Management Accounting Systems for Financial Analysis

VerifiedAdded on 2021/02/20

|17

|5463

|140

Report

AI Summary

This report provides a detailed analysis of management accounting principles and their application within LM Engineering Ltd., a manufacturing company. It explores various management accounting systems, including cost accounting, inventory management, and price optimization, highlighting their benefits. The report examines different methods used for management accounting reporting, such as budget reports, inventory reports, and performance reports. It delves into cost accounting techniques for preparing income statements, including absorption and marginal costing. Furthermore, it analyzes the advantages and disadvantages of planning tools used for budgetary control and compares organizational approaches to solving financial problems using management accounting systems. The report concludes with a discussion on the role of management accounting in responding to financial problems and ensuring sustainable success.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems...........................................................................................1

P2. Explain different methods used for management accounting reporting..........................3

M1 Evaluation of benefits of various management accounting systems...............................4

D1 Management accounting reporting and management accounting system that is related with

organisation process...............................................................................................................5

TASK 2............................................................................................................................................5

P3: Cost accounting techniques to prepare an income statement...........................................5

M2. Management accounting techniques that is used to prepare financial reporting documents

................................................................................................................................................8

D2 Financial reports that interpret data for different types of business activity....................8

TASK 3............................................................................................................................................8

P4 Advantages and Disadvantage of planning tools that are used for budgetary control .....8

M3 Analyse of different planning tools and their application in organisation to prepare and

forecast budget......................................................................................................................10

TASK 4..........................................................................................................................................11

P5 Comparison of organisation to solve the financial problem with the help of management

accounting system................................................................................................................11

M4 Responding to financial problems and management accounting to sustainable success13

D3 Planning tools of accounting period for responding financial problems appropriately. 13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems...........................................................................................1

P2. Explain different methods used for management accounting reporting..........................3

M1 Evaluation of benefits of various management accounting systems...............................4

D1 Management accounting reporting and management accounting system that is related with

organisation process...............................................................................................................5

TASK 2............................................................................................................................................5

P3: Cost accounting techniques to prepare an income statement...........................................5

M2. Management accounting techniques that is used to prepare financial reporting documents

................................................................................................................................................8

D2 Financial reports that interpret data for different types of business activity....................8

TASK 3............................................................................................................................................8

P4 Advantages and Disadvantage of planning tools that are used for budgetary control .....8

M3 Analyse of different planning tools and their application in organisation to prepare and

forecast budget......................................................................................................................10

TASK 4..........................................................................................................................................11

P5 Comparison of organisation to solve the financial problem with the help of management

accounting system................................................................................................................11

M4 Responding to financial problems and management accounting to sustainable success13

D3 Planning tools of accounting period for responding financial problems appropriately. 13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is used by business to analyse their internal financial reports and

statistical information. Preparation of this reports will help the business in their decision making

process. It can also be termed as the process of collecting, interpreting and summarising all the

financial and non financial data. To understand the concept of management accounting in

broader sense, the chosen association in this project is LM engineering Ltd. which is the largest

manufacturing company it deals in manufacturing for both, commercial and domestic market.

LM engineering Ltd. Manufacturer is the foremost manufacturer of glue mixer, doctor roll glue,

mortar glue mixer and plywood machinery. The company has built trust among their customers

(Jamil, and et. al., 2015). In this assignment the company has focused on the certain areas that

are various techniques of management accounting, different tools of planning used in

management accounting in order to enhance their business. Here, company also looks into the

matter of total production cost, cost per units, sales cost and profit and loss statements of the

business so that the amount of profitability can be determined. Apart from this, at last the

company has focused on the role of management accounting in solving the issues and financial

problems of the business.

TASK 1

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.

To monitor the financial condition, every business is required to record their financial as

well as non financial data. Management accounting helps the organisation's in determining their

expenses and income (van Helden, and Uddin, 2016). LM engineering Ltd. Is required to

implement this concept of management accounting in their business so that they can evaluate the

performance of their business can predict about the company’s financial condition and status.

This would also help the business in developing the strategies so that they can operate their

operations effectively. These are prepared as per the requirement of the companies for

understanding budgeting, break even charts, products cost analysis, trend charts and forecasting.

