Management Accounting Report: Planning, Costing, and Financial Issues

VerifiedAdded on 2020/11/23

|16

|5084

|485

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and practices. It begins with an introduction to management accounting, highlighting its essential requirements and benefits, including the importance of effective accounting systems for recording financial transactions and achieving organizational goals. The report then delves into various costing techniques, such as normal, standard, and actual costing, along with inventory management systems like LIFO and FIFO, and job-costing systems, all of which are crucial for calculating net income and making informed business decisions. Furthermore, it explores the merits and demerits of planning tools used in budgeting, offering insights into how these tools can be utilized to manage and control financial issues within an organization. The report also examines different types of management reporting, including performance reports, inventory management reports, and job cost reports, emphasizing their role in evaluating financial performance and making strategic decisions. Overall, the report provides a detailed overview of management accounting, covering costing, planning, and financial analysis, and the effective use of accounting systems to resolve financial problems.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Discussion about management accounting and their essential requirements.......................1

M1: Benefits of management accounting system.......................................................................3

P2: Different types of management reporting ...........................................................................4

D1: Critical evaluation of accounting system reporting.............................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing techniques that are use for calculating net income.......................6

M2: Various types of management accounting techniques.........................................................9

D2: Critical analyse of data collected from income statements................................................10

TASK 3..........................................................................................................................................10

P4: Merit and demerits of using planning tools use in budgets................................................10

M3: Analysis of use planning tools...........................................................................................12

D3: Critical evaluation to reduce financial issues.....................................................................12

TASK 4..........................................................................................................................................12

P5: Effective use of accounting system to resolve financial problem .....................................12

M4: Analysis of financial problem...........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Discussion about management accounting and their essential requirements.......................1

M1: Benefits of management accounting system.......................................................................3

P2: Different types of management reporting ...........................................................................4

D1: Critical evaluation of accounting system reporting.............................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing techniques that are use for calculating net income.......................6

M2: Various types of management accounting techniques.........................................................9

D2: Critical analyse of data collected from income statements................................................10

TASK 3..........................................................................................................................................10

P4: Merit and demerits of using planning tools use in budgets................................................10

M3: Analysis of use planning tools...........................................................................................12

D3: Critical evaluation to reduce financial issues.....................................................................12

TASK 4..........................................................................................................................................12

P5: Effective use of accounting system to resolve financial problem .....................................12

M4: Analysis of financial problem...........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Accounting is a systematic process of identify, recording, summarising and interpreting

financial data in effective manner. While management is held responsible for provide all

necessary requirements or support to financial accountants in respect to make better report during

an accounting period of time. The major objectives of doing so is to attain more benefits through

proper utilisation of resources of an organisation. It reveals profit or loss for providing specific

value of nature of firms assets, liabilities and companies owners. This consists of at least two

recording entries for all essential transaction that are done in a financial period of time.

This particular report is providing crucial information about accounting and reporting

methods those are useful for evaluating financial transactions in proper manner. Calculation of

net profit through using various costing method. Merits and demerits of various planning tools

helpful for budgets control. However, analysis of financial issues those are being arises in an

organisations are done by making comparison among other companies. Further, some financial

tools are used to deal with all issues that are present at internal level (Wickramasinghe and

Alawattage, 2012).

TASK 1

P1: Discussion about management accounting and their essential requirements

Nowadays, it has been determine the management of every companies are always

looking to have a well effective accounting systems that are assist them to record their every day

financial transactions that occur during the period of time. The main aim of finance managers is

to attain organisation aims and objectives that are always be helpful to make future planning to

increase growth and profitability for longer period. There are various sources from which data

can be collected that are always helpful for companies like Rowlinson Knitwear (Lavia López

and Hiebl, 2014).

Management accounting is said to be continuous improvement process which is aid to

planning, formulating, measuring and operating both financial and non-financial data of an

organisation. It used to motivate behaviour and support or create cultural values which is

necessary to attain an organisations strategies and operational objectives within financial

departments. The main trust of this term is towards crucial policy and developing plan to attain

desired objectives of management. It assist administration in planning and analysing the

1

Accounting is a systematic process of identify, recording, summarising and interpreting

financial data in effective manner. While management is held responsible for provide all

necessary requirements or support to financial accountants in respect to make better report during

an accounting period of time. The major objectives of doing so is to attain more benefits through

proper utilisation of resources of an organisation. It reveals profit or loss for providing specific

value of nature of firms assets, liabilities and companies owners. This consists of at least two

recording entries for all essential transaction that are done in a financial period of time.

This particular report is providing crucial information about accounting and reporting

methods those are useful for evaluating financial transactions in proper manner. Calculation of

net profit through using various costing method. Merits and demerits of various planning tools

helpful for budgets control. However, analysis of financial issues those are being arises in an

organisations are done by making comparison among other companies. Further, some financial

tools are used to deal with all issues that are present at internal level (Wickramasinghe and

Alawattage, 2012).

TASK 1

P1: Discussion about management accounting and their essential requirements

Nowadays, it has been determine the management of every companies are always

looking to have a well effective accounting systems that are assist them to record their every day

financial transactions that occur during the period of time. The main aim of finance managers is

to attain organisation aims and objectives that are always be helpful to make future planning to

increase growth and profitability for longer period. There are various sources from which data

can be collected that are always helpful for companies like Rowlinson Knitwear (Lavia López

and Hiebl, 2014).

