Management Accounting Report: TECK (UK) Ltd - Costing and Budgeting

VerifiedAdded on 2020/06/03

|17

|4969

|36

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on costing and budgeting techniques within the context of TECK (UK) Limited. It begins with an introduction to management accounting, outlining its concepts, essential requirements, and its distinction from financial accounting. The report delves into various costing methods employed to compute net profitability, including job costing, batch costing, and contract process costing. It examines different types of budgets, their advantages and disadvantages, and the use of budget planning tools. Furthermore, the report explores the balance scorecard approach for analyzing financial problems and critically evaluates potential solutions to overcome financial issues. The report includes an analysis of financial statements and the importance of management accounting reports in decision-making processes, offering valuable insights for improving business operations and financial performance.

Management Accounting:

Costing and Budgeting

Costing and Budgeting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting concept and essential requirements of MA system .....................1

P2: (A) Different types of managerial accounting report............................................................4

B(II): Importance of management accounting report..................................................................5

M1: Benefits of using management accounting system..............................................................5

D1: Critically evaluate management accounting reporting system.............................................5

TASK 2............................................................................................................................................5

P3: Various costing methods which is used in computing net profitability................................5

M2: Use of management accounting techniques........................................................................8

D2: Data interpretation collected from income statements.........................................................8

TASK 3............................................................................................................................................9

P4: Different types of budgets and their advantage and disadvantage........................................9

M3: Use and analysis of budget planning tools........................................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard approach ...............................................................................................11

M4: Analysis of financial problems..........................................................................................13

D3: Critically evaluate solution to overcome financial issues..................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting concept and essential requirements of MA system .....................1

P2: (A) Different types of managerial accounting report............................................................4

B(II): Importance of management accounting report..................................................................5

M1: Benefits of using management accounting system..............................................................5

D1: Critically evaluate management accounting reporting system.............................................5

TASK 2............................................................................................................................................5

P3: Various costing methods which is used in computing net profitability................................5

M2: Use of management accounting techniques........................................................................8

D2: Data interpretation collected from income statements.........................................................8

TASK 3............................................................................................................................................9

P4: Different types of budgets and their advantage and disadvantage........................................9

M3: Use and analysis of budget planning tools........................................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard approach ...............................................................................................11

M4: Analysis of financial problems..........................................................................................13

D3: Critically evaluate solution to overcome financial issues..................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In every business organisation, management accounting is a key competent that would assist

the managers to record and analyse their financial transactions is systematic format. The primary

role of an organisation is to maximise their profit through producing large amount of products

and services during the year. To manage and control day to day expense and costs of the

company they required a well organise systems which would help them to record data in an

effective manner. The project report is providing valuable information about “TECK (UK)

Limited” daily operations (Schaltegger and Burritt, 2017).

Essential requirements of management accounting system and reporting are discuss under

this specific report. Some effective costing methods are used which is helpful in evaluating total

net profits for the company. Understanding of various kinds of budgets and their merits and

demerits to increasing efficiency of the company. Further, this report is examined financial

problems and effective measure to resolve them to get better outcomes for an organisation.

TASK 1

P1: Management accounting concept and essential requirements of MA system

In order to generate more effective results for the company. The managers required to

make sure of accounting systems in more effective manner. Management accounting is a

systematic format of recording, summarising, communicating and evaluating overall condition of

the company. The primary motive of using such kind of reporting system is to provide valuable

information to manager and owners of the company to make sound decision. The objective is not

to combine with external demands such as increase dividend, but rather than capturing crucial

information that can be utilised by TECH Ltd in near future (Hilton and Platt, 2013). It is helpful

to describe modern concepts of accounts as effective tools of management in respect to

conventional periodical data series. The object is use to expand the financial and statistical data

so as to bring light on every stage of activities of TECH Ltd. It evolves a systematic plan of

accounting that lays maximum emphasis on the strategies of future forecasting.

Difference analysis:

Basis Management Accounting Financial Accounting

Subject Matter Under this, the maximum attention is In this accounting, the enterprises

1

In every business organisation, management accounting is a key competent that would assist

the managers to record and analyse their financial transactions is systematic format. The primary

role of an organisation is to maximise their profit through producing large amount of products

and services during the year. To manage and control day to day expense and costs of the

company they required a well organise systems which would help them to record data in an

effective manner. The project report is providing valuable information about “TECK (UK)

Limited” daily operations (Schaltegger and Burritt, 2017).

