Management Accounting Systems and Techniques: Atex Media Analysis

VerifiedAdded on 2020/12/10

|16

|4052

|252

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques. It begins with an introduction to management accounting, emphasizing its significance in organizational growth and the need for appropriate systems. The report then delves into various management accounting methods, including cost accounting, actual costing, normal costing, and standard costing, with a focus on their application within Atex Media. Inventory management systems, including perpetual and periodic inventory methods, as well as FIFO, LIFO, and Just-in-Time approaches, are also discussed. Furthermore, the report examines job costing systems and the different types of management accounting reports, such as cost accounting reports, budget reports, and accounts receivable reports, highlighting their importance in decision-making and providing transparent information. The report also differentiates between marginal costing and absorption costing, including a detailed comparison of their characteristics and impacts on profitability, supported by numerical examples. Finally, the report explores the advantages and disadvantages of planning tools used for budgetary control and compares the management accounting systems adopted by Atex Media and its competitor, Wolfram Research, in response to financial challenges, providing a well-rounded understanding of the subject.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Main Body.......................................................................................................................................1

P1 Management Accounting and its requirements......................................................................1

P2 The following are methods of that are used in Management Accounting Reporting............4

P3 Difference Between Marginal Costing and Absorption Costing...........................................5

P4. Advantages and Disadvantages of planning tools which are used for budgetary control....8

P5. Comparison of different management accounting system which are adapted by Atex

Media and its competitor Wolfram Research to respond financial problems.............................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

Main Body.......................................................................................................................................1

P1 Management Accounting and its requirements......................................................................1

P2 The following are methods of that are used in Management Accounting Reporting............4

P3 Difference Between Marginal Costing and Absorption Costing...........................................5

P4. Advantages and Disadvantages of planning tools which are used for budgetary control....8

P5. Comparison of different management accounting system which are adapted by Atex

Media and its competitor Wolfram Research to respond financial problems.............................9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is the specialised branch of accounting, as it plays very

important role in surviving and accomplishing growth in an organization(Macintosh and

Quattrone, 2010). In this presented scenario, there is a huge requirement for presence of

appropriate management accounting system to ensure proper functioning and operation of day to

day financial and non financial activities. This presented report will provide a brief discussion its

significance and types on the basis of Atex media. It will also put emphasis on various

information which is related to management accounting reports and its importance to

management. Further, advantages and disadvantages of accounting systems are also highlighted

with their application. Practical aspect of this report contains calculation on the basis of break

even formula accompanied by margin of safety. Moreover, different types of planning tools of

budgetary control are also mentioned in this paper.

Main Body

P1 Management Accounting and its requirements

Accounting- It is an systematic process to identify, record, summarize, measure and

communicate information about financial transactions that had been taken place in Atex Media.

Management Accounting - It is an process of preparation of management reports, accounts for

providing timely and accurate statistical and financial information that is required by managers

for making decisions in normal course of business(Ward, 2012). It helps in formulating policies

and that are to be adopted by management.

Financial Accounting – It is a field of accounting wherein preparation of financial statements

with help of money transactions that had occurred in business over a period of time(Shah, Malik

and Malik, 2011.).

If Financial accounting is considered which produces annual reports that are mainly for

stakeholders of company whereas management reports are generated monthly or weekly for Atex

Media internal persons such as Chief Executive Officers and managers of different departments.

The different types of management accounting systems that can be used by different departments

are-:

1. Cost Accounting – This is an method of accounting wherein all costs that are incurred

from an activity for completing any process are collected, classified and

recorded(Bebbington and Thomson, 2013). The aim of cost accounting is to know

1

Management accounting is the specialised branch of accounting, as it plays very

important role in surviving and accomplishing growth in an organization(Macintosh and

Quattrone, 2010). In this presented scenario, there is a huge requirement for presence of

appropriate management accounting system to ensure proper functioning and operation of day to

day financial and non financial activities. This presented report will provide a brief discussion its

significance and types on the basis of Atex media. It will also put emphasis on various

information which is related to management accounting reports and its importance to

management. Further, advantages and disadvantages of accounting systems are also highlighted

with their application. Practical aspect of this report contains calculation on the basis of break

even formula accompanied by margin of safety. Moreover, different types of planning tools of

budgetary control are also mentioned in this paper.

Main Body

P1 Management Accounting and its requirements

Accounting- It is an systematic process to identify, record, summarize, measure and

communicate information about financial transactions that had been taken place in Atex Media.