Management accounting is said to be continuous improvement process which is aid to

planning, formulating, measuring and operating both financial and non-financial data of an

organisation. It used to motivate behaviour and support or create cultural values which is

necessary to attain an organisations strategies and operational objectives within financial

departments. The main trust of this term is towards crucial policy and developing plan to attain

desired objectives of management. It assist administration in planning and analysing the

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

performance of an organisation in respect to follow right directions of regular improvements. It

would utilises the principles and practices of financial accounting in addition to other modern

management tools for effective operations of an organisation's.

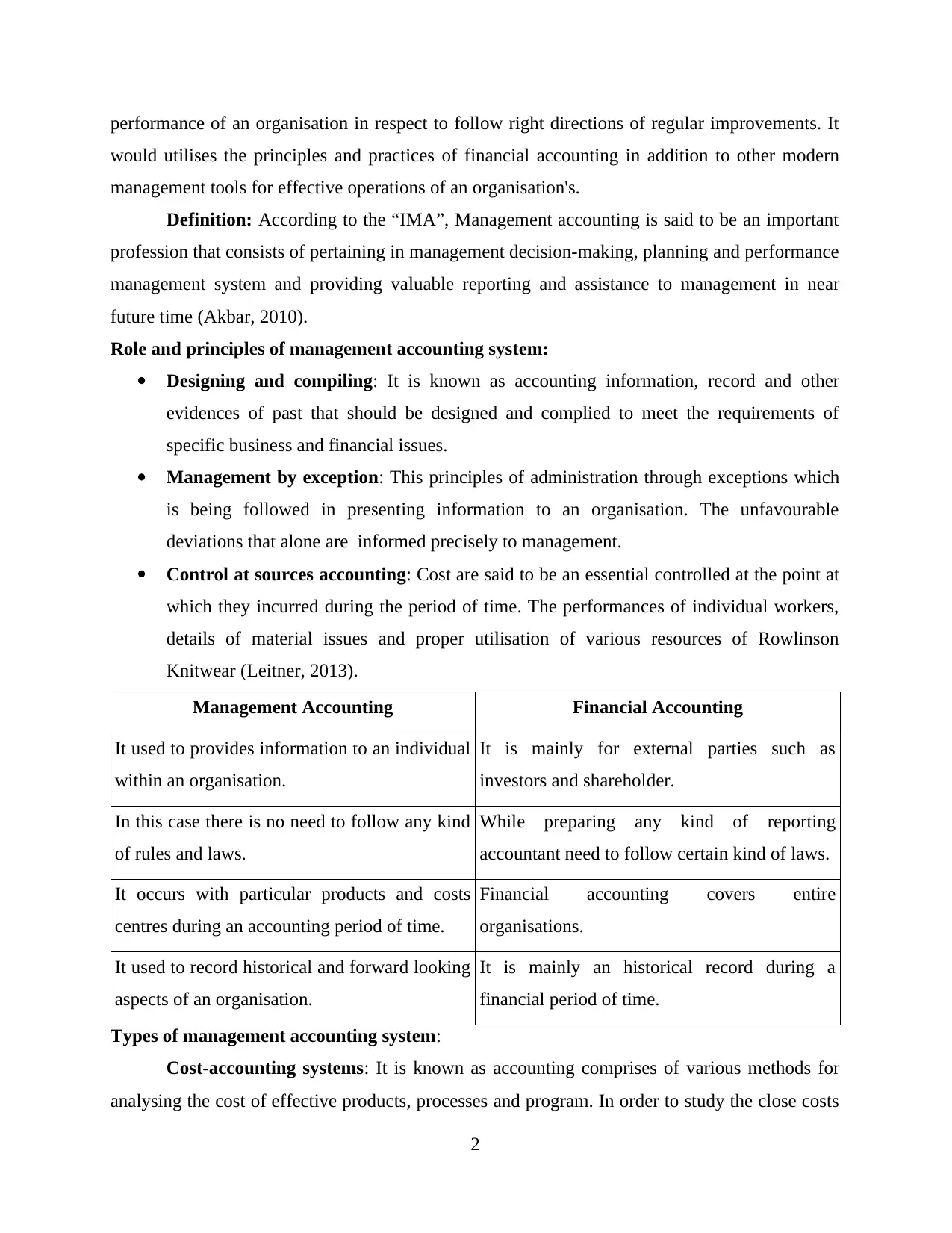

Definition: According to the “IMA”, Management accounting is said to be an important

profession that consists of pertaining in management decision-making, planning and performance

management system and providing valuable reporting and assistance to management in near

future time (Akbar, 2010).

Role and principles of management accounting system:

Designing and compiling: It is known as accounting information, record and other

evidences of past that should be designed and complied to meet the requirements of

specific business and financial issues.

Management by exception: This principles of administration through exceptions which

is being followed in presenting information to an organisation. The unfavourable

deviations that alone are informed precisely to management.

Control at sources accounting: Cost are said to be an essential controlled at the point at

which they incurred during the period of time. The performances of individual workers,

details of material issues and proper utilisation of various resources of Rowlinson

Knitwear (Leitner, 2013).

Management Accounting Financial Accounting

It used to provides information to an individual

within an organisation.

It is mainly for external parties such as

investors and shareholder.

In this case there is no need to follow any kind

of rules and laws.

While preparing any kind of reporting

accountant need to follow certain kind of laws.

It occurs with particular products and costs

centres during an accounting period of time.

Financial accounting covers entire

organisations.

It used to record historical and forward looking

aspects of an organisation.

It is mainly an historical record during a

financial period of time.

