Management Accounting Report for The Ledbury Restaurant, UK

VerifiedAdded on 2020/06/03

|15

|4885

|251

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive analysis of various systems and methodologies. It begins with an explanation of different management accounting schemes, including cost accounting, job costing, and process costing, highlighting their significance and applications within a business context, specifically referencing The Ledbury Restaurant. The report then explores different management accounting reporting methods, such as budget reports, job cost reports, income statements, and accounts receivable reporting, evaluating their advantages and disadvantages. Furthermore, it examines absorption and marginal costing methods, providing a comparative analysis of their impact on profitability. The report concludes by discussing the adoption of management accounting schemes to address financial problems, offering insights into how these systems can be leveraged to improve decision-making and operational efficiency. The report serves as a valuable resource for understanding and applying management accounting principles in real-world scenarios.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1.Explanation of administration explanation and essential necessitate of different

administration accounting schemes.............................................................................................1

P.2.Various methods utilised for administration accounting coverage.......................................3

TASK 2............................................................................................................................................5

P.3.Absorption and marginal costing method.............................................................................5

TASK 3............................................................................................................................................8

P.4.Advantage and disadvantage of using various planning instrument that can be utilised for

fund control at workplace............................................................................................................8

P.5.Adoption of administration accounting scheme to answer to financial problems..............10

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P.1.Explanation of administration explanation and essential necessitate of different

administration accounting schemes.............................................................................................1

P.2.Various methods utilised for administration accounting coverage.......................................3

TASK 2............................................................................................................................................5

P.3.Absorption and marginal costing method.............................................................................5

TASK 3............................................................................................................................................8

P.4.Advantage and disadvantage of using various planning instrument that can be utilised for

fund control at workplace............................................................................................................8

P.5.Adoption of administration accounting scheme to answer to financial problems..............10

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting is the one of the field that have vast substance for the firms. It

can be discovered that it assists company in measuring its operational efficiency. In the recent

report different management accounting systems are explained in detail and along with this

reporting modes are discussed in investigation study. In mediate part of the report, marginal and

absorption costing is done and results are interpreted. At end if the report, different systems that

can be used to respond to financial is sues are discussed briefly. Through these research study is

passed and completed.

TASK 1

P.1.Explanation of administration explanation and essential necessitate of different

administration accounting schemes

To

The Director of The Ledbury Restaurant, London, UK. Date: 15th january 2018

Sub: Management accounting systems adoption and their significance

Management accounting is the field that helps company in estimating internal efficiency that is

in the business operation. Normally, corporations operating in manufacturing field aimed to

control cost at workplace. Focus need to be made on improving internal efficiency of the

business operations so that cost remain below ascertained standard extent(B Douglas Clinton

CMA, and CFM, 2012). Numbers of tools and techniques are present in the management

accounting that help firm to compare its performance against set criterion and recognising fields

where innovation require to be done in business operation. Several sorts of approaches like

variance analysis and budget etc. are accessible in mentioned discipline that helps managers in

making hard core business decision whenever required. All these approaches have done due

importance for the company because they help companies in working in right direction in

legitimate manner. Management accounting method have due significant with respect to

application of these methods. This is because management accounting system reflects relevant

manner in which data, information or facts could be stored in books of accounts. It is the

information that is produced by system which assists corporation in obtaining several results on

application of these approaches at workplace. Different management accounting system that re

available of corporations are give below: Cost accounting system: Cost accounting system is one of the most essential system that

1

Management accounting is the one of the field that have vast substance for the firms. It

can be discovered that it assists company in measuring its operational efficiency. In the recent

report different management accounting systems are explained in detail and along with this

reporting modes are discussed in investigation study. In mediate part of the report, marginal and

absorption costing is done and results are interpreted. At end if the report, different systems that

can be used to respond to financial is sues are discussed briefly. Through these research study is

passed and completed.

TASK 1

P.1.Explanation of administration explanation and essential necessitate of different

administration accounting schemes

To

The Director of The Ledbury Restaurant, London, UK. Date: 15th january 2018

Sub: Management accounting systems adoption and their significance

Management accounting is the field that helps company in estimating internal efficiency that is

in the business operation. Normally, corporations operating in manufacturing field aimed to

control cost at workplace. Focus need to be made on improving internal efficiency of the

business operations so that cost remain below ascertained standard extent(B Douglas Clinton

CMA, and CFM, 2012). Numbers of tools and techniques are present in the management

accounting that help firm to compare its performance against set criterion and recognising fields

where innovation require to be done in business operation. Several sorts of approaches like

variance analysis and budget etc. are accessible in mentioned discipline that helps managers in

making hard core business decision whenever required. All these approaches have done due

importance for the company because they help companies in working in right direction in

legitimate manner. Management accounting method have due significant with respect to

application of these methods. This is because management accounting system reflects relevant

manner in which data, information or facts could be stored in books of accounts. It is the

information that is produced by system which assists corporation in obtaining several results on

application of these approaches at workplace. Different management accounting system that re

available of corporations are give below: Cost accounting system: Cost accounting system is one of the most essential system that

