Management Accounting Report: Analysis of Continental Clothing Company

VerifiedAdded on 2021/02/19

|20

|4951

|144

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive overview of its principles, types, and applications, with a specific focus on the Continental Clothing Company. The report begins by defining management accounting and its role in internal reporting, differentiating it from financial accounting. It then explores various management accounting systems, including cost accounting, inventory management, job costing, and price optimization, illustrating their benefits and applications within the context of Continental Clothing. The report also examines different methods of management accounting reporting, emphasizing the importance of reliable, accurate, and understandable information. Furthermore, it discusses the integration of management accounting systems with organizational processes, highlighting how these systems support decision-making across different departments. The report concludes with an analysis of the benefits of these systems, providing insights into how Continental Clothing leverages them to improve efficiency, control costs, and optimize pricing strategies. The report is a detailed analysis of management accounting practices and their impact on business operations.

MANAGEMENT

ACCOUNT

ACCOUNT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Part (A)...................................................................................................................................3

Part (B)...................................................................................................................................8

CONCLUSION................................................................................................................................9

TASK 2..........................................................................................................................................10

Part (A).................................................................................................................................10

Part (B).................................................................................................................................12

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

Part (A)...................................................................................................................................3

Part (B)...................................................................................................................................8

CONCLUSION................................................................................................................................9

TASK 2..........................................................................................................................................10

Part (A).................................................................................................................................10

Part (B).................................................................................................................................12

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting may be defined as a kind of accounting that is associated to the

preparation of the internal reports on the basis of monetary and non monetary information of

businesses (Christ, Burritt and Varsei, 2016). Due to help of these reports companies make

maximum use of available resources in an effective manner, this is why because of better internal

management. For better understanding of term management accounting Continental clothing

company Ltd company is selected. This company operates in the manufacture of cloths and

located in London. The project report is categorised into two tasks in which first task includes

different types of management accounting and methods of reporting along with planning tools.

On the other hand, second task contains preparation of income statements by help of marginal

and absorption costing. Apart from it, financial analysis of above respective company is done

whose objective is to provide detailed information to the management.

TASK 1

Part (A)

(A) Management accounting and types.

Management accounting: The term management accounting may be defined as a systematic

process of gathering and managing the available information about quantitative and qualitative

business transactions with an objective to produce internal reports (Jakobsen, 2012). As well as

this accounting is not a mandatory like other accounting. Though its role is wide in the context of

organisations because it acts as a guide for the managers to take futuristic decisions.

Management accounting system- This can be defined as a kind of accounting system which is

related to the preparation of internal reports with the help of available information of financial

and non financial transactions of companies.

Importance to integrate with organisation- It is mandatory for the organisations to align the

management accounting within process. Due to this systems and functions of companies can be

managed and arranged in an effective manner. For example in the above respective, continental

clothing limited company implements this accounting in their operations and activities for

making effective decisions on the basis of internal reports.

Origin, role and principle of management accounting:

Management accounting may be defined as a kind of accounting that is associated to the

preparation of the internal reports on the basis of monetary and non monetary information of

businesses (Christ, Burritt and Varsei, 2016). Due to help of these reports companies make

maximum use of available resources in an effective manner, this is why because of better internal

management. For better understanding of term management accounting Continental clothing

company Ltd company is selected. This company operates in the manufacture of cloths and

located in London. The project report is categorised into two tasks in which first task includes

different types of management accounting and methods of reporting along with planning tools.

On the other hand, second task contains preparation of income statements by help of marginal

and absorption costing. Apart from it, financial analysis of above respective company is done

whose objective is to provide detailed information to the management.

TASK 1

Part (A)

(A) Management accounting and types.

Management accounting: The term management accounting may be defined as a systematic

process of gathering and managing the available information about quantitative and qualitative

business transactions with an objective to produce internal reports (Jakobsen, 2012). As well as

this accounting is not a mandatory like other accounting. Though its role is wide in the context of

organisations because it acts as a guide for the managers to take futuristic decisions.

Management accounting system- This can be defined as a kind of accounting system which is

related to the preparation of internal reports with the help of available information of financial

and non financial transactions of companies.

Importance to integrate with organisation- It is mandatory for the organisations to align the

management accounting within process. Due to this systems and functions of companies can be

managed and arranged in an effective manner. For example in the above respective, continental

clothing limited company implements this accounting in their operations and activities for

making effective decisions on the basis of internal reports.

Origin, role and principle of management accounting:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

