Management Accounting: Financial Consultancy Report Analysis

VerifiedAdded on 2021/02/22

|19

|5431

|62

Report

AI Summary

This report delves into the realm of management accounting, presenting a comprehensive analysis of its core principles and practical applications within a financial consultancy context. The report begins with an introduction to management accounting, distinguishing it from financial accounting and highlighting its importance for internal decision-making. It then explores various management accounting systems, including cost accounting, inventory management, price optimization, and job costing, along with their respective advantages. The report further examines methods of management accounting reporting, emphasizing the importance of understandable information presentation and detailing different types of reports such as cost accounting reports, account receivable aging reports, inventory management reports, and performance reports. The report also discusses costing techniques for preparing financial statements, including cost volume profit analysis, flexible budgeting, cost variance, absorption & marginal costing, and cost allocation, along with the concepts of fixed and variable costs. The report concludes by addressing how management accounting can be used to overcome financial issues. The report uses Bright star financial consultancy and its client Stitchland Ltd to illustrate the concepts.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explanation of management accounting and essential requirement of various accounting

systems........................................................................................................................................3

P2. Explanation of various kind of methods of management accounting reporting...................6

TASK 2. ..........................................................................................................................................7

P3 Costing Techniques for preparing the financial statements...................................................7

TASK 3..........................................................................................................................................12

P4 Benefits and drawbacks of different planning tools............................................................12

TASK 4..........................................................................................................................................16

P5 Management accounting in response to overcome financial issues.....................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explanation of management accounting and essential requirement of various accounting

systems........................................................................................................................................3

P2. Explanation of various kind of methods of management accounting reporting...................6

TASK 2. ..........................................................................................................................................7

P3 Costing Techniques for preparing the financial statements...................................................7

TASK 3..........................................................................................................................................12

P4 Benefits and drawbacks of different planning tools............................................................12

TASK 4..........................................................................................................................................16

P5 Management accounting in response to overcome financial issues.....................................16

CONCLUSION..............................................................................................................................18

REFERENCES..............................................................................................................................19

INTRODUCTION

Management accounting is an accounting system that arranges financial and non-

financial information in a systematic manner which becomes a basis for the managers for internal

management (Carpenter and Mahoney, 2012). In other way, this accounting system can be

defined as a type of accounting process, which provide reports to the managers so that they can

make competitive policies and plans for future. In the project report, management accounting is

defined in a broad sense including demonstration about various management accounting systems,

use of costing techniques for presenting the income statements. As well as use of planning tools

and management, accounting systems in overcoming from the financial crises is mentioned. For

better understanding about these a financial consultancy, company is selected that is Bright star

financial consultancy and it is located in UK. This company provides consultancy services to

different companies and Stitchland Ltd is one of them which manufacturer the cloths.

TASK 1.

P1 Explanation of management accounting and essential requirement of various accounting

systems.

Management accounting- Management accounting is an accounting system which is linked

with the internal management of the companies so that they can take maximum use of available

resources (Ross, 2017). Such as the Stitchland Ltd company, use this accounting system in their

operations of manufacturing process.

Management accounting system- The management accounting is a kind of system that arranges

the monetary and non monetary information of company in an effective manner for the purpose

of internal decision-making. It is important to know about the management accounting system

that it is beneficial for only to the internal stakeholders not for external stakeholders.

Importance to integrate different accounting systems within the organisations: Different

kind of accounting systems are useful in the Stitchland Ltd company. Like the cost accounting

system helps in computing the cost as well as inventory management system is beneficial in

effective management of stock (Munday,Turner and Jones, 2013). Apart from it price

optimisation system provides a framework for determining the prices. So this is why these

accounting systems have their importance.

Management accounting is an accounting system that arranges financial and non-

financial information in a systematic manner which becomes a basis for the managers for internal

management (Carpenter and Mahoney, 2012). In other way, this accounting system can be

defined as a type of accounting process, which provide reports to the managers so that they can

make competitive policies and plans for future. In the project report, management accounting is

defined in a broad sense including demonstration about various management accounting systems,

use of costing techniques for presenting the income statements. As well as use of planning tools

and management, accounting systems in overcoming from the financial crises is mentioned. For

better understanding about these a financial consultancy, company is selected that is Bright star

financial consultancy and it is located in UK. This company provides consultancy services to

different companies and Stitchland Ltd is one of them which manufacturer the cloths.

TASK 1.

P1 Explanation of management accounting and essential requirement of various accounting

systems.

Management accounting- Management accounting is an accounting system which is linked

with the internal management of the companies so that they can take maximum use of available

resources (Ross, 2017). Such as the Stitchland Ltd company, use this accounting system in their

operations of manufacturing process.

Management accounting system- The management accounting is a kind of system that arranges

the monetary and non monetary information of company in an effective manner for the purpose

of internal decision-making. It is important to know about the management accounting system

that it is beneficial for only to the internal stakeholders not for external stakeholders.