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

is usually used by the most of the business corporations. In this system usually, costs or

expenses are recorded on basis of fixed expenses, variable expenses and semi variable

expenses(Abdel-Kader, ed., 2011). Nature of all these expenses is totally different from

each other. It could be seen that in this accounting method, all expenses are recorded in

theses mentioned class. Number of advantages are connected with the concerned

accounting system because on the basis of obtained records, managers easily find out

that how much amount they spend on fixed, variable and semi-variable class. This assist

them in preparing a plan about cost control in the business and making adjustment in it

so that cost reduction task could be accomplish in the company. Thus, it can be said that

there is huge significance of cost accounting systems for the companies. The Ledbury

Restaurant can make use of this accounting system because this would assist it in

tracking rate at which variable disbursal are elevating in the company and steps required

to be taken to manage huge situation. Operational efficiency can be raised in the firm by

working on inputs that are furnished by the accounting methodology to the restaurant. Job costing systems: Job costing system is another methodology that is used by those

companies specially that re operating their business in manufacturing system. Several

times, companies have to acquire customised products in large amount for their clients.

Due to various specification obviously, costing would also be different and due to this

reason, it is very important to do costing of products separately(.Bebbington, Unerman,

and O'Dwyer, eds., 2014). Job costing technique assists corporations in accomplishing

its desired targets and under this, separate accounts books are made for each product line

and different form of expenses are recorded in them. It could be said that job costing

procedure is more suitable for the companies that re operating multiple product lines in

their business. The Ledbury Restaurant is one of the growing restaurant in the UK and

in short duration of time period, it gained huge popularity. It could be ascertained that in

this restaurant, broad variety of food products are served to the customers across

different price range. It is very essential to do accounting of expenses in these products

line separately so that better overview can be obtained about their costing and actions

can be taken in right path to make sure that expenses will remain in control in business.

Process costings: This is also one of the methodology that is made by many companies

because it helps them in doing coasting of product lines more accurately. In method

2

expenses are recorded on basis of fixed expenses, variable expenses and semi variable

expenses(Abdel-Kader, ed., 2011). Nature of all these expenses is totally different from

each other. It could be seen that in this accounting method, all expenses are recorded in

theses mentioned class. Number of advantages are connected with the concerned

accounting system because on the basis of obtained records, managers easily find out

that how much amount they spend on fixed, variable and semi-variable class. This assist

them in preparing a plan about cost control in the business and making adjustment in it

so that cost reduction task could be accomplish in the company. Thus, it can be said that

there is huge significance of cost accounting systems for the companies. The Ledbury

Restaurant can make use of this accounting system because this would assist it in

tracking rate at which variable disbursal are elevating in the company and steps required

to be taken to manage huge situation. Operational efficiency can be raised in the firm by

working on inputs that are furnished by the accounting methodology to the restaurant. Job costing systems: Job costing system is another methodology that is used by those

companies specially that re operating their business in manufacturing system. Several

times, companies have to acquire customised products in large amount for their clients.

Due to various specification obviously, costing would also be different and due to this

reason, it is very important to do costing of products separately(.Bebbington, Unerman,

and O'Dwyer, eds., 2014). Job costing technique assists corporations in accomplishing

its desired targets and under this, separate accounts books are made for each product line

and different form of expenses are recorded in them. It could be said that job costing

procedure is more suitable for the companies that re operating multiple product lines in

their business. The Ledbury Restaurant is one of the growing restaurant in the UK and

in short duration of time period, it gained huge popularity. It could be ascertained that in

this restaurant, broad variety of food products are served to the customers across

different price range. It is very essential to do accounting of expenses in these products

line separately so that better overview can be obtained about their costing and actions

can be taken in right path to make sure that expenses will remain in control in business.

Process costings: This is also one of the methodology that is made by many companies

because it helps them in doing coasting of product lines more accurately. In method

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

costing approach, usually costing of each form is calculated and then relevant cost is

added to recognise overall cost of each product line(Boyns, and Edwards, 2013). There

are numbers of advantages of using process costing approach because under this it could

be easily find out that for which production process stage cost is raising quickly and

need control on time so that cost could be managed in the company. It could be said that

deeper information about costing of product is collected by process costing techniques

than any other costing system. If The Ledbury Restaurant does not adopt this accounting

system in its business then also there is no issue because for manufacturing dishes long

time is not needed in order of different stages. Hence, it could be said that there is wide

necessity of process costing system for the company because due to limited length of

operations it does not too much require use of process costing management accounting

system at workplace.

P.2.Various methods utilised for administration accounting coverage

There are various approaches of management accounting reporting because varied

operations are performed in the company(Callahan, Stetz, and Brooks, 2011). In these different

variety of reports, company execution is measured in different way. Different approaches of

management accounting are explained below: Budget report: In fund reporting method, there are number of items that are covered and

with regard of this, standards are given in the table. Again these standards there are

effective results that are acquiring by quantifaying business performance(Christ, 2014).