Types of management accounting system:

Cost-accounting systems: It is known as accounting comprises of various methods for

analysing the cost of effective products, processes and program. In order to study the close costs

2

would utilises the principles and practices of financial accounting in addition to other modern

management tools for effective operations of an organisation's.

Definition: According to the “IMA”, Management accounting is said to be an important

profession that consists of pertaining in management decision-making, planning and performance

management system and providing valuable reporting and assistance to management in near

future time (Akbar, 2010).

Role and principles of management accounting system:

Designing and compiling: It is known as accounting information, record and other

evidences of past that should be designed and complied to meet the requirements of

specific business and financial issues.

Management by exception: This principles of administration through exceptions which

is being followed in presenting information to an organisation. The unfavourable

deviations that alone are informed precisely to management.

Control at sources accounting: Cost are said to be an essential controlled at the point at

which they incurred during the period of time. The performances of individual workers,

details of material issues and proper utilisation of various resources of Rowlinson

Knitwear (Leitner, 2013).

Management Accounting Financial Accounting

It used to provides information to an individual

within an organisation.

It is mainly for external parties such as

investors and shareholder.

In this case there is no need to follow any kind

of rules and laws.

While preparing any kind of reporting

accountant need to follow certain kind of laws.

It occurs with particular products and costs

centres during an accounting period of time.

Financial accounting covers entire

organisations.

It used to record historical and forward looking

aspects of an organisation.

It is mainly an historical record during a

financial period of time.

Types of management accounting system:

Cost-accounting systems: It is known as accounting comprises of various methods for

analysing the cost of effective products, processes and program. In order to study the close costs

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

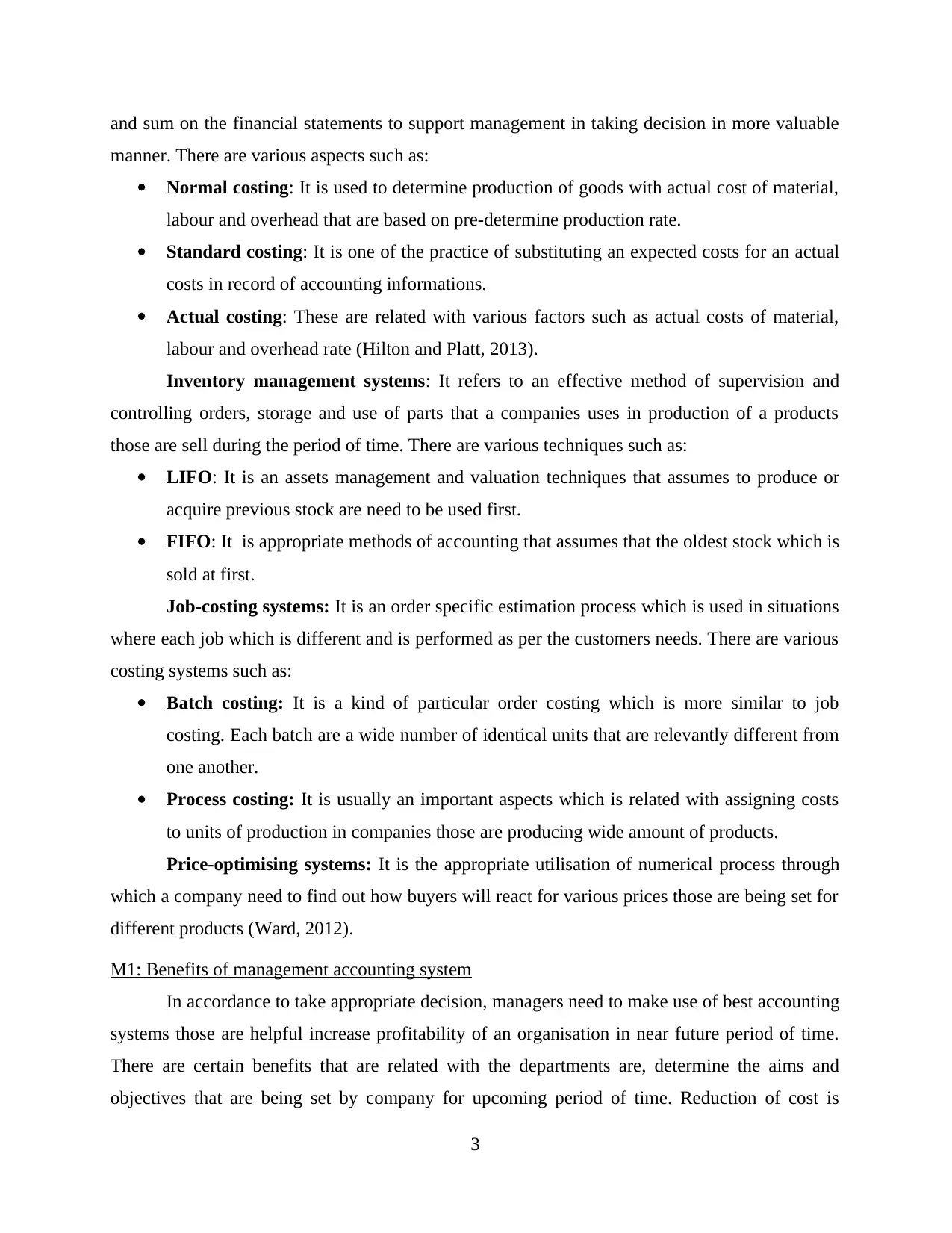

and sum on the financial statements to support management in taking decision in more valuable

manner. There are various aspects such as:

Normal costing: It is used to determine production of goods with actual cost of material,

labour and overhead that are based on pre-determine production rate.

