Management Accounting Report: Financial Issues and Solutions

VerifiedAdded on 2020/06/06

|16

|4283

|47

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within Tata Motors. It begins with an introduction to management accounting, outlining its functions and differentiating it from financial accounting. The report then delves into various accounting systems, including price optimization, cost accounting, and inventory management, and their importance in reporting. It evaluates the benefits of these systems, such as cost reduction and improved decision-making. The report further examines different costing methods, including absorption and marginal costing, and their implications for pricing and profitability. It also discusses the merits and demerits of planning tools in budgetary control, as well as financial issues and potential solutions. The report concludes with an evaluation of management accounting and reporting systems within an organizational context and emphasizes the role of management accounting in analyzing and resolving financial problems. Overall, the report provides a detailed overview of management accounting practices and their significance in the context of a major automotive company.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Different types of accounting system and their essential requirements...........................1

P2: Various accounting system use in reporting....................................................................3

M1: Evaluate the benefits of management accounting systems and their application within an

organisation............................................................................................................................4

D1: Critically evaluate the management accounting and reporting systems and its integration

within organisational process.................................................................................................5

TASK 2............................................................................................................................................5

P3: Different costing methods................................................................................................5

M2: Various types of accounting techniques.........................................................................7

D2: Data interpretation...........................................................................................................7

TASK 3............................................................................................................................................8

P4: Merits and demerits of using planning tools in budgetary control...................................8

M3: Use of different planning tools and their applications..................................................10

TASK 4..........................................................................................................................................10

P5: Various financial issues and measure to resolve it.........................................................10

M4: Roles of management accounting in analysing financial problems..............................11

D3: Evaluation of planning tools for respond financial issues.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Different types of accounting system and their essential requirements...........................1

P2: Various accounting system use in reporting....................................................................3

M1: Evaluate the benefits of management accounting systems and their application within an

organisation............................................................................................................................4

D1: Critically evaluate the management accounting and reporting systems and its integration

within organisational process.................................................................................................5

TASK 2............................................................................................................................................5

P3: Different costing methods................................................................................................5

M2: Various types of accounting techniques.........................................................................7

D2: Data interpretation...........................................................................................................7

TASK 3............................................................................................................................................8

P4: Merits and demerits of using planning tools in budgetary control...................................8

M3: Use of different planning tools and their applications..................................................10

TASK 4..........................................................................................................................................10

P5: Various financial issues and measure to resolve it.........................................................10

M4: Roles of management accounting in analysing financial problems..............................11

D3: Evaluation of planning tools for respond financial issues.............................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is such a tool which is used to assist management in order to

make an effective planning and controlling the business operations with a motive of achieving

desired goals and objectives. It is applicable to every organisation irrespective of the size

whether small, medium and large. It is helpful for management of company to make an effective

decision with the help of data and information gathered through various accounting and reporting

systems. Tata motors Limited, an Indian automotive company which deals in manufacturing

wide variety of passenger vehicles such as cars, trucks, construction equipment. It has operated

in many countries such as UK, Italy, south Korea etc. thus captured large market share. The

project covers various accounting and reporting system which brings useful information to

company. Different planning tools to control budgetary control and few techniques to solve

financial problems are also discussed under this report (Armitage, Webb and Glynn, 2016).

TASK 1

P1: Different types of accounting system and their essential requirements

Definitions of Management accounting:

According to the CIMA, Management accounting refers to the process of identifying,

measuring, accumulating, analysis, interpreting and communicating relevant information which

is used by management to make an effective plans and policies with a motive of utilising

available resources in an optimum manner.

According to the Wilson and Wal, the management accounting refers to techniques and

tool which is used with an intention to provide financial and non-financial information in order

to make profitable decision to achieve desired goals and objectives.

Functions of Management Accounting

There are mainly four types of functions such as Planning, Organising, Controlling and

Decision-making. Management accounting plays an important role in these managerial functions

which need to be performed by managers with a motive of achieving desired goals and objective

within limited period of time.

Planning: It refers to making an effective planning with the help of using information

gathers through accounting system in order to achieve desired goals and objectives. A budget is

financial planning which is prepared with a motive of utilising financial resources in an optimum

1

Management accounting is such a tool which is used to assist management in order to

make an effective planning and controlling the business operations with a motive of achieving

desired goals and objectives. It is applicable to every organisation irrespective of the size

whether small, medium and large. It is helpful for management of company to make an effective

decision with the help of data and information gathered through various accounting and reporting

systems. Tata motors Limited, an Indian automotive company which deals in manufacturing

wide variety of passenger vehicles such as cars, trucks, construction equipment. It has operated

in many countries such as UK, Italy, south Korea etc. thus captured large market share. The

project covers various accounting and reporting system which brings useful information to

company. Different planning tools to control budgetary control and few techniques to solve

financial problems are also discussed under this report (Armitage, Webb and Glynn, 2016).