On comparison of both value, information about company performance is acquired by the

managers. Thus, this report not only assist firm in examination its own performance in

order to standard but is also assists them in finding out that in comparison to past months

how much difference comes their performance. Hence, it could be said that budget report

has due importance for the companies as it assists it in measuring performance from

multiple regions. Thus, in perfect direction company endeavors going due to usage o

budget report in the business. The Ledbury Restaurant could make use of the budget

reporting system in the company as it is very simple to set up budget and for specific

individual need not to be hired that have strong technical background. However, one

3

added to recognise overall cost of each product line(Boyns, and Edwards, 2013). There

are numbers of advantages of using process costing approach because under this it could

be easily find out that for which production process stage cost is raising quickly and

need control on time so that cost could be managed in the company. It could be said that

deeper information about costing of product is collected by process costing techniques

than any other costing system. If The Ledbury Restaurant does not adopt this accounting

system in its business then also there is no issue because for manufacturing dishes long

time is not needed in order of different stages. Hence, it could be said that there is wide

necessity of process costing system for the company because due to limited length of

operations it does not too much require use of process costing management accounting

system at workplace.

P.2.Various methods utilised for administration accounting coverage

There are various approaches of management accounting reporting because varied

operations are performed in the company(Callahan, Stetz, and Brooks, 2011). In these different

variety of reports, company execution is measured in different way. Different approaches of

management accounting are explained below: Budget report: In fund reporting method, there are number of items that are covered and

with regard of this, standards are given in the table. Again these standards there are

effective results that are acquiring by quantifaying business performance(Christ, 2014).

On comparison of both value, information about company performance is acquired by the

managers. Thus, this report not only assist firm in examination its own performance in

order to standard but is also assists them in finding out that in comparison to past months

how much difference comes their performance. Hence, it could be said that budget report

has due importance for the companies as it assists it in measuring performance from

multiple regions. Thus, in perfect direction company endeavors going due to usage o

budget report in the business. The Ledbury Restaurant could make use of the budget

reporting system in the company as it is very simple to set up budget and for specific

individual need not to be hired that have strong technical background. However, one

3

require to take care while making forecasting by approximation growth rate of sales

revenue and expenses in the firm. In terms of solve this problem, skilled person can be

given target to prepare budget for the business(Zimmerman, and Yahya-Zadeh, 2011).

Advantages are already explained above. One of the major disadvantage of using budget

report is that assuming is made in it and on the basis, standards are determined which

might be wrong in future time period. Usually, in a year prediction is made about future

time period in terms of growth rate of business and its expenses. These projections might

prove wrong for the company and in case this happened then it is possible that

corporation performance good but it is considered bad by the manager because actual

conclusion are not matching to the forecasted values. Thus, it is one of the big limitation

of budgeting process. Job cost report: It is another most essential reporting manner because under this in the

report cost for different jobs of business projects are prepared in the books and accounts.

This reporting method is utilized by most of business corporations at workplace(DRURY,

2013). In the job cost report for all product lines individually figures are calculated in

order to disbursal that are made in the business. Thus, it could be said that job cost report

gives more deep information about cost of product lines and due to this reason, most of

the companies preferred to make job cost report in the business. The Ledbury Restaurant

can also prepare job cost report for its different products lines because by using same, it

can better gain insights of its business. On single report, managers recognise that which

product line is in their control in order to expenses and which product line is out of

control in the company. Thus, it can be said that input is received about the product line

on which special attention required to be paid to increase the profitability of the

company. Income statement: Income statement is also one of the management accounting report

approach. Under this in depth of segregation of expenses is not done in the firm(Groot,

and Selto, 2013). One can see final value of all expenses that are made in the business.

Income statements of quarters are compared to each other in terms of find out that in

which fields firm perform good and in which areas it gives poor performance in the

business. Income statement also provide overall overview of the firm performance and

due to this reason, it is broadly used in the business for making decision. Only limitation

4

revenue and expenses in the firm. In terms of solve this problem, skilled person can be

given target to prepare budget for the business(Zimmerman, and Yahya-Zadeh, 2011).

Advantages are already explained above. One of the major disadvantage of using budget

report is that assuming is made in it and on the basis, standards are determined which

might be wrong in future time period. Usually, in a year prediction is made about future

time period in terms of growth rate of business and its expenses. These projections might

prove wrong for the company and in case this happened then it is possible that

corporation performance good but it is considered bad by the manager because actual

conclusion are not matching to the forecasted values. Thus, it is one of the big limitation

of budgeting process. Job cost report: It is another most essential reporting manner because under this in the

report cost for different jobs of business projects are prepared in the books and accounts.

This reporting method is utilized by most of business corporations at workplace(DRURY,

2013). In the job cost report for all product lines individually figures are calculated in

order to disbursal that are made in the business. Thus, it could be said that job cost report

gives more deep information about cost of product lines and due to this reason, most of

the companies preferred to make job cost report in the business. The Ledbury Restaurant

can also prepare job cost report for its different products lines because by using same, it

can better gain insights of its business. On single report, managers recognise that which

product line is in their control in order to expenses and which product line is out of

control in the company. Thus, it can be said that input is received about the product line

on which special attention required to be paid to increase the profitability of the

company. Income statement: Income statement is also one of the management accounting report

approach. Under this in depth of segregation of expenses is not done in the firm(Groot,

and Selto, 2013). One can see final value of all expenses that are made in the business.

