Management Accounting Report: Processes, Techniques, and Evaluation

VerifiedAdded on 2021/01/03

|17

|5119

|319

Report

AI Summary

This report delves into the core concepts of management accounting, exploring its processes, techniques, and applications within a business context. It begins by defining management accounting and its role in organizational planning, control, and decision-making, contrasting it with financial accounting. The report then examines various management accounting tools such as cost accounting systems (normal costing, standard costing), job costing, and inventory management techniques (FIFO, LIFO, weighted average). It further analyzes different types of managerial accounting reports, including budget reports, accounts receivable reports, and inventory management reports, emphasizing their importance for informed decision-making. The report also evaluates the benefits of using a management accounting system and critically assesses different accounting reporting techniques, culminating in a discussion of financial issues and the balance scorecard method. The content includes a table of contents, introduction, task-based analysis, and conclusion, providing a comprehensive overview of management accounting principles and practices. The report concludes by evaluating financial issues and the balance scorecard method.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management Accounting process.........................................................................................1

B). Presently financial information:............................................................................................4

M1 Benefits of using management accounting system...............................................................5

D1 Critical evaluation of accounting reporting techniques.........................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing method used to calculate total net profit.......................................6

M2: Various types of accounting techniques..............................................................................8

D2: Analysis of data collected or reconciliation.........................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of various types of budget....................................................................9

M3: Analysis of different planning tools..................................................................................11

D3: Critical evaluation of financial issues................................................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard method..................................................................................................11

M4: Evaluating financial issues................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management Accounting process.........................................................................................1

B). Presently financial information:............................................................................................4

M1 Benefits of using management accounting system...............................................................5

D1 Critical evaluation of accounting reporting techniques.........................................................5

TASK 2............................................................................................................................................6

P3: Various types of costing method used to calculate total net profit.......................................6

M2: Various types of accounting techniques..............................................................................8

D2: Analysis of data collected or reconciliation.........................................................................9

TASK 3............................................................................................................................................9

P4: Merits and demerits of various types of budget....................................................................9

M3: Analysis of different planning tools..................................................................................11

D3: Critical evaluation of financial issues................................................................................11

TASK 4..........................................................................................................................................11

P5: Balance scorecard method..................................................................................................11

M4: Evaluating financial issues................................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Currently, there is a strong need to adopt various management accounting systems in the

business in order to grow rapidly, nowadays, there is a strong need to adopt this tool in an

efficient manner that can be used by the management accountant in the firm for gaining the

sustainable development (Amoako, 2013). This is the report which is based upon the diverse

management accountant tools that could help out to gain the sustainability for the longer term.

Now, on the basis of the such systems, accountant would able to make certain reports which

would help out to gain the sustainability in an effective manner. Apart from that, net profits as

per the marginal costing and absorption costing is calculated in this report. Advantages and

disadvantages of the diverse budgetary tools are mentioned under this report which would help

out to gain the pre-set objectives in an effective manner. financial problems are overcome by

way of using certain management accounting systems that could lead to gain the competitive

advantages in an effective manner.

TASK 1

P1. Management Accounting process

MA is the process which ultimately helps the organisation to gain the better planning and

control over the firm. This is the most relevant for whole kinds of firm covering a non-

governmental organisation, governmental and proprietorships firms. This is not an easy task

which mostly requires highly educated professional bodies. Management accounting systems are

the one which can be used by the organisation in order to make certain objectives in an effective

manner. now, there are so many tools which can be used by the organisation in order to gain

tools in an effective manner (Klemstine and Maher, 2014). There are so many management

accounting tools which can be used by the organisation in order to gain the sustainability.

Management accounting is the accounting resources of a company which ensure a maximum

utilization of the resources.

The main aim behind management accounting are as follows:

Forming crucial strategic decisions about the organisation.

Planning for future organisation activities.

Assessing and controlling of performance.

Appropriate use of resources.

1

Currently, there is a strong need to adopt various management accounting systems in the

business in order to grow rapidly, nowadays, there is a strong need to adopt this tool in an

efficient manner that can be used by the management accountant in the firm for gaining the

sustainable development (Amoako, 2013). This is the report which is based upon the diverse

management accountant tools that could help out to gain the sustainability for the longer term.

Now, on the basis of the such systems, accountant would able to make certain reports which

would help out to gain the sustainability in an effective manner. Apart from that, net profits as

per the marginal costing and absorption costing is calculated in this report. Advantages and

disadvantages of the diverse budgetary tools are mentioned under this report which would help

out to gain the pre-set objectives in an effective manner. financial problems are overcome by

way of using certain management accounting systems that could lead to gain the competitive

advantages in an effective manner.

TASK 1

P1. Management Accounting process

MA is the process which ultimately helps the organisation to gain the better planning and

control over the firm. This is the most relevant for whole kinds of firm covering a non-

governmental organisation, governmental and proprietorships firms. This is not an easy task

which mostly requires highly educated professional bodies. Management accounting systems are

the one which can be used by the organisation in order to make certain objectives in an effective

manner. now, there are so many tools which can be used by the organisation in order to gain

tools in an effective manner (Klemstine and Maher, 2014). There are so many management

accounting tools which can be used by the organisation in order to gain the sustainability.

