Management Accounting Techniques, Budgeting and Performance Report

VerifiedAdded on 2020/10/05

|14

|2890

|237

Report

AI Summary

This report delves into the realm of management accounting, presenting a comprehensive analysis of its core concepts and practical applications. It begins by exploring income statement preparation using absorption and marginal costing techniques, providing detailed calculations and comparisons. The report then examines various management accounting techniques, including absorption and marginal costing, and their interpretations. A significant portion is dedicated to budgetary control, discussing the advantages and disadvantages of planning tools such as forecasting, scenario, and contingency planning. The high-low method is applied to estimate expenses, and the purposes of budgeting and cash budget preparation are explained. Finally, the report compares the performances of UCK Woodworks and UCK Furniture using key performance measures like ROCE, asset turnover, and operating profit margin. It concludes by describing how management accounting enhances financial performance through KPIs, benchmarking, and financial governance, offering valuable insights for business improvement.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

1.1 Preparation of income statement and calculating the costs by using appropriate techniques

of costs analysis ..........................................................................................................................1

1.2 Range of management accounting techniques......................................................................4

1.3 Interpretation of costing techniques and financial reports ...................................................4

TASK 2............................................................................................................................................4

2.1 Describing advantages and disadvantages of disadvantages of planning tools used for

budgetary control ......................................................................................................................4

2.2 Estimation of the expenses if the number of hours required for July and August by

adapting the high-low method.....................................................................................................6

2.3 Explanation of purposes of budget and preparation of cash budget ....................................7

TASK 3............................................................................................................................................7

3.1 Comparison between the performances of UCK Woodworks and UCK Furniture on the

basis of three performance measures..........................................................................................7

3.2 Describing how management accounting helps in improving the financial performance of

organisation ................................................................................................................................9

3.3 Evaluating planning tools helps in reducing the financial problem for accomplishing the

success ........................................................................................................................................9

CONCLUSION..............................................................................................................................10

RFERENCES.................................................................................................................................11

.......................................................................................................................................................11

INTRODUCTION...........................................................................................................................1

1.1 Preparation of income statement and calculating the costs by using appropriate techniques

of costs analysis ..........................................................................................................................1

1.2 Range of management accounting techniques......................................................................4

1.3 Interpretation of costing techniques and financial reports ...................................................4

TASK 2............................................................................................................................................4

2.1 Describing advantages and disadvantages of disadvantages of planning tools used for

budgetary control ......................................................................................................................4

2.2 Estimation of the expenses if the number of hours required for July and August by

adapting the high-low method.....................................................................................................6

2.3 Explanation of purposes of budget and preparation of cash budget ....................................7

TASK 3............................................................................................................................................7

3.1 Comparison between the performances of UCK Woodworks and UCK Furniture on the

basis of three performance measures..........................................................................................7

3.2 Describing how management accounting helps in improving the financial performance of

organisation ................................................................................................................................9

3.3 Evaluating planning tools helps in reducing the financial problem for accomplishing the

success ........................................................................................................................................9

CONCLUSION..............................................................................................................................10

RFERENCES.................................................................................................................................11

.......................................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

It is true that the present business life-cycle of each and every organisation requires for

some crucial purposes, the management accounting and its tools for budget controlling and for

effective decision making, devising planning and performance management systems and

rendering expertise financial reporting and controlling in order to ascertain the management

formulation and implementation of an organisation' strategy (Alyousef and Alnasser, 2015).

These all tasks performed by the managers of the organisation with the help of management

accounting systems, techniques and its tools. Therefore, the management accounting commonly

known as the managerial accounting. This report pertain the information about the management

accounting system, its techniques and its tools with the illustrative example of UCK furnitures

operational data, for the proper understanding of the effectiveness of management accounting in

business.

TASK 1

1.1 Preparation of income statement and calculating the costs by using appropriate techniques of

costs analysis

Income Statement by using absorption and marginal costing techniques of management

accounting are below.

1

It is true that the present business life-cycle of each and every organisation requires for

some crucial purposes, the management accounting and its tools for budget controlling and for

effective decision making, devising planning and performance management systems and

rendering expertise financial reporting and controlling in order to ascertain the management

formulation and implementation of an organisation' strategy (Alyousef and Alnasser, 2015).

These all tasks performed by the managers of the organisation with the help of management

accounting systems, techniques and its tools. Therefore, the management accounting commonly

known as the managerial accounting. This report pertain the information about the management

accounting system, its techniques and its tools with the illustrative example of UCK furnitures

operational data, for the proper understanding of the effectiveness of management accounting in

business.

TASK 1

1.1 Preparation of income statement and calculating the costs by using appropriate techniques of

costs analysis

Income Statement by using absorption and marginal costing techniques of management