Income statements of quarters are compared to each other in terms of find out that in

which fields firm perform good and in which areas it gives poor performance in the

business. Income statement also provide overall overview of the firm performance and

due to this reason, it is broadly used in the business for making decision. Only limitation

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of this method is that it does not show segregation of marketing expenses in the firm.

Hence, it cannot be recognised by looking at income statement that in marketing

expenses which firm if expenditure are highly made like expenses on social media and

public relations etc.

Account receivable reporting: Account receivable reporting is another mode of reporting

as under this approach receivables are reported in the books of accounts and firm comes

to know that how many receivables can be turned into bed debts and how much could be

encased immediately in short duration(Herzig, and et.al., 2012). Cash management

strategy is better developed on basis of account receivable reporting method. Hence, it

can be assumed that there is high necessity of account receivable system. The Ledbury

Restaurant time to time prepare account receivable reporting in its business because

usually in business there are debtors. If debtors size increase at quick rate then there are

huge chances of the cash can be locked in bed debts. It is the account receivable reporting

that helps managers in making sure that on time debt amount is recovered from debtors in

the business. It depends on the Ledbury Restaurant that by using account receivables in

which manner it manages cash inflow in the company.

TASK 2

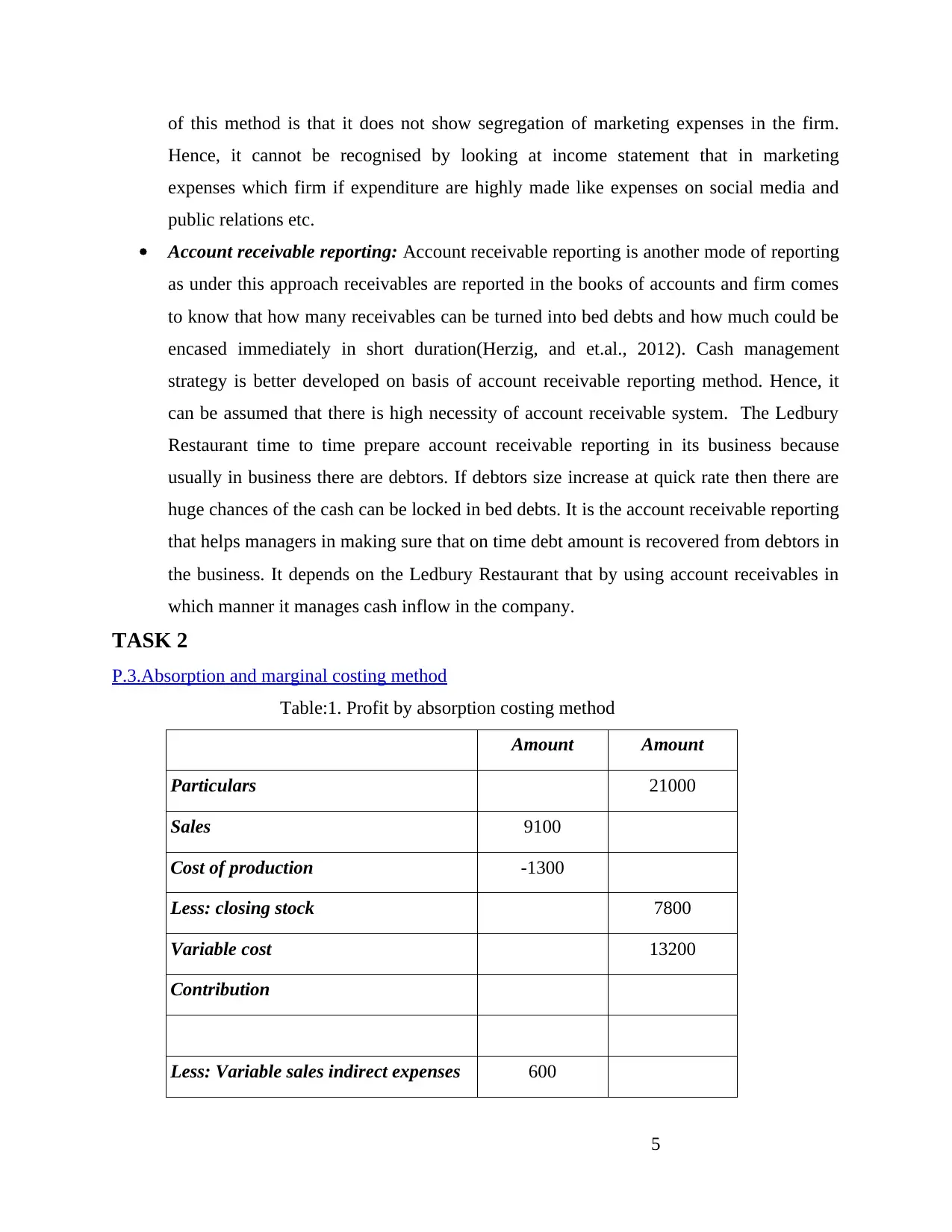

P.3.Absorption and marginal costing method

Table:1. Profit by absorption costing method

Amount Amount

Particulars 21000

Sales 9100

Cost of production -1300

Less: closing stock 7800

Variable cost 13200

Contribution

Less: Variable sales indirect expenses 600

5

Hence, it cannot be recognised by looking at income statement that in marketing

expenses which firm if expenditure are highly made like expenses on social media and

public relations etc.

