Management Accounting Report: Principles and Applications

VerifiedAdded on 2020/10/22

|12

|3096

|460

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and practices. It begins with defining management accounting, its role, and its differences from financial accounting. The report then delves into various management accounting systems, including cash budgets and inventory management systems, highlighting their benefits. It defines and explains the importance of budgeting, covering different types like static, zero-based, rolling, and incremental budgets, along with their advantages and disadvantages. The report also discusses inventory valuation methods, specifically LIFO and FIFO, outlining their definitions, advantages, and disadvantages. Furthermore, it presents break-even analysis and explores the role of management information systems in addressing financial challenges within an organization. The content aims to provide a solid understanding of management accounting concepts and their practical applications in business operations.

MANAGEMENT ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

(a) Define management accounting and its role ........................................................................3

Different types of management accounting systems and their benefits .....................................5

Define budgets............................................................................................................................6

Explain the importance of budget...............................................................................................8

Define what is perceptual inventory system...............................................................................8

Write the definition of LIFO and FIFO with their advantages and disadvantages. ...................9

Explain how an organization uses the management information systems …………………..10

CONCLUSION.........................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................3

(a) Define management accounting and its role ........................................................................3

Different types of management accounting systems and their benefits .....................................5

Define budgets............................................................................................................................6

Explain the importance of budget...............................................................................................8

Define what is perceptual inventory system...............................................................................8

Write the definition of LIFO and FIFO with their advantages and disadvantages. ...................9

Explain how an organization uses the management information systems …………………..10

CONCLUSION.........................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

The objective of this report is to focus on management accounting which are used in

business operation. Present report will consist of meanings, types and roles of management

accounting in an organization. The report will give a deeper insight of the budget and its types

with their benefits and drawbacks. The various inventory valuation is also discussed in this

reports. This assignment will help in identifying the break-even point of an organization which

will help in efficient decision-making. Apart from this, the report will cover the uses of

management information system in responding with financial problems.

(a) Role of Management Accounting

Management accounting can be defined as a process of preparation of reports for

management and the official books which give timely as well as accurate information of statistics

which helps managers to take short–term and long-term decisions (Chiarini and Vagnoni, 2015).

It identifies, analyzes, communicates and interprets the useful information that allows

organizations to go with their goals.

Management accounting is different from financial accounting. Management accounting

mostly provide the information inside the organization to the managers so that they can work

efficiently for making decisions.

Roles and Functions

The roles and functions of the management accounting in a company are as follows:

Helping to forecast future

There are many questions to be answered in an organization like it must invest more in

equipment, and must expand into marketplace etc. for decision making. Therefore, forecasting

aids the decision making.

Helping in making or buying decisions

For the minimization of the cost in an organization, managers need to take decisions

whether they have to buy raw materials or they have to do production inside the firm. Therefore,

management accounting will aid in making decisions at strategic and operational levels.

The objective of this report is to focus on management accounting which are used in

business operation. Present report will consist of meanings, types and roles of management

accounting in an organization. The report will give a deeper insight of the budget and its types

with their benefits and drawbacks. The various inventory valuation is also discussed in this

reports. This assignment will help in identifying the break-even point of an organization which

will help in efficient decision-making. Apart from this, the report will cover the uses of

management information system in responding with financial problems.

(a) Role of Management Accounting

Management accounting can be defined as a process of preparation of reports for

management and the official books which give timely as well as accurate information of statistics

which helps managers to take short–term and long-term decisions (Chiarini and Vagnoni, 2015).

It identifies, analyzes, communicates and interprets the useful information that allows

organizations to go with their goals.

Management accounting is different from financial accounting. Management accounting

mostly provide the information inside the organization to the managers so that they can work

efficiently for making decisions.

Roles and Functions

The roles and functions of the management accounting in a company are as follows:

Helping to forecast future

There are many questions to be answered in an organization like it must invest more in

equipment, and must expand into marketplace etc. for decision making. Therefore, forecasting

aids the decision making.

Helping in making or buying decisions

For the minimization of the cost in an organization, managers need to take decisions

whether they have to buy raw materials or they have to do production inside the firm. Therefore,

management accounting will aid in making decisions at strategic and operational levels.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cash-flows Forecast

To forecast the flow of cash and its impact on any industry is a necessary step. An

organization must be able to bear the costs for the future. From where then revenue will come is

an essential task for the managers to take. Therefore, the management accounting helps the

manager to forecast the future of the cash flows.

Examination of rate of returns

Initially, any project or activity involves a huge financing for an organization where it

will be required to investigate and scan the expected rate of return. This could be decided with

the help of accounting management.

(B) Differentiate between the management accounting and financial accounting.