Importance to integrate different accounting systems within the organisations: Different

kind of accounting systems are useful in the Stitchland Ltd company. Like the cost accounting

system helps in computing the cost as well as inventory management system is beneficial in

effective management of stock (Munday,Turner and Jones, 2013). Apart from it price

optimisation system provides a framework for determining the prices. So this is why these

accounting systems have their importance.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Origin, role and principle of management accounting system:

Origin- The origin of management accounting system can be tracked during the time period of

revolution of industries in England (Parker and Northcott, 2016). As well as the conceptual

framework of this accounting system was evolved in 500 BC.

Principles- This accounting system includes mainly four types of principles like influence,

relevance, trust and value. All the principles have their importance for effective result of

management accounting.

Difference between financial and management accounting system:

Basis Management accounting system Financial accounting system

Importance The management accounting system

is useful for internal stakeholders.

On the other hand, this accounting

system is beneficial for external and

internal stakeholders.

Time period There is no specific time of

preparation of reports in this

accounting system.

Under this, financial statements are

prepared at the end of financial year.

Various kind of systems of management accounting: Cost accounting system- It is an accounting system is also known by costing system. In

general terms, this an accounting system which provides a framework for the purpose of

estimating the cost of products. As well as due to this accounting system companies can

calculate total cost of production and services. Eventually, it is useful for those

organisations which operates in the manufacturing sector. Such as the Stitchland Ltd

company, they implemented this accounting system and through this they are able to

manage and control their cost of manufacturing of cloths. So overall cost accounting

system is essential for predicting the cost and evaluating the profitability of various cost

of activities. Inventory management system- The inventory management system is an accounting

system that is associated with the tracking the goods in the supply chain or in

manufacturing process (Correa and Larrinaga, 2015). As well as it manages the quantity

Origin- The origin of management accounting system can be tracked during the time period of

revolution of industries in England (Parker and Northcott, 2016). As well as the conceptual

framework of this accounting system was evolved in 500 BC.

Principles- This accounting system includes mainly four types of principles like influence,

relevance, trust and value. All the principles have their importance for effective result of

management accounting.

Difference between financial and management accounting system:

Basis Management accounting system Financial accounting system

Importance The management accounting system

is useful for internal stakeholders.

On the other hand, this accounting

system is beneficial for external and

internal stakeholders.

Time period There is no specific time of

preparation of reports in this

accounting system.

Under this, financial statements are

prepared at the end of financial year.

Various kind of systems of management accounting: Cost accounting system- It is an accounting system is also known by costing system. In

general terms, this an accounting system which provides a framework for the purpose of

estimating the cost of products. As well as due to this accounting system companies can

calculate total cost of production and services. Eventually, it is useful for those

organisations which operates in the manufacturing sector. Such as the Stitchland Ltd

company, they implemented this accounting system and through this they are able to

manage and control their cost of manufacturing of cloths. So overall cost accounting

system is essential for predicting the cost and evaluating the profitability of various cost

of activities. Inventory management system- The inventory management system is an accounting

system that is associated with the tracking the goods in the supply chain or in

manufacturing process (Correa and Larrinaga, 2015). As well as it manages the quantity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

of raw material and finished goods so that companies can take suitable steps accordingly.

This is why because on the basis of it, companies make further decisions about

purchasing of raw material. Basically, it is essential for effective management of

inventories whether it is raw material or prepared products. The client company,

Stitchland Ltd of Bright-star financial consultancy applies this accounting system.

Eventually, this system is required to track the quantity of raw material such as woollen,

cotton etc. As well as they produce cloths in accordance to available stock which helps

them in satisfying the demand of customers. Price optimisation system- The price optimisation system is a type of accounting system

of management accounting that provides a basis for determining the price at an effective

level. It assigns the price by considering cost and required profit of the organisation along

with considering customers satisfaction. So this accounting system is essential for fixing

right price for products and services. Such as in the above mentioned respective

company, this management accounting system is required for the purpose of getting right

price of their cloths from the customers. As well as to evaluate the impact of customers

on different pricing levels.

Job costing system- The job costing system is an accounting system that assigns and

computes the job of cost of different activities individually (Nakajima, Kimura and

Wagner, 2015). Eventually, this accounting system is useful in those entities in which

there are lot of activities and jobs are assigned to each activity. Such as in the Stitchland

Ltd, accounting system is essential as they get the information about cost of jobs in their

manufacturing activities.

Advantage of management accounting systems:

Cost accounting system- This accounting system has its importance for calculating the

cost of various activities and operations. For Stitchland Ltd company, this accounting

system is useful in getting information about overall cost of manufacturing of cloths.

Inventory management system- It is beneficial in tracking the availability of stock in

warehouses. Such as in the above respective company they manage the stock of their

prepared cloths by this accounting system.