Account receivable reporting: Account receivable reporting is another mode of reporting

as under this approach receivables are reported in the books of accounts and firm comes

to know that how many receivables can be turned into bed debts and how much could be

encased immediately in short duration(Herzig, and et.al., 2012). Cash management

strategy is better developed on basis of account receivable reporting method. Hence, it

can be assumed that there is high necessity of account receivable system. The Ledbury

Restaurant time to time prepare account receivable reporting in its business because

usually in business there are debtors. If debtors size increase at quick rate then there are

huge chances of the cash can be locked in bed debts. It is the account receivable reporting

that helps managers in making sure that on time debt amount is recovered from debtors in

the business. It depends on the Ledbury Restaurant that by using account receivables in

which manner it manages cash inflow in the company.

TASK 2

P.3.Absorption and marginal costing method

Table:1. Profit by absorption costing method

Amount Amount

Particulars 21000

Sales 9100

Cost of production -1300

Less: closing stock 7800

Variable cost 13200

Contribution

Less: Variable sales indirect expenses 600

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less:Fixed cost, production overhead 2000

Administration expenses 700

Selling cost 600 3900

Net profit 9300

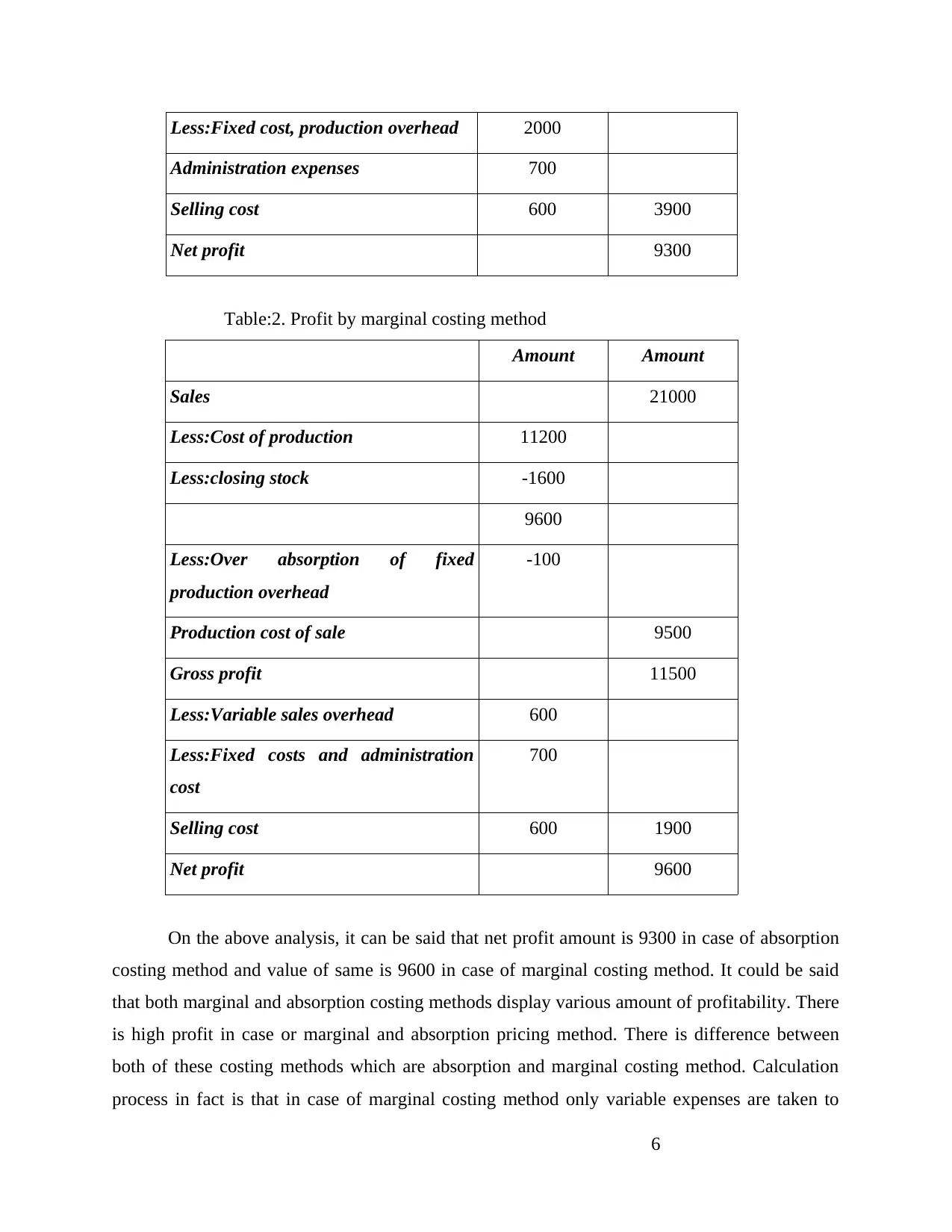

Table:2. Profit by marginal costing method

Amount Amount

Sales 21000

Less:Cost of production 11200

Less:closing stock -1600

9600

Less:Over absorption of fixed

production overhead

-100

Production cost of sale 9500

Gross profit 11500

Less:Variable sales overhead 600

Less:Fixed costs and administration

cost

700

Selling cost 600 1900

Net profit 9600

On the above analysis, it can be said that net profit amount is 9300 in case of absorption