TASK 1

P1: Different types of accounting system and their essential requirements

Definitions of Management accounting:

According to the CIMA, Management accounting refers to the process of identifying,

measuring, accumulating, analysis, interpreting and communicating relevant information which

is used by management to make an effective plans and policies with a motive of utilising

available resources in an optimum manner.

According to the Wilson and Wal, the management accounting refers to techniques and

tool which is used with an intention to provide financial and non-financial information in order

to make profitable decision to achieve desired goals and objectives.

Functions of Management Accounting

There are mainly four types of functions such as Planning, Organising, Controlling and

Decision-making. Management accounting plays an important role in these managerial functions

which need to be performed by managers with a motive of achieving desired goals and objective

within limited period of time.

Planning: It refers to making an effective planning with the help of using information

gathers through accounting system in order to achieve desired goals and objectives. A budget is

financial planning which is prepared with a motive of utilising financial resources in an optimum

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

manner (DRURY, 2013). It helps in guiding and motivating employees to perform in right

direction to achieve desired target.

Organising: It is a process of creating framework and assigning roles and responsibilities

to members of an organisation on the basis of their skills and knowledge in order to bring

positive outcome in near future. Thus, it is important for manager to first identify their

capabilities of employees through analysing their previous performance and accordingly

assigning roles and responsibilities in order to get positive result.

Controlling: It is the process of monitoring, analysing the actual result in order to find

out whether an organisation moves towards right direction or not. For this, manager is required

to collect feedback from employees in order to find out deviation and accordingly take corrective

steps on time. The management of company should required ton use various accounting systems

which help them to control business activities with a motive of preventing wastage.

Decision-making: An effective plan cannot be made without an effective decision thus

the manager need to first target objectives and accordingly decide organisation structure in order

to operate business operations in an effective and efficient manner (Ferreira, Moulang and

Hendro, 2010). Thus, it is important to collect feedbacks from the employees and accordingly

focus on removing issues while taking an effective decision.

Difference between Management and financial accounting:

Management accounting Financial accounting

The main aim of MA is to provide sufficient

and important data to managers regarding

formulating an effective planning and

strategies to achieve set objectives.

The main aim of FA is to provide financial

position of company through preparing

financial statements such as P&L a/c, Balance

sheet.

The information obtained through managerial

accounting is useful for external parties such as

shareholders, creditors etc.

The information obtained through financial

accounting is useful for managers and

employees.

It is more emphasis on the future. It is more emphasis on past.

It is not mandatory by law. It is essentially required to prepare financial

statements on annual basis as per the law.

2

direction to achieve desired target.

Organising: It is a process of creating framework and assigning roles and responsibilities

to members of an organisation on the basis of their skills and knowledge in order to bring

positive outcome in near future. Thus, it is important for manager to first identify their

capabilities of employees through analysing their previous performance and accordingly

assigning roles and responsibilities in order to get positive result.

Controlling: It is the process of monitoring, analysing the actual result in order to find

out whether an organisation moves towards right direction or not. For this, manager is required

to collect feedback from employees in order to find out deviation and accordingly take corrective

steps on time. The management of company should required ton use various accounting systems

which help them to control business activities with a motive of preventing wastage.

Decision-making: An effective plan cannot be made without an effective decision thus

the manager need to first target objectives and accordingly decide organisation structure in order

to operate business operations in an effective and efficient manner (Ferreira, Moulang and

Hendro, 2010). Thus, it is important to collect feedbacks from the employees and accordingly

focus on removing issues while taking an effective decision.

Difference between Management and financial accounting:

Management accounting Financial accounting

The main aim of MA is to provide sufficient

and important data to managers regarding

formulating an effective planning and

strategies to achieve set objectives.

The main aim of FA is to provide financial

position of company through preparing

financial statements such as P&L a/c, Balance

sheet.

The information obtained through managerial

accounting is useful for external parties such as

shareholders, creditors etc.

The information obtained through financial

accounting is useful for managers and

employees.

It is more emphasis on the future. It is more emphasis on past.

It is not mandatory by law. It is essentially required to prepare financial

statements on annual basis as per the law.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Types of accounting system:

Price optimisation: This system helps in identifying the interest and buying behaviour of

customers towards the price the company charged for their products and services. For this, the

managers of Tata Motors are required to use mathematical analysis which help company to

examine customer's requirements and changes required in price and product.

Cost accounting system: This accounting system is important for an organisation as it

helps in determining the total cost which is required to produce quality products and services

(Grabner and Moers, 2013). The cost accountant of Tata Motors is held liable to estimate cost

before production process so that it can help company in achieving profitability. For example the

manager of Tata Motors should required to estimate total cost in manufacturing vehicle along

with the additional features implemented to make product more attractive and efficient.

