Analysis of Management Accounting Systems and Reporting at Oshodi PLC

VerifiedAdded on 2021/02/20

|18

|4814

|319

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its crucial role in providing timely and relevant financial information to facilitate effective decision-making and strategic planning within organizations. The report uses Oshodi PLC, a manufacturing firm specializing in JOJO fruit juice, as a case study to illustrate various management accounting systems, including price optimization, inventory management, cost accounting, and job costing. It examines different types of management accounting reporting, such as budget reports, accounts receivable reports, performance reports, and competitor analysis reports. Furthermore, the report demonstrates the production of income statements using both marginal and absorption costing methods, comparing their implications. It also explores planning tools for budgetary control, including the advantages and disadvantages of budgeting and zero-base budgeting. The report concludes by defining a financial problem and comparing different organizations using management accounting systems.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Introduction......................................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different kind of management accounting system..................1

P2: Different types of management accounting reporting. ........................................................2

TASK 2............................................................................................................................................4

P3: Produce income statement by using marginal or absorption costing method.......................4

TASK 3............................................................................................................................................6

P4. Planning tools for budgetary control ....................................................................................6

TASK 4............................................................................................................................................9

P5: Define financial problem and comparison different organisation by masking the use of

management accounting system..................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

Introduction......................................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and different kind of management accounting system..................1

P2: Different types of management accounting reporting. ........................................................2

TASK 2............................................................................................................................................4

P3: Produce income statement by using marginal or absorption costing method.......................4

TASK 3............................................................................................................................................6

P4. Planning tools for budgetary control ....................................................................................6

TASK 4............................................................................................................................................9

P5: Define financial problem and comparison different organisation by masking the use of

management accounting system..................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

In the current business world the biggest shortcomings for businesses is proper

information availability at the right time with relevant data. Management accounting has evolved

over the years since its inception into a broad fundamental system of providing critical financial

information related to business to the management body(Adler, R., 2013). This information helps

the management in interpreting financial performance, profitability, market value, and future

decision-making for the firm. This report includes a study on management accounting, its tools

and techniques, processes, systems and organisational influence taking Oshodi PLC, a

manufacturing firm engaged in production of JOJO fruit juice.

TASK 1

P1: Management accounting and different kind of management accounting system.

Management Accounting: It is a fundamental principle of preparing financial and non

financial statements of the business to aid the management body in decision making and strategic

planning for the future endeavours. It is an internal management principle as opposed to the

financial accounting which is an external principle (Altman and et. al. 1979). It deals with

preparing business reports, data and statements in an accurate format for the business managers

to be used by them to analyse the functioning of the business, analyse its profitability position

and plan for the future based on the insights drawn from past evaluations. Oshodi PLC analysts

has acquired an efficient system of reporting critical information to the managers using its

internal systems.