For maintaining this the company is required to cover various types of management accounting

which are mentioned below:

1

Management accounting is used by business to analyse their internal financial reports and

statistical information. Preparation of this reports will help the business in their decision making

process. It can also be termed as the process of collecting, interpreting and summarising all the

financial and non financial data. To understand the concept of management accounting in

broader sense, the chosen association in this project is LM engineering Ltd. which is the largest

manufacturing company it deals in manufacturing for both, commercial and domestic market.

LM engineering Ltd. Manufacturer is the foremost manufacturer of glue mixer, doctor roll glue,

mortar glue mixer and plywood machinery. The company has built trust among their customers

(Jamil, and et. al., 2015). In this assignment the company has focused on the certain areas that

are various techniques of management accounting, different tools of planning used in

management accounting in order to enhance their business. Here, company also looks into the

matter of total production cost, cost per units, sales cost and profit and loss statements of the

business so that the amount of profitability can be determined. Apart from this, at last the

company has focused on the role of management accounting in solving the issues and financial

problems of the business.

TASK 1

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems.

To monitor the financial condition, every business is required to record their financial as

well as non financial data. Management accounting helps the organisation's in determining their

expenses and income (van Helden, and Uddin, 2016). LM engineering Ltd. Is required to

implement this concept of management accounting in their business so that they can evaluate the

performance of their business can predict about the company’s financial condition and status.

This would also help the business in developing the strategies so that they can operate their

operations effectively. These are prepared as per the requirement of the companies for

understanding budgeting, break even charts, products cost analysis, trend charts and forecasting.

For maintaining this the company is required to cover various types of management accounting

which are mentioned below:

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system: This concept of management accounting has been designed for

manufacturer so that they can easily track the flow of inventory continuously through the phases

of productions. This would help the business of LM engineering Ltd. in computing the overall

cost of operation separately and will also help them in determining which product is beneficial

and which is not by providing them the exact information of inflow and out flows of inventory.

Company can also use the different type of cost accounting in order to identify the amount of

inventory the firm needs to produce (Shields, 2015). These types are job order costing and

process costing.

Job order costing: This type of cost accounting will help the business of LM engineering

Ltd. In calculating the cost of each job separately and will record all the cost more accurately and

efficiently to facilitate the cost control in the business operations. This will also support the

organisation in evaluating the spoilage and defective products in the process of production so

that they can smoothly compare their actuals with their estimates.

Process costing: This will support the business in calculating the cost of manufacturing

for the each process individually. It would also help LM engineering Ltd. In allocating their

expenses to each process so that they can compute the exact cost.

Inventory management system: To maintain the levels of raw materials, finished goods stock

the organisation uses inventory management system. The company like LM engineering Ltd.

Would used this to balance the level of inventory and to determine how much inventory is

needed exactly by the organisations to carry out their operations smoothly. This would also help

the company in maintaining high efficiency. The company here can also adopt some techniques

in order to maintain their level of inventory these are :

Just in time method : This is the method of controlling inventory which will allow LM

engineering Ltd. To control the level of inventory. As this concept states that no extra amount of

inventory should be produced if it is not required during the production process.

Economic order quantity: This techniques is used by the company to minimise the total

holding cost and ordering cost. (Tappura, and et. al., 2015). This will also help the business in

saving the cost of ordering as this involves producing an inventory at the time only when the

order is placed. Through this the business will be able to place the right amount of inventory that

is required by the business.

2

manufacturer so that they can easily track the flow of inventory continuously through the phases

of productions. This would help the business of LM engineering Ltd. in computing the overall

cost of operation separately and will also help them in determining which product is beneficial

and which is not by providing them the exact information of inflow and out flows of inventory.

Company can also use the different type of cost accounting in order to identify the amount of

inventory the firm needs to produce (Shields, 2015). These types are job order costing and

process costing.

Job order costing: This type of cost accounting will help the business of LM engineering

Ltd. In calculating the cost of each job separately and will record all the cost more accurately and

efficiently to facilitate the cost control in the business operations. This will also support the

organisation in evaluating the spoilage and defective products in the process of production so

that they can smoothly compare their actuals with their estimates.