Inventory management system: With the help of such system the Tata Motors Ltd. can

able to reduce inventory cost and improves profitability. The manager should required to ordered

raw material used in production process whenever they required so that cost of storing unwanted

raw materials in warehouses will be saved. Through this, the company can able to meet

customer's needs and demands on time.

P2: Various accounting system use in reporting

Reports: Reports are considered as document which provides all sufficient and crucial

information regarding business transaction happened on daily basis. Such reports are required to

prepared on daily, weekly and monthly basis. As there are various departments in Tata Motors

whose main aim is to achieve organisational goals thus collecting information about their

performance will help to get know about whether the departments are performed in right

direction or not. Such information may useful to both internal and external parties and also

improve decision making process. For example financial statement is one of the type of report

which should required to prepare by Tata Motors on annual basis so as to provide financial

position of company towards internal and external parties (Håkansson, Kraus and Lind, 2010).

Thus, there are various types of reporting which are defined as below:

Performance report: This type of report contains information regarding the performance

of company through which the manager can able to identify whether the company has move

towards right direction or not so that if any deviation found which restricts members to perform

3

Price optimisation: This system helps in identifying the interest and buying behaviour of

customers towards the price the company charged for their products and services. For this, the

managers of Tata Motors are required to use mathematical analysis which help company to

examine customer's requirements and changes required in price and product.

Cost accounting system: This accounting system is important for an organisation as it

helps in determining the total cost which is required to produce quality products and services

(Grabner and Moers, 2013). The cost accountant of Tata Motors is held liable to estimate cost

before production process so that it can help company in achieving profitability. For example the

manager of Tata Motors should required to estimate total cost in manufacturing vehicle along

with the additional features implemented to make product more attractive and efficient.

Inventory management system: With the help of such system the Tata Motors Ltd. can

able to reduce inventory cost and improves profitability. The manager should required to ordered

raw material used in production process whenever they required so that cost of storing unwanted

raw materials in warehouses will be saved. Through this, the company can able to meet

customer's needs and demands on time.

P2: Various accounting system use in reporting

Reports: Reports are considered as document which provides all sufficient and crucial

information regarding business transaction happened on daily basis. Such reports are required to

prepared on daily, weekly and monthly basis. As there are various departments in Tata Motors

whose main aim is to achieve organisational goals thus collecting information about their

performance will help to get know about whether the departments are performed in right

direction or not. Such information may useful to both internal and external parties and also

improve decision making process. For example financial statement is one of the type of report

which should required to prepare by Tata Motors on annual basis so as to provide financial

position of company towards internal and external parties (Håkansson, Kraus and Lind, 2010).

Thus, there are various types of reporting which are defined as below:

Performance report: This type of report contains information regarding the performance

of company through which the manager can able to identify whether the company has move

towards right direction or not so that if any deviation found which restricts members to perform

3

better can be resolved within limited period of time. It helps Tata Motors in achieving

competitive advantage and sustain in market for longer period of time.

Inventory management report: This report contains the information regarding the

amount of inventory maintained in warehouses which helps Tata motors in meeting needs and

demands of customers on time. The managers can able to run the production process smoothly

without facing any interruptions.

Accounts receivable report: This type of reports contains the list of debtors whose

payment to company may due. It helps managers of Tata Motors in getting information of their

debtors so that due amount can be covered on time which improves their financial position of

company. It is an effective tools which should be adopted by every business in order to collect

accounting details which are related with credit payment options (Kotas, 2014).

M1: Evaluate the benefits of management accounting systems and their application within an

organisation

Tata Motors Ltd. may get several benefits from management accounting systems which

are briefly described under the below :

Management accounting systems Benefits

Cost accounting systems It facilitate an organisation in minimising

wastage through assigning cost to particular

departments according to their needs and

analyse outcomes received in future.

Inventory management system It help Tata Motors Ltd. In maintain raw raw

material used in production process so as to

meet customer needs and demands in market.

Price optimisation system It help in achieving loyalty of targeted

customers and retail them for longer period of

time through setting an effective pricing

policies.

Job costing system It facilitate company in determining the total

cost invested in producing individual product

4

competitive advantage and sustain in market for longer period of time.

Inventory management report: This report contains the information regarding the

amount of inventory maintained in warehouses which helps Tata motors in meeting needs and

demands of customers on time. The managers can able to run the production process smoothly

without facing any interruptions.

Accounts receivable report: This type of reports contains the list of debtors whose

payment to company may due. It helps managers of Tata Motors in getting information of their

debtors so that due amount can be covered on time which improves their financial position of

company. It is an effective tools which should be adopted by every business in order to collect

accounting details which are related with credit payment options (Kotas, 2014).