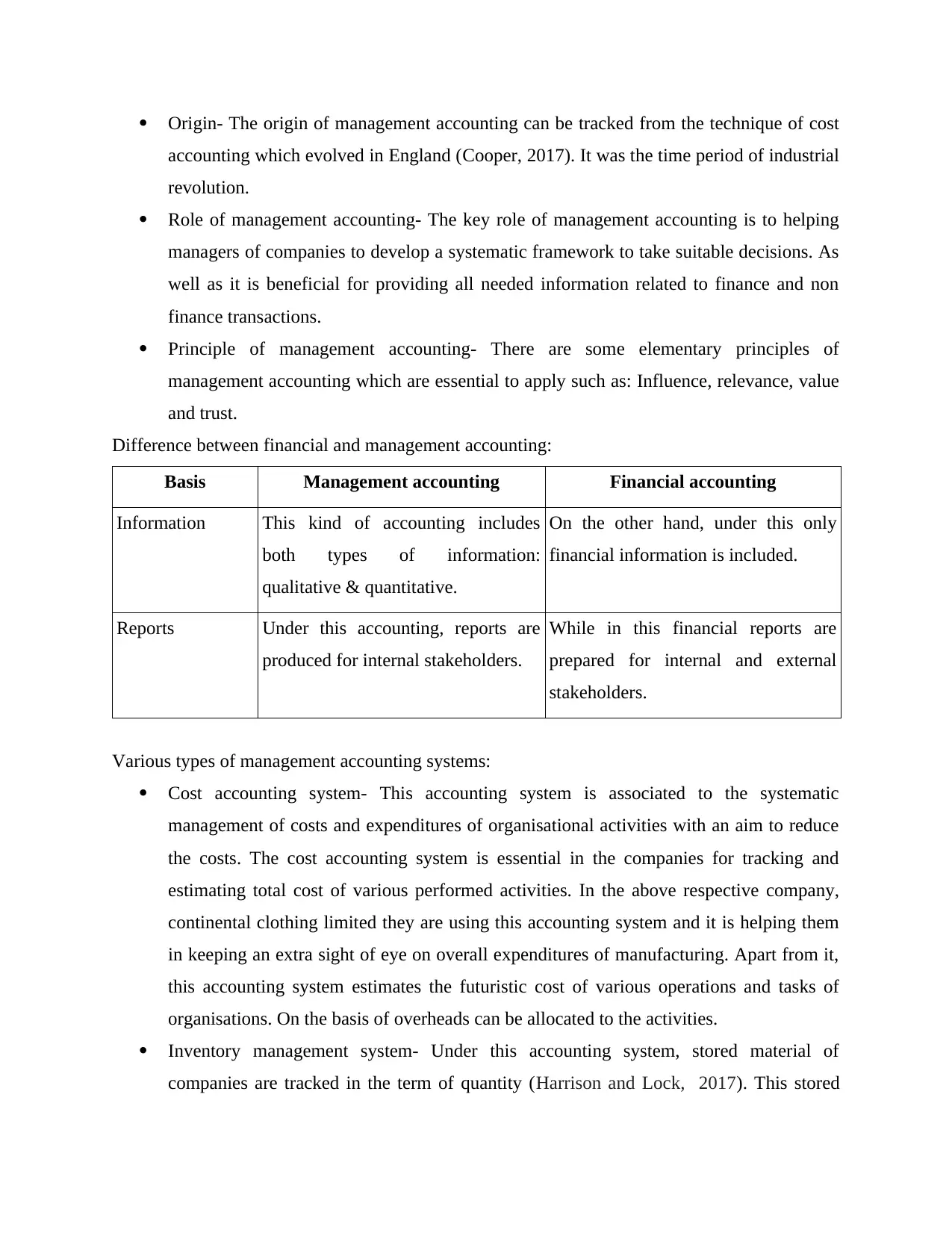

Origin- The origin of management accounting can be tracked from the technique of cost

accounting which evolved in England (Cooper, 2017). It was the time period of industrial

revolution.

Role of management accounting- The key role of management accounting is to helping

managers of companies to develop a systematic framework to take suitable decisions. As

well as it is beneficial for providing all needed information related to finance and non

finance transactions.

Principle of management accounting- There are some elementary principles of

management accounting which are essential to apply such as: Influence, relevance, value

and trust.

Difference between financial and management accounting:

Basis Management accounting Financial accounting

Information This kind of accounting includes

both types of information:

qualitative & quantitative.

On the other hand, under this only

financial information is included.

Reports Under this accounting, reports are

produced for internal stakeholders.

While in this financial reports are

prepared for internal and external

stakeholders.

Various types of management accounting systems:

Cost accounting system- This accounting system is associated to the systematic

management of costs and expenditures of organisational activities with an aim to reduce

the costs. The cost accounting system is essential in the companies for tracking and

estimating total cost of various performed activities. In the above respective company,

continental clothing limited they are using this accounting system and it is helping them

in keeping an extra sight of eye on overall expenditures of manufacturing. Apart from it,

this accounting system estimates the futuristic cost of various operations and tasks of

organisations. On the basis of overheads can be allocated to the activities.

Inventory management system- Under this accounting system, stored material of

companies are tracked in the term of quantity (Harrison and Lock, 2017). This stored

accounting which evolved in England (Cooper, 2017). It was the time period of industrial

revolution.

Role of management accounting- The key role of management accounting is to helping

managers of companies to develop a systematic framework to take suitable decisions. As

well as it is beneficial for providing all needed information related to finance and non

finance transactions.

Principle of management accounting- There are some elementary principles of

management accounting which are essential to apply such as: Influence, relevance, value

and trust.

Difference between financial and management accounting:

Basis Management accounting Financial accounting

Information This kind of accounting includes

both types of information:

qualitative & quantitative.

On the other hand, under this only

financial information is included.

Reports Under this accounting, reports are

produced for internal stakeholders.

While in this financial reports are

prepared for internal and external

stakeholders.

Various types of management accounting systems:

Cost accounting system- This accounting system is associated to the systematic

management of costs and expenditures of organisational activities with an aim to reduce

the costs. The cost accounting system is essential in the companies for tracking and

estimating total cost of various performed activities. In the above respective company,

continental clothing limited they are using this accounting system and it is helping them

in keeping an extra sight of eye on overall expenditures of manufacturing. Apart from it,

this accounting system estimates the futuristic cost of various operations and tasks of

organisations. On the basis of overheads can be allocated to the activities.