Management Accounting - It is an process of preparation of management reports, accounts for

providing timely and accurate statistical and financial information that is required by managers

for making decisions in normal course of business(Ward, 2012). It helps in formulating policies

and that are to be adopted by management.

Financial Accounting – It is a field of accounting wherein preparation of financial statements

with help of money transactions that had occurred in business over a period of time(Shah, Malik

and Malik, 2011.).

If Financial accounting is considered which produces annual reports that are mainly for

stakeholders of company whereas management reports are generated monthly or weekly for Atex

Media internal persons such as Chief Executive Officers and managers of different departments.

The different types of management accounting systems that can be used by different departments

are-:

1. Cost Accounting – This is an method of accounting wherein all costs that are incurred

from an activity for completing any process are collected, classified and

recorded(Bebbington and Thomson, 2013). The aim of cost accounting is to know

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company's cost of production through assessment of different costs at each stage of

production that re incurred.

1. Actual Costing – It is type of cost accounting wherein Atex Media can use any

system which uses actual fixed costs and direct costs, actual qualities that are used in

production for determination of cost of products(DRURY, 2013). The actual cost

accounting for calculating product costs are based on factors that are given below-:

1. Cost of Material= Actual Cost of Material* Actual Quantity Purchased

2. Cost of Labour= Actual Cost rates * Actual Quantities used

3. Overheads Costs that are allocated using actual quantity that are used in reporting

period.

This all cost are considered on actual basis that had been incurred.

2. Normal Costing – In this method cost are allocated on basis of material, labour, and

overheads that had been required in production of any product(Gupta, Pevzner and

Seethamraju, 2010). The total of all these costs are product costs that are used to

calculate Cost of Goods Sold and valuation of inventory. In this system of costing, cost

rates of manufacturing overhead are decided by management as these expenses includes

rent, electricity, depreciation etc that are related in production of product but can't be

directly applied to different items.

3. Standard Costing – In this technique of cost accounting where manufacturers identify

difference between actual costs of goods produced and with planned costs of production

of that product(Berry, 2010). Many manufacturers rather than assigning actual cost of

material, labour, overhead they assign expected or budgeted cost. So there valuation of

inventory and cost of goods sold are valued at standard cost but, as they have to pay

actual costs, so difference arising between these costs are known as variance(Tsorakidis

and et.al., 2011). The following are different types of variances-:

1. Material Variance

2. Labour Variance

3. Overhead Variance

4. Sales Variance

2

production that re incurred.

1. Actual Costing – It is type of cost accounting wherein Atex Media can use any

system which uses actual fixed costs and direct costs, actual qualities that are used in

production for determination of cost of products(DRURY, 2013). The actual cost

accounting for calculating product costs are based on factors that are given below-:

1. Cost of Material= Actual Cost of Material* Actual Quantity Purchased

2. Cost of Labour= Actual Cost rates * Actual Quantities used

3. Overheads Costs that are allocated using actual quantity that are used in reporting

period.

This all cost are considered on actual basis that had been incurred.

2. Normal Costing – In this method cost are allocated on basis of material, labour, and

overheads that had been required in production of any product(Gupta, Pevzner and

Seethamraju, 2010). The total of all these costs are product costs that are used to

calculate Cost of Goods Sold and valuation of inventory. In this system of costing, cost

rates of manufacturing overhead are decided by management as these expenses includes

rent, electricity, depreciation etc that are related in production of product but can't be

directly applied to different items.

3. Standard Costing – In this technique of cost accounting where manufacturers identify

difference between actual costs of goods produced and with planned costs of production

of that product(Berry, 2010). Many manufacturers rather than assigning actual cost of

material, labour, overhead they assign expected or budgeted cost. So there valuation of

inventory and cost of goods sold are valued at standard cost but, as they have to pay

actual costs, so difference arising between these costs are known as variance(Tsorakidis

and et.al., 2011). The following are different types of variances-:

1. Material Variance

2. Labour Variance

3. Overhead Variance

4. Sales Variance

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

If Actual costs are more than standards cost that are measured than it is an Unfavourable

Variance which states that if other things related to cost are constant that profit that had been

planned will be more than actual.

If Planned costs are more than actual costs than it is an Favourable Variance which states that if

other things are constant than profit of company will be more than what had been planned.

