Detailed Management Accounting Report for Qbic Hotel (Unit 5)

VerifiedAdded on 2020/10/05

|19

|5526

|327

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their practical application within the context of Qbic Hotel. It begins with an introduction to management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report then delves into various management accounting reports, such as budget reports, accounting receivable aging, job cost reports, and inventory reports, evaluating their benefits and drawbacks. The core of the report involves a detailed analysis of costing methods, specifically absorption costing and marginal costing, including the preparation of income statements using both methods and the calculation of break-even analysis. The report also examines budgetary control, planning tools, and how management accounting systems respond to and analyze financial problems. It concludes with an evaluation of planning tools and offers recommendations for implementing management accounting techniques to address financial challenges, ultimately aiming to improve decision-making and financial performance within the hotel.

UNIT 5 Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management Accounting and its different types of systems.............................................1

B. Management Accounting Reports.....................................................................................2

C. Evaluation of Benefits of management accounting system...............................................3

D. Evaluation of management accounting systems and management accounting reporting. 5

TASK 2............................................................................................................................................5

A.1 Absorption Costing and Marginal Costing methods......................................................5

A.2 Preparation of income statement as marginal and absorption costing method................5

B. Calculation of Break Even Analysis..................................................................................7

C. Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately..............................................................................................8

D. Interpretation of data for business activities as shown in Task 2......................................9

TASK 3..........................................................................................................................................10

A. Advantages and Disadvantages of budgetary control......................................................10

B. Application of planning Tools.........................................................................................11

C. Management Accounting System response to financial problems..................................12

D. Analysis of Management Accounting Techniques used to respond Financial Problems13

E. Evaluation of planning tools to solve financial problems................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management Accounting and its different types of systems.............................................1

B. Management Accounting Reports.....................................................................................2

C. Evaluation of Benefits of management accounting system...............................................3

D. Evaluation of management accounting systems and management accounting reporting. 5

TASK 2............................................................................................................................................5

A.1 Absorption Costing and Marginal Costing methods......................................................5

A.2 Preparation of income statement as marginal and absorption costing method................5

B. Calculation of Break Even Analysis..................................................................................7

C. Apply the range of management accounting techniques and produce appropriate financial

reporting documents accurately..............................................................................................8

D. Interpretation of data for business activities as shown in Task 2......................................9

TASK 3..........................................................................................................................................10

A. Advantages and Disadvantages of budgetary control......................................................10

B. Application of planning Tools.........................................................................................11

C. Management Accounting System response to financial problems..................................12

D. Analysis of Management Accounting Techniques used to respond Financial Problems13

E. Evaluation of planning tools to solve financial problems................................................14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting field of finance lays high level of emphasis on the internal

control through the means of several tools and techniques. In simple words, it can be stated that

management accounting includes both financial and non-financial provisions which in turn helps

account managers in decision making. In the following assignment, detailed information is given

about management accounting and its systems in context of Qbic Hotel. Such small sized hotel

unit provides accommodation services to the customers at cost effective prices. This project

report contains various types of accounting reports that are used and implemented by an

organization.

Criticism will also be done on benefits of different types of accounting system with their

techniques such as marginal costing and absorption costing. Moreover, requirements and needs

are contrasted for different types of management accounting. Further, practical aspects of project

are fulfilled by preparing income statement based on calculations of cost, calculating breakeven

point, etc. Last part of project report will highlight suggestions and recommendations for

implementing management accounting techniques pertaining to respond monetary problems.

TASK 1

A. Management Accounting and its different types of systems

Management Accounting could be termed as the process of managing reports and

accounts that are used to provide accurate financial condition of firm which helps in making day

to day decisions in an organisation (Agbejule, 2011). It is also known as cost accounting, a

process of measuring, interpreting, identifying, analysing and communicating information to

managers for achieving organizational goals. This process of communicating information helps

manager of Qbic, a hotel to cope up with changes and to evaluate actual requirement of financial

and non-financial provisions that are used in making decision.

Different types of management accounting system that can be used by Qbic are as follows:

It is a framework which is used to predict the cost of services for analysing profitability,

cost control and inventory valuation. Following are some accounting system such as:

Cost Accounting System: It is also known as product costing system, it is used by Qbic

hotel to identify the cost of their services for analysing profitability, controlling cost and

Management accounting field of finance lays high level of emphasis on the internal

control through the means of several tools and techniques. In simple words, it can be stated that

management accounting includes both financial and non-financial provisions which in turn helps

account managers in decision making. In the following assignment, detailed information is given

about management accounting and its systems in context of Qbic Hotel. Such small sized hotel

unit provides accommodation services to the customers at cost effective prices. This project

report contains various types of accounting reports that are used and implemented by an

organization.

Criticism will also be done on benefits of different types of accounting system with their

techniques such as marginal costing and absorption costing. Moreover, requirements and needs

are contrasted for different types of management accounting. Further, practical aspects of project

are fulfilled by preparing income statement based on calculations of cost, calculating breakeven

point, etc. Last part of project report will highlight suggestions and recommendations for

implementing management accounting techniques pertaining to respond monetary problems.

TASK 1

A. Management Accounting and its different types of systems

Management Accounting could be termed as the process of managing reports and

accounts that are used to provide accurate financial condition of firm which helps in making day

to day decisions in an organisation (Agbejule, 2011). It is also known as cost accounting, a

process of measuring, interpreting, identifying, analysing and communicating information to

managers for achieving organizational goals. This process of communicating information helps

manager of Qbic, a hotel to cope up with changes and to evaluate actual requirement of financial

and non-financial provisions that are used in making decision.

Different types of management accounting system that can be used by Qbic are as follows:

It is a framework which is used to predict the cost of services for analysing profitability,

cost control and inventory valuation. Following are some accounting system such as:

Cost Accounting System: It is also known as product costing system, it is used by Qbic

hotel to identify the cost of their services for analysing profitability, controlling cost and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

evaluating inventory. A firm focus on evaluating profitability of products by estimating

correct cost of the services and products.