BASE FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

Objective and

Aim

Its objective is to inform outside

parties. Outside party consists of

customers, debtors, investors etc.

It is meant for managers to take

decisions with the information

collected from an organization by

managers.

Regulatory

requirements

It is a mandatory to have financial

accounting for every public

organization by the government. It is

governed by accounting standards

boards, companies law and

government.

It is a choice for the management.

There is no mandatory requirement

but have some framework and

formats provided by institutes like

CIMA ICWAI etc.

Governing

principles

Financial accounting is governed by the

GAAP i.e. generally accepted

accounting principles (Chiwamit,

Modell and Scapens, 2017.).

Management accounting statements

do not require any standards for the

preparation of accounting. In this

accounting, preparation of statement

is based on the requirements asked

by their group.

Time horizon In financial accounting, timeline is

‘past’. Mostly, it is one financial year.

There is no specified timeline and

they focus mainly on future.

Reporting They are usually arranged for the Reports prepared under management

To forecast the flow of cash and its impact on any industry is a necessary step. An

organization must be able to bear the costs for the future. From where then revenue will come is

an essential task for the managers to take. Therefore, the management accounting helps the

manager to forecast the future of the cash flows.

Examination of rate of returns

Initially, any project or activity involves a huge financing for an organization where it

will be required to investigate and scan the expected rate of return. This could be decided with

the help of accounting management.

(B) Differentiate between the management accounting and financial accounting.

BASE FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

Objective and

Aim

Its objective is to inform outside

parties. Outside party consists of

customers, debtors, investors etc.

It is meant for managers to take

decisions with the information

collected from an organization by

managers.

Regulatory

requirements

It is a mandatory to have financial

accounting for every public

organization by the government. It is

governed by accounting standards

boards, companies law and

government.

It is a choice for the management.

There is no mandatory requirement

but have some framework and

formats provided by institutes like

CIMA ICWAI etc.

Governing

principles

Financial accounting is governed by the

GAAP i.e. generally accepted

accounting principles (Chiwamit,

Modell and Scapens, 2017.).

Management accounting statements

do not require any standards for the

preparation of accounting. In this

accounting, preparation of statement

is based on the requirements asked

by their group.

Time horizon In financial accounting, timeline is

‘past’. Mostly, it is one financial year.

There is no specified timeline and

they focus mainly on future.

Reporting They are usually arranged for the Reports prepared under management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