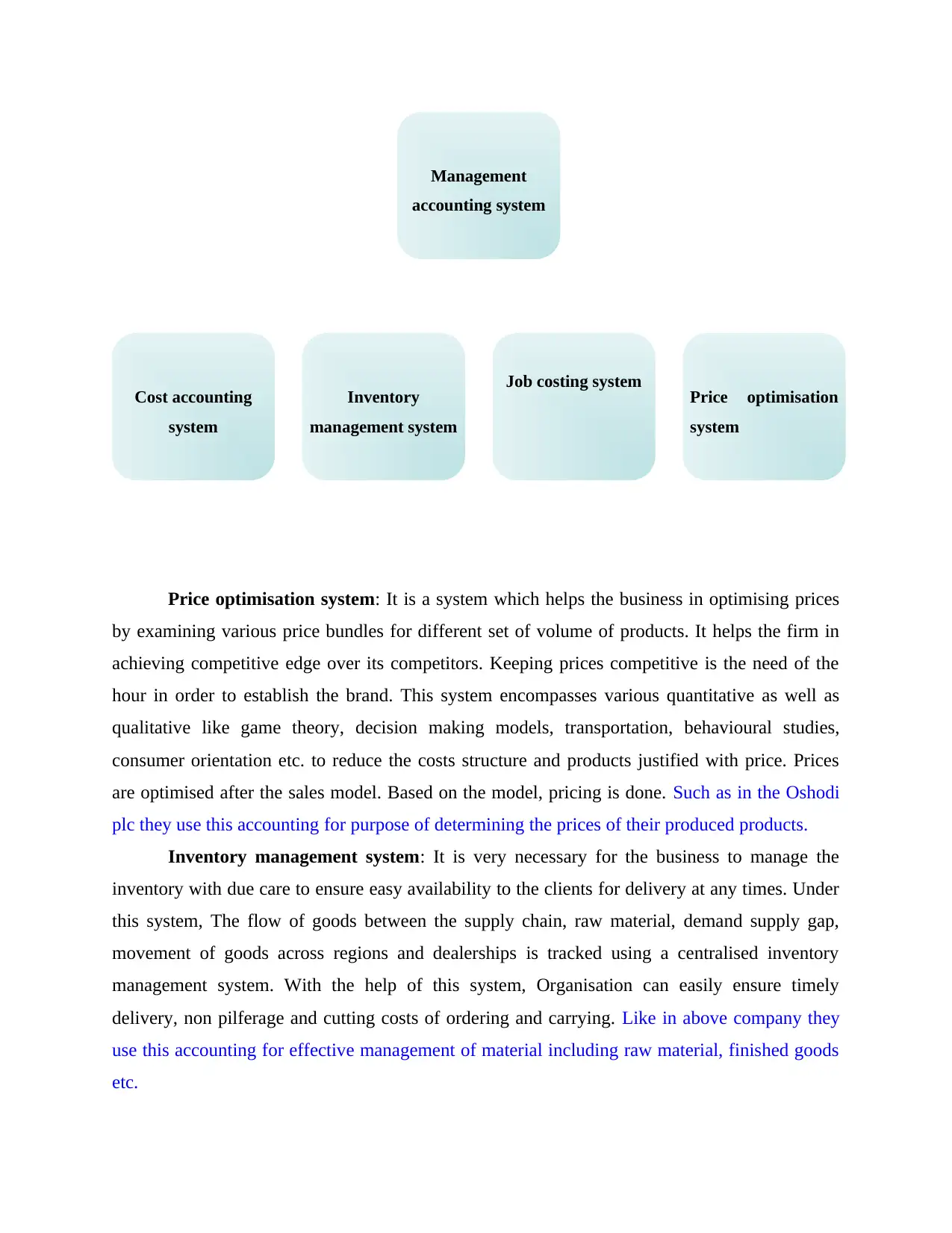

Management Accounting systems: Management accounting systems are cohesive

collaboration of various integral systems which as a complex whole makes it a theory (Kaplan,

R.S. and Atkinson, A.A., 2015). These systems provides sectoral information which has

individual characteristics and importance. Based on the reports generated by these systems, the

management body of Oshodi PLC is able to take some serious decision about the adaptation of

new business policies and practices. The cardinal systems used by Oshodi plc are as follows:

In the current business world the biggest shortcomings for businesses is proper

information availability at the right time with relevant data. Management accounting has evolved

over the years since its inception into a broad fundamental system of providing critical financial

information related to business to the management body(Adler, R., 2013). This information helps

the management in interpreting financial performance, profitability, market value, and future

decision-making for the firm. This report includes a study on management accounting, its tools

and techniques, processes, systems and organisational influence taking Oshodi PLC, a

manufacturing firm engaged in production of JOJO fruit juice.

TASK 1

P1: Management accounting and different kind of management accounting system.

Management Accounting: It is a fundamental principle of preparing financial and non

financial statements of the business to aid the management body in decision making and strategic

planning for the future endeavours. It is an internal management principle as opposed to the

financial accounting which is an external principle (Altman and et. al. 1979). It deals with

preparing business reports, data and statements in an accurate format for the business managers

to be used by them to analyse the functioning of the business, analyse its profitability position

and plan for the future based on the insights drawn from past evaluations. Oshodi PLC analysts

has acquired an efficient system of reporting critical information to the managers using its

internal systems.