Inventory Management System: It is a system of tracking goods and services through

the whole supply chain or a portion where a business operates (Baldvinsdottir, Mitchell

and Nørreklit, 2010). In simple words, it enables Qbic hotel to see all moving parts of its

operations activity by allowing them to make better decisions and investments.

Job Costing System: This system tracks the cost, income of job and assists in identifying

profitability in job. Qbic hotel uses this accounting system to allow number of jobs that

are assigned to every individual including items of expense and revenues.

Price Optimization System: This accounting system uses mathematical tools to analyse

customer’s response to different prices of its products and services through different

mediums and channels. Qbic hotel use this system to determine the best methods of

achieving objectives such as profit maximisation from operations.

B. Management Accounting Reports

These reports provide hotel information for cutting down cost, rewarding high

performing employees and investment in goods that offer the best financial return from

business. Reports could be generated quarterly, half yearly, monthly or on daily basis. Following

are some types of management accounting reports that could be used by Qbic hotel:

Budget Report: This report provides deeper insight to the management team about the

extent to which budgeted figures are met. This type of report assist management in

analysing business as well as their own department and to control cost (Lee Jr, Johnson

and Joyce, 2012). This report is important for controlling different departments of

organization and to control cost services.

Accounting Receivable Aging: This is a type of tool for managing cash flow after

extension of credit to business customers. Management team of Qbic hotel can use this

tool to identify problems which are being faced by company's collection process. This

tool will assist hotel in solving problems related to collection process for smooth

functioning of business transactions.

Job Cost Reports: This reports displays expenses made in finance for a specific project

by business. Qbic hotel can easily match these with the revenue to evaluate job's

profitability. From this, company can identify high earning areas of the business so that

correct cost of the services and products.

Inventory Management System: It is a system of tracking goods and services through

the whole supply chain or a portion where a business operates (Baldvinsdottir, Mitchell

and Nørreklit, 2010). In simple words, it enables Qbic hotel to see all moving parts of its

operations activity by allowing them to make better decisions and investments.

Job Costing System: This system tracks the cost, income of job and assists in identifying

profitability in job. Qbic hotel uses this accounting system to allow number of jobs that

are assigned to every individual including items of expense and revenues.

Price Optimization System: This accounting system uses mathematical tools to analyse

customer’s response to different prices of its products and services through different

mediums and channels. Qbic hotel use this system to determine the best methods of

achieving objectives such as profit maximisation from operations.

B. Management Accounting Reports

These reports provide hotel information for cutting down cost, rewarding high

performing employees and investment in goods that offer the best financial return from

business. Reports could be generated quarterly, half yearly, monthly or on daily basis. Following

are some types of management accounting reports that could be used by Qbic hotel:

Budget Report: This report provides deeper insight to the management team about the

extent to which budgeted figures are met. This type of report assist management in

analysing business as well as their own department and to control cost (Lee Jr, Johnson

and Joyce, 2012). This report is important for controlling different departments of

organization and to control cost services.

Accounting Receivable Aging: This is a type of tool for managing cash flow after

extension of credit to business customers. Management team of Qbic hotel can use this

tool to identify problems which are being faced by company's collection process. This

tool will assist hotel in solving problems related to collection process for smooth

functioning of business transactions.

Job Cost Reports: This reports displays expenses made in finance for a specific project

by business. Qbic hotel can easily match these with the revenue to evaluate job's

profitability. From this, company can identify high earning areas of the business so that

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

more focus could be made on them instead wasting time and money on areas generating

low profits. This report could be important for Qbic hotel to put efforts in areas which

requires improvement.

Inventory and Manufacturing: This managerial accounting report is used to make

manufacturing process more efficient (Lusardi and Mitchell, 2011). This is significant in

comparing different assembly lines within business to highlight areas which needs

improvement. C. Evaluation of Benefits of management accounting system

Cost Accounting System

Advantages Disadvantages

Elimination of Wastes: A good system

eliminates wastes by fixing standards.

Cost Reduction: Use of new and

improved production methods leads to

cost reduction.

Identify reasons of profits and losses: A

good cost accounting system highlights

reasons for increasing and decreasing

profits.

Advises on decisions: By gaining cost

information management could decide

whether to make or buy a product in

open market.

Price Fixation: Total cost that is

available in the costing records is

useful in fixing up price of a product or

services.

Decision is taken by management about

future but only past records are

available in costing records.

Cost data are not so useful as cost of

previous is not same in the succeeding

year.

Cost may not be accurate if capacity is

partly utilized.

Can lead to over absorption or under

absorption of overheads.

Cost accounting system is rigid in

nature, hence cannot serve all purposes.

Job Costing System

low profits. This report could be important for Qbic hotel to put efforts in areas which

requires improvement.

Inventory and Manufacturing: This managerial accounting report is used to make

manufacturing process more efficient (Lusardi and Mitchell, 2011). This is significant in

comparing different assembly lines within business to highlight areas which needs

improvement. C. Evaluation of Benefits of management accounting system

Cost Accounting System

Advantages Disadvantages

Elimination of Wastes: A good system

eliminates wastes by fixing standards.

Cost Reduction: Use of new and

improved production methods leads to

cost reduction.

Identify reasons of profits and losses: A

good cost accounting system highlights

reasons for increasing and decreasing

profits.

Advises on decisions: By gaining cost

information management could decide

whether to make or buy a product in

open market.

Price Fixation: Total cost that is

available in the costing records is

useful in fixing up price of a product or

services.

Decision is taken by management about

future but only past records are

available in costing records.

Cost data are not so useful as cost of

previous is not same in the succeeding

year.

Cost may not be accurate if capacity is

partly utilized.

Can lead to over absorption or under

absorption of overheads.

Cost accounting system is rigid in

nature, hence cannot serve all purposes.