Price optimisation system- This accounting system is useful in determining the prices of

products of Stitchland Ltd company.

This is why because on the basis of it, companies make further decisions about

purchasing of raw material. Basically, it is essential for effective management of

inventories whether it is raw material or prepared products. The client company,

Stitchland Ltd of Bright-star financial consultancy applies this accounting system.

Eventually, this system is required to track the quantity of raw material such as woollen,

cotton etc. As well as they produce cloths in accordance to available stock which helps

them in satisfying the demand of customers. Price optimisation system- The price optimisation system is a type of accounting system

of management accounting that provides a basis for determining the price at an effective

level. It assigns the price by considering cost and required profit of the organisation along

with considering customers satisfaction. So this accounting system is essential for fixing

right price for products and services. Such as in the above mentioned respective

company, this management accounting system is required for the purpose of getting right

price of their cloths from the customers. As well as to evaluate the impact of customers

on different pricing levels.

Job costing system- The job costing system is an accounting system that assigns and

computes the job of cost of different activities individually (Nakajima, Kimura and

Wagner, 2015). Eventually, this accounting system is useful in those entities in which

there are lot of activities and jobs are assigned to each activity. Such as in the Stitchland

Ltd, accounting system is essential as they get the information about cost of jobs in their

manufacturing activities.

Advantage of management accounting systems:

Cost accounting system- This accounting system has its importance for calculating the

cost of various activities and operations. For Stitchland Ltd company, this accounting

system is useful in getting information about overall cost of manufacturing of cloths.

Inventory management system- It is beneficial in tracking the availability of stock in

warehouses. Such as in the above respective company they manage the stock of their

prepared cloths by this accounting system.

Price optimisation system- This accounting system is useful in determining the prices of

products of Stitchland Ltd company.

Job costing system- The job costing system is useful for providing information about cost

of job individually. As well as it is beneficial in getting information about the cost of job

of different activities assigned in manufacturing process of Stitchland Ltd company.

P2. Explanation of various kind of methods of management accounting reporting.

Features of effective information system:

Reliability- This is the main feature of an information system that information should be

reliable as per the activities of the organisation.

Accuracy- It is mandatory that information should be accurate so that internal reports of

management accounting can be prepared without any error (Antipova and Bourmistrov,

2013).

Up to date- As well as financial and non financial information should be up to date as per

the day to day transactions.

Importance of presenting the informations understandable: The presentation of information

should be understandable for the purpose of preparation of internal reports. Along with these

information provides framework for better decision-making.

Different types of management accounting reports:

Management accounting reports- These reports are important elements of the management

accounting system on which managers take internal decisions. As well as on these reports are

produced by help of financial and non financial transactions of the organisations. Like in the

Stitchland Ltd company, they prepare different kind of reports which are elaborated below:

Cost accounting reports- The cost accounting report is a type of report that includes

information about the total cost of different functions and operations. Like the above

respective company produce this report that helps them in maintaining the cost of their

manufacturing activities.

Account receivable ageing report- It is a report in that all the information is included

regarding to the collection from the debtors in the market (Collison, Ferguson and

Stevenson, 2014). As well as it consists time period also on which credit transaction

happened. For example in Stitchland Ltd company, they tracks the debtors in the market

whose payment is due.

of job individually. As well as it is beneficial in getting information about the cost of job

of different activities assigned in manufacturing process of Stitchland Ltd company.

P2. Explanation of various kind of methods of management accounting reporting.

Features of effective information system:

Reliability- This is the main feature of an information system that information should be

reliable as per the activities of the organisation.

Accuracy- It is mandatory that information should be accurate so that internal reports of

management accounting can be prepared without any error (Antipova and Bourmistrov,

2013).

Up to date- As well as financial and non financial information should be up to date as per

the day to day transactions.

Importance of presenting the informations understandable: The presentation of information

should be understandable for the purpose of preparation of internal reports. Along with these

information provides framework for better decision-making.

Different types of management accounting reports:

Management accounting reports- These reports are important elements of the management

accounting system on which managers take internal decisions. As well as on these reports are

produced by help of financial and non financial transactions of the organisations. Like in the

Stitchland Ltd company, they prepare different kind of reports which are elaborated below:

Cost accounting reports- The cost accounting report is a type of report that includes

information about the total cost of different functions and operations. Like the above

respective company produce this report that helps them in maintaining the cost of their

manufacturing activities.

Account receivable ageing report- It is a report in that all the information is included

regarding to the collection from the debtors in the market (Collison, Ferguson and

Stevenson, 2014). As well as it consists time period also on which credit transaction

happened. For example in Stitchland Ltd company, they tracks the debtors in the market

whose payment is due.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory management report- This is a type of report which provides information about

the quantity of stock available in the warehouses. In the Stitchland Ltd company, they

take important decisions about manufacturing of new products as per the information

provided by this report.

