Management Accounting Report: Financial Planning and Costing Analysis

VerifiedAdded on 2021/01/02

|18

|4726

|492

Report

AI Summary

This report provides a comprehensive overview of management accounting, its importance in organizational decision-making, and the different types of management accounting systems. It critically evaluates the benefits of these systems and MA reporting within an organizational context, with specific examples and data. The report includes detailed calculations of absorption and marginal costing, along with reconciliation statements. Furthermore, it explores the planning tools of management accounting, assessing their effectiveness for Nero Ltd. in solving financial problems. The report analyzes the use of these planning tools and identifies the most effective management accounting tools for financial problem-solving within the company, culminating in conclusions and references for further study.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1 and LO 2.................................................................................................................................1

1. Importance of management accounting in decision-making process of organisation............1

2. Explanation of different types of management accounting system which used in reporting

and its integration in business operation.....................................................................................2

3. Critically evaluating benefits of management accounting system and MA reporting in

context of organisational process................................................................................................3

4. Calculation of absorption and marginal costing and reconciliation statements......................6

LO 3 and LO 4.................................................................................................................................9

Planning tools of management accounting which indicate levels of effectiveness for Nero Ltd.

Organisation................................................................................................................................9

Use of planning tool in solving financial problem of organisation...........................................11

Effective tools of management accounting in solving financial problems of Nero Ltd...........12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

LO 1 and LO 2.................................................................................................................................1

1. Importance of management accounting in decision-making process of organisation............1

2. Explanation of different types of management accounting system which used in reporting

and its integration in business operation.....................................................................................2

3. Critically evaluating benefits of management accounting system and MA reporting in

context of organisational process................................................................................................3

4. Calculation of absorption and marginal costing and reconciliation statements......................6

LO 3 and LO 4.................................................................................................................................9

Planning tools of management accounting which indicate levels of effectiveness for Nero Ltd.

Organisation................................................................................................................................9

Use of planning tool in solving financial problem of organisation...........................................11

Effective tools of management accounting in solving financial problems of Nero Ltd...........12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the tool which used to prepare management reports and

accounts in organisation (Kaplan and Atkinson, 2015). These are statements which provides an

accurate and statistical financial information to managers in developing short term decisions and

to analysing day-to-day business operations. This report provides an assessment which relates to

importance of management accounting in developing decision making process in Sewport

company. Types of management accounting system is also to be elaborated in this report with its

critical evaluation. Further, an explanation is to be provided on three planning tools used in MA

and its level of effectiveness for solving financial problems of Nero Ltd organisation. Thus,

illustration is given on importance of management accounting in achieving organisation success.

LO 1 and LO 2

1. Importance of management accounting in decision-making process of organisation

Business owners and managers of Sewport company have to face numerous decisions in

regular operations of organisation (Importance of Management Accounting, 2018). Therefore, for

developing effective decision in organisation, management accounting statements provides

useful and accurate information which is related to day-to-day business operations. Such

information will relate to profit margin and labour utilisation which overall helps management in

developing effective decision in achieving success of organisation. Its importance are as follows-

Relevant Cost Analysis:

Management accounting information used by mangers of company in deciding products which

needs to produce for increasing sales volume of organisation. For developing effective products,

MA helps in analysing revenue which earned by company and expenses which incurred for

developing business operations (Otley, 2016). Therefore, this accounting tool used to determine

whether to add any product line in organisation or to discontinue business operations.

Activity-based Costing Techniques:

This is the technique which helps management in determining activities which required to

perform in selling products of organisation among customers. This is the activity which overall

helps in deciding which product has demand in business market which overall helps in

generating profit for Sewport company.

1

Management accounting is the tool which used to prepare management reports and

accounts in organisation (Kaplan and Atkinson, 2015). These are statements which provides an

accurate and statistical financial information to managers in developing short term decisions and

to analysing day-to-day business operations. This report provides an assessment which relates to

importance of management accounting in developing decision making process in Sewport

company. Types of management accounting system is also to be elaborated in this report with its

critical evaluation. Further, an explanation is to be provided on three planning tools used in MA

and its level of effectiveness for solving financial problems of Nero Ltd organisation. Thus,

illustration is given on importance of management accounting in achieving organisation success.

