Comprehensive Report on Management Accounting Principles at Tesco

VerifiedAdded on 2021/02/19

|14

|2931

|217

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its role within an organization, particularly using Tesco as a case study. It delves into the various types of costs, including direct, indirect, fixed, and variable costs, and their classification based on function and behavior. The report then explores the effectiveness of marginal costing systems, outlining their advantages and disadvantages for businesses. Furthermore, it examines the objectives of budgeting, emphasizing its role in promoting organizational effectiveness through structure, cash flow prediction, resource allocation, performance measurement, and goal communication. The analysis highlights how these accounting tools contribute to decision-making, forecasting, and overall financial management within the retail sector.

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

Role of management accounting in the organization..................................................................3

Section 2...........................................................................................................................................5

Various types of cost in management accounting.......................................................................5

Section 3...........................................................................................................................................7

Effectiveness of marginal accounting system and their pros and cons to the organization........7

Section 4...........................................................................................................................................8

Objectives of budgeting in regard to promote effectiveness.......................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

Section 1...........................................................................................................................................3

Role of management accounting in the organization..................................................................3

Section 2...........................................................................................................................................5

Various types of cost in management accounting.......................................................................5

Section 3...........................................................................................................................................7

Effectiveness of marginal accounting system and their pros and cons to the organization........7

Section 4...........................................................................................................................................8

Objectives of budgeting in regard to promote effectiveness.......................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Accounting is the process of systematically recording, measuring, analysing and

evaluating the accounting data to get the final information for the decision-making and to know

the financial position in the market. The various types of accounting like management

accounting, cost accounting, financial accounting are used for the different purpose. Tesco is 3rd

largest supermarket if UK. It is retail service based goods and services based industry which use

the accounting tools to measure and evaluate the financial position and market share. The report

highlight the role of management accounting in the organization. It helps to explain the various

kind of cost on different basis such on the type direct and indirect cost, on the basis of function

production if non production cost etc. The report also highlight the marginal cost with their

advantages and disadvantages and how the cost affect the effectiveness of the organization. It

also includes the different objectives of preparing budget for the company.

Section 1

Role of management accounting in the organization

Management accounting play an important role in the organization. It provides data to get

the useful information for making decision and improve the efficiency and effectiveness of the

company (Kieso, Weygandt, and Warfield, 2016). The role of management accounting are as

follows :

Forecasting : Forecasting is the process of determining the future situation to take the

current decisions. Management accounting provides various data regarding the company

performance to forecast the future condition. For example the growth of the supermarket of

Tesco in past few month help to forecast the increasing demand of product and services in the

future.

Recording : Management accounting role is to record the financial data to get the useful

information. They record the data in different formats. For example the sales, purchases,

operating expenses are recorded in trading account by the Tesco to get the gross profit of the

organization (Schaltegger, and Burritt, 2017). The all non operating expenses and income are

recorded in income statement to know the net profit of the organization. Tesco record all its

assents and liability in the balance sheet account to get the real debtor and creditor of the

organization or to know the profitability of the company.

3

Accounting is the process of systematically recording, measuring, analysing and

evaluating the accounting data to get the final information for the decision-making and to know

the financial position in the market. The various types of accounting like management

accounting, cost accounting, financial accounting are used for the different purpose. Tesco is 3rd

largest supermarket if UK. It is retail service based goods and services based industry which use

the accounting tools to measure and evaluate the financial position and market share. The report

highlight the role of management accounting in the organization. It helps to explain the various

kind of cost on different basis such on the type direct and indirect cost, on the basis of function

production if non production cost etc. The report also highlight the marginal cost with their

advantages and disadvantages and how the cost affect the effectiveness of the organization. It

also includes the different objectives of preparing budget for the company.

Section 1

Role of management accounting in the organization

Management accounting play an important role in the organization. It provides data to get

the useful information for making decision and improve the efficiency and effectiveness of the

company (Kieso, Weygandt, and Warfield, 2016). The role of management accounting are as

follows :

Forecasting : Forecasting is the process of determining the future situation to take the

current decisions. Management accounting provides various data regarding the company

performance to forecast the future condition. For example the growth of the supermarket of

Tesco in past few month help to forecast the increasing demand of product and services in the

future.

