Analysis of Management Accounting Techniques for Qbic Hotel's Success

VerifiedAdded on 2021/02/21

|23

|5512

|40

Report

AI Summary

This report examines the role of management accounting (MA) in decision-making, focusing on Qbic Hotel. It explores MA tools such as job costing, cost accounting, inventory accounting, and price optimization systems. The report assesses the use of managerial reporting, including budget reports, job cost reports, and accounts receivable aging reports, for effective decision-making. Furthermore, it provides a detailed comparison of marginal costing and absorption costing methods, calculating income statements under both approaches. The report also analyzes the advantages and disadvantages of planning tools used in budgetary control and compares how different organizations adapt MA to address financial challenges. The conclusion emphasizes how MA techniques contribute to sustainable business success and how planning tools suitably respond to financial problems. The report emphasizes the importance of MA in helping businesses achieve goals and gain a competitive advantage.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION .....................................................................................................................3

LO1.............................................................................................................................................3

P1 Explaining management accounting along with their essential requirements ................3

P2 Assessing the use of managerial reporting in decision making .......................................5

LO 2........................................................................................................................................6

P 3 Calculation of Income statement under Marginal costing and Absorption costing

method....................................................................................................................................6

LO 3..........................................................................................................................................12

P 4 Advantages and Disadvantages of planning tools used by budgetary control...............12

LO 4..........................................................................................................................................14

Comparison between different organizations regarding how they are adapting management

accounting for dealing with their financial problems...........................................................14

Managerial accounting leads business enterprises towards sustainable success..................15

Evaluation of how planning tools for accounting respond suitably for solving Financial

problems to lead organizations to sustainable success.........................................................16

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................18

INTRODUCTION .....................................................................................................................3

LO1.............................................................................................................................................3

P1 Explaining management accounting along with their essential requirements ................3

P2 Assessing the use of managerial reporting in decision making .......................................5

LO 2........................................................................................................................................6

P 3 Calculation of Income statement under Marginal costing and Absorption costing

method....................................................................................................................................6

LO 3..........................................................................................................................................12

P 4 Advantages and Disadvantages of planning tools used by budgetary control...............12

LO 4..........................................................................................................................................14

Comparison between different organizations regarding how they are adapting management

accounting for dealing with their financial problems...........................................................14

Managerial accounting leads business enterprises towards sustainable success..................15

Evaluation of how planning tools for accounting respond suitably for solving Financial

problems to lead organizations to sustainable success.........................................................16

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................18

INTRODUCTION

In the context of business, management accounting (MA) plays a significant role in

decision making. Now, managers lay focus on tracking business performance with the motive

to develop suitable or competent strategic framework. This in turn helps firm in attaining

goals and gaining competitive position over others. The present report is based on Qbic hotel

which offers accommodation services to the customers. In this, report will provide deeper

insight about MA tools which business units undertake for reporting purpose. Besides this, it

will shed light on the manner in which MA report aid in profitable decision making. It also

depicts the use of costing system namely absorption and marginal in the assessment of cost

and profitability aspects. Report also presents MA tools that can be used by Qbic for planning

purpose. It also entails how MA techniques assist in responding financial problems.

LO1

P1 Explaining management accounting along with their essential requirements

Management accounting may be defined as a process which lay focus on analyzing

business cost and operations for preparing internal financial report.

“Management accounting is the discipline which deals with the gathering, sorting, and

processing of financial, and non- financial information in order to produce reports that add

value to the business, and provide insight to the managers who make decisions based on these

reports aiming to concrete the organization’s strategic steering”. This provides managers with

suitable framework for decision making and contributes in goal attainment (Cowton, 2018).

There are several management accounting systems which Qbic can undertake for ensuring

smooth functioning of operations from both monetary and non-monetary perspective such as:

Job costing

In MA, this system is highly important which emphasizes on capturing or tracking

cost associated with each task. It presents cost of material, labor and overhead associated with

production aspect. Thus, by summing up all the expenditures total cost of job can be

identified. By dividing total costs from number of units, CPU can be assessed prominently.

Advantages Disadvantages

Offers detailed information about Expensive and time consuming

In the context of business, management accounting (MA) plays a significant role in

decision making. Now, managers lay focus on tracking business performance with the motive

to develop suitable or competent strategic framework. This in turn helps firm in attaining

goals and gaining competitive position over others. The present report is based on Qbic hotel

which offers accommodation services to the customers. In this, report will provide deeper

insight about MA tools which business units undertake for reporting purpose. Besides this, it

will shed light on the manner in which MA report aid in profitable decision making. It also

depicts the use of costing system namely absorption and marginal in the assessment of cost

and profitability aspects. Report also presents MA tools that can be used by Qbic for planning

purpose. It also entails how MA techniques assist in responding financial problems.

LO1

P1 Explaining management accounting along with their essential requirements

Management accounting may be defined as a process which lay focus on analyzing

business cost and operations for preparing internal financial report.

“Management accounting is the discipline which deals with the gathering, sorting, and

processing of financial, and non- financial information in order to produce reports that add

value to the business, and provide insight to the managers who make decisions based on these

reports aiming to concrete the organization’s strategic steering”. This provides managers with

suitable framework for decision making and contributes in goal attainment (Cowton, 2018).

There are several management accounting systems which Qbic can undertake for ensuring

smooth functioning of operations from both monetary and non-monetary perspective such as:

Job costing

In MA, this system is highly important which emphasizes on capturing or tracking

cost associated with each task. It presents cost of material, labor and overhead associated with

production aspect. Thus, by summing up all the expenditures total cost of job can be

identified. By dividing total costs from number of units, CPU can be assessed prominently.