accounting are below.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

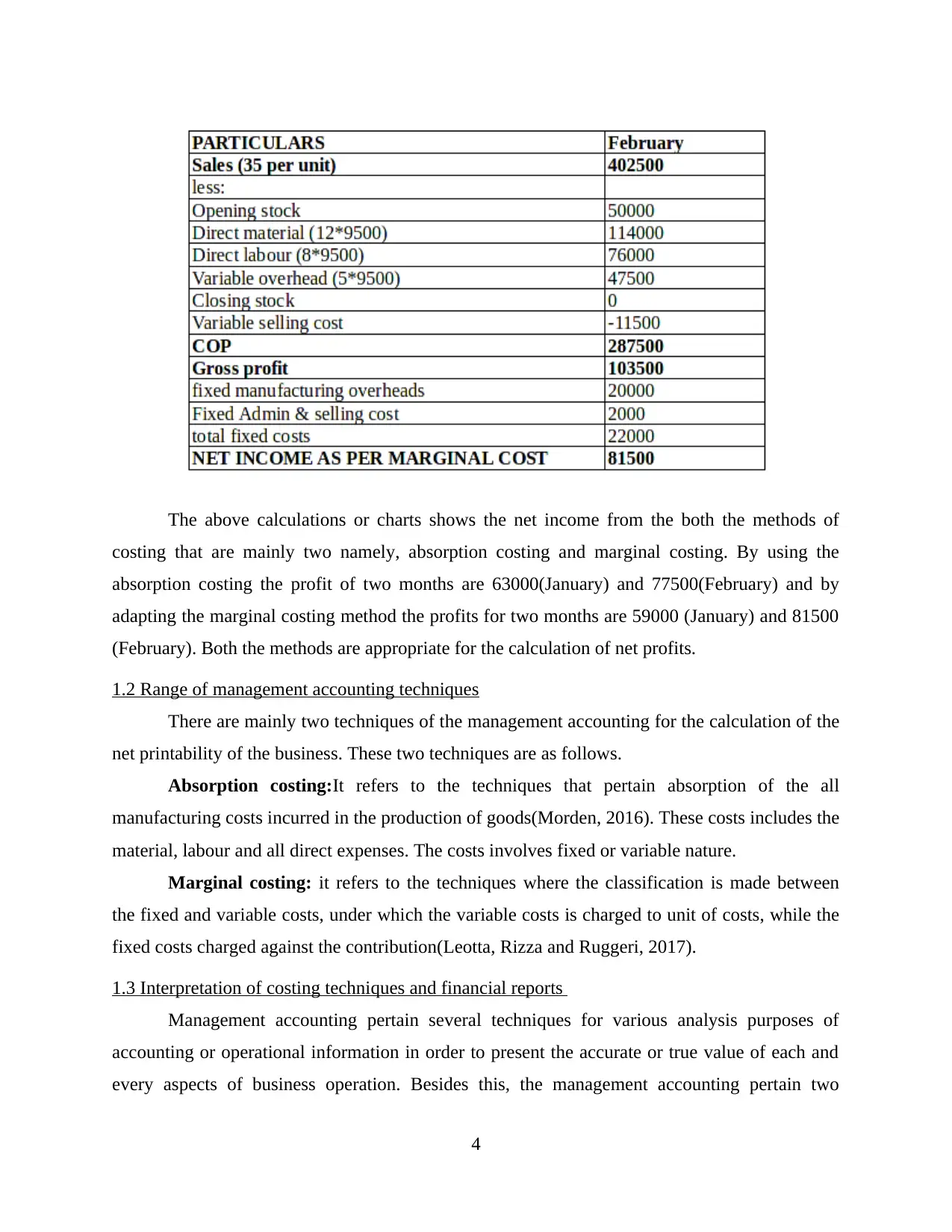

The above calculation shows the net profit quantified by the techniques of absorption comprises

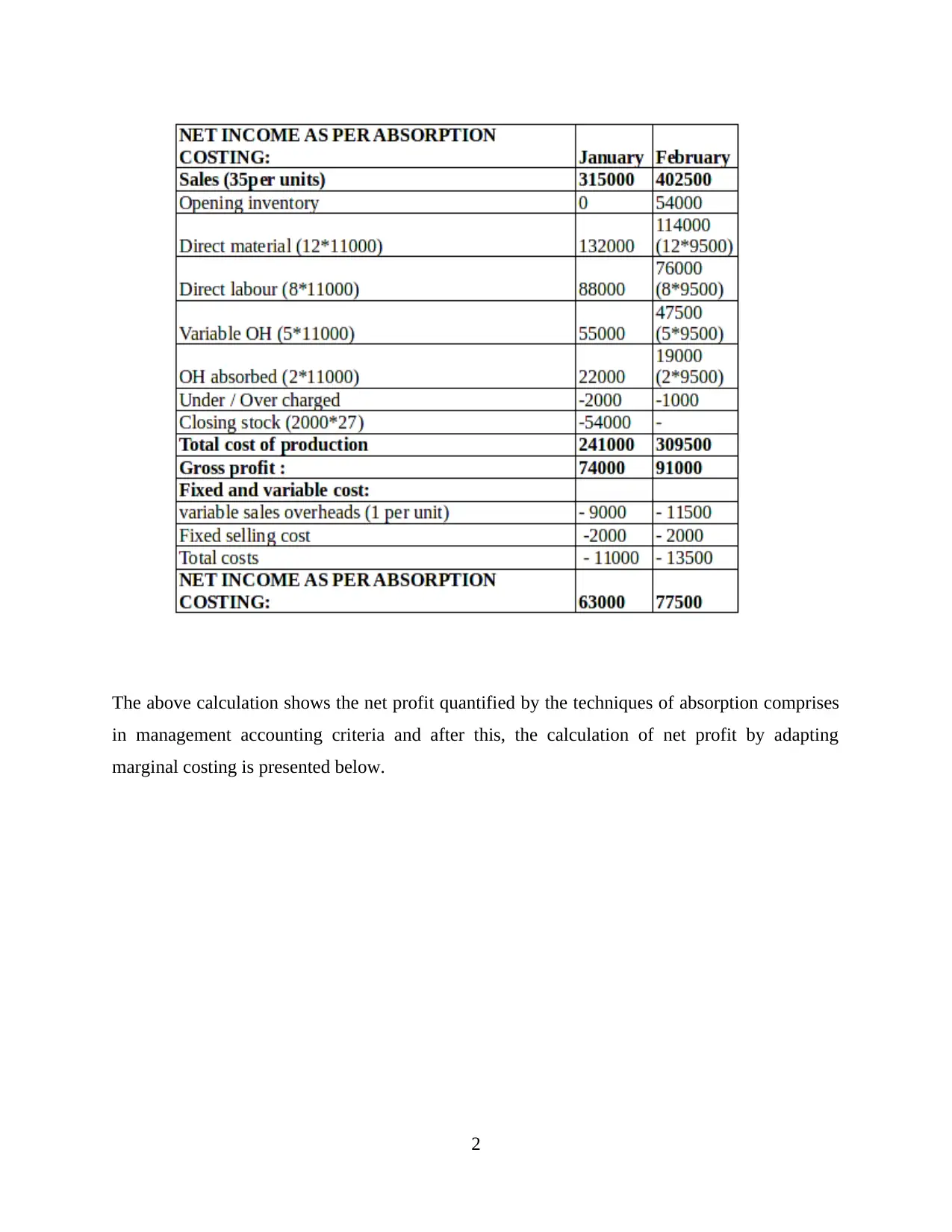

in management accounting criteria and after this, the calculation of net profit by adapting

marginal costing is presented below.

2

in management accounting criteria and after this, the calculation of net profit by adapting

marginal costing is presented below.