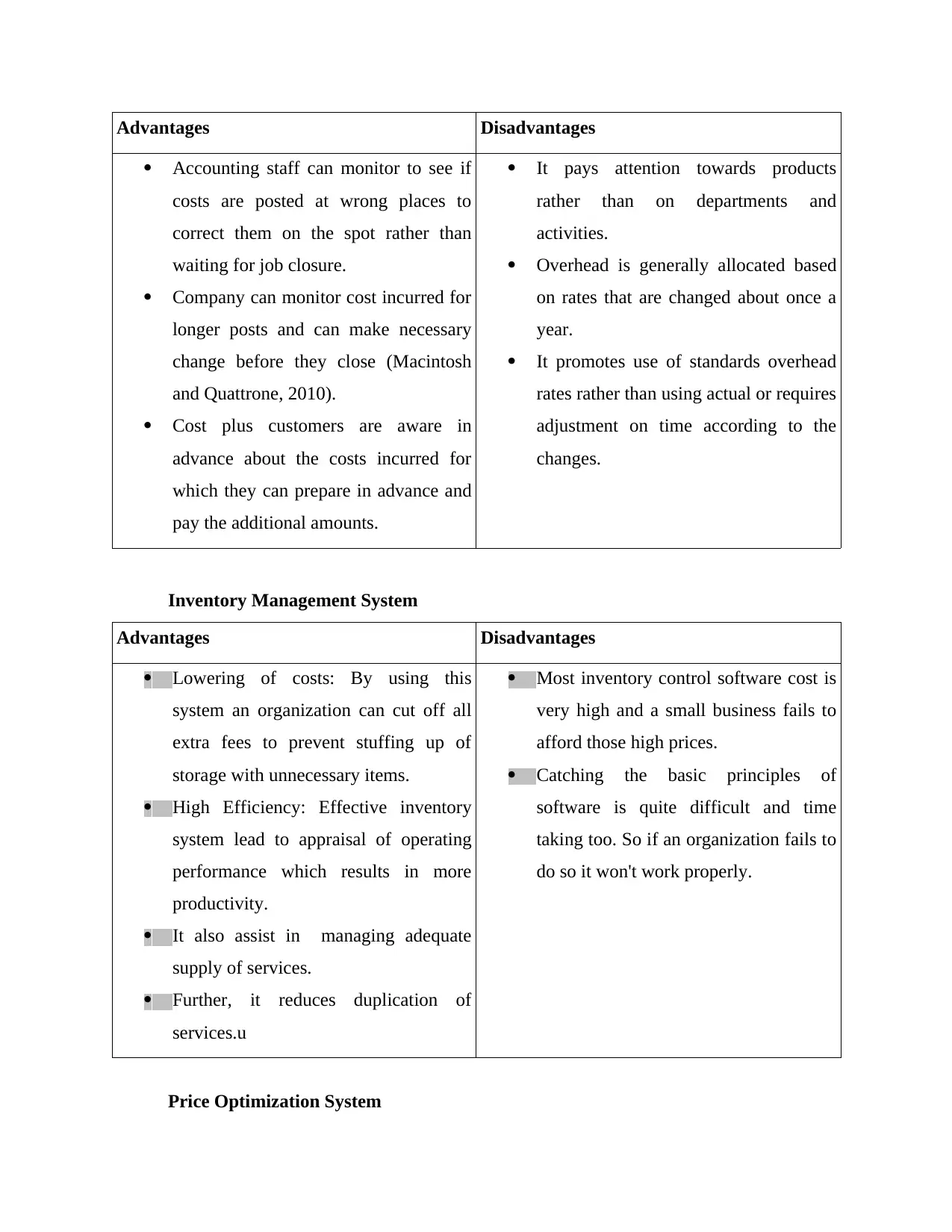

Job Costing System

Advantages Disadvantages

Accounting staff can monitor to see if

costs are posted at wrong places to

correct them on the spot rather than

waiting for job closure.

Company can monitor cost incurred for

longer posts and can make necessary

change before they close (Macintosh

and Quattrone, 2010).

Cost plus customers are aware in

advance about the costs incurred for

which they can prepare in advance and

pay the additional amounts.

It pays attention towards products

rather than on departments and

activities.

Overhead is generally allocated based

on rates that are changed about once a

year.

It promotes use of standards overhead

rates rather than using actual or requires

adjustment on time according to the

changes.

Inventory Management System

Advantages Disadvantages

Lowering of costs: By using this

system an organization can cut off all

extra fees to prevent stuffing up of

storage with unnecessary items.

High Efficiency: Effective inventory

system lead to appraisal of operating

performance which results in more

productivity.

It also assist in managing adequate

supply of services.

Further, it reduces duplication of

services.u

Most inventory control software cost is

very high and a small business fails to

afford those high prices.

Catching the basic principles of

software is quite difficult and time

taking too. So if an organization fails to

do so it won't work properly.

Price Optimization System

Accounting staff can monitor to see if

costs are posted at wrong places to

correct them on the spot rather than

waiting for job closure.

Company can monitor cost incurred for

longer posts and can make necessary

change before they close (Macintosh

and Quattrone, 2010).

Cost plus customers are aware in

advance about the costs incurred for

which they can prepare in advance and

pay the additional amounts.

It pays attention towards products

rather than on departments and

activities.

Overhead is generally allocated based

on rates that are changed about once a

year.

It promotes use of standards overhead

rates rather than using actual or requires

adjustment on time according to the

changes.

Inventory Management System

Advantages Disadvantages

Lowering of costs: By using this

system an organization can cut off all

extra fees to prevent stuffing up of

storage with unnecessary items.

High Efficiency: Effective inventory

system lead to appraisal of operating

performance which results in more

productivity.

It also assist in managing adequate

supply of services.

Further, it reduces duplication of

services.u

Most inventory control software cost is

very high and a small business fails to

afford those high prices.

Catching the basic principles of

software is quite difficult and time

taking too. So if an organization fails to

do so it won't work properly.