Essential requirements of management accounting system and reporting are discuss under

this specific report. Some effective costing methods are used which is helpful in evaluating total

net profits for the company. Understanding of various kinds of budgets and their merits and

demerits to increasing efficiency of the company. Further, this report is examined financial

problems and effective measure to resolve them to get better outcomes for an organisation.

TASK 1

P1: Management accounting concept and essential requirements of MA system

In order to generate more effective results for the company. The managers required to

make sure of accounting systems in more effective manner. Management accounting is a

systematic format of recording, summarising, communicating and evaluating overall condition of

the company. The primary motive of using such kind of reporting system is to provide valuable

information to manager and owners of the company to make sound decision. The objective is not

to combine with external demands such as increase dividend, but rather than capturing crucial

information that can be utilised by TECH Ltd in near future (Hilton and Platt, 2013). It is helpful

to describe modern concepts of accounts as effective tools of management in respect to

conventional periodical data series. The object is use to expand the financial and statistical data

so as to bring light on every stage of activities of TECH Ltd. It evolves a systematic plan of

accounting that lays maximum emphasis on the strategies of future forecasting.

Difference analysis:

Basis Management Accounting Financial Accounting

Subject Matter Under this, the maximum attention is In this accounting, the enterprises

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

directed towards different parts of

business organisation which work on the

combination of various aspects.

are operating as a whole toward

increase performance of an

organization.

Nature In case of management accounting, it is

concern with future plans and policies.

Financial accounting is related

almost with exclusively with

historical data of Tech Ltd.

Characteristics It provides maximum emphasizes on

those aspects which will increase the

value of data in wide variety of uses.

It places wide stress on those

qualities in data which can rely on

universal confidence such as

validity and objectivity.

Types of data Only quality data is being analysed

under this accounting system.

Financial accounting makes sure of

crucial information to make sure of

data which is measure in

quantitative and monetary term.

Importance of management accounting in decision making process

In every business organisation, it has been seen that management always search of getting

more effective results by using data of the company. This would assists them to make use fo

accounting systems in well organise manner so that chances of getting better results can be

enhances in future. There is some crucial significance of using accounting systems which is

being discussed underneath:

It is use for future forecasting: As decision making is done to make control over all

those aspects those are affecting the profitability of an organization. This will aid company to

make analysis of all those aspects those are associated with the company whether they are

getting valuable amount of return from their total capital investments (Importance of

management accounting, 2016).

Future cash flow forecasting: It is essential for the company to predicting cash flows

and make impacts of cash on the business. It consists of budget and trend charts and managers

those are using information to decide in order to allocate funds and resources to incurred the

estimated profit growth.

2

business organisation which work on the

combination of various aspects.

are operating as a whole toward

increase performance of an

organization.

Nature In case of management accounting, it is

concern with future plans and policies.

Financial accounting is related

almost with exclusively with

historical data of Tech Ltd.

Characteristics It provides maximum emphasizes on

those aspects which will increase the

value of data in wide variety of uses.

It places wide stress on those

qualities in data which can rely on

universal confidence such as

validity and objectivity.

Types of data Only quality data is being analysed

under this accounting system.

Financial accounting makes sure of

crucial information to make sure of

data which is measure in

quantitative and monetary term.

Importance of management accounting in decision making process

In every business organisation, it has been seen that management always search of getting

more effective results by using data of the company. This would assists them to make use fo

accounting systems in well organise manner so that chances of getting better results can be

enhances in future. There is some crucial significance of using accounting systems which is

being discussed underneath:

It is use for future forecasting: As decision making is done to make control over all

those aspects those are affecting the profitability of an organization. This will aid company to

make analysis of all those aspects those are associated with the company whether they are

getting valuable amount of return from their total capital investments (Importance of

management accounting, 2016).

Future cash flow forecasting: It is essential for the company to predicting cash flows

and make impacts of cash on the business. It consists of budget and trend charts and managers

those are using information to decide in order to allocate funds and resources to incurred the

estimated profit growth.

2

Understanding performance variances: It is important to make understanding of

various aspects among total predication and actually what they are achieving from their total

investments.

