Management Accounting Report: Pizza Restaurant Case Study Analysis

VerifiedAdded on 2020/06/06

|13

|2884

|27

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to a new pizza restaurant venture. It begins with an introduction to the business, its mission, and vision, followed by the creation of a cost card to determine per-unit costs. The report then prepares various budgets, including sales, production, direct materials, direct labor, variable overhead, fixed overhead, and share capital budgets. A key component involves calculating and analyzing variances across these budgets, explaining their importance in assessing performance and identifying areas for improvement. The report also analyzes the statement, 'Management accounting is forward-looking while Financial Accounting is more historical,' comparing and contrasting the two accounting disciplines. Finally, the report concludes with a summary of findings and references.

Contribute Materials

Your contribution can guide someone’s learning journey. Share your

documents today.

Management Accounting

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Introduce a business and its product. Also prepare a cost card to calculate per unit cost of

stated product..........................................................................................................................1

TASK 2............................................................................................................................................3

Prepare different types of budgets..........................................................................................3

TASK 3............................................................................................................................................5

Calculate variance of different budgets and explain importance of calculating variances....5

TASK 4............................................................................................................................................8

"Management accounting is forward looking while Financial Accounting is more historical".

Analyse the statement.............................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Introduce a business and its product. Also prepare a cost card to calculate per unit cost of

stated product..........................................................................................................................1

TASK 2............................................................................................................................................3

Prepare different types of budgets..........................................................................................3

TASK 3............................................................................................................................................5

Calculate variance of different budgets and explain importance of calculating variances....5

TASK 4............................................................................................................................................8

"Management accounting is forward looking while Financial Accounting is more historical".

Analyse the statement.............................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Organisation is required to make its budget so that it may keep on track of its activities by

making budget forecast and analysing actual results and finding out variances if any (Fullerton,

Kennedy and Widener, 2014). The enclosed report is based on new company which is starting its

venture in food sector. As such, management accounting should be sound enough for effective

results.

TASK 1

Introduce a business and its product. Also prepare a cost card to calculate per unit cost of stated

product

Report

To:

From: Angel Syndicate

Subject: Introducing a restaurant

Mission-

The company is introducing the business of pizza restaurant. Foe demand fulfilment of

customers, it is launching its new business. Pizza has been preferred by almost of all age

groups. It will be help for company to establish and provides pizzas to public for their

satisfaction. It is required that company should be efficient enough to provide services to

customers. The mission of company is to establish brand image in front of the public so that it

may enhance them and satisfy them. It is required that organisation should deliver quality of

product to customers as when quality is not achieved, products fail. As a result, brand image is

lost. For ensuring proper quality, standards should be set by it so that customers are delighted

by food experience. For starting restaurant, efficient staff is required which can deliver food to

customers instantly and with full dedication. For this purpose, staff is hired by manager on

behalf of organisation. Key factor in firm is try to synchronise and coordinates team effort for

achievement of objectives of organisation.

Vision-

The vision of company is to increased its market share and to broaden customer base. For

1

Organisation is required to make its budget so that it may keep on track of its activities by

making budget forecast and analysing actual results and finding out variances if any (Fullerton,

Kennedy and Widener, 2014). The enclosed report is based on new company which is starting its

venture in food sector. As such, management accounting should be sound enough for effective

results.

TASK 1

Introduce a business and its product. Also prepare a cost card to calculate per unit cost of stated

product

Report

To:

From: Angel Syndicate

Subject: Introducing a restaurant

Mission-

The company is introducing the business of pizza restaurant. Foe demand fulfilment of

customers, it is launching its new business. Pizza has been preferred by almost of all age

groups. It will be help for company to establish and provides pizzas to public for their

satisfaction. It is required that company should be efficient enough to provide services to

customers. The mission of company is to establish brand image in front of the public so that it

may enhance them and satisfy them. It is required that organisation should deliver quality of

product to customers as when quality is not achieved, products fail. As a result, brand image is

lost. For ensuring proper quality, standards should be set by it so that customers are delighted

by food experience. For starting restaurant, efficient staff is required which can deliver food to

customers instantly and with full dedication. For this purpose, staff is hired by manager on

behalf of organisation. Key factor in firm is try to synchronise and coordinates team effort for

achievement of objectives of organisation.

Vision-

The vision of company is to increased its market share and to broaden customer base. For

1

increasing market share, it is required that it deliver product as per quality standards. Quality

management should be efficient so that customers are delighted with by the experience. Market

share can also be increased by implementing competitive strategies in ahead of competitors so

that organisation may lead ahead of them. By framing competitive strategies, it may flourish in

the market which ultimately maximises its market share. Next vision is to maximise customer

base which may be achieved by attracting customers by various schemes and discounts on food

products. This strategy can make speedy sales and eventually leads to increase in customer

base. Customer are delighted and satisfied by providing quality pizzas at lowest pricers and

which makes effective sales of restaurant.