Price Optimization System

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Advantages Disadvantages

Industry Standard: Pricing according to

the mix of cost of producing the

product is quite easy.

Price Management : Some managers

price the product to maintain cost

effectiveness of goods and services

regardless of buyers expectations , this

lead the organization to suffer losses.

D. Evaluation of management accounting systems and management accounting reporting

From assessment, it has identified that management accouting systems and reporting is

highly integrated with each other. It is very important for Qbic hotel to translate their effects of

operations into financial information to accomplish goals in a well manner. By quantifying

effects and ramifications of stakeholder’s information, management team can get suitable data

for decision making. It is better to start computerized accounting as it is more efficient and fast

as well, this process is compact also with minimised costs (Marks, Sisirak and Heller, 2010).

Integration helps in standardizing procedures for recording transactions and disseminating

financial information. It interconnects the reporting activities of different functional areas of your

business such as point of sale, stores, back office and front office. Hence, management

accounting reports and systems are integrated to supply accurate information for taking decision.

It is important as well to integrate management accounting system, to avail accurate and specific

information which in turn results in effective decision making. It is very good for an organization

to have an effective decision making power to set standards for procedures of recording

transactions.

TASK 2

A.1 Absorption Costing and Marginal Costing methods

For determining cost and assessing profitability aspect Qbic can use one of the following

techniques such as:

Absorption Costing: Such method focuses on absorbing manufacturing costs by the units

produced. In simple words, it includes cost of finished unit in inventory inclusive of direct

materials and labours. This is also known as full, direct and variable costing as it considers both

Industry Standard: Pricing according to

the mix of cost of producing the

product is quite easy.

Price Management : Some managers

price the product to maintain cost

effectiveness of goods and services

regardless of buyers expectations , this

lead the organization to suffer losses.

D. Evaluation of management accounting systems and management accounting reporting

From assessment, it has identified that management accouting systems and reporting is

highly integrated with each other. It is very important for Qbic hotel to translate their effects of

operations into financial information to accomplish goals in a well manner. By quantifying

effects and ramifications of stakeholder’s information, management team can get suitable data

for decision making. It is better to start computerized accounting as it is more efficient and fast

as well, this process is compact also with minimised costs (Marks, Sisirak and Heller, 2010).

Integration helps in standardizing procedures for recording transactions and disseminating

financial information. It interconnects the reporting activities of different functional areas of your

business such as point of sale, stores, back office and front office. Hence, management

accounting reports and systems are integrated to supply accurate information for taking decision.

It is important as well to integrate management accounting system, to avail accurate and specific

information which in turn results in effective decision making. It is very good for an organization

to have an effective decision making power to set standards for procedures of recording

transactions.

TASK 2

A.1 Absorption Costing and Marginal Costing methods

For determining cost and assessing profitability aspect Qbic can use one of the following

techniques such as:

Absorption Costing: Such method focuses on absorbing manufacturing costs by the units

produced. In simple words, it includes cost of finished unit in inventory inclusive of direct

materials and labours. This is also known as full, direct and variable costing as it considers both

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

fixed and variable expenses while determining production cost. For the determination of

production expenses company considers both fixed and variable expenses. This type of costing is

often needed for external financial reporting and beneficial for income tax purpose.