Advantages Disadvantages

Offers detailed information about Expensive and time consuming

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost regarding material, labor and

overhead

Profitability of job can be gauged

using this system

Prevents duplication of work

Helps in evaluating quality of work

(Job costing: advantages and

disadvantages, 2019)

exercise

Lack of standardized process

Cost accounting

This system of MA may be served as a framework which firm’s undertake with the

motive to make appropriate estimation about product price and performing profitability

analysis. Cost accounting system includes fixed, variable, direct and indirect expenditure

incurred by the firm. Profit attainment is the main motive of an organization for the purpose

of survival and gaining competitive position. In this regard, using such system charge per unit

can be assessed by the manager of Qbic using this accounting system. Hence, by adding

profit margin in per unit charge manager of Qbic can set price for the products or services

offered.

Advantages Disadvantages

Assist in identifying cost per unit

and price

Facilitates better monitoring and

controlling of labor costs

Ensures profit maximization by

eliminating waste, losses and

inefficiencies (Cost accounting:

advantages and disadvantages,

2019)

Leads problem in relation to under

or over absorption of overhead

Focuses on past performance,

whereas management is concerned

about future

Imposes more expense due to high

maintenance associated with the

installation of cost accounting

system

Inventory accounting

This system of MA includes several tools which help in taking appropriate decision

about stock such as LIFO, FIFO, economic order quantity (EOQ), just in time (JIT) etc. In the

context of business unit, effectual inventory management is highly required for controlling

cost and enhancing profitability aspect (de Campos and Rodrigues, 2016). Thus, Qbic should

employ EOQ which clearly entails stock that need to be maintained within the firm for

meeting customer’s requirements. By using this tool firm can avoid unnecessary cost

associated with holding and ordering aspects.

overhead

Profitability of job can be gauged

using this system

Prevents duplication of work

Helps in evaluating quality of work

(Job costing: advantages and

disadvantages, 2019)

exercise

Lack of standardized process

Cost accounting

This system of MA may be served as a framework which firm’s undertake with the

motive to make appropriate estimation about product price and performing profitability

analysis. Cost accounting system includes fixed, variable, direct and indirect expenditure

incurred by the firm. Profit attainment is the main motive of an organization for the purpose

of survival and gaining competitive position. In this regard, using such system charge per unit

can be assessed by the manager of Qbic using this accounting system. Hence, by adding

profit margin in per unit charge manager of Qbic can set price for the products or services

offered.

Advantages Disadvantages

Assist in identifying cost per unit

and price

Facilitates better monitoring and

controlling of labor costs

Ensures profit maximization by

eliminating waste, losses and

inefficiencies (Cost accounting:

advantages and disadvantages,

2019)

Leads problem in relation to under

or over absorption of overhead

Focuses on past performance,

whereas management is concerned

about future

Imposes more expense due to high

maintenance associated with the

installation of cost accounting

system

Inventory accounting

This system of MA includes several tools which help in taking appropriate decision

about stock such as LIFO, FIFO, economic order quantity (EOQ), just in time (JIT) etc. In the

context of business unit, effectual inventory management is highly required for controlling

cost and enhancing profitability aspect (de Campos and Rodrigues, 2016). Thus, Qbic should

employ EOQ which clearly entails stock that need to be maintained within the firm for

meeting customer’s requirements. By using this tool firm can avoid unnecessary cost

associated with holding and ordering aspects.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages Disadvantages

Helps in reducing cost and

improving profitability

Ensures better stock management

Time consuming exercise

Requires detailed assessment

Price optimization system

This system or software enables Qbic to evaluate customer’s responses at different

price level pertaining to the services offered. By this, manager of Qbic can set suitable price

of the services and thereby would become able to attract large number of customers. Hence,

such system of MA helps in setting competent pricing framework and thereby ensures

competitive advantage (Malina, 2018).

Advantages Disadvantages

Facilitates price fixation

Helps in building and sustaining

competitive position

Imposes cost in front of company

regarding maintenance, training &

development of personnel

Requires highly skilled personnel for

such mathematical analysis

P2 Assessing the use of managerial reporting in decision making

Managerial reports include budget, job cost, accounts receivable aging, inventory etc

which provides information about departmental performance. In the recent times, managerial

reports are highly significant from the perspective of decision making in relation to trim cost,

rewarding best performing employees as well as resources. There are several managerial

reports which can be undertaken by Qbic for the purpose of decision making such as:

Budget report: Manager can make assessment of departmental performance using this

report. Moreover, it clearly exhibits deviations which take place in departmental

performance. Hence, considering this report manager can assess reasons behind deviations

and thereby would become able to take corrective measures on time (de Campos and

Rodrigues, 2016). In other words, budget report helps Qbic in making appropriate estimation

about income & expenses pertaining to proposed budget. Further, with the help of such report

manager can provide employees with suitable incentives. Through this, training &

development need of personnel can also be assessed.

Job cost report: This report provides high level of assistance to the manager in

evaluating profitability. In this, actually generated revenue is compared in against to the

Helps in reducing cost and

improving profitability

Ensures better stock management

Time consuming exercise

Requires detailed assessment

Price optimization system

This system or software enables Qbic to evaluate customer’s responses at different

price level pertaining to the services offered. By this, manager of Qbic can set suitable price

of the services and thereby would become able to attract large number of customers. Hence,

such system of MA helps in setting competent pricing framework and thereby ensures

competitive advantage (Malina, 2018).