Inventory Management System-: This is a process where monitoring and maintenance of

products that are kept as stock whether this product are raw material or it can be finished goods

that are ready to use in manufacturing process or for sale to end consumers(Cafferky, and

Wentworth, 2010). It is a system that can be used for managing inventory levels, Purchase

orders, Sales orders etc. of Atex Media. There are three types of Inventory

1. Raw Material-: These are material that are used in primary production or manufacturing

any product.(Cull and et.al., 2014) It is also known as unprocessed material than can be

used to produce any finished goods. For example a manufacturer of garments Cloth will

be there raw material

2. Work in Progress-: These inventory are that had been partially converted to finished

goods and can be said as finished goods which are awaiting for completion. For Example

cloth converted to any product like shirt but buttons that are to be stitched are left this

inventory is WIP.

3. Finished Goods-: These are end product of production after completion of

manufacturing process that will be used for sale to end consumers. Ex Shirt that had been

made by manufacturer.

The Different Methods through which inventory can be managed

1. Perpetual Inventory- It is a method which records sales and purchase at point of sale or

on daily basis. In this Book inventory will be same as physical stock that had been kept in

godown.

2. Periodic Inventory- In this method updates are made on periodical basis in which

physical stock is taken at specific intervals. This system is applied only where there no of

products are low and are slow moving(Cull, R., and et.al., 2014).

3. FIFO- First in First out method states that material that are purchased first are to sold first

by Atex Media.

3

Variance which states that if other things related to cost are constant that profit that had been

planned will be more than actual.

If Planned costs are more than actual costs than it is an Favourable Variance which states that if

other things are constant than profit of company will be more than what had been planned.

Inventory Management System-: This is a process where monitoring and maintenance of

products that are kept as stock whether this product are raw material or it can be finished goods

that are ready to use in manufacturing process or for sale to end consumers(Cafferky, and

Wentworth, 2010). It is a system that can be used for managing inventory levels, Purchase

orders, Sales orders etc. of Atex Media. There are three types of Inventory

1. Raw Material-: These are material that are used in primary production or manufacturing

any product.(Cull and et.al., 2014) It is also known as unprocessed material than can be

used to produce any finished goods. For example a manufacturer of garments Cloth will

be there raw material

2. Work in Progress-: These inventory are that had been partially converted to finished

goods and can be said as finished goods which are awaiting for completion. For Example

cloth converted to any product like shirt but buttons that are to be stitched are left this

inventory is WIP.

3. Finished Goods-: These are end product of production after completion of

manufacturing process that will be used for sale to end consumers. Ex Shirt that had been

made by manufacturer.

The Different Methods through which inventory can be managed

1. Perpetual Inventory- It is a method which records sales and purchase at point of sale or

on daily basis. In this Book inventory will be same as physical stock that had been kept in

godown.

2. Periodic Inventory- In this method updates are made on periodical basis in which

physical stock is taken at specific intervals. This system is applied only where there no of

products are low and are slow moving(Cull, R., and et.al., 2014).

3. FIFO- First in First out method states that material that are purchased first are to sold first

by Atex Media.

3

4. LIFO- Last in First out states that material that had been purchased last will be sold first.

This method of inventory valuation is banned by HMRC.

5. Just in Time- In this system strategy of management is to assign raw material order from

suppliers when as required in production process. By this it eliminates an good amount of

investment in inventory that are required in production process which directly reduces

working capital of Atex Media.

Job Costing Systems- this is method of costing are used in situation when it is order specific and

where each work is different and to be done as per specification of customers. It can be said as

process for determining material and labour cost for a specific Job for creating information that

is to be quoted of customer.

Example of Job Costing -: A company XYZ Ltd had ordered a specific machine to ABC Ltd for

which XYZ had to make new construction in company and buy specific products for making that

So the costing that had been specifically done for making that machine is known as Job Costing.

P2 The following are methods of that are used in Management Accounting Reporting

Management Accounting Reports

These are reports that provide information that are needed in reducing costs, awarding

performance of employees, eliminating product lines that are not profitable and provide the best

financial return to business(Cull, R., and et.al., 2014). These reports are made on weekely,

monthly which is depended upon time sensitivity of financial information. The following are

types of Management Reports-:

1. Cost Accounting Report-: It is a management report that states that costs that had been

occurred till date on different products. This helps in knowing management about costs

that are been incurred for manufacturing any product and expenses that are associated

with it.

2. Budget Report-: This report is an internal report that is been used by management for

comparing estimated data with actual performance of Atex Media. Budgets are based on

estimations so they can be inaccurate and can differ largely from actuals that had been

4

This method of inventory valuation is banned by HMRC.

5. Just in Time- In this system strategy of management is to assign raw material order from

suppliers when as required in production process. By this it eliminates an good amount of

investment in inventory that are required in production process which directly reduces

working capital of Atex Media.