2

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

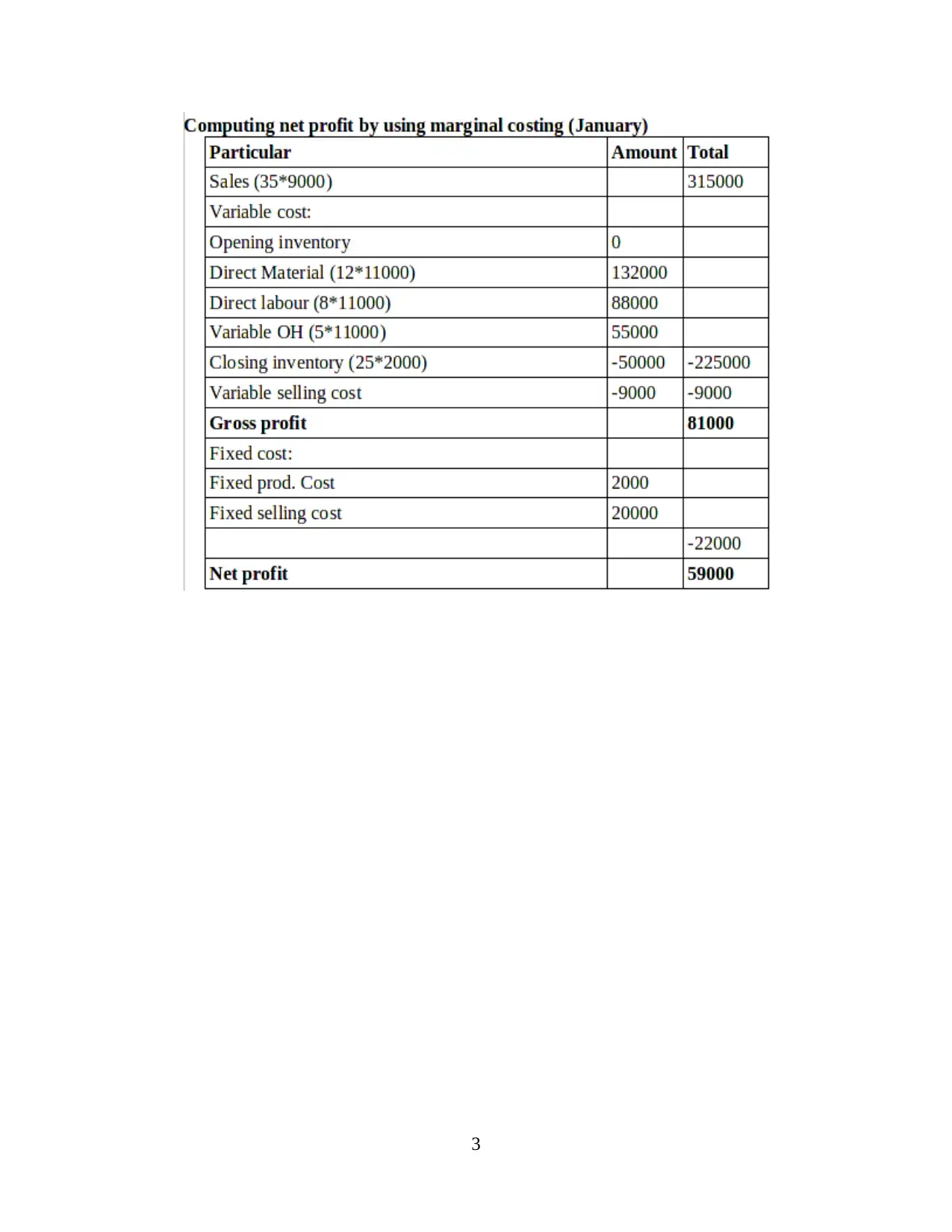

The above calculations or charts shows the net income from the both the methods of

costing that are mainly two namely, absorption costing and marginal costing. By using the

absorption costing the profit of two months are 63000(January) and 77500(February) and by

adapting the marginal costing method the profits for two months are 59000 (January) and 81500

(February). Both the methods are appropriate for the calculation of net profits.

1.2 Range of management accounting techniques

There are mainly two techniques of the management accounting for the calculation of the

net printability of the business. These two techniques are as follows.

Absorption costing:It refers to the techniques that pertain absorption of the all

manufacturing costs incurred in the production of goods(Morden, 2016). These costs includes the

material, labour and all direct expenses. The costs involves fixed or variable nature.

Marginal costing: it refers to the techniques where the classification is made between

the fixed and variable costs, under which the variable costs is charged to unit of costs, while the

fixed costs charged against the contribution(Leotta, Rizza and Ruggeri, 2017).

1.3 Interpretation of costing techniques and financial reports

Management accounting pertain several techniques for various analysis purposes of

accounting or operational information in order to present the accurate or true value of each and

every aspects of business operation. Besides this, the management accounting pertain two

4

costing that are mainly two namely, absorption costing and marginal costing. By using the

absorption costing the profit of two months are 63000(January) and 77500(February) and by

adapting the marginal costing method the profits for two months are 59000 (January) and 81500

(February). Both the methods are appropriate for the calculation of net profits.

1.2 Range of management accounting techniques

There are mainly two techniques of the management accounting for the calculation of the

net printability of the business. These two techniques are as follows.

Absorption costing:It refers to the techniques that pertain absorption of the all

manufacturing costs incurred in the production of goods(Morden, 2016). These costs includes the

material, labour and all direct expenses. The costs involves fixed or variable nature.

Marginal costing: it refers to the techniques where the classification is made between

the fixed and variable costs, under which the variable costs is charged to unit of costs, while the

fixed costs charged against the contribution(Leotta, Rizza and Ruggeri, 2017).