Advantages Disadvantages

Facilitates price fixation

Helps in building and sustaining

competitive position

Imposes cost in front of company

regarding maintenance, training &

development of personnel

Requires highly skilled personnel for

such mathematical analysis

P2 Assessing the use of managerial reporting in decision making

Managerial reports include budget, job cost, accounts receivable aging, inventory etc

which provides information about departmental performance. In the recent times, managerial

reports are highly significant from the perspective of decision making in relation to trim cost,

rewarding best performing employees as well as resources. There are several managerial

reports which can be undertaken by Qbic for the purpose of decision making such as:

Budget report: Manager can make assessment of departmental performance using this

report. Moreover, it clearly exhibits deviations which take place in departmental

performance. Hence, considering this report manager can assess reasons behind deviations

and thereby would become able to take corrective measures on time (de Campos and

Rodrigues, 2016). In other words, budget report helps Qbic in making appropriate estimation

about income & expenses pertaining to proposed budget. Further, with the help of such report

manager can provide employees with suitable incentives. Through this, training &

development need of personnel can also be assessed.

Job cost report: This report provides high level of assistance to the manager in

evaluating profitability. In this, actually generated revenue is compared in against to the

actual one. By this, manager of can Qbic identify areas where resources should be used

instead of wasting time and money on low or unprofitable projects.

Inventory report: Manager of Qbic can make manufacturing process more efficient

by using stock report. Moreover, such report provides information stock wastage, hourly

labor and overhead cost etc. Thus, referring this, different assembly lines can be compared

effectually and best performing departments identified (Managerial accounting reports,

2019).

Accounts receivable aging report: By taking into account this report hotel unit can

manage its cash flow more effectually. Moreover, such report gives clear indication to the

firm that whether credit should be extended to the customers or not. It clearly highlights

customer balances and thereby helps in assessing amount they owed. Through this, manager

of hotel unit can track days within which debtors are making payment. By using this

company can find out problems exist in cash collection process. In the case of high defaults,

firm should tighten its credit policies. Referring all the aspects it can be stated that account

receivable aging report helps in assessing or evaluating company’s debt level.

LO 2

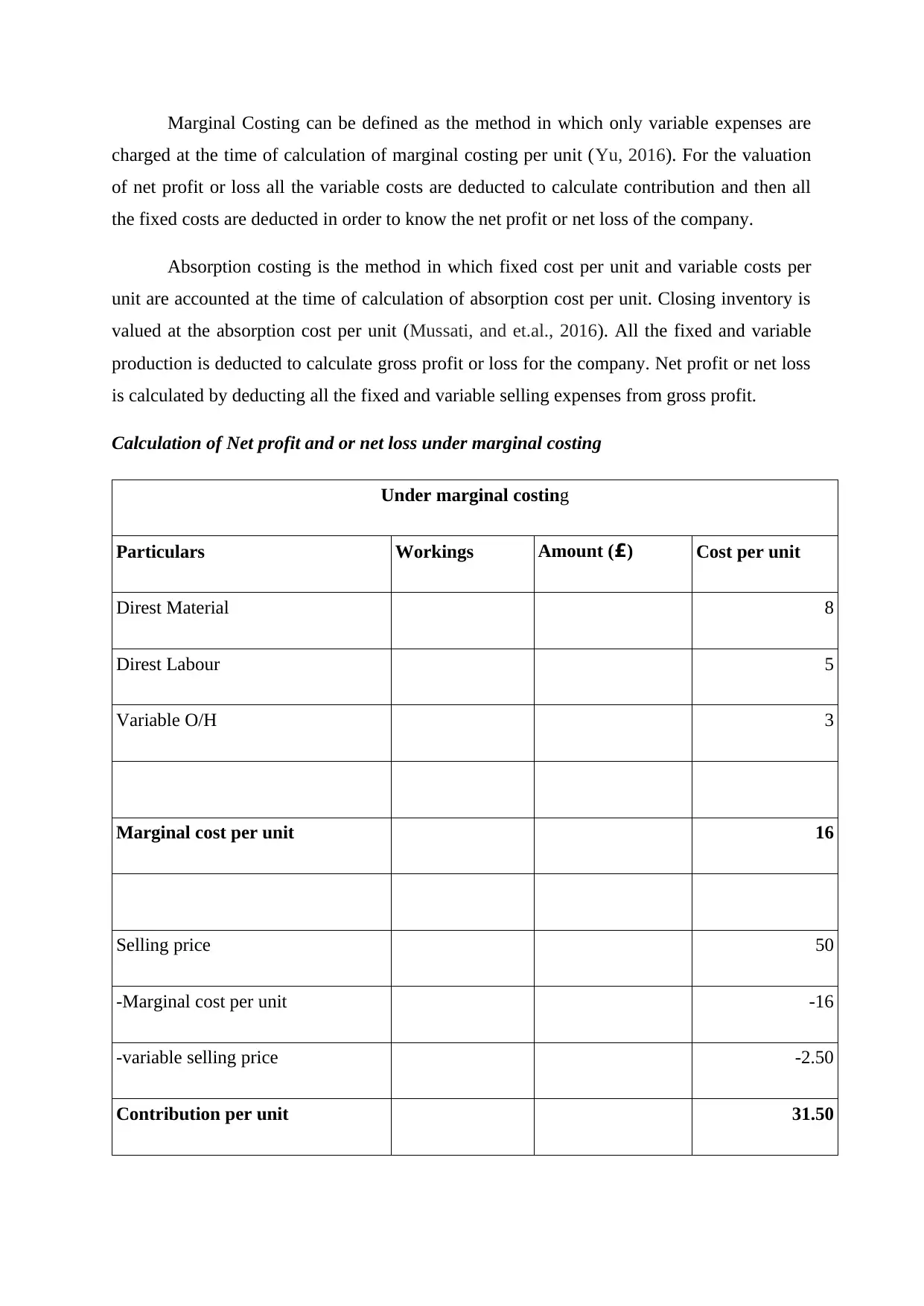

P 3 Calculation of Income statement under Marginal costing and Absorption costing method

Cost can be defined as the total expenses incurred by the company in order to know

the cost incurred in the production of goods. The cost consists of various expenses such as

raw material cost, labor cost and overheads cost (Pearce, 2016). Cost analysis relationship is

defined as the relation between cost of input by company and output of goods.