Recording : Management accounting role is to record the financial data to get the useful

information. They record the data in different formats. For example the sales, purchases,

operating expenses are recorded in trading account by the Tesco to get the gross profit of the

organization (Schaltegger, and Burritt, 2017). The all non operating expenses and income are

recorded in income statement to know the net profit of the organization. Tesco record all its

assents and liability in the balance sheet account to get the real debtor and creditor of the

organization or to know the profitability of the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Analysing : Management accounting play a vital role in analysing the financial data.

They use the recorded financial data to analyse the performance of the company that weather the

company is producing the profit of not (Loughran, and McDonald, 2016). Tesco analyse the

performance by considering the different data such as the sales of the month and compare it with

the previous month sale to get the fluctuation and variances in data and find out the reason

behind the variances.

Support decision-making : the role of management accounting is also to support the

decision-making system. It provides information regarding the company performance and give

them different alternative to make decisions (Ahmed, and et.al., 2017). For example the

increasing sales of grocery items reflect that customer is more wiling to buy the grocery items

via online and offline method which help the management to take the decision regarding the

increasing production of grocery items.

Comparison of management accounting and financial accounting

Meaning : the focus of financial accounting is to prepare the financial statement such as

balance sheet, income statement, profit and loss account and cash flow whereas the focus of

management accounting is to use the financial data for making policies, strategies and plan for

the organization.

Information : Financial accounting is mainly provides the monetary information such as

the profit, sales, operating expenses etc. whereas management accounting provides the both

monetary and non monetary information (Difference between the financial accounting and

management accounting, 2019).

Objective : The objective of financial accounting is to provide the information to the

outside users such as suppliers, creditors, customer, government, shareholders etc. whereas the

objective of management accounting is to provide the information to the internal department like

owner, employees and mangers (Butler, and Ghosh, 2015).

Time frame : Financial accounting prepares the financial statement at the end of

accounting period whereas the management accounting prepare the report on the requirement of

data.

4

They use the recorded financial data to analyse the performance of the company that weather the

company is producing the profit of not (Loughran, and McDonald, 2016). Tesco analyse the

performance by considering the different data such as the sales of the month and compare it with

the previous month sale to get the fluctuation and variances in data and find out the reason

behind the variances.

Support decision-making : the role of management accounting is also to support the

decision-making system. It provides information regarding the company performance and give

them different alternative to make decisions (Ahmed, and et.al., 2017). For example the

increasing sales of grocery items reflect that customer is more wiling to buy the grocery items

via online and offline method which help the management to take the decision regarding the

increasing production of grocery items.

Comparison of management accounting and financial accounting

Meaning : the focus of financial accounting is to prepare the financial statement such as

balance sheet, income statement, profit and loss account and cash flow whereas the focus of

management accounting is to use the financial data for making policies, strategies and plan for

the organization.

Information : Financial accounting is mainly provides the monetary information such as

the profit, sales, operating expenses etc. whereas management accounting provides the both

monetary and non monetary information (Difference between the financial accounting and

management accounting, 2019).

Objective : The objective of financial accounting is to provide the information to the

outside users such as suppliers, creditors, customer, government, shareholders etc. whereas the

objective of management accounting is to provide the information to the internal department like

owner, employees and mangers (Butler, and Ghosh, 2015).

Time frame : Financial accounting prepares the financial statement at the end of

accounting period whereas the management accounting prepare the report on the requirement of

data.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Section 2

Various types of cost in management accounting

The cost of the organization may be classified on different basis such as functional basis, on the

basis of types and on the basis of behaviour.

On the basis of types

Direct cost : The cost which are directly connected to the operation or manufacturing

department are known as direct cost. The relation of the cost is to the cost objective. For example

the direct labour, direct material, direct overhead all are included in direct cost. Most of the

direct cost vary with change in output. For example a company want to produce more product

than it need more material and labour. So with the change in output the cost of the product and

services also change (Amos, and et.al., 2018).

Indirect cost : the cost of the production activity which connect to the creating product

to maintain the price of the product is known as indirect cost. For example to fulfil the day to day

requirement of the company the needed material and supplies are comes under the indirect cost.

