Management Accounting Report: Systems, Applications, and Analysis

VerifiedAdded on 2020/01/16

|14

|3937

|221

Report

AI Summary

This report provides a comprehensive overview of management accounting, emphasizing its significance in organizational decision-making, planning, and performance management. It explores the importance of management accounting, highlighting its role in measuring performance, assessing risks, allocating resources, and presenting financial statements. The report then delves into different types of management accounting systems, including responsibility accounting, budgetary accounting, and variance analysis accounting, detailing their applications and benefits within an organization. Furthermore, the report analyzes income statements using absorption and marginal costing techniques, comparing their impact on profit calculations. The report includes practical examples and analysis to establish the relevance of different aspects of management accounting and their impact on improving cash flows and financial returns. The report underscores the practical application of management accounting systems, such as responsibility accounting, in decentralization, performance evaluation, and transfer pricing. It also details the applications of budgetary accounting in forecasting, resource control, and performance monitoring, along with the benefits of variance analysis in establishing materiality, evaluating performance, and fostering accountability.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

SECTION-1.....................................................................................................................................3

1 Importance of Management Accounting..................................................................................3

2 Types of Management Accounting Systems.............................................................................4

3 Application and Benefits of Management Accounting Systems in an Organization................5

4 Income Statements....................................................................................................................6

Section-2 .........................................................................................................................................9

Part-A...........................................................................................................................................9

Part-B.........................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION...........................................................................................................................3

SECTION-1.....................................................................................................................................3

1 Importance of Management Accounting..................................................................................3

2 Types of Management Accounting Systems.............................................................................4

3 Application and Benefits of Management Accounting Systems in an Organization................5

4 Income Statements....................................................................................................................6

Section-2 .........................................................................................................................................9

Part-A...........................................................................................................................................9

Part-B.........................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

2

INTRODUCTION

Management accounting is the process of systematic analysis, interpretation and

presentation of accounting information collected with the help of financial and cost accounting

for the purpose of assisting management in many areas such as decision making and framing

long term and short term policies (Ball, Grubnic and Birchall, 2014). Therefore, management

accounting is based on the costing principles. Management accounting reports are for the internal

assessment of an organization. These reports usually consist of details about the cash, sales

revenues as well as organization's accounts payable and receivables (Bebbington, Unerman, and

O'Dwyer, 2014). The present report is going to discuss various useful aspects of management

accounting along with their applications. Along with that different types of costing methods

specifically absorption and marginal costing will be discussed in detail. The present report

effectively addresses the importance of management accounting in the companies. The various

uses and applications of the management accounting has been analyzed. Also necessary

examples have been cited for the purpose of establishing the relevance of the different aspects

used in management accounting. Moreover the explanation of how management accounting can

be used to improve the cash flows and financial returns of the business.

SECTION-1

1. Importance of Management Accounting

Management Accounting makes an efficient partnering with the other financial aspects of

an organisation. It also has a great significance in the decision making, devising planning and

performance management systems and thus providing expertise in the financial reporting and

control to assist the management in the formulation and implementation of an organisation

strategy (Bebbington, Unerman, and O'Dwyer, 2014). Following are some of the reasons

highlighting importance of use of management accounting concept in various organizations .

Measuring Performance- Two types of performances can be measured with the help of

management accounting. Firstly, analysis is made at the individual employee’s level that is the

performance of employees. Secondly, efficiency of performing various tasks is measured with

that of their respective standards maintained by the organization. In this process, actual

performance is compared with the standard performance and the deviations are analysed as well.

3

Management accounting is the process of systematic analysis, interpretation and

presentation of accounting information collected with the help of financial and cost accounting

for the purpose of assisting management in many areas such as decision making and framing

long term and short term policies (Ball, Grubnic and Birchall, 2014). Therefore, management

accounting is based on the costing principles. Management accounting reports are for the internal

assessment of an organization. These reports usually consist of details about the cash, sales

revenues as well as organization's accounts payable and receivables (Bebbington, Unerman, and

O'Dwyer, 2014). The present report is going to discuss various useful aspects of management

accounting along with their applications. Along with that different types of costing methods

specifically absorption and marginal costing will be discussed in detail. The present report

effectively addresses the importance of management accounting in the companies. The various

uses and applications of the management accounting has been analyzed. Also necessary

examples have been cited for the purpose of establishing the relevance of the different aspects

used in management accounting. Moreover the explanation of how management accounting can

be used to improve the cash flows and financial returns of the business.

SECTION-1

1. Importance of Management Accounting

Management Accounting makes an efficient partnering with the other financial aspects of

an organisation. It also has a great significance in the decision making, devising planning and

performance management systems and thus providing expertise in the financial reporting and

control to assist the management in the formulation and implementation of an organisation

strategy (Bebbington, Unerman, and O'Dwyer, 2014). Following are some of the reasons

highlighting importance of use of management accounting concept in various organizations .