On the basis of level of activity cost can be divided in two parts i.e. Fixed cost and

variable cost. Fixed cost remains at every level of activity in the company and does not

change with the change in the level of activity (Nas, 2016). Variable costs are defined as the

change in the variable costs with the change in the level of activity in the company. Normal

costing can be defined as the actual cost occurred in the company at the time of production of

goods. Standard costing is the method of setting up set targets by the management in order to

achieve those budgets and then compare with the actual cost of the company.

Meaning of Marginal costing and Absorption costing

instead of wasting time and money on low or unprofitable projects.

Inventory report: Manager of Qbic can make manufacturing process more efficient

by using stock report. Moreover, such report provides information stock wastage, hourly

labor and overhead cost etc. Thus, referring this, different assembly lines can be compared

effectually and best performing departments identified (Managerial accounting reports,

2019).

Accounts receivable aging report: By taking into account this report hotel unit can

manage its cash flow more effectually. Moreover, such report gives clear indication to the

firm that whether credit should be extended to the customers or not. It clearly highlights

customer balances and thereby helps in assessing amount they owed. Through this, manager

of hotel unit can track days within which debtors are making payment. By using this

company can find out problems exist in cash collection process. In the case of high defaults,

firm should tighten its credit policies. Referring all the aspects it can be stated that account

receivable aging report helps in assessing or evaluating company’s debt level.

LO 2

P 3 Calculation of Income statement under Marginal costing and Absorption costing method

Cost can be defined as the total expenses incurred by the company in order to know

the cost incurred in the production of goods. The cost consists of various expenses such as

raw material cost, labor cost and overheads cost (Pearce, 2016). Cost analysis relationship is

defined as the relation between cost of input by company and output of goods.

On the basis of level of activity cost can be divided in two parts i.e. Fixed cost and

variable cost. Fixed cost remains at every level of activity in the company and does not

change with the change in the level of activity (Nas, 2016). Variable costs are defined as the

change in the variable costs with the change in the level of activity in the company. Normal

costing can be defined as the actual cost occurred in the company at the time of production of

goods. Standard costing is the method of setting up set targets by the management in order to

achieve those budgets and then compare with the actual cost of the company.

Meaning of Marginal costing and Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal Costing can be defined as the method in which only variable expenses are

charged at the time of calculation of marginal costing per unit (Yu, 2016). For the valuation

of net profit or loss all the variable costs are deducted to calculate contribution and then all

the fixed costs are deducted in order to know the net profit or net loss of the company.