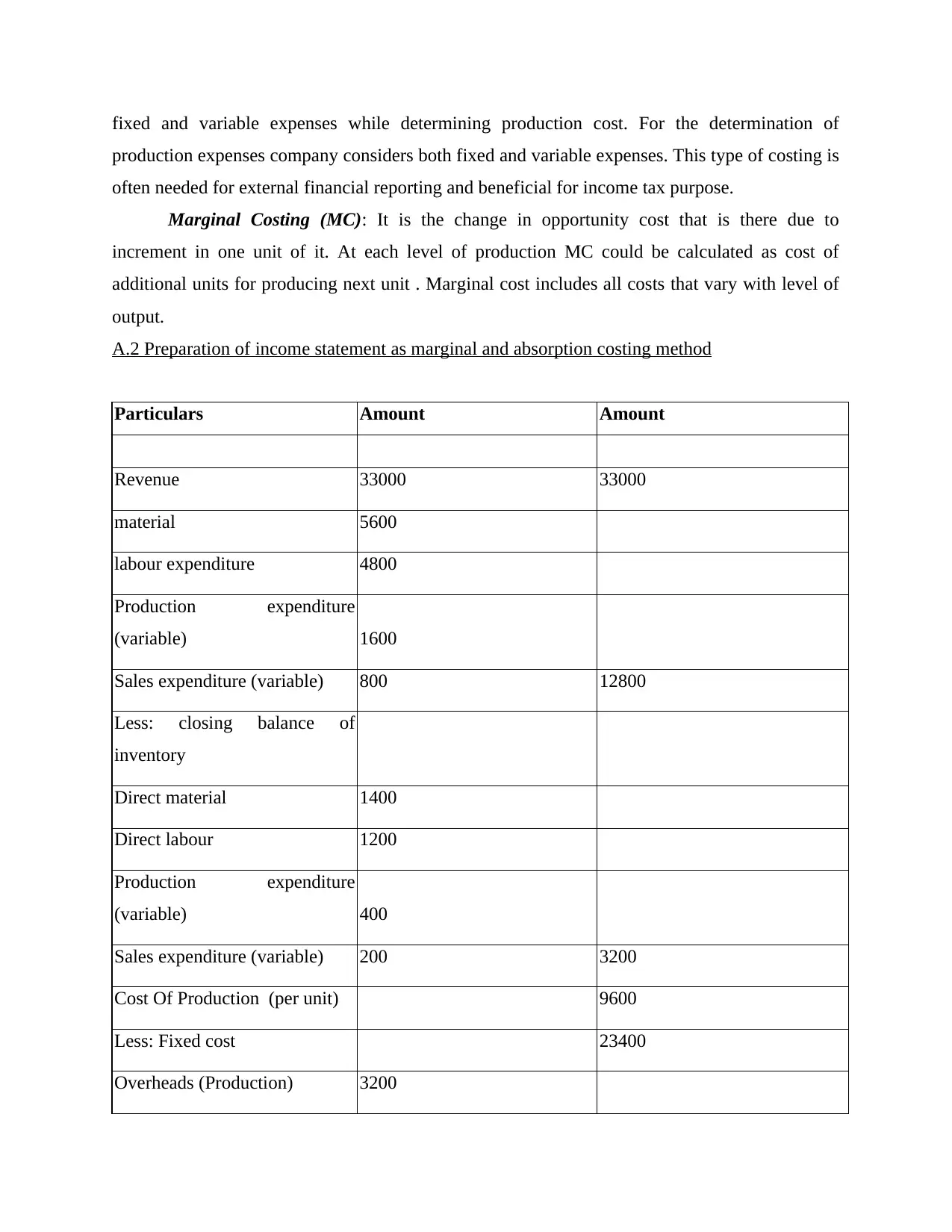

Marginal Costing (MC): It is the change in opportunity cost that is there due to

increment in one unit of it. At each level of production MC could be calculated as cost of

additional units for producing next unit . Marginal cost includes all costs that vary with level of

output.

A.2 Preparation of income statement as marginal and absorption costing method

Particulars Amount Amount

Revenue 33000 33000

material 5600

labour expenditure 4800

Production expenditure

(variable) 1600

Sales expenditure (variable) 800 12800

Less: closing balance of

inventory

Direct material 1400

Direct labour 1200

Production expenditure

(variable) 400

Sales expenditure (variable) 200 3200

Cost Of Production (per unit) 9600

Less: Fixed cost 23400

Overheads (Production) 3200

production expenses company considers both fixed and variable expenses. This type of costing is

often needed for external financial reporting and beneficial for income tax purpose.

Marginal Costing (MC): It is the change in opportunity cost that is there due to

increment in one unit of it. At each level of production MC could be calculated as cost of

additional units for producing next unit . Marginal cost includes all costs that vary with level of

output.