Standard costing: It is one of the practice of substituting an expected costs for an actual

costs in record of accounting informations.

Actual costing: These are related with various factors such as actual costs of material,

labour and overhead rate (Hilton and Platt, 2013).

Inventory management systems: It refers to an effective method of supervision and

controlling orders, storage and use of parts that a companies uses in production of a products

those are sell during the period of time. There are various techniques such as:

LIFO: It is an assets management and valuation techniques that assumes to produce or

acquire previous stock are need to be used first.

FIFO: It is appropriate methods of accounting that assumes that the oldest stock which is

sold at first.

Job-costing systems: It is an order specific estimation process which is used in situations

where each job which is different and is performed as per the customers needs. There are various

costing systems such as:

Batch costing: It is a kind of particular order costing which is more similar to job

costing. Each batch are a wide number of identical units that are relevantly different from

one another.

Process costing: It is usually an important aspects which is related with assigning costs

to units of production in companies those are producing wide amount of products.

Price-optimising systems: It is the appropriate utilisation of numerical process through

which a company need to find out how buyers will react for various prices those are being set for

different products (Ward, 2012).

M1: Benefits of management accounting system

In accordance to take appropriate decision, managers need to make use of best accounting

systems those are helpful increase profitability of an organisation in near future period of time.

There are certain benefits that are related with the departments are, determine the aims and

objectives that are being set by company for upcoming period of time. Reduction of cost is

3

manner. There are various aspects such as:

Normal costing: It is used to determine production of goods with actual cost of material,

labour and overhead that are based on pre-determine production rate.

Standard costing: It is one of the practice of substituting an expected costs for an actual

costs in record of accounting informations.

Actual costing: These are related with various factors such as actual costs of material,

labour and overhead rate (Hilton and Platt, 2013).

Inventory management systems: It refers to an effective method of supervision and

controlling orders, storage and use of parts that a companies uses in production of a products

those are sell during the period of time. There are various techniques such as:

LIFO: It is an assets management and valuation techniques that assumes to produce or

acquire previous stock are need to be used first.

FIFO: It is appropriate methods of accounting that assumes that the oldest stock which is

sold at first.

Job-costing systems: It is an order specific estimation process which is used in situations

where each job which is different and is performed as per the customers needs. There are various

costing systems such as:

Batch costing: It is a kind of particular order costing which is more similar to job

costing. Each batch are a wide number of identical units that are relevantly different from

one another.

Process costing: It is usually an important aspects which is related with assigning costs

to units of production in companies those are producing wide amount of products.

Price-optimising systems: It is the appropriate utilisation of numerical process through

which a company need to find out how buyers will react for various prices those are being set for

different products (Ward, 2012).

M1: Benefits of management accounting system

In accordance to take appropriate decision, managers need to make use of best accounting

systems those are helpful increase profitability of an organisation in near future period of time.

There are certain benefits that are related with the departments are, determine the aims and

objectives that are being set by company for upcoming period of time. Reduction of cost is

3

primary motive of every finance manager. Increasing efficiency for an organisation. All the

accounting systems are more valuable and have certain amount of benefits. Cost accounting is

effectively useful to increase profitability for the company.

P2: Different types of management reporting

In respect to increase future aims and objective a company need to make use of reporting

systems in more reliable and effective manner. It is primary decision of every business

organisation which is to make use of best suitable reporting methods that used to provide more

reliable and accurate outcomes for the company during allotted time period. This assist managers

to take responsibility of managers to look for effective system for upcoming development and to

control additional costs of Rowlinson Knitwear. They used to record all transactions related with

financial information those are being helpful in taking crucial decision for increase goodwill and

profitability for an organisation. Apart for this, all report are presented in front of all investors

and outside investors and stakeholder those are held responsible to make analysis of present

financial position of the company (Soin and Collier, 2013). On the basis of this, a valuable

decision will be made so that they can get more healthy and effective outcomes in near future

time. The data will be recorded through collecting information from various departments. The

main motive of data collection should be taken from internal departments. Some effective data

can be gather from financial and non-financial sources. There are certain accounting system

which are properly helpful for the company some of them are discussed underneath:

Schedule report: It is an essential activities that lets an organisation information from

one or more that data that are arises in an organisation. It sets up a report to run effectively their

business during the course of action.

Demand report: It is known as of the effective report that is not pre-planned but develop

as per the requirements of interested parties.

Types of accounting reporting method:

Performance report: It happens to be utmost essential aspects for every managers to

evaluate companies ability for the purpose of making valuable comparison between actual and

standard outcomes. During this process, managers required to make use of previous data and

make analysis to attain their future aims and objectives during the period of time. All the issues

are needed to be resolve by making proper decision regarding upliftment of employees moral

within an organisation.

4

accounting systems are more valuable and have certain amount of benefits. Cost accounting is

effectively useful to increase profitability for the company.

P2: Different types of management reporting

In respect to increase future aims and objective a company need to make use of reporting

systems in more reliable and effective manner. It is primary decision of every business

organisation which is to make use of best suitable reporting methods that used to provide more

reliable and accurate outcomes for the company during allotted time period. This assist managers

to take responsibility of managers to look for effective system for upcoming development and to

control additional costs of Rowlinson Knitwear. They used to record all transactions related with

financial information those are being helpful in taking crucial decision for increase goodwill and

profitability for an organisation. Apart for this, all report are presented in front of all investors

and outside investors and stakeholder those are held responsible to make analysis of present

financial position of the company (Soin and Collier, 2013). On the basis of this, a valuable

decision will be made so that they can get more healthy and effective outcomes in near future

time. The data will be recorded through collecting information from various departments. The

main motive of data collection should be taken from internal departments. Some effective data

can be gather from financial and non-financial sources. There are certain accounting system

which are properly helpful for the company some of them are discussed underneath:

Schedule report: It is an essential activities that lets an organisation information from

one or more that data that are arises in an organisation. It sets up a report to run effectively their

business during the course of action.