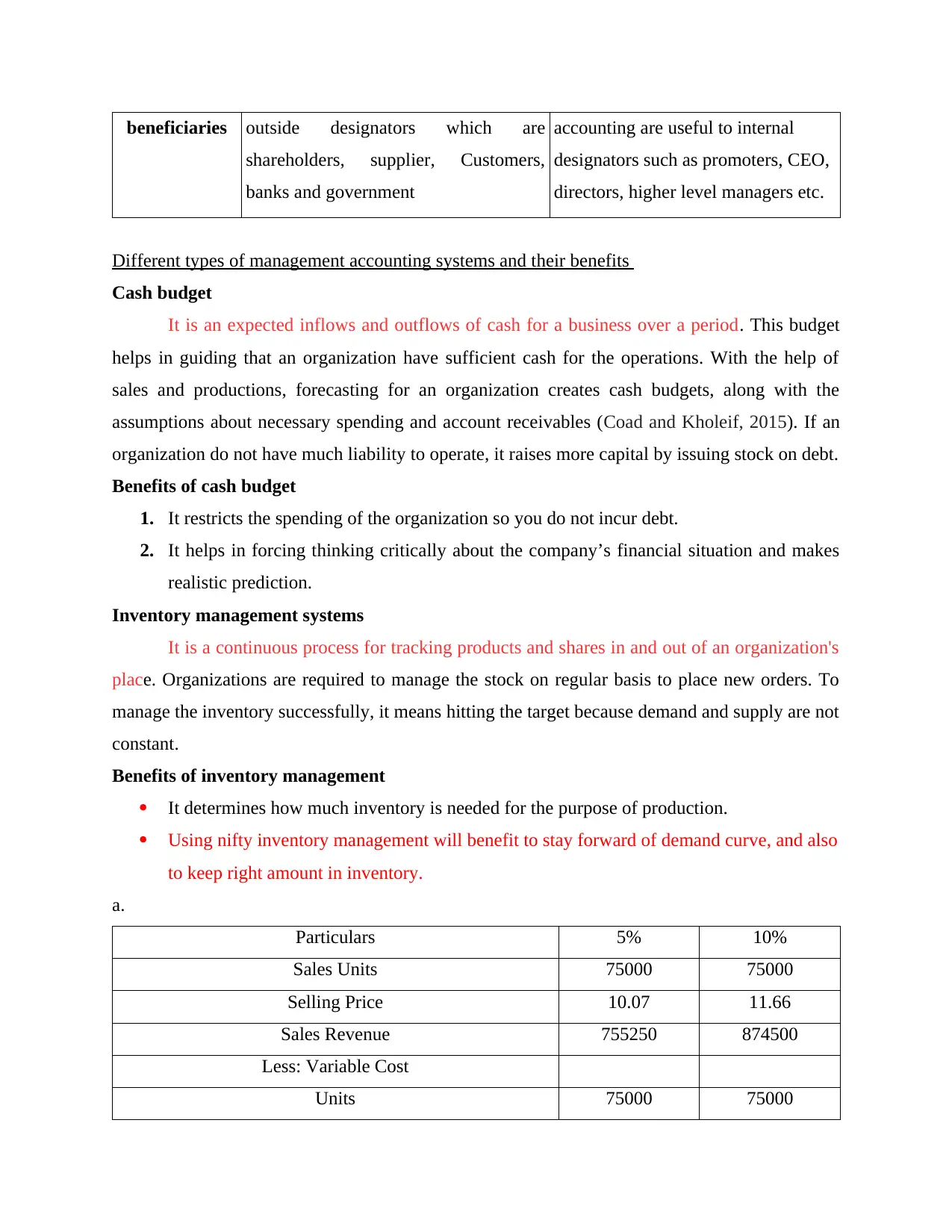

beneficiaries outside designators which are

shareholders, supplier, Customers,

banks and government

accounting are useful to internal

designators such as promoters, CEO,

directors, higher level managers etc.

Different types of management accounting systems and their benefits

Cash budget

It is an expected inflows and outflows of cash for a business over a period. This budget

helps in guiding that an organization have sufficient cash for the operations. With the help of

sales and productions, forecasting for an organization creates cash budgets, along with the

assumptions about necessary spending and account receivables (Coad and Kholeif, 2015). If an

organization do not have much liability to operate, it raises more capital by issuing stock on debt.

Benefits of cash budget

1. It restricts the spending of the organization so you do not incur debt.

2. It helps in forcing thinking critically about the company’s financial situation and makes

realistic prediction.

Inventory management systems

It is a continuous process for tracking products and shares in and out of an organization's

place. Organizations are required to manage the stock on regular basis to place new orders. To

manage the inventory successfully, it means hitting the target because demand and supply are not

constant.

Benefits of inventory management

It determines how much inventory is needed for the purpose of production.

Using nifty inventory management will benefit to stay forward of demand curve, and also

to keep right amount in inventory.