Management Accounting systems: Management accounting systems are cohesive

collaboration of various integral systems which as a complex whole makes it a theory (Kaplan,

R.S. and Atkinson, A.A., 2015). These systems provides sectoral information which has

individual characteristics and importance. Based on the reports generated by these systems, the

management body of Oshodi PLC is able to take some serious decision about the adaptation of

new business policies and practices. The cardinal systems used by Oshodi plc are as follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimisation system: It is a system which helps the business in optimising prices

by examining various price bundles for different set of volume of products. It helps the firm in

achieving competitive edge over its competitors. Keeping prices competitive is the need of the

hour in order to establish the brand. This system encompasses various quantitative as well as

qualitative like game theory, decision making models, transportation, behavioural studies,

consumer orientation etc. to reduce the costs structure and products justified with price. Prices

are optimised after the sales model. Based on the model, pricing is done. Such as in the Oshodi

plc they use this accounting for purpose of determining the prices of their produced products.

Inventory management system: It is very necessary for the business to manage the

inventory with due care to ensure easy availability to the clients for delivery at any times. Under

this system, The flow of goods between the supply chain, raw material, demand supply gap,

movement of goods across regions and dealerships is tracked using a centralised inventory

management system. With the help of this system, Organisation can easily ensure timely

delivery, non pilferage and cutting costs of ordering and carrying. Like in above company they

use this accounting for effective management of material including raw material, finished goods

etc.

Management

accounting system

Cost accounting

system

Inventory

management system

Job costing system Price optimisation

system

by examining various price bundles for different set of volume of products. It helps the firm in

achieving competitive edge over its competitors. Keeping prices competitive is the need of the

hour in order to establish the brand. This system encompasses various quantitative as well as

qualitative like game theory, decision making models, transportation, behavioural studies,

consumer orientation etc. to reduce the costs structure and products justified with price. Prices

are optimised after the sales model. Based on the model, pricing is done. Such as in the Oshodi

plc they use this accounting for purpose of determining the prices of their produced products.

Inventory management system: It is very necessary for the business to manage the

inventory with due care to ensure easy availability to the clients for delivery at any times. Under

this system, The flow of goods between the supply chain, raw material, demand supply gap,

movement of goods across regions and dealerships is tracked using a centralised inventory

management system. With the help of this system, Organisation can easily ensure timely

delivery, non pilferage and cutting costs of ordering and carrying. Like in above company they

use this accounting for effective management of material including raw material, finished goods

etc.

Management

accounting system

Cost accounting

system

Inventory

management system

Job costing system Price optimisation

system

Cost accounting system: Costs incurred in production adds up to the final price. Hence,

to analyse costs, organisations has designed cost accounting systems. Cost accounting is a

technique which deals with the cost control mechanism (Wickramasinghe, D. and Alawattage,

C., 2012). This system studies the cost to output ratio between each factor of production engaged

in production activities. If the costs are irrelevant or undermines the value of the product then

they are eliminated or replaced. Costing technique helps the management in evaluating

profitability of the business by analysing performance of each cost in relation to the profits

earned. For example in above company they use this system for managing their overall

expenditures in an effective manner so that their expenditures can be reduced.

Job costing system: This system tracks the revenue and costs based on the 'job' work

done in producing the product. It analyses the profitability ratio based on the job performance. In

the application of job costing technique, Direct and indirect costs are added up to the 'job'. This is

a system of determining labour and materials costs for each job in a phased manner used to

finally quote a price for the client. In a job costing system, costs are added up either by a job or

by a batch. It fundamentally differs from process costing which is based on the costs of

processes. In above Oshidi Plc company, they apply it for getting information about cost of job.

P2: Different types of management accounting reporting.

Management accounting reporting is a system of generating internal management reports

based on the information generated by the management accounting systems. These reports

include past and present data in a curated format, performances evaluation of internal systems for

the years, deviations between the budgeted and actual performances and the relative

departmental data based on the responsibilities (Cardoş, I.R., 2014). These reports provide all the

maximum data into a concised format which makes it legible for the managers to quickly

understand it and take further actions for the coming years. Oshodi plc has designed a nexus

between various management accounting reports generated through their individual systems.