In Tesco, the cost related to add the services in the product or maintain the product in

warehouses are the indirect cost.

On the basis of Functions

Production cost : Production cost are also known as manufacturing cost. Those cost

which are related to the production of gods and services is known as production cost such as

consumable manufacturing supplies, labour, raw material, general overhead, power, water supply

all are comes under the production cost (Shepherd, 2015).

Non production cost : The cost which are not related to the production activity are

known as non-production cost such cost of advertising, promotion, packaging and transfer the

finished goods to the various store and end user. Non production cost normally are used to add

value to the product and services.

On the basis of behaviour

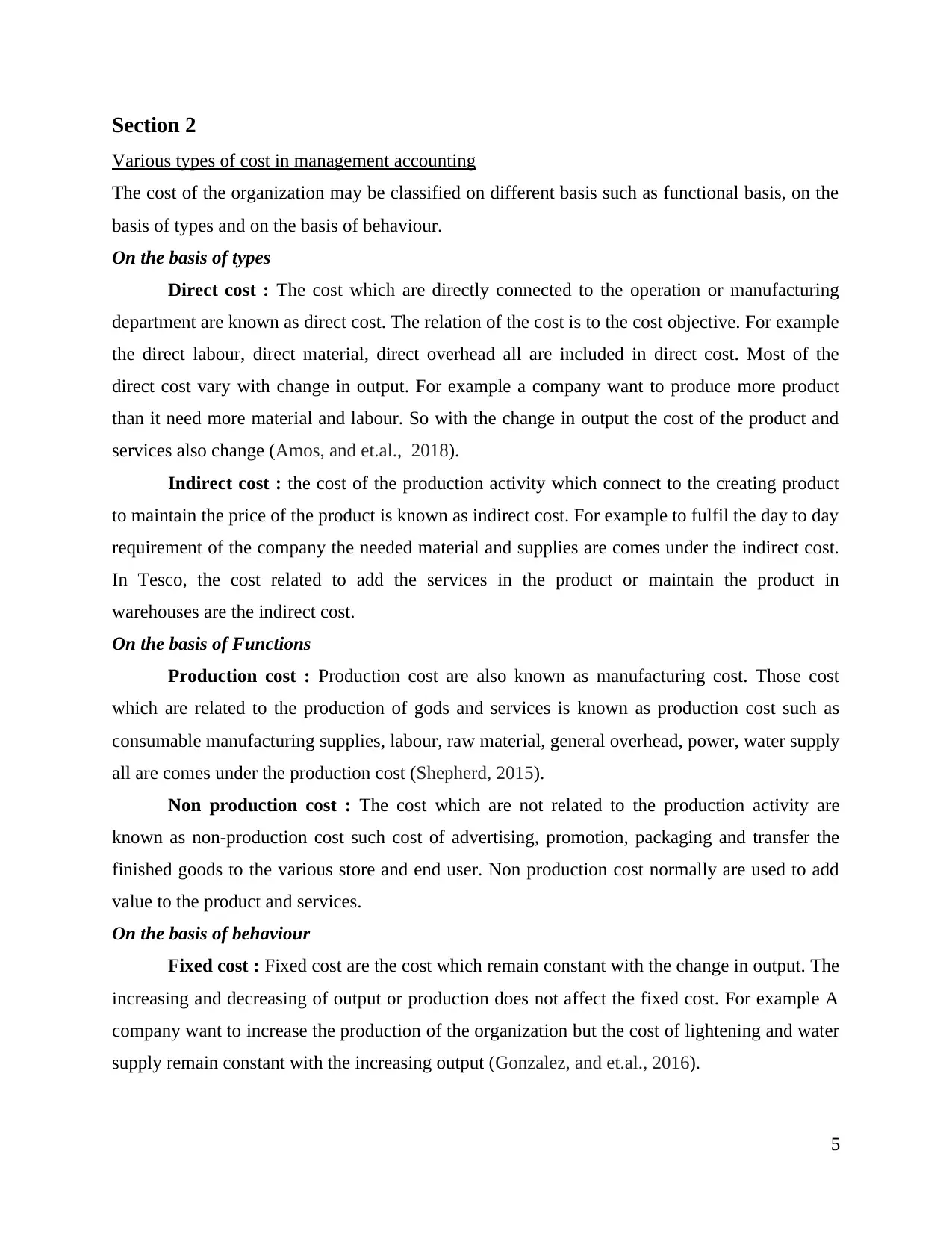

Fixed cost : Fixed cost are the cost which remain constant with the change in output. The