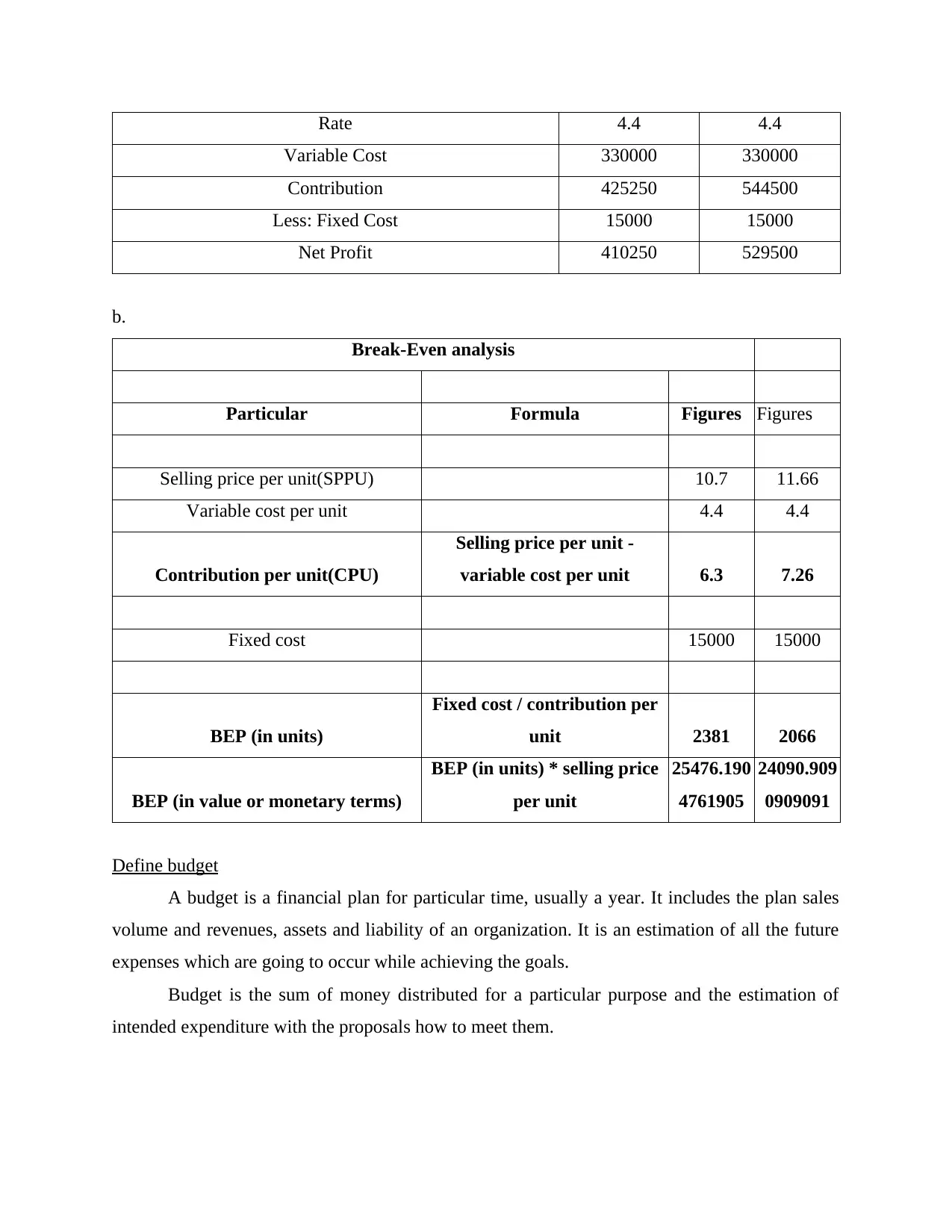

a.

Particulars 5% 10%

Sales Units 75000 75000

Selling Price 10.07 11.66

Sales Revenue 755250 874500

Less: Variable Cost

Units 75000 75000

shareholders, supplier, Customers,

banks and government

accounting are useful to internal

designators such as promoters, CEO,

directors, higher level managers etc.

Different types of management accounting systems and their benefits

Cash budget

It is an expected inflows and outflows of cash for a business over a period. This budget

helps in guiding that an organization have sufficient cash for the operations. With the help of

sales and productions, forecasting for an organization creates cash budgets, along with the

assumptions about necessary spending and account receivables (Coad and Kholeif, 2015). If an

organization do not have much liability to operate, it raises more capital by issuing stock on debt.

Benefits of cash budget

1. It restricts the spending of the organization so you do not incur debt.

2. It helps in forcing thinking critically about the company’s financial situation and makes

realistic prediction.

Inventory management systems

It is a continuous process for tracking products and shares in and out of an organization's

place. Organizations are required to manage the stock on regular basis to place new orders. To

manage the inventory successfully, it means hitting the target because demand and supply are not

constant.

Benefits of inventory management

It determines how much inventory is needed for the purpose of production.

Using nifty inventory management will benefit to stay forward of demand curve, and also

to keep right amount in inventory.

a.