Management accounting is the accounting resources of a company which ensure a maximum

utilization of the resources.

The main aim behind management accounting are as follows:

Forming crucial strategic decisions about the organisation.

Planning for future organisation activities.

Assessing and controlling of performance.

Appropriate use of resources.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Forming the basis of financial reports.

Asset safeguarding.

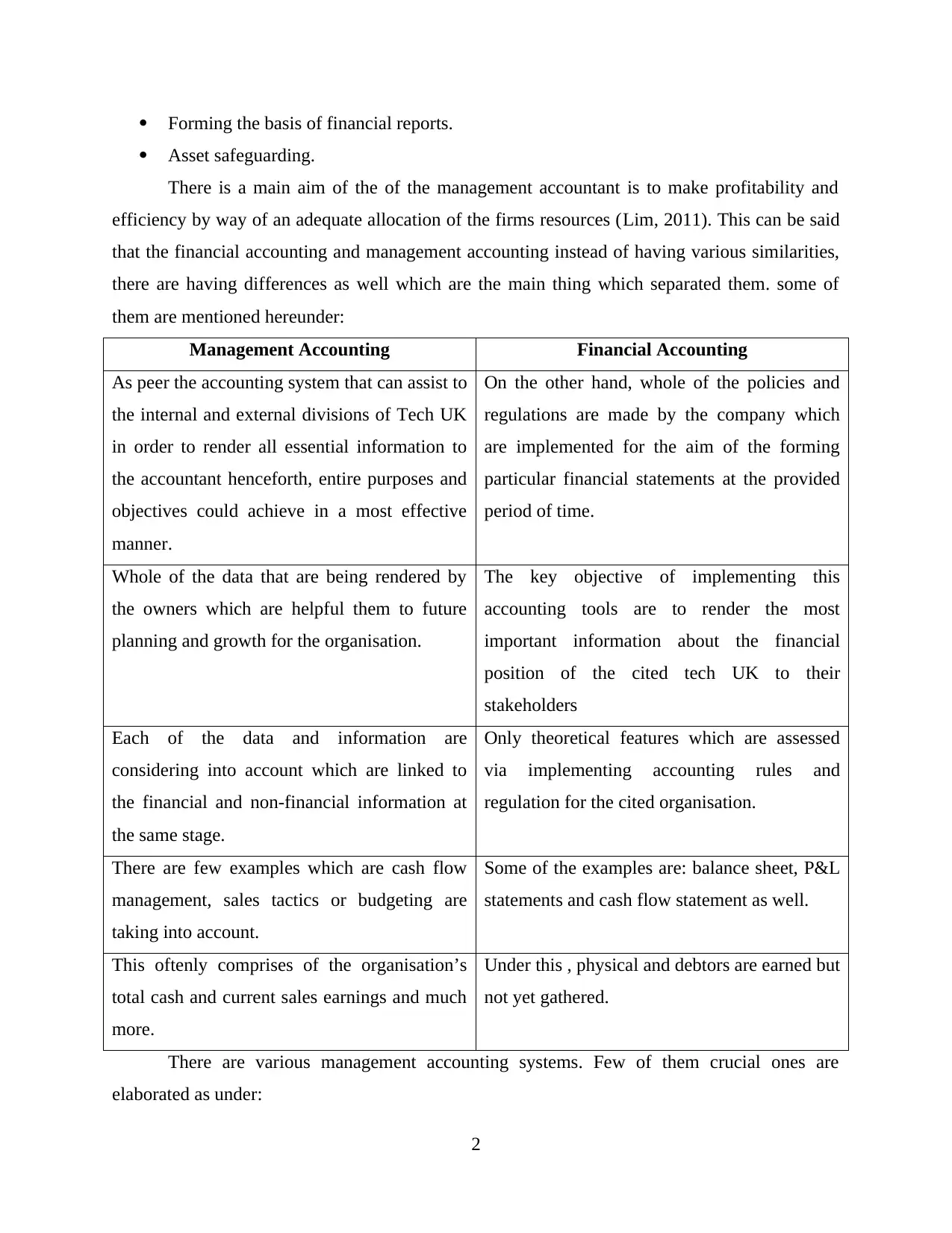

There is a main aim of the of the management accountant is to make profitability and

efficiency by way of an adequate allocation of the firms resources (Lim, 2011). This can be said

that the financial accounting and management accounting instead of having various similarities,

there are having differences as well which are the main thing which separated them. some of

them are mentioned hereunder:

Management Accounting Financial Accounting

As peer the accounting system that can assist to

the internal and external divisions of Tech UK

in order to render all essential information to

the accountant henceforth, entire purposes and

objectives could achieve in a most effective

manner.

On the other hand, whole of the policies and

regulations are made by the company which

are implemented for the aim of the forming

particular financial statements at the provided

period of time.

Whole of the data that are being rendered by

the owners which are helpful them to future

planning and growth for the organisation.