increasing and decreasing of output or production does not affect the fixed cost. For example A

company want to increase the production of the organization but the cost of lightening and water

supply remain constant with the increasing output (Gonzalez, and et.al., 2016).

5

Various types of cost in management accounting

The cost of the organization may be classified on different basis such as functional basis, on the

basis of types and on the basis of behaviour.

On the basis of types

Direct cost : The cost which are directly connected to the operation or manufacturing

department are known as direct cost. The relation of the cost is to the cost objective. For example

the direct labour, direct material, direct overhead all are included in direct cost. Most of the

direct cost vary with change in output. For example a company want to produce more product

than it need more material and labour. So with the change in output the cost of the product and

services also change (Amos, and et.al., 2018).

Indirect cost : the cost of the production activity which connect to the creating product

to maintain the price of the product is known as indirect cost. For example to fulfil the day to day

requirement of the company the needed material and supplies are comes under the indirect cost.

In Tesco, the cost related to add the services in the product or maintain the product in

warehouses are the indirect cost.

On the basis of Functions

Production cost : Production cost are also known as manufacturing cost. Those cost

which are related to the production of gods and services is known as production cost such as

consumable manufacturing supplies, labour, raw material, general overhead, power, water supply

all are comes under the production cost (Shepherd, 2015).

Non production cost : The cost which are not related to the production activity are

known as non-production cost such cost of advertising, promotion, packaging and transfer the

finished goods to the various store and end user. Non production cost normally are used to add

value to the product and services.

On the basis of behaviour

Fixed cost : Fixed cost are the cost which remain constant with the change in output. The

increasing and decreasing of output or production does not affect the fixed cost. For example A

company want to increase the production of the organization but the cost of lightening and water

supply remain constant with the increasing output (Gonzalez, and et.al., 2016).