1.3 Interpretation of costing techniques and financial reports

Management accounting pertain several techniques for various analysis purposes of

accounting or operational information in order to present the accurate or true value of each and

every aspects of business operation. Besides this, the management accounting pertain two

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

techniques for the calculation of the net income from the production or operational activities as

these both techniques are effective in calculating the net income. As

TASK 2

2.1 Describing advantages and disadvantages of disadvantages of planning tools used for

budgetary control

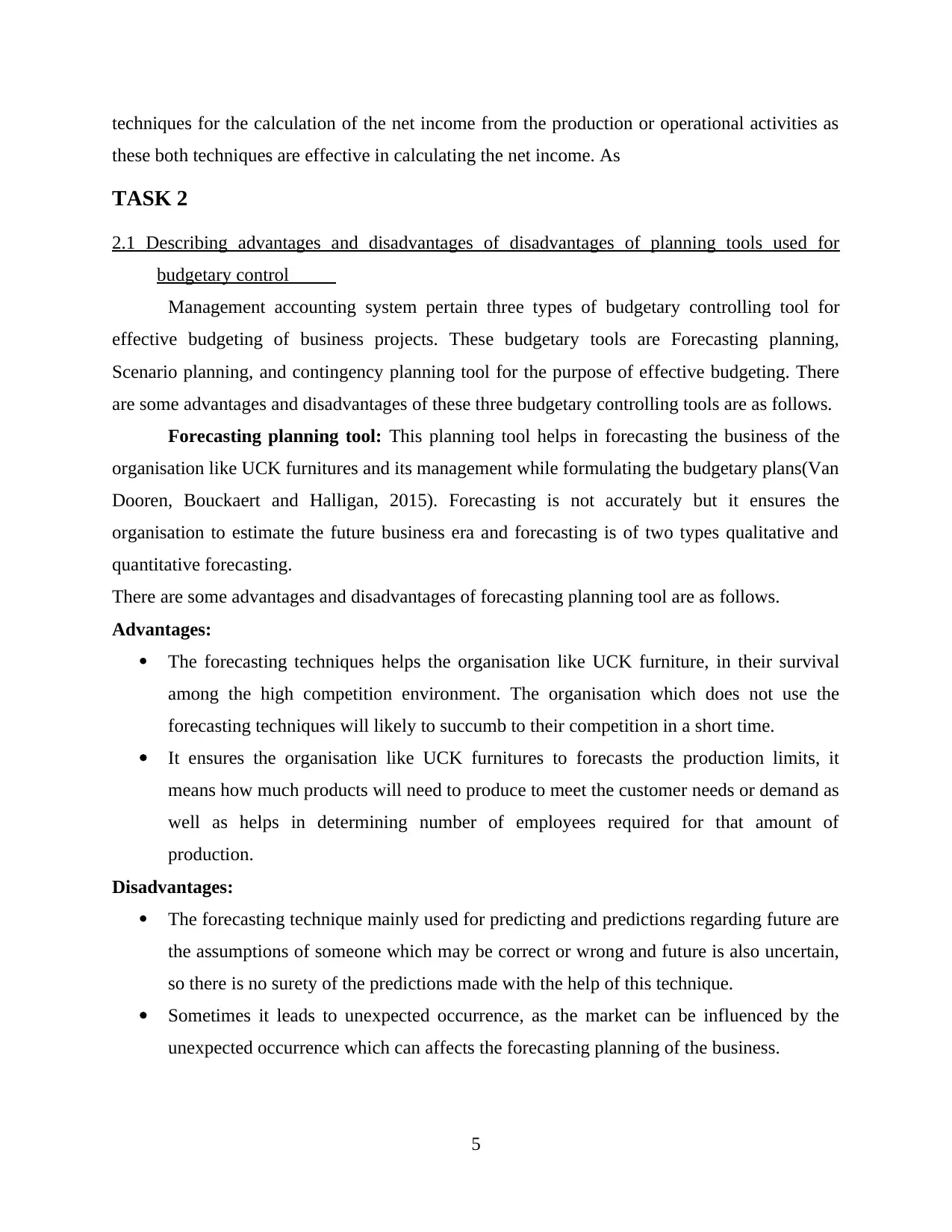

Management accounting system pertain three types of budgetary controlling tool for

effective budgeting of business projects. These budgetary tools are Forecasting planning,

Scenario planning, and contingency planning tool for the purpose of effective budgeting. There

are some advantages and disadvantages of these three budgetary controlling tools are as follows.

Forecasting planning tool: This planning tool helps in forecasting the business of the

organisation like UCK furnitures and its management while formulating the budgetary plans(Van

Dooren, Bouckaert and Halligan, 2015). Forecasting is not accurately but it ensures the

organisation to estimate the future business era and forecasting is of two types qualitative and

quantitative forecasting.

There are some advantages and disadvantages of forecasting planning tool are as follows.

Advantages:

The forecasting techniques helps the organisation like UCK furniture, in their survival

among the high competition environment. The organisation which does not use the

forecasting techniques will likely to succumb to their competition in a short time.

It ensures the organisation like UCK furnitures to forecasts the production limits, it

means how much products will need to produce to meet the customer needs or demand as

well as helps in determining number of employees required for that amount of

production.

Disadvantages:

The forecasting technique mainly used for predicting and predictions regarding future are

the assumptions of someone which may be correct or wrong and future is also uncertain,

so there is no surety of the predictions made with the help of this technique.

Sometimes it leads to unexpected occurrence, as the market can be influenced by the

unexpected occurrence which can affects the forecasting planning of the business.

5

these both techniques are effective in calculating the net income. As

TASK 2

2.1 Describing advantages and disadvantages of disadvantages of planning tools used for

budgetary control

Management accounting system pertain three types of budgetary controlling tool for

effective budgeting of business projects. These budgetary tools are Forecasting planning,

Scenario planning, and contingency planning tool for the purpose of effective budgeting. There

are some advantages and disadvantages of these three budgetary controlling tools are as follows.

Forecasting planning tool: This planning tool helps in forecasting the business of the

organisation like UCK furnitures and its management while formulating the budgetary plans(Van

Dooren, Bouckaert and Halligan, 2015). Forecasting is not accurately but it ensures the

organisation to estimate the future business era and forecasting is of two types qualitative and

quantitative forecasting.

There are some advantages and disadvantages of forecasting planning tool are as follows.

Advantages:

The forecasting techniques helps the organisation like UCK furniture, in their survival

among the high competition environment. The organisation which does not use the

forecasting techniques will likely to succumb to their competition in a short time.

It ensures the organisation like UCK furnitures to forecasts the production limits, it

means how much products will need to produce to meet the customer needs or demand as

well as helps in determining number of employees required for that amount of

production.

Disadvantages:

The forecasting technique mainly used for predicting and predictions regarding future are

the assumptions of someone which may be correct or wrong and future is also uncertain,

so there is no surety of the predictions made with the help of this technique.

Sometimes it leads to unexpected occurrence, as the market can be influenced by the

unexpected occurrence which can affects the forecasting planning of the business.