costing method and value of same is 9600 in case of marginal costing method. It could be said

that both marginal and absorption costing methods display various amount of profitability. There

is high profit in case or marginal and absorption pricing method. There is difference between

both of these costing methods which are absorption and marginal costing method. Calculation

process in fact is that in case of marginal costing method only variable expenses are taken to

6

Administration expenses 700

Selling cost 600 3900

Net profit 9300

Table:2. Profit by marginal costing method

Amount Amount

Sales 21000

Less:Cost of production 11200

Less:closing stock -1600

9600

Less:Over absorption of fixed

production overhead

-100

Production cost of sale 9500

Gross profit 11500

Less:Variable sales overhead 600

Less:Fixed costs and administration

cost

700

Selling cost 600 1900

Net profit 9600

On the above analysis, it can be said that net profit amount is 9300 in case of absorption

costing method and value of same is 9600 in case of marginal costing method. It could be said

that both marginal and absorption costing methods display various amount of profitability. There

is high profit in case or marginal and absorption pricing method. There is difference between

both of these costing methods which are absorption and marginal costing method. Calculation

process in fact is that in case of marginal costing method only variable expenses are taken to

6

account for computing overall cost of the products(Kokubu, and Kitada, 2015). Contrary to this,

absorption costing is completely opposite and under this fixed and variable expenses both are

taken into account to do costing of product. Thus, there is little difference but it conveys big

fluctuation in results. Marginal costing operation indicate more profitability than absorption

costing method due to non-financial of fixed expenses in the business. Before further discussion

these approaches is more detailed manner it is very essential to understand fixed expenses,

variable expenses and semi variable expenses nature. Fixed expenses are those that remain

unchanged and always remain stable in the business. On the other part, variable expenses are

those that never remain same and values are changing consistently in the company. Semi

variable expenses are those in which some portion remain fixed a some remain variable. In

different combinations, these expenses are made in the firm. Usually, in the company variable

expenses are made by the corporations by higher amount. While doing calculation always one of

the question comes in front of managers that which of approach they must use in their business

for calculation. In other word it can be said that it is hard for manager to recognise whether they

should use marginal and absorption costing method in their company(Lavia López, and Hiebl,

2014). There is importance of both costing method in the corporation. In case of absorption

costing fixed expenses are taken in to consideration along with variable expenses. It can be

observed that every year purchase of fixed asset is not done that directly make na important

contribution to entire production method. If same happened truly in case of any company then in

that case, it is better to make use of marginal costing in the business because inclusion of fixed

expenses in the company does not ensure. On other hand, in case of marginal costing one thing

can be considered which is that even fixed expenses are not incurred directly in relation to

production process it is the cost that is incurred in the firm and business have to cover that cost

out of cash flows. From this point of view if condition is taken into consideration then inclusion

of fixed expenses in the firm seems right. Thus, it can be said that both costing method must be

used in the firm. There is benefit of using this strategy because if marginal costing is only used

then in that case managers can easily recognise that what amount of profit is earned if only those

expenses are taken into consideration that are heavily contributing to production process. On

other hand, if absorption costing is used then it id recognised that how much profit is earned if

both expenses are taken into the account(ainun Tuanmat, and Smith, 2011). Hence, by doing so

effect of these expenses on company revenue is calculated and it can be said that analysis help

7

absorption costing is completely opposite and under this fixed and variable expenses both are

taken into account to do costing of product. Thus, there is little difference but it conveys big

fluctuation in results. Marginal costing operation indicate more profitability than absorption

costing method due to non-financial of fixed expenses in the business. Before further discussion

these approaches is more detailed manner it is very essential to understand fixed expenses,

variable expenses and semi variable expenses nature. Fixed expenses are those that remain

unchanged and always remain stable in the business. On the other part, variable expenses are

those that never remain same and values are changing consistently in the company. Semi

variable expenses are those in which some portion remain fixed a some remain variable. In

different combinations, these expenses are made in the firm. Usually, in the company variable

expenses are made by the corporations by higher amount. While doing calculation always one of

the question comes in front of managers that which of approach they must use in their business

for calculation. In other word it can be said that it is hard for manager to recognise whether they

should use marginal and absorption costing method in their company(Lavia López, and Hiebl,