Inventory management system- Under this accounting system, stored material of

companies are tracked in the term of quantity (Harrison and Lock, 2017). This stored

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

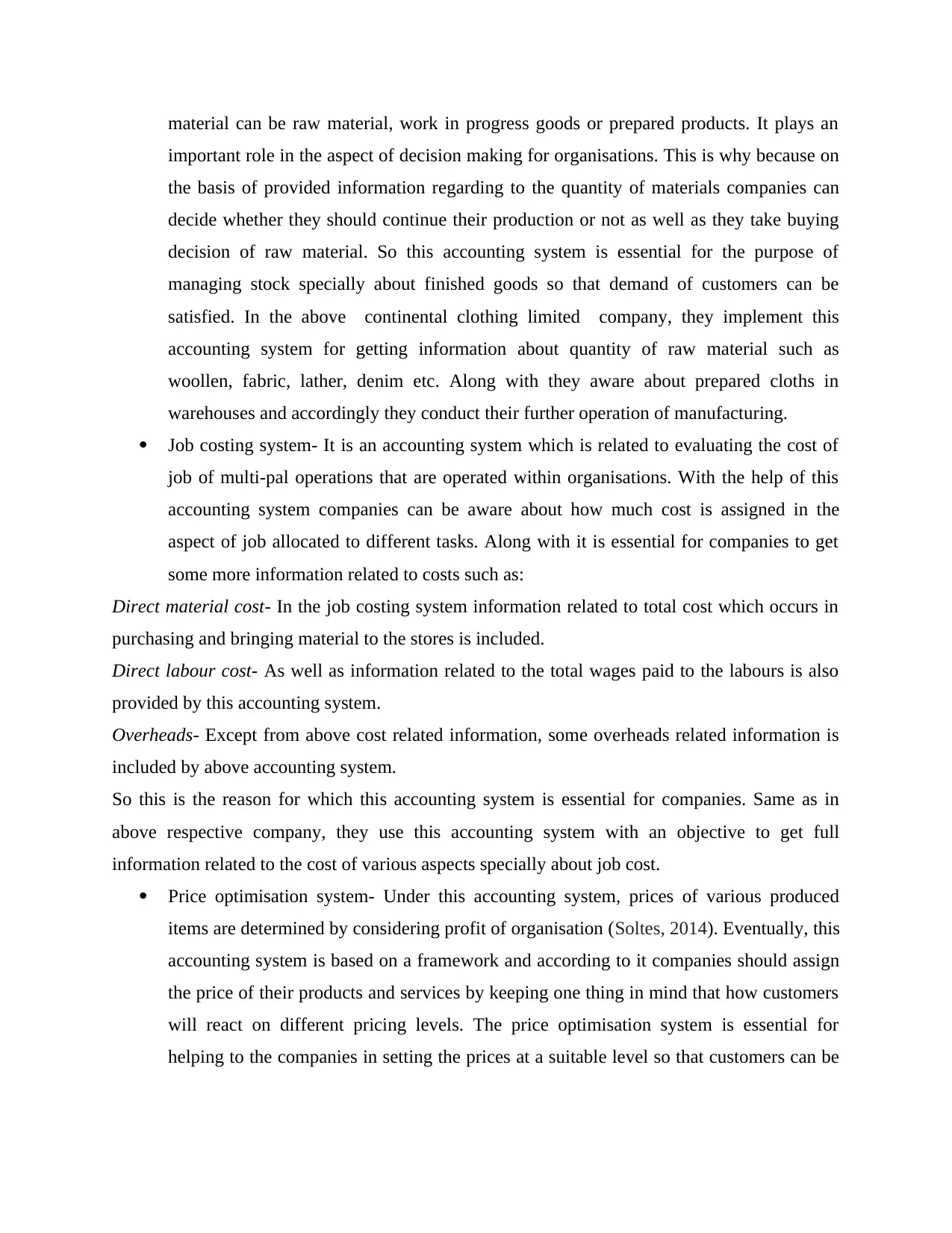

material can be raw material, work in progress goods or prepared products. It plays an

important role in the aspect of decision making for organisations. This is why because on

the basis of provided information regarding to the quantity of materials companies can

decide whether they should continue their production or not as well as they take buying

decision of raw material. So this accounting system is essential for the purpose of

managing stock specially about finished goods so that demand of customers can be

satisfied. In the above continental clothing limited company, they implement this

accounting system for getting information about quantity of raw material such as

woollen, fabric, lather, denim etc. Along with they aware about prepared cloths in

warehouses and accordingly they conduct their further operation of manufacturing.

Job costing system- It is an accounting system which is related to evaluating the cost of

job of multi-pal operations that are operated within organisations. With the help of this

accounting system companies can be aware about how much cost is assigned in the

aspect of job allocated to different tasks. Along with it is essential for companies to get

some more information related to costs such as:

Direct material cost- In the job costing system information related to total cost which occurs in

purchasing and bringing material to the stores is included.

Direct labour cost- As well as information related to the total wages paid to the labours is also

provided by this accounting system.

Overheads- Except from above cost related information, some overheads related information is

included by above accounting system.

So this is the reason for which this accounting system is essential for companies. Same as in

above respective company, they use this accounting system with an objective to get full

information related to the cost of various aspects specially about job cost.

Price optimisation system- Under this accounting system, prices of various produced

items are determined by considering profit of organisation (Soltes, 2014). Eventually, this

accounting system is based on a framework and according to it companies should assign

the price of their products and services by keeping one thing in mind that how customers

will react on different pricing levels. The price optimisation system is essential for

helping to the companies in setting the prices at a suitable level so that customers can be

important role in the aspect of decision making for organisations. This is why because on

the basis of provided information regarding to the quantity of materials companies can

decide whether they should continue their production or not as well as they take buying

decision of raw material. So this accounting system is essential for the purpose of

managing stock specially about finished goods so that demand of customers can be

satisfied. In the above continental clothing limited company, they implement this

accounting system for getting information about quantity of raw material such as

woollen, fabric, lather, denim etc. Along with they aware about prepared cloths in

warehouses and accordingly they conduct their further operation of manufacturing.