M1: Evaluate the benefits of management accounting systems and their application within an

organisation

Tata Motors Ltd. may get several benefits from management accounting systems which

are briefly described under the below :

Management accounting systems Benefits

Cost accounting systems It facilitate an organisation in minimising

wastage through assigning cost to particular

departments according to their needs and

analyse outcomes received in future.

Inventory management system It help Tata Motors Ltd. In maintain raw raw

material used in production process so as to

meet customer needs and demands in market.

Price optimisation system It help in achieving loyalty of targeted

customers and retail them for longer period of

time through setting an effective pricing

policies.

Job costing system It facilitate company in determining the total

cost invested in producing individual product

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

or group of products.

D1: Critically evaluate the management accounting and reporting systems and its integration

within organisational process

There are several forms of accounting and reporting system which assist management in

making an effective and profitable decisions through acquiring sufficient relevant information

with the help of such systems. For example, accounting receivable report facilitate management

of Tata Motors in acquiring list of unpaid debtors which forces management to change its credit

policies so as to prevent uncertainties regarding recovery of payment.

TASK 2

P3: Different costing methods

Cost refers to an amount of value which are required to incur in the business operations

without any interruptions so as to achieve desired goals and objectives. It can be incurred in

production process, payment made to employees etc. Therefore the cost accountant is held liable

to estimate cost and accordingly allocate to their different departments on the basis of

requirements so that no department faces shortage of funds while operating business activities.

Tata motors which is already a established brand across worldwide capture large market share

and attained large number of loyal customers. Thus it is important for them to maintain their

strong brand image through providing efficient vehicle products along with the unique features

which makes them different from their rivals. The manager need to first divide people on the

basis of their purchasing capabilities and accordingly produce wide range of products so as to

maximise their satisfaction level (Lavia López and Hiebl, 2014). Thus, costing factor is an

important element which attracts buying behaviour of customers. There are suitable techniques

and measure which help company in reducing extra cost incurred in manufacturing process

which directly affects their profitability in positive manner. There are mainly two types of

costing methods which help in fixing the price of products they should charged from their

customers. Such methods includes:

Absorption Costing: It is a techniques which is related with spending costs on producing

specific products at optimum quality. It includes both fixed and variable cost. Cost of final

products includes direct labour, material and overhead expenses.

5

D1: Critically evaluate the management accounting and reporting systems and its integration

within organisational process

There are several forms of accounting and reporting system which assist management in

making an effective and profitable decisions through acquiring sufficient relevant information

with the help of such systems. For example, accounting receivable report facilitate management

of Tata Motors in acquiring list of unpaid debtors which forces management to change its credit

policies so as to prevent uncertainties regarding recovery of payment.

TASK 2

P3: Different costing methods

Cost refers to an amount of value which are required to incur in the business operations

without any interruptions so as to achieve desired goals and objectives. It can be incurred in

production process, payment made to employees etc. Therefore the cost accountant is held liable

to estimate cost and accordingly allocate to their different departments on the basis of

requirements so that no department faces shortage of funds while operating business activities.

Tata motors which is already a established brand across worldwide capture large market share

and attained large number of loyal customers. Thus it is important for them to maintain their

strong brand image through providing efficient vehicle products along with the unique features

which makes them different from their rivals. The manager need to first divide people on the

basis of their purchasing capabilities and accordingly produce wide range of products so as to

maximise their satisfaction level (Lavia López and Hiebl, 2014). Thus, costing factor is an

important element which attracts buying behaviour of customers. There are suitable techniques

and measure which help company in reducing extra cost incurred in manufacturing process

which directly affects their profitability in positive manner. There are mainly two types of

costing methods which help in fixing the price of products they should charged from their

customers. Such methods includes:

Absorption Costing: It is a techniques which is related with spending costs on producing

specific products at optimum quality. It includes both fixed and variable cost. Cost of final

products includes direct labour, material and overhead expenses.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