Particulars 5% 10%

Sales Units 75000 75000

Selling Price 10.07 11.66

Sales Revenue 755250 874500

Less: Variable Cost

Units 75000 75000

Rate 4.4 4.4

Variable Cost 330000 330000

Contribution 425250 544500

Less: Fixed Cost 15000 15000

Net Profit 410250 529500

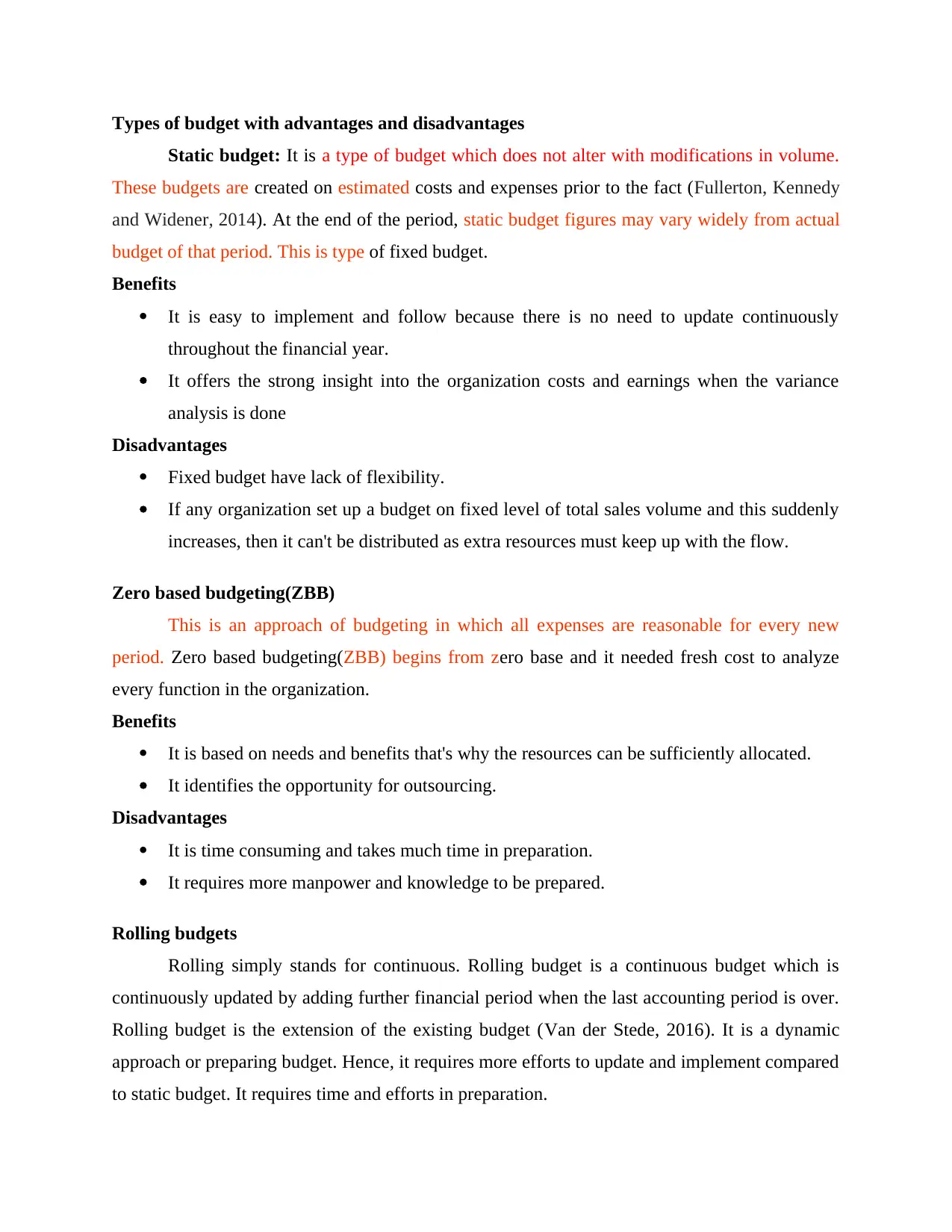

b.

Break-Even analysis

Particular Formula Figures Figures

Selling price per unit(SPPU) 10.7 11.66

Variable cost per unit 4.4 4.4

Contribution per unit(CPU)

Selling price per unit -

variable cost per unit 6.3 7.26

Fixed cost 15000 15000

BEP (in units)

Fixed cost / contribution per

unit 2381 2066

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit

25476.190

4761905

24090.909

0909091

Define budget

A budget is a financial plan for particular time, usually a year. It includes the plan sales

volume and revenues, assets and liability of an organization. It is an estimation of all the future

expenses which are going to occur while achieving the goals.

Budget is the sum of money distributed for a particular purpose and the estimation of

intended expenditure with the proposals how to meet them.

Variable Cost 330000 330000

Contribution 425250 544500

Less: Fixed Cost 15000 15000

Net Profit 410250 529500

b.

Break-Even analysis

Particular Formula Figures Figures

Selling price per unit(SPPU) 10.7 11.66

Variable cost per unit 4.4 4.4

Contribution per unit(CPU)

Selling price per unit -

variable cost per unit 6.3 7.26

Fixed cost 15000 15000

BEP (in units)

Fixed cost / contribution per

unit 2381 2066

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit

25476.190

4761905

24090.909

0909091

Define budget

A budget is a financial plan for particular time, usually a year. It includes the plan sales

volume and revenues, assets and liability of an organization. It is an estimation of all the future

expenses which are going to occur while achieving the goals.

Budget is the sum of money distributed for a particular purpose and the estimation of

intended expenditure with the proposals how to meet them.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Types of budget with advantages and disadvantages

Static budget: It is a type of budget which does not alter with modifications in volume.

These budgets are created on estimated costs and expenses prior to the fact (Fullerton, Kennedy

and Widener, 2014). At the end of the period, static budget figures may vary widely from actual

budget of that period. This is type of fixed budget.

Benefits

It is easy to implement and follow because there is no need to update continuously

throughout the financial year.

It offers the strong insight into the organization costs and earnings when the variance

analysis is done

Disadvantages

Fixed budget have lack of flexibility.