2014). There is importance of both costing method in the corporation. In case of absorption

costing fixed expenses are taken in to consideration along with variable expenses. It can be

observed that every year purchase of fixed asset is not done that directly make na important

contribution to entire production method. If same happened truly in case of any company then in

that case, it is better to make use of marginal costing in the business because inclusion of fixed

expenses in the company does not ensure. On other hand, in case of marginal costing one thing

can be considered which is that even fixed expenses are not incurred directly in relation to

production process it is the cost that is incurred in the firm and business have to cover that cost

out of cash flows. From this point of view if condition is taken into consideration then inclusion

of fixed expenses in the firm seems right. Thus, it can be said that both costing method must be

used in the firm. There is benefit of using this strategy because if marginal costing is only used

then in that case managers can easily recognise that what amount of profit is earned if only those

expenses are taken into consideration that are heavily contributing to production process. On

other hand, if absorption costing is used then it id recognised that how much profit is earned if

both expenses are taken into the account(ainun Tuanmat, and Smith, 2011). Hence, by doing so

effect of these expenses on company revenue is calculated and it can be said that analysis help

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

managers in making decision more in appropriate way. It could be said that corporation must use

both approaches at workplace as there are few of positive and negative points associated with

these approaches. According to need these approached must be used at workplace and proper

evaluation must be done in the firm so that better decision can be made and operation can be

governed in appropriate way.

TASK 3

P.4.Advantage and disadvantage of using various planning instrument that can be utilised for

fund control at workplace

There are number of planning tools that are used by the companies in their business and

all of them have some advantage and disadvantages(Luft, and Shields, 2010). Different form of

planning tools that are available to the business firms are budget and capital budgeting

approaches. In class of budget classifications can be done. Cash budget: It is one of the most essential type of budget that is fitted out by all variety

of business corporations. In the cash budget estimations are made about cash inflow and

outflow and on that basis net available balance is recognised. By using cash budget

planning is done about expenditures that would be made in the company(Macintosh,

N.and Quattrone, 2010). In other words to could be said that efforts are made to make

expenses within determined limit and in this regard plan is made. On this basis it can be

said that cash budget is the one of the essential planning tools for the corporation. There

are number of advantages and disadvantage of the cash budget.

Advantage:

One of the major advantage of cash budget is that by using same expenses can be

controlled in the business in proper manner(Otley, and Emmanuel, 2013). This would

lead to raise in profit in business.

Second main advantage of cash budget is that it is easy to prepare it and there is no need

to hire specific talented person to prepare budget.

Disadvantage: Major disadvantage of using cash budget is that it is based on approximation and if

estimation wold be made wrongly then in that case wrong business decision cab be taken

on the basis of budget.

8

both approaches at workplace as there are few of positive and negative points associated with

these approaches. According to need these approached must be used at workplace and proper

evaluation must be done in the firm so that better decision can be made and operation can be

governed in appropriate way.

TASK 3

P.4.Advantage and disadvantage of using various planning instrument that can be utilised for

fund control at workplace

There are number of planning tools that are used by the companies in their business and

all of them have some advantage and disadvantages(Luft, and Shields, 2010). Different form of

planning tools that are available to the business firms are budget and capital budgeting

approaches. In class of budget classifications can be done. Cash budget: It is one of the most essential type of budget that is fitted out by all variety

of business corporations. In the cash budget estimations are made about cash inflow and

outflow and on that basis net available balance is recognised. By using cash budget

planning is done about expenditures that would be made in the company(Macintosh,

N.and Quattrone, 2010). In other words to could be said that efforts are made to make

expenses within determined limit and in this regard plan is made. On this basis it can be

said that cash budget is the one of the essential planning tools for the corporation. There

are number of advantages and disadvantage of the cash budget.

Advantage:

One of the major advantage of cash budget is that by using same expenses can be

controlled in the business in proper manner(Otley, and Emmanuel, 2013). This would

lead to raise in profit in business.

Second main advantage of cash budget is that it is easy to prepare it and there is no need

to hire specific talented person to prepare budget.

Disadvantage: Major disadvantage of using cash budget is that it is based on approximation and if

estimation wold be made wrongly then in that case wrong business decision cab be taken

on the basis of budget.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Fixed Budget: Fixed budget is another alternative that is available to the business firm. It

is totally inverse of cash budget as in this form of budget values of all elements of budget

is made invariant(Parker, 2012). Like cash budget there are some merits and demerits of

fixed budget.

Advantage

One of major advantage of fixed budget is that its value almost remain same and never

get changed. Hence, firm manager do need to dedicate its special time for formulation of

budget for the company. Other main advantage of using fixed budget is that one just require to take a look at

budget to make sure that it could be used in the company even firm situation change

slightly.

Disadvantage One of disadvantage of using fixed budget is that in case business condition changed at

fast rate it is not possible to make use of fixed budget in the business(Renz, 2016). If it

would be used then in that case wrong decision can be taken in the firm. Zero based budgeting: It is slightly different approach because under this approach

simply no allocations are made to any department until manager present its own

department budget in front of senior managers. There are some of advantage and

disadvantage of zero budgeting which are given below.