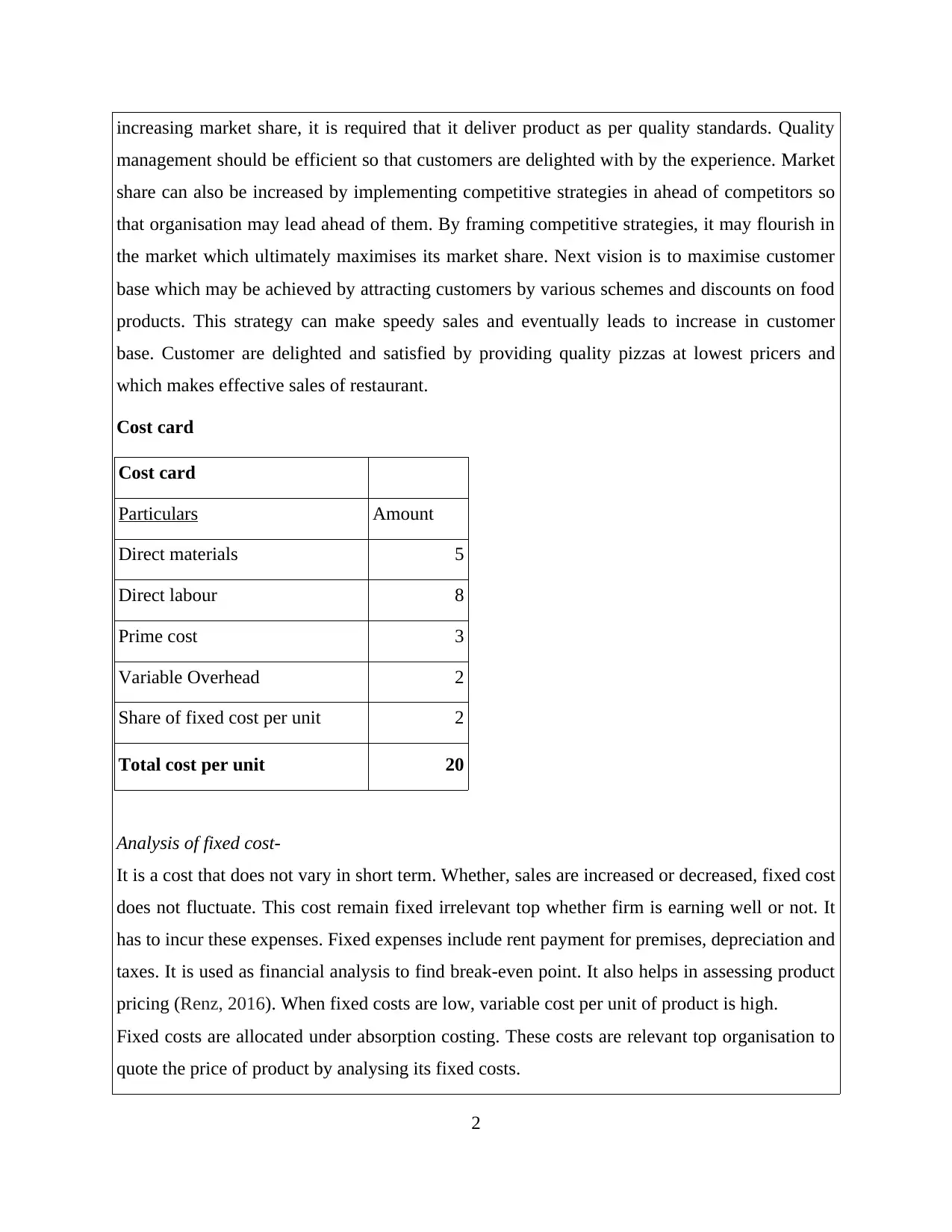

Cost card

Cost card

Particulars Amount

Direct materials 5

Direct labour 8

Prime cost 3

Variable Overhead 2

Share of fixed cost per unit 2

Total cost per unit 20

Analysis of fixed cost-

It is a cost that does not vary in short term. Whether, sales are increased or decreased, fixed cost

does not fluctuate. This cost remain fixed irrelevant top whether firm is earning well or not. It

has to incur these expenses. Fixed expenses include rent payment for premises, depreciation and

taxes. It is used as financial analysis to find break-even point. It also helps in assessing product

pricing (Renz, 2016). When fixed costs are low, variable cost per unit of product is high.

Fixed costs are allocated under absorption costing. These costs are relevant top organisation to

quote the price of product by analysing its fixed costs.

2

management should be efficient so that customers are delighted with by the experience. Market

share can also be increased by implementing competitive strategies in ahead of competitors so

that organisation may lead ahead of them. By framing competitive strategies, it may flourish in

the market which ultimately maximises its market share. Next vision is to maximise customer

base which may be achieved by attracting customers by various schemes and discounts on food

products. This strategy can make speedy sales and eventually leads to increase in customer

base. Customer are delighted and satisfied by providing quality pizzas at lowest pricers and

which makes effective sales of restaurant.

Cost card

Cost card

Particulars Amount

Direct materials 5

Direct labour 8

Prime cost 3

Variable Overhead 2

Share of fixed cost per unit 2

Total cost per unit 20

Analysis of fixed cost-

It is a cost that does not vary in short term. Whether, sales are increased or decreased, fixed cost

does not fluctuate. This cost remain fixed irrelevant top whether firm is earning well or not. It

has to incur these expenses. Fixed expenses include rent payment for premises, depreciation and

taxes. It is used as financial analysis to find break-even point. It also helps in assessing product

pricing (Renz, 2016). When fixed costs are low, variable cost per unit of product is high.

Fixed costs are allocated under absorption costing. These costs are relevant top organisation to

quote the price of product by analysing its fixed costs.