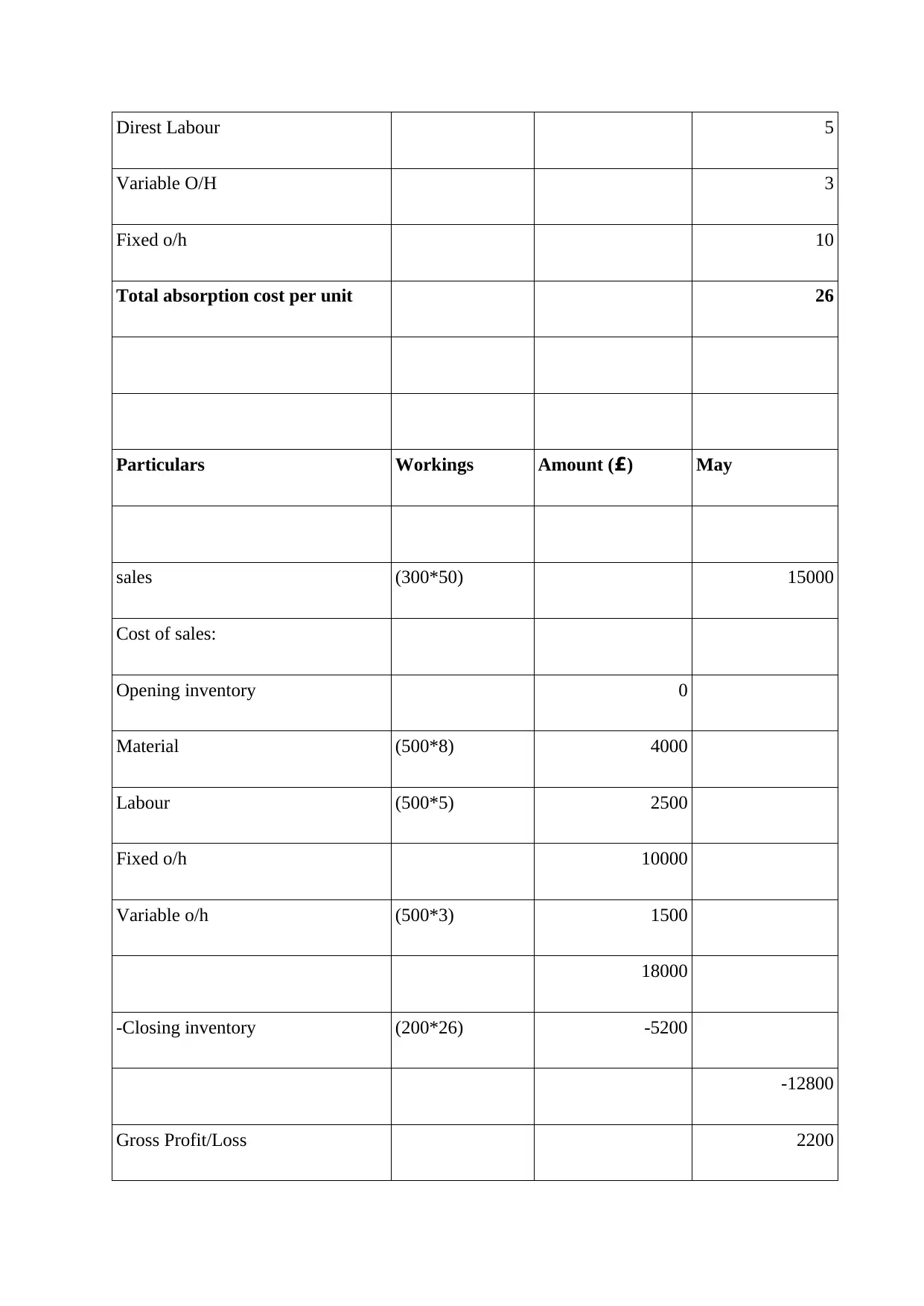

Absorption costing is the method in which fixed cost per unit and variable costs per

unit are accounted at the time of calculation of absorption cost per unit. Closing inventory is

valued at the absorption cost per unit (Mussati, and et.al., 2016). All the fixed and variable

production is deducted to calculate gross profit or loss for the company. Net profit or net loss

is calculated by deducting all the fixed and variable selling expenses from gross profit.

Calculation of Net profit and or net loss under marginal costing

Under marginal costing

Particulars Workings Amount (£) Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

charged at the time of calculation of marginal costing per unit (Yu, 2016). For the valuation

of net profit or loss all the variable costs are deducted to calculate contribution and then all

the fixed costs are deducted in order to know the net profit or net loss of the company.

Absorption costing is the method in which fixed cost per unit and variable costs per

unit are accounted at the time of calculation of absorption cost per unit. Closing inventory is

valued at the absorption cost per unit (Mussati, and et.al., 2016). All the fixed and variable

production is deducted to calculate gross profit or loss for the company. Net profit or net loss

is calculated by deducting all the fixed and variable selling expenses from gross profit.