5

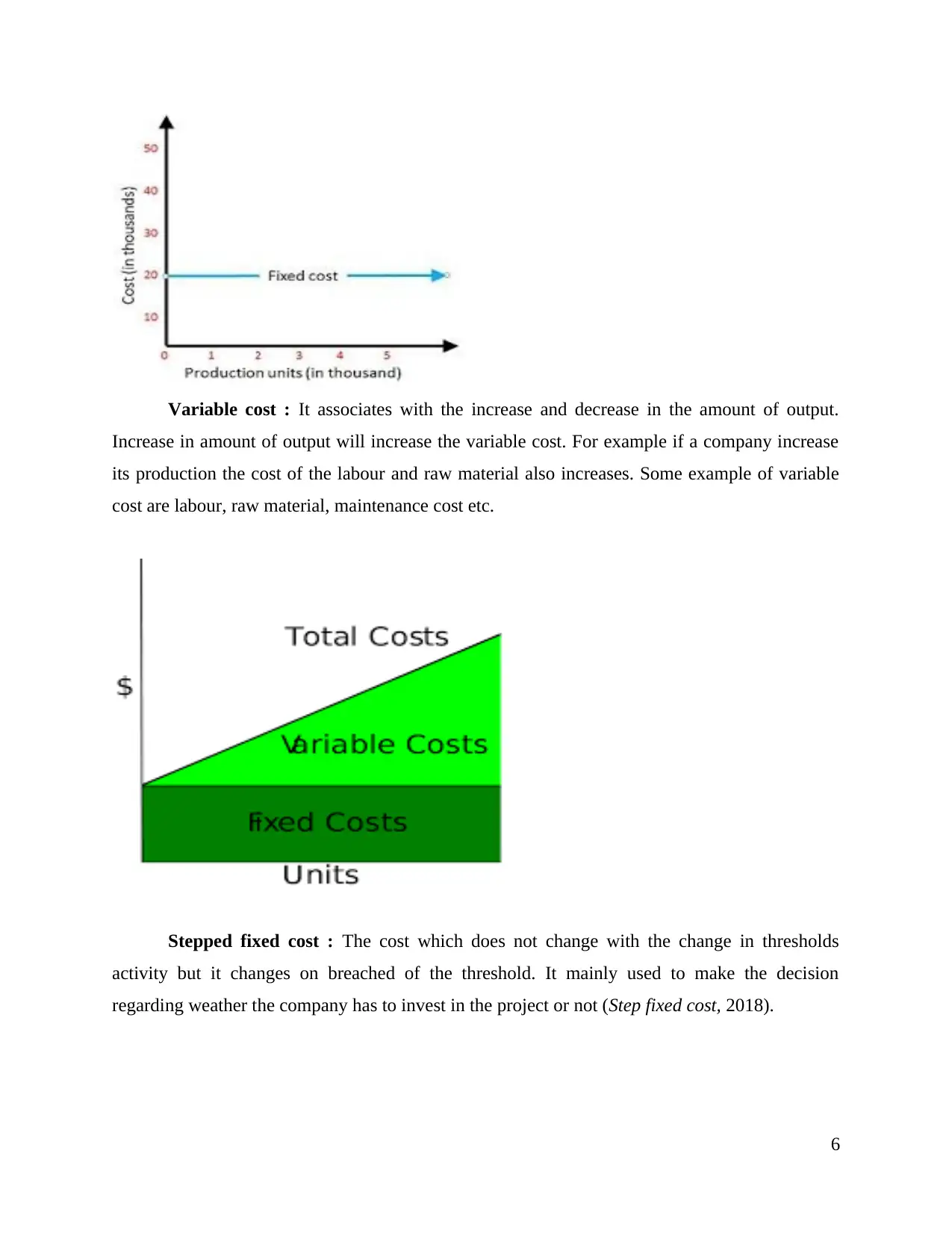

Variable cost : It associates with the increase and decrease in the amount of output.

Increase in amount of output will increase the variable cost. For example if a company increase

its production the cost of the labour and raw material also increases. Some example of variable

cost are labour, raw material, maintenance cost etc.

Stepped fixed cost : The cost which does not change with the change in thresholds

activity but it changes on breached of the threshold. It mainly used to make the decision

regarding weather the company has to invest in the project or not (Step fixed cost, 2018).

6

Increase in amount of output will increase the variable cost. For example if a company increase

its production the cost of the labour and raw material also increases. Some example of variable

cost are labour, raw material, maintenance cost etc.

Stepped fixed cost : The cost which does not change with the change in thresholds

activity but it changes on breached of the threshold. It mainly used to make the decision

regarding weather the company has to invest in the project or not (Step fixed cost, 2018).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Section 3

Effectiveness of marginal accounting system and their pros and cons to the organization

Marginal costing system : It is used by the organization to evaluate the impact of

change in variable cost due to the change in the volume of the output. In this variable cost is

charged due to the cost unit while the fixed cost of the particular time period is written off. It

other words it adds the additional cost in the output due to producing extra unit of product and

services (Hall, 2018).

Uses of marginal costing

Marginal costing is used to ascertain the cost of the company with recording the cost and

also reporting to the management. It helps the company to control the cost of different activity to

maximize the profit by minimizing the cost. Marginal costing system mainly used in

manufacturing industry because the change in variable cost or product output is quite common in

manufacturing company.

Advantages and disadvantages of marginal costing to the organization

Advantages

Simple to understand : It is simple to understand and operate the business by using

marginal costing because they do not include the fixed cost in the cost of production and also

there is absence of arbitrary apportionment (Alshamrani, and Bahattab, 2015).

Decision making : it helps the organization to make the short term decision regarding

minimize the cost with increase in profit. Marginal accounting also provide the sufficient tool to

7

Effectiveness of marginal accounting system and their pros and cons to the organization

Marginal costing system : It is used by the organization to evaluate the impact of

change in variable cost due to the change in the volume of the output. In this variable cost is

charged due to the cost unit while the fixed cost of the particular time period is written off. It

other words it adds the additional cost in the output due to producing extra unit of product and

services (Hall, 2018).