2

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

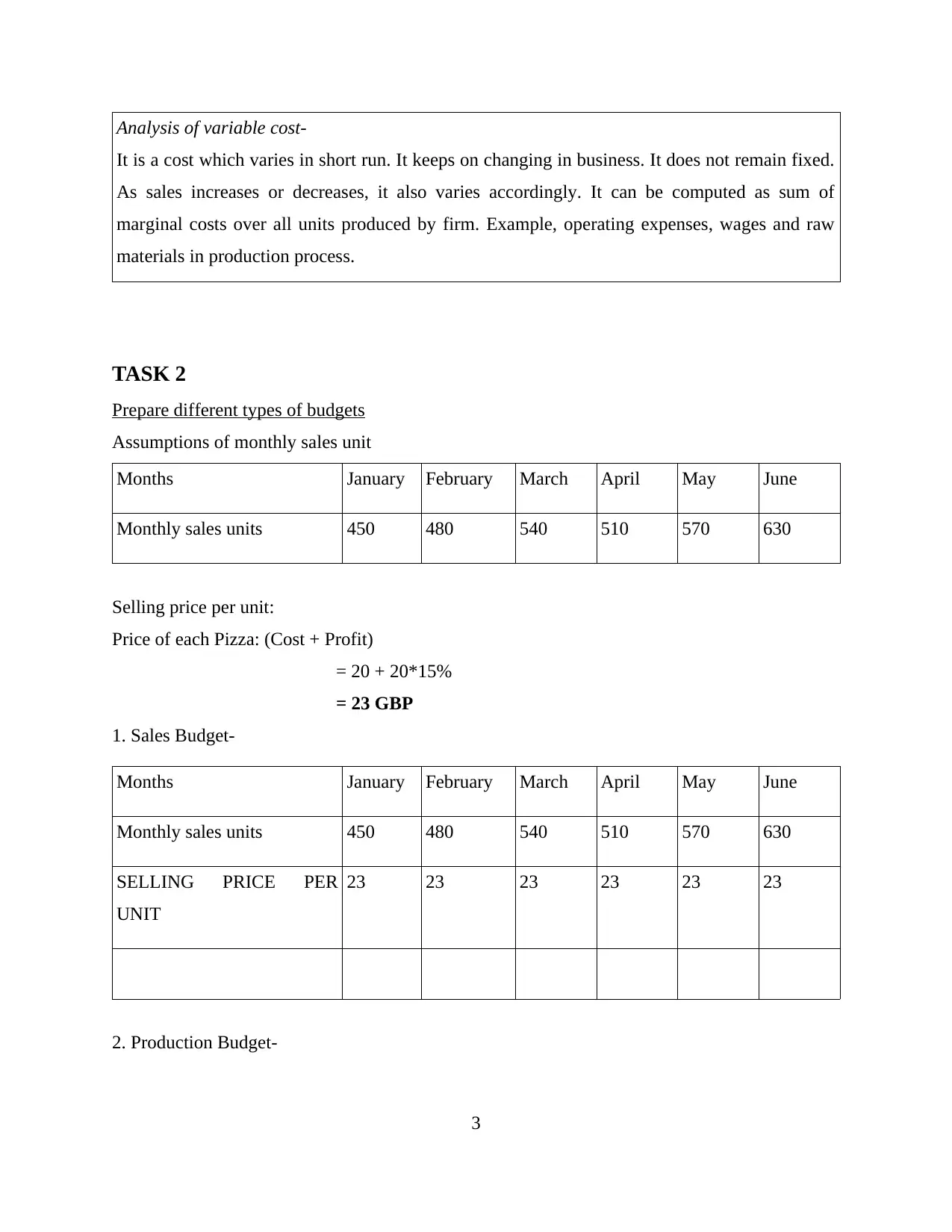

Analysis of variable cost-

It is a cost which varies in short run. It keeps on changing in business. It does not remain fixed.

As sales increases or decreases, it also varies accordingly. It can be computed as sum of

marginal costs over all units produced by firm. Example, operating expenses, wages and raw

materials in production process.

TASK 2

Prepare different types of budgets

Assumptions of monthly sales unit

Months January February March April May June

Monthly sales units 450 480 540 510 570 630

Selling price per unit:

Price of each Pizza: (Cost + Profit)

= 20 + 20*15%

= 23 GBP

1. Sales Budget-

Months January February March April May June

Monthly sales units 450 480 540 510 570 630

SELLING PRICE PER

UNIT

23 23 23 23 23 23

2. Production Budget-

3

It is a cost which varies in short run. It keeps on changing in business. It does not remain fixed.

As sales increases or decreases, it also varies accordingly. It can be computed as sum of

marginal costs over all units produced by firm. Example, operating expenses, wages and raw

materials in production process.

TASK 2

Prepare different types of budgets

Assumptions of monthly sales unit

Months January February March April May June

Monthly sales units 450 480 540 510 570 630

Selling price per unit:

Price of each Pizza: (Cost + Profit)