Cost accounting system: It is one of the important accounting systems which is helpful for the

managers to determine their total cost incur during the production of products and services. It

summarises of various aspects those are directly or indirectly associated with a product. It a well

organise framework which is use by the firms to estimate total costs of their goods for gaining

profitability for the company. There are some other costs which are associated with them. Such

as:

Normal: It is known as those costs which are normal paid or incur by the company

during manufacturing of a products.

Actual: According to this costs which are mainly liable to the company with direct labour

and production overhead bases on predetermine overhead charges.

Standard: It is related with standard costs which are associated with the cost of goods

sold and for valuation of stock.

Inventory management system: It is said to be one of the crucial methods which is helpful in

managing and controlling their stock position of the company. This will assists in recording of

opening and closing entries of data about inventory kept by Tech Ltd.

FIFO: These are said to be inventories valuation techniques. The outcomes in deflated

net outcomes and lower ending balances in stock is compare to be FIFO.

LIFO: It is an asset management and stock valuation techniques that assumes as assets

produced or kept by company would be used at initial stage.

AVCO: This seems to use as calculation of ending stock and cost of product sold during

the period of time.

Job costing system: It is an effective system for assigning products costs to a single products or

group. Basically, the job order costing system is helpful in only those situation in which products

produce are entirely different from each other (Klychova and et. al., 2015).

Batch costing: It is a form of particular order costing which is more similar to job

costing. Each batch are given some identical number units but are different from each

other.

3

various aspects among total predication and actually what they are achieving from their total

investments.

Cost accounting system: It is one of the important accounting systems which is helpful for the

managers to determine their total cost incur during the production of products and services. It

summarises of various aspects those are directly or indirectly associated with a product. It a well

organise framework which is use by the firms to estimate total costs of their goods for gaining

profitability for the company. There are some other costs which are associated with them. Such

as:

Normal: It is known as those costs which are normal paid or incur by the company

during manufacturing of a products.

Actual: According to this costs which are mainly liable to the company with direct labour

and production overhead bases on predetermine overhead charges.

Standard: It is related with standard costs which are associated with the cost of goods

sold and for valuation of stock.

Inventory management system: It is said to be one of the crucial methods which is helpful in

managing and controlling their stock position of the company. This will assists in recording of

opening and closing entries of data about inventory kept by Tech Ltd.

FIFO: These are said to be inventories valuation techniques. The outcomes in deflated

net outcomes and lower ending balances in stock is compare to be FIFO.

LIFO: It is an asset management and stock valuation techniques that assumes as assets

produced or kept by company would be used at initial stage.

AVCO: This seems to use as calculation of ending stock and cost of product sold during

the period of time.

Job costing system: It is an effective system for assigning products costs to a single products or

group. Basically, the job order costing system is helpful in only those situation in which products

produce are entirely different from each other (Klychova and et. al., 2015).

Batch costing: It is a form of particular order costing which is more similar to job

costing. Each batch are given some identical number units but are different from each

other.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Contract process costing: This seems to be one of the method of assigning costs to units

of products in companies that are producing wide amount of quantity for various

homogeneous products.

P2: (A) Different types of managerial accounting report

In every manufacturing business organization, it has been seen that a well organize

accounting system reporting is needed to make proper entries of financial transaction those are

being done in an accounting year. The reports are more crucial aspects for every business that

would present effective solution to organization problems. There are various sources from which

data is being collected from the purpose of making a systematic detail reports. The major sources

of data collection are taken from various departments such as HR, Marketing and finance

department. This is mostly prepared at internal level so that chances of getting more accurate and

reliable outcomes can be increase in easier manner. There are various accounting reporting

system which will be helpful in order to record financial transaction in more detail and

systematic mode. Some of them are discussed underneath:

Performance report: According to this particular report, every information related with

past and present financial performance is recorded in it. It is an important activity in any project

communication management system. It consists of collecting and presenting detail information,

utilization of resources and estimating for the future growth and sustainability (Bebbington,

Unerman and O'Dwyer, 2014).

Account receivable aging report: It is known as company’s more crucial report because

it provide vital information about total list of unpaid customers invoices and credit memos. The

primary tool which used by gathering personnel to examine which payment is overdue.