5

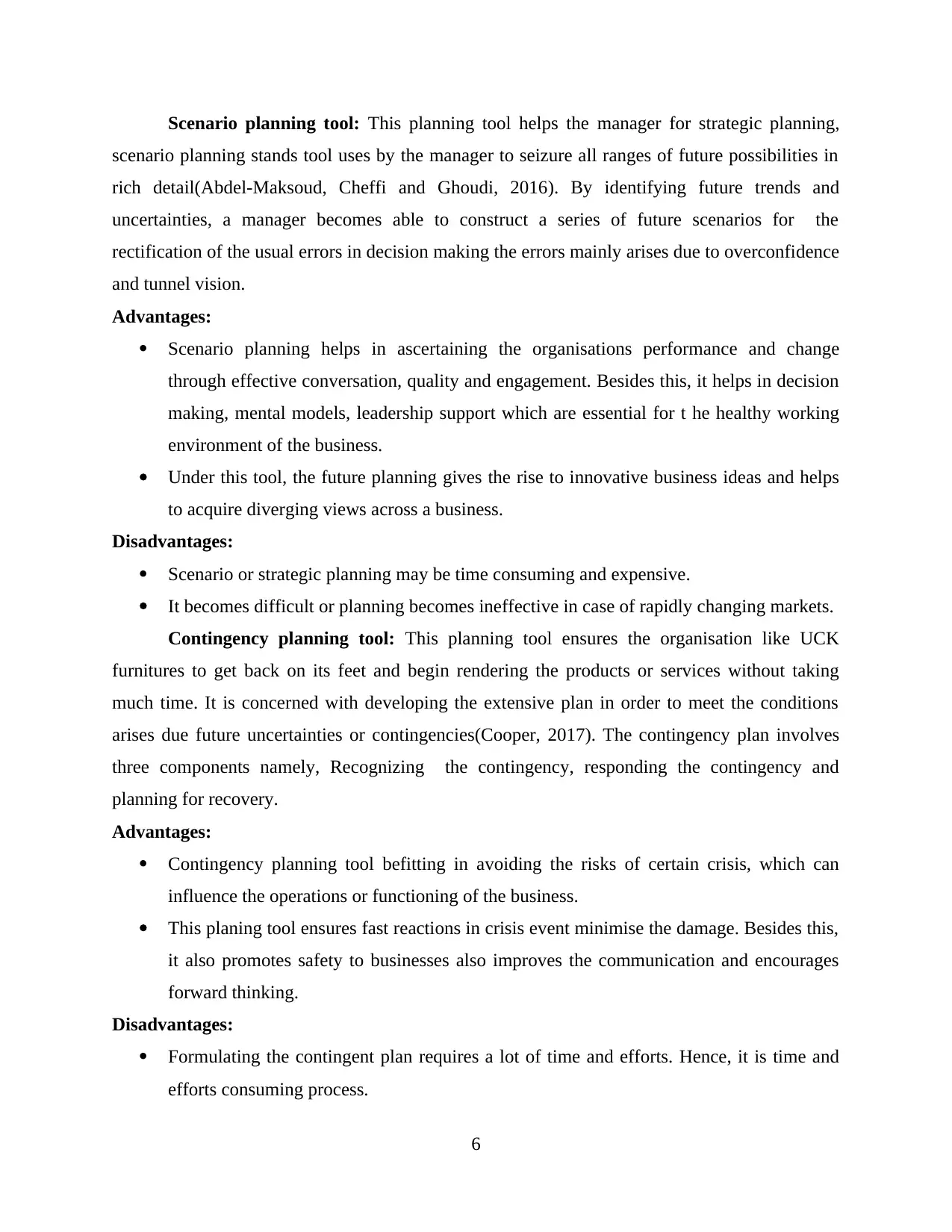

Scenario planning tool: This planning tool helps the manager for strategic planning,

scenario planning stands tool uses by the manager to seizure all ranges of future possibilities in

rich detail(Abdel-Maksoud, Cheffi and Ghoudi, 2016). By identifying future trends and

uncertainties, a manager becomes able to construct a series of future scenarios for the

rectification of the usual errors in decision making the errors mainly arises due to overconfidence

and tunnel vision.

Advantages:

Scenario planning helps in ascertaining the organisations performance and change

through effective conversation, quality and engagement. Besides this, it helps in decision

making, mental models, leadership support which are essential for t he healthy working

environment of the business.

Under this tool, the future planning gives the rise to innovative business ideas and helps

to acquire diverging views across a business.

Disadvantages:

Scenario or strategic planning may be time consuming and expensive.

It becomes difficult or planning becomes ineffective in case of rapidly changing markets.

Contingency planning tool: This planning tool ensures the organisation like UCK

furnitures to get back on its feet and begin rendering the products or services without taking

much time. It is concerned with developing the extensive plan in order to meet the conditions

arises due future uncertainties or contingencies(Cooper, 2017). The contingency plan involves

three components namely, Recognizing the contingency, responding the contingency and

planning for recovery.

Advantages:

Contingency planning tool befitting in avoiding the risks of certain crisis, which can

influence the operations or functioning of the business.

This planing tool ensures fast reactions in crisis event minimise the damage. Besides this,

it also promotes safety to businesses also improves the communication and encourages

forward thinking.

Disadvantages:

Formulating the contingent plan requires a lot of time and efforts. Hence, it is time and

efforts consuming process.

6

scenario planning stands tool uses by the manager to seizure all ranges of future possibilities in

rich detail(Abdel-Maksoud, Cheffi and Ghoudi, 2016). By identifying future trends and

uncertainties, a manager becomes able to construct a series of future scenarios for the

rectification of the usual errors in decision making the errors mainly arises due to overconfidence

and tunnel vision.

Advantages:

Scenario planning helps in ascertaining the organisations performance and change

through effective conversation, quality and engagement. Besides this, it helps in decision

making, mental models, leadership support which are essential for t he healthy working

environment of the business.

Under this tool, the future planning gives the rise to innovative business ideas and helps

to acquire diverging views across a business.

Disadvantages:

Scenario or strategic planning may be time consuming and expensive.

It becomes difficult or planning becomes ineffective in case of rapidly changing markets.