Job costing system- It is an accounting system which is related to evaluating the cost of

job of multi-pal operations that are operated within organisations. With the help of this

accounting system companies can be aware about how much cost is assigned in the

aspect of job allocated to different tasks. Along with it is essential for companies to get

some more information related to costs such as:

Direct material cost- In the job costing system information related to total cost which occurs in

purchasing and bringing material to the stores is included.

Direct labour cost- As well as information related to the total wages paid to the labours is also

provided by this accounting system.

Overheads- Except from above cost related information, some overheads related information is

included by above accounting system.

So this is the reason for which this accounting system is essential for companies. Same as in

above respective company, they use this accounting system with an objective to get full

information related to the cost of various aspects specially about job cost.

Price optimisation system- Under this accounting system, prices of various produced

items are determined by considering profit of organisation (Soltes, 2014). Eventually, this

accounting system is based on a framework and according to it companies should assign

the price of their products and services by keeping one thing in mind that how customers

will react on different pricing levels. The price optimisation system is essential for

helping to the companies in setting the prices at a suitable level so that customers can be

satisfied as well as sell can be increase. The continental clothing limited company, sets

their prices at a level which is affordable for a particular customer segment.

(B) Methods of management accounting reporting.

It is essential that information which is becoming a basis of management accounting

reports should consists below mentioned features:

Reliability- As per this feature of accounting information, it is important that all

information should be reliable in accordance to business activities of companies.

Accuracy- The information must be accurate without including any error. This is why

because any error in information can result in wrong preparation of accounting reports.

As well as it may leads to wrong decisions. Up date- In a running business venture, there are a lot of transactions which occur on a

regular basis. Hence it is important that information must be updated so the internal

reports can become more useful.

Role of presenting the information understandable- It is necessary that financial and non

financial information must be simple and easy to understand so that accounting reports can be

made in less time. On the other hand, if accounting information will not be understandable then it

can be difficult to management accountant to produce the accounting reports.

Methods of management accounting reporting- There are wide range of methods of

management accounting reporting and some of these are mentioned below:

Cost accounting report- Under this report a detailed information is included about cost of

various kind of activities such as cost of material, labour etc. As well as with the help of

this report companies can determine about total actual cost and can compare to estimated

cost. Thus it is useful in assessing information regarding to overall cost and expenditure

of multi-pal operations of companies. Same as in the above respective company,

continental clothing limited they make this report whose objective is to minimising the

total cost on the basis of provided information.

Inventory management reports- In this report, information related to the quantity of

available inventories in warehouses as well as cost which is occurring in the process of

storing the stock (Sedevich Fons, 2012). In other words, the inventory management

report contains information about cost of buying the inventories, along with ordering

their prices at a level which is affordable for a particular customer segment.

(B) Methods of management accounting reporting.

It is essential that information which is becoming a basis of management accounting

reports should consists below mentioned features:

Reliability- As per this feature of accounting information, it is important that all

information should be reliable in accordance to business activities of companies.

Accuracy- The information must be accurate without including any error. This is why

because any error in information can result in wrong preparation of accounting reports.

As well as it may leads to wrong decisions. Up date- In a running business venture, there are a lot of transactions which occur on a

regular basis. Hence it is important that information must be updated so the internal

reports can become more useful.

Role of presenting the information understandable- It is necessary that financial and non

financial information must be simple and easy to understand so that accounting reports can be

made in less time. On the other hand, if accounting information will not be understandable then it

can be difficult to management accountant to produce the accounting reports.

Methods of management accounting reporting- There are wide range of methods of

management accounting reporting and some of these are mentioned below:

Cost accounting report- Under this report a detailed information is included about cost of

various kind of activities such as cost of material, labour etc. As well as with the help of

this report companies can determine about total actual cost and can compare to estimated

cost. Thus it is useful in assessing information regarding to overall cost and expenditure

of multi-pal operations of companies. Same as in the above respective company,

continental clothing limited they make this report whose objective is to minimising the

total cost on the basis of provided information.

Inventory management reports- In this report, information related to the quantity of

available inventories in warehouses as well as cost which is occurring in the process of

storing the stock (Sedevich Fons, 2012). In other words, the inventory management

report contains information about cost of buying the inventories, along with ordering

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

cost, hiring cost etc. By preparation of this report companies can aware about quantity of

stored material in warehouses and accordingly they take further decisions. For example in

above respective company, they produce this report with an objective to track the record

of all inventories.

Account receivable ageing report- This is a kind of report which includes information

related to the total debtors which a company has. As well as under it, time period is also

included on which credit transaction is done by companies with buyers. The importance

of this report is that it useful in determining to companies about how much amount they

have in the market which is being paid by debtors. Same as in above continental clothing

limited company, they produce this report which provides them information about how

much debtors crossed the due date to pay the amount. On the basis of it, they charge

interest amount. Their debtors are mostly those customers who acquire their cloths on

credit.

Budget report- This report is based on information about estimated and actual income &

costs (Rieckhof, Bergmann and Guenther, 2015). Along with it provides comparison

between actual income and budgeted income as well as actual costs and budgeted costs.

Due to this companies can assess their actual financial performance and can take

corrective decisions accordingly. For example the continental cloths limited they produce

this report and it helps them in tracking the actual performance of various kind of

business activities.

(C) Benefits and application of management accounting systems in the context of selected

company.