Process costing: This will support the business in calculating the cost of manufacturing

for the each process individually. It would also help LM engineering Ltd. In allocating their

expenses to each process so that they can compute the exact cost.

Inventory management system: To maintain the levels of raw materials, finished goods stock

the organisation uses inventory management system. The company like LM engineering Ltd.

Would used this to balance the level of inventory and to determine how much inventory is

needed exactly by the organisations to carry out their operations smoothly. This would also help

the company in maintaining high efficiency. The company here can also adopt some techniques

in order to maintain their level of inventory these are :

Just in time method : This is the method of controlling inventory which will allow LM

engineering Ltd. To control the level of inventory. As this concept states that no extra amount of

inventory should be produced if it is not required during the production process.

Economic order quantity: This techniques is used by the company to minimise the total

holding cost and ordering cost. (Tappura, and et. al., 2015). This will also help the business in

saving the cost of ordering as this involves producing an inventory at the time only when the

order is placed. Through this the business will be able to place the right amount of inventory that

is required by the business.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimisation system: These are the type of management accounting system which is used

by the organisation in order to identify the reactions of customer on different prices of products

and services. This would help the business of LM engineering Ltd. In allocating optimised

prices to the products which benefits company as well as their customers. This would also help

the business in their initial pricing, promotional pricing and discount pricing.

Initial pricing: This price optimisation tool works well when the organisation has a

stable base and long lasting life of their services. This would help the organisation in building the

goodwill, recovering the cost and in earning high amount of profitability.

Promotional pricing: This will help the organisation in setting temporary prices of their

services to build large customer base (Quattrone, 2016). This would also help the business of

LM engineering Ltd. in increasing the amount of their cash flow, and will also leads to the

revenue growth of the company.

Discount pricing: This would help the business to sell short term services like insurance,

credit facilities. This would help the business of LM engineering Ltd. in identifying the customer

to whom they should reward and who purchases in bulk, so that their can come up with the

customer loyalty for their business.

P2. Explain different methods used for management accounting reporting.

Every organisation as to prepare their accounting reports in order to compare their actuals

performance with the targeted standard. There are various type of reports which an organisation

need to prepare such as -

Budget report: These are the reports which are prepared primarily to compare the actual

budgets with the estimated ones. It is the blueprint for the organisation's objective (Cuganesan,

Dunford, and Palmer, 2012). This would help LM engineering Ltd. In comparing their

performance with the standard one and would allow them in identifying the amount of expenses

that incurred during a year.

Inventory reports: This is the type of report which is prepared by every organisation in

order to evaluate the level of inventory an organisation holds. This will help LM engineering

Ltd. in determining the current level of inventory available to them and the cost and prices to

maintain that amount of stock in the organisation so that they can achieve their targets.

Cost managerial accounting report : This report is prepared to know the cost of amount

spent on manufacturing the product. It provides full detail about the money invested in carrying

3

by the organisation in order to identify the reactions of customer on different prices of products

and services. This would help the business of LM engineering Ltd. In allocating optimised

prices to the products which benefits company as well as their customers. This would also help

the business in their initial pricing, promotional pricing and discount pricing.

Initial pricing: This price optimisation tool works well when the organisation has a

stable base and long lasting life of their services. This would help the organisation in building the

goodwill, recovering the cost and in earning high amount of profitability.

Promotional pricing: This will help the organisation in setting temporary prices of their

services to build large customer base (Quattrone, 2016). This would also help the business of

LM engineering Ltd. in increasing the amount of their cash flow, and will also leads to the

revenue growth of the company.

Discount pricing: This would help the business to sell short term services like insurance,

credit facilities. This would help the business of LM engineering Ltd. in identifying the customer

to whom they should reward and who purchases in bulk, so that their can come up with the

customer loyalty for their business.

P2. Explain different methods used for management accounting reporting.