= 20 + 20*15%

= 23 GBP

1. Sales Budget-

Months January February March April May June

Monthly sales units 450 480 540 510 570 630

SELLING PRICE PER

UNIT

23 23 23 23 23 23

2. Production Budget-

3

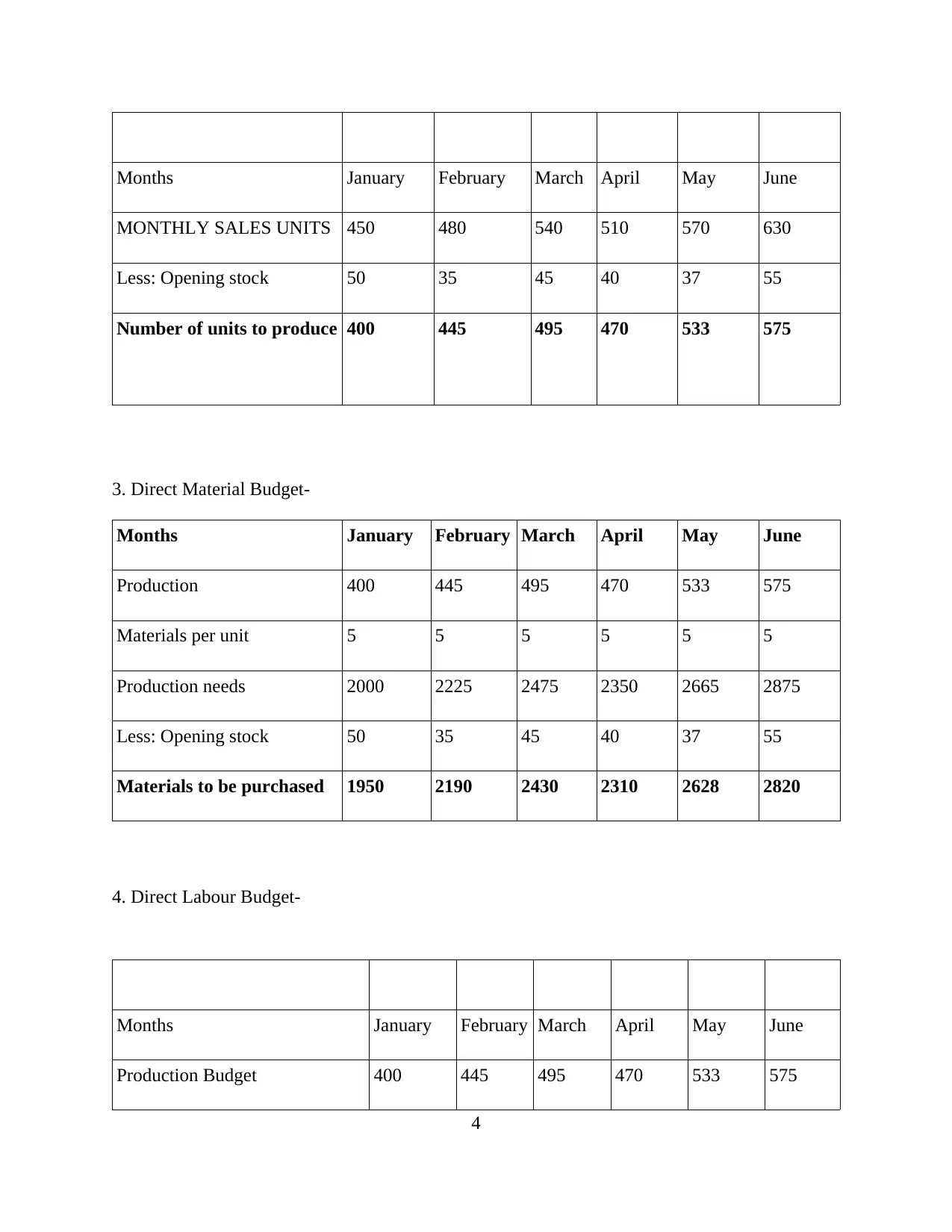

Months January February March April May June

MONTHLY SALES UNITS 450 480 540 510 570 630

Less: Opening stock 50 35 45 40 37 55

Number of units to produce 400 445 495 470 533 575

3. Direct Material Budget-

Months January February March April May June

Production 400 445 495 470 533 575

Materials per unit 5 5 5 5 5 5

Production needs 2000 2225 2475 2350 2665 2875

Less: Opening stock 50 35 45 40 37 55

Materials to be purchased 1950 2190 2430 2310 2628 2820

4. Direct Labour Budget-

Months January February March April May June

Production Budget 400 445 495 470 533 575

4

MONTHLY SALES UNITS 450 480 540 510 570 630

Less: Opening stock 50 35 45 40 37 55

Number of units to produce 400 445 495 470 533 575

3. Direct Material Budget-

Months January February March April May June

Production 400 445 495 470 533 575

Materials per unit 5 5 5 5 5 5

Production needs 2000 2225 2475 2350 2665 2875

Less: Opening stock 50 35 45 40 37 55

Materials to be purchased 1950 2190 2430 2310 2628 2820

4. Direct Labour Budget-

Months January February March April May June

Production Budget 400 445 495 470 533 575

4

Direct labour hours per unit 1 1 1 1 1 1

Total direct labour needed 400 445 495 470 533 575

Direct labour cost per hour 8 8 8 8 8 8

Cost of labour 3200 3560 3960 3760 4264 4600

5. Variable Overhead Budget-

Months January February March April May June

Budgeted Production 450 480 540 510 570 630

Variable Overhead 2 2 2 2 2 2

Budgeted Variable Overhead 900 960 1080 1020 1140 1260

6. Fixed Overhead Budget-

Months January February March April May June

Budgeted Production 450 480 540 510 570 630

Fixed Overhead 2 2 2 2 2 2

Budgeted Fixed Overhead 900 960 1080 1020 1140 1260

7. Share Capital Budget-

Months January February March April May June

5

Total direct labour needed 400 445 495 470 533 575

Direct labour cost per hour 8 8 8 8 8 8

Cost of labour 3200 3560 3960 3760 4264 4600

5. Variable Overhead Budget-

Months January February March April May June

Budgeted Production 450 480 540 510 570 630

Variable Overhead 2 2 2 2 2 2

Budgeted Variable Overhead 900 960 1080 1020 1140 1260

6. Fixed Overhead Budget-