Some of the reports are as follows:

to analyse costs, organisations has designed cost accounting systems. Cost accounting is a

technique which deals with the cost control mechanism (Wickramasinghe, D. and Alawattage,

C., 2012). This system studies the cost to output ratio between each factor of production engaged

in production activities. If the costs are irrelevant or undermines the value of the product then

they are eliminated or replaced. Costing technique helps the management in evaluating

profitability of the business by analysing performance of each cost in relation to the profits

earned. For example in above company they use this system for managing their overall

expenditures in an effective manner so that their expenditures can be reduced.

Job costing system: This system tracks the revenue and costs based on the 'job' work

done in producing the product. It analyses the profitability ratio based on the job performance. In

the application of job costing technique, Direct and indirect costs are added up to the 'job'. This is

a system of determining labour and materials costs for each job in a phased manner used to

finally quote a price for the client. In a job costing system, costs are added up either by a job or

by a batch. It fundamentally differs from process costing which is based on the costs of

processes. In above Oshidi Plc company, they apply it for getting information about cost of job.

P2: Different types of management accounting reporting.

Management accounting reporting is a system of generating internal management reports

based on the information generated by the management accounting systems. These reports

include past and present data in a curated format, performances evaluation of internal systems for

the years, deviations between the budgeted and actual performances and the relative

departmental data based on the responsibilities (Cardoş, I.R., 2014). These reports provide all the

maximum data into a concised format which makes it legible for the managers to quickly

understand it and take further actions for the coming years. Oshodi plc has designed a nexus

between various management accounting reports generated through their individual systems.

Some of the reports are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: A budget report carries data related to the organisational and

departmental actual performance outcomes based on the relativity of budgeted positions. The

report examines the performance standards of each area of production which is incidental or

auxiliary to the core activities. This report also encompasses the yearly budget performance

which helps the management to evaluate the constant performance for the years, which helps

them in constantly evolving towards setting better performance standards for each budget period.

The Oshodi plc company, use this report for proper allocation of financial resources in the

activities and functions.

Account receivable report: This report provides Oshodi plc with critical information

about all the debtors and creditors, bills to be received, due dates, addresses and the time line for

each payment. This report increases the overall financial cycle efficiency of the business by

ensuring smooth flow of funds. With the help of this report, Organisation can ensure that no

money gets pilfered or unpaid due to cumbersome system of dealing with the fund flow system.

Keeping a track on the funds makes the liquidity position of the firm strong. The above company

analyse about total receivable amount from various debtors with the help of this report.

Performance report: Based on the performance standards as evaluated by key

performance indicators set by the firm, this report includes the performance of each factor

system based on the allocated budget and variation between the outcomes (Sian, S. and Roberts,

C., 2009). Evaluation of performances is necessary for a business to evolve with time. This

report helps in identification of key factors which has favoured in the performance enhancement

Management

accounting

reports

Budget reports Competitor

analysis report

Account

receivable

reports

Performance

management

reports

departmental actual performance outcomes based on the relativity of budgeted positions. The

report examines the performance standards of each area of production which is incidental or

auxiliary to the core activities. This report also encompasses the yearly budget performance

which helps the management to evaluate the constant performance for the years, which helps

them in constantly evolving towards setting better performance standards for each budget period.

The Oshodi plc company, use this report for proper allocation of financial resources in the

activities and functions.

Account receivable report: This report provides Oshodi plc with critical information

about all the debtors and creditors, bills to be received, due dates, addresses and the time line for

each payment. This report increases the overall financial cycle efficiency of the business by

ensuring smooth flow of funds. With the help of this report, Organisation can ensure that no

money gets pilfered or unpaid due to cumbersome system of dealing with the fund flow system.

Keeping a track on the funds makes the liquidity position of the firm strong. The above company

analyse about total receivable amount from various debtors with the help of this report.

Performance report: Based on the performance standards as evaluated by key

performance indicators set by the firm, this report includes the performance of each factor

system based on the allocated budget and variation between the outcomes (Sian, S. and Roberts,

C., 2009). Evaluation of performances is necessary for a business to evolve with time. This

report helps in identification of key factors which has favoured in the performance enhancement

Management

accounting

reports

Budget reports Competitor

analysis report

Account

receivable

reports

Performance

management

reports

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and the factors which has led to decline in the performance. Based on such report, executives can

design new policy framework for increasing efficiency. Such as in above respective company,

this report is important in analysing the performance of various activities and functions.