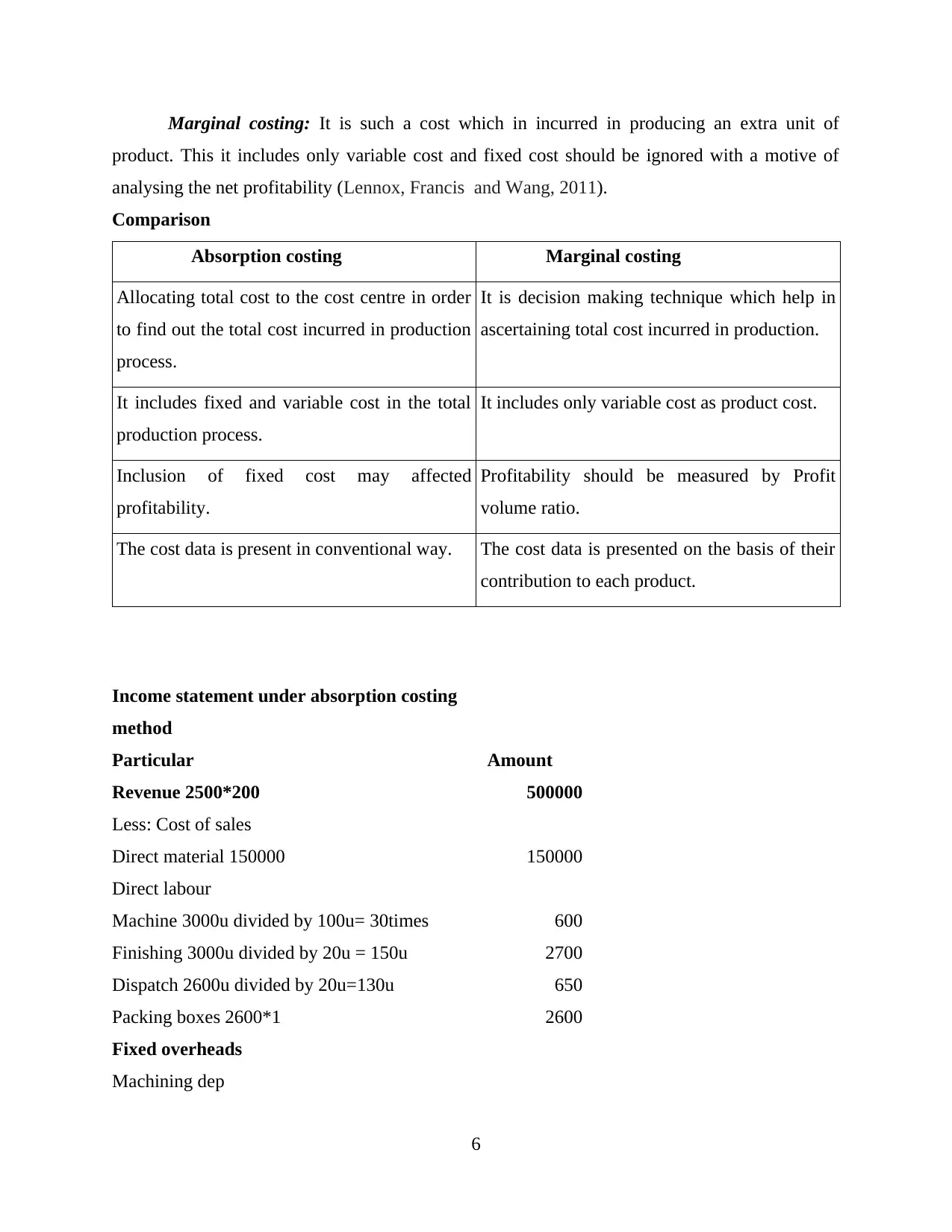

Marginal costing: It is such a cost which in incurred in producing an extra unit of

product. This it includes only variable cost and fixed cost should be ignored with a motive of

analysing the net profitability (Lennox, Francis and Wang, 2011).

Comparison

Absorption costing Marginal costing

Allocating total cost to the cost centre in order

to find out the total cost incurred in production

process.

It is decision making technique which help in

ascertaining total cost incurred in production.

It includes fixed and variable cost in the total

production process.

It includes only variable cost as product cost.

Inclusion of fixed cost may affected

profitability.

Profitability should be measured by Profit

volume ratio.

The cost data is present in conventional way. The cost data is presented on the basis of their

contribution to each product.

Income statement under absorption costing

method

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Machine 3000u divided by 100u= 30times 600

Finishing 3000u divided by 20u = 150u 2700

Dispatch 2600u divided by 20u=130u 650

Packing boxes 2600*1 2600

Fixed overheads

Machining dep

6

product. This it includes only variable cost and fixed cost should be ignored with a motive of

analysing the net profitability (Lennox, Francis and Wang, 2011).

Comparison

Absorption costing Marginal costing

Allocating total cost to the cost centre in order

to find out the total cost incurred in production

process.

It is decision making technique which help in

ascertaining total cost incurred in production.

It includes fixed and variable cost in the total

production process.

It includes only variable cost as product cost.

Inclusion of fixed cost may affected

profitability.

Profitability should be measured by Profit

volume ratio.

The cost data is present in conventional way. The cost data is presented on the basis of their

contribution to each product.