LO 1 and LO 2

1. Importance of management accounting in decision-making process of organisation

Business owners and managers of Sewport company have to face numerous decisions in

regular operations of organisation (Importance of Management Accounting, 2018). Therefore, for

developing effective decision in organisation, management accounting statements provides

useful and accurate information which is related to day-to-day business operations. Such

information will relate to profit margin and labour utilisation which overall helps management in

developing effective decision in achieving success of organisation. Its importance are as follows-

Relevant Cost Analysis:

Management accounting information used by mangers of company in deciding products which

needs to produce for increasing sales volume of organisation. For developing effective products,

MA helps in analysing revenue which earned by company and expenses which incurred for

developing business operations (Otley, 2016). Therefore, this accounting tool used to determine

whether to add any product line in organisation or to discontinue business operations.

Activity-based Costing Techniques:

This is the technique which helps management in determining activities which required to

perform in selling products of organisation among customers. This is the activity which overall

helps in deciding which product has demand in business market which overall helps in

generating profit for Sewport company.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Make or Buy analysis:

Importance of managerial accounting is to provide information related to manufacturing process

of company. This process used to analysis overall revenue and expenses which incurred by

company during its business operations. This analysis overall helps in developing decision in

manufacturing product which provide more profit to company.

Utilizing the Data:

Management accounting provides information which helps in analysing utilization of resources

in organisation. Statements which provide effective guidance in developing decisions which

helps in improving performance of Sewport company are budgeting, financial statements and

balance scorecards.

Creates budget which helps in developing growth:

This is the accounting process which helps in developing effective budget for operating business

operations in business market (Cooper, Ezzamel and Qu, 2017). Set budget with information of

MA overall develops long-term profitability and growth of the company.

These are the importance of management accounting which is used by owners of

Sewport, in developing effective decision-making process. Decisions which developed with

considering information of management accounting will overall result in long term profitability

and growth of organisation.

2. Explanation of different types of management accounting system which used in reporting and

its integration in business operation

Management accounting system is the software which is used in Sewport organisation to

track accounting activities of company. Its objective is to provide information related to internal

operations of company. This information develop more emphasis on planning and controlling

process of company. Different types of management accounting system which used in preparing

reports are as follows-

Cost Accounting Systems:

It is a framework which used by Sewport organisation in estimating the overall cost of

products and services which offered by company in business market. This accounting system

evaluate profitability, inventory valuation and cost control of goods and services of company.

2

Importance of managerial accounting is to provide information related to manufacturing process

of company. This process used to analysis overall revenue and expenses which incurred by

company during its business operations. This analysis overall helps in developing decision in

manufacturing product which provide more profit to company.

Utilizing the Data:

Management accounting provides information which helps in analysing utilization of resources

in organisation. Statements which provide effective guidance in developing decisions which

helps in improving performance of Sewport company are budgeting, financial statements and

balance scorecards.

Creates budget which helps in developing growth:

This is the accounting process which helps in developing effective budget for operating business

operations in business market (Cooper, Ezzamel and Qu, 2017). Set budget with information of

MA overall develops long-term profitability and growth of the company.

These are the importance of management accounting which is used by owners of

Sewport, in developing effective decision-making process. Decisions which developed with

considering information of management accounting will overall result in long term profitability

and growth of organisation.

2. Explanation of different types of management accounting system which used in reporting and

its integration in business operation

Management accounting system is the software which is used in Sewport organisation to

track accounting activities of company. Its objective is to provide information related to internal

operations of company. This information develop more emphasis on planning and controlling

process of company. Different types of management accounting system which used in preparing

reports are as follows-

Cost Accounting Systems:

It is a framework which used by Sewport organisation in estimating the overall cost of

products and services which offered by company in business market. This accounting system

evaluate profitability, inventory valuation and cost control of goods and services of company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Therefore, it is the accounting system which used by organisation in tracking its raw materials

which is used in production stage and will convert into finished goods. This method helps

management in analysing individual cost of products which helps in comparing financial

performance of organisation. There are two cost accounting system that is-

Job order costing which overall accumulates manufacturing cost of organisation.

Sewport company apply this costing technique in providing unique and special products among

consumers.