Performance report- It is a kind of report that contains information about the

performance of employees and various activities. Due to this companies can evaluate

each factor's performance separately. Such as in above respected company, they control

the performance effectively by help of this report.

TASK 2.

P3 Costing Techniques for preparing the financial statements.

Cost- The cost is an addition of all the expenditures that incurs in different kind of

activities and operations of organisations. It can be categorised into different types such as

direct , indirect, fixed and variable cost etc. Like in the Stitchland Ltd company, different kind of

costs occurs for example cost of material, labour etc.

Cost analysis is a process of computing total cost of various activities so that each

activity's cost can be evaluated.

Cost volume profit analysis- This is a type of analysing technique that is associated with

the analysing the difference in the cost and profits. The basic objective of this type of analysis is

to measure the financial condition of the companies as per the variation in cost and volume. In

the above respective company, they evaluate the difference in cost and volume by this analysis.

Flexible budgeting- It is a kind of budgeting technique in which values of budgets can be

change in relation to change sales and volume (Hoque, 2018). Like in the Stitchland Ltd

company, they apply this budgeting method so that they can change in relation to change in sales

of cloths.

Cost variance- The cost variance can be defined as a variation in the estimated cost and

actual cost. Such as in above mentioned company they analyse the variance between their actual

cost of manufacturing and estimated cost.

Absorption & marginal costing:

the quantity of stock available in the warehouses. In the Stitchland Ltd company, they

take important decisions about manufacturing of new products as per the information

provided by this report.

Performance report- It is a kind of report that contains information about the

performance of employees and various activities. Due to this companies can evaluate

each factor's performance separately. Such as in above respected company, they control

the performance effectively by help of this report.

TASK 2.

P3 Costing Techniques for preparing the financial statements.

Cost- The cost is an addition of all the expenditures that incurs in different kind of

activities and operations of organisations. It can be categorised into different types such as

direct , indirect, fixed and variable cost etc. Like in the Stitchland Ltd company, different kind of

costs occurs for example cost of material, labour etc.

Cost analysis is a process of computing total cost of various activities so that each

activity's cost can be evaluated.

Cost volume profit analysis- This is a type of analysing technique that is associated with

the analysing the difference in the cost and profits. The basic objective of this type of analysis is

to measure the financial condition of the companies as per the variation in cost and volume. In

the above respective company, they evaluate the difference in cost and volume by this analysis.

Flexible budgeting- It is a kind of budgeting technique in which values of budgets can be

change in relation to change sales and volume (Hoque, 2018). Like in the Stitchland Ltd

company, they apply this budgeting method so that they can change in relation to change in sales

of cloths.

Cost variance- The cost variance can be defined as a variation in the estimated cost and

actual cost. Such as in above mentioned company they analyse the variance between their actual

cost of manufacturing and estimated cost.

Absorption & marginal costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Absorption costing- The absorption costing is a type of costing technique under which

fixed and variable costing are taken as the cost of product.

Marginal costing- This costing technique is different from the absorption costing

technique. Under this, variable cost is taken as the unit cost while fixed cost as period cost.

Cost allocation- The cost allocation may be defined as a process of allocating the

overheads as per the activities. Such as the respective company, they assign the expenditures as

per the different activities of manufacturing.

Fixed cost- This is a type of cost which is not based on the level of output (Gooneratne,

and Hoque, 2013). In other words, it is a kind of cost which do not varies as per change in the

quantity of production or sales. Rent, telephone charges etc. are common example of the fixed

cost.

Variable cost- It is a kind of cost that can be change as per the variation in quantity of

production and sales. So overall this cost has different nature from the fixed cost. Some example

of this cost is variable overhead, material cost.

Normal costing- The normal costing is a type of cost that includes cost of any product

including cost of labour, material etc.

Standard costing- The standard costing is a cost which is predicted for future time period

for various kind of activities. As well as it acts as basis for comparing actual performance. Such

as in Stitchland Ltd company, they use this costing for measuring the actual cost.

Activity based costing- The activity based costing is a type of costing system in that cost

is allocated to various activities individually.

Inventory cost- As the name assists, this a kind of cost which includes cost of ordering,

cost of storing and carrying etc. In the above respective company, they calculate the cost of

inventory so that they can manage the cost.

Valuation methods:

LIFO- The LIFO is a type of method in which those raw materials are use that came in

last but being used first (Saleem Salem Alzoubi, 2016). For example in Stitchland Ltd company,

they use the raw materials which brought last.

FIFO- This method is opposite of above mentioned method. In this stock which brought

first is being used first.

fixed and variable costing are taken as the cost of product.

Marginal costing- This costing technique is different from the absorption costing

technique. Under this, variable cost is taken as the unit cost while fixed cost as period cost.

Cost allocation- The cost allocation may be defined as a process of allocating the

overheads as per the activities. Such as the respective company, they assign the expenditures as

per the different activities of manufacturing.