Calculation of Net profit and or net loss under marginal costing

Under marginal costing

Particulars Workings Amount (£) Cost per unit

Direst Material 8

Direst Labour 5

Variable O/H 3

Marginal cost per unit 16

Selling price 50

-Marginal cost per unit -16

-variable selling price -2.50

Contribution per unit 31.50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

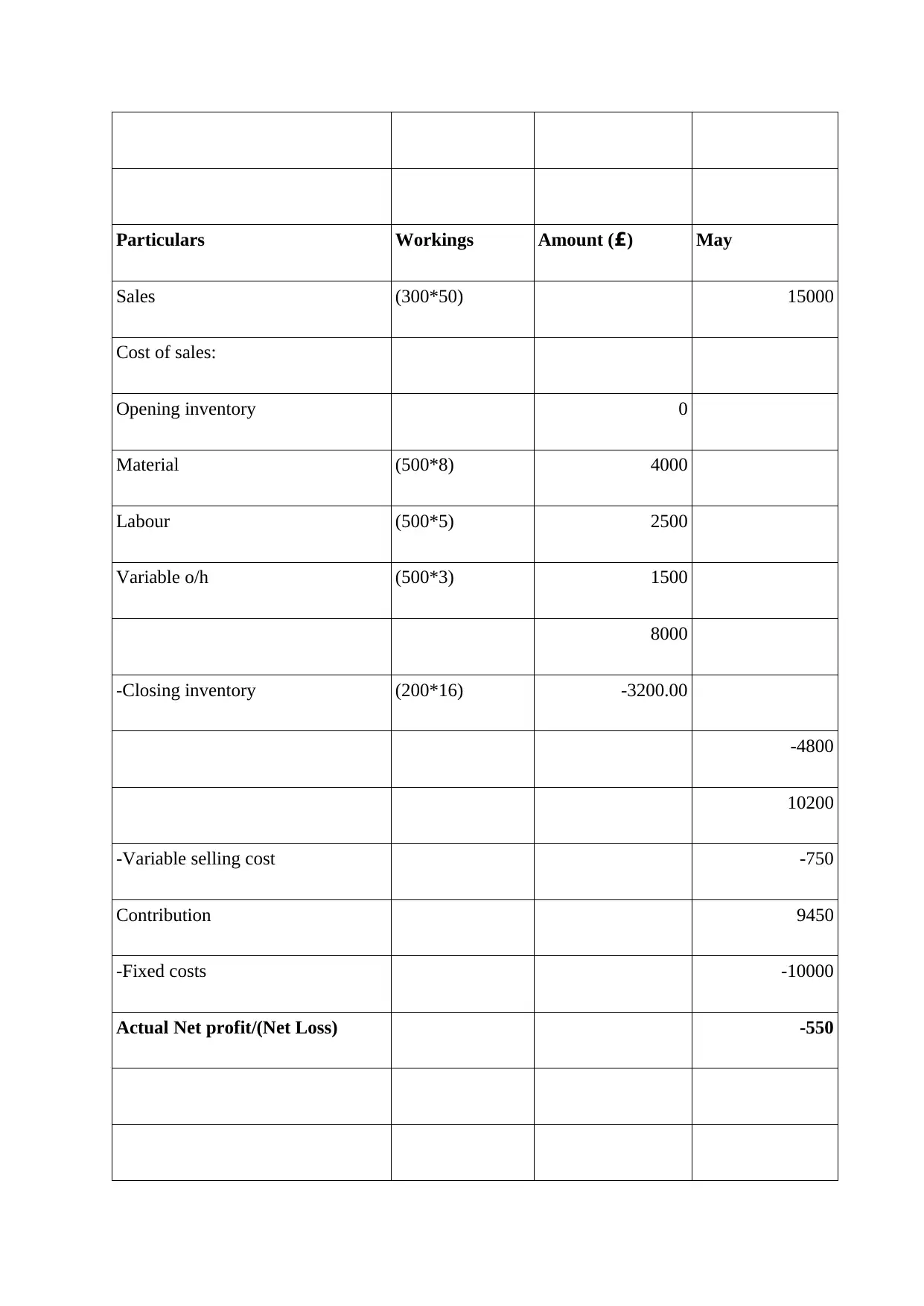

Particulars Workings Amount (£) May

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

Sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Variable o/h (500*3) 1500

8000

-Closing inventory (200*16) -3200.00

-4800

10200

-Variable selling cost -750

Contribution 9450

-Fixed costs -10000

Actual Net profit/(Net Loss) -550

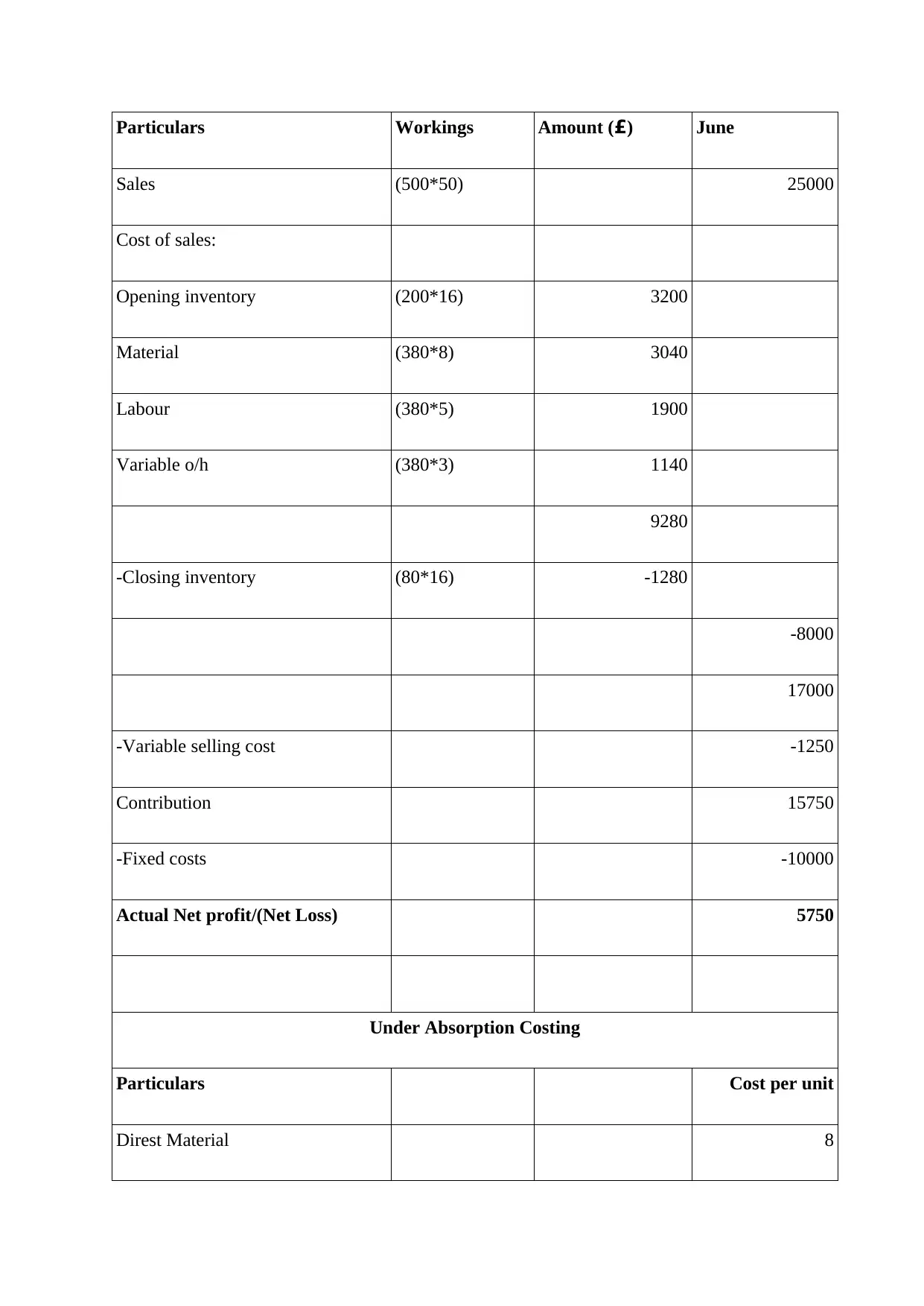

Particulars Workings Amount (£) June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Particulars Cost per unit