Measuring Performance- Two types of performances can be measured with the help of

management accounting. Firstly, analysis is made at the individual employee’s level that is the

performance of employees. Secondly, efficiency of performing various tasks is measured with

that of their respective standards maintained by the organization. In this process, actual

performance is compared with the standard performance and the deviations are analysed as well.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These deviations will be finally reported to the management and hence individual accountability

for different tasks will be established (Sandalgaard and Nikolaj Bukh, 2014). This will help in

the performance assessment of each employee and the respective departments. Also, the policies

regarding incentives can be framed with reference to their performance (Bebbington, Unerman

and O'Dwyer, 2014).

Risk Assessment- This is also one of the major objectives ofmanagement accounting. It is

used for the assessment of risks andfor managing them effectively in order to prevent any

uninterrupted business operations.

Systematic Allocation of Resources-udgeting is an important area in management

accounting which includes the allocation of resources for different business operations. This will

prevent the wastage and production of damaged unitsincompany. Proper resource allocation is

also important for the purpose efficiently managing all the scarce resources available in the

organisation. The management accountant has been appointed to utilise the current resources as

their primary aim is to minimise the costs. The cost reduction is the basic factor which is

followed by devising of strategies to ensure its achievement of several goals and the objectives.

The resources that is financial resources are optimally utilised in the best possible manner to fa

ciliate various users. The budgeting will determine the current requirements of the resources in a

business to meet the needs and the expectations of the existing business.

Presenting Financial Statements to the Management- Management accounting reports are

of great significance for the purpose of preparing financial statements of organisation. The

financial statements incorporate information which is available from the reports presented by

management accountant of company. The good presentation of the financial statements will help

an entity in order to attract wide number of investors to invest in the current business. The

accoutring standards will also guide an entity to follow various frameworks in order to present

the financial statements in a better way.

2. Types of Management Accounting Systems Responsibility Accounting- This system is based on the concept that managers of

respective departments are only accountable to the items to which they exercise control.

For instance: purchase manager will only be held responsible for the purchase of

4

for different tasks will be established (Sandalgaard and Nikolaj Bukh, 2014). This will help in

the performance assessment of each employee and the respective departments. Also, the policies

regarding incentives can be framed with reference to their performance (Bebbington, Unerman

and O'Dwyer, 2014).

Risk Assessment- This is also one of the major objectives ofmanagement accounting. It is

used for the assessment of risks andfor managing them effectively in order to prevent any

uninterrupted business operations.

Systematic Allocation of Resources-udgeting is an important area in management

accounting which includes the allocation of resources for different business operations. This will

prevent the wastage and production of damaged unitsincompany. Proper resource allocation is

also important for the purpose efficiently managing all the scarce resources available in the

organisation. The management accountant has been appointed to utilise the current resources as

their primary aim is to minimise the costs. The cost reduction is the basic factor which is

followed by devising of strategies to ensure its achievement of several goals and the objectives.

The resources that is financial resources are optimally utilised in the best possible manner to fa

ciliate various users. The budgeting will determine the current requirements of the resources in a

business to meet the needs and the expectations of the existing business.

Presenting Financial Statements to the Management- Management accounting reports are

of great significance for the purpose of preparing financial statements of organisation. The

financial statements incorporate information which is available from the reports presented by

management accountant of company. The good presentation of the financial statements will help

an entity in order to attract wide number of investors to invest in the current business. The

accoutring standards will also guide an entity to follow various frameworks in order to present

the financial statements in a better way.

2. Types of Management Accounting Systems Responsibility Accounting- This system is based on the concept that managers of

respective departments are only accountable to the items to which they exercise control.

For instance: purchase manager will only be held responsible for the purchase of

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

inventory and no other unrelated matter (Management accounting techniques, 2016). This

accountability system emphasises on the importance of settingvarious financial goals,

measuring them and then reporting the performance. This accounting systems refers to

the identification ofthree types ofresponsibility standards which are cost investment and

profit centres. This aspect covers the management reporting system and the way it is

useful formanagement and organisation as a whole to makeeffective and efficient

decision-making. The current approach will emphasises on increasing decisdion

makinga bility of a person by making strong decisions in the business. Budgetary Accounting- Budgets are prepared for different departments in an organisation.

The different budgets reports presents the allocation of the resources to a particular

department. This ensures an effective planning that will help in decision-making. The

budgets are framed for respective departments and for the different costs to be incurred.

For instance: cash budgets, sales budgets, etc. are presented for the respective periods.

These budgets show the prediction of figures hat can be used in decision making.

Variance Analysis Accounting- After the preparation of budgets, actual performance will

be measured with that of the budgeted andrespective variance will be analysed. Variance

analysis will further help in controlling the wastage ofresources in respective activities.

Variance analysis report will assist the management in efficiently establishing the

accountability to respective managers .Variances involves differences ofstandard and

actual figure which assists the management in efficient decision-making (Management

accounting techniques. 2016).

3. Application and benefits of the Management Accounting Systems in an Organisation

Responsibility accounting is applied in all the spheres of organisation for primary

objective of establishing the accountability for various operations carried out in an organisation.