If any organization set up a budget on fixed level of total sales volume and this suddenly

increases, then it can't be distributed as extra resources must keep up with the flow.

Zero based budgeting(ZBB)

This is an approach of budgeting in which all expenses are reasonable for every new

period. Zero based budgeting(ZBB) begins from zero base and it needed fresh cost to analyze

every function in the organization.

Benefits

It is based on needs and benefits that's why the resources can be sufficiently allocated.

It identifies the opportunity for outsourcing.

Disadvantages

It is time consuming and takes much time in preparation.

It requires more manpower and knowledge to be prepared.

Rolling budgets

Rolling simply stands for continuous. Rolling budget is a continuous budget which is

continuously updated by adding further financial period when the last accounting period is over.

Rolling budget is the extension of the existing budget (Van der Stede, 2016). It is a dynamic

approach or preparing budget. Hence, it requires more efforts to update and implement compared

to static budget. It requires time and efforts in preparation.

Static budget: It is a type of budget which does not alter with modifications in volume.

These budgets are created on estimated costs and expenses prior to the fact (Fullerton, Kennedy

and Widener, 2014). At the end of the period, static budget figures may vary widely from actual

budget of that period. This is type of fixed budget.

Benefits

It is easy to implement and follow because there is no need to update continuously

throughout the financial year.

It offers the strong insight into the organization costs and earnings when the variance

analysis is done

Disadvantages

Fixed budget have lack of flexibility.

If any organization set up a budget on fixed level of total sales volume and this suddenly

increases, then it can't be distributed as extra resources must keep up with the flow.

Zero based budgeting(ZBB)

This is an approach of budgeting in which all expenses are reasonable for every new

period. Zero based budgeting(ZBB) begins from zero base and it needed fresh cost to analyze

every function in the organization.

Benefits

It is based on needs and benefits that's why the resources can be sufficiently allocated.

It identifies the opportunity for outsourcing.

Disadvantages

It is time consuming and takes much time in preparation.

It requires more manpower and knowledge to be prepared.

Rolling budgets

Rolling simply stands for continuous. Rolling budget is a continuous budget which is

continuously updated by adding further financial period when the last accounting period is over.

Rolling budget is the extension of the existing budget (Van der Stede, 2016). It is a dynamic

approach or preparing budget. Hence, it requires more efforts to update and implement compared

to static budget. It requires time and efforts in preparation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantages

It reduces the elements of uncertainty in budgeting process, meanwhile they focus on the

short term when ambiguity degree is smaller.

It helps organizations to construct new and improved budgets.

Disadvantages

These are expensive and time intensive than incremental budgets.

There could be a trouble that budget may become terminal budget.

Incremental budget

Incremental budget is a budget prepared with the help of using previous or last year

budget and actual performance as the basis for incremental amounts. It is a type of accounting in

management which is based on concept of making little or small changes in the current budget to

arrive at new budget. Incremental amounts are to be added in a budget to come at new budget.

The management thought that all the branches will keep on operating at their current level of

expenses and in such a case, where extra sum is required then it will get added for future year

budgeting estimation.

Advantages

It does not entail any complex calculation, as this method is easy to implement.

Organization can easy observe the impact of the change in case of incremental budgeting

Disadvantages

It motivates high expenditure so that the budget can be arranged with respect to the

coming year.

This budget can originate everlasting allocation of resources which may change over a

period and will be of no use in future years.

Importance of budget

Budgeting permits implementing a spending plan for the money, it ensures that the

organization will have sufficient amount of money that organization needed to meet out the

expenses. Implementation of budget will keep the organization out for the debt. It helps in

balancing the firms’ expenses to the income. Moreover, some importance of budgeting is as

discussed.

It helps to keep eye on the prize

It reduces the elements of uncertainty in budgeting process, meanwhile they focus on the

short term when ambiguity degree is smaller.

It helps organizations to construct new and improved budgets.

Disadvantages

These are expensive and time intensive than incremental budgets.

There could be a trouble that budget may become terminal budget.

Incremental budget

Incremental budget is a budget prepared with the help of using previous or last year

budget and actual performance as the basis for incremental amounts. It is a type of accounting in

management which is based on concept of making little or small changes in the current budget to

arrive at new budget. Incremental amounts are to be added in a budget to come at new budget.

The management thought that all the branches will keep on operating at their current level of

expenses and in such a case, where extra sum is required then it will get added for future year

budgeting estimation.

Advantages

It does not entail any complex calculation, as this method is easy to implement.

Organization can easy observe the impact of the change in case of incremental budgeting

Disadvantages

It motivates high expenditure so that the budget can be arranged with respect to the

coming year.