Direst Material 8

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*16) 3200

Material (380*8) 3040

Labour (380*5) 1900

Variable o/h (380*3) 1140

9280

-Closing inventory (80*16) -1280

-8000

17000

-Variable selling cost -1250

Contribution 15750

-Fixed costs -10000

Actual Net profit/(Net Loss) 5750

Under Absorption Costing

Particulars Cost per unit

Direst Material 8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direst Labour 5

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

Particulars Workings Amount (£) May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

Variable O/H 3

Fixed o/h 10

Total absorption cost per unit 26

Particulars Workings Amount (£) May

sales (300*50) 15000

Cost of sales:

Opening inventory 0

Material (500*8) 4000

Labour (500*5) 2500

Fixed o/h 10000

Variable o/h (500*3) 1500

18000

-Closing inventory (200*26) -5200

-12800

Gross Profit/Loss 2200

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

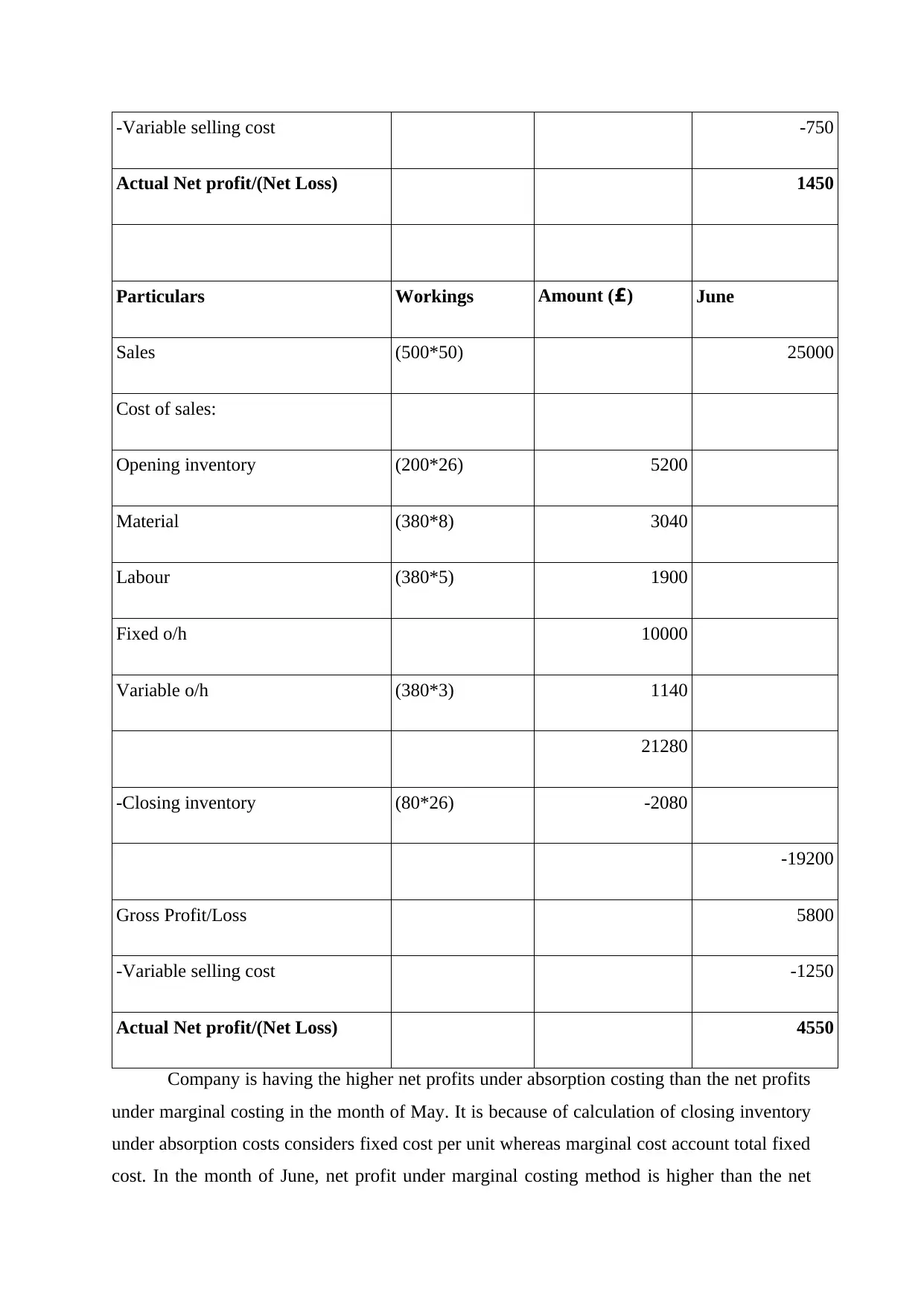

-Variable selling cost -750

Actual Net profit/(Net Loss) 1450

Particulars Workings Amount (£) June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Company is having the higher net profits under absorption costing than the net profits

under marginal costing in the month of May. It is because of calculation of closing inventory

under absorption costs considers fixed cost per unit whereas marginal cost account total fixed

cost. In the month of June, net profit under marginal costing method is higher than the net

Actual Net profit/(Net Loss) 1450

Particulars Workings Amount (£) June

Sales (500*50) 25000

Cost of sales:

Opening inventory (200*26) 5200

Material (380*8) 3040

Labour (380*5) 1900

Fixed o/h 10000

Variable o/h (380*3) 1140

21280

-Closing inventory (80*26) -2080

-19200

Gross Profit/Loss 5800

-Variable selling cost -1250

Actual Net profit/(Net Loss) 4550

Company is having the higher net profits under absorption costing than the net profits

under marginal costing in the month of May. It is because of calculation of closing inventory

under absorption costs considers fixed cost per unit whereas marginal cost account total fixed

cost. In the month of June, net profit under marginal costing method is higher than the net

profit under absorption costing. It is because of low closing inventory which leads to lower

costs under marginal cost and higher profits.