Operational budget report: According to this particular budget every crucial

information regarding total sales and production level are recorded accordingly. This would

assist in providing useful information about their total cost and expense incur during the time.

Job cost report: It is an effective technique to record total costs of a production job

rather than a complete process. By this, a project manager use to keep regular track of the total

cost of each job (Bennett, Schaltegger and Zvezdov, 2013).

Inventory management report: As per this reporting, it has been notices that every

stock record is maintained by using appropriate tools and techniques. Such as, ABC costing,

inventory turnover ratio and EOQ.

4

of products in companies that are producing wide amount of quantity for various

homogeneous products.

P2: (A) Different types of managerial accounting report

In every manufacturing business organization, it has been seen that a well organize

accounting system reporting is needed to make proper entries of financial transaction those are

being done in an accounting year. The reports are more crucial aspects for every business that

would present effective solution to organization problems. There are various sources from which

data is being collected from the purpose of making a systematic detail reports. The major sources

of data collection are taken from various departments such as HR, Marketing and finance

department. This is mostly prepared at internal level so that chances of getting more accurate and

reliable outcomes can be increase in easier manner. There are various accounting reporting

system which will be helpful in order to record financial transaction in more detail and

systematic mode. Some of them are discussed underneath:

Performance report: According to this particular report, every information related with

past and present financial performance is recorded in it. It is an important activity in any project

communication management system. It consists of collecting and presenting detail information,

utilization of resources and estimating for the future growth and sustainability (Bebbington,

Unerman and O'Dwyer, 2014).

Account receivable aging report: It is known as company’s more crucial report because

it provide vital information about total list of unpaid customers invoices and credit memos. The

primary tool which used by gathering personnel to examine which payment is overdue.

Operational budget report: According to this particular budget every crucial

information regarding total sales and production level are recorded accordingly. This would

assist in providing useful information about their total cost and expense incur during the time.

Job cost report: It is an effective technique to record total costs of a production job

rather than a complete process. By this, a project manager use to keep regular track of the total

cost of each job (Bennett, Schaltegger and Zvezdov, 2013).

Inventory management report: As per this reporting, it has been notices that every

stock record is maintained by using appropriate tools and techniques. Such as, ABC costing,

inventory turnover ratio and EOQ.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B(II): Importance of management accounting report

It is essential for reporting that gives executives a clear picture of financial health of an

arrangement that used to provide an organization certain information through performing at on

operational level. Performance report is most effective reporting method that are used to analyze

performance of actual or standard one. While account receivable can assist them to examine total

list of unpaid customer invoices. Management reporting provides crucial information about

company total financial healthy condition. It does not provide all information which is essential

to assists them to find out the business is working at their operational level. This would help in

making vital capital investment decision regarding future objectives so that profitability can get

enhanced.

M1: Benefits of using management accounting system

It is crucial for the department to make use of accounting system that can be able to

generate more valuable outcomes for the company. The most important aspects of using

accounting systems to increase productivity of Tech UK Ltd. The another benefits of accounting

system us to maintain efficiency of Tech Ltd through using proper systems such as price

optimization, cost accounting and job costing system. There are various important accounting

reports systems and all of them are having equal benefits to an organization. Increase the bar of

profitability and simplifies the decision making in financial report of the cited company. Some of

them are cost accounting system that is liable to determine total cost and expenses that are incur

during the period of time. Inventory management inventory system used to track opening and

closing stock position of the company.

D1: Critically evaluate management accounting reporting system

According to the above mentioned various accounting system reporting, managers can

easily make their business more safe and profitable. There are various tools and techniques such

as account receivable and performance report which will always assists in generating more

crucial information about current position of Tech Ltd.

TASK 2

P3: Various costing methods which is used in computing net profitability

Cost is the value of money that is needed to get something. These are directly associated

with the production of products and services. In manufacturing business, the cost can be said that

5

It is essential for reporting that gives executives a clear picture of financial health of an

arrangement that used to provide an organization certain information through performing at on

operational level. Performance report is most effective reporting method that are used to analyze

performance of actual or standard one. While account receivable can assist them to examine total

list of unpaid customer invoices. Management reporting provides crucial information about

company total financial healthy condition. It does not provide all information which is essential

to assists them to find out the business is working at their operational level. This would help in

making vital capital investment decision regarding future objectives so that profitability can get

enhanced.