Job Costing Systems- this is method of costing are used in situation when it is order specific and

where each work is different and to be done as per specification of customers. It can be said as

process for determining material and labour cost for a specific Job for creating information that

is to be quoted of customer.

Example of Job Costing -: A company XYZ Ltd had ordered a specific machine to ABC Ltd for

which XYZ had to make new construction in company and buy specific products for making that

So the costing that had been specifically done for making that machine is known as Job Costing.

P2 The following are methods of that are used in Management Accounting Reporting

Management Accounting Reports

These are reports that provide information that are needed in reducing costs, awarding

performance of employees, eliminating product lines that are not profitable and provide the best

financial return to business(Cull, R., and et.al., 2014). These reports are made on weekely,

monthly which is depended upon time sensitivity of financial information. The following are

types of Management Reports-:

1. Cost Accounting Report-: It is a management report that states that costs that had been

occurred till date on different products. This helps in knowing management about costs

that are been incurred for manufacturing any product and expenses that are associated

with it.

2. Budget Report-: This report is an internal report that is been used by management for

comparing estimated data with actual performance of Atex Media. Budgets are based on

estimations so they can be inaccurate and can differ largely from actuals that had been

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

occurred. So for finding estimations that are made are going in correct manner budget

reports are formed.

3. Account Receivable Report-:This reports provides lists of unpaid amount of debtors. This

report are mostly used by collection department for determining invoices which are due

for payment and name of parties from whom payment is due(Parmenter, 2015).

The Following are importance of such reports-:

1. It helps In decision making-: This management reports helps in decision making of Atex

Media as through this they will know how work is going on in there organisation and

make changes according to it.

2. Helps in speeding up there process and can save time of Atex Media

3. Management reports helps in providing transparent and reliable information to users for

whom they are mane

4. Through these reports' clarification part of managers reduces so as everything is

presented in data form.

P3 Difference Between Marginal Costing and Absorption Costing

Basis of Difference Absorption Costing Marginal Costing

Meaning For Determination of product cost

total cost is apportioned to cost centre

It is an decision making technique

through which total cost of any

production is ascertained.

Overheads

Classification

Administration, Production, Selling

and Distribution

Variable and Fixed

Profitability As in this fixed cost is included profit

gets affected

Measured through PV Ratio ie

Profit Volume ratio

Recognition of

Cost

Variable and Fixed Cost both are

considered as cost of product

Fixed cost is recognised as period

cost whereas variable cost is

product cost.

Cost Per Unit Difference in opening and closing

inventory affects cost per unit

No influence of opening and

closing stock

Cost Data In this costing, cost data is presented It is presented for outline of total

5

reports are formed.

3. Account Receivable Report-:This reports provides lists of unpaid amount of debtors. This

report are mostly used by collection department for determining invoices which are due

for payment and name of parties from whom payment is due(Parmenter, 2015).

The Following are importance of such reports-:

1. It helps In decision making-: This management reports helps in decision making of Atex

Media as through this they will know how work is going on in there organisation and

make changes according to it.

2. Helps in speeding up there process and can save time of Atex Media

3. Management reports helps in providing transparent and reliable information to users for

whom they are mane

4. Through these reports' clarification part of managers reduces so as everything is

presented in data form.

P3 Difference Between Marginal Costing and Absorption Costing

Basis of Difference Absorption Costing Marginal Costing

Meaning For Determination of product cost

total cost is apportioned to cost centre

It is an decision making technique

through which total cost of any

production is ascertained.

Overheads

Classification

Administration, Production, Selling

and Distribution

Variable and Fixed

Profitability As in this fixed cost is included profit

gets affected

Measured through PV Ratio ie

Profit Volume ratio

Recognition of

Cost

Variable and Fixed Cost both are

considered as cost of product

Fixed cost is recognised as period

cost whereas variable cost is

product cost.

Cost Per Unit Difference in opening and closing

inventory affects cost per unit

No influence of opening and

closing stock

Cost Data In this costing, cost data is presented It is presented for outline of total

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

in traditional form NP is ascertained

after deducting Fixed and variable

cost

cost of each product

Calculation of Net profit using Absorption Costing-:

Sales Revenue

Particulars Amount in Pounds

Sale Price per Unit 55

No. of Units 600

Total Sales Revenue(a) 33000

Calculation of Total Overheads

No. of Units 600

Direct Material Per Unit 7

Direct Labour Per Unit 6

Variable Production Overheads P.U 2

Variable Sales Overhead P.U 1

Total Overheads 16

Total Cost of Production (b) 9600

Calculation of Contribution

Contribution c=(a-b) 23400

Calculation of Total fixed Costs

Production Overheads 3200

Administration Overheads 1200

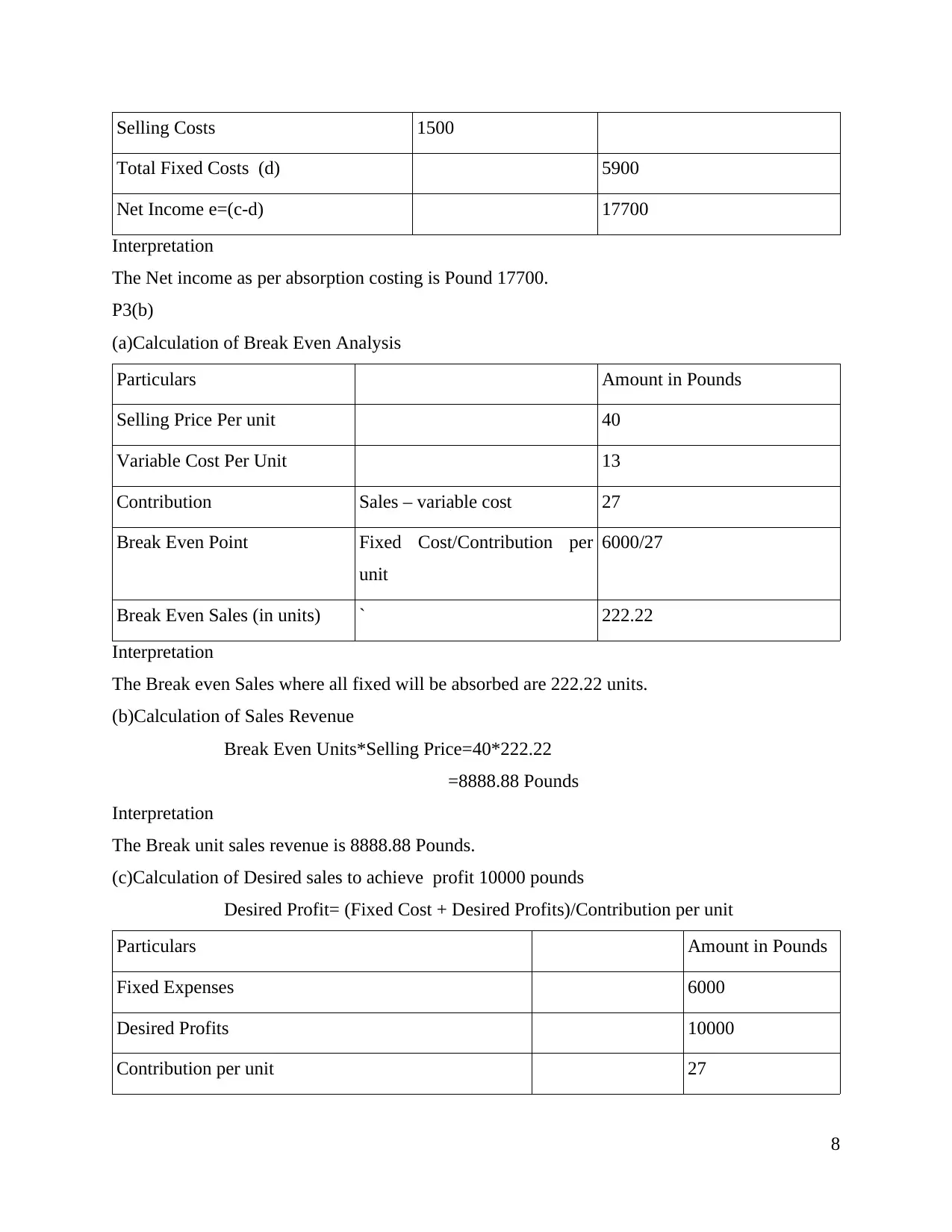

Selling Costs 1500

Total Fixed Costs (d) 5900

6

after deducting Fixed and variable

cost

cost of each product

Calculation of Net profit using Absorption Costing-:

Sales Revenue

Particulars Amount in Pounds

Sale Price per Unit 55

No. of Units 600

Total Sales Revenue(a) 33000

Calculation of Total Overheads

No. of Units 600

Direct Material Per Unit 7

Direct Labour Per Unit 6

Variable Production Overheads P.U 2

Variable Sales Overhead P.U 1

Total Overheads 16

Total Cost of Production (b) 9600

Calculation of Contribution

Contribution c=(a-b) 23400

Calculation of Total fixed Costs

Production Overheads 3200

Administration Overheads 1200

Selling Costs 1500

Total Fixed Costs (d) 5900

6

Net Income e=(c-d) 17500

Interpretation

The net income without using absorption costing is pound 17500.