The key objective of implementing this

accounting tools are to render the most

important information about the financial

position of the cited tech UK to their

stakeholders

Each of the data and information are

considering into account which are linked to

the financial and non-financial information at

the same stage.

Only theoretical features which are assessed

via implementing accounting rules and

regulation for the cited organisation.

There are few examples which are cash flow

management, sales tactics or budgeting are

taking into account.

Some of the examples are: balance sheet, P&L

statements and cash flow statement as well.

This oftenly comprises of the organisation’s

total cash and current sales earnings and much

more.

Under this , physical and debtors are earned but

not yet gathered.

There are various management accounting systems. Few of them crucial ones are

elaborated as under:

2

Asset safeguarding.

There is a main aim of the of the management accountant is to make profitability and

efficiency by way of an adequate allocation of the firms resources (Lim, 2011). This can be said

that the financial accounting and management accounting instead of having various similarities,

there are having differences as well which are the main thing which separated them. some of

them are mentioned hereunder:

Management Accounting Financial Accounting

As peer the accounting system that can assist to

the internal and external divisions of Tech UK

in order to render all essential information to

the accountant henceforth, entire purposes and

objectives could achieve in a most effective

manner.

On the other hand, whole of the policies and

regulations are made by the company which

are implemented for the aim of the forming

particular financial statements at the provided

period of time.

Whole of the data that are being rendered by

the owners which are helpful them to future

planning and growth for the organisation.

The key objective of implementing this

accounting tools are to render the most

important information about the financial

position of the cited tech UK to their

stakeholders

Each of the data and information are

considering into account which are linked to

the financial and non-financial information at

the same stage.

Only theoretical features which are assessed

via implementing accounting rules and

regulation for the cited organisation.

There are few examples which are cash flow

management, sales tactics or budgeting are

taking into account.

Some of the examples are: balance sheet, P&L

statements and cash flow statement as well.

This oftenly comprises of the organisation’s

total cash and current sales earnings and much

more.

Under this , physical and debtors are earned but

not yet gathered.

There are various management accounting systems. Few of them crucial ones are

elaborated as under:

2

Cost accounting system: This is also known as the framework which is used by the

organisation in order to forecast the cost of their goods for profitability analysis, inventory

valuation and cost control. Forecasting of an appropriate costs of the items is critical for the

profitable operations. An organisation is required to assess which items are profitable and which

one are not, and this could be identified only when this has forecasted this costing system which

assists in forecasting the closing value of the material inventory, work in progress and closing

inventory for the ultimate objective of the financial statement.

1. Normal costing: This can be rightly said the cost accounting system is used the costs

which can be real direct material at the time of forecasting of the overhead costs. Normal

costs are the general costs at the time of the cost of overheads. Normal costs are the one

which are common expenses of the organisation that occurs the normal operations of the

organisation. For example: normal expense are the repairs expenses which repairs and

maintenance, salaries and wages to the employees, office and administration expenses.

2. Standard costing: This is a tool of the accounting which produce in order to find out the

differences or the variances as well (Van der Stede, 2015). the main differences between

actual costs of the goods and services which occurred at the time of production. Costs

which should have been incurred at the time of the manufacturing of the goods and

services which is called as the standard costs.

If actual costs of the organisation these direct material costs, direct labour costs which are

emerged to be more to standards which are fixed by the cited organisation or the standard

cost than the forecasted net earnings would not appropriate.

Job costing systems: This is the system which gather the manufacturing costs individually

for each job. This is the clear that the organisation is totally engaged in the manufacturing of the

antique products and special orders.

Inventory management accounting: This is the system which is used by the organisation in

order to know the cost of the production in an effective manner. However, this can be rightly

said that the management of cited organisation needs to use their resources so that the optimum

benefits can be gained in an effective manner. there are certain ways through which the inventory

can be optimum used. Some of the main ways are mentioned hereunder:

3

organisation in order to forecast the cost of their goods for profitability analysis, inventory

valuation and cost control. Forecasting of an appropriate costs of the items is critical for the

profitable operations. An organisation is required to assess which items are profitable and which

one are not, and this could be identified only when this has forecasted this costing system which

assists in forecasting the closing value of the material inventory, work in progress and closing

inventory for the ultimate objective of the financial statement.

1. Normal costing: This can be rightly said the cost accounting system is used the costs

which can be real direct material at the time of forecasting of the overhead costs. Normal

costs are the general costs at the time of the cost of overheads. Normal costs are the one

which are common expenses of the organisation that occurs the normal operations of the

organisation. For example: normal expense are the repairs expenses which repairs and

maintenance, salaries and wages to the employees, office and administration expenses.

2. Standard costing: This is a tool of the accounting which produce in order to find out the

differences or the variances as well (Van der Stede, 2015). the main differences between

actual costs of the goods and services which occurred at the time of production. Costs

which should have been incurred at the time of the manufacturing of the goods and

services which is called as the standard costs.

If actual costs of the organisation these direct material costs, direct labour costs which are

emerged to be more to standards which are fixed by the cited organisation or the standard

cost than the forecasted net earnings would not appropriate.