Process costing system is accounting method which is used in Sewport company to

accumulate manufacturing cost for each process in company (Tappura and et.al., 2015). This

system used by organisation to analyse process requires inflows of cash in different department

of business areas.

Job Costing Systems:

This is method which is used by Sewport company for assigning manufacturing cost of

products which offered by company. This system only used by company when they are offering

diversified products in business market. Therefore, this method helps in recording direct material

and direct labour used to assign each job in company.

Inventory Management Systems:

It is the system which helps in tracking entire supply chain or portion which used in

business operation of company. This is the system which helps management of Sewport to see all

small moving parts of business operation which overall helps in developing effective decisions

for company. There are different methods of this system which includes-

Set par levels by which management set par levels for each products of company. It

shows minimum amount of products which must be present in organisation all the times.

First-in First-Out is the important principle which means that oldest inventory of

company will sell first and then newest inventory will get sold.

Last-in First-out is the method which used by company in selling the newest stock first

and oldest stock at the end.

3. Critically evaluating benefits of management accounting system and MA reporting in context

of organisational process

Importance of management accounting systems

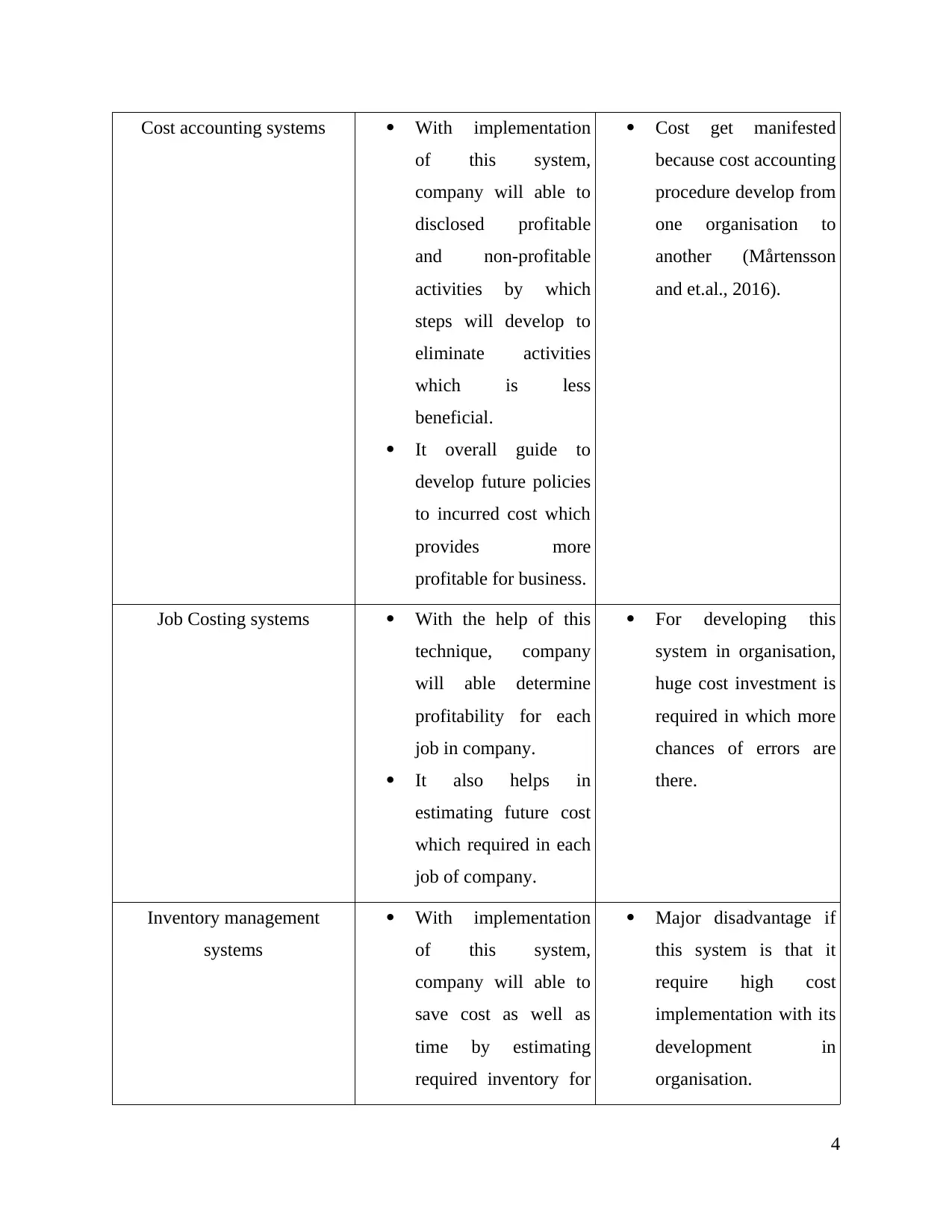

Methods Advantages Disadvantages

3

which is used in production stage and will convert into finished goods. This method helps

management in analysing individual cost of products which helps in comparing financial

performance of organisation. There are two cost accounting system that is-

Job order costing which overall accumulates manufacturing cost of organisation.

Sewport company apply this costing technique in providing unique and special products among

consumers.

Process costing system is accounting method which is used in Sewport company to

accumulate manufacturing cost for each process in company (Tappura and et.al., 2015). This

system used by organisation to analyse process requires inflows of cash in different department

of business areas.

Job Costing Systems:

This is method which is used by Sewport company for assigning manufacturing cost of

products which offered by company. This system only used by company when they are offering

diversified products in business market. Therefore, this method helps in recording direct material

and direct labour used to assign each job in company.

Inventory Management Systems:

It is the system which helps in tracking entire supply chain or portion which used in

business operation of company. This is the system which helps management of Sewport to see all

small moving parts of business operation which overall helps in developing effective decisions

for company. There are different methods of this system which includes-

Set par levels by which management set par levels for each products of company. It