This budget can originate everlasting allocation of resources which may change over a

period and will be of no use in future years.

Importance of budget

Budgeting permits implementing a spending plan for the money, it ensures that the

organization will have sufficient amount of money that organization needed to meet out the

expenses. Implementation of budget will keep the organization out for the debt. It helps in

balancing the firms’ expenses to the income. Moreover, some importance of budgeting is as

discussed.

It helps to keep eye on the prize

It helps to have an effective control towards the goals of an organization. For efficient

location of cost and earning, it ensures to map out goals, save money and keep the track of an

organization's progress and make the dream a reality.

It helps in preparing for emergencies

It should include the emergency fund that is consisted of at least three to six months’

worth of live expenses. That save money helps organization if any emergency takes place

(Tappura and et.al. 2015).

Define what is perceptual inventory system

Perpetual inventory system

It is an accounting system which keeps a record of purchases and sale of instant inventory

with the help of organization's asset management system or software and computerized point of

sale system (Nitzl, 2018). It gives an elaborated and thorough information about change in stock

and also gives a report about the actual amount of inventory available.

This system is a better method than ancient episodic inventory system as it permits a

direct and quick tracking about level of sales and inventory of each and every item. It doesn't

need any manual adjustment with any accountant except in disagrees or loss in count due to theft

or damage.

Write the definition of LIFO and FIFO with their advantages and disadvantages.

LIFO is last in first out method. It operates on the ideologies and values that last item of

any inventory which is obtained and will be issued first (Renz, 2016). The valuation in last in

first out method of the material issued is done according to the latest purchase price of materials.

In LIFO the closing stock is taken always on earliest price of materials.

Advantages

LIFO method is suitable for matching of cost with revenue.

Last in first out method is easy to understand and its operation is also simple.

Last in first out method facilitates complete recovery of material cost.

Last in first out method is most suitable when prices are rising.

Disadvantages

Current prices are therefore useless reflected in this method.

Cost comparison of jobs of similar type is not possible due to price disparities.

location of cost and earning, it ensures to map out goals, save money and keep the track of an

organization's progress and make the dream a reality.

It helps in preparing for emergencies

It should include the emergency fund that is consisted of at least three to six months’

worth of live expenses. That save money helps organization if any emergency takes place

(Tappura and et.al. 2015).

Define what is perceptual inventory system

Perpetual inventory system

It is an accounting system which keeps a record of purchases and sale of instant inventory

with the help of organization's asset management system or software and computerized point of

sale system (Nitzl, 2018). It gives an elaborated and thorough information about change in stock

and also gives a report about the actual amount of inventory available.

This system is a better method than ancient episodic inventory system as it permits a

direct and quick tracking about level of sales and inventory of each and every item. It doesn't

need any manual adjustment with any accountant except in disagrees or loss in count due to theft

or damage.

Write the definition of LIFO and FIFO with their advantages and disadvantages.

LIFO is last in first out method. It operates on the ideologies and values that last item of

any inventory which is obtained and will be issued first (Renz, 2016). The valuation in last in

first out method of the material issued is done according to the latest purchase price of materials.

In LIFO the closing stock is taken always on earliest price of materials.

Advantages

LIFO method is suitable for matching of cost with revenue.

Last in first out method is easy to understand and its operation is also simple.

Last in first out method facilitates complete recovery of material cost.

Last in first out method is most suitable when prices are rising.

Disadvantages

Current prices are therefore useless reflected in this method.

Cost comparison of jobs of similar type is not possible due to price disparities.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FIFO Method

It is an inventory valuation method in which valuation is done on the basis of first come first

serve basis. (Otley, 2016). The FIFO stands for first in first out methods. In this method the

material is issued in a chronological order. In FIFO method, opening stock gets allotted first and

the price of material for closing stock is at the cost of the current purchase.

Advantages

It is easy and simple to operate, for application in understanding and functionality.

It is appropriate for materials which are bulky and highly priced.

Disadvantages of FIFO

In inflation, FIFO method overstates profit.

The current production cost may be understated if the prices of material rise rapidly.

Explain how the organization uses the management information systems to responds financial

problems.

The report consist of many ways by which management accountants may guide their company's

in responding the financial problem. They are discussed under-

Management accounting system identified the environmental and social trends which can

have impact of capability of organization to build the value over time (Ax and Greve,

2017.).

Management information system helps in linking in the sustainable business challenges

to the strategy of the firm, outlook of the performance, model of the business, and license

to function.

It helps in implementing the KPIs which support strategic and sustainable goals.

Generates reports which consist of information about the sustainability effects to inform

pricing and budgeting decision, investment appraisal and strategic planning.