Management accounting

system

Benefits

Cost accounting system The key benefit of this accounting system is that it helps in

estimating future costs as well as minimise total costs. In the

continental clothing limited company, they apply this accounting

system which helps them in keeping the cost of manufacturing

operations below the estimated costs.

stored material in warehouses and accordingly they take further decisions. For example in

above respective company, they produce this report with an objective to track the record

of all inventories.

Account receivable ageing report- This is a kind of report which includes information

related to the total debtors which a company has. As well as under it, time period is also

included on which credit transaction is done by companies with buyers. The importance

of this report is that it useful in determining to companies about how much amount they

have in the market which is being paid by debtors. Same as in above continental clothing

limited company, they produce this report which provides them information about how

much debtors crossed the due date to pay the amount. On the basis of it, they charge

interest amount. Their debtors are mostly those customers who acquire their cloths on

credit.

Budget report- This report is based on information about estimated and actual income &

costs (Rieckhof, Bergmann and Guenther, 2015). Along with it provides comparison

between actual income and budgeted income as well as actual costs and budgeted costs.

Due to this companies can assess their actual financial performance and can take

corrective decisions accordingly. For example the continental cloths limited they produce

this report and it helps them in tracking the actual performance of various kind of

business activities.

(C) Benefits and application of management accounting systems in the context of selected

company.

Management accounting

system

Benefits

Cost accounting system The key benefit of this accounting system is that it helps in

estimating future costs as well as minimise total costs. In the

continental clothing limited company, they apply this accounting

system which helps them in keeping the cost of manufacturing

operations below the estimated costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management

system

This accounting system is useful for tracking the record of

available inventories in stores as well as to minimise the storage

cost. Same as in the above company, this accounting system is

linked with the manufacturing operations and they take further

decisions accordingly about production and purchasing.

Job costing system It is beneficial for managing the cost of job in various activities.

For example in above company, they get the information about

cost of material, labour etc. with the help of this accounting

system.

Price optimisation system It is useful for companies in assigning the prices of manufactured

products. In the continental clothing limited company, they mark

the prices of their manufactured cloths on the basis of this

accounting system by considering customers reaction on different

prices.

(D) Integration of management accounting systems and reporting with organisational process.

The management accounting systems are aligned with the process of companies. This can

be understand by example of above mentioned company (Horton and de Araujo Wanderley,

2018). They are using cost accounting system, job costing system, price optimisation system and

inventory management systems in their operations. Like price optimisation system is linked with

sales department because it helps in setting prices at a level on which sales can be increase. Same

as in the context of accounting reports like cost-accounting reports, inventory management

reports etc. are linked with the process of above mentioned company. This is why because the

cost accounting reports are aligned with the finance department because these reports help in

keeping the cost of operations low. Thus the MA reports and systems are linked to the

organisational process.

Part (B)

Analysis of three planning tools.

system

This accounting system is useful for tracking the record of

available inventories in stores as well as to minimise the storage

cost. Same as in the above company, this accounting system is

linked with the manufacturing operations and they take further

decisions accordingly about production and purchasing.

Job costing system It is beneficial for managing the cost of job in various activities.

For example in above company, they get the information about

cost of material, labour etc. with the help of this accounting

system.

Price optimisation system It is useful for companies in assigning the prices of manufactured

products. In the continental clothing limited company, they mark

the prices of their manufactured cloths on the basis of this

accounting system by considering customers reaction on different

prices.

(D) Integration of management accounting systems and reporting with organisational process.

The management accounting systems are aligned with the process of companies. This can

be understand by example of above mentioned company (Horton and de Araujo Wanderley,

2018). They are using cost accounting system, job costing system, price optimisation system and

inventory management systems in their operations. Like price optimisation system is linked with

sales department because it helps in setting prices at a level on which sales can be increase. Same

as in the context of accounting reports like cost-accounting reports, inventory management

reports etc. are linked with the process of above mentioned company. This is why because the

cost accounting reports are aligned with the finance department because these reports help in

keeping the cost of operations low. Thus the MA reports and systems are linked to the

organisational process.

Part (B)

Analysis of three planning tools.

In the management accounting various kind of planning tools are included and some of

these are mentioned below:

Cash flow budgeting- It can be defined as a kind of budget which is related to providing

the information about cash inflow and outflows for a particular time period. This is also

known by the cash budget because it is linked with the cash flow projection. Like in

above respective company, they make this budget which helps them in determining the

need of cash. It has following advantages and disadvantages:

Advantage- It is beneficial in ignoring the debts because this budget limits the unwanted

expenditures.

Disadvantage- This budgeting consumes too much cost and time during preparation of budgets.

Break even analysis- It can be defined as a kind of analysis which is related to find out

how much units should be sold so that incurred costs can be recovered at a point on

which there is no loss and no profit (Storey, 2014). The continental clothing limited

company, does this analysis to evaluate the point of selling on which their total cost can

be recovered.

Advantage- This analysis is beneficial in taking important decisions by management. As well as

it helps in assessing the units which are needed to be sold to recover the costs.

Disadvantage- Its main disadvantage is that it is based completely on assumptions. Along with it

does not include information about capital employed.

Benchmarking- This is a kind of planning tool which is related to the comparing an

organisation's processes, performance and policies with other companies of same

industries. For example in above company, they compare their plans and policies with

other companies so that they can find out level of difference.

Advantage- It is beneficial for making competitive strategies so that companies can achieve the

advantage over rivalry firms.

Disadvantage- Its disadvantage is related to complacency and arrogance.