Demand report: It is known as of the effective report that is not pre-planned but develop

as per the requirements of interested parties.

Types of accounting reporting method:

Performance report: It happens to be utmost essential aspects for every managers to

evaluate companies ability for the purpose of making valuable comparison between actual and

standard outcomes. During this process, managers required to make use of previous data and

make analysis to attain their future aims and objectives during the period of time. All the issues

are needed to be resolve by making proper decision regarding upliftment of employees moral

within an organisation.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management report: Such kind of accounting reporting method included all

crucial information regarding analysing stock position that are being kept by the company during

an accounting period of time. Vital reviews are collected from accounts managers regarding

opening and closing of inventories that are used within a financial period of time. There are

various effective methods those are valuable for increase profitability and efficiency in more

proper ways. Total position and capacity of stock that are keep with an organisation are needs to

record positively within an accounting period of time. As it has been determine that stock level of

the company used to be maintained in the right manner (Modell, 2014).

Account receivable report: As per this reporting techniques which is used to identify

total list of unpaid customer invoices and credit memo within an accounting period. By this

Rowlinson company used to examine total time to get recovery of amounts from debtors.

Through using reporting methods that easily be able to determine additional time of recovery

amount that are overdue.

Job cost report: It is known as all report that can assist for evaluating vital record of

products produce must be revenant to one another. This would be determine that overall cost can

be going to incur for developing one addition product out of a group manufactured during the

period of time.

Operational budget report: According to this, every data related with their total costs

and expenditure that are going to be invested for production of products so that it will be

recorded in more effective manner. It is necessary to make use of data through preparing various

kind of budgets such as sales, production and raw material budgets that are being consumed

during an accounting period of time (Hopper and Bui, 2016).

D1: Critical evaluation of accounting system reporting

According to the above discussed various types of accounting reports, it has been

examine that all crucial aspects for incurring maximum outcomes for Rowlinson Knitwear. If

management to make use of them that held responsible for generating more accurate and reliable

manner they within a less period of time. The main motive is to attain all aims and objectives that

are being set by the company. In accordance with this, performance report will be evaluated in

more effective ways so that exact detail information regarding financial position can easily be

analyse in properly. It has been determine the managers can have two options from which they

can easily be able to reach at certain solution within sort span of time.

5

crucial information regarding analysing stock position that are being kept by the company during

an accounting period of time. Vital reviews are collected from accounts managers regarding

opening and closing of inventories that are used within a financial period of time. There are

various effective methods those are valuable for increase profitability and efficiency in more

proper ways. Total position and capacity of stock that are keep with an organisation are needs to

record positively within an accounting period of time. As it has been determine that stock level of

the company used to be maintained in the right manner (Modell, 2014).

Account receivable report: As per this reporting techniques which is used to identify

total list of unpaid customer invoices and credit memo within an accounting period. By this

Rowlinson company used to examine total time to get recovery of amounts from debtors.

Through using reporting methods that easily be able to determine additional time of recovery

amount that are overdue.

Job cost report: It is known as all report that can assist for evaluating vital record of

products produce must be revenant to one another. This would be determine that overall cost can

be going to incur for developing one addition product out of a group manufactured during the

period of time.

Operational budget report: According to this, every data related with their total costs

and expenditure that are going to be invested for production of products so that it will be

recorded in more effective manner. It is necessary to make use of data through preparing various

kind of budgets such as sales, production and raw material budgets that are being consumed

during an accounting period of time (Hopper and Bui, 2016).

D1: Critical evaluation of accounting system reporting

According to the above discussed various types of accounting reports, it has been

examine that all crucial aspects for incurring maximum outcomes for Rowlinson Knitwear. If

management to make use of them that held responsible for generating more accurate and reliable

manner they within a less period of time. The main motive is to attain all aims and objectives that

are being set by the company. In accordance with this, performance report will be evaluated in

more effective ways so that exact detail information regarding financial position can easily be

analyse in properly. It has been determine the managers can have two options from which they

can easily be able to reach at certain solution within sort span of time.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 2

P3: Various types of costing techniques that are use for calculating net income

In accordance with all business accounting related aspects that are important for the

process of producing effective products and services for the company. It is an essential aspects

for an organisation to make use of tools in right manner. This is essential for managers to make

use of microeconomic factors in regular course of action to generate more reliable results in

coming time. This use to make effective aspects which will assistance, whether resources of an

organisation are utilised within internal department. This would aids operational department to

make desirable and appropriate goodwill in near future. In accordance with getting more

effective outcomes through using a definite set in respect to their continuous cost of productions.

Cost is one of the important amount of value which is being charged in respect to get

more crucial outcomes for the company (Senftlechner and Hiebl, 2015). These are directly or

indirectly associated with production of products and services. This will help to enhance

productivity as well as growth for the company by proper utilisation of resources. It has been

determine that without having proper support of finance to management that cannot be able to

take valuable decision in respect to their future coming projects. This will used to make huge

impacts in order to get desire long and short term aims and objectives. There are various costing

techniques which will be effectively utilise by Rowlinson knitwear to determine total net earning

for the company. Some crucial aspects are mentioned underneath:

Cost volume profit (CVP): It is necessary method which is being used to determine

different changes in accordance with the total cost and volume those are affect performances of

companies. It provide vital information about operating earnings as well as net flexible aspects

within an organisation.

