Management Accounting Report: Methods, Benefits and Analysis

VerifiedAdded on 2021/02/21

|18

|4450

|51

Report

AI Summary

This report delves into the realm of management accounting, analyzing its core concepts and practical applications within the context of Hewland Engineering Limited. It begins by defining management accounting and its system, highlighting various types such as price optimization, inventory management, job costing, and cost accounting systems. The report then explores different management accounting reporting methods, including budget reports, performance reports, and inventory management reports, alongside their benefits. Furthermore, it evaluates the integration of management accounting systems and reporting within organizational structures. The report also covers the preparation of income statements using both absorption and marginal costing techniques, providing detailed calculations and working notes. Finally, it examines the application of management accounting techniques, such as activity-based costing, and discusses the benefits and weaknesses of various planning tools in budgetary control, offering a comprehensive overview of management accounting practices and their impact on business operations.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION

In past (around 150-200 years back), private organisations experience the need of an

internal accounting system to supervises and control the internal environment of a business

organisation in order to ensure their existence in the market. For this, a practice which is evolved

commonly known as managerial accounting. Such accounting technique provides information to

the managers so that they can be assisted in making decisions and planning for achievement of

organizational goals.

For better understanding of management accounting, a famous engineering company

Hewland Engineering Limited has been selected in this report. The company is founded in

1957 by Mike Hewland in Maidenhead, England and conducts its business in automotive sector

specialises in racing-car gearboxes.

This report covers definition and various aspects of MAS, knowledge of MA reporting,

budgetary tools as well as such system helps the company in solving various financial problems

within its working environment and assist in answering to such issues. This report provides the

various methods that may help in estimating and analysing future business conditions in

organizational context.

ACTIVITY 1

P1. Management Accounting System and its various kind:

Management Accounting: It may be defined as collection, documentation, abstracting,

evaluating and supervising the data to assist the management (for maintain sustainability in

functioning of the entity to attain its target. Management accounting may be defined as technique

which is utilised by the management of an entity to be able to take effect of its internal

operations and functions. The essential task that a management accountant of an entity has to

accomplish are planning, organizing and supervising activities of the firm (Serena Chiucchi,

2013).

Management Accounting System: MAS may be defined as approach that includes

creation of several documents and estimations of company's future requirements for assisting the

managers. With help of MAS, Hewland Engineering limited can prepare its income statements at

each year end. An entity may utilise distinct kinds of MAS that are as follows:

In past (around 150-200 years back), private organisations experience the need of an

internal accounting system to supervises and control the internal environment of a business

organisation in order to ensure their existence in the market. For this, a practice which is evolved

commonly known as managerial accounting. Such accounting technique provides information to

the managers so that they can be assisted in making decisions and planning for achievement of

organizational goals.

For better understanding of management accounting, a famous engineering company

Hewland Engineering Limited has been selected in this report. The company is founded in

1957 by Mike Hewland in Maidenhead, England and conducts its business in automotive sector

specialises in racing-car gearboxes.

This report covers definition and various aspects of MAS, knowledge of MA reporting,

budgetary tools as well as such system helps the company in solving various financial problems

within its working environment and assist in answering to such issues. This report provides the

various methods that may help in estimating and analysing future business conditions in

organizational context.

ACTIVITY 1

P1. Management Accounting System and its various kind:

Management Accounting: It may be defined as collection, documentation, abstracting,

evaluating and supervising the data to assist the management (for maintain sustainability in

functioning of the entity to attain its target. Management accounting may be defined as technique

which is utilised by the management of an entity to be able to take effect of its internal

operations and functions. The essential task that a management accountant of an entity has to

accomplish are planning, organizing and supervising activities of the firm (Serena Chiucchi,

2013).

Management Accounting System: MAS may be defined as approach that includes

creation of several documents and estimations of company's future requirements for assisting the

managers. With help of MAS, Hewland Engineering limited can prepare its income statements at

each year end. An entity may utilise distinct kinds of MAS that are as follows:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Price Optimisation System: It is a technique that assist in understanding that how the

potential consumer will behave on several quotations for a specific commodity. Price

optimisation system helps in choosing best price which is satisfactory on both behalf (i.e.

company and customers). Respective organization utilises such technique to fix amounts of

several products in market as per several circumstances for its potential consumers.