Competitor analysis report: Identification of competition is way important for a

manufacturing firm like Oshodi plc which is engaged in beverages business which is a highly

competitive field where new products are launched by competitors on daily basis. This report is

developed with the help of fundamental theoretical principles propounded by great management

thinkers (Kokubu, K. and Kitada, H., 2015). With the help of the report, the executive body of

the firm enables itself to identify the latest trends followed by other businesses which aids the

business in evolving with the trends. So overall, this report is useful for companies like Oshodi

plc in providing information about total competitors in the environment.

TASK 2

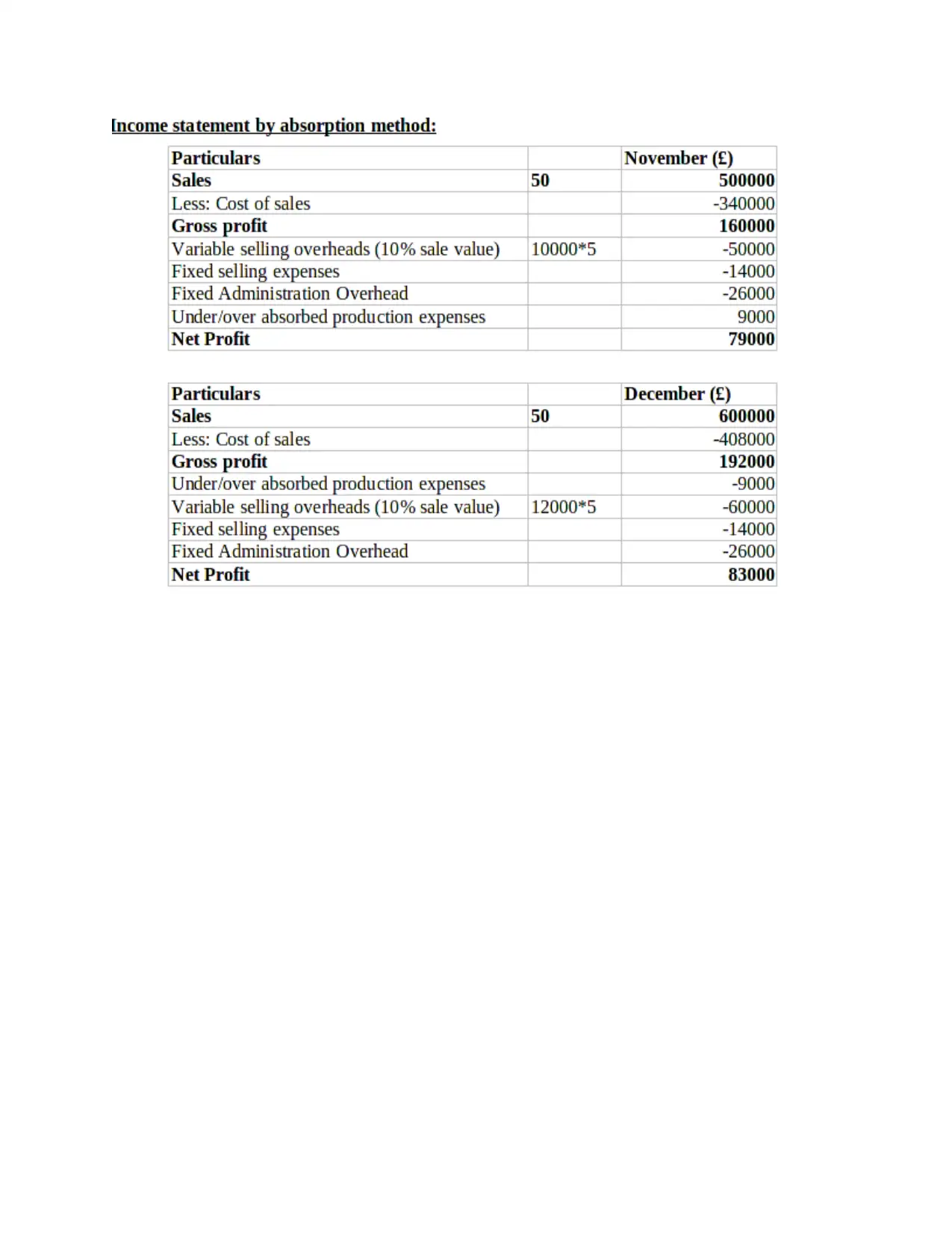

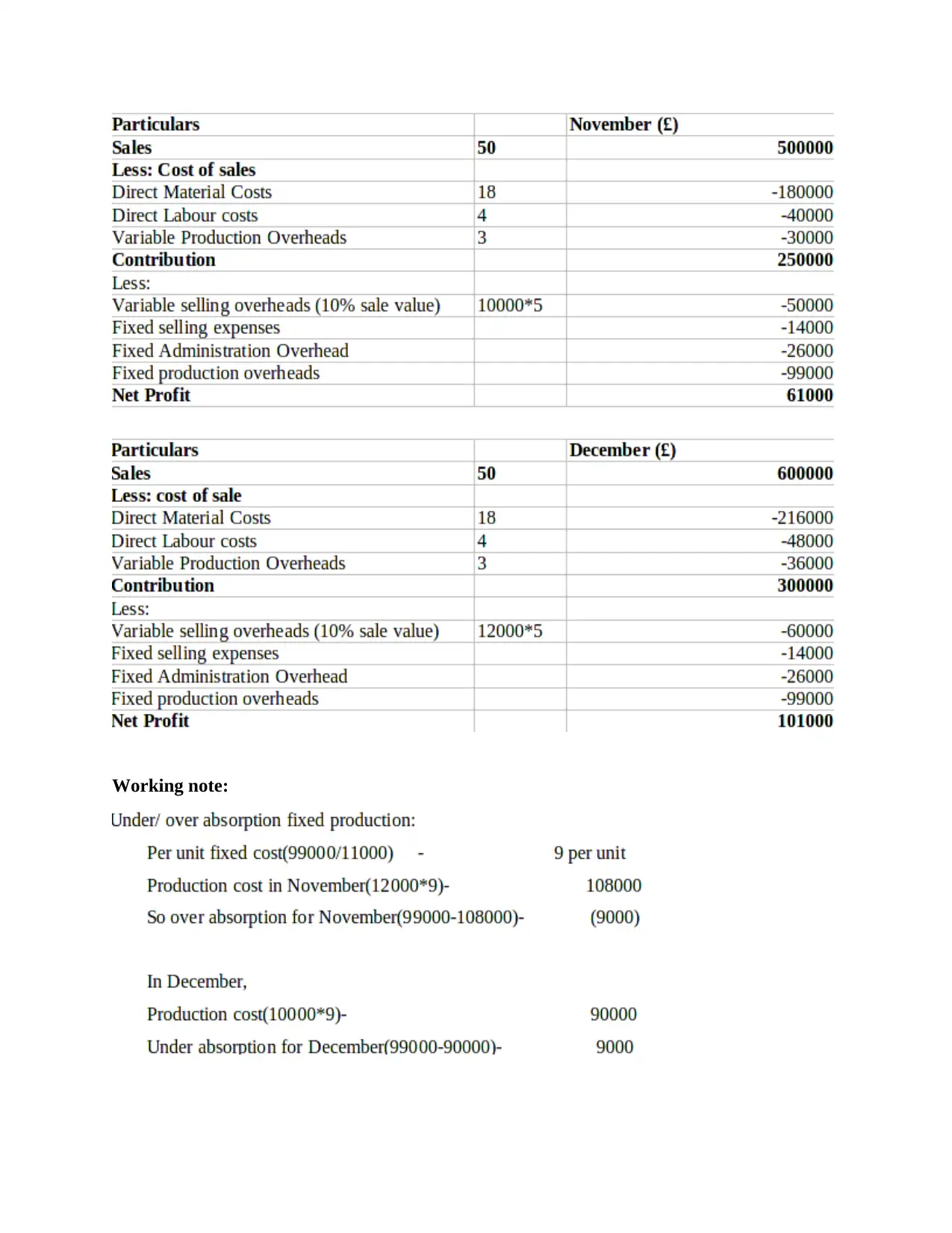

P3: Produce income statement by using marginal or absorption costing method.