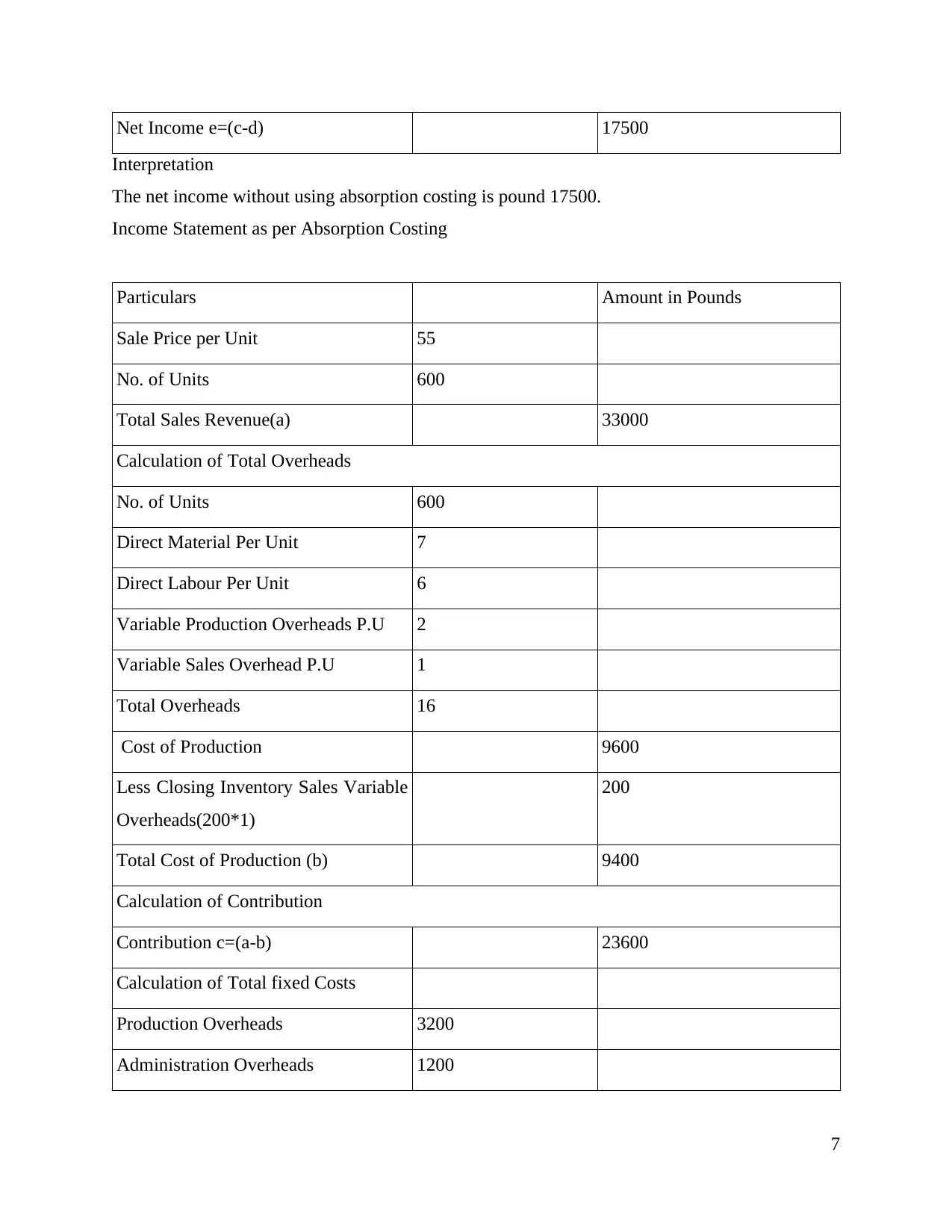

Income Statement as per Absorption Costing

Particulars Amount in Pounds

Sale Price per Unit 55

No. of Units 600

Total Sales Revenue(a) 33000

Calculation of Total Overheads

No. of Units 600

Direct Material Per Unit 7

Direct Labour Per Unit 6

Variable Production Overheads P.U 2

Variable Sales Overhead P.U 1

Total Overheads 16

Cost of Production 9600

Less Closing Inventory Sales Variable

Overheads(200*1)

200

Total Cost of Production (b) 9400

Calculation of Contribution

Contribution c=(a-b) 23600

Calculation of Total fixed Costs

Production Overheads 3200

Administration Overheads 1200

7

Interpretation

The net income without using absorption costing is pound 17500.