Months January February March April May June

Budgeted Production 450 480 540 510 570 630

Fixed Overhead 2 2 2 2 2 2

Budgeted Fixed Overhead 900 960 1080 1020 1140 1260

7. Share Capital Budget-

Months January February March April May June

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

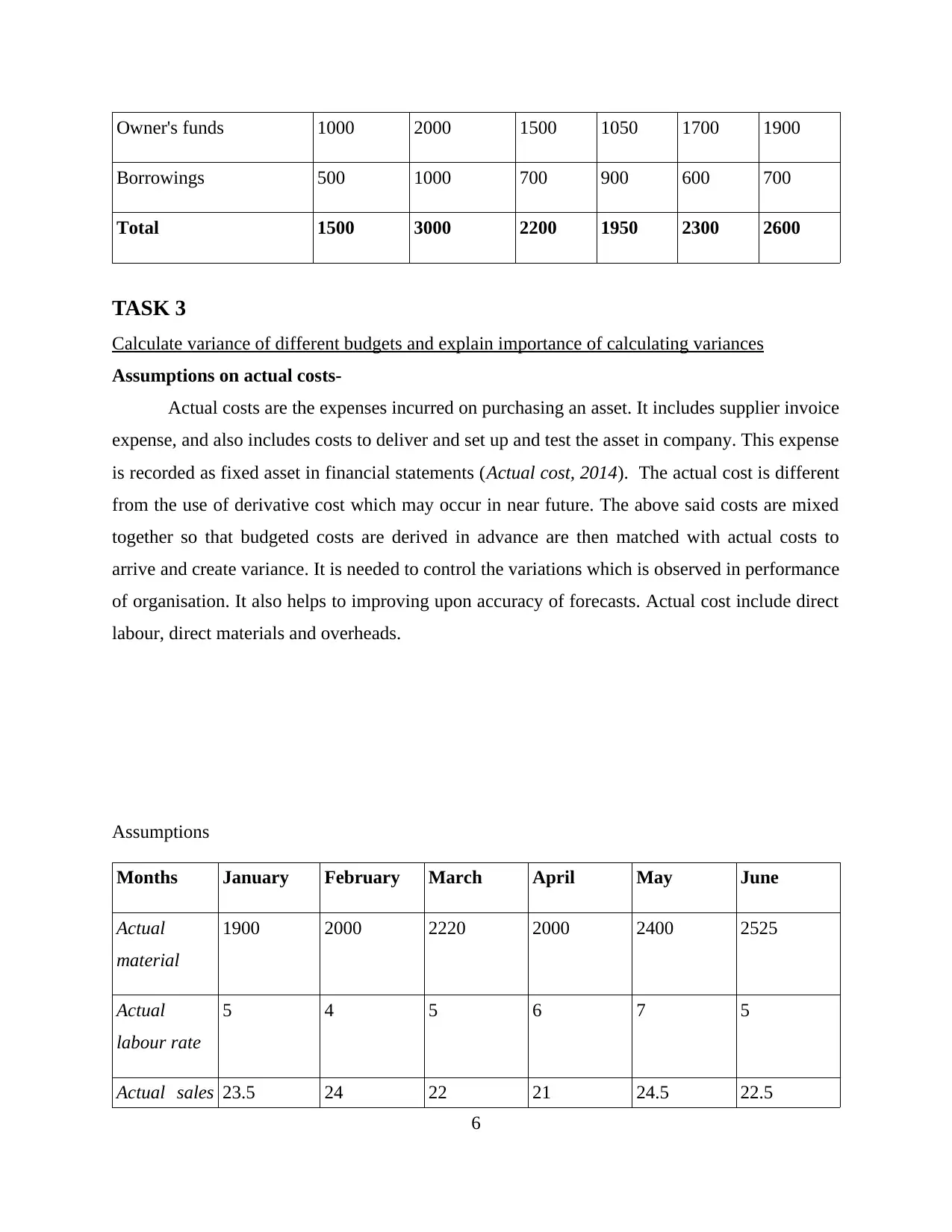

Owner's funds 1000 2000 1500 1050 1700 1900

Borrowings 500 1000 700 900 600 700

Total 1500 3000 2200 1950 2300 2600

TASK 3

Calculate variance of different budgets and explain importance of calculating variances

Assumptions on actual costs-

Actual costs are the expenses incurred on purchasing an asset. It includes supplier invoice

expense, and also includes costs to deliver and set up and test the asset in company. This expense

is recorded as fixed asset in financial statements (Actual cost, 2014). The actual cost is different

from the use of derivative cost which may occur in near future. The above said costs are mixed

together so that budgeted costs are derived in advance are then matched with actual costs to

arrive and create variance. It is needed to control the variations which is observed in performance

of organisation. It also helps to improving upon accuracy of forecasts. Actual cost include direct

labour, direct materials and overheads.

Assumptions

Months January February March April May June

Actual

material

1900 2000 2220 2000 2400 2525

Actual

labour rate

5 4 5 6 7 5

Actual sales 23.5 24 22 21 24.5 22.5

6

Borrowings 500 1000 700 900 600 700

Total 1500 3000 2200 1950 2300 2600

TASK 3

Calculate variance of different budgets and explain importance of calculating variances

Assumptions on actual costs-

Actual costs are the expenses incurred on purchasing an asset. It includes supplier invoice

expense, and also includes costs to deliver and set up and test the asset in company. This expense

is recorded as fixed asset in financial statements (Actual cost, 2014). The actual cost is different

from the use of derivative cost which may occur in near future. The above said costs are mixed

together so that budgeted costs are derived in advance are then matched with actual costs to

arrive and create variance. It is needed to control the variations which is observed in performance

of organisation. It also helps to improving upon accuracy of forecasts. Actual cost include direct

labour, direct materials and overheads.