M1: Benefits of using management accounting system

It is crucial for the department to make use of accounting system that can be able to

generate more valuable outcomes for the company. The most important aspects of using

accounting systems to increase productivity of Tech UK Ltd. The another benefits of accounting

system us to maintain efficiency of Tech Ltd through using proper systems such as price

optimization, cost accounting and job costing system. There are various important accounting

reports systems and all of them are having equal benefits to an organization. Increase the bar of

profitability and simplifies the decision making in financial report of the cited company. Some of

them are cost accounting system that is liable to determine total cost and expenses that are incur

during the period of time. Inventory management inventory system used to track opening and

closing stock position of the company.

D1: Critically evaluate management accounting reporting system

According to the above mentioned various accounting system reporting, managers can

easily make their business more safe and profitable. There are various tools and techniques such

as account receivable and performance report which will always assists in generating more

crucial information about current position of Tech Ltd.

TASK 2

P3: Various costing methods which is used in computing net profitability

Cost is the value of money that is needed to get something. These are directly associated

with the production of products and services. In manufacturing business, the cost can be said that

5

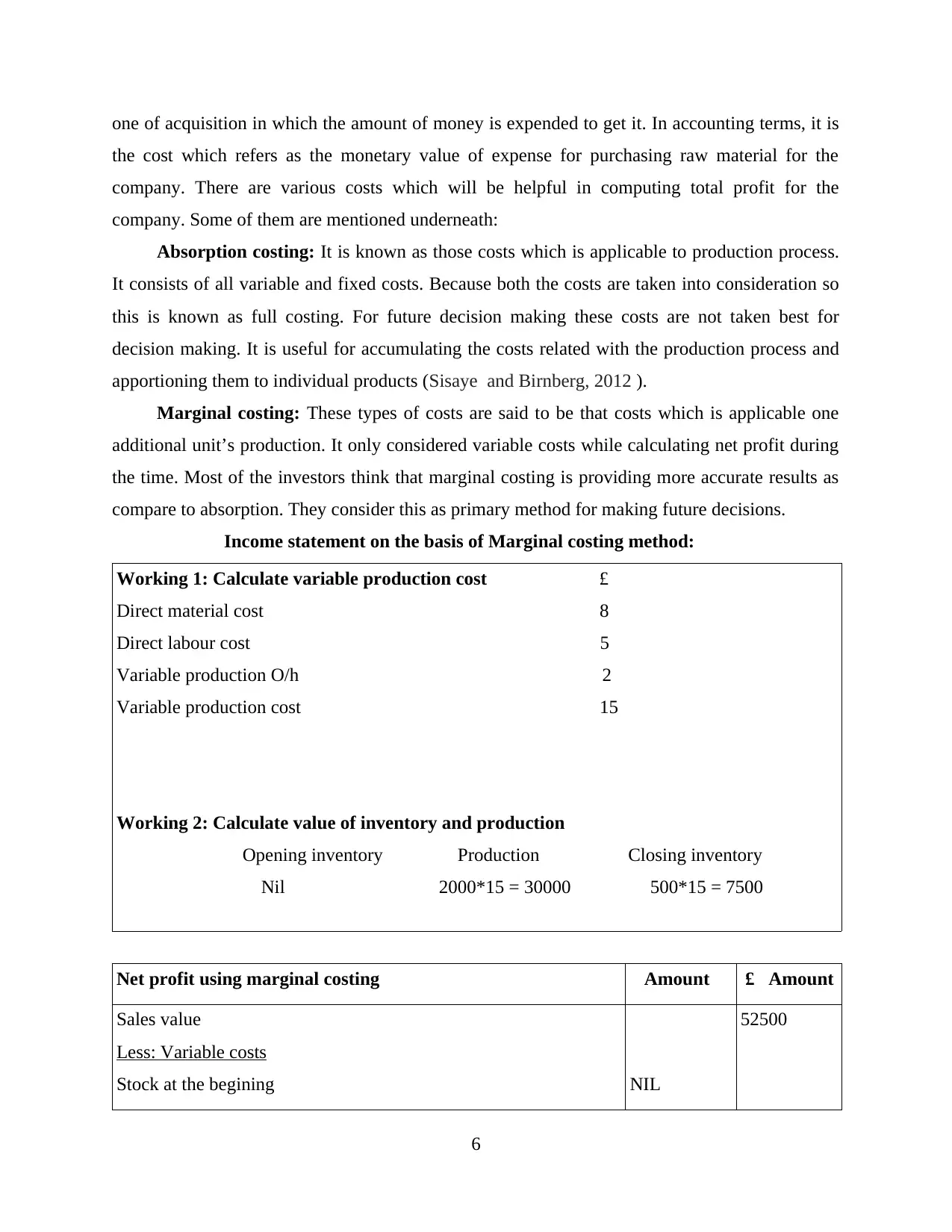

one of acquisition in which the amount of money is expended to get it. In accounting terms, it is

the cost which refers as the monetary value of expense for purchasing raw material for the

company. There are various costs which will be helpful in computing total profit for the

company. Some of them are mentioned underneath:

Absorption costing: It is known as those costs which is applicable to production process.

It consists of all variable and fixed costs. Because both the costs are taken into consideration so

this is known as full costing. For future decision making these costs are not taken best for

decision making. It is useful for accumulating the costs related with the production process and

apportioning them to individual products (Sisaye and Birnberg, 2012 ).

Marginal costing: These types of costs are said to be that costs which is applicable one

additional unit’s production. It only considered variable costs while calculating net profit during

the time. Most of the investors think that marginal costing is providing more accurate results as

compare to absorption. They consider this as primary method for making future decisions.