However, following are some of the specific areas where concept of responsibility accounting

can be applied:

Decentralisation- In the process of applying responsibility accounting organisation is

divided into smaller subunits. This division makes an organisation all the more manageable and

structured.

5

accountability system emphasises on the importance of settingvarious financial goals,

measuring them and then reporting the performance. This accounting systems refers to

the identification ofthree types ofresponsibility standards which are cost investment and

profit centres. This aspect covers the management reporting system and the way it is

useful formanagement and organisation as a whole to makeeffective and efficient

decision-making. The current approach will emphasises on increasing decisdion

makinga bility of a person by making strong decisions in the business. Budgetary Accounting- Budgets are prepared for different departments in an organisation.

The different budgets reports presents the allocation of the resources to a particular

department. This ensures an effective planning that will help in decision-making. The

budgets are framed for respective departments and for the different costs to be incurred.

For instance: cash budgets, sales budgets, etc. are presented for the respective periods.

These budgets show the prediction of figures hat can be used in decision making.

Variance Analysis Accounting- After the preparation of budgets, actual performance will

be measured with that of the budgeted andrespective variance will be analysed. Variance

analysis will further help in controlling the wastage ofresources in respective activities.

Variance analysis report will assist the management in efficiently establishing the

accountability to respective managers .Variances involves differences ofstandard and

actual figure which assists the management in efficient decision-making (Management

accounting techniques. 2016).

3. Application and benefits of the Management Accounting Systems in an Organisation

Responsibility accounting is applied in all the spheres of organisation for primary

objective of establishing the accountability for various operations carried out in an organisation.

However, following are some of the specific areas where concept of responsibility accounting

can be applied:

Decentralisation- In the process of applying responsibility accounting organisation is

divided into smaller subunits. This division makes an organisation all the more manageable and

structured.

5

Performance Evaluation- The concept of responsibility accounting establishes a fair and

sound system of performance evaluation of every manager and other personnel. Hence, the

performance of each responsibility centre is measured and presented in the periodically presented

performance reports by an organisation (Management accounting techniques, 2016).

Motivation Responsibility accounting specifically emphasises on the performance

evaluation of every individual working in organisation. It makes the job more challenging for

employees and keeps them motivated to continuously enhance their performance. The motivated

employees are valuable assets for company and contribute effectively to increase the value of

business.

Transfer Pricing- Responsibility accounting involves the division of an enterprise into

different autonomous responsibility centres. In such situations, any product of one division can

be transferred to another department of the same organisation by charging a transfer price. This

will lead to the creation of inter competitive environment that will make all divisions of an

organisation more efficient and profitable.

Budgetary accounting is used for the purpose of planning and controlling expenditures of

organisations. Some of the important applications of budgetary accounting are discussed

hereunder-

Forecasting of Income & Expenditures - Budgeting is a critical part of business planning

process. The owners and management require an estimation or prediction of profitability of

business. This prediction can be made by applying budgetary accounting . Presentation of future

incomes and expenditures in the form of structured budgets clarifies picture of future incomes

and expenditures application of various strategies, plans and events.

Exercising Control over the resources- Budgets are prepared with a primary motive of

allocation of resources to different departments in organisation so as to ensure an effective use.

Also, the excess utilisation by any department can be traced very easily and the reasons can be

evaluated (Bebbington, Unerman and O'Dwyer, 2014). Hence, the concept of economies of scale

can be easily established which will lead to the optimised use of resources and increase of

profitability for an organisation as a whole.

Monitoring Performance- Primary purpose of budgeting is to enable the actual

performance ofvarious operations with that of business performance to ensure that whether

6

sound system of performance evaluation of every manager and other personnel. Hence, the

performance of each responsibility centre is measured and presented in the periodically presented

performance reports by an organisation (Management accounting techniques, 2016).

Motivation Responsibility accounting specifically emphasises on the performance

evaluation of every individual working in organisation. It makes the job more challenging for

employees and keeps them motivated to continuously enhance their performance. The motivated

employees are valuable assets for company and contribute effectively to increase the value of

business.

Transfer Pricing- Responsibility accounting involves the division of an enterprise into

different autonomous responsibility centres. In such situations, any product of one division can

be transferred to another department of the same organisation by charging a transfer price. This

will lead to the creation of inter competitive environment that will make all divisions of an

organisation more efficient and profitable.

Budgetary accounting is used for the purpose of planning and controlling expenditures of

organisations. Some of the important applications of budgetary accounting are discussed

hereunder-

Forecasting of Income & Expenditures - Budgeting is a critical part of business planning

process. The owners and management require an estimation or prediction of profitability of

business. This prediction can be made by applying budgetary accounting . Presentation of future

incomes and expenditures in the form of structured budgets clarifies picture of future incomes

and expenditures application of various strategies, plans and events.

Exercising Control over the resources- Budgets are prepared with a primary motive of

allocation of resources to different departments in organisation so as to ensure an effective use.