Job costing systems: This is the system which gather the manufacturing costs individually

for each job. This is the clear that the organisation is totally engaged in the manufacturing of the

antique products and special orders.

Inventory management accounting: This is the system which is used by the organisation in

order to know the cost of the production in an effective manner. However, this can be rightly

said that the management of cited organisation needs to use their resources so that the optimum

benefits can be gained in an effective manner. there are certain ways through which the inventory

can be optimum used. Some of the main ways are mentioned hereunder:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

First in First out: This is known as the FIFO method. Under this, the inventory provided the

order or directions to use the inventory which are firstly placed which simply means that the raw

material which are firstly use is firstly used for making the production in an effective manner.

Last in First Out: This is also known as the LIFO method. Which simply used the raw

material which are lastly placed. The manager used the raw material which is lastly placed.

Weighted average system of the inventory: Under this system, the inventory took place

according to the weighted average amount of the inventory which emerge from the first to last

and then implemented inventory in the manufacturing of the goods.

B). Presently financial information:

Different kinds of managerial accounting reports:

Managerial accounting covers the costs that comprises insider information which are

attained from the financial accounting. Managerial accounting reports are implemented for

planning, regulation, decision making and calculating of performance. These managerial reports

are produced via financial and accounting years according to requirements. Various critical

decisions are based on these reports which are being appropriate. Managers assess these reports

which are mostly careful and convert them into an effective information that are being required

by the organisation (Lavia López and Hiebl, 2014). Managers of the cited organisation evaluates

these reports in order to come to the reliable conclusions. There are so many kinds of the useful

information that are needed by the organisation. Some of the management accounting reports are

elaborated as under:

Budget Report: This is the managerial accounting tools which assist the managers and

the company’s top level executives about the future forecasting of expenses or revenues for a

certain period of time. Budget report are formed by implementing by implementing past

experiences, on the other hand, by taking help of budget report, organisation is trying to attain its

pre-set targets by implementing budgeted amount. An efficient budget report could assist the

organisations to cut costs of the production and also could contribute to the optimisation of the

profits by cutting of the cost in the raw materials which are being supplied to the organisation.

Accounts receivables report: If the organisation is among those organisations that are

based upon the extending credits then this is crucial to form account receivables reports. This

have the information which are related to the debtors and defaulters as well.

4

order or directions to use the inventory which are firstly placed which simply means that the raw

material which are firstly use is firstly used for making the production in an effective manner.

Last in First Out: This is also known as the LIFO method. Which simply used the raw

material which are lastly placed. The manager used the raw material which is lastly placed.

Weighted average system of the inventory: Under this system, the inventory took place

according to the weighted average amount of the inventory which emerge from the first to last

and then implemented inventory in the manufacturing of the goods.

B). Presently financial information:

Different kinds of managerial accounting reports:

Managerial accounting covers the costs that comprises insider information which are

attained from the financial accounting. Managerial accounting reports are implemented for

planning, regulation, decision making and calculating of performance. These managerial reports

are produced via financial and accounting years according to requirements. Various critical

decisions are based on these reports which are being appropriate. Managers assess these reports

which are mostly careful and convert them into an effective information that are being required

by the organisation (Lavia López and Hiebl, 2014). Managers of the cited organisation evaluates

these reports in order to come to the reliable conclusions. There are so many kinds of the useful

information that are needed by the organisation. Some of the management accounting reports are

elaborated as under:

Budget Report: This is the managerial accounting tools which assist the managers and

the company’s top level executives about the future forecasting of expenses or revenues for a

certain period of time. Budget report are formed by implementing by implementing past

experiences, on the other hand, by taking help of budget report, organisation is trying to attain its

pre-set targets by implementing budgeted amount. An efficient budget report could assist the

organisations to cut costs of the production and also could contribute to the optimisation of the

profits by cutting of the cost in the raw materials which are being supplied to the organisation.

Accounts receivables report: If the organisation is among those organisations that are

based upon the extending credits then this is crucial to form account receivables reports. This

have the information which are related to the debtors and defaulters as well.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Inventory management Report: This comprises one of the most efficient system which

could be measured the whole stock of a company. Inventory management system which assist in

the guidance of total supply, distribution and storage of the inventory which are kept by the

organisation. Inventory management system takes into account opening and closing stocks of the

inventory.

Importance of format of implementing reporting systems: This reporting system is

much crucial as various aspect of an enterprise. These system of report can help the division in

making certain whether the decision of valuable investment is conducted for the enterprise. This

report is utilised to ascertain comparison of actual and standard reports.

Setting performance booster and considering this: Effective use of proper

interpretation of such report of information can assist in finalising the suitable solution of

provided issues I.e. emerged within the referred organisation.

Reliability Optimisation: The foremost and initial manager role is to accumulate

information in more efficient manner (Bennett, Schaltegger and Zvezdov, 2013). Through the

assistance of effective reporting framework, organisation can control and improve their mistake

the influence of organisation’s production procedure.

