementing

the management accounting techniques of both marginal and absorption costing method. As per

the calculation above, it can be said that the organisation should choose absorption costing

method above marginal costing in determining net income of business concern. Absorption

costing considered both fixed as well as variable cost in evaluating the final product cost.

While, marginal costing considered only variable cost in determining product cost assuming

fixed cost as constant. Calculating net income through absorption method will give higher net

10

Number of units required to sell

(Fixed cost + desired profit

margin) / CPU

592.59259

25926

Margin of safety

Actual sales – Break-even point

/ Actual sales

0.72

Interpretation:

Break even analysis is a calculation of a point called breakeven point where, revenue

from a product is equal to the expenses of production of that product. From the above calculation

of breakeven analysis, it can be interpreted that the number of product to be sold to reach the

breakeven is 222. The breakeven point in terms of sales revenue is 8888.89 pound. From the

above calculation it can be said that to make profit of at-least 10000 pound, the number of

products IS 25926. The marginal safety at 800 products is .72.

C. Financial report on management accounting techniques to General Manager

To,

The General Manager,

R. Robson & Son Ltd.

London, United Kingdom

Date: 25-09-2018

Sir,

This report is to inform the higher authority of R Robson & son Ltd about implementing

the management accounting techniques of both marginal and absorption costing method. As per

the calculation above, it can be said that the organisation should choose absorption costing

method above marginal costing in determining net income of business concern. Absorption

costing considered both fixed as well as variable cost in evaluating the final product cost.

While, marginal costing considered only variable cost in determining product cost assuming

fixed cost as constant. Calculating net income through absorption method will give higher net

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.