Contingency planning tool: This planning tool ensures the organisation like UCK

furnitures to get back on its feet and begin rendering the products or services without taking

much time. It is concerned with developing the extensive plan in order to meet the conditions

arises due future uncertainties or contingencies(Cooper, 2017). The contingency plan involves

three components namely, Recognizing the contingency, responding the contingency and

planning for recovery.

Advantages:

Contingency planning tool befitting in avoiding the risks of certain crisis, which can

influence the operations or functioning of the business.

This planing tool ensures fast reactions in crisis event minimise the damage. Besides this,

it also promotes safety to businesses also improves the communication and encourages

forward thinking.

Disadvantages:

Formulating the contingent plan requires a lot of time and efforts. Hence, it is time and

efforts consuming process.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

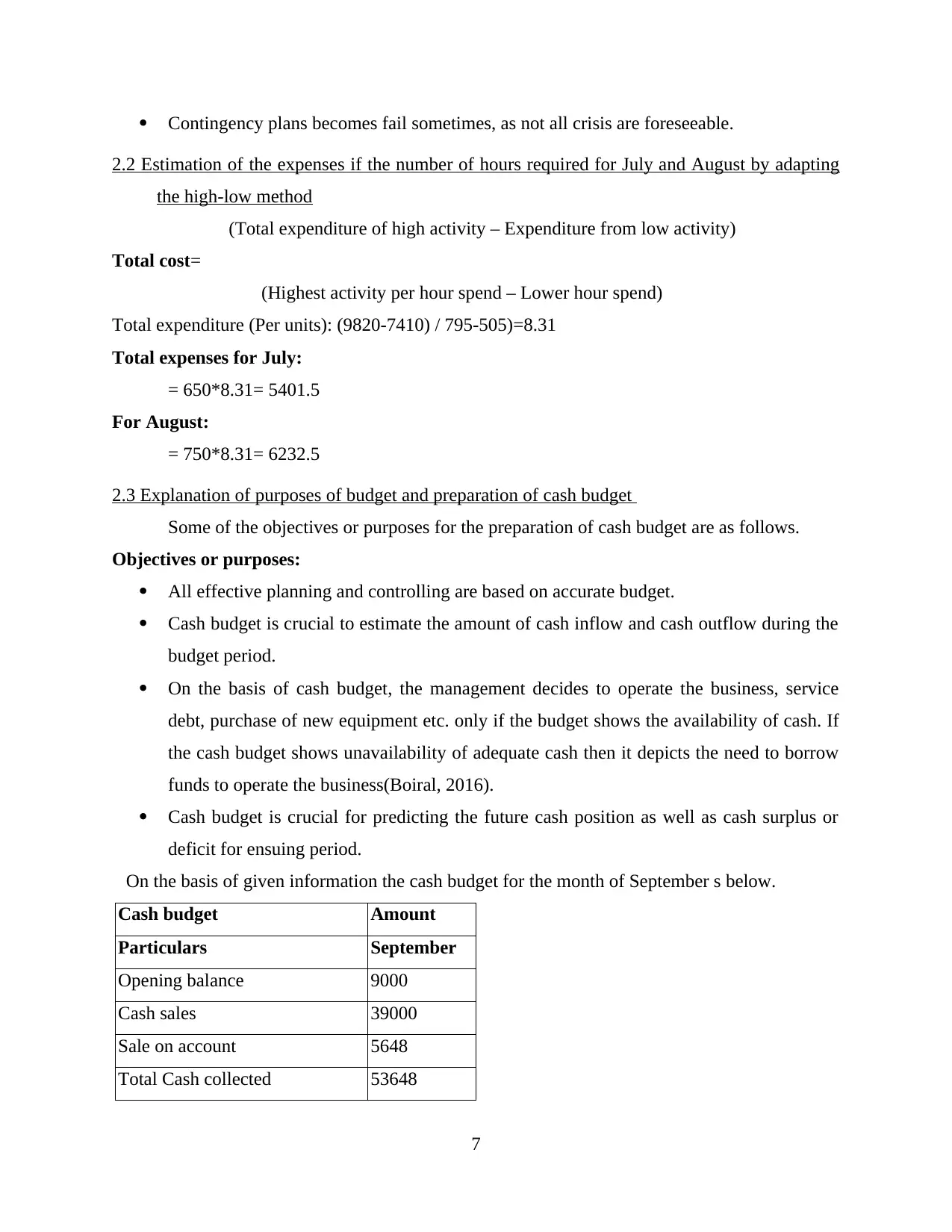

Contingency plans becomes fail sometimes, as not all crisis are foreseeable.

2.2 Estimation of the expenses if the number of hours required for July and August by adapting

the high-low method

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

2.3 Explanation of purposes of budget and preparation of cash budget

Some of the objectives or purposes for the preparation of cash budget are as follows.

Objectives or purposes:

All effective planning and controlling are based on accurate budget.

Cash budget is crucial to estimate the amount of cash inflow and cash outflow during the

budget period.

On the basis of cash budget, the management decides to operate the business, service

debt, purchase of new equipment etc. only if the budget shows the availability of cash. If

the cash budget shows unavailability of adequate cash then it depicts the need to borrow

funds to operate the business(Boiral, 2016).

Cash budget is crucial for predicting the future cash position as well as cash surplus or

deficit for ensuing period.

On the basis of given information the cash budget for the month of September s below.

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

7

2.2 Estimation of the expenses if the number of hours required for July and August by adapting

the high-low method

(Total expenditure of high activity – Expenditure from low activity)

Total cost=

(Highest activity per hour spend – Lower hour spend)

Total expenditure (Per units): (9820-7410) / 795-505)=8.31

Total expenses for July:

= 650*8.31= 5401.5

For August:

= 750*8.31= 6232.5

2.3 Explanation of purposes of budget and preparation of cash budget

Some of the objectives or purposes for the preparation of cash budget are as follows.

Objectives or purposes:

All effective planning and controlling are based on accurate budget.

Cash budget is crucial to estimate the amount of cash inflow and cash outflow during the

budget period.

On the basis of cash budget, the management decides to operate the business, service

debt, purchase of new equipment etc. only if the budget shows the availability of cash. If

the cash budget shows unavailability of adequate cash then it depicts the need to borrow

funds to operate the business(Boiral, 2016).

Cash budget is crucial for predicting the future cash position as well as cash surplus or

deficit for ensuing period.