Fixed cost- This is a type of cost which is not based on the level of output (Gooneratne,

and Hoque, 2013). In other words, it is a kind of cost which do not varies as per change in the

quantity of production or sales. Rent, telephone charges etc. are common example of the fixed

cost.

Variable cost- It is a kind of cost that can be change as per the variation in quantity of

production and sales. So overall this cost has different nature from the fixed cost. Some example

of this cost is variable overhead, material cost.

Normal costing- The normal costing is a type of cost that includes cost of any product

including cost of labour, material etc.

Standard costing- The standard costing is a cost which is predicted for future time period

for various kind of activities. As well as it acts as basis for comparing actual performance. Such

as in Stitchland Ltd company, they use this costing for measuring the actual cost.

Activity based costing- The activity based costing is a type of costing system in that cost

is allocated to various activities individually.

Inventory cost- As the name assists, this a kind of cost which includes cost of ordering,

cost of storing and carrying etc. In the above respective company, they calculate the cost of

inventory so that they can manage the cost.

Valuation methods:

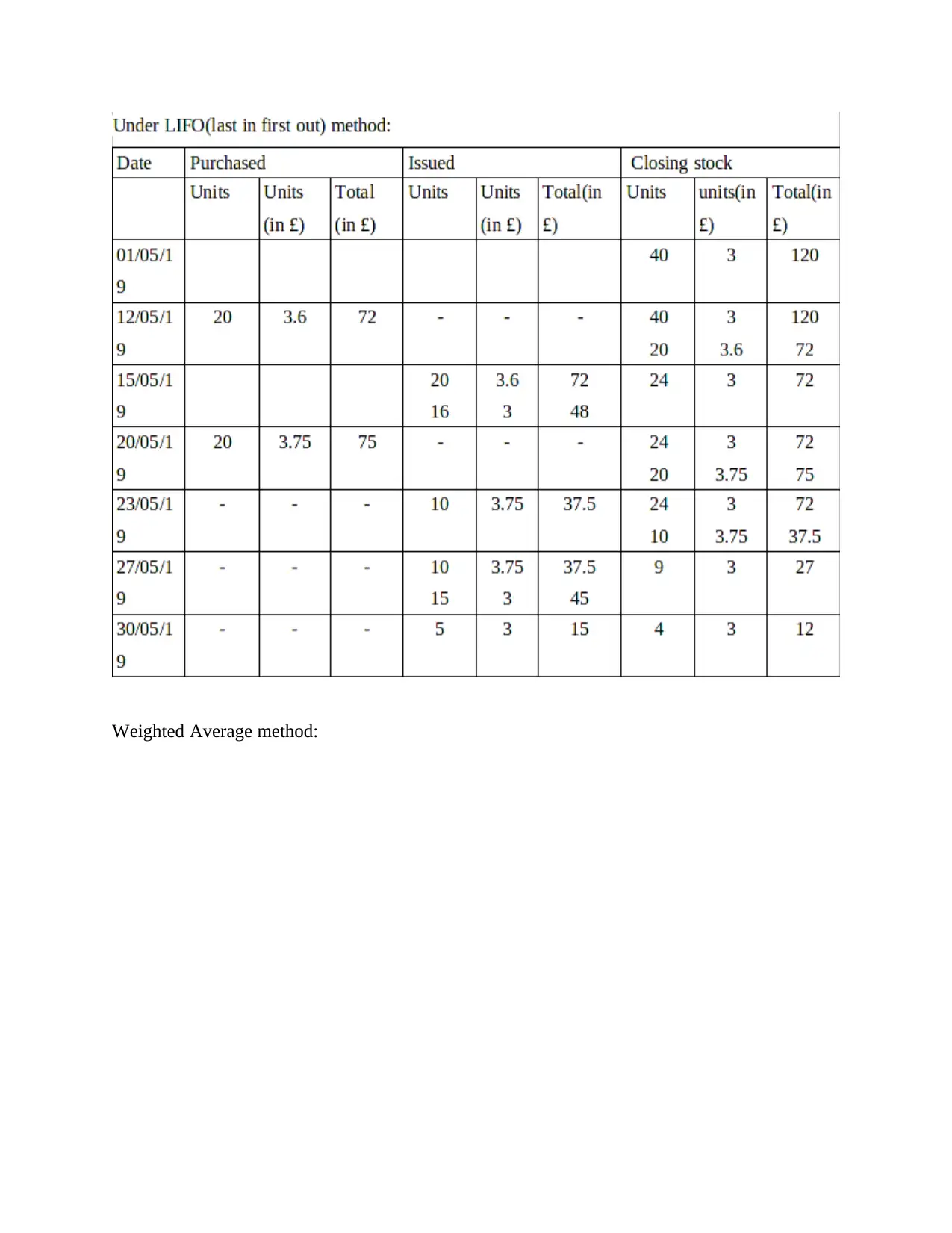

LIFO- The LIFO is a type of method in which those raw materials are use that came in

last but being used first (Saleem Salem Alzoubi, 2016). For example in Stitchland Ltd company,

they use the raw materials which brought last.