shows minimum amount of products which must be present in organisation all the times.

First-in First-Out is the important principle which means that oldest inventory of

company will sell first and then newest inventory will get sold.

Last-in First-out is the method which used by company in selling the newest stock first

and oldest stock at the end.

3. Critically evaluating benefits of management accounting system and MA reporting in context

of organisational process

Importance of management accounting systems

Methods Advantages Disadvantages

3

Cost accounting systems With implementation

of this system,

company will able to

disclosed profitable

and non-profitable

activities by which

steps will develop to

eliminate activities

which is less

beneficial.

It overall guide to

develop future policies

to incurred cost which

provides more

profitable for business.

Cost get manifested

because cost accounting

procedure develop from

one organisation to

another (Mårtensson

and et.al., 2016).

Job Costing systems With the help of this

technique, company

will able determine

profitability for each

job in company.

It also helps in

estimating future cost

which required in each

job of company.

For developing this

system in organisation,

huge cost investment is

required in which more

chances of errors are

there.

Inventory management

systems

With implementation

of this system,

company will able to

save cost as well as

time by estimating

required inventory for

Major disadvantage if

this system is that it

require high cost

implementation with its

development in

organisation.

4

of this system,

company will able to

disclosed profitable

and non-profitable

activities by which

steps will develop to

eliminate activities

which is less

beneficial.

It overall guide to

develop future policies

to incurred cost which

provides more

profitable for business.

Cost get manifested

because cost accounting

procedure develop from

one organisation to

another (Mårtensson

and et.al., 2016).

Job Costing systems With the help of this

technique, company

will able determine

profitability for each

job in company.

It also helps in

estimating future cost

which required in each

job of company.

For developing this

system in organisation,

huge cost investment is

required in which more

chances of errors are

there.

Inventory management

systems

With implementation

of this system,

company will able to

save cost as well as

time by estimating

required inventory for

Major disadvantage if

this system is that it

require high cost

implementation with its

development in

organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

operations of business.

With the help of this

technique, overall

efficiency of

organisation will get

increased (Kerzner and

Kerzner, 2017).

Importance of management accounting reporting

Budget Report:

This is the report which is used by management and owners to analyse business performance and

cost control in organisation. Budget which developed in Sewport organisation is by comparing

actual expenses from previous year. This budget report was also used by managers in deciding

incentive of employees of company which overall lead to develop motivation among them in

achieving financial objectives of company.