Uses of marginal costing

Marginal costing is used to ascertain the cost of the company with recording the cost and

also reporting to the management. It helps the company to control the cost of different activity to

maximize the profit by minimizing the cost. Marginal costing system mainly used in

manufacturing industry because the change in variable cost or product output is quite common in

manufacturing company.

Advantages and disadvantages of marginal costing to the organization

Advantages

Simple to understand : It is simple to understand and operate the business by using

marginal costing because they do not include the fixed cost in the cost of production and also

there is absence of arbitrary apportionment (Alshamrani, and Bahattab, 2015).

Decision making : it helps the organization to make the short term decision regarding

minimize the cost with increase in profit. Marginal accounting also provide the sufficient tool to

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

control the cost of the organization activities by evaluating each unit cost and different

alternatives to choose the best option.

Planning : Marginal costing system explain the relation between the cost, profit and

volume which help the organization to prepare the short term profit plan. It also helps the

management team in production planning by providing the various alternative and their effects.

Disadvantages

Based on unrealistic assumptions : The marginal accounting based on certain

unrealistic assumptions that all the cost of the organization divided in fixed cost and variable

cost. But in long term planning the fixed cost and price and sales vary from the changes in the

activities.

Long term planning : Marginal costing is helpful for the short term planning of cost and

profit but it is not suitable for the long term planning. Because for the long term, planning the

forecasting of profit and cost is not suitable because it varies from the changes in output and

external forces.

Section 4

Objectives of budgeting in regard to promote effectiveness

Budgeting : It is a financial plan which is made to estimate the future expenses and the

profit to plan and strategies the activities according to the estimated budget (Bogsnes, 2016). It

mainly used to control the cost and regulate the activities for accomplish the task on time of

within the budget.

Objectives of budgeting

Provide structure : The budget of the company provides the proper guideline to the

company to direct the different activities of the company. Basically budget provides the structure

for plan the activity for the future growth of the company by achieving the current objectives.

Predict cash flow : The objective of budgeting is to predict the cash inflow and outflow

of the company to meet the day to day requirement of cash. It helps the company to control the

irregular sales pattern.

Allocate resources : Many companies also use the budgeting system for allocating the

resources such as manpower and fund for different activities such as determining the fixed cost,

variable cost, labour cost etc.

8

alternatives to choose the best option.

Planning : Marginal costing system explain the relation between the cost, profit and

volume which help the organization to prepare the short term profit plan. It also helps the

management team in production planning by providing the various alternative and their effects.

Disadvantages

Based on unrealistic assumptions : The marginal accounting based on certain

unrealistic assumptions that all the cost of the organization divided in fixed cost and variable

cost. But in long term planning the fixed cost and price and sales vary from the changes in the

activities.

Long term planning : Marginal costing is helpful for the short term planning of cost and

profit but it is not suitable for the long term planning. Because for the long term, planning the

forecasting of profit and cost is not suitable because it varies from the changes in output and

external forces.

Section 4

Objectives of budgeting in regard to promote effectiveness

Budgeting : It is a financial plan which is made to estimate the future expenses and the

profit to plan and strategies the activities according to the estimated budget (Bogsnes, 2016). It

mainly used to control the cost and regulate the activities for accomplish the task on time of

within the budget.

Objectives of budgeting

Provide structure : The budget of the company provides the proper guideline to the

company to direct the different activities of the company. Basically budget provides the structure

for plan the activity for the future growth of the company by achieving the current objectives.

Predict cash flow : The objective of budgeting is to predict the cash inflow and outflow

of the company to meet the day to day requirement of cash. It helps the company to control the

irregular sales pattern.

Allocate resources : Many companies also use the budgeting system for allocating the

resources such as manpower and fund for different activities such as determining the fixed cost,

variable cost, labour cost etc.

8

Measure performance : the objective of budgeting is to measure the performance of the

organization by comparing the current year budget with the previous year budget and analyse the

reason behind the variances on budgeting,

Communicate the goal : the objective of preparing budget is to communicate the goal of

the organization to its managers. By estimating the cost of different activities it provides a basic

structure about the task perform by the organization to its employees.