FIFO- This method is opposite of above mentioned method. In this stock which brought

first is being used first.

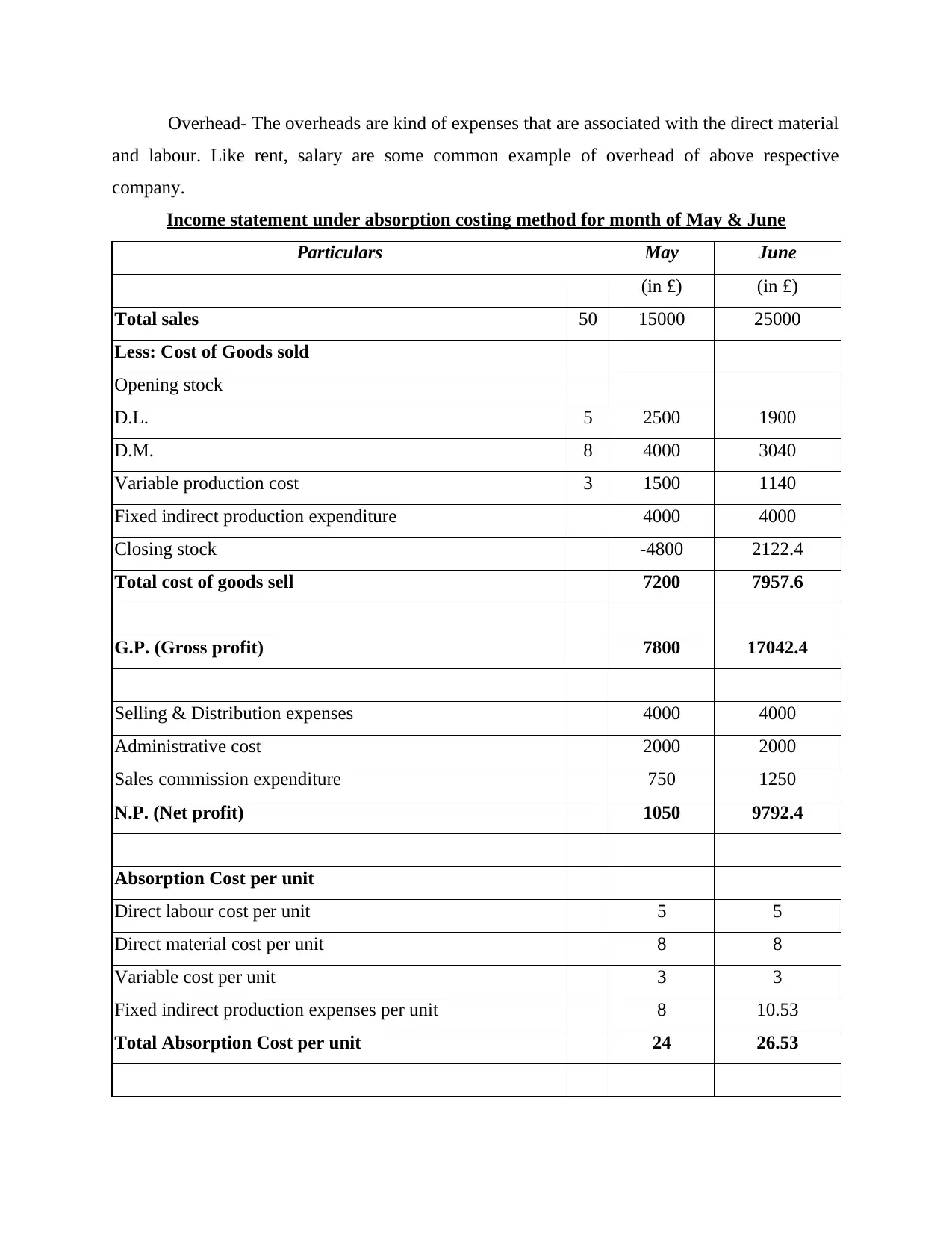

Overhead- The overheads are kind of expenses that are associated with the direct material

and labour. Like rent, salary are some common example of overhead of above respective

company.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

and labour. Like rent, salary are some common example of overhead of above respective

company.