Also, the excess utilisation by any department can be traced very easily and the reasons can be

evaluated (Bebbington, Unerman and O'Dwyer, 2014). Hence, the concept of economies of scale

can be easily established which will lead to the optimised use of resources and increase of

profitability for an organisation as a whole.

Monitoring Performance- Primary purpose of budgeting is to enable the actual

performance ofvarious operations with that of business performance to ensure that whether

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business activities are conducted as per the expectations or not. The variances are evaluated and

necessary corrective measures are taken (Sandalgaard and Nikolaj Bukh, 2014).

Maintaining Records of the past years- The cost reports of previous years are maintained

and kept for record keeping. These statements are than retained by organisations to compare the

results of company from that of previous years. This will help in comparison of results and thus,

effective assessment of performance can be done (Management accounting techniques, 2016).

Variance analysis helps the management of an organisation in monitoring excess use of

essential resources and take necessary steps to control this excessive use. An effective variance

analysis helps an organisation in spotting the issues, trends and opportunities in the path of long

term and short term success. Some of the benefits derived by organisations fromconcept of

variance analysis are discussed as below-

Establishing Materiality- Materiality is a threshold level of respective statistical variances

that are to be worth noting). For the variances that are identified, the materiality levels are

required to be ascertained.

Effective Evaluation- Variances help in the timely evaluation of the present situation

which will further help in taking the necessary timely rectification actions. Thus, the

performance can be enhanced with the timely analysis of all variances and their reasons.

Accountability- By the evaluation,individual accountability is being established for

various departments operating in an organisation (Management accounting techniques, 2016).

This will further be useful for the purpose of evaluating performance and thereby, framing

policies for them.

4. Income Statements

A) Income Statement using Absorption and Marginal Costing Techniques

Analysis of profit per unit-

Number of Units Manufactured = 60000

Variable cost per unit .65

Fixed cost per unit .20

Profit per unit .15

Total selling Price £ 1

7

necessary corrective measures are taken (Sandalgaard and Nikolaj Bukh, 2014).

Maintaining Records of the past years- The cost reports of previous years are maintained

and kept for record keeping. These statements are than retained by organisations to compare the

results of company from that of previous years. This will help in comparison of results and thus,

effective assessment of performance can be done (Management accounting techniques, 2016).

Variance analysis helps the management of an organisation in monitoring excess use of

essential resources and take necessary steps to control this excessive use. An effective variance

analysis helps an organisation in spotting the issues, trends and opportunities in the path of long

term and short term success. Some of the benefits derived by organisations fromconcept of

variance analysis are discussed as below-

Establishing Materiality- Materiality is a threshold level of respective statistical variances

that are to be worth noting). For the variances that are identified, the materiality levels are

required to be ascertained.

Effective Evaluation- Variances help in the timely evaluation of the present situation

which will further help in taking the necessary timely rectification actions. Thus, the

performance can be enhanced with the timely analysis of all variances and their reasons.

Accountability- By the evaluation,individual accountability is being established for

various departments operating in an organisation (Management accounting techniques, 2016).

This will further be useful for the purpose of evaluating performance and thereby, framing

policies for them.