On the basis of given information the cash budget for the month of September s below.

Cash budget Amount

Particulars September

Opening balance 9000

Cash sales 39000

Sale on account 5648

Total Cash collected 53648

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

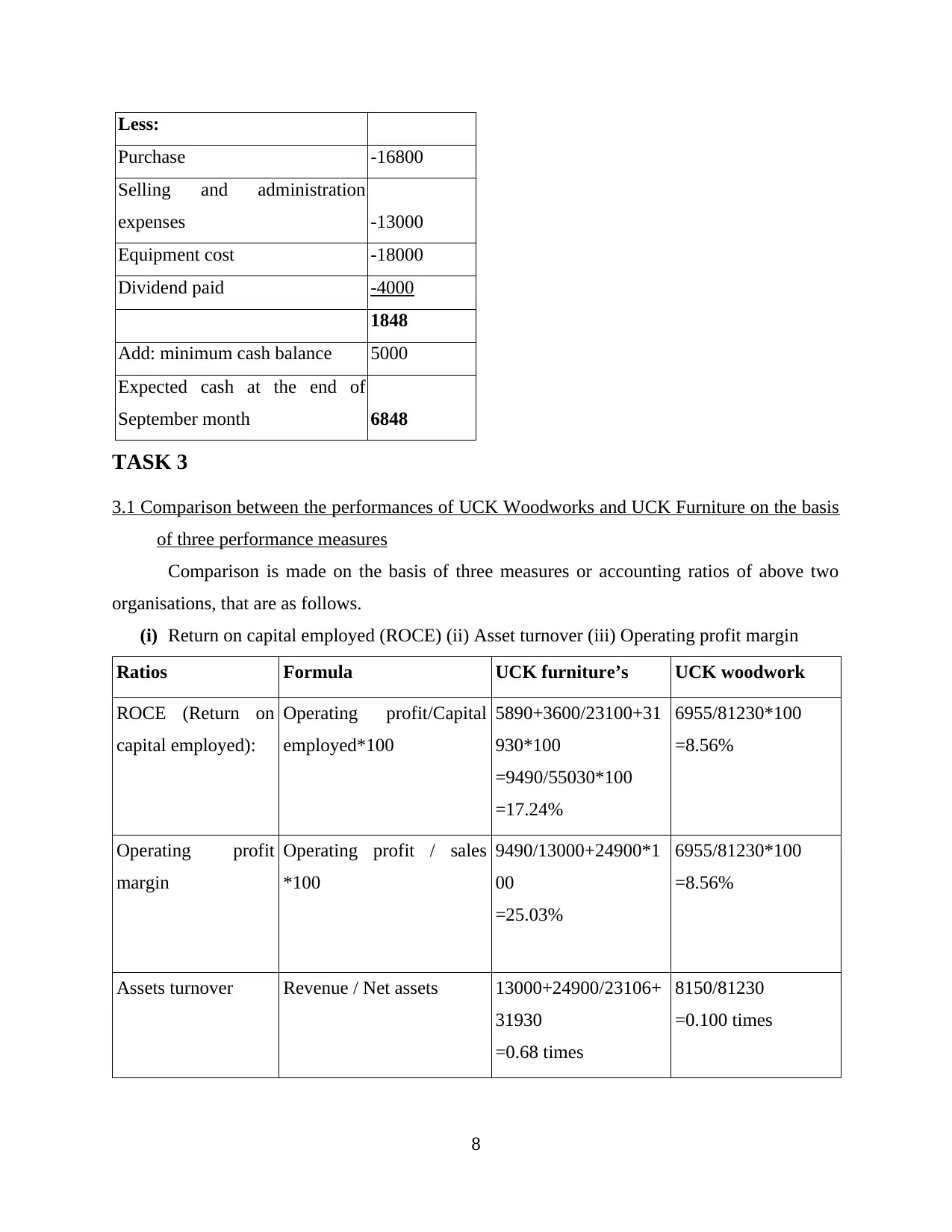

Less:

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1 Comparison between the performances of UCK Woodworks and UCK Furniture on the basis

of three performance measures

Comparison is made on the basis of three measures or accounting ratios of above two

organisations, that are as follows.

(i) Return on capital employed (ROCE) (ii) Asset turnover (iii) Operating profit margin

Ratios Formula UCK furniture’s UCK woodwork

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

8

Purchase -16800

Selling and administration

expenses -13000

Equipment cost -18000

Dividend paid -4000

1848

Add: minimum cash balance 5000

Expected cash at the end of

September month 6848

TASK 3

3.1 Comparison between the performances of UCK Woodworks and UCK Furniture on the basis

of three performance measures

Comparison is made on the basis of three measures or accounting ratios of above two

organisations, that are as follows.

(i) Return on capital employed (ROCE) (ii) Asset turnover (iii) Operating profit margin

Ratios Formula UCK furniture’s UCK woodwork

ROCE (Return on

capital employed):