A.2 Preparation of income statement as marginal and absorption costing method

Particulars Amount Amount

Revenue 33000 33000

material 5600

labour expenditure 4800

Production expenditure

(variable) 1600

Sales expenditure (variable) 800 12800

Less: closing balance of

inventory

Direct material 1400

Direct labour 1200

Production expenditure

(variable) 400

Sales expenditure (variable) 200 3200

Cost Of Production (per unit) 9600

Less: Fixed cost 23400

Overheads (Production) 3200

Fixed administrative

expenditure 1200

Fixed selling expenditure 1500

5900

Net income 17500

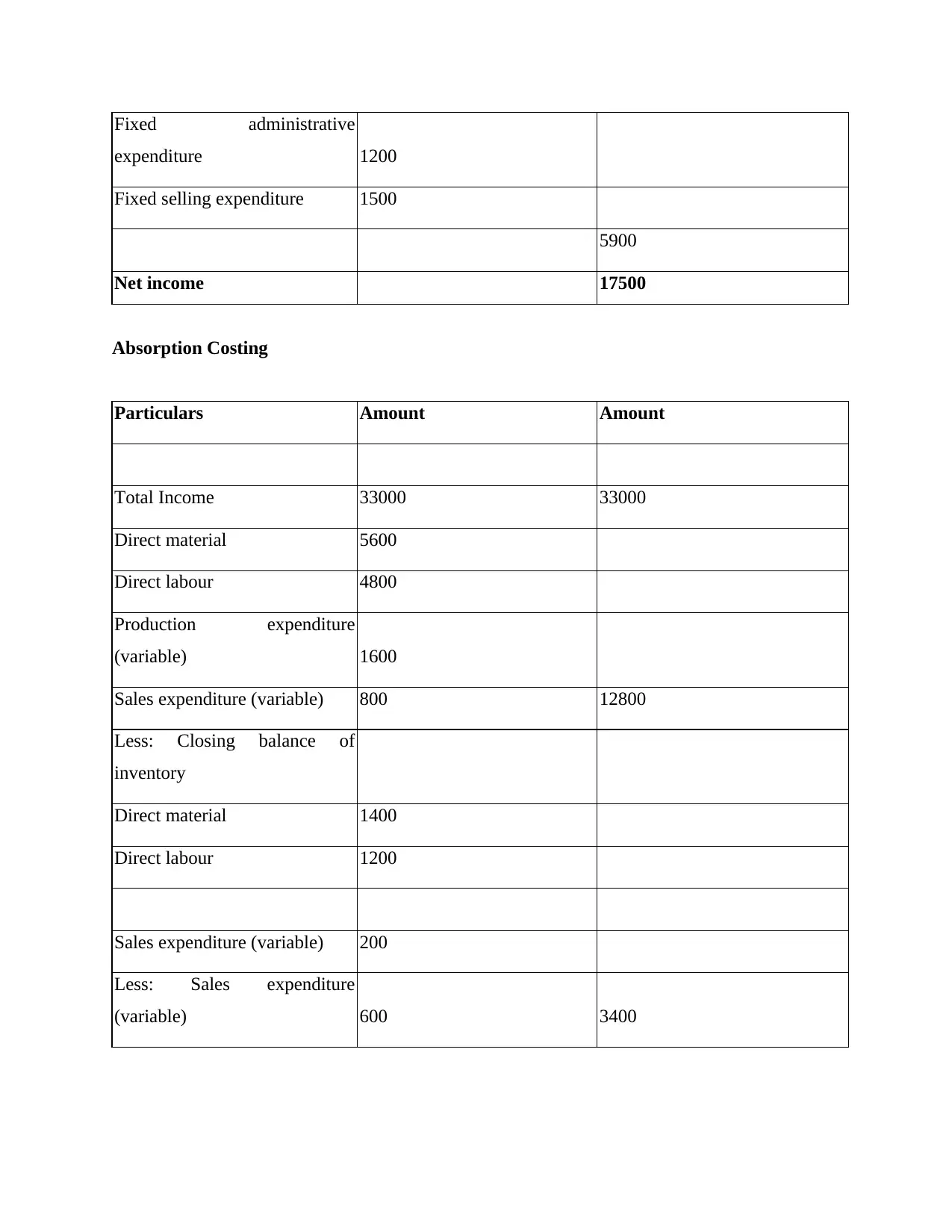

Absorption Costing

Particulars Amount Amount

Total Income 33000 33000

Direct material 5600

Direct labour 4800

Production expenditure

(variable) 1600

Sales expenditure (variable) 800 12800

Less: Closing balance of

inventory

Direct material 1400

Direct labour 1200

Sales expenditure (variable) 200

Less: Sales expenditure

(variable) 600 3400

expenditure 1200

Fixed selling expenditure 1500

5900

Net income 17500

Absorption Costing

Particulars Amount Amount

Total Income 33000 33000

Direct material 5600

Direct labour 4800

Production expenditure

(variable) 1600

Sales expenditure (variable) 800 12800

Less: Closing balance of

inventory

Direct material 1400

Direct labour 1200

Sales expenditure (variable) 200

Less: Sales expenditure

(variable) 600 3400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

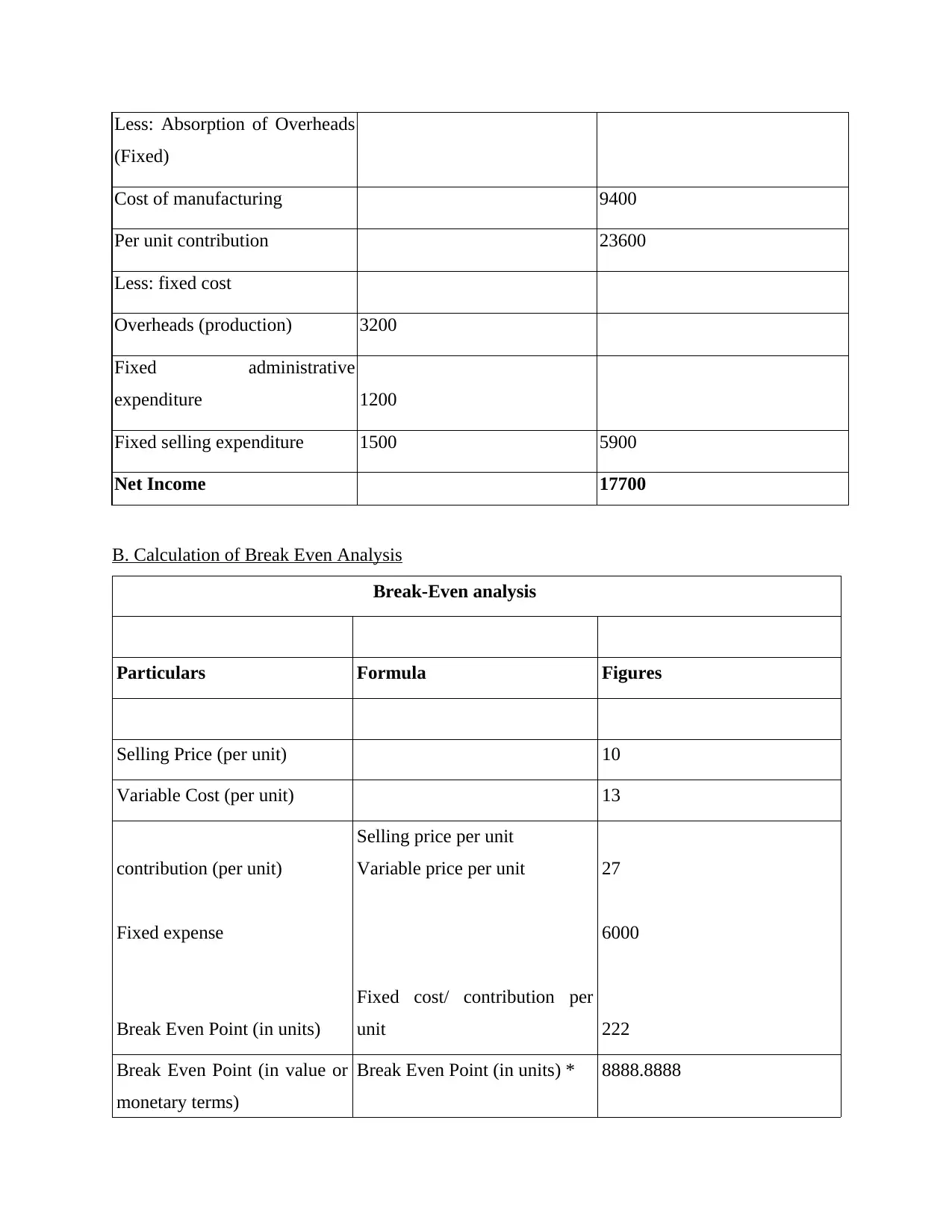

Less: Absorption of Overheads

(Fixed)

Cost of manufacturing 9400

Per unit contribution 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative

expenditure 1200

Fixed selling expenditure 1500 5900

Net Income 17700

B. Calculation of Break Even Analysis

Break-Even analysis

Particulars Formula Figures

Selling Price (per unit) 10

Variable Cost (per unit) 13

contribution (per unit)

Fixed expense

Break Even Point (in units)

Selling price per unit

Variable price per unit

Fixed cost/ contribution per

unit

27

6000

222

Break Even Point (in value or

monetary terms)

Break Even Point (in units) * 8888.8888

(Fixed)

Cost of manufacturing 9400

Per unit contribution 23600

Less: fixed cost

Overheads (production) 3200

Fixed administrative

expenditure 1200

Fixed selling expenditure 1500 5900

Net Income 17700

B. Calculation of Break Even Analysis

Break-Even analysis

Particulars Formula Figures

Selling Price (per unit) 10

Variable Cost (per unit) 13

contribution (per unit)