CONCLUSION

On the basis of above mentioned project report it has been concluded that MA has its

important role in the aspect of company's management. In report, MAS are concluded such as

cost accounting, job costing, inventory management system etc. which are important for above

these are mentioned below:

Cash flow budgeting- It can be defined as a kind of budget which is related to providing

the information about cash inflow and outflows for a particular time period. This is also

known by the cash budget because it is linked with the cash flow projection. Like in

above respective company, they make this budget which helps them in determining the

need of cash. It has following advantages and disadvantages:

Advantage- It is beneficial in ignoring the debts because this budget limits the unwanted

expenditures.

Disadvantage- This budgeting consumes too much cost and time during preparation of budgets.

Break even analysis- It can be defined as a kind of analysis which is related to find out

how much units should be sold so that incurred costs can be recovered at a point on

which there is no loss and no profit (Storey, 2014). The continental clothing limited

company, does this analysis to evaluate the point of selling on which their total cost can

be recovered.

Advantage- This analysis is beneficial in taking important decisions by management. As well as

it helps in assessing the units which are needed to be sold to recover the costs.

Disadvantage- Its main disadvantage is that it is based completely on assumptions. Along with it

does not include information about capital employed.

Benchmarking- This is a kind of planning tool which is related to the comparing an

organisation's processes, performance and policies with other companies of same

industries. For example in above company, they compare their plans and policies with

other companies so that they can find out level of difference.

Advantage- It is beneficial for making competitive strategies so that companies can achieve the

advantage over rivalry firms.

Disadvantage- Its disadvantage is related to complacency and arrogance.

CONCLUSION

On the basis of above mentioned project report it has been concluded that MA has its

important role in the aspect of company's management. In report, MAS are concluded such as

cost accounting, job costing, inventory management system etc. which are important for above

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. Along with MA reports are also concluded like inventory management report, costing

reports which provide detailed information to managers. Apart from it three planning tools:

benchmarking, cash flow budgeting and break even analysis is mentioned. As well as income

statements are prepared with the use of absorption and marginal costing. In the end, business

memo is produced indicating to the managers of selected company about financial position.

TASK 2.

Part (A)

Cost- It may be defined as an addition of all the expenditures that incurs during the procedure of

completing any task. Eventually, every organisation wants that the cost should be low as much as

possible. For example in continental clothing limited company, they produce cloths and in that

process cost occurs. As well as cost can be categorised into various types such as fixed cost,

variable costs etc.

Cost analysis- This is related to a systematic process of computing total cost of various kind of

activities (Schuster, 2015). The purpose of this analysis is to getting detailed information

regarding to all expenses so that cost be controlled.

Cost volume profit- This can be defined as analysis of difference between the cost and profits.

The aim of this type of analysis is to measuring the financial performance as per the variation in

cost and volume. Same as in above company, they do the cost volume profit analysis to find out

difference in cost and revenues.

Flexible budgeting- It is a kind of budgeting technique that is related to preparation of

budgets which can be change if sales and profits vary from the actual level (Bragg, 2012. ). Same

as in above respective company, they use this budgeting technique for short time period.

Cost variance- In this actual cost is compared by estimated costs so that variation can be

find out. With the use of it, organisations can evaluate about whether their cost of operations and

activities is under control or not. For example in the above company, they conduct this analysis

for finding the variation in costs.

Absorption and marginal costing:

Absorption costing- This is a kind of costing technique which is related to the taking fixed cost

as a period cost and variable cost as a unit cost for preparation of income statements.

reports which provide detailed information to managers. Apart from it three planning tools:

benchmarking, cash flow budgeting and break even analysis is mentioned. As well as income

statements are prepared with the use of absorption and marginal costing. In the end, business

memo is produced indicating to the managers of selected company about financial position.

TASK 2.

Part (A)

Cost- It may be defined as an addition of all the expenditures that incurs during the procedure of

completing any task. Eventually, every organisation wants that the cost should be low as much as

possible. For example in continental clothing limited company, they produce cloths and in that

process cost occurs. As well as cost can be categorised into various types such as fixed cost,

variable costs etc.

Cost analysis- This is related to a systematic process of computing total cost of various kind of

activities (Schuster, 2015). The purpose of this analysis is to getting detailed information

regarding to all expenses so that cost be controlled.

Cost volume profit- This can be defined as analysis of difference between the cost and profits.

The aim of this type of analysis is to measuring the financial performance as per the variation in

cost and volume. Same as in above company, they do the cost volume profit analysis to find out

difference in cost and revenues.

Flexible budgeting- It is a kind of budgeting technique that is related to preparation of

budgets which can be change if sales and profits vary from the actual level (Bragg, 2012. ). Same

as in above respective company, they use this budgeting technique for short time period.

Cost variance- In this actual cost is compared by estimated costs so that variation can be

find out. With the use of it, organisations can evaluate about whether their cost of operations and

activities is under control or not. For example in the above company, they conduct this analysis

for finding the variation in costs.

Absorption and marginal costing:

Absorption costing- This is a kind of costing technique which is related to the taking fixed cost

as a period cost and variable cost as a unit cost for preparation of income statements.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal costing- Under this costing technique fixed and variable costs are taken as a cost of

product (Guthrie, Parker, 2014).

Inventory cost- It can be defined as a kind of cost which is related to the calculating the total

expenditures which occurs during the process of keeping the stock in warehouses.

Valuation method- There are some types of valuation methods for inventories such as:

LIFO- Under this method, those raw materials are being used for production which was

brought last.

FIFO- Under it, raw material which came first in the warehouses is being used first for

production (Mussnig, 2013). Overheads- Under it, various kind of expenses are included that are not associated with

direct material and labour. For example rent, wages etc.