Assumptions

Months January February March April May June

Actual

material

1900 2000 2220 2000 2400 2525

Actual

labour rate

5 4 5 6 7 5

Actual sales 23.5 24 22 21 24.5 22.5

6

price

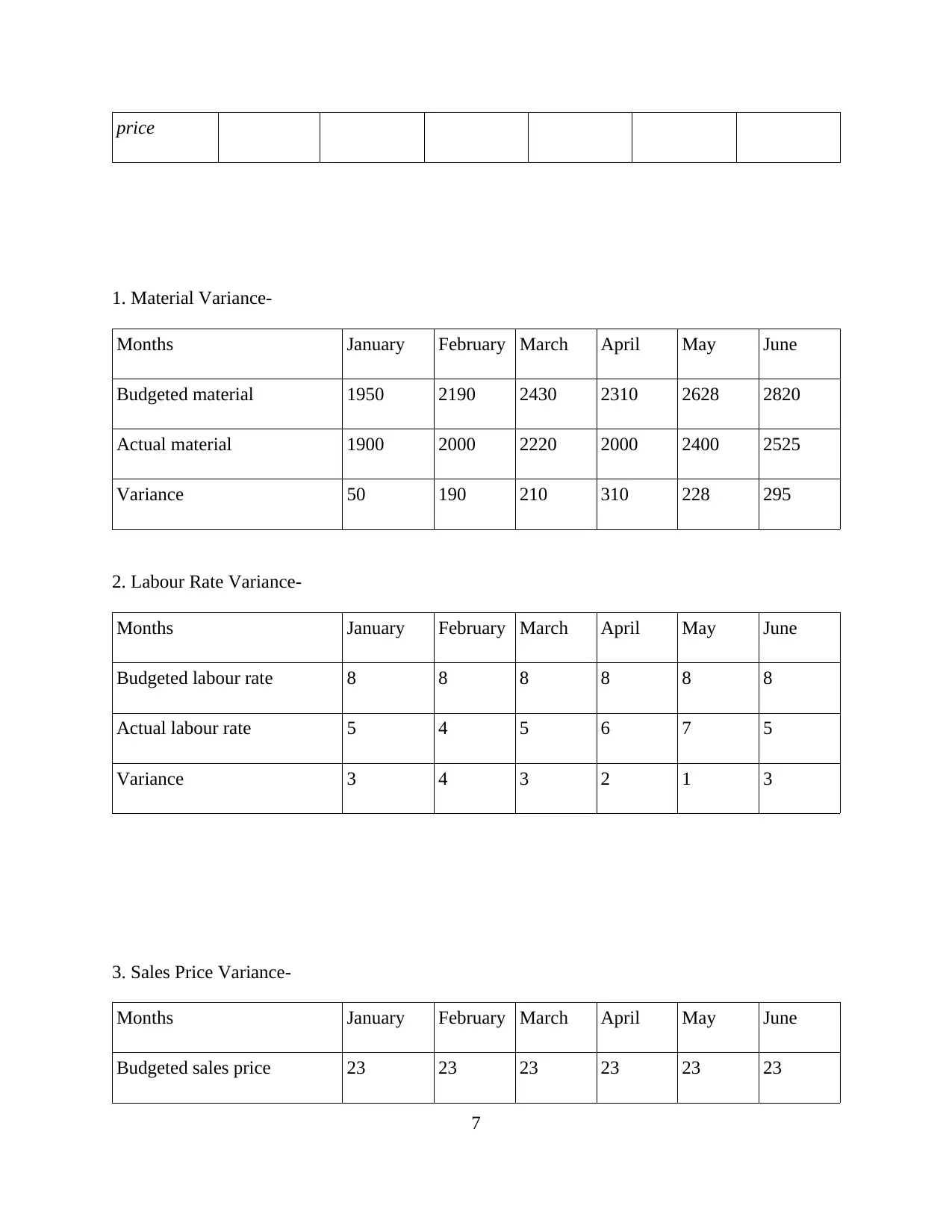

1. Material Variance-

Months January February March April May June

Budgeted material 1950 2190 2430 2310 2628 2820

Actual material 1900 2000 2220 2000 2400 2525

Variance 50 190 210 310 228 295

2. Labour Rate Variance-

Months January February March April May June

Budgeted labour rate 8 8 8 8 8 8

Actual labour rate 5 4 5 6 7 5

Variance 3 4 3 2 1 3

3. Sales Price Variance-

Months January February March April May June

Budgeted sales price 23 23 23 23 23 23

7

1. Material Variance-

Months January February March April May June

Budgeted material 1950 2190 2430 2310 2628 2820

Actual material 1900 2000 2220 2000 2400 2525

Variance 50 190 210 310 228 295

2. Labour Rate Variance-

Months January February March April May June

Budgeted labour rate 8 8 8 8 8 8

Actual labour rate 5 4 5 6 7 5

Variance 3 4 3 2 1 3

3. Sales Price Variance-

Months January February March April May June

Budgeted sales price 23 23 23 23 23 23

7

Actual sales price 23.5 24 25 23.5 24.5 22.5

Variance 0.5 1 3 0.5 1.5 -0.5

Discussion of variance-

Variance analysis are important in organisation as it determines and assess the deviations

between actual and budget results. Variance analysis is vital as firm is able to make improvement

in its activities so that it may get corrective action in timely manner. The sales price variance

which is highlighted in above table represents that company may able to have effective growth as

it making good sales then it had made budgeted sales (Grabner and Moers, 2013). It is

performing good in delighting customers. Next variance is labour rate variance which states that

labour efficiency is not up to mark as they are taking more time to accomplish the tasks which

requires lot of time to complete the work. Also, another variance is material variance which

highlight material of company which is used in production. It also showing variances in

budgeted and actual materials as it was not provided timely from suppliers. Variance helps

organisation to improve their activities so that it may impart good performance. This is required

so that production is done in timely manner and it may fulfil demands and needs of consumers

by taking corrective action.