Flexible budgeting: It refers as one of the fixed budget that will be adjusted or flexes for

making modification in volume of activities. The flexible budget is more effective and useful

than other budget which remain at one similar cost.

Cost variances: It is said to be cost variances which is related with essential differences

among actual costs and their budgeted amount. This will be more common for making better

understanding of all those variations those are incurred during manufacturing process.

Absorption costing: It is known as one of the most significant costing method that

directly associated with production of products and services. These includes both variable and

6

P3: Various types of costing techniques that are use for calculating net income

In accordance with all business accounting related aspects that are important for the

process of producing effective products and services for the company. It is an essential aspects

for an organisation to make use of tools in right manner. This is essential for managers to make

use of microeconomic factors in regular course of action to generate more reliable results in

coming time. This use to make effective aspects which will assistance, whether resources of an

organisation are utilised within internal department. This would aids operational department to

make desirable and appropriate goodwill in near future. In accordance with getting more

effective outcomes through using a definite set in respect to their continuous cost of productions.

Cost is one of the important amount of value which is being charged in respect to get

more crucial outcomes for the company (Senftlechner and Hiebl, 2015). These are directly or

indirectly associated with production of products and services. This will help to enhance

productivity as well as growth for the company by proper utilisation of resources. It has been

determine that without having proper support of finance to management that cannot be able to

take valuable decision in respect to their future coming projects. This will used to make huge

impacts in order to get desire long and short term aims and objectives. There are various costing

techniques which will be effectively utilise by Rowlinson knitwear to determine total net earning

for the company. Some crucial aspects are mentioned underneath:

Cost volume profit (CVP): It is necessary method which is being used to determine

different changes in accordance with the total cost and volume those are affect performances of

companies. It provide vital information about operating earnings as well as net flexible aspects

within an organisation.

Flexible budgeting: It refers as one of the fixed budget that will be adjusted or flexes for

making modification in volume of activities. The flexible budget is more effective and useful

than other budget which remain at one similar cost.

Cost variances: It is said to be cost variances which is related with essential differences

among actual costs and their budgeted amount. This will be more common for making better

understanding of all those variations those are incurred during manufacturing process.

Absorption costing: It is known as one of the most significant costing method that

directly associated with production of products and services. These includes both variable and

6

fixed cost during the same point of time. Because of this aspects, it is known as full costing

method. It is not so effective to make future decision-making (Absorption costing, 2018).