Marginal costing : It is the total change in cost that occurs as a result of change in one

additional unit of production. This technique is used to determine the level at which the

organisation which achieve economies of scale (Fisher, J.G. and Krumwiede, K., 2015). It is

used by the management body of the business to sideline the optimum production level and to

reach a point where analysis of an additional unit added in the production line could be done

through marginal costing mechanism.

Absorption costing: This technique is used in evaluation of inventory. It considers cost

of materials, labour, fixed and variable overheads. It is considered as full costing technique. The

biggest benefit associated with this method is that it is GAAP compliant and Is required for

preparing financial statements and valuation of stocks. It helps in determination of selling price

of the products. (Göx, R.F., 2000)

design new policy framework for increasing efficiency. Such as in above respective company,

this report is important in analysing the performance of various activities and functions.

Competitor analysis report: Identification of competition is way important for a

manufacturing firm like Oshodi plc which is engaged in beverages business which is a highly

competitive field where new products are launched by competitors on daily basis. This report is

developed with the help of fundamental theoretical principles propounded by great management

thinkers (Kokubu, K. and Kitada, H., 2015). With the help of the report, the executive body of

the firm enables itself to identify the latest trends followed by other businesses which aids the

business in evolving with the trends. So overall, this report is useful for companies like Oshodi

plc in providing information about total competitors in the environment.

TASK 2

P3: Produce income statement by using marginal or absorption costing method.

Marginal costing : It is the total change in cost that occurs as a result of change in one

additional unit of production. This technique is used to determine the level at which the

organisation which achieve economies of scale (Fisher, J.G. and Krumwiede, K., 2015). It is

used by the management body of the business to sideline the optimum production level and to

reach a point where analysis of an additional unit added in the production line could be done

through marginal costing mechanism.

Absorption costing: This technique is used in evaluation of inventory. It considers cost

of materials, labour, fixed and variable overheads. It is considered as full costing technique. The

biggest benefit associated with this method is that it is GAAP compliant and Is required for

preparing financial statements and valuation of stocks. It helps in determination of selling price

of the products. (Göx, R.F., 2000)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation- As per the above solved numerical, it has been analysed that both income

statements are showing different amount of profits. Like by absorption costing method the net

profit is of 79000 and 83000 for November and December month. while in marginal costing it is

of 61000 and 101000 . There is difference in the net profit because in absorption costing method,

the net profit is calculated by considering fixed and variable cost as unit cost. On the other hand

in marginal costing only variable cost is taken as unit cost.

TASK 3

P4. Planning tools for budgetary control

Budgetary control: Budget preparation is the first task for a financial year of the business but

the next part which has to be taken care of is controlling the movement of budget. It is the

departmental tendencies to misbehave with the budgets which disrupts the overall organisational

fund structure (Kung, F.H., Huang, C.L. and Cheng, C.L., 2013). To safeguard from such ulterior

events, Budget control is necessary. It could be achieved with the help of devising tools and

techniques offered by management accounting literature in the form of budgets. An

amalgamation of series of budgets helps a business in planning well for the future through

playing on the characteristics of various budgets. Some prominent budgets used by Oshodi PLC

to tackle the budgetary control are as follows:

Budget: A budget is statutory financial statement which comprises of income and

expenditure of the future activities. It is a fund allocation process under which funds are

allocated to each department for their respective activities for a budgeted period to work as per

the budgeted figures. It also suggests the motives of the business for the future along with targets

to be achieved for the coming years. It gives a scope to the business which has to be followed by

the business ardently. The management is supposed to be compliant with the budget because the

variations would result in disruption of budget. It has following advantages and disadvantages:

statements are showing different amount of profits. Like by absorption costing method the net

profit is of 79000 and 83000 for November and December month. while in marginal costing it is

of 61000 and 101000 . There is difference in the net profit because in absorption costing method,

the net profit is calculated by considering fixed and variable cost as unit cost. On the other hand

in marginal costing only variable cost is taken as unit cost.