Income statement under absorption costing method for month of May & June

Particulars May June

(in £) (in £)

Total sales 50 15000 25000

Less: Cost of Goods sold

Opening stock

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable production cost 3 1500 1140

Fixed indirect production expenditure 4000 4000

Closing stock -4800 2122.4

Total cost of goods sell 7200 7957.6

G.P. (Gross profit) 7800 17042.4

Selling & Distribution expenses 4000 4000

Administrative cost 2000 2000

Sales commission expenditure 750 1250

N.P. (Net profit) 1050 9792.4

Absorption Cost per unit

Direct labour cost per unit 5 5

Direct material cost per unit 8 8

Variable cost per unit 3 3

Fixed indirect production expenses per unit 8 10.53

Total Absorption Cost per unit 24 26.53

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

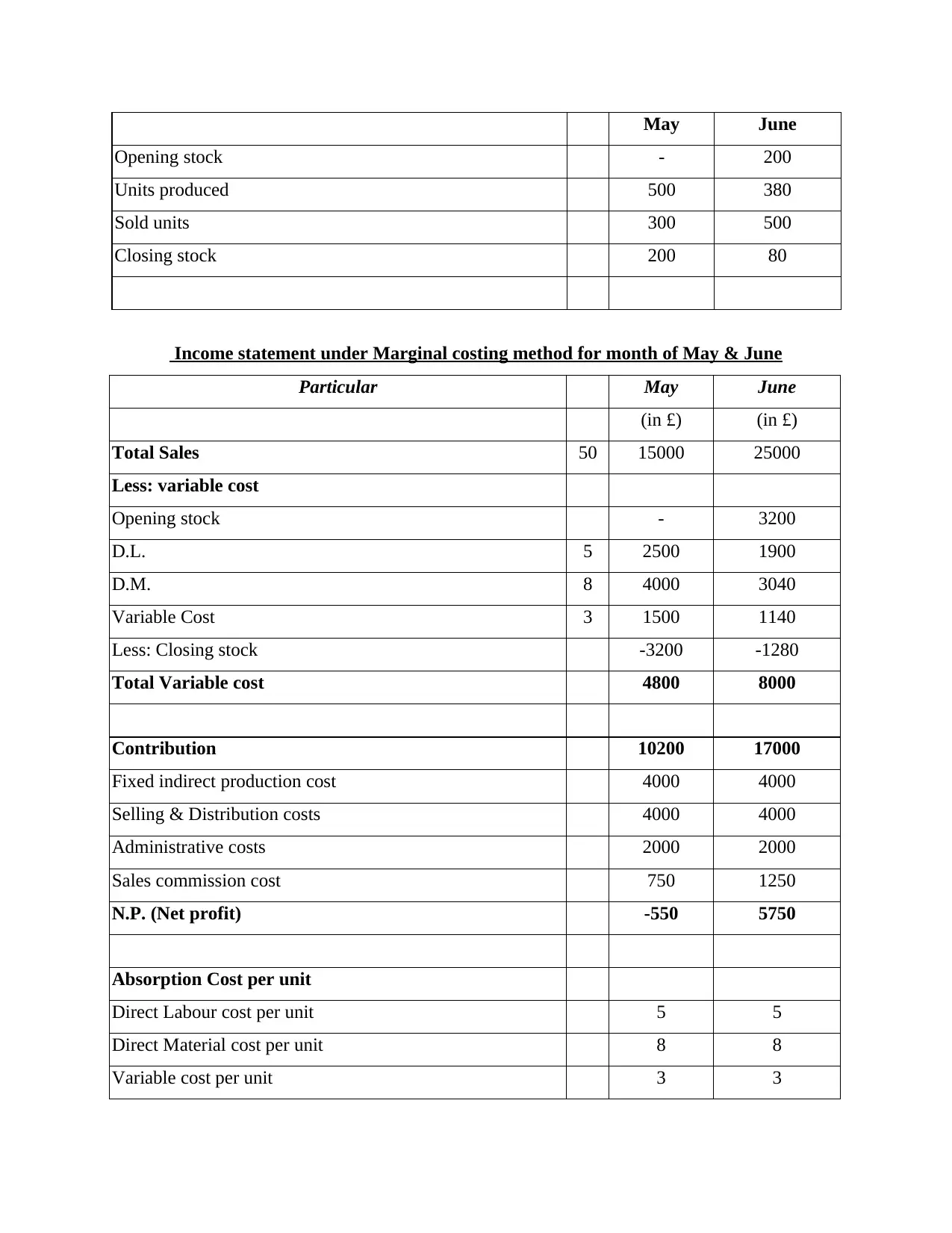

May June

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Opening stock - 200

Units produced 500 380

Sold units 300 500

Closing stock 200 80

Income statement under Marginal costing method for month of May & June

Particular May June

(in £) (in £)