Advantage One of major advantage of using zero based budgeting is that under this systematic

approach is followed to prepare budgeting for the company(Whittington, 2011). Hence, it

can be said that in zero based budget projections are highly appropriate to the business.

Disadvantage: One of the major disadvantage of using zero based budgeting is that its process is time

consuming and lengthy. Capital budgeting method: In this approach project evaluation is done and under this

project value method. Some of advantage and disadvantage of capital budgeting method

are explained below:

Advantage

9

is totally inverse of cash budget as in this form of budget values of all elements of budget

is made invariant(Parker, 2012). Like cash budget there are some merits and demerits of

fixed budget.

Advantage

One of major advantage of fixed budget is that its value almost remain same and never

get changed. Hence, firm manager do need to dedicate its special time for formulation of

budget for the company. Other main advantage of using fixed budget is that one just require to take a look at

budget to make sure that it could be used in the company even firm situation change

slightly.

Disadvantage One of disadvantage of using fixed budget is that in case business condition changed at

fast rate it is not possible to make use of fixed budget in the business(Renz, 2016). If it

would be used then in that case wrong decision can be taken in the firm. Zero based budgeting: It is slightly different approach because under this approach

simply no allocations are made to any department until manager present its own

department budget in front of senior managers. There are some of advantage and

disadvantage of zero budgeting which are given below.

Advantage One of major advantage of using zero based budgeting is that under this systematic

approach is followed to prepare budgeting for the company(Whittington, 2011). Hence, it

can be said that in zero based budget projections are highly appropriate to the business.

Disadvantage: One of the major disadvantage of using zero based budgeting is that its process is time

consuming and lengthy. Capital budgeting method: In this approach project evaluation is done and under this

project value method. Some of advantage and disadvantage of capital budgeting method

are explained below:

Advantage

9

Major advantage of using this approach is that projection is made about disbursal that can

be incurred in business project. Hence, planning goes hand in hand with passage of

project duration.

Disadvantage

Major disadvantage of this approach is that with raise in duration project cost might

increase and it can be arduous task to set up plan in reliable manner which lead to

wastage of time.

P.5.Adoption of administration accounting scheme to answer to financial problems

Financial issues are faced by most of the business corporations and it is the management

accounting systems that are used to respond to financial problems(Scapens, and Bromwich,

2010). Some management accounting methodology that could be utilized to respond to financial

issues are as follows: Key performance indicators: KPI is the one of the most essential tool that is used to

respond to financial problems. Currently, The Ledbury Restaurant is facing financial

issue like less availability of cash in business. In terms of respond to problem KPI can be

used in which actual values can be compared to standards and on that basis it can be

recognised how big is financial issue. According to level of recognised issue steps that

can be taken to solve problem are identified in this firm respond to financial problem. Balanced scorecard: Balanced score card is one of the most essential point of view as

under this process there are four parameters where company performance is measured

and evaluated. These four parameters might be financial, customer and stakeholder,

internal process and organisational capacity(Suomala, and Lyly-Yrjänäinen, 2012). On

these four parameters some targets are determined and actual performance is compared

against targets. By doing so firm performance is evaluated and areas where focus need to

be made like improper management of cash are recognised. In this manners sore card

help firm to respond to financial issues.

Financial governance: Financial governance is the specific approach to respond to

financial problems. In this approach rules are regulations are already determined and

same demand to be followed while performing task(Ward, 2012). In case someone that is

performing activities related to finance is facing specific problem and make mistakes in

company then in that situation that specific person would be held responsible for its

10

be incurred in business project. Hence, planning goes hand in hand with passage of

project duration.

Disadvantage

Major disadvantage of this approach is that with raise in duration project cost might

increase and it can be arduous task to set up plan in reliable manner which lead to

wastage of time.

P.5.Adoption of administration accounting scheme to answer to financial problems

Financial issues are faced by most of the business corporations and it is the management

accounting systems that are used to respond to financial problems(Scapens, and Bromwich,

2010). Some management accounting methodology that could be utilized to respond to financial

issues are as follows: Key performance indicators: KPI is the one of the most essential tool that is used to

respond to financial problems. Currently, The Ledbury Restaurant is facing financial

issue like less availability of cash in business. In terms of respond to problem KPI can be

used in which actual values can be compared to standards and on that basis it can be

recognised how big is financial issue. According to level of recognised issue steps that

can be taken to solve problem are identified in this firm respond to financial problem. Balanced scorecard: Balanced score card is one of the most essential point of view as

under this process there are four parameters where company performance is measured

and evaluated. These four parameters might be financial, customer and stakeholder,

internal process and organisational capacity(Suomala, and Lyly-Yrjänäinen, 2012). On

these four parameters some targets are determined and actual performance is compared

against targets. By doing so firm performance is evaluated and areas where focus need to

be made like improper management of cash are recognised. In this manners sore card

help firm to respond to financial issues.

Financial governance: Financial governance is the specific approach to respond to

financial problems. In this approach rules are regulations are already determined and

same demand to be followed while performing task(Ward, 2012). In case someone that is

performing activities related to finance is facing specific problem and make mistakes in

company then in that situation that specific person would be held responsible for its

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.