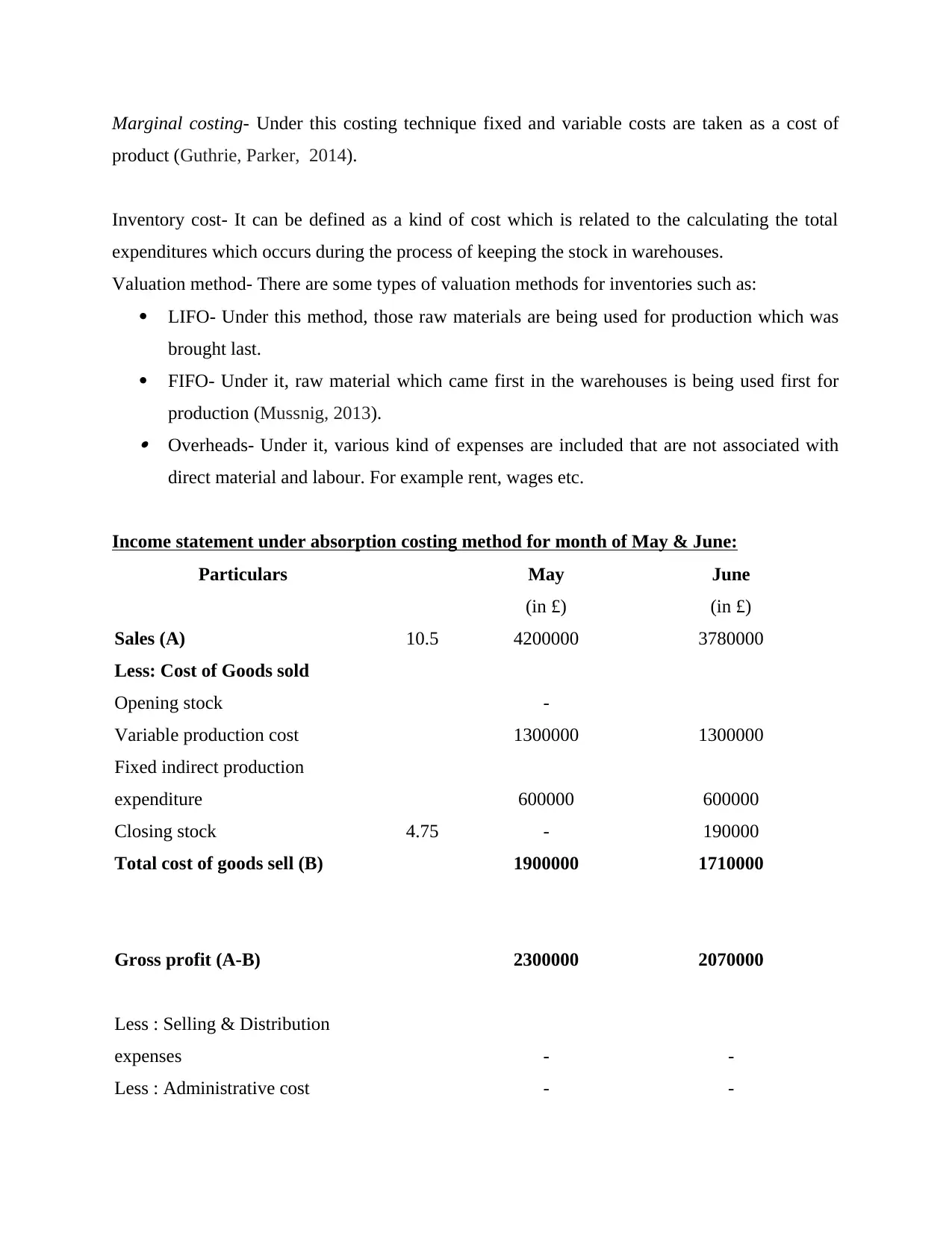

Income statement under absorption costing method for month of May & June:

Particulars May June

(in £) (in £)

Sales (A) 10.5 4200000 3780000

Less: Cost of Goods sold

Opening stock -

Variable production cost 1300000 1300000

Fixed indirect production

expenditure 600000 600000

Closing stock 4.75 - 190000

Total cost of goods sell (B) 1900000 1710000

Gross profit (A-B) 2300000 2070000

Less : Selling & Distribution

expenses - -

Less : Administrative cost - -

product (Guthrie, Parker, 2014).

Inventory cost- It can be defined as a kind of cost which is related to the calculating the total

expenditures which occurs during the process of keeping the stock in warehouses.

Valuation method- There are some types of valuation methods for inventories such as:

LIFO- Under this method, those raw materials are being used for production which was

brought last.

FIFO- Under it, raw material which came first in the warehouses is being used first for

production (Mussnig, 2013). Overheads- Under it, various kind of expenses are included that are not associated with

direct material and labour. For example rent, wages etc.