Income statement under absorption costing

method

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Machine 3000u divided by 100u= 30times 600

Finishing 3000u divided by 20u = 150u 2700

Dispatch 2600u divided by 20u=130u 650

Packing boxes 2600*1 2600

Fixed overheads

Machining dep

6

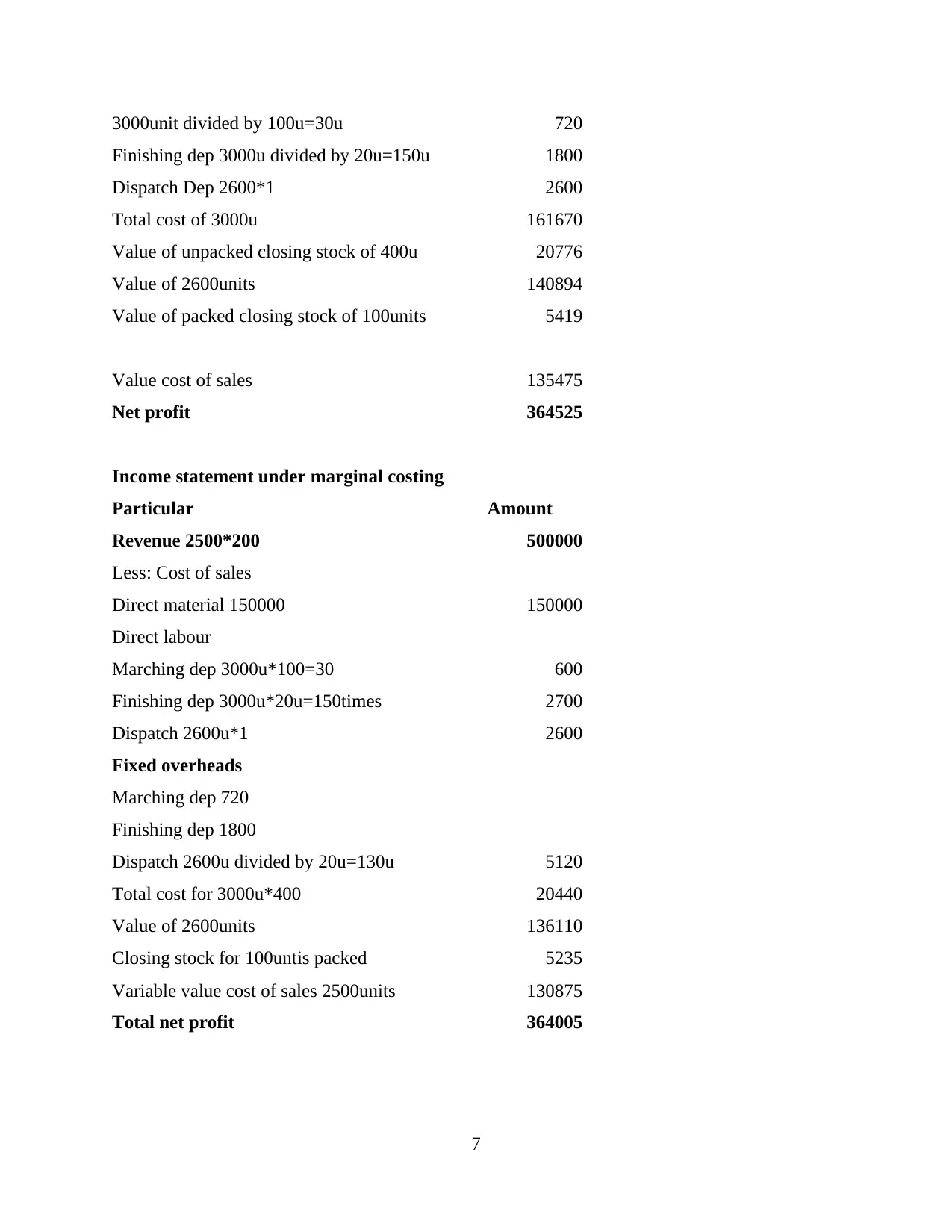

3000unit divided by 100u=30u 720

Finishing dep 3000u divided by 20u=150u 1800

Dispatch Dep 2600*1 2600

Total cost of 3000u 161670

Value of unpacked closing stock of 400u 20776

Value of 2600units 140894

Value of packed closing stock of 100units 5419

Value cost of sales 135475

Net profit 364525

Income statement under marginal costing

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Marching dep 3000u*100=30 600

Finishing dep 3000u*20u=150times 2700

Dispatch 2600u*1 2600

Fixed overheads

Marching dep 720

Finishing dep 1800

Dispatch 2600u divided by 20u=130u 5120

Total cost for 3000u*400 20440

Value of 2600units 136110

Closing stock for 100untis packed 5235

Variable value cost of sales 2500units 130875

Total net profit 364005

7

Finishing dep 3000u divided by 20u=150u 1800

Dispatch Dep 2600*1 2600

Total cost of 3000u 161670

Value of unpacked closing stock of 400u 20776

Value of 2600units 140894

Value of packed closing stock of 100units 5419

Value cost of sales 135475

Net profit 364525

Income statement under marginal costing

Particular Amount

Revenue 2500*200 500000

Less: Cost of sales

Direct material 150000 150000

Direct labour

Marching dep 3000u*100=30 600

Finishing dep 3000u*20u=150times 2700

Dispatch 2600u*1 2600

Fixed overheads

Marching dep 720

Finishing dep 1800

Dispatch 2600u divided by 20u=130u 5120

Total cost for 3000u*400 20440

Value of 2600units 136110

Closing stock for 100untis packed 5235

Variable value cost of sales 2500units 130875

Total net profit 364005

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2: Various types of accounting techniques