Every organisation as to prepare their accounting reports in order to compare their actuals

performance with the targeted standard. There are various type of reports which an organisation

need to prepare such as -

Budget report: These are the reports which are prepared primarily to compare the actual

budgets with the estimated ones. It is the blueprint for the organisation's objective (Cuganesan,

Dunford, and Palmer, 2012). This would help LM engineering Ltd. In comparing their

performance with the standard one and would allow them in identifying the amount of expenses

that incurred during a year.

Inventory reports: This is the type of report which is prepared by every organisation in

order to evaluate the level of inventory an organisation holds. This will help LM engineering

Ltd. in determining the current level of inventory available to them and the cost and prices to

maintain that amount of stock in the organisation so that they can achieve their targets.

Cost managerial accounting report : This report is prepared to know the cost of amount

spent on manufacturing the product. It provides full detail about the money invested in carrying

3

out business operations. LM engineering LTD. needs to prepared this, to control the cost which

unnecessarily affects the profitability of the business and to understand the exact expenditure of

the organisations so that the optimization of resources can be done properly.

Performance report: This report is prepared to evaluate, analyse, and in identifying the

performance level of organisation as well as employee's. It is design to measure the performance

of something (Caglio, and Ditillo, 2012). LM engineering Ltd. Will use this type of management

accounting reports to measure the performance of their employees and organisations and to

compare it with the standard one so that they can analyse the difference and keeps on improving

it to achieve the efficiency in the performance of the organisation.

Account receivable ageing reports- Account Receivables are the expected payments

due from the customers. Accounts receivable ageing report is a list of customers of the

organization that provides necessary informations about sum of amount due from the customers,

due dates for receipts, over due receivables' dates, interest on due amount, contact details of

debtors, bad-debt and other important details regarding payments from the customers of selected

organization . The management of respective firm LM engineering Ltd. prepares accounts

receivable reports on a regular basis so that it can manage records of its debtors and decide the

potency of its credit collection period.

M1 Evaluation of benefits of various management accounting systems

Management accounting provides different benefits to the organisation that is uses by them

to accomplish their desired goals and objectives. In this task some system of management

accounting and its benefits are discussed in the organisation.

Advantage of cost accounting system

This is useful for the management because it helps them to decide the price of product or

service through analysing the cost that is invested y them to complete the process. The another benefit that measure by LM Engineering Limited is to reduce their

production cost by cutting the extra expenses that incurred in their production process.

(Tucker, and Lowe, 2014).

Advantages of inventory management system

This system helps LM Engineering limited to manage their inventory that is required by

them to manufacture their products by utilising their resources in optimum way.

4

unnecessarily affects the profitability of the business and to understand the exact expenditure of

the organisations so that the optimization of resources can be done properly.

Performance report: This report is prepared to evaluate, analyse, and in identifying the

performance level of organisation as well as employee's. It is design to measure the performance

of something (Caglio, and Ditillo, 2012). LM engineering Ltd. Will use this type of management

accounting reports to measure the performance of their employees and organisations and to

compare it with the standard one so that they can analyse the difference and keeps on improving

it to achieve the efficiency in the performance of the organisation.

Account receivable ageing reports- Account Receivables are the expected payments

due from the customers. Accounts receivable ageing report is a list of customers of the

organization that provides necessary informations about sum of amount due from the customers,

due dates for receipts, over due receivables' dates, interest on due amount, contact details of

debtors, bad-debt and other important details regarding payments from the customers of selected

organization . The management of respective firm LM engineering Ltd. prepares accounts

receivable reports on a regular basis so that it can manage records of its debtors and decide the

potency of its credit collection period.

M1 Evaluation of benefits of various management accounting systems

Management accounting provides different benefits to the organisation that is uses by them

to accomplish their desired goals and objectives. In this task some system of management

accounting and its benefits are discussed in the organisation.

Advantage of cost accounting system

This is useful for the management because it helps them to decide the price of product or

service through analysing the cost that is invested y them to complete the process. The another benefit that measure by LM Engineering Limited is to reduce their

production cost by cutting the extra expenses that incurred in their production process.

(Tucker, and Lowe, 2014).

Advantages of inventory management system

This system helps LM Engineering limited to manage their inventory that is required by

them to manufacture their products by utilising their resources in optimum way.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Accurate inventory management system helps an organisation to manage their inventory

position effectively that is useful for making effective decision of the organisation.