M1 Benefits of using management accounting system

It has been seen that every one of those accounting strategies an organization is utilizing

as a part of an association are having some sort of advantages which will help with expanding

general development and productivity for the organization. In the event that Tech UK is utilizing

taken a toll bookkeeping framework they can decide particular relationship sum ordinary, real

and standard cost they are bringing about underway of items. While stock administration

framework which help them to track current position of stock those are being kept by an

association with them. Though work costing is use to investigate add up to cost they are putting

resources into assembling of a particular occupation cost.

D1 Critical evaluation of accounting reporting techniques

As per creating more suitable outcomes for the organization. Supervisor need to make

utilization of important announting techniques. These reports are being displaying before

different financial specialists and partner to make future important choice with respect to their

capital interest in their up and coming ventures. Strategies like execution report which is should

have been actualized in particular way so real position can be investigate. While of record

5

could be measured the whole stock of a company. Inventory management system which assist in

the guidance of total supply, distribution and storage of the inventory which are kept by the

organisation. Inventory management system takes into account opening and closing stocks of the

inventory.

Importance of format of implementing reporting systems: This reporting system is

much crucial as various aspect of an enterprise. These system of report can help the division in

making certain whether the decision of valuable investment is conducted for the enterprise. This

report is utilised to ascertain comparison of actual and standard reports.

Setting performance booster and considering this: Effective use of proper

interpretation of such report of information can assist in finalising the suitable solution of

provided issues I.e. emerged within the referred organisation.

Reliability Optimisation: The foremost and initial manager role is to accumulate

information in more efficient manner (Bennett, Schaltegger and Zvezdov, 2013). Through the

assistance of effective reporting framework, organisation can control and improve their mistake

the influence of organisation’s production procedure.

M1 Benefits of using management accounting system

It has been seen that every one of those accounting strategies an organization is utilizing

as a part of an association are having some sort of advantages which will help with expanding

general development and productivity for the organization. In the event that Tech UK is utilizing

taken a toll bookkeeping framework they can decide particular relationship sum ordinary, real

and standard cost they are bringing about underway of items. While stock administration

framework which help them to track current position of stock those are being kept by an

association with them. Though work costing is use to investigate add up to cost they are putting

resources into assembling of a particular occupation cost.

D1 Critical evaluation of accounting reporting techniques

As per creating more suitable outcomes for the organization. Supervisor need to make

utilization of important announting techniques. These reports are being displaying before

different financial specialists and partner to make future important choice with respect to their

capital interest in their up and coming ventures. Strategies like execution report which is should

have been actualized in particular way so real position can be investigate. While of record

5

receivable report which is utilized to decide add up to day and age for gathering fundamental

capital from the borrowers.

TASK 2

P3: Various types of costing method used to calculate total net profit

Cost in paramount part for producing the commodities of manufacturing organisation to

evaluate their entire required cost of entire product production unit. The initial purpose of

utilising these price is to ascertain whether certain evaluation of net capital which organisation

are going to invest in the goods and production procedure (Ahmad, 2012). The price is generally

determined as the amount value i.e. being paid in order to attain something. There are numerous

costing types which are optimised through analyse of accounting in regard of analysing whole

benefit of organisation. Some of those costing techniques are discussed as below:

Absorption costing: This can be referred as one of the most significant methods i.e.

utilised through Tech UK at the manufacturing goods between the process. These price consist of

both fixed and variable price due to which this is considered as whole costing method. This is not

suitable in order to make certain the company's further decision making.

Marginal costing: This can be referred as the most suitable method of costing i.e. is

assisting or can be implacable for the organisation which is paid for the additional unit

production. This include of fixed and variable cost which are avoided for evaluating entire

company's benefit (BSC Terminology: Perspective, 2017. It can be considered as more reliable

method i.e. used for future decision making procedure.