Accounts Receivable Aging:

This is the report which is used by Sewport company for managing overall cash flow of company

which credited to customers of organisation. This report generally used by owners in finding

problems related to collection process of company (Harrison and Lock, 2017). If there are clients

which will not able to pay amount of company then will tight its credit policies for developing

effective business operations.

Job Cost Reports

This is the report which shows finance of specific projects of company. To evaluate job

profitability this reports are matched with estimation of revenues which helps in identifying

higher- earning area of company. This report also helps management in eliminating areas which

are incurring higher expense and have no use in the production process of company.

Inventory and Manufacturing:

To make manufacturing process more efficient in company, this managerial accounting report

produced by management in developing effective decision in improving manufacturing process

5

With the help of this

technique, overall

efficiency of

organisation will get

increased (Kerzner and

Kerzner, 2017).

Importance of management accounting reporting

Budget Report:

This is the report which is used by management and owners to analyse business performance and

cost control in organisation. Budget which developed in Sewport organisation is by comparing

actual expenses from previous year. This budget report was also used by managers in deciding

incentive of employees of company which overall lead to develop motivation among them in

achieving financial objectives of company.

Accounts Receivable Aging:

This is the report which is used by Sewport company for managing overall cash flow of company

which credited to customers of organisation. This report generally used by owners in finding

problems related to collection process of company (Harrison and Lock, 2017). If there are clients

which will not able to pay amount of company then will tight its credit policies for developing

effective business operations.

Job Cost Reports

This is the report which shows finance of specific projects of company. To evaluate job

profitability this reports are matched with estimation of revenues which helps in identifying

higher- earning area of company. This report also helps management in eliminating areas which

are incurring higher expense and have no use in the production process of company.

Inventory and Manufacturing:

To make manufacturing process more efficient in company, this managerial accounting report

produced by management in developing effective decision in improving manufacturing process

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of company. Items which included in this report are inventory waste, hourly labour cost or per-

units of overheads.

For developing effective business operations, integration of these reports will prove

beneficial in organisational process of Sewport company (Dale and Plunkett, 2017).

4. Calculation of absorption and marginal costing and reconciliation statements

a.) Calculation of absorption and marginal costing:

Profit & Loss Statement using Absorption Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

Cost of goods sold:

Variable cost 78000 0.65 50700

Add: fixed cost 78000 0.2 15600

Total production

cost

66300

Add: opening stock 0

Total stock

available for sale

66300

Less: closing stock 12000 0.85 10200

Cost of goods sold: 56100

GROSS PROFIT 9900

Less: under

absorption of fixed

overhead

16000 15600 400

Less: selling and

admin cost

5200

6

units of overheads.

For developing effective business operations, integration of these reports will prove

beneficial in organisational process of Sewport company (Dale and Plunkett, 2017).

4. Calculation of absorption and marginal costing and reconciliation statements

a.) Calculation of absorption and marginal costing:

Profit & Loss Statement using Absorption Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

Cost of goods sold:

Variable cost 78000 0.65 50700

Add: fixed cost 78000 0.2 15600

Total production

cost

66300

Add: opening stock 0

Total stock

available for sale

66300

Less: closing stock 12000 0.85 10200

Cost of goods sold: 56100

GROSS PROFIT 9900

Less: under

absorption of fixed

overhead

16000 15600 400

Less: selling and

admin cost

5200

6

NET PROFIT 4300

Profit & Loss Statement using Absorption Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Cost of goods sold:

Variable cost 66000 0.65 42900

Add: fixed cost 66000 0.2 13200

Total production

cost

56100

Add: opening stock 12000 0.85 10200

Total stock

available for sale

66300

Less: closing stock 4000 0.85 3400

Cost of goods sold: 62900

GROSS PROFIT 11100

Less: under

absorption of fixed

overhead

16000 13200 2800

Less: selling and

admin cost

5200

NET PROFIT 3100

7

Profit & Loss Statement using Absorption Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Cost of goods sold:

Variable cost 66000 0.65 42900

Add: fixed cost 66000 0.2 13200

Total production

cost

56100

Add: opening stock 12000 0.85 10200

Total stock

available for sale

66300

Less: closing stock 4000 0.85 3400

Cost of goods sold: 62900

GROSS PROFIT 11100

Less: under

absorption of fixed

overhead

16000 13200 2800

Less: selling and

admin cost

5200

NET PROFIT 3100

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profit & Loss Statement using Marginal Costing