TASK 3

P4. Planning tools for budgetary control

Budgetary control: Budget preparation is the first task for a financial year of the business but

the next part which has to be taken care of is controlling the movement of budget. It is the

departmental tendencies to misbehave with the budgets which disrupts the overall organisational

fund structure (Kung, F.H., Huang, C.L. and Cheng, C.L., 2013). To safeguard from such ulterior

events, Budget control is necessary. It could be achieved with the help of devising tools and

techniques offered by management accounting literature in the form of budgets. An

amalgamation of series of budgets helps a business in planning well for the future through

playing on the characteristics of various budgets. Some prominent budgets used by Oshodi PLC

to tackle the budgetary control are as follows:

Budget: A budget is statutory financial statement which comprises of income and

expenditure of the future activities. It is a fund allocation process under which funds are

allocated to each department for their respective activities for a budgeted period to work as per

the budgeted figures. It also suggests the motives of the business for the future along with targets

to be achieved for the coming years. It gives a scope to the business which has to be followed by

the business ardently. The management is supposed to be compliant with the budget because the

variations would result in disruption of budget. It has following advantages and disadvantages:

Advantages- It is beneficial for managing income and expenditure of companies for a

particular time period because of future estimation.

Disadvantage- This is not suitable for small organisations because they can not afford the

expenditure of budget preparation.

Zero base budget: It is a budget which is prepared by zeroing down the previous

budgets and creating a new budget for each new session from scratch. As the budget eliminates

the previous values and allocates new budget solely on the importance of tasks and departmental

performances this budgeting technique has become quite famous among the businesses around

the globe. This technique is very beneficial for cost saving and reduces the chances of unwanted

wastage of money (Pyhrr, P.A., 2012). Under this technique all expenses incurred should be

justified by the departmental managers during the period.

Advantages

This method increases the accuracy of the business by keeping a check on each

department's performance and through creating a sense of accountability within them for

the expenses incurred.

This budget ensures that no money gets wasted owing to the hands of managers who have

ulterior motives and manipulates budgets to receive extra funds.

Disadvantages

This method is time consuming process which consumes a lot of time resources and

human staff tom prepare the budget. Such constraints leads to bureaucracy in the

business.

Sometimes it is very difficult for departments to justify their expenditures as they are in

the form of intangible nature like research and development, marketing, advertising etc.,

the outcomes of these activities is hard to be justified.

Flexible budget: As the name suggests, this type of budget is widely used in modern

context where the level of activities could not be same throughout the year. This budget varies

with the variation in the level of performances. This budget considers variable cost per rate

instead of a fixed rate per unit (Van der Stede, W.A., 2001). The allocation of budget depends on

the variability of the tasks. This budget adjust according to variance levels in the performances.

particular time period because of future estimation.

Disadvantage- This is not suitable for small organisations because they can not afford the

expenditure of budget preparation.

Zero base budget: It is a budget which is prepared by zeroing down the previous

budgets and creating a new budget for each new session from scratch. As the budget eliminates

the previous values and allocates new budget solely on the importance of tasks and departmental

performances this budgeting technique has become quite famous among the businesses around

the globe. This technique is very beneficial for cost saving and reduces the chances of unwanted

wastage of money (Pyhrr, P.A., 2012). Under this technique all expenses incurred should be

justified by the departmental managers during the period.

Advantages

This method increases the accuracy of the business by keeping a check on each

department's performance and through creating a sense of accountability within them for

the expenses incurred.

This budget ensures that no money gets wasted owing to the hands of managers who have

ulterior motives and manipulates budgets to receive extra funds.

Disadvantages

This method is time consuming process which consumes a lot of time resources and

human staff tom prepare the budget. Such constraints leads to bureaucracy in the

business.

Sometimes it is very difficult for departments to justify their expenditures as they are in

the form of intangible nature like research and development, marketing, advertising etc.,

the outcomes of these activities is hard to be justified.

Flexible budget: As the name suggests, this type of budget is widely used in modern

context where the level of activities could not be same throughout the year. This budget varies

with the variation in the level of performances. This budget considers variable cost per rate

instead of a fixed rate per unit (Van der Stede, W.A., 2001). The allocation of budget depends on

the variability of the tasks. This budget adjust according to variance levels in the performances.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.