Fixed expense

Break Even Point (in units)

Selling price per unit

Variable price per unit

Fixed cost/ contribution per

unit

27

6000

222

Break Even Point (in value or

monetary terms)

Break Even Point (in units) * 8888.8888

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

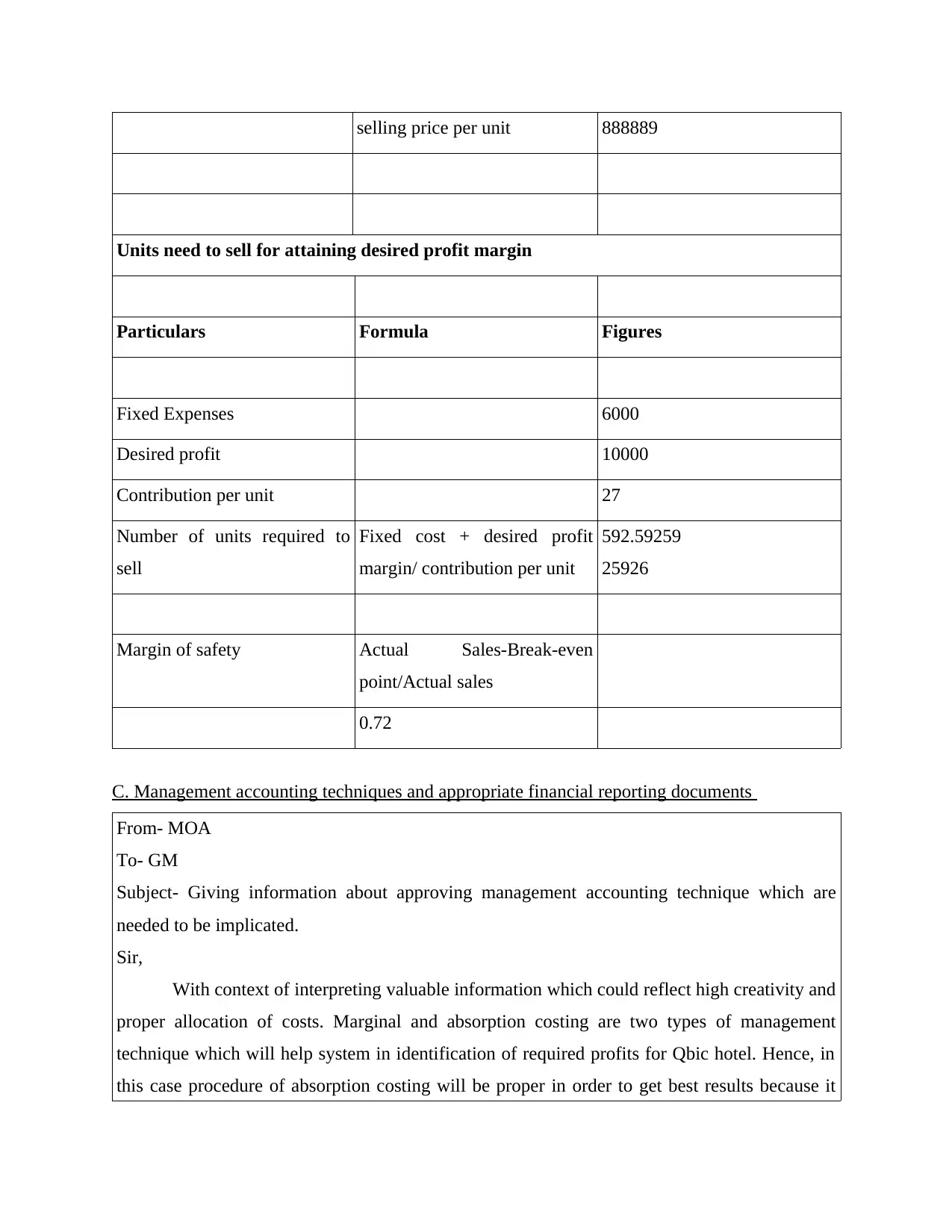

selling price per unit 888889

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed Expenses 6000

Desired profit 10000

Contribution per unit 27

Number of units required to

sell

Fixed cost + desired profit

margin/ contribution per unit

592.59259

25926

Margin of safety Actual Sales-Break-even

point/Actual sales

0.72

C. Management accounting techniques and appropriate financial reporting documents

From- MOA

To- GM

Subject- Giving information about approving management accounting technique which are

needed to be implicated.

Sir,

With context of interpreting valuable information which could reflect high creativity and

proper allocation of costs. Marginal and absorption costing are two types of management

technique which will help system in identification of required profits for Qbic hotel. Hence, in

this case procedure of absorption costing will be proper in order to get best results because it

Units need to sell for attaining desired profit margin

Particulars Formula Figures

Fixed Expenses 6000

Desired profit 10000

Contribution per unit 27

Number of units required to

sell

Fixed cost + desired profit

margin/ contribution per unit

592.59259

25926

Margin of safety Actual Sales-Break-even

point/Actual sales

0.72

C. Management accounting techniques and appropriate financial reporting documents

From- MOA

To- GM

Subject- Giving information about approving management accounting technique which are

needed to be implicated.