(Quarter 1)

particulars £ £

sales 66000 1 66000

Production cost:

Variable cost 78000 0.65 50700

Add: opening stock 0

Total stock

available for sale

50700

Less: closing stock 12000 0.65 7800

Cost of goods sold: 42900

Contribution

margin

23100

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 19000

Profit & Loss Statement using Marginal Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Production cost:

8

(Quarter 1)

particulars £ £

sales 66000 1 66000

Production cost:

Variable cost 78000 0.65 50700

Add: opening stock 0

Total stock

available for sale

50700

Less: closing stock 12000 0.65 7800

Cost of goods sold: 42900

Contribution

margin

23100

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 19000

Profit & Loss Statement using Marginal Costing

(Quarter 2)

particulars £ £

sales 74000 1 74000

Production cost:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

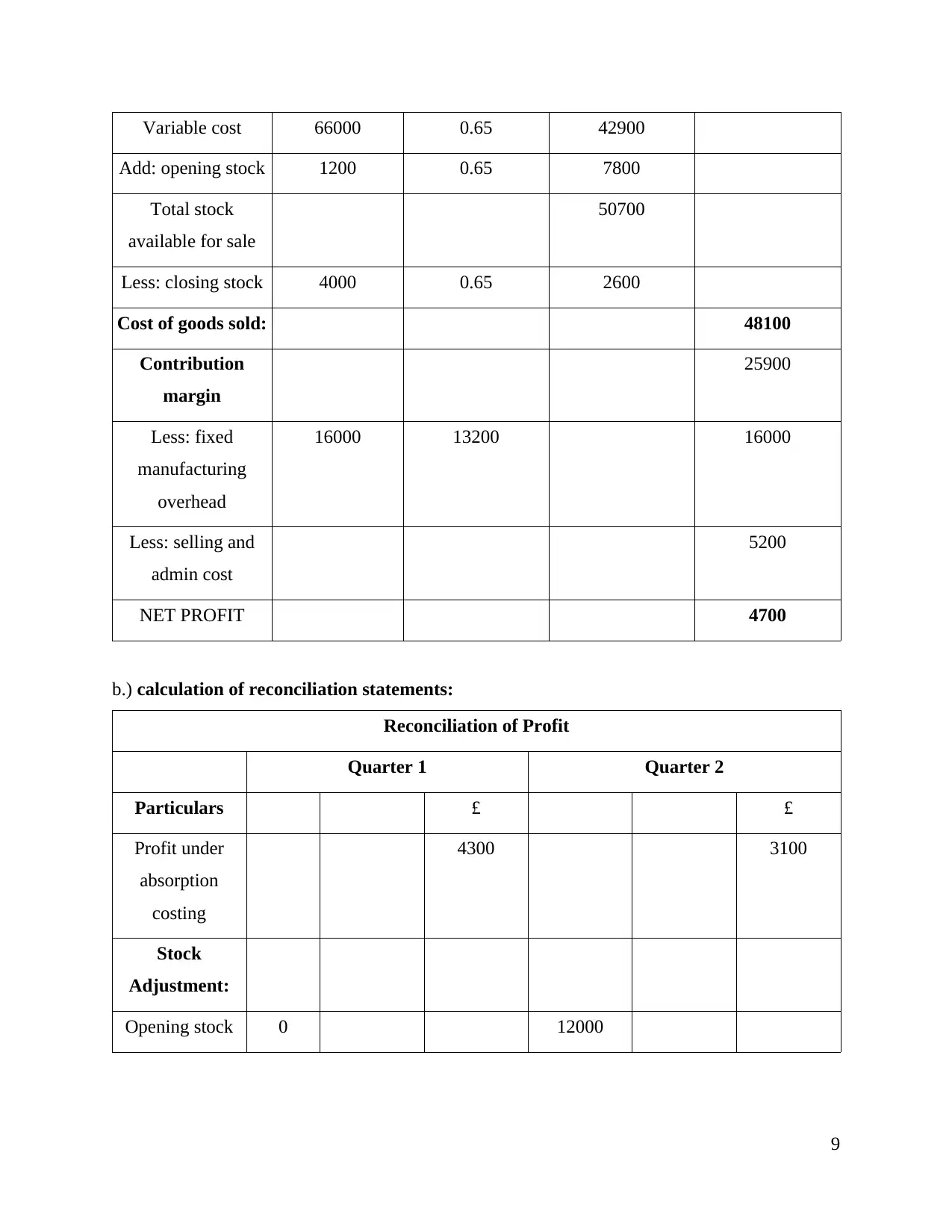

Variable cost 66000 0.65 42900

Add: opening stock 1200 0.65 7800

Total stock

available for sale

50700

Less: closing stock 4000 0.65 2600

Cost of goods sold: 48100

Contribution

margin

25900

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 4700

b.) calculation of reconciliation statements:

Reconciliation of Profit

Quarter 1 Quarter 2

Particulars £ £

Profit under

absorption

costing

4300 3100

Stock

Adjustment:

Opening stock 0 12000

9

Add: opening stock 1200 0.65 7800

Total stock

available for sale

50700

Less: closing stock 4000 0.65 2600

Cost of goods sold: 48100

Contribution

margin

25900

Less: fixed

manufacturing

overhead

16000 13200 16000

Less: selling and

admin cost

5200

NET PROFIT 4700

b.) calculation of reconciliation statements:

Reconciliation of Profit

Quarter 1 Quarter 2

Particulars £ £

Profit under

absorption

costing

4300 3100

Stock

Adjustment:

Opening stock 0 12000

9

Less: closing

stock

12000 4000

12000 8000

Fixed overhead

rate

0.2 -2400 0.2 1600

Profit under

marginal costing

19000 4700

LO 3 and LO 4

Part A

Planning tools of management accounting which indicate levels of effectiveness for Nero Ltd.

Organisation

For managing business operations of Nero Ltd. Planning tools are effective budgetary

control analysis which helps in managing overall cost of organisation. This planing tools also

helps in maximizing profits of the company. Therefore, its development is necessary in

managerial accounting because it keeps focus on different important things, plans and policies of

organisation. It also helps in developing effective pricing strategies for products and services of