4. Income Statements

A) Income Statement using Absorption and Marginal Costing Techniques

Analysis of profit per unit-

Number of Units Manufactured = 60000

Variable cost per unit .65

Fixed cost per unit .20

Profit per unit .15

Total selling Price £ 1

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

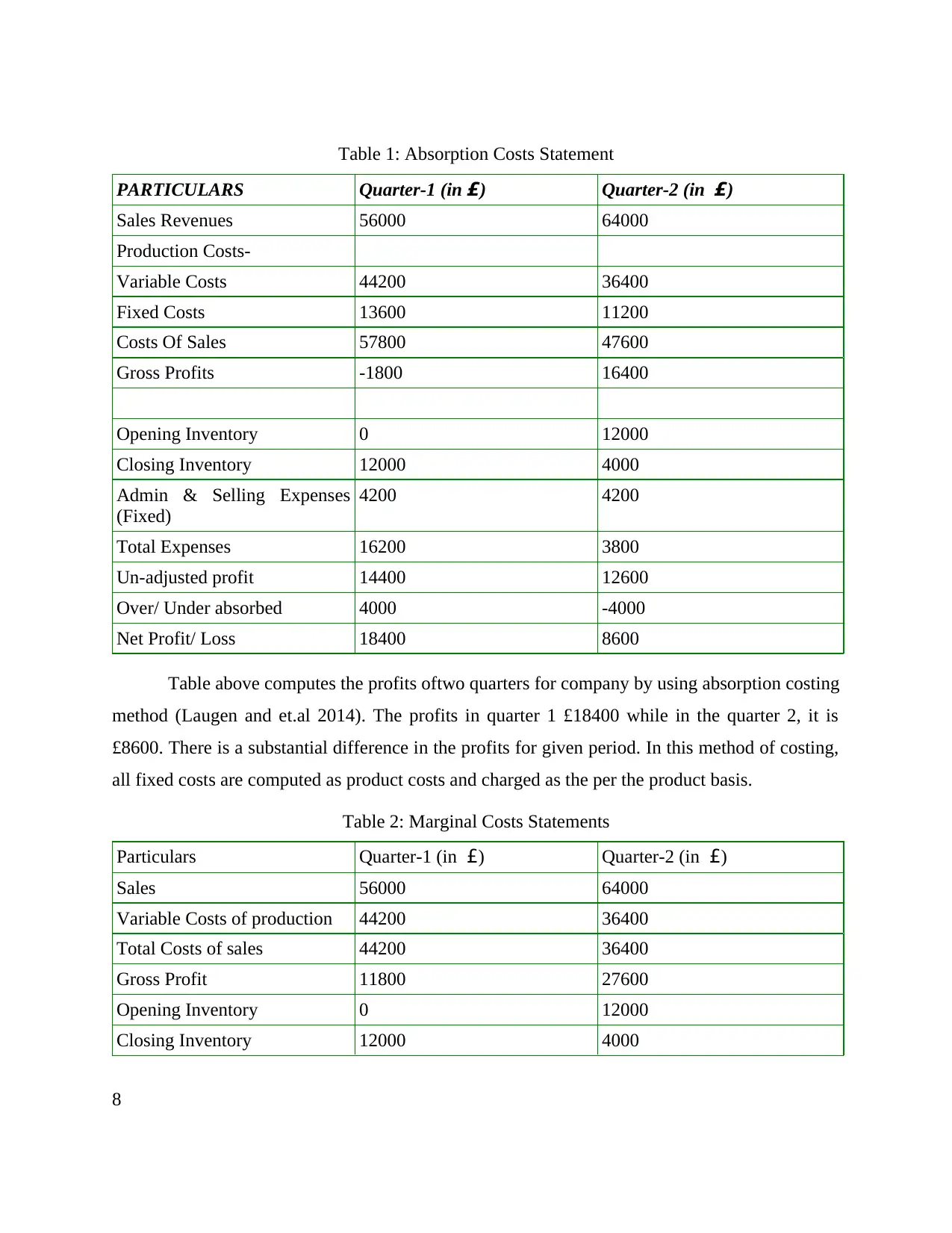

Table 1: Absorption Costs Statement

PARTICULARS Quarter-1 (in £) Quarter-2 (in £)

Sales Revenues 56000 64000

Production Costs-

Variable Costs 44200 36400

Fixed Costs 13600 11200

Costs Of Sales 57800 47600

Gross Profits -1800 16400

Opening Inventory 0 12000

Closing Inventory 12000 4000

Admin & Selling Expenses

(Fixed)

4200 4200

Total Expenses 16200 3800

Un-adjusted profit 14400 12600

Over/ Under absorbed 4000 -4000

Net Profit/ Loss 18400 8600

Table above computes the profits oftwo quarters for company by using absorption costing

method (Laugen and et.al 2014). The profits in quarter 1 £18400 while in the quarter 2, it is

£8600. There is a substantial difference in the profits for given period. In this method of costing,

all fixed costs are computed as product costs and charged as the per the product basis.

Table 2: Marginal Costs Statements

Particulars Quarter-1 (in £) Quarter-2 (in £)

Sales 56000 64000

Variable Costs of production 44200 36400

Total Costs of sales 44200 36400

Gross Profit 11800 27600

Opening Inventory 0 12000

Closing Inventory 12000 4000

8

PARTICULARS Quarter-1 (in £) Quarter-2 (in £)

Sales Revenues 56000 64000

Production Costs-

Variable Costs 44200 36400

Fixed Costs 13600 11200

Costs Of Sales 57800 47600

Gross Profits -1800 16400

Opening Inventory 0 12000

Closing Inventory 12000 4000

Admin & Selling Expenses

(Fixed)

4200 4200

Total Expenses 16200 3800

Un-adjusted profit 14400 12600

Over/ Under absorbed 4000 -4000

Net Profit/ Loss 18400 8600

Table above computes the profits oftwo quarters for company by using absorption costing

method (Laugen and et.al 2014). The profits in quarter 1 £18400 while in the quarter 2, it is

£8600. There is a substantial difference in the profits for given period. In this method of costing,

all fixed costs are computed as product costs and charged as the per the product basis.

Table 2: Marginal Costs Statements

Particulars Quarter-1 (in £) Quarter-2 (in £)