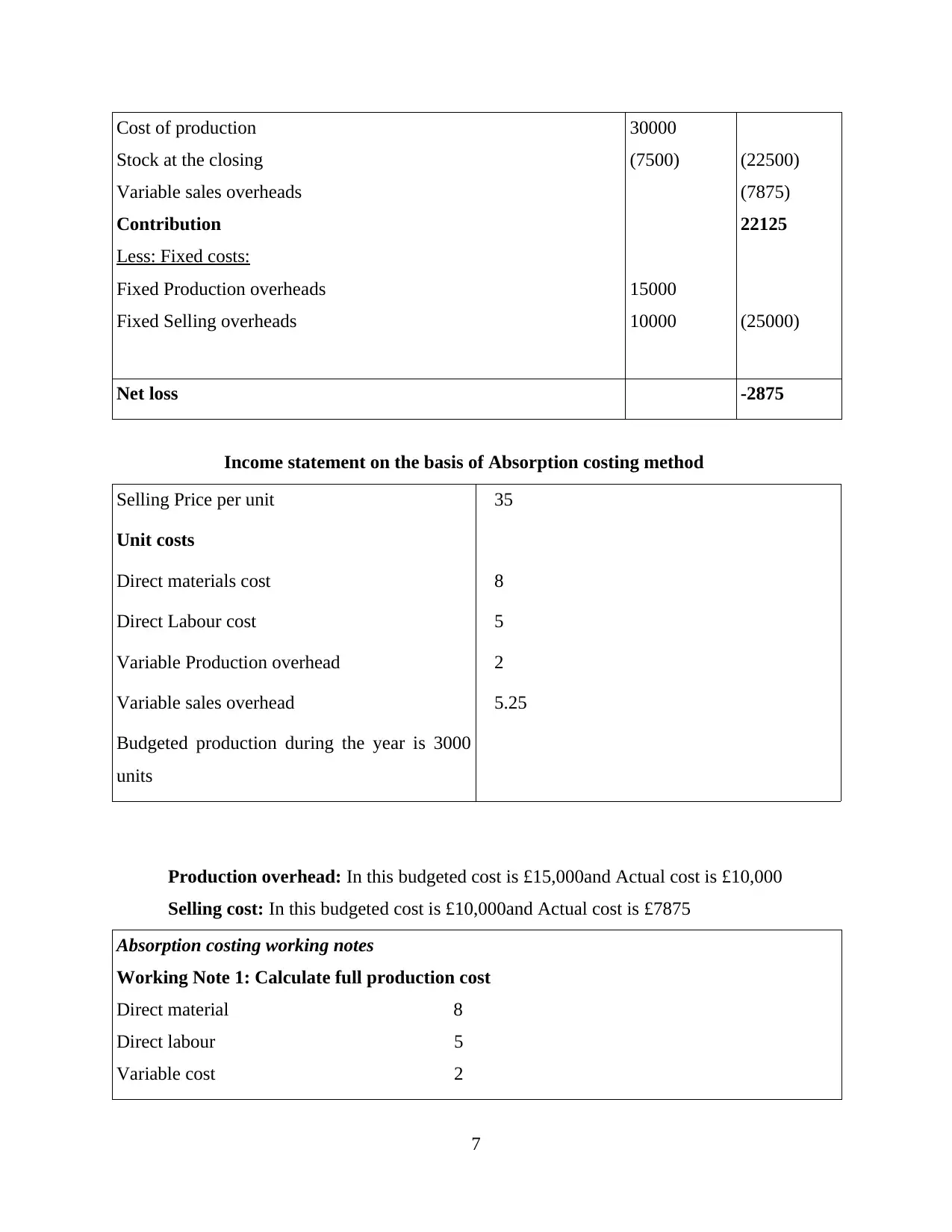

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining NIL

52500

6

the cost which refers as the monetary value of expense for purchasing raw material for the

company. There are various costs which will be helpful in computing total profit for the

company. Some of them are mentioned underneath:

Absorption costing: It is known as those costs which is applicable to production process.

It consists of all variable and fixed costs. Because both the costs are taken into consideration so

this is known as full costing. For future decision making these costs are not taken best for

decision making. It is useful for accumulating the costs related with the production process and

apportioning them to individual products (Sisaye and Birnberg, 2012 ).

Marginal costing: These types of costs are said to be that costs which is applicable one

additional unit’s production. It only considered variable costs while calculating net profit during

the time. Most of the investors think that marginal costing is providing more accurate results as

compare to absorption. They consider this as primary method for making future decisions.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining NIL

52500

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

7

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

30000

(7500)

15000

10000

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: In this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