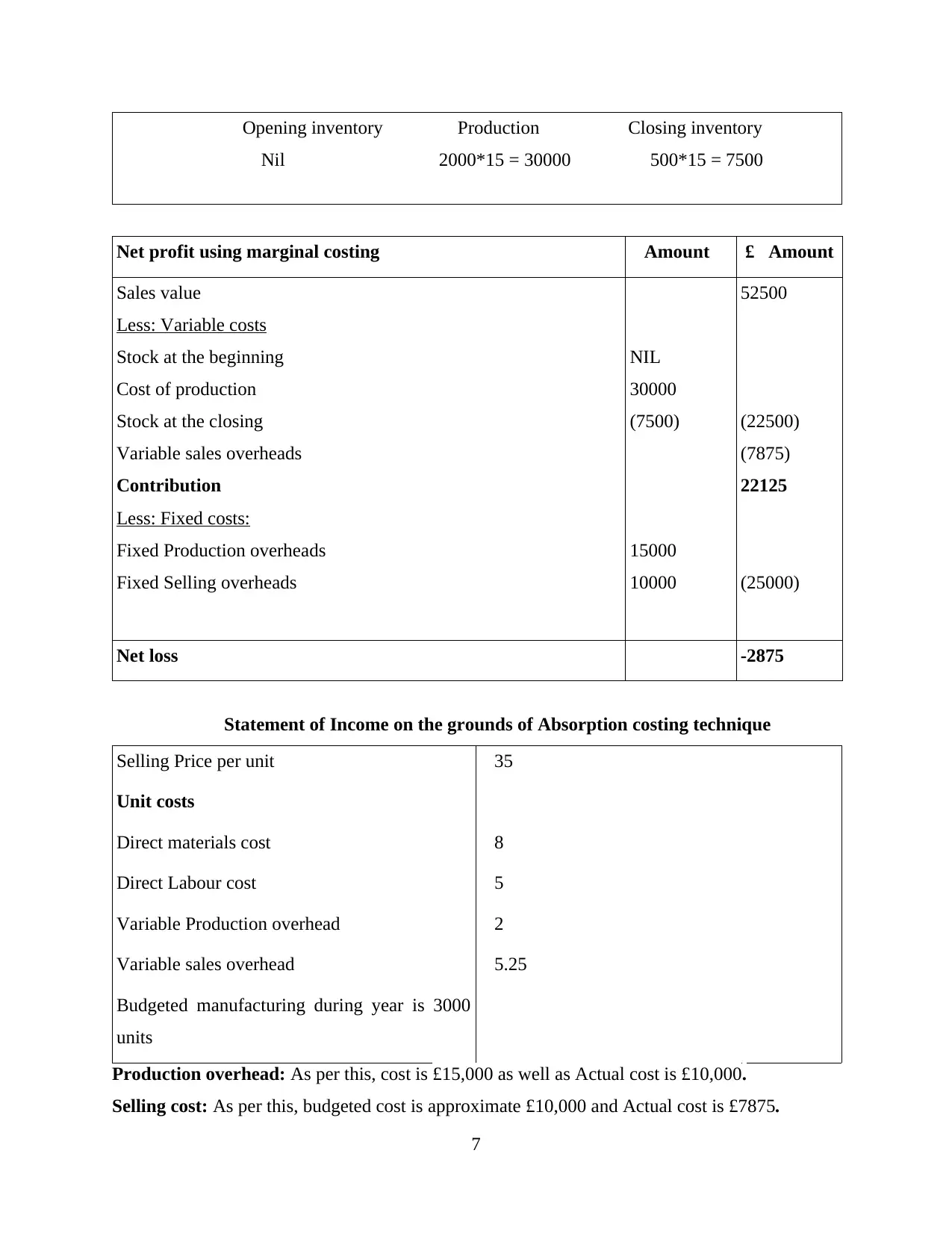

Statement of Income as on September through utilizing method of Marginal costing:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

6

capital from the borrowers.

TASK 2

P3: Various types of costing method used to calculate total net profit

Cost in paramount part for producing the commodities of manufacturing organisation to

evaluate their entire required cost of entire product production unit. The initial purpose of

utilising these price is to ascertain whether certain evaluation of net capital which organisation

are going to invest in the goods and production procedure (Ahmad, 2012). The price is generally

determined as the amount value i.e. being paid in order to attain something. There are numerous

costing types which are optimised through analyse of accounting in regard of analysing whole

benefit of organisation. Some of those costing techniques are discussed as below:

Absorption costing: This can be referred as one of the most significant methods i.e.

utilised through Tech UK at the manufacturing goods between the process. These price consist of

both fixed and variable price due to which this is considered as whole costing method. This is not

suitable in order to make certain the company's further decision making.

Marginal costing: This can be referred as the most suitable method of costing i.e. is

assisting or can be implacable for the organisation which is paid for the additional unit

production. This include of fixed and variable cost which are avoided for evaluating entire

company's benefit (BSC Terminology: Perspective, 2017. It can be considered as more reliable

method i.e. used for future decision making procedure.

Statement of Income as on September through utilizing method of Marginal costing:

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Statement of Income on the grounds of Absorption costing technique

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted manufacturing during year is 3000

units

Production overhead: As per this, cost is £15,000 as well as Actual cost is £10,000.

Selling cost: As per this, budgeted cost is approximate £10,000 and Actual cost is £7875.

7

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the beginning

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Statement of Income on the grounds of Absorption costing technique

Selling Price per unit £35

Unit costs

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted manufacturing during year is 3000

units

Production overhead: As per this, cost is £15,000 as well as Actual cost is £10,000.

Selling cost: As per this, budgeted cost is approximate £10,000 and Actual cost is £7875.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