Importance of variance-

Variance is important part of organisation. It measures the differences between actual and

budgeted results. It is very vital as evaluates the performance of organisation so that it can

analyse the difference why the deviations has arises (Baldvinsdottir, Mitchell and Nørreklit,

2010). By assessing the difference, organisation can improve upon the errors or defects which

has aroused in actual results. It helps firm to improve upon its functioning in that way so it may

accomplish its set targets in effective manner. Also, sometimes budgets are not prepared properly

as a result, it may show variances. So, budgets should be prepared adequately so that firm may

forecast its activities in effectual way.

In simple words, variance analysis is a way to identify causes of deviation that has been

observed in actual and budgeted targets. It makes firm effective as it works upon such deviations

to improve its working. Also, variance means that income and expenses of current year are

8

Variance 0.5 1 3 0.5 1.5 -0.5

Discussion of variance-

Variance analysis are important in organisation as it determines and assess the deviations

between actual and budget results. Variance analysis is vital as firm is able to make improvement

in its activities so that it may get corrective action in timely manner. The sales price variance

which is highlighted in above table represents that company may able to have effective growth as

it making good sales then it had made budgeted sales (Grabner and Moers, 2013). It is

performing good in delighting customers. Next variance is labour rate variance which states that

labour efficiency is not up to mark as they are taking more time to accomplish the tasks which

requires lot of time to complete the work. Also, another variance is material variance which

highlight material of company which is used in production. It also showing variances in

budgeted and actual materials as it was not provided timely from suppliers. Variance helps

organisation to improve their activities so that it may impart good performance. This is required

so that production is done in timely manner and it may fulfil demands and needs of consumers

by taking corrective action.

Importance of variance-

Variance is important part of organisation. It measures the differences between actual and

budgeted results. It is very vital as evaluates the performance of organisation so that it can

analyse the difference why the deviations has arises (Baldvinsdottir, Mitchell and Nørreklit,

2010). By assessing the difference, organisation can improve upon the errors or defects which

has aroused in actual results. It helps firm to improve upon its functioning in that way so it may

accomplish its set targets in effective manner. Also, sometimes budgets are not prepared properly

as a result, it may show variances. So, budgets should be prepared adequately so that firm may

forecast its activities in effectual way.

In simple words, variance analysis is a way to identify causes of deviation that has been

observed in actual and budgeted targets. It makes firm effective as it works upon such deviations

to improve its working. Also, variance means that income and expenses of current year are

8

Secure Best Marks with AI Grader

Need help grading? Try our AI Grader for instant feedback on your assignments.

deviated from the budgeted values. It analyses to understand that why fluctuations are arrived

and what can be do to reduce it.