Sir,

With context of interpreting valuable information which could reflect high creativity and

proper allocation of costs. Marginal and absorption costing are two types of management

technique which will help system in identification of required profits for Qbic hotel. Hence, in

this case procedure of absorption costing will be proper in order to get best results because it

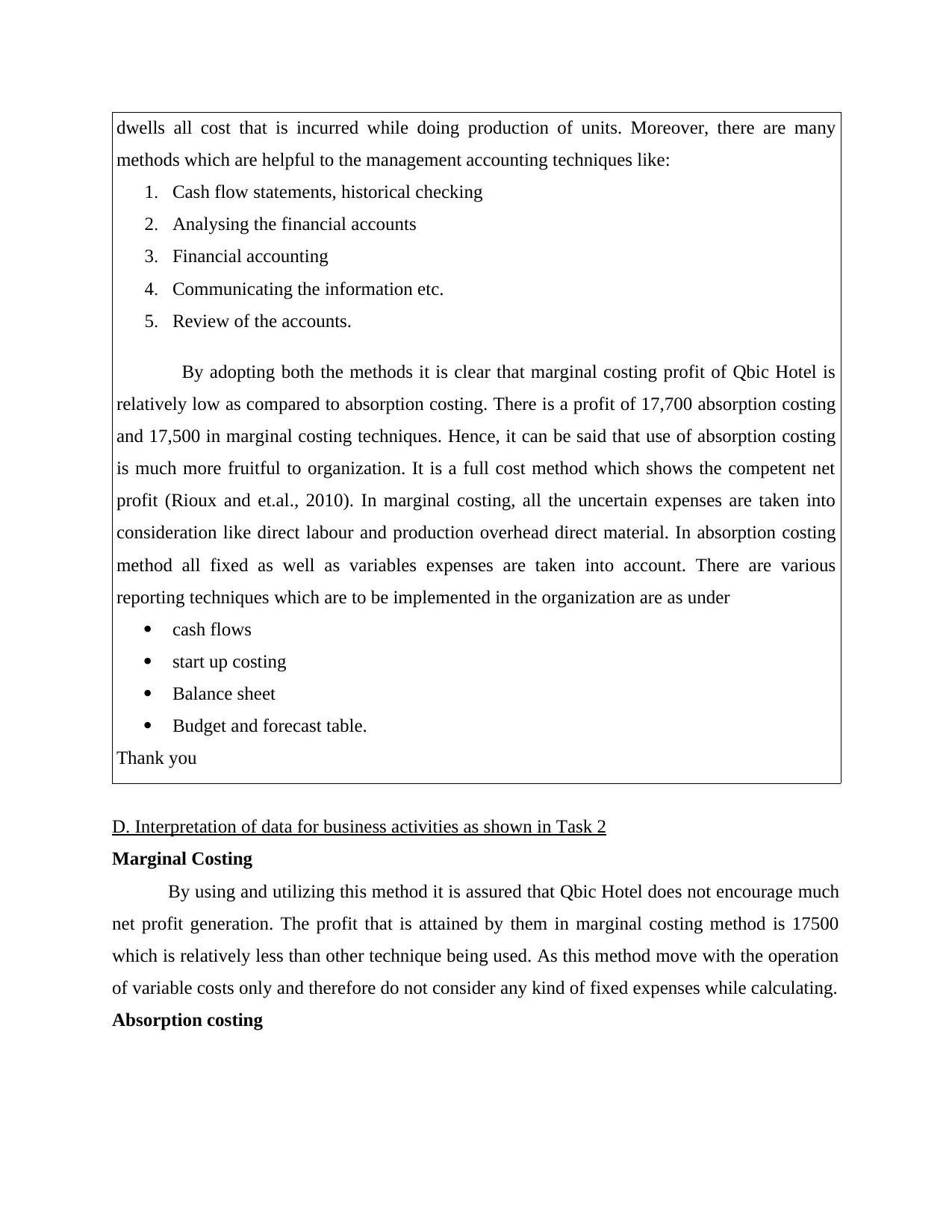

dwells all cost that is incurred while doing production of units. Moreover, there are many

methods which are helpful to the management accounting techniques like:

1. Cash flow statements, historical checking

2. Analysing the financial accounts

3. Financial accounting

4. Communicating the information etc.

5. Review of the accounts.

By adopting both the methods it is clear that marginal costing profit of Qbic Hotel is

relatively low as compared to absorption costing. There is a profit of 17,700 absorption costing

and 17,500 in marginal costing techniques. Hence, it can be said that use of absorption costing

is much more fruitful to organization. It is a full cost method which shows the competent net

profit (Rioux and et.al., 2010). In marginal costing, all the uncertain expenses are taken into

consideration like direct labour and production overhead direct material. In absorption costing

method all fixed as well as variables expenses are taken into account. There are various

reporting techniques which are to be implemented in the organization are as under

cash flows

start up costing

Balance sheet

Budget and forecast table.

Thank you

D. Interpretation of data for business activities as shown in Task 2

Marginal Costing

By using and utilizing this method it is assured that Qbic Hotel does not encourage much

net profit generation. The profit that is attained by them in marginal costing method is 17500

which is relatively less than other technique being used. As this method move with the operation

of variable costs only and therefore do not consider any kind of fixed expenses while calculating.

Absorption costing

methods which are helpful to the management accounting techniques like:

1. Cash flow statements, historical checking

2. Analysing the financial accounts

3. Financial accounting

4. Communicating the information etc.

5. Review of the accounts.

By adopting both the methods it is clear that marginal costing profit of Qbic Hotel is

relatively low as compared to absorption costing. There is a profit of 17,700 absorption costing

and 17,500 in marginal costing techniques. Hence, it can be said that use of absorption costing

is much more fruitful to organization. It is a full cost method which shows the competent net

profit (Rioux and et.al., 2010). In marginal costing, all the uncertain expenses are taken into

consideration like direct labour and production overhead direct material. In absorption costing

method all fixed as well as variables expenses are taken into account. There are various

reporting techniques which are to be implemented in the organization are as under

cash flows

start up costing

Balance sheet

Budget and forecast table.

Thank you

D. Interpretation of data for business activities as shown in Task 2

Marginal Costing

By using and utilizing this method it is assured that Qbic Hotel does not encourage much

net profit generation. The profit that is attained by them in marginal costing method is 17500

which is relatively less than other technique being used. As this method move with the operation

of variable costs only and therefore do not consider any kind of fixed expenses while calculating.

Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.