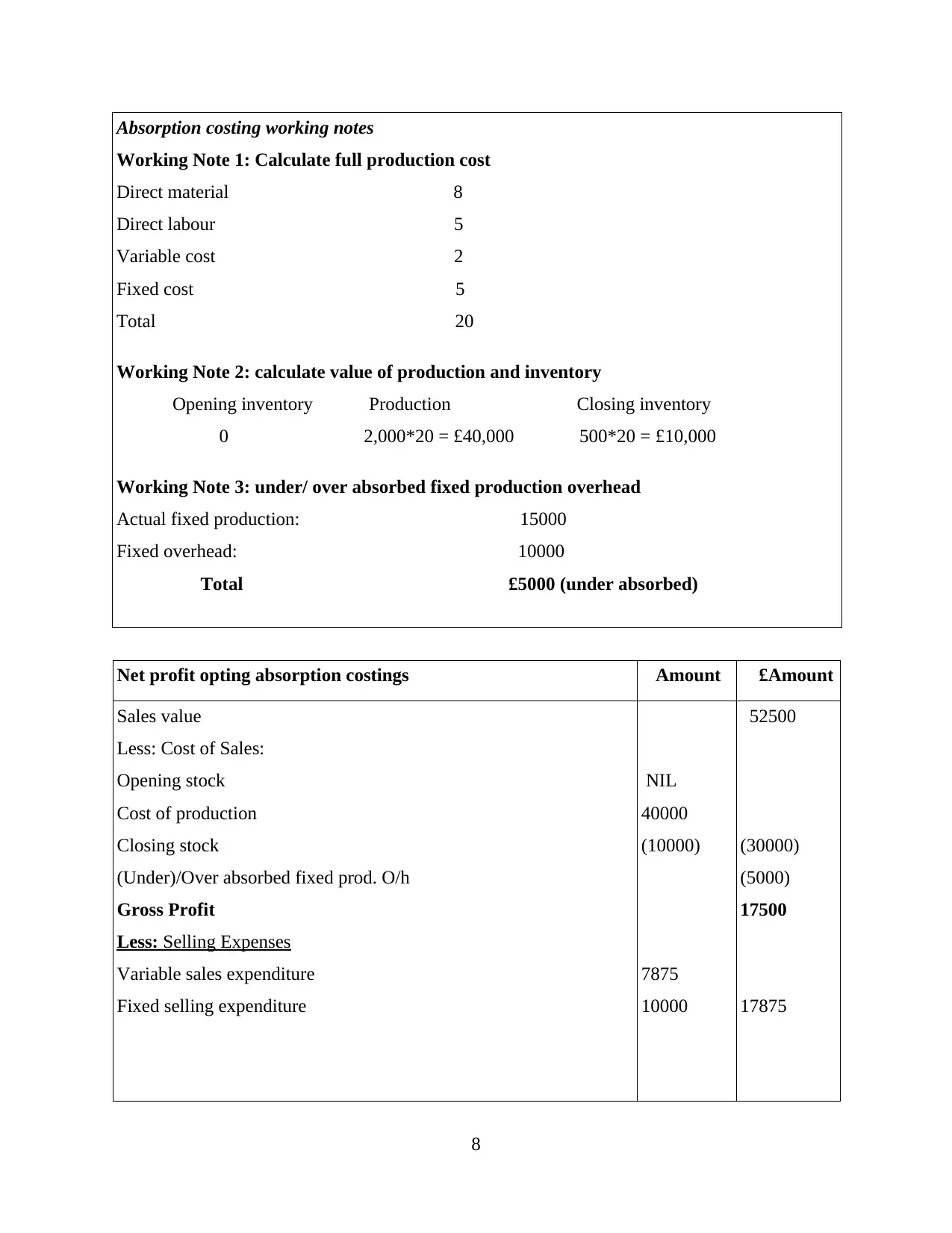

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of production and inventory

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit opting absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

8

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of production and inventory

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit opting absorption costings £Amount £Amount

Sales value

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

52500

(30000)

(5000)

17500

17875

8

Net loss -375

M2: Various types of accounting techniques

In regard of analysing the financial position within the Tech UK, this is essential for

manager to make certain the use of numerous accounting methods i.e. assisting for creating

sustainability and growth of enterprise. Few techniques are ABC costing i.e. utilised to

classifying certain commodities according to the nature (Renz and Herman, 2016). While

working over performance technique, this can aid them in setting current situation through

analysing net capital accessible. Standard techniques of costing are utilised in order to compare

the actual result with the standard one. A marginal technique is more reliable for growth decision

making and creating more sustainability in future business purpose.