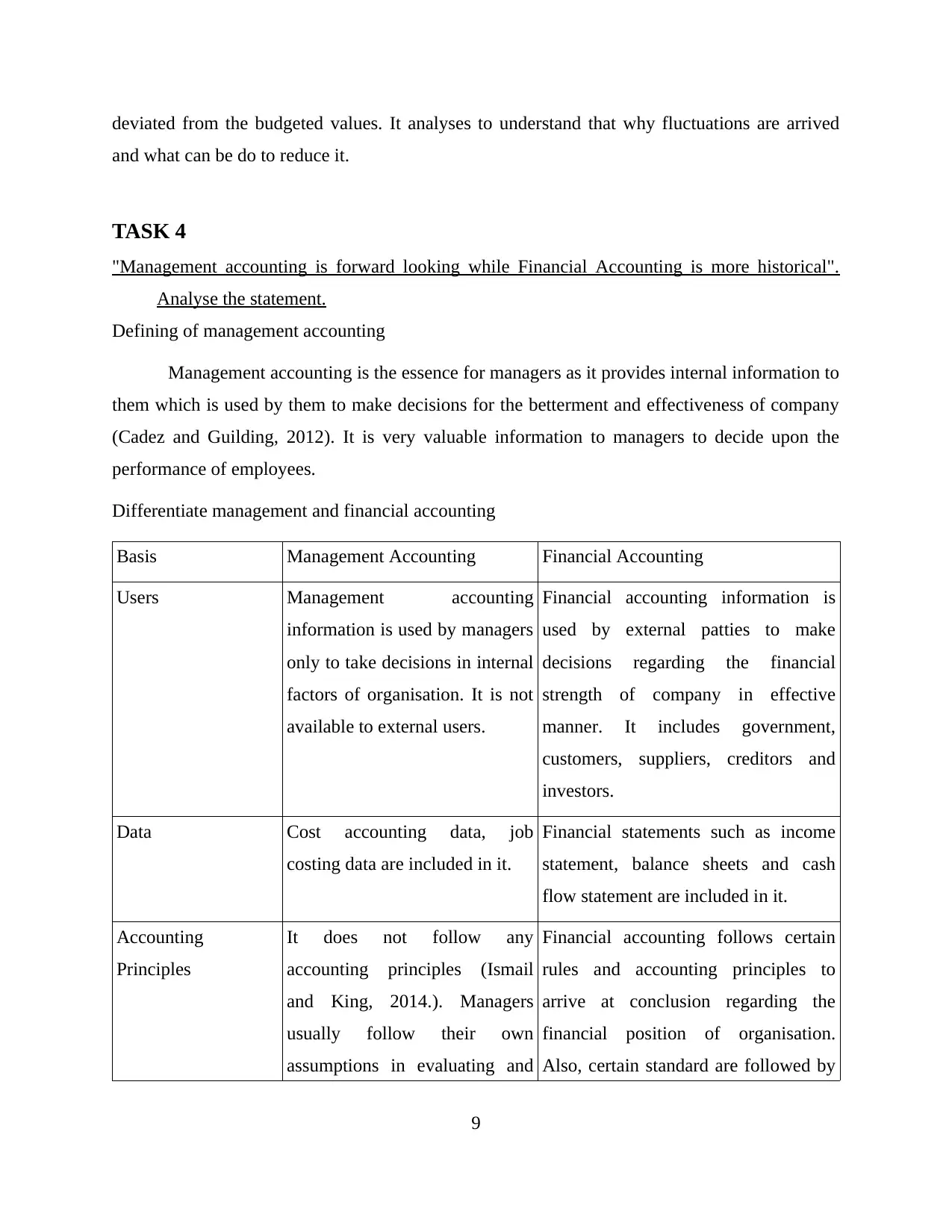

TASK 4

"Management accounting is forward looking while Financial Accounting is more historical".

Analyse the statement.

Defining of management accounting

Management accounting is the essence for managers as it provides internal information to

them which is used by them to make decisions for the betterment and effectiveness of company

(Cadez and Guilding, 2012). It is very valuable information to managers to decide upon the

performance of employees.

Differentiate management and financial accounting

Basis Management Accounting Financial Accounting

Users Management accounting

information is used by managers

only to take decisions in internal

factors of organisation. It is not

available to external users.

Financial accounting information is

used by external patties to make

decisions regarding the financial

strength of company in effective

manner. It includes government,

customers, suppliers, creditors and

investors.

Data Cost accounting data, job

costing data are included in it.

Financial statements such as income

statement, balance sheets and cash

flow statement are included in it.

Accounting

Principles

It does not follow any

accounting principles (Ismail

and King, 2014.). Managers

usually follow their own

assumptions in evaluating and

Financial accounting follows certain

rules and accounting principles to

arrive at conclusion regarding the

financial position of organisation.

Also, certain standard are followed by

9

and what can be do to reduce it.

TASK 4

"Management accounting is forward looking while Financial Accounting is more historical".

Analyse the statement.

Defining of management accounting

Management accounting is the essence for managers as it provides internal information to

them which is used by them to make decisions for the betterment and effectiveness of company

(Cadez and Guilding, 2012). It is very valuable information to managers to decide upon the

performance of employees.

Differentiate management and financial accounting

Basis Management Accounting Financial Accounting

Users Management accounting

information is used by managers

only to take decisions in internal

factors of organisation. It is not

available to external users.

Financial accounting information is

used by external patties to make

decisions regarding the financial

strength of company in effective

manner. It includes government,

customers, suppliers, creditors and

investors.

Data Cost accounting data, job

costing data are included in it.

Financial statements such as income

statement, balance sheets and cash

flow statement are included in it.

Accounting

Principles

It does not follow any

accounting principles (Ismail

and King, 2014.). Managers

usually follow their own

assumptions in evaluating and

Financial accounting follows certain

rules and accounting principles to

arrive at conclusion regarding the

financial position of organisation.

Also, certain standard are followed by

9

assessing the information. it. Accounting principles include going

concern, money measurement and

many more/ It guides accountant to

arrive at conclusion and accomplish

accounting.

Purpose Purpose of management

accounting is to impart internal

information to managers so that

if any discrepancies are

observed, they may rectify it.

Also, internal decisions are

made by them using this

information (Cooper, Ezzamel

and Qu, 2017).

It is used for purpose of providing

information to the external users to

take decisions towards company.

Auditing It does not require auditing. Financial accounting requires auditing.

Organisation appoints an auditor to

assess the fairness of financial

statements of organisation.

CONCLUSION

Hereby it can be concluded that organisation has to make certain strategies to flourish in

the market. Also, it takes certain information from management accounting to accomplish its set

targets. The variance also play essential role in improving effectiveness of organisation. Sales

variances, material variances and labour rate variances are important to organisation so that it

may deliver its best to customers by improving its deviations. As such, for new business to

flourish, financial stability is very vital.

10

concern, money measurement and

many more/ It guides accountant to

arrive at conclusion and accomplish

accounting.

Purpose Purpose of management

accounting is to impart internal

information to managers so that

if any discrepancies are

observed, they may rectify it.

Also, internal decisions are

made by them using this

information (Cooper, Ezzamel

and Qu, 2017).

It is used for purpose of providing

information to the external users to

take decisions towards company.

Auditing It does not require auditing. Financial accounting requires auditing.

Organisation appoints an auditor to

assess the fairness of financial

statements of organisation.

CONCLUSION

Hereby it can be concluded that organisation has to make certain strategies to flourish in

the market. Also, it takes certain information from management accounting to accomplish its set

targets. The variance also play essential role in improving effectiveness of organisation. Sales

variances, material variances and labour rate variances are important to organisation so that it

may deliver its best to customers by improving its deviations. As such, for new business to

flourish, financial stability is very vital.

10

REFERENCES

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

11

Books and Journals

Baldvinsdottir, G., Mitchell, F. and Nørreklit, H., 2010. Issues in the relationship between theory

and practice in management accounting. Management Accounting Research. 21(2).

pp.79-82.

11

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

© 2024 | Zucol Services PVT LTD | All rights reserved.