Total Sales 50 15000 25000

Less: variable cost

Opening stock - 3200

D.L. 5 2500 1900

D.M. 8 4000 3040

Variable Cost 3 1500 1140

Less: Closing stock -3200 -1280

Total Variable cost 4800 8000

Contribution 10200 17000

Fixed indirect production cost 4000 4000

Selling & Distribution costs 4000 4000

Administrative costs 2000 2000

Sales commission cost 750 1250

N.P. (Net profit) -550 5750

Absorption Cost per unit

Direct Labour cost per unit 5 5

Direct Material cost per unit 8 8

Variable cost per unit 3 3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

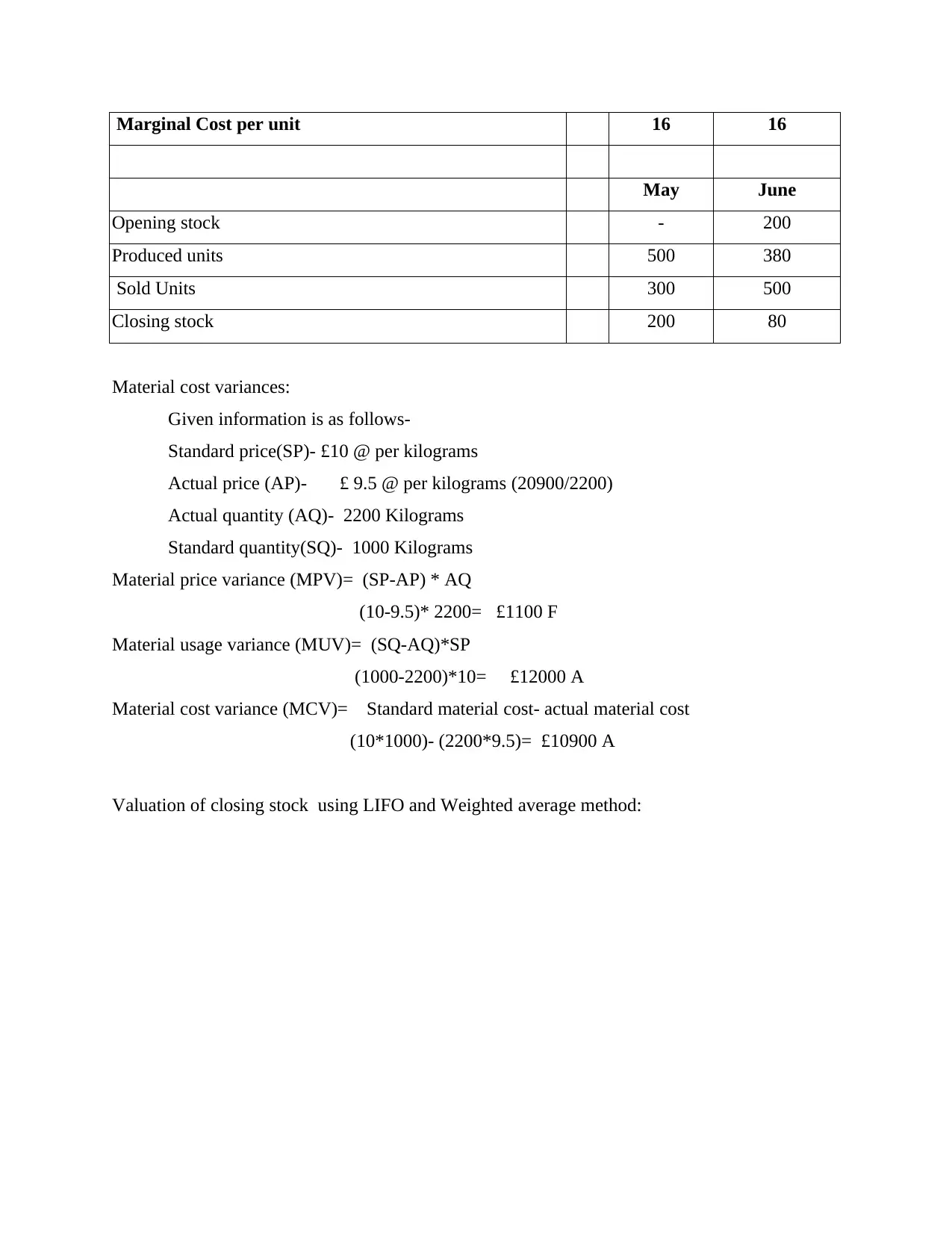

Marginal Cost per unit 16 16

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

(10*1000)- (2200*9.5)= £10900 A

Valuation of closing stock using LIFO and Weighted average method:

May June

Opening stock - 200

Produced units 500 380

Sold Units 300 500

Closing stock 200 80

Material cost variances:

Given information is as follows-

Standard price(SP)- £10 @ per kilograms

Actual price (AP)- £ 9.5 @ per kilograms (20900/2200)

Actual quantity (AQ)- 2200 Kilograms

Standard quantity(SQ)- 1000 Kilograms

Material price variance (MPV)= (SP-AP) * AQ

(10-9.5)* 2200= £1100 F

Material usage variance (MUV)= (SQ-AQ)*SP

(1000-2200)*10= £12000 A

Material cost variance (MCV)= Standard material cost- actual material cost

(10*1000)- (2200*9.5)= £10900 A

Valuation of closing stock using LIFO and Weighted average method:

Weighted Average method:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.