Income Statement as per Absorption Costing

Particulars Amount in Pounds

Sale Price per Unit 55

No. of Units 600

Total Sales Revenue(a) 33000

Calculation of Total Overheads

No. of Units 600

Direct Material Per Unit 7

Direct Labour Per Unit 6

Variable Production Overheads P.U 2

Variable Sales Overhead P.U 1

Total Overheads 16

Cost of Production 9600

Less Closing Inventory Sales Variable

Overheads(200*1)

200

Total Cost of Production (b) 9400

Calculation of Contribution

Contribution c=(a-b) 23600

Calculation of Total fixed Costs

Production Overheads 3200

Administration Overheads 1200

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Selling Costs 1500

Total Fixed Costs (d) 5900

Net Income e=(c-d) 17700

Interpretation

The Net income as per absorption costing is Pound 17700.

P3(b)

(a)Calculation of Break Even Analysis

Particulars Amount in Pounds

Selling Price Per unit 40

Variable Cost Per Unit 13

Contribution Sales – variable cost 27

Break Even Point Fixed Cost/Contribution per

unit

6000/27

Break Even Sales (in units) ` 222.22

Interpretation

The Break even Sales where all fixed will be absorbed are 222.22 units.

(b)Calculation of Sales Revenue

Break Even Units*Selling Price=40*222.22

=8888.88 Pounds

Interpretation

The Break unit sales revenue is 8888.88 Pounds.

(c)Calculation of Desired sales to achieve profit 10000 pounds

Desired Profit= (Fixed Cost + Desired Profits)/Contribution per unit

Particulars Amount in Pounds

Fixed Expenses 6000

Desired Profits 10000

Contribution per unit 27

8

Total Fixed Costs (d) 5900

Net Income e=(c-d) 17700

Interpretation

The Net income as per absorption costing is Pound 17700.

P3(b)

(a)Calculation of Break Even Analysis

Particulars Amount in Pounds

Selling Price Per unit 40

Variable Cost Per Unit 13

Contribution Sales – variable cost 27

Break Even Point Fixed Cost/Contribution per

unit

6000/27

Break Even Sales (in units) ` 222.22

Interpretation

The Break even Sales where all fixed will be absorbed are 222.22 units.

(b)Calculation of Sales Revenue

Break Even Units*Selling Price=40*222.22

=8888.88 Pounds

Interpretation

The Break unit sales revenue is 8888.88 Pounds.

(c)Calculation of Desired sales to achieve profit 10000 pounds

Desired Profit= (Fixed Cost + Desired Profits)/Contribution per unit

Particulars Amount in Pounds

Fixed Expenses 6000

Desired Profits 10000

Contribution per unit 27

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

No of Units that are required to achieve desired profits (6000+10000)/27 592.60 units

Interpretation

To achieve desired profits of Pound 10000 the organisation needs to sale 592.60 units

(d)Calculation of Margin of Safety if 800 units are sold

Margin of Safety=(Actual Sales- Break Even Point)/Actual Sales

=(800-222.22)/800

=.7223

Interpretation

The Margin of safety at 800 units is .7223.

P4. Advantages and Disadvantages of planning tools which are used for budgetary control

2. Cash Budget: This type of budgets are an estimation of the cash outflow and inflow in a

business for a specific time period(Cull, R., and et.al., 2014).

Advantages

4. It can avoid debt: It helps an organization to keep a safe amount of cash aside which

could be utilise to spend in emergency situation which can prevent any kind of debt.

5. Forced to budget better: As there are no out with this type of budgets which forces

households and businesses to budget in a better way(Cash Budget Advantages and

Disadvantages, 2018).

Disadvantages

4. Creates a danger of theft: Cash is the easiest asset that could be steal because it is not so

very easy to trace, as it is not possible to list each and every serial number of every bill a

business send outside(Attom, 2013).

5. It limits spending power: It is noticeable that many business have stopped accepting

cash for certain activities which has limited the spending power of Atex Media.

6. Operating budget: It is a financial plan which assists company in meeting its debt

obligations and to sustain growth for long term.

Advantages

4. Long ranged planning needs: Operational budget helps small businesses to allocate

money for over several quarters to three years in the future. It also allows an organization

to predict its costs and to manage its spending in the short term to meet its long etrm

financial needs.