Sales 56000 64000

Variable Costs of production 44200 36400

Total Costs of sales 44200 36400

Gross Profit 11800 27600

Opening Inventory 0 12000

Closing Inventory 12000 4000

8

Fixed Costs 4200 4200

Total Expenses -16200 3800

Profit -4400 31400

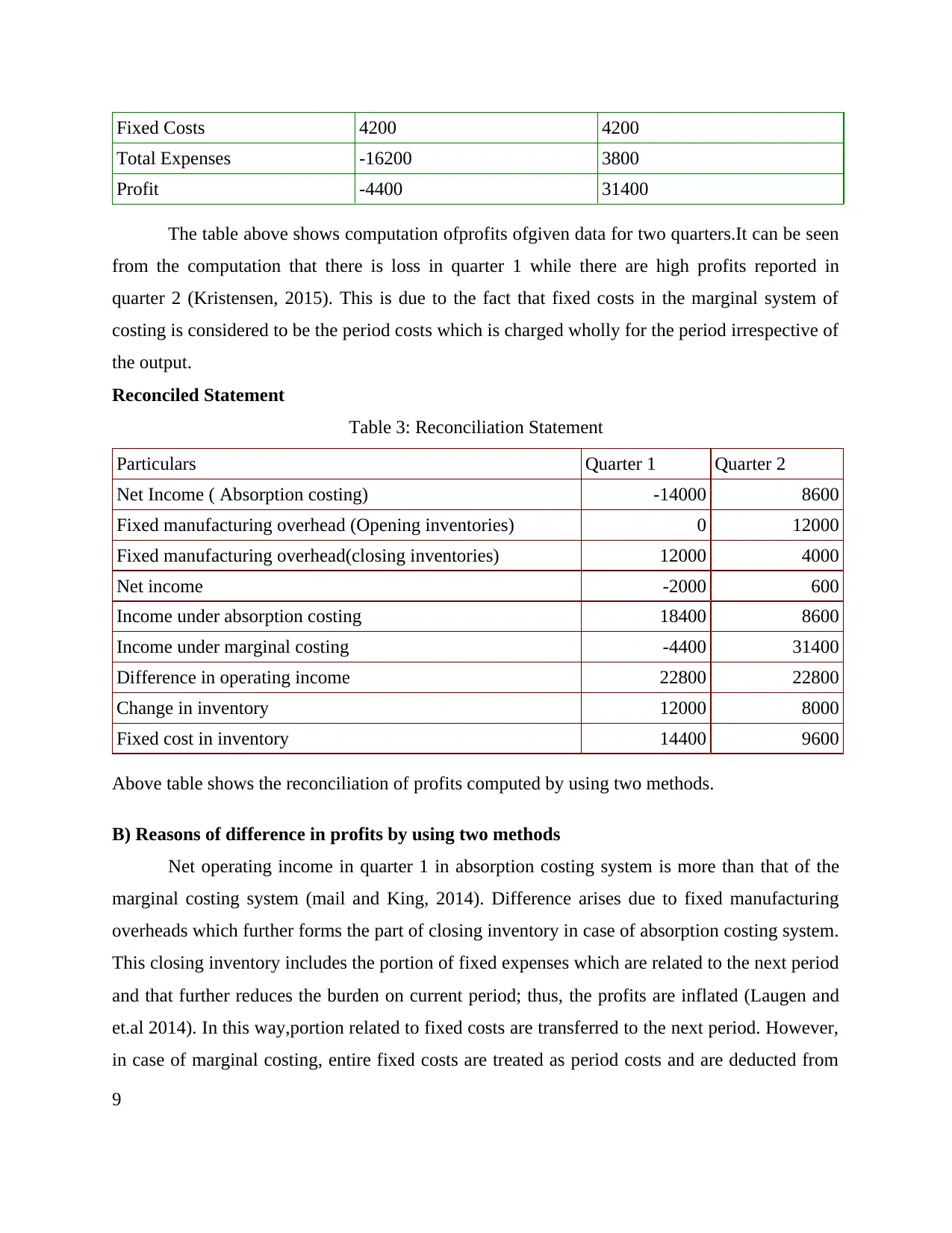

The table above shows computation ofprofits ofgiven data for two quarters.It can be seen

from the computation that there is loss in quarter 1 while there are high profits reported in

quarter 2 (Kristensen, 2015). This is due to the fact that fixed costs in the marginal system of

costing is considered to be the period costs which is charged wholly for the period irrespective of

the output.

Reconciled Statement

Table 3: Reconciliation Statement

Particulars Quarter 1 Quarter 2

Net Income ( Absorption costing) -14000 8600

Fixed manufacturing overhead (Opening inventories) 0 12000

Fixed manufacturing overhead(closing inventories) 12000 4000

Net income -2000 600

Income under absorption costing 18400 8600

Income under marginal costing -4400 31400

Difference in operating income 22800 22800

Change in inventory 12000 8000

Fixed cost in inventory 14400 9600

Above table shows the reconciliation of profits computed by using two methods.

B) Reasons of difference in profits by using two methods

Net operating income in quarter 1 in absorption costing system is more than that of the

marginal costing system (mail and King, 2014). Difference arises due to fixed manufacturing

overheads which further forms the part of closing inventory in case of absorption costing system.

This closing inventory includes the portion of fixed expenses which are related to the next period

and that further reduces the burden on current period; thus, the profits are inflated (Laugen and

et.al 2014). In this way,portion related to fixed costs are transferred to the next period. However,

in case of marginal costing, entire fixed costs are treated as period costs and are deducted from

9

Total Expenses -16200 3800

Profit -4400 31400

The table above shows computation ofprofits ofgiven data for two quarters.It can be seen

from the computation that there is loss in quarter 1 while there are high profits reported in

quarter 2 (Kristensen, 2015). This is due to the fact that fixed costs in the marginal system of

costing is considered to be the period costs which is charged wholly for the period irrespective of

the output.