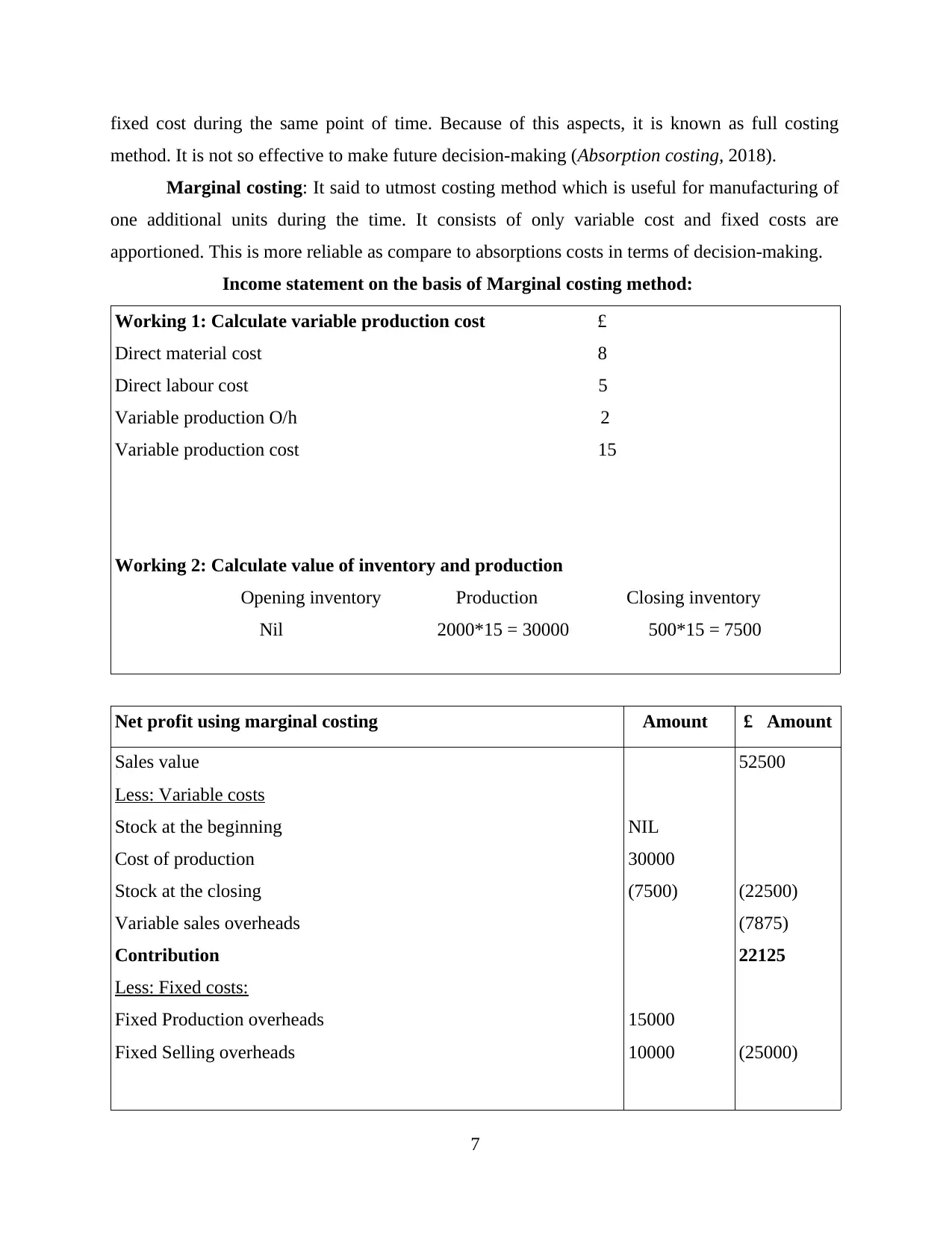

Marginal costing: It said to utmost costing method which is useful for manufacturing of

one additional units during the time. It consists of only variable cost and fixed costs are

apportioned. This is more reliable as compare to absorptions costs in terms of decision-making.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

7

method. It is not so effective to make future decision-making (Absorption costing, 2018).

Marginal costing: It said to utmost costing method which is useful for manufacturing of

one additional units during the time. It consists of only variable cost and fixed costs are

apportioned. This is more reliable as compare to absorptions costs in terms of decision-making.

Income statement on the basis of Marginal costing method:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

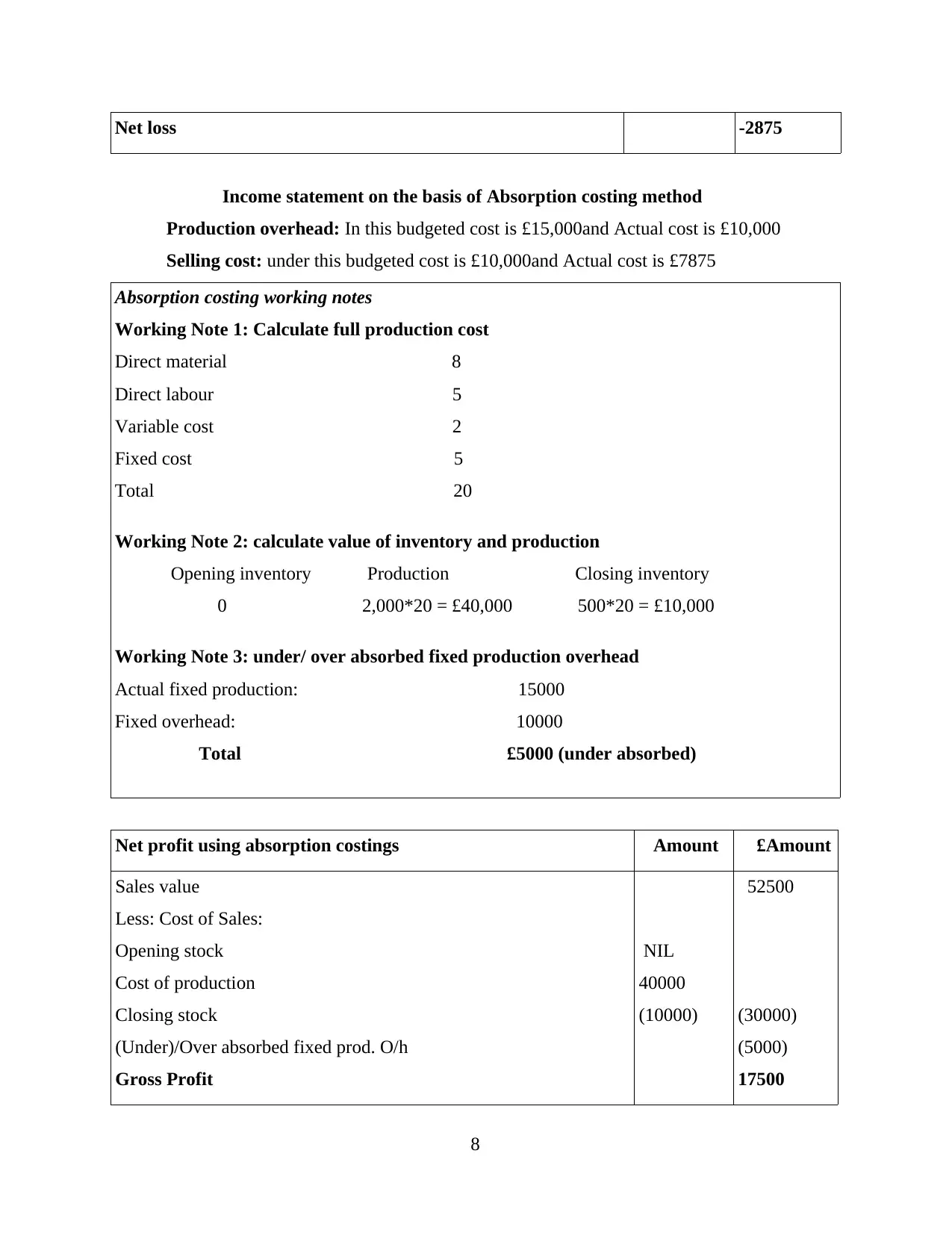

Net loss -2875

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

NIL

40000

(10000)

52500

(30000)

(5000)

17500

8

Income statement on the basis of Absorption costing method

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

NIL

40000

(10000)

52500

(30000)

(5000)

17500

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

7875

10000 17875

Net loss -375

Product costing: There are various costs those are directly associated with the production

of goods and services. Some of them are discussed underneath:

Fixed: These are said to be that costs which remain unchanged with the production any

additional units of products by an organisation. Such as office rent, insurances.