D1 Management accounting reporting and management accounting system that is related with

organisation process

LM Engineering limited is integrated their accounting system as well as their reporting

system with each other that assist their financial department to make accurate decision and plans

to achieve their desired goals and objectives. Example- In order to maintain the financial records

management of LM Engineering Limited makes effective reports which generates long term

profits for the organisation. Like cost accounting system helps them to decide the price of

products in order to ensure their specific profits.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost- The term cost refers to the value or amount that is charged by the organisation for

their products or services from the customer. It includes the price that is invested by them to

produce the goods. This process is required on every stage from operations to functional

department of the organisation.

Absorption costing- This process is defined as the technique that is used to compute the

figure which is invested for manufacturing different products or services. This includes fixed as

well as variable cost for the organisation to enhance the overall productivity of the organisation.

Marginal costing- This method is used by the organisation to calculate the net profits by

including all of its variable cost (Merchant, 2012). Mostly small and medium organisation adopt

this method that show profitability by preparing financial statement of them. LM Engineering

Limited uses this technique in order to identify their current financial position in the market.

Some calculation of LM Engineering limited by using the both method is mention as

below:

Annex (A)

Budget 2019 2020 2021

Cost

Budgeted

production

Basis of

production

Cost

per Hours Cost Hours Cost Hours Cost

5

position effectively that is useful for making effective decision of the organisation.

D1 Management accounting reporting and management accounting system that is related with

organisation process

LM Engineering limited is integrated their accounting system as well as their reporting

system with each other that assist their financial department to make accurate decision and plans

to achieve their desired goals and objectives. Example- In order to maintain the financial records

management of LM Engineering Limited makes effective reports which generates long term

profits for the organisation. Like cost accounting system helps them to decide the price of

products in order to ensure their specific profits.

TASK 2

P3: Cost accounting techniques to prepare an income statement

Cost- The term cost refers to the value or amount that is charged by the organisation for

their products or services from the customer. It includes the price that is invested by them to

produce the goods. This process is required on every stage from operations to functional

department of the organisation.

Absorption costing- This process is defined as the technique that is used to compute the

figure which is invested for manufacturing different products or services. This includes fixed as

well as variable cost for the organisation to enhance the overall productivity of the organisation.

Marginal costing- This method is used by the organisation to calculate the net profits by

including all of its variable cost (Merchant, 2012). Mostly small and medium organisation adopt

this method that show profitability by preparing financial statement of them. LM Engineering

Limited uses this technique in order to identify their current financial position in the market.

Some calculation of LM Engineering limited by using the both method is mention as

below:

Annex (A)

Budget 2019 2020 2021

Cost

Budgeted

production

Basis of

production

Cost

per Hours Cost Hours Cost Hours Cost

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Centre

overhead

costs in £)

(overhead

absorption) Hour

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

6

overhead

costs in £)