company. For developing pricing strategies, Nero Ltd. Will analyse financial statements of its

competitors to offer products and services to customers.

Job costing helps company in accumulating manufacturing cost of goods and services. To

offer special products to consumers this costing method is used by company. Process costing

method used by company in accumulating process of manufacturing products of company

(Weygandt, Kimmel and Kieso, 2015). Batch costing technique is used by organisation to find

cost of identical unit of each batch of goods and services. Tools of management accounting are

as follows-

Actual Costing-

Actual costing is the tool which is used in Nero Ltd to find the actual cost of material, labour and

overhead. With the use of this technique, company will able to trace direct cost of the object

which has measurable cost. Therefore, this is the method which is used to calculate actual cost

10

stock

12000 4000

12000 8000

Fixed overhead

rate

0.2 -2400 0.2 1600

Profit under

marginal costing

19000 4700

LO 3 and LO 4

Part A

Planning tools of management accounting which indicate levels of effectiveness for Nero Ltd.

Organisation

For managing business operations of Nero Ltd. Planning tools are effective budgetary

control analysis which helps in managing overall cost of organisation. This planing tools also

helps in maximizing profits of the company. Therefore, its development is necessary in

managerial accounting because it keeps focus on different important things, plans and policies of

organisation. It also helps in developing effective pricing strategies for products and services of

company. For developing pricing strategies, Nero Ltd. Will analyse financial statements of its

competitors to offer products and services to customers.

Job costing helps company in accumulating manufacturing cost of goods and services. To

offer special products to consumers this costing method is used by company. Process costing

method used by company in accumulating process of manufacturing products of company

(Weygandt, Kimmel and Kieso, 2015). Batch costing technique is used by organisation to find

cost of identical unit of each batch of goods and services. Tools of management accounting are

as follows-

Actual Costing-

Actual costing is the tool which is used in Nero Ltd to find the actual cost of material, labour and

overhead. With the use of this technique, company will able to trace direct cost of the object

which has measurable cost. Therefore, this is the method which is used to calculate actual cost

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.