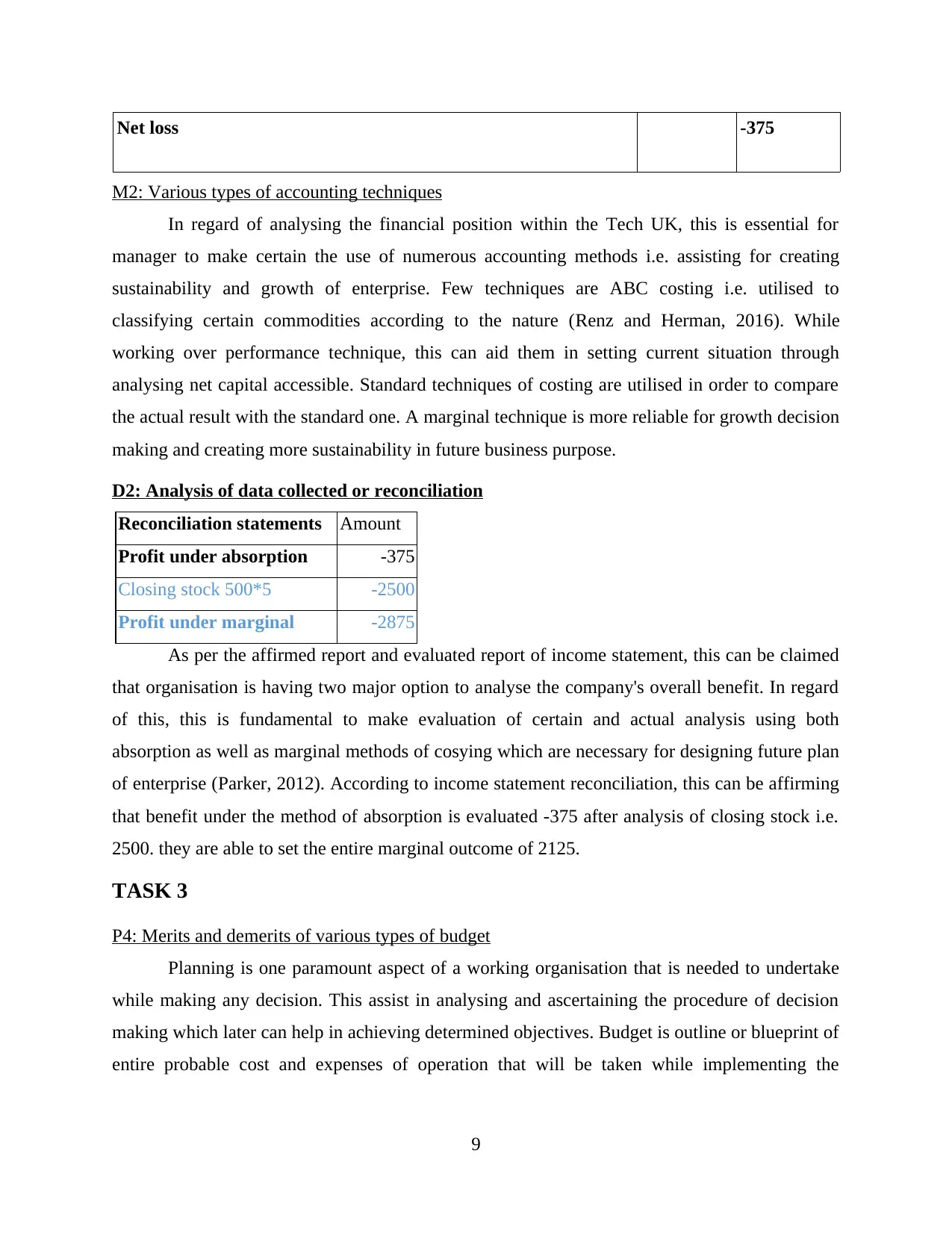

D2: Analysis of data collected or reconciliation

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 -2500

Profit under marginal -2875

As per the affirmed report and evaluated report of income statement, this can be claimed

that organisation is having two major option to analyse the company's overall benefit. In regard

of this, this is fundamental to make evaluation of certain and actual analysis using both

absorption as well as marginal methods of cosying which are necessary for designing future plan

of enterprise (Parker, 2012). According to income statement reconciliation, this can be affirming

that benefit under the method of absorption is evaluated -375 after analysis of closing stock i.e.

2500. they are able to set the entire marginal outcome of 2125.

TASK 3

P4: Merits and demerits of various types of budget

Planning is one paramount aspect of a working organisation that is needed to undertake

while making any decision. This assist in analysing and ascertaining the procedure of decision

making which later can help in achieving determined objectives. Budget is outline or blueprint of

entire probable cost and expenses of operation that will be taken while implementing the

9

M2: Various types of accounting techniques

In regard of analysing the financial position within the Tech UK, this is essential for

manager to make certain the use of numerous accounting methods i.e. assisting for creating

sustainability and growth of enterprise. Few techniques are ABC costing i.e. utilised to

classifying certain commodities according to the nature (Renz and Herman, 2016). While

working over performance technique, this can aid them in setting current situation through

analysing net capital accessible. Standard techniques of costing are utilised in order to compare

the actual result with the standard one. A marginal technique is more reliable for growth decision

making and creating more sustainability in future business purpose.

D2: Analysis of data collected or reconciliation

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 -2500

Profit under marginal -2875

As per the affirmed report and evaluated report of income statement, this can be claimed

that organisation is having two major option to analyse the company's overall benefit. In regard

of this, this is fundamental to make evaluation of certain and actual analysis using both

absorption as well as marginal methods of cosying which are necessary for designing future plan

of enterprise (Parker, 2012). According to income statement reconciliation, this can be affirming

that benefit under the method of absorption is evaluated -375 after analysis of closing stock i.e.

2500. they are able to set the entire marginal outcome of 2125.

TASK 3

P4: Merits and demerits of various types of budget

Planning is one paramount aspect of a working organisation that is needed to undertake

while making any decision. This assist in analysing and ascertaining the procedure of decision

making which later can help in achieving determined objectives. Budget is outline or blueprint of

entire probable cost and expenses of operation that will be taken while implementing the

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.