(overhead

absorption) Hour

A 66000 22000 3 24200 72600 26620 79860 27500 82500

B 75000 15000 5 16500 82500 18150 90750 19500 97500

C 83600 41800 2 45980 91960 50578

10115

6 51500

10300

0

Annex (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

6

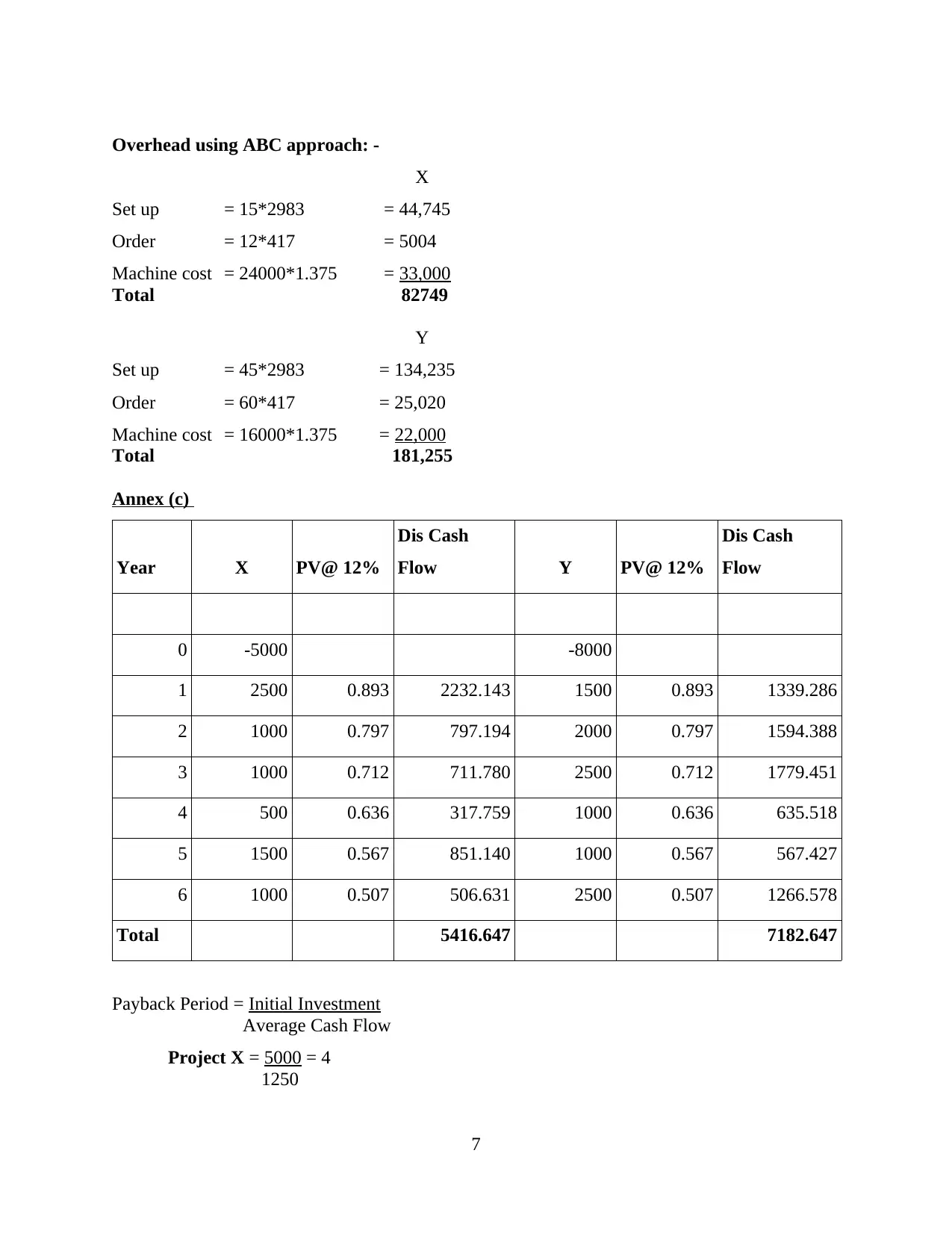

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

7

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Annex (c)

Year X PV@ 12%

Dis Cash

Flow Y PV@ 12%

Dis Cash

Flow

0 -5000 -8000

1 2500 0.893 2232.143 1500 0.893 1339.286

2 1000 0.797 797.194 2000 0.797 1594.388

3 1000 0.712 711.780 2500 0.712 1779.451

4 500 0.636 317.759 1000 0.636 635.518

5 1500 0.567 851.140 1000 0.567 567.427

6 1000 0.507 506.631 2500 0.507 1266.578

Total 5416.647 7182.647

Payback Period = Initial Investment

Average Cash Flow

Project X = 5000 = 4

1250

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

*Average Cash Flow = 7500 = 1250

6

Project Y = 8000 = 4

1750

*Average Cash Flow = 10500 = 1750

6

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

M2. Management accounting techniques that is used to prepare financial reporting documents

Techniques of management accounting plays an essential role to prepare the financial

statement for an organisation (Cooper, Ezzamel, and Qu, 2017). Most of the organisation uses

this technique to formulate an effective framework that considers their financial reports within

appropriate way. In this task LM Engineering limited records all of their financial transaction

that is useful for them to prepare an accurate income statement through use of marginal costing

method.