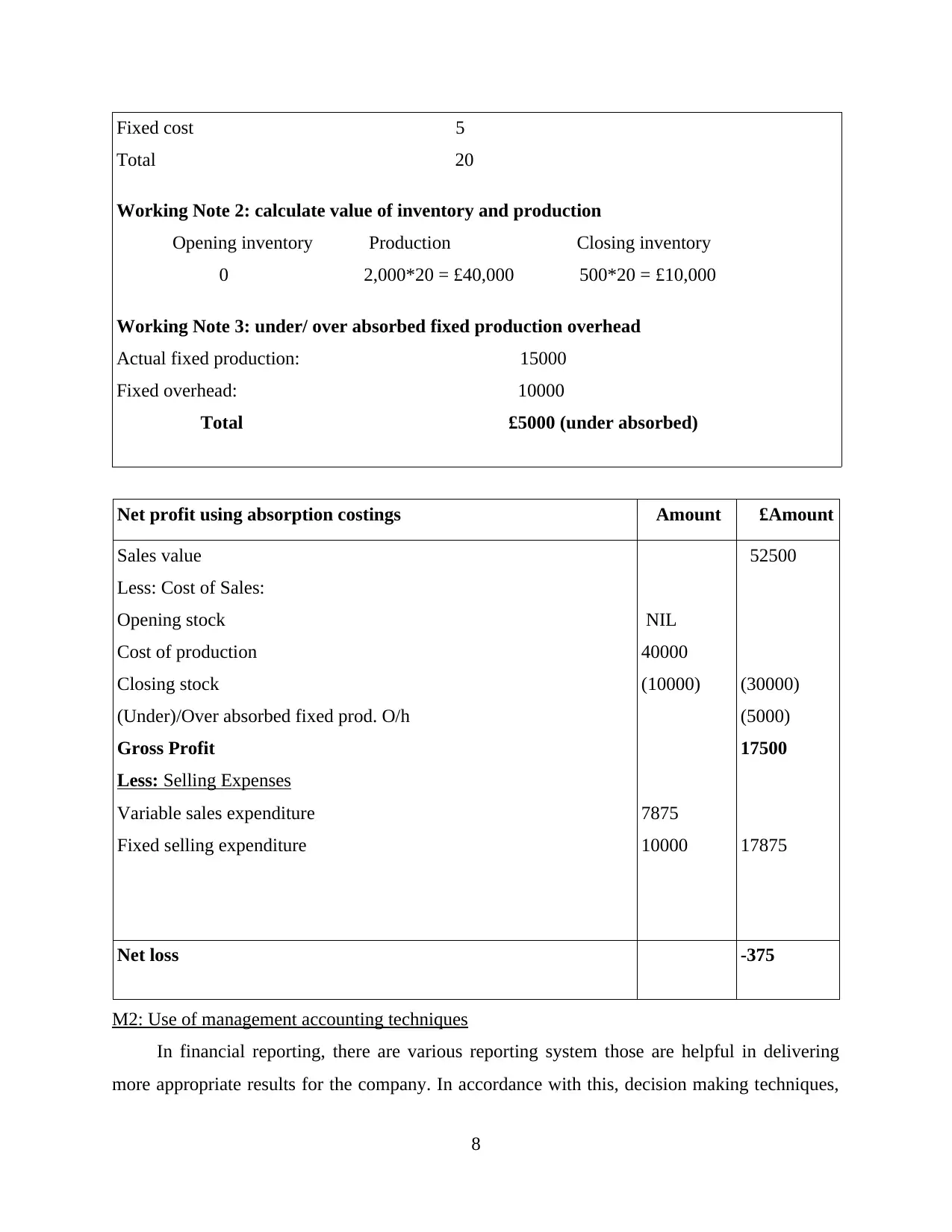

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2: Use of management accounting techniques

In financial reporting, there are various reporting system those are helpful in delivering

more appropriate results for the company. In accordance with this, decision making techniques,

8

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

Net loss -375

M2: Use of management accounting techniques

In financial reporting, there are various reporting system those are helpful in delivering

more appropriate results for the company. In accordance with this, decision making techniques,

8

marginal costing, standard costing and historical data costing tools are available. These

techniques are more suitable for making valuable decision in coming time. These are more

reliable in reconciling total net profitability of Tech Ltd which is collected out of their total

financial transactions.

D2: Data interpretation collected from income statements

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

In order to get positive results from the costing methods, managers of Tech Ltd has

decided to use two crucial methods such as marginal and absorption. The results are fluctuating

from both the methods. If they are going to use marginal costing they are able to generate net

loss of 2875. While with the use of absorption costing they are getting net loss of 375. The point

of this changes are arises because of the fixed cost treatments. The overall performance of the

company is not as suitable as in the month of September.

TASK 3

P4: Different types of budgets and their advantage and disadvantage

In every business, budget is an essential part by which company can control their costs and

expenses those are being going to be incur in near future. There are various types of budgets

which will be helpful in projecting their overall profitability. Some of them are mentioned

underneath:

Operational budgets: This kind of budget is more effective for the company at

functional level. There are some operational budgets such as sales budget, production budget and

raw material budgets. These budgets are made for controlling overall production ability of the