Reconciled Statement

Table 3: Reconciliation Statement

Particulars Quarter 1 Quarter 2

Net Income ( Absorption costing) -14000 8600

Fixed manufacturing overhead (Opening inventories) 0 12000

Fixed manufacturing overhead(closing inventories) 12000 4000

Net income -2000 600

Income under absorption costing 18400 8600

Income under marginal costing -4400 31400

Difference in operating income 22800 22800

Change in inventory 12000 8000

Fixed cost in inventory 14400 9600

Above table shows the reconciliation of profits computed by using two methods.

B) Reasons of difference in profits by using two methods

Net operating income in quarter 1 in absorption costing system is more than that of the

marginal costing system (mail and King, 2014). Difference arises due to fixed manufacturing

overheads which further forms the part of closing inventory in case of absorption costing system.

This closing inventory includes the portion of fixed expenses which are related to the next period

and that further reduces the burden on current period; thus, the profits are inflated (Laugen and

et.al 2014). In this way,portion related to fixed costs are transferred to the next period. However,

in case of marginal costing, entire fixed costs are treated as period costs and are deducted from

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the income statement and thus, no segregation of fixed costs are made. Therefore, no portion of

fixed overheads are included in the closing inventory. Hence, it reports the losses in quarter 1 but

there are high profits in quarter 2.The differences are adjusted and reconciliation is presented as

shown above (Management accounting techniques, 2016).

SECTION-2

Part-A

Assessing the Planning Tools and their effectiveness in Management Accounting

Management accounting is an effective tool for assisting the management in achieving

better planning and exercising control over company.Various cost accounting tools that can be

used by Nero Ltd are-

Budgeting & Variance Analysis-Company should prepare periodical budgets for the

assessment of performance. Purpose of preparing budgets are for short and long term planning of

company's objectives. After that variance is analysed which is the difference between actual and

budgeted results (Management accounting techniques, 2016). This process is of great

significance for the calculation of the deviations. However, these deviations are either favourable

or adverse. Therefore, rectification steps are taken immediately for the adverse variances. But, it

is difficult to apply in the service industry as the major portion of costs is related to the overhead

expenses. Moreover, proper responsibilities cannot be assigned by using variance analysis as

variances can be due to many reasons such as using unrealistic standards.

Cost Volume Profit Analysis- This analysis assists managers of Nero Ltd in determining

the level of outputs at which all costs become equal to the revenues (Kristensen, 2015). This is

also called as breakeven point that is the situation of no profit and no loss. It also used to analyse

the change in costs and volume which affects the operating income of Nero Ltd. (Khanna and

Gogia, 2014). However, this approach can be applied to the limited information and products.

Therefore, it is computed by the management on single product. This analysis cannot be applied

to all products manufactured within organization (Management accounting techniques, 2016).

Activity Based Costing- This method can be used by Nero Ltd. to effectively allocate its

overheads on those departments which actually use them in their respective activities. Thus, the

cost ofmanufactured products can be assessed accurately. This assessment will further help

10

fixed overheads are included in the closing inventory. Hence, it reports the losses in quarter 1 but

there are high profits in quarter 2.The differences are adjusted and reconciliation is presented as

shown above (Management accounting techniques, 2016).

SECTION-2

Part-A

Assessing the Planning Tools and their effectiveness in Management Accounting

Management accounting is an effective tool for assisting the management in achieving

better planning and exercising control over company.Various cost accounting tools that can be

used by Nero Ltd are-

Budgeting & Variance Analysis-Company should prepare periodical budgets for the

assessment of performance. Purpose of preparing budgets are for short and long term planning of

company's objectives. After that variance is analysed which is the difference between actual and

budgeted results (Management accounting techniques, 2016). This process is of great

significance for the calculation of the deviations. However, these deviations are either favourable

or adverse. Therefore, rectification steps are taken immediately for the adverse variances. But, it

is difficult to apply in the service industry as the major portion of costs is related to the overhead

expenses. Moreover, proper responsibilities cannot be assigned by using variance analysis as

variances can be due to many reasons such as using unrealistic standards.

Cost Volume Profit Analysis- This analysis assists managers of Nero Ltd in determining

the level of outputs at which all costs become equal to the revenues (Kristensen, 2015). This is

also called as breakeven point that is the situation of no profit and no loss. It also used to analyse

the change in costs and volume which affects the operating income of Nero Ltd. (Khanna and

Gogia, 2014). However, this approach can be applied to the limited information and products.

Therefore, it is computed by the management on single product. This analysis cannot be applied

to all products manufactured within organization (Management accounting techniques, 2016).