Operating profit/Capital

employed*100

5890+3600/23100+31

930*100

=9490/55030*100

=17.24%

6955/81230*100

=8.56%

Operating profit

margin

Operating profit / sales

*100

9490/13000+24900*1

00

=25.03%

6955/81230*100

=8.56%

Assets turnover Revenue / Net assets 13000+24900/23106+

31930

=0.68 times

8150/81230

=0.100 times

8

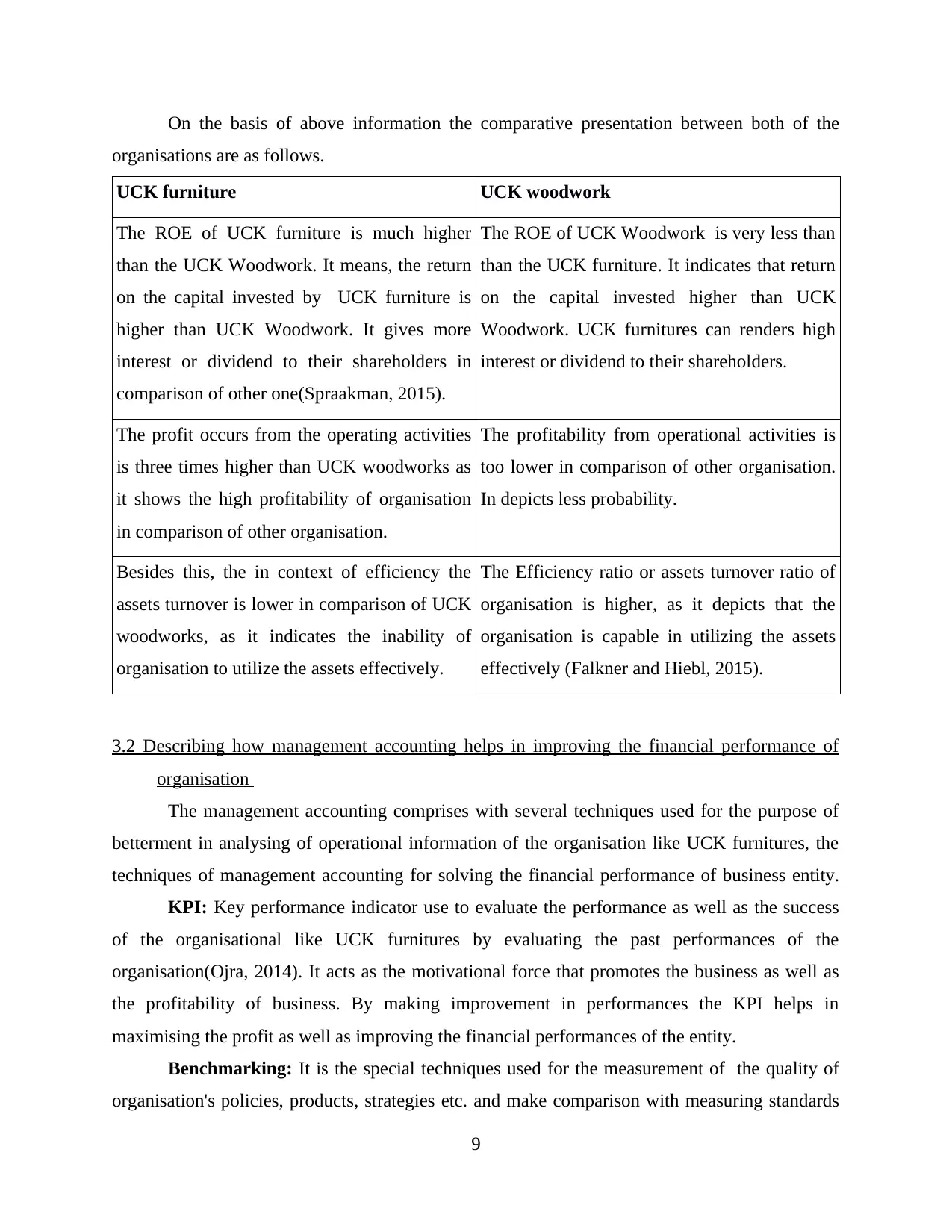

On the basis of above information the comparative presentation between both of the

organisations are as follows.

UCK furniture UCK woodwork

The ROE of UCK furniture is much higher

than the UCK Woodwork. It means, the return

on the capital invested by UCK furniture is

higher than UCK Woodwork. It gives more

interest or dividend to their shareholders in

comparison of other one(Spraakman, 2015).

The ROE of UCK Woodwork is very less than

than the UCK furniture. It indicates that return

on the capital invested higher than UCK

Woodwork. UCK furnitures can renders high

interest or dividend to their shareholders.

The profit occurs from the operating activities

is three times higher than UCK woodworks as

it shows the high profitability of organisation

in comparison of other organisation.

The profitability from operational activities is

too lower in comparison of other organisation.

In depicts less probability.

Besides this, the in context of efficiency the

assets turnover is lower in comparison of UCK

woodworks, as it indicates the inability of

organisation to utilize the assets effectively.

The Efficiency ratio or assets turnover ratio of

organisation is higher, as it depicts that the

organisation is capable in utilizing the assets

effectively (Falkner and Hiebl, 2015).

3.2 Describing how management accounting helps in improving the financial performance of

organisation

The management accounting comprises with several techniques used for the purpose of

betterment in analysing of operational information of the organisation like UCK furnitures, the

techniques of management accounting for solving the financial performance of business entity.

KPI: Key performance indicator use to evaluate the performance as well as the success

of the organisational like UCK furnitures by evaluating the past performances of the

organisation(Ojra, 2014). It acts as the motivational force that promotes the business as well as

the profitability of business. By making improvement in performances the KPI helps in

maximising the profit as well as improving the financial performances of the entity.

Benchmarking: It is the special techniques used for the measurement of the quality of

organisation's policies, products, strategies etc. and make comparison with measuring standards

9

organisations are as follows.

UCK furniture UCK woodwork

The ROE of UCK furniture is much higher

than the UCK Woodwork. It means, the return

on the capital invested by UCK furniture is

higher than UCK Woodwork. It gives more

interest or dividend to their shareholders in

comparison of other one(Spraakman, 2015).

The ROE of UCK Woodwork is very less than

than the UCK furniture. It indicates that return

on the capital invested higher than UCK

Woodwork. UCK furnitures can renders high

interest or dividend to their shareholders.

The profit occurs from the operating activities

is three times higher than UCK woodworks as

it shows the high profitability of organisation

in comparison of other organisation.

The profitability from operational activities is

too lower in comparison of other organisation.

In depicts less probability.

Besides this, the in context of efficiency the

assets turnover is lower in comparison of UCK

woodworks, as it indicates the inability of

organisation to utilize the assets effectively.

The Efficiency ratio or assets turnover ratio of

organisation is higher, as it depicts that the

organisation is capable in utilizing the assets

effectively (Falkner and Hiebl, 2015).

3.2 Describing how management accounting helps in improving the financial performance of

organisation

The management accounting comprises with several techniques used for the purpose of

betterment in analysing of operational information of the organisation like UCK furnitures, the

techniques of management accounting for solving the financial performance of business entity.

KPI: Key performance indicator use to evaluate the performance as well as the success

of the organisational like UCK furnitures by evaluating the past performances of the

organisation(Ojra, 2014). It acts as the motivational force that promotes the business as well as

the profitability of business. By making improvement in performances the KPI helps in

maximising the profit as well as improving the financial performances of the entity.

Benchmarking: It is the special techniques used for the measurement of the quality of

organisation's policies, products, strategies etc. and make comparison with measuring standards

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.