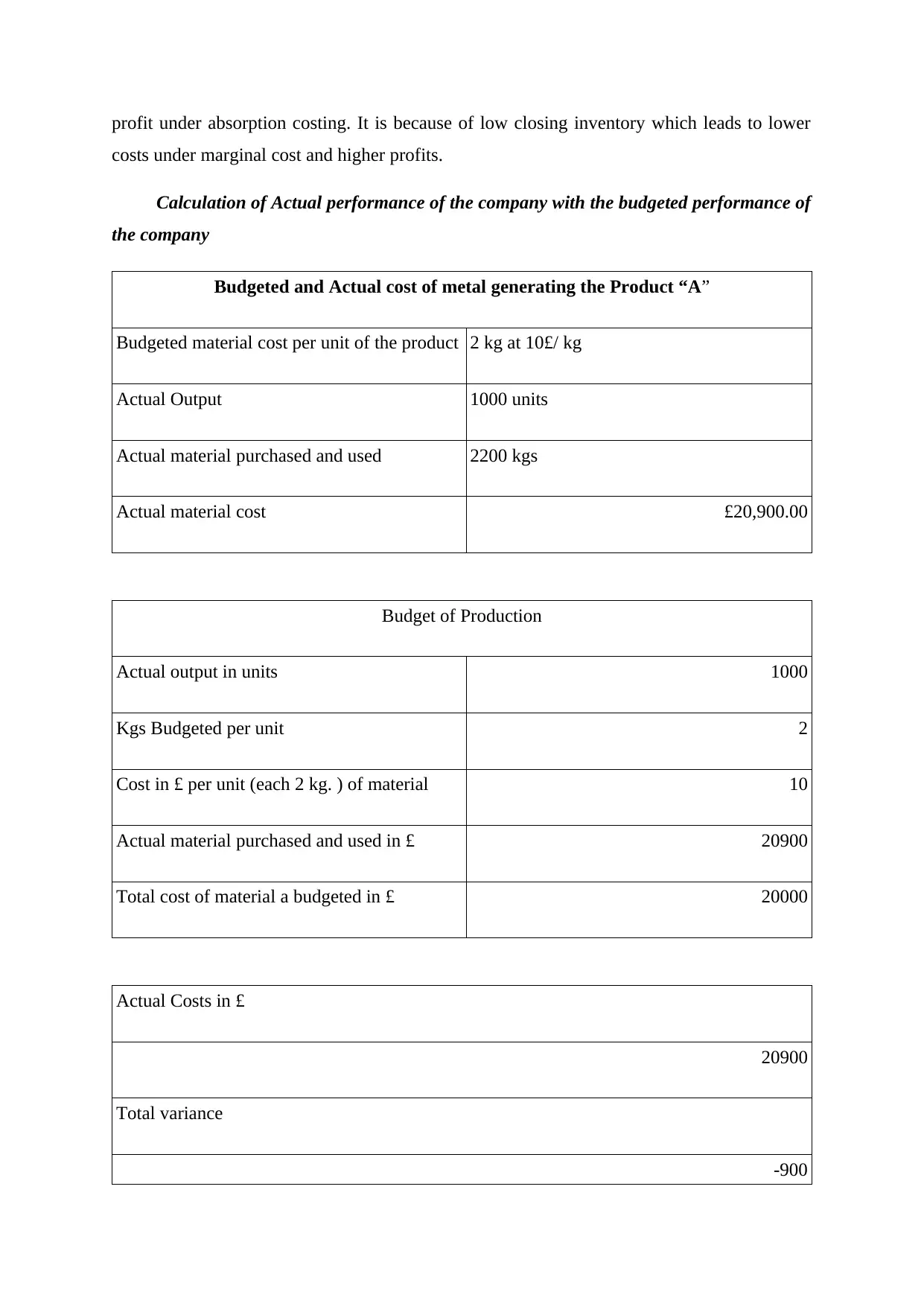

Calculation of Actual performance of the company with the budgeted performance of

the company

Budgeted and Actual cost of metal generating the Product “A”

Budgeted material cost per unit of the product 2 kg at 10£/ kg

Actual Output 1000 units

Actual material purchased and used 2200 kgs

Actual material cost £20,900.00

Budget of Production

Actual output in units 1000

Kgs Budgeted per unit 2

Cost in £ per unit (each 2 kg. ) of material 10

Actual material purchased and used in £ 20900

Total cost of material a budgeted in £ 20000

Actual Costs in £

20900

Total variance

-900

costs under marginal cost and higher profits.

Calculation of Actual performance of the company with the budgeted performance of

the company

Budgeted and Actual cost of metal generating the Product “A”

Budgeted material cost per unit of the product 2 kg at 10£/ kg

Actual Output 1000 units

Actual material purchased and used 2200 kgs

Actual material cost £20,900.00

Budget of Production

Actual output in units 1000

Kgs Budgeted per unit 2

Cost in £ per unit (each 2 kg. ) of material 10

Actual material purchased and used in £ 20900

Total cost of material a budgeted in £ 20000

Actual Costs in £

20900

Total variance

-900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.