CONCLUSION

From the above report, it is concluded that a company has correct management

accounting system that is necessary for selecting an appropriate administrator in a corporation.

Management accounting offers the accurate information to an organization for better decision

making. The study of management accounting assisted the students by illustrations given by the

It is an inventory valuation method in which valuation is done on the basis of first come first

serve basis. (Otley, 2016). The FIFO stands for first in first out methods. In this method the

material is issued in a chronological order. In FIFO method, opening stock gets allotted first and

the price of material for closing stock is at the cost of the current purchase.

Advantages

It is easy and simple to operate, for application in understanding and functionality.

It is appropriate for materials which are bulky and highly priced.

Disadvantages of FIFO

In inflation, FIFO method overstates profit.

The current production cost may be understated if the prices of material rise rapidly.

Explain how the organization uses the management information systems to responds financial

problems.

The report consist of many ways by which management accountants may guide their company's

in responding the financial problem. They are discussed under-

Management accounting system identified the environmental and social trends which can

have impact of capability of organization to build the value over time (Ax and Greve,

2017.).

Management information system helps in linking in the sustainable business challenges

to the strategy of the firm, outlook of the performance, model of the business, and license

to function.

It helps in implementing the KPIs which support strategic and sustainable goals.

Generates reports which consist of information about the sustainability effects to inform

pricing and budgeting decision, investment appraisal and strategic planning.

CONCLUSION

From the above report, it is concluded that a company has correct management

accounting system that is necessary for selecting an appropriate administrator in a corporation.

Management accounting offers the accurate information to an organization for better decision

making. The study of management accounting assisted the students by illustrations given by the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

professors that cannot uphold any blooper. Management accounting played an important role to

assist the decision-making in an efficient manner. The report had summed up with all the

essential aspects of management accounting such as budgeting, inventory evaluation for the

purpose of making the profitable decision for an organization.

assist the decision-making in an efficient manner. The report had summed up with all the

essential aspects of management accounting such as budgeting, inventory evaluation for the

purpose of making the profitable decision for an organization.

REFERENCES

Books and Journals

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34,

pp.59-74.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting Review.

49(1). pp.4-24.

Chiarini, A. and Vagnoni, E., 2015. World-class manufacturing by Fiat. Comparison with Toyota

production system from a strategic management, management accounting, operations

management and performance measurement dimension. International Journal of

Production Research. 53(2). pp.590-606.

Chiwamit, P., Modell, S. and Scapens, R.W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management, .12(2). pp.153-171.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Nitzl, C., 2018. Management Accounting and Partial Least Squares-Structural Equation

Modelling (PLS-SEM): Some Illustrative Examples. In Partial Least Squares Structural

Equation Modeling (pp. 211-229). Springer, Cham.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Tappura, S. and et.al. 2015. A management accounting perspective on safety. Safety science. 71.

pp.151-159.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

Books and Journals

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research, 34,

pp.59-74.

Bui, B. and De Villiers, C., 2017. Business strategies and management accounting in response to

climate change risk exposure and regulatory uncertainty. The British Accounting Review.

49(1). pp.4-24.

Chiarini, A. and Vagnoni, E., 2015. World-class manufacturing by Fiat. Comparison with Toyota

production system from a strategic management, management accounting, operations

management and performance measurement dimension. International Journal of

Production Research. 53(2). pp.590-606.

Chiwamit, P., Modell, S. and Scapens, R.W., 2017. Regulation and adaptation of management

accounting innovations: The case of economic value added in Thai state-owned

enterprises. Management Accounting Research. 37. pp.30-48.

Coad, A., Jack, L. and Kholeif, A.O.R., 2015. Structuration theory: reflections on its further

potential for management accounting research. Qualitative Research in Accounting &

Management, .12(2). pp.153-171.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2014. Lean manufacturing and firm

performance: The incremental contribution of lean management accounting

practices. Journal of Operations Management. 32(7-8). pp.414-428.

Nitzl, C., 2018. Management Accounting and Partial Least Squares-Structural Equation

Modelling (PLS-SEM): Some Illustrative Examples. In Partial Least Squares Structural

Equation Modeling (pp. 211-229). Springer, Cham.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–

2014. Management accounting research. 31. pp.45-62.

Renz, D.O., 2016. The Jossey-Bass handbook of nonprofit leadership and management. John

Wiley & Sons.

Tappura, S. and et.al. 2015. A management accounting perspective on safety. Safety science. 71.

pp.151-159.

Van der Stede, W.A., 2016. Management accounting in context: Industry, regulation and

informatics. Management Accounting Research. 31. pp.100-102.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.