D2 Financial reports that interpret data for different types of business activity

The above part of the organisation show that project Y required investment more than

the project X. This data undertakes fixed cost that refer to machine cost. Moreover it also

involves variable cost which determine cost of raw-material and other expenses directly impact

on cost. LM Engineering limited prepares financial reports such as cash flow statement, fund

flow statement, balance sheet and profit & loss account to keep records all the financial

transaction that take place while performing their operations. This helps them to evaluate their

current financial position. For performing this management first interpret the data that is useful

for perform various business activities which is invested for each business activity.

8

6

Project Y = 8000 = 4

1750

*Average Cash Flow = 10500 = 1750

6

NPV: -

Project X = Dis Cash Flow – Initial Investment

= 5416.647 – 5000

= £416.647

Project Y = Dis Cash Flow – Initial Investment

= 7182.647 – 8000

= - £817.353

M2. Management accounting techniques that is used to prepare financial reporting documents

Techniques of management accounting plays an essential role to prepare the financial

statement for an organisation (Cooper, Ezzamel, and Qu, 2017). Most of the organisation uses

this technique to formulate an effective framework that considers their financial reports within

appropriate way. In this task LM Engineering limited records all of their financial transaction

that is useful for them to prepare an accurate income statement through use of marginal costing

method.

D2 Financial reports that interpret data for different types of business activity

The above part of the organisation show that project Y required investment more than

the project X. This data undertakes fixed cost that refer to machine cost. Moreover it also

involves variable cost which determine cost of raw-material and other expenses directly impact

on cost. LM Engineering limited prepares financial reports such as cash flow statement, fund

flow statement, balance sheet and profit & loss account to keep records all the financial

transaction that take place while performing their operations. This helps them to evaluate their

current financial position. For performing this management first interpret the data that is useful

for perform various business activities which is invested for each business activity.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 3

P4 Advantages and Disadvantage of planning tools that are used for budgetary control

Planning tools work as effective instrument for the organisation that helps them to

achieve their plan through implementing specific plans for the organisation. Budgetary control is

formulated as written document or booklet that considers the objective which are required to

perform daily operations of the business ( Morales, and Lambert, 2013). The major intention of

budget document is to achieve organisation objective within the specified budget that is decided

by the management. In this task some type of budget along with their advantages and

disadvantage are mention that are executed by the HSBC in order to attain their goals.

Static budget- Budget plays an essential role in the organisation they help them to track

their current financial position. It helps them to analyse their expenses with different alternative

through to enhance their profits. Static budget is always remains similar for the organisation

either there are changes in the volume of their sales or not. With implementation of static budget

an organisation will follow them on regular basis in order to track their actual expenses. Some

advantages and disadvantage of them is mention as follow:

Advantages

The major benefit of formulating static budget is that they are easy to follow and

implement in the organisation because of their stable nature. Static budget allow a company to keep monitoring their regular expenses so if they are

overestimate or underestimate organisation control their variances to follow the budget

effectively (Cadez, and Guilding, 2012).

Disadvantages

Drawback of static budget is that they are not flexible. In a situation if there is increase or

decrease in the sales that organisation does not modify their business resources.

Static budget are based on the data of previous years therefore new organisation face

challenges in order to develop or formulate them.

Zero based budget- Zero based budget of management accounting formulate the budget

that is started from zero. It undertakes several aspects like re-evaluating of cash flow statement in

order to justify all expenses that are incurred by LM engineering limited. Therefore, zero based

budget develops a new method in which they calculate all the actual expenses that take place in

the organisation. Advantages and disadvantage of zero based budgeting:

9

P4 Advantages and Disadvantage of planning tools that are used for budgetary control

Planning tools work as effective instrument for the organisation that helps them to

achieve their plan through implementing specific plans for the organisation. Budgetary control is

formulated as written document or booklet that considers the objective which are required to

perform daily operations of the business ( Morales, and Lambert, 2013). The major intention of

budget document is to achieve organisation objective within the specified budget that is decided

by the management. In this task some type of budget along with their advantages and

disadvantage are mention that are executed by the HSBC in order to attain their goals.