Income statement under absorption costing method for month of May & June:

Particulars May June

(in £) (in £)

Sales (A) 10.5 4200000 3780000

Less: Cost of Goods sold

Opening stock -

Variable production cost 1300000 1300000

Fixed indirect production

expenditure 600000 600000

Closing stock 4.75 - 190000

Total cost of goods sell (B) 1900000 1710000

Gross profit (A-B) 2300000 2070000

Less : Selling & Distribution

expenses - -

Less : Administrative cost - -

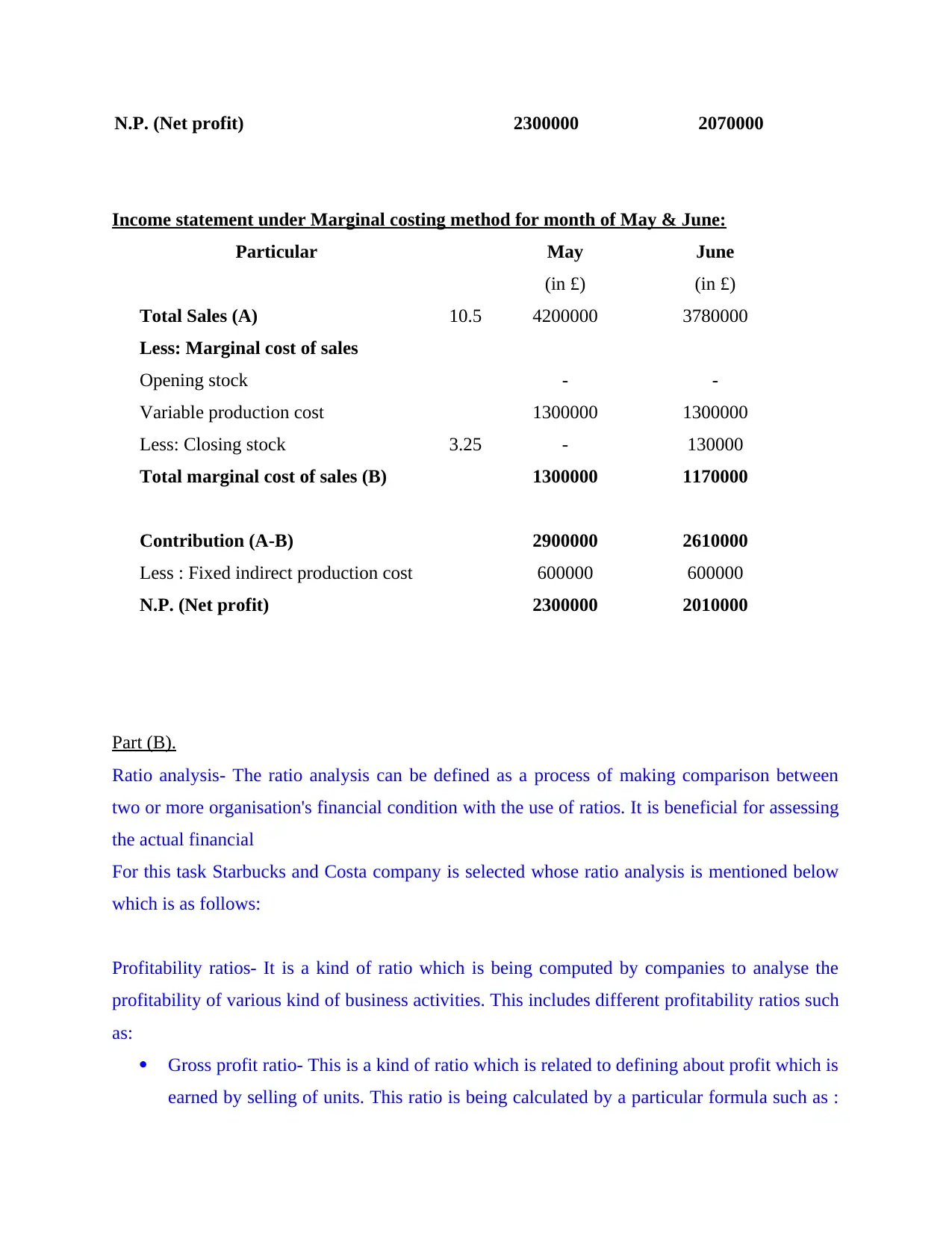

N.P. (Net profit) 2300000 2070000

Income statement under Marginal costing method for month of May & June:

Particular May June

(in £) (in £)

Total Sales (A) 10.5 4200000 3780000

Less: Marginal cost of sales

Opening stock - -

Variable production cost 1300000 1300000

Less: Closing stock 3.25 - 130000

Total marginal cost of sales (B) 1300000 1170000

Contribution (A-B) 2900000 2610000

Less : Fixed indirect production cost 600000 600000

N.P. (Net profit) 2300000 2010000

Part (B).

Ratio analysis- The ratio analysis can be defined as a process of making comparison between

two or more organisation's financial condition with the use of ratios. It is beneficial for assessing

the actual financial

For this task Starbucks and Costa company is selected whose ratio analysis is mentioned below

which is as follows:

Profitability ratios- It is a kind of ratio which is being computed by companies to analyse the

profitability of various kind of business activities. This includes different profitability ratios such

as:

Gross profit ratio- This is a kind of ratio which is related to defining about profit which is

earned by selling of units. This ratio is being calculated by a particular formula such as :

Income statement under Marginal costing method for month of May & June:

Particular May June

(in £) (in £)

Total Sales (A) 10.5 4200000 3780000

Less: Marginal cost of sales

Opening stock - -

Variable production cost 1300000 1300000

Less: Closing stock 3.25 - 130000

Total marginal cost of sales (B) 1300000 1170000

Contribution (A-B) 2900000 2610000

Less : Fixed indirect production cost 600000 600000

N.P. (Net profit) 2300000 2010000

Part (B).

Ratio analysis- The ratio analysis can be defined as a process of making comparison between

two or more organisation's financial condition with the use of ratios. It is beneficial for assessing

the actual financial

For this task Starbucks and Costa company is selected whose ratio analysis is mentioned below

which is as follows:

Profitability ratios- It is a kind of ratio which is being computed by companies to analyse the

profitability of various kind of business activities. This includes different profitability ratios such

as:

Gross profit ratio- This is a kind of ratio which is related to defining about profit which is

earned by selling of units. This ratio is being calculated by a particular formula such as :

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.