There are basically two types of accounting techniques which may adopted by Tata

Motors Ltd. Such are given as below:

Standard costing: It is more helpful in determining future profession through considering

various aspects which includes future sales revenue, costs and demand. It is the method adopted

by most of the companies such as Tata Motors due to ascertaining future outcomes.

Marginal costing: It is adopted by almost every organization including Tata Motors Ltd.

so as to ascertain net profits through considering only variable costs.

D2: Data interpretation

As per the above calculation, there are two methods which are used to calculate

net profitability. While using absorption costing method, the profit is 364525 whereas using

marginal costing method the profit is 364005. Such difference of 520 comes due to changing in

variable cost. Thus, Tata motors Ltd. are required to adopt absorption method in order to increase

its profitability.

TASK 3

P4: Merits and demerits of using planning tools in budgetary control

Budgetary control: It is the process of identifying and analysing the performance of an

organisation through comparing actual with standard so that that find out the deviations if any.

This will help management of Tata Motors to take crucial steps to avoid such deviations within

limited period of time so that it cannot affects profitability of company (Morales and Lambert,

2013).

Objectives of Budgetary control:

It helps in determining the desired objectives of company which need to be achieved in

near future.

Its main motive is to communicate plans to the different departments in order to achieve

desired target on time.

Cost allocation to cost centre in order to produce quality product without any

interruptions.

Allocating roles and duties to members according to their capabilities (Moser, 2012).

There are different types of planning tools in budgetary control which are as follows:

8

There are basically two types of accounting techniques which may adopted by Tata

Motors Ltd. Such are given as below:

Standard costing: It is more helpful in determining future profession through considering

various aspects which includes future sales revenue, costs and demand. It is the method adopted

by most of the companies such as Tata Motors due to ascertaining future outcomes.

Marginal costing: It is adopted by almost every organization including Tata Motors Ltd.

so as to ascertain net profits through considering only variable costs.

D2: Data interpretation

As per the above calculation, there are two methods which are used to calculate

net profitability. While using absorption costing method, the profit is 364525 whereas using

marginal costing method the profit is 364005. Such difference of 520 comes due to changing in

variable cost. Thus, Tata motors Ltd. are required to adopt absorption method in order to increase

its profitability.

TASK 3

P4: Merits and demerits of using planning tools in budgetary control

Budgetary control: It is the process of identifying and analysing the performance of an

organisation through comparing actual with standard so that that find out the deviations if any.

This will help management of Tata Motors to take crucial steps to avoid such deviations within

limited period of time so that it cannot affects profitability of company (Morales and Lambert,

2013).

Objectives of Budgetary control:

It helps in determining the desired objectives of company which need to be achieved in

near future.

Its main motive is to communicate plans to the different departments in order to achieve

desired target on time.

Cost allocation to cost centre in order to produce quality product without any

interruptions.

Allocating roles and duties to members according to their capabilities (Moser, 2012).

There are different types of planning tools in budgetary control which are as follows:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental budgeting: It is budget prepared on the basis of previous budget so that the

managers can able to know the required amount in new budget period. The resources are

allocated after analysing the past budget period which helps in getting positive outcome in near

future. It motivates managers to spend more amount in the execution of project activities which

may affects the budget prepared for next year (Otley and Emmanuel, 2013).

Advantages:

It becomes easy for employees to understand and operate the system in more effective

and efficient manner.

Proper coordination between the departments helps in maintaining healthy relations

which brings positive result to company.

As every departments gets equal support and guidance due to which the chances of

arising conflicts will be minimum.

Disadvantages:

The employees gets no incentives and rewards for new ideas which demotivate them.

Spending huge amount on current budget which brings difficulties for company to

prepare next period budget.

The budget has been prepared manually due to which the priority for resources may

changed (Tucker and Lowe, 2014).

Zero Based Budgeting: It is a method of budgeting in which the expenses required to invest in

production process for new period are determined. It starts from zero with having no experience

thus managers need to first analyses the needs and cost. The manager is required to take fresh

and innovative decision regarding execution of project activities every year.

Advantages:

It assures proper allocation of resources as it is based on needs and avoids irrelevant

expenses.