Variable costs: It is known as that costs that varies with the production of products and

services during an accounting period of time.

Cost allocation: A cost object is any vital activity or product for which they wants to

make separately measure cost of production. Such as sales region and a departments.

ABC costing: It is an accounting techniques that determine the activity which a company

perform and then assign indirect costs of products. In this products can be market as per

their quality and features (Nielsen, Mitchell and Nørreklit, 2015).

M2: Various types of management accounting techniques

In respect to get more reliable outcomes a company need to make use of accounting tools

and techniques. By using appropriate techniques chances of getting more reliable and accurate

outcomes can be enhanced. Planning and budgeting is effective tools that can make company to

plan their future resources in effective ways. While through performance measurement they

would be attain their desire aims and objectives that are being set during the course of actions.

D2: Critical analyse of data collected from income statements

According to the above information collected from profit and loss statements that are

being analyse by using different types of costing methods. These data collected are taken to

determine actual net profit generated during an accounting period of time.

Reconciliation statements Amount

9

Variable sales expenditure

Fixed selling expenditure

7875

10000 17875

Net loss -375

Product costing: There are various costs those are directly associated with the production

of goods and services. Some of them are discussed underneath:

Fixed: These are said to be that costs which remain unchanged with the production any

additional units of products by an organisation. Such as office rent, insurances.

Variable costs: It is known as that costs that varies with the production of products and

services during an accounting period of time.

Cost allocation: A cost object is any vital activity or product for which they wants to

make separately measure cost of production. Such as sales region and a departments.

ABC costing: It is an accounting techniques that determine the activity which a company

perform and then assign indirect costs of products. In this products can be market as per

their quality and features (Nielsen, Mitchell and Nørreklit, 2015).

M2: Various types of management accounting techniques

In respect to get more reliable outcomes a company need to make use of accounting tools

and techniques. By using appropriate techniques chances of getting more reliable and accurate

outcomes can be enhanced. Planning and budgeting is effective tools that can make company to

plan their future resources in effective ways. While through performance measurement they

would be attain their desire aims and objectives that are being set during the course of actions.

D2: Critical analyse of data collected from income statements

According to the above information collected from profit and loss statements that are

being analyse by using different types of costing methods. These data collected are taken to

determine actual net profit generated during an accounting period of time.

Reconciliation statements Amount

9

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

From the above table, it has been determine that profit generated from absorption

collected during the time is showing negative outcomes with -375. The point of differences are

seen because of fixed cost adjustments.

TASK 3

P4: Merit and demerits of using planning tools use in budgets

Planning is an essential aspects which are needed to be taken into consideration. All the

mentioned tools are effectively responsible for increasing productivity as well as efficiency with

using proper outcomes for the company. Some of the effective budgets are:

Operational budget: It is known as one of the primary budget which depend upon effective

decision-making collected from total revenue collected out of their functional operations of an

organisation.

Advantages: This seems to be more reliable for managers those are responsible for

producing products for the company. Some of them are sales, production and purchase budgets.

Disadvantage: This happens to be more time consuming while making reporting for the

company..

Rolling budget: It refers to continuous update that included into a new budget time framework

as more recent period completion. It consists of incremental extensions of current budget model.

Advantage: This particular assumption would be helpful to formulate maximum value

for forecasting to the company.

Disadvantage: It seems to be more time consuming while preparing budgets from using

general figures.

Fixed budgets: This seems to be utmost important budget that would be changes on flex during

sales or some other activities though which it can increase of decrease at the same period of time.

Advantage: The major limitation of this budgets which is being accounted for life

unpredictable activities.

Disadvantages: It has been use to analyse small business transactions that are done

during the period of time.

10

Closing stock 500*5 2500

Profit under marginal 2125

From the above table, it has been determine that profit generated from absorption

collected during the time is showing negative outcomes with -375. The point of differences are

seen because of fixed cost adjustments.

TASK 3

P4: Merit and demerits of using planning tools use in budgets

Planning is an essential aspects which are needed to be taken into consideration. All the

mentioned tools are effectively responsible for increasing productivity as well as efficiency with

using proper outcomes for the company. Some of the effective budgets are:

Operational budget: It is known as one of the primary budget which depend upon effective

decision-making collected from total revenue collected out of their functional operations of an

organisation.

Advantages: This seems to be more reliable for managers those are responsible for

producing products for the company. Some of them are sales, production and purchase budgets.

Disadvantage: This happens to be more time consuming while making reporting for the

company..

Rolling budget: It refers to continuous update that included into a new budget time framework

as more recent period completion. It consists of incremental extensions of current budget model.

Advantage: This particular assumption would be helpful to formulate maximum value

for forecasting to the company.

Disadvantage: It seems to be more time consuming while preparing budgets from using

general figures.

Fixed budgets: This seems to be utmost important budget that would be changes on flex during

sales or some other activities though which it can increase of decrease at the same period of time.

Advantage: The major limitation of this budgets which is being accounted for life

unpredictable activities.

Disadvantages: It has been use to analyse small business transactions that are done

during the period of time.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.