Activity Based Costing- This method can be used by Nero Ltd. to effectively allocate its

overheads on those departments which actually use them in their respective activities. Thus, the

cost ofmanufactured products can be assessed accurately. This assessment will further help

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

company in setting an appropriate profit margin and competitive selling price.Use of this method

of overhead allocation also helpcompany in identifying true costs which support the pricing

policy of company and reveal unnecessary costs incurred that should be eliminated. However,

the implementation of ABC is expensive and not suitable for small sector companies (Cole,

Upstate and Claiborne, 2015). At times, it is not suitable and easy to identifydrivers associated

with the costs. Also, it is difficult for companies to evaluate costs on the basis of activities.

Part-B

Management accounting system of any organization has a direct impact on its financial

statements. Management and financial accounting concepts are interrelated with each other.

However the information of management accounting is for internal use of the company but it

forms an important base for the preparation of the financial statements. It can be said that the

management accounting provides data to be presented in financial statements. Following are the

areas in financial accounting where management accounting plays a vital role-

Capital Budgeting Decisions- These decisions are involved in making the decisions

regarding investment of capital in order to generate maximum profits for an organization as the

whole. For the purpose of maximizing profits of company, information regarding costs and other

related data of projects are required (Ward and Peppard, 2016). These data is required to be

provided by the management accountant of the company. The more accuracy in this data will

lead to make analysis of more beneficial investing decisions and hence, it will increase the

profitability.

Costs controlling decisions- Costs related to different projects are required to be

evaluated first in order to exercise the controlling function. Correct evaluation of different cost

statements are presented by employing an effective management accounting system and hence,

various measures can be designed by the management of company to control excessive costs

(Bovens, Goodin and Schillemans , 2014). The variance analysis in costing will present an

accurate estimation of difference in standard and actual costs that will present a clear picture in

the minds of financial decision makers to frame the policies of controlling costs.

Cash Flows Analysis & Efficient management of working capital- Management of

working capital is of prime importance for any company. In order to run the business

11

of overhead allocation also helpcompany in identifying true costs which support the pricing

policy of company and reveal unnecessary costs incurred that should be eliminated. However,

the implementation of ABC is expensive and not suitable for small sector companies (Cole,

Upstate and Claiborne, 2015). At times, it is not suitable and easy to identifydrivers associated

with the costs. Also, it is difficult for companies to evaluate costs on the basis of activities.

Part-B

Management accounting system of any organization has a direct impact on its financial

statements. Management and financial accounting concepts are interrelated with each other.

However the information of management accounting is for internal use of the company but it

forms an important base for the preparation of the financial statements. It can be said that the

management accounting provides data to be presented in financial statements. Following are the

areas in financial accounting where management accounting plays a vital role-

Capital Budgeting Decisions- These decisions are involved in making the decisions

regarding investment of capital in order to generate maximum profits for an organization as the

whole. For the purpose of maximizing profits of company, information regarding costs and other

related data of projects are required (Ward and Peppard, 2016). These data is required to be

provided by the management accountant of the company. The more accuracy in this data will

lead to make analysis of more beneficial investing decisions and hence, it will increase the

profitability.

Costs controlling decisions- Costs related to different projects are required to be

evaluated first in order to exercise the controlling function. Correct evaluation of different cost

statements are presented by employing an effective management accounting system and hence,

various measures can be designed by the management of company to control excessive costs

(Bovens, Goodin and Schillemans , 2014). The variance analysis in costing will present an

accurate estimation of difference in standard and actual costs that will present a clear picture in

the minds of financial decision makers to frame the policies of controlling costs.

Cash Flows Analysis & Efficient management of working capital- Management of

working capital is of prime importance for any company. In order to run the business

11

successfully, company needs to effectively manage its liquidity position to pay its outstanding

liabilities. Proper assessment of different components of costs like labor, material and overheads

will ensure the computation of accurate working capital for a particular period. This will further

help in assessment of various options required to finance the requisite working capital to

effectively manage the business activities (Ball, Grubnic and Birchall, 2014).

Hence, it can be said that management accounting is of prime importance and generates

data on which major financial decisions are based and thus, it majorly affects the profitability of

a company.

CONCLUSION

Moreover the use of management accounting in the presenting the financial statements

of the company has been explained in detail along with suitable examples. The importance of

management accounting has been identified and applied in the management accounting. Thus it

can be concluded that the main objective of management accountant in an organisation is to

effectively manage costs, and handle other administrative aspects. Budgets also hold an

important significance in the management accounting.

12

liabilities. Proper assessment of different components of costs like labor, material and overheads

will ensure the computation of accurate working capital for a particular period. This will further

help in assessment of various options required to finance the requisite working capital to

effectively manage the business activities (Ball, Grubnic and Birchall, 2014).

Hence, it can be said that management accounting is of prime importance and generates

data on which major financial decisions are based and thus, it majorly affects the profitability of

a company.

CONCLUSION

Moreover the use of management accounting in the presenting the financial statements

of the company has been explained in detail along with suitable examples. The importance of

management accounting has been identified and applied in the management accounting. Thus it

can be concluded that the main objective of management accountant in an organisation is to

effectively manage costs, and handle other administrative aspects. Budgets also hold an

important significance in the management accounting.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.