Static budget- Budget plays an essential role in the organisation they help them to track

their current financial position. It helps them to analyse their expenses with different alternative

through to enhance their profits. Static budget is always remains similar for the organisation

either there are changes in the volume of their sales or not. With implementation of static budget

an organisation will follow them on regular basis in order to track their actual expenses. Some

advantages and disadvantage of them is mention as follow:

Advantages

The major benefit of formulating static budget is that they are easy to follow and

implement in the organisation because of their stable nature. Static budget allow a company to keep monitoring their regular expenses so if they are

overestimate or underestimate organisation control their variances to follow the budget

effectively (Cadez, and Guilding, 2012).

Disadvantages

Drawback of static budget is that they are not flexible. In a situation if there is increase or

decrease in the sales that organisation does not modify their business resources.

Static budget are based on the data of previous years therefore new organisation face

challenges in order to develop or formulate them.

Zero based budget- Zero based budget of management accounting formulate the budget

that is started from zero. It undertakes several aspects like re-evaluating of cash flow statement in

order to justify all expenses that are incurred by LM engineering limited. Therefore, zero based

budget develops a new method in which they calculate all the actual expenses that take place in

the organisation. Advantages and disadvantage of zero based budgeting:

9

Advantages

Zero based budget helps an organisation to increase the accuracy in their operations by

justifying, explaining and managing the expenses of the organisation. In helps an organisation to identify different opportunities that generates unnecessary

expenses in their operations. It results that they create more effective results for LM

engineering limited.

Disadvantage

In order to formulate an effective zero based budget management need to invest too much

time. It creates an intensive exercise for the organisation which is complex and hard

method for organisation (Schaltegger, Gibassier, and Zvezdov, 2013).

It is difficult for LM engineering limited to explain their all activities because it requires

trained or experienced employees.

Flexible budget- This types of budget are flexible and adopt changes whenever there is

change in the volume of product sales. Moreover, it is beneficial for organisation because it

develops with the cost that changed with the rate in per unit of their operations. It undertakes all

the aspects that directly impact on budget such as sale of products, purchase of raw-material etc.

therefore, it is easy for LM engineering limited to measure and evaluate the efficiency of their

manager.

Advantages

Flexible budget is beneficial for an organisation as they are easy to develop and modify

them according to the needs of market (Contrafatto, and Burns, 2013). This types of budget modifies themselves as per needs of the functions. So it is easy for

organisation to collect resources that are required to complete their operations.

Disadvantage

Sometimes due to flexible nature of budget different changes in the organisation impact

on their functions. It creates confusion for the management because of regular changes in

their figures.

Flexible budget is not disciplined in nature so for every month there is change in

organisation that develop hindrances to achieve their objective.

10

Zero based budget helps an organisation to increase the accuracy in their operations by

justifying, explaining and managing the expenses of the organisation. In helps an organisation to identify different opportunities that generates unnecessary

expenses in their operations. It results that they create more effective results for LM

engineering limited.

Disadvantage

In order to formulate an effective zero based budget management need to invest too much

time. It creates an intensive exercise for the organisation which is complex and hard

method for organisation (Schaltegger, Gibassier, and Zvezdov, 2013).

It is difficult for LM engineering limited to explain their all activities because it requires

trained or experienced employees.

Flexible budget- This types of budget are flexible and adopt changes whenever there is

change in the volume of product sales. Moreover, it is beneficial for organisation because it

develops with the cost that changed with the rate in per unit of their operations. It undertakes all

the aspects that directly impact on budget such as sale of products, purchase of raw-material etc.

therefore, it is easy for LM engineering limited to measure and evaluate the efficiency of their

manager.

Advantages

Flexible budget is beneficial for an organisation as they are easy to develop and modify

them according to the needs of market (Contrafatto, and Burns, 2013). This types of budget modifies themselves as per needs of the functions. So it is easy for

organisation to collect resources that are required to complete their operations.

Disadvantage

Sometimes due to flexible nature of budget different changes in the organisation impact

on their functions. It creates confusion for the management because of regular changes in

their figures.

Flexible budget is not disciplined in nature so for every month there is change in

organisation that develop hindrances to achieve their objective.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.