company.

Advantages: These budgets are more effectively helpful in determining their regular

costs and expense which are incurred by the company during production process.

Disadvantage: The main limitation of using this budget is too costly because, it is

prepared at continuous basis.

9

techniques are more suitable for making valuable decision in coming time. These are more

reliable in reconciling total net profitability of Tech Ltd which is collected out of their total

financial transactions.

D2: Data interpretation collected from income statements

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

In order to get positive results from the costing methods, managers of Tech Ltd has

decided to use two crucial methods such as marginal and absorption. The results are fluctuating

from both the methods. If they are going to use marginal costing they are able to generate net

loss of 2875. While with the use of absorption costing they are getting net loss of 375. The point

of this changes are arises because of the fixed cost treatments. The overall performance of the

company is not as suitable as in the month of September.

TASK 3

P4: Different types of budgets and their advantage and disadvantage

In every business, budget is an essential part by which company can control their costs and

expenses those are being going to be incur in near future. There are various types of budgets

which will be helpful in projecting their overall profitability. Some of them are mentioned

underneath:

Operational budgets: This kind of budget is more effective for the company at

functional level. There are some operational budgets such as sales budget, production budget and

raw material budgets. These budgets are made for controlling overall production ability of the

company.

Advantages: These budgets are more effectively helpful in determining their regular

costs and expense which are incurred by the company during production process.

Disadvantage: The main limitation of using this budget is too costly because, it is

prepared at continuous basis.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.