9

Interpretation

To achieve desired profits of Pound 10000 the organisation needs to sale 592.60 units

(d)Calculation of Margin of Safety if 800 units are sold

Margin of Safety=(Actual Sales- Break Even Point)/Actual Sales

=(800-222.22)/800

=.7223

Interpretation

The Margin of safety at 800 units is .7223.

P4. Advantages and Disadvantages of planning tools which are used for budgetary control

2. Cash Budget: This type of budgets are an estimation of the cash outflow and inflow in a

business for a specific time period(Cull, R., and et.al., 2014).

Advantages

4. It can avoid debt: It helps an organization to keep a safe amount of cash aside which

could be utilise to spend in emergency situation which can prevent any kind of debt.

5. Forced to budget better: As there are no out with this type of budgets which forces

households and businesses to budget in a better way(Cash Budget Advantages and

Disadvantages, 2018).

Disadvantages

4. Creates a danger of theft: Cash is the easiest asset that could be steal because it is not so

very easy to trace, as it is not possible to list each and every serial number of every bill a

business send outside(Attom, 2013).

5. It limits spending power: It is noticeable that many business have stopped accepting

cash for certain activities which has limited the spending power of Atex Media.

6. Operating budget: It is a financial plan which assists company in meeting its debt

obligations and to sustain growth for long term.

Advantages

4. Long ranged planning needs: Operational budget helps small businesses to allocate

money for over several quarters to three years in the future. It also allows an organization

to predict its costs and to manage its spending in the short term to meet its long etrm

financial needs.

9

5. Building budget flexibility: It provides small businesses with more financial freedom as

it helps in building flexible spending amounts in order to meet unanticipated costs or to

seize new opportunities.

Disadvantages

5. Federal Tax complications: Building an operational budget to function at a loss can

result in generation of an IRS investigation and audit.

6. Keeping accurate information: As the financial information of a business changes from

one month to another(Pros & Cons of an Operational Budget, 2018). So in case if

operational budget is unable to change according to the changes and fails to reflect new

income figures, any projections that are contained in the operational budgets are

immediately inaccurate.

P5. Comparison of different management accounting system which are adapted by Atex Media

and its competitor Wolfram Research to respond financial problems

Bench Marking: In this financial problems are responded by measuring company's

products and services against the set standards of other businesses of same industry

which are considered to be the best.

Financial governance: In this type of management accounting system financial

problems are responded by managing, collecting, monitoring and controlling financial

information of Atex media. In simple words, these are the procedures and policies which

are used to manage data of business and to ensure its correctness(DRURY, 2013).

KPIs Key Performance Indicators: Atex media make use of this management

accounting system to measure effectiveness of company in achieving its main objectives

with the use of value in order to respond financial problems effectively.

Following mentioned accounting systems are used by Wolfram Research to respond financial

problems:

Balanced score Card: This metric is used by Wolfram Research to show performance

and strategic management in order to identify and improve various internal functions with

their resulting outcomes. This also helps in improving internal management function and

resulting outcome.

Budgetary Target: This is used by company with a basic motive of deriving cost targets

in a goal oriented manner.

10

it helps in building flexible spending amounts in order to meet unanticipated costs or to

seize new opportunities.

Disadvantages

5. Federal Tax complications: Building an operational budget to function at a loss can

result in generation of an IRS investigation and audit.

6. Keeping accurate information: As the financial information of a business changes from

one month to another(Pros & Cons of an Operational Budget, 2018). So in case if

operational budget is unable to change according to the changes and fails to reflect new

income figures, any projections that are contained in the operational budgets are

immediately inaccurate.

P5. Comparison of different management accounting system which are adapted by Atex Media

and its competitor Wolfram Research to respond financial problems

Bench Marking: In this financial problems are responded by measuring company's

products and services against the set standards of other businesses of same industry

which are considered to be the best.

Financial governance: In this type of management accounting system financial

problems are responded by managing, collecting, monitoring and controlling financial

information of Atex media. In simple words, these are the procedures and policies which

are used to manage data of business and to ensure its correctness(DRURY, 2013).

KPIs Key Performance Indicators: Atex media make use of this management

accounting system to measure effectiveness of company in achieving its main objectives

with the use of value in order to respond financial problems effectively.

Following mentioned accounting systems are used by Wolfram Research to respond financial

problems:

Balanced score Card: This metric is used by Wolfram Research to show performance

and strategic management in order to identify and improve various internal functions with

their resulting outcomes. This also helps in improving internal management function and

resulting outcome.

Budgetary Target: This is used by company with a basic motive of deriving cost targets

in a goal oriented manner.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.