Promote the effectiveness of the company

By providing the structure of the company it helps the manager to set the business by

estimating the future requirement of the organization like the need of raw material, power

supply, labour etc. Through the basic structure manager can accomplish the need and demand of

the customer by setting budget for different activities in fulfilling the demand (Dudin, and et.al.,

2015).

The use of budgeting in predicting the cash flow help the managers to set the requirement

of cash for each activity. The prediction of cash flow also help them to prepare the plan for

getting the cash from the various sources such as capital venture, shares, long term borrowing

etc. for setting the business (Addabbo, and et.al., 2019).

Manager uses the budgeting to allocate resources by estimating the requirement of

resources in the business and find the various sources to collect the resources. Allocation of fund

help them to estimate the expected expenditure of the company to compete with competitors.

The measurement of performance through budgeting help the manager to evaluate the

various are of variances and measure different alternatives to get the final solution for improving

the performance of the company. The evaluation of various area improve the control upon the

different activities which ultimately improve the effectiveness of the managers and company.

Communicating goal to the manager help the company and manager to decide or plan the

activities and various way to performs these activities stated in the budget planning. By planning

the activity an organization can easily achieve the purpose of setting business and effective work

of the employees and managers.

9

organization by comparing the current year budget with the previous year budget and analyse the

reason behind the variances on budgeting,

Communicate the goal : the objective of preparing budget is to communicate the goal of

the organization to its managers. By estimating the cost of different activities it provides a basic

structure about the task perform by the organization to its employees.

Promote the effectiveness of the company

By providing the structure of the company it helps the manager to set the business by

estimating the future requirement of the organization like the need of raw material, power

supply, labour etc. Through the basic structure manager can accomplish the need and demand of

the customer by setting budget for different activities in fulfilling the demand (Dudin, and et.al.,

2015).

The use of budgeting in predicting the cash flow help the managers to set the requirement

of cash for each activity. The prediction of cash flow also help them to prepare the plan for

getting the cash from the various sources such as capital venture, shares, long term borrowing

etc. for setting the business (Addabbo, and et.al., 2019).

Manager uses the budgeting to allocate resources by estimating the requirement of

resources in the business and find the various sources to collect the resources. Allocation of fund

help them to estimate the expected expenditure of the company to compete with competitors.

The measurement of performance through budgeting help the manager to evaluate the

various are of variances and measure different alternatives to get the final solution for improving

the performance of the company. The evaluation of various area improve the control upon the

different activities which ultimately improve the effectiveness of the managers and company.

Communicating goal to the manager help the company and manager to decide or plan the

activities and various way to performs these activities stated in the budget planning. By planning

the activity an organization can easily achieve the purpose of setting business and effective work

of the employees and managers.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

CONCLUSION

The report summarizes the role of marginal accounting in the business organization that

how it helps the company to make decisions and policies to improve the productivity and

profitability of the organization. It also provides a comparison of financial accounting and

management accounting to get the effect of different accounting system on the organizations. It

can be concluded from the study that different type of cost are used in the organization for

different purpose like variable cost is used to find the changes in the production cost due to

change in the output. The report also summarizes the effect of marginal cost in the company with

its advantages and disadvantages. It can also be concluded from the study that preparation of

budget promote the effectiveness in the organization or work place.

10

The report summarizes the role of marginal accounting in the business organization that

how it helps the company to make decisions and policies to improve the productivity and

profitability of the organization. It also provides a comparison of financial accounting and

management accounting to get the effect of different accounting system on the organizations. It

can be concluded from the study that different type of cost are used in the organization for

different purpose like variable cost is used to find the changes in the production cost due to

change in the output. The report also summarizes the effect of marginal cost in the company with

its advantages and disadvantages. It can also be concluded from the study that preparation of

budget promote the effectiveness in the organization or work place.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFERENCES

Books and Journals

Addabbo, T., and et.al., 2019. Gender budgeting from a capability approach perspective:

evidences from Senegal. Academic Conferences and Publishing International Limited.

Ahmed, A., and et.al., 2017. Pavement repair marginal costs: accounting for heterogeneity using

random-parameters regression. Journal of Infrastructure Systems, 23(4). p.04017012.