This technique helps in identifying and eliminating wastage of raw materials.

This approach helps in directing cost centres to link their mission in order to achieve

desired objectives.

Disadvantage:

Sometimes it becomes difficult for manager to take decision regarding investing amount

in project activities which consumes more time (Papaspyropoulos and et. al., 2012).

9

managers can able to know the required amount in new budget period. The resources are

allocated after analysing the past budget period which helps in getting positive outcome in near

future. It motivates managers to spend more amount in the execution of project activities which

may affects the budget prepared for next year (Otley and Emmanuel, 2013).

Advantages:

It becomes easy for employees to understand and operate the system in more effective

and efficient manner.

Proper coordination between the departments helps in maintaining healthy relations

which brings positive result to company.

As every departments gets equal support and guidance due to which the chances of

arising conflicts will be minimum.

Disadvantages:

The employees gets no incentives and rewards for new ideas which demotivate them.

Spending huge amount on current budget which brings difficulties for company to

prepare next period budget.

The budget has been prepared manually due to which the priority for resources may

changed (Tucker and Lowe, 2014).

Zero Based Budgeting: It is a method of budgeting in which the expenses required to invest in

production process for new period are determined. It starts from zero with having no experience

thus managers need to first analyses the needs and cost. The manager is required to take fresh

and innovative decision regarding execution of project activities every year.

Advantages:

It assures proper allocation of resources as it is based on needs and avoids irrelevant

expenses.

This technique helps in identifying and eliminating wastage of raw materials.

This approach helps in directing cost centres to link their mission in order to achieve

desired objectives.

Disadvantage:

Sometimes it becomes difficult for manager to take decision regarding investing amount

in project activities which consumes more time (Papaspyropoulos and et. al., 2012).

9

The members are liable to specify all expenditures incurred by them which restricts other

department to spend less.

Activity Based Budgeting: It is a technique in which the cost allocated for specific

project activities are clearly defined and analysed so that profitable outcome may received future.

It is prepared on the basis of activities which need to executed without having any past budgeting

information. It is manually prepared which mainly focusing on developing budgets on the basis

of activities that will help in bringing efficiency in business operation (Renz, 2016).

Advantages:

As whole business will be viewed as a single unit thus it becomes easy for manager to

prepared an effective budget without thinking too much.

It helps company in maintaining healthy relation with their customers through providing

quality features in their product. It helps company in reducing cost through eliminating unnecessary activities.

Disadvantages:

It becomes difficult for manager to understand various functional areas of the business as

it requires special skills and knowledge.

It is complex in nature which required research and evaluation of different factors.

It consumes a lot of resources of an organisation as it required to employee members to

conduct analyses and research (van der Steen, 2011).

M3: Use of different planning tools and their applications

Budgetary control brings profitable result to company in form of controlling unnecessary

expenses and utilizing allocated cost in an optimum manner. For this, there are various tools

which are used by company such as Activity Based Budgeting, Zero Based Budgeting etc. Such

tools assist management in determining the cost incurred in execution of project activities and

minimizing wastage.

TASK 4

P5: Various financial issues and measure to resolve it

Tata motors already attains strong brand image in competitive market world through

providing efficient vehicle product with unique and innovative design and features. But due to

high competition with their rivals, the sales figure may goes down due to which the company's

10

department to spend less.

Activity Based Budgeting: It is a technique in which the cost allocated for specific

project activities are clearly defined and analysed so that profitable outcome may received future.

It is prepared on the basis of activities which need to executed without having any past budgeting

information. It is manually prepared which mainly focusing on developing budgets on the basis

of activities that will help in bringing efficiency in business operation (Renz, 2016).

Advantages:

As whole business will be viewed as a single unit thus it becomes easy for manager to

prepared an effective budget without thinking too much.

It helps company in maintaining healthy relation with their customers through providing

quality features in their product. It helps company in reducing cost through eliminating unnecessary activities.

Disadvantages:

It becomes difficult for manager to understand various functional areas of the business as

it requires special skills and knowledge.

It is complex in nature which required research and evaluation of different factors.

It consumes a lot of resources of an organisation as it required to employee members to

conduct analyses and research (van der Steen, 2011).

M3: Use of different planning tools and their applications

Budgetary control brings profitable result to company in form of controlling unnecessary

expenses and utilizing allocated cost in an optimum manner. For this, there are various tools

which are used by company such as Activity Based Budgeting, Zero Based Budgeting etc. Such

tools assist management in determining the cost incurred in execution of project activities and

minimizing wastage.

TASK 4

P5: Various financial issues and measure to resolve it

Tata motors already attains strong brand image in competitive market world through

providing efficient vehicle product with unique and innovative design and features. But due to

high competition with their rivals, the sales figure may goes down due to which the company's

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.