Alshamrani, A. and Bahattab, A., 2015. A comparison between three SDLC models waterfall

model, spiral model, and Incremental/Iterative model. International Journal of

Computer Science Issues (IJCSI), 12(1). p.106.

Amos, T.B., and et.al., 2018. Direct and Indirect Cost Burden and Change of Employment

Status in Treatment-Resistant Depression: A Matched-Cohort Study Using a US

Commercial Claims Database. The Journal of clinical psychiatry, 79(2).

Bogsnes, B., 2016. Implementing beyond budgeting: Unlocking the performance potential. John

Wiley & Sons.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1). pp.33-45.

Dudin, M., and et.al., 2015. The innovative business model canvas in the system of effective

budgeting. Asian Social Science, 11(7). pp.290-296.

Gonzalez, P.H., and et.al., 2016. A variable fixing heuristic with Local Branching for the fixed

charge uncapacitated network design problem with user-optimal flow. Computers &

Operations Research, 76. pp.134-146.

Hall, R.E., 2018. New evidence on the markup of prices over marginal costs and the role of

mega-firms in the us economy(No. w24574). National Bureau of Economic Research.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder Ready

Version. John Wiley & Sons.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4). pp.1187-1230.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Shepherd, R.W., 2015. Theory of cost and production functions. Princeton University Press.

Online

Difference between the financial accounting and management accounting. 2019. [Online].

Available through : <https://www.wallstreetmojo.com/financial-accounting-vs-management-

accounting/>

Step fixed cost. 2018. [Online]. Available through :

<https://www.accountingtools.com/articles/what-is-a-step-fixed-cost.html>

11

Books and Journals

Addabbo, T., and et.al., 2019. Gender budgeting from a capability approach perspective:

evidences from Senegal. Academic Conferences and Publishing International Limited.

Ahmed, A., and et.al., 2017. Pavement repair marginal costs: accounting for heterogeneity using

random-parameters regression. Journal of Infrastructure Systems, 23(4). p.04017012.

Alshamrani, A. and Bahattab, A., 2015. A comparison between three SDLC models waterfall

model, spiral model, and Incremental/Iterative model. International Journal of

Computer Science Issues (IJCSI), 12(1). p.106.

Amos, T.B., and et.al., 2018. Direct and Indirect Cost Burden and Change of Employment

Status in Treatment-Resistant Depression: A Matched-Cohort Study Using a US

Commercial Claims Database. The Journal of clinical psychiatry, 79(2).

Bogsnes, B., 2016. Implementing beyond budgeting: Unlocking the performance potential. John

Wiley & Sons.

Butler, S.A. and Ghosh, D., 2015. Individual differences in managerial accounting judgments

and decision making. The British Accounting Review, 47(1). pp.33-45.

Dudin, M., and et.al., 2015. The innovative business model canvas in the system of effective

budgeting. Asian Social Science, 11(7). pp.290-296.

Gonzalez, P.H., and et.al., 2016. A variable fixing heuristic with Local Branching for the fixed

charge uncapacitated network design problem with user-optimal flow. Computers &

Operations Research, 76. pp.134-146.

Hall, R.E., 2018. New evidence on the markup of prices over marginal costs and the role of

mega-firms in the us economy(No. w24574). National Bureau of Economic Research.

Kieso, D.E., Weygandt, J.J. and Warfield, T.D., 2016. Intermediate Accounting, Binder Ready

Version. John Wiley & Sons.

Loughran, T. and McDonald, B., 2016. Textual analysis in accounting and finance: A

survey. Journal of Accounting Research, 54(4). pp.1187-1230.

Schaltegger, S. and Burritt, R., 2017. Contemporary environmental accounting: issues, concepts

and practice. Routledge.

Shepherd, R.W., 2015. Theory of cost and production functions. Princeton University Press.

Online

Difference between the financial accounting and management accounting. 2019. [Online].

Available through : <https://www.wallstreetmojo.com/financial-accounting-vs-management-

accounting/>

Step fixed cost. 2018. [Online]. Available through :

<https://www.accountingtools.com/articles/what-is-a-step-fixed-cost.html>

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.