Inventory Management System: This type is evolved to maintain and manage the most

essential source of organizational income viz. the inventory or stock of products. It keeps record

of raw material, WIP, finished goods dispatched for delivery, sales return and goods on

consignment, etc. The management of respective enterprise may be capable in selecting

appropriate method for inventory valuation, these are as below:

LIFO: In such valuation method, closing stock are valued based on price of last inventory

purchased.

FIFO: In technique, inventory is valued on the basis rate of first inventory purchased. Weighted average method: In this method, company divides the total cost of goods

available for sale with number of quantity available.

Job Costing System: Such type of MAS is used by an enterprise for a specific job in

calculating the cost of such particular job by adding all the costs such as materials, labour and

overheads (Lindholm, Laine and Suomala, 2017). In other words, it may be said that Job costing

system act as a tool in an organisation for tracing costs related to individual’s jobs and evaluate

the performance of such job to reduce the costs of all future jobs. For example, an enterprise may

produce custom made machines as job A and It may construct custom-designed buildings as job

B.

Cost Accounting System: It is a type of MAS that helps a manufacturer to find and

measure several costs in manufacturing process. Cost accounting system helps the company in

estimating the correct cost of its products because it is very essential to control the cost for better

profitability. The management of Hewland Engineering Limited utilises such type of MAS for

estimating the expenses of its products and calculate the profit of the organization. A company

by implementing such can reduce its costs related to manufacturing process that may be used for

improving its several business operations (Stechemesser and Guenther, 2012).

potential consumer will behave on several quotations for a specific commodity. Price

optimisation system helps in choosing best price which is satisfactory on both behalf (i.e.

company and customers). Respective organization utilises such technique to fix amounts of

several products in market as per several circumstances for its potential consumers.

Inventory Management System: This type is evolved to maintain and manage the most

essential source of organizational income viz. the inventory or stock of products. It keeps record

of raw material, WIP, finished goods dispatched for delivery, sales return and goods on

consignment, etc. The management of respective enterprise may be capable in selecting

appropriate method for inventory valuation, these are as below:

LIFO: In such valuation method, closing stock are valued based on price of last inventory

purchased.

FIFO: In technique, inventory is valued on the basis rate of first inventory purchased. Weighted average method: In this method, company divides the total cost of goods

available for sale with number of quantity available.

Job Costing System: Such type of MAS is used by an enterprise for a specific job in

calculating the cost of such particular job by adding all the costs such as materials, labour and

overheads (Lindholm, Laine and Suomala, 2017). In other words, it may be said that Job costing

system act as a tool in an organisation for tracing costs related to individual’s jobs and evaluate

the performance of such job to reduce the costs of all future jobs. For example, an enterprise may

produce custom made machines as job A and It may construct custom-designed buildings as job

B.

Cost Accounting System: It is a type of MAS that helps a manufacturer to find and

measure several costs in manufacturing process. Cost accounting system helps the company in

estimating the correct cost of its products because it is very essential to control the cost for better

profitability. The management of Hewland Engineering Limited utilises such type of MAS for

estimating the expenses of its products and calculate the profit of the organization. A company

by implementing such can reduce its costs related to manufacturing process that may be used for

improving its several business operations (Stechemesser and Guenther, 2012).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2. Different method used for Management Accounting Reporting:

Management Accounting Reporting: It covers evaluation, analysis and verdict

preparing technique with benefit of data furnished by the management and statements. This

process gives a opinion of operational structure to the executive managers to implement several

plans. The main function of these reports is to calculate variance between real and estimated

budgets or outcomes. In business environment, several reports utilised by staff of Hewland

Engineering limited to develop management reporting system. Few are as follows:

Budget Reports: It consists information regarding several business activities of an

organisation and accordingly preparation of various budgets for different activities of various

department. It helps the company in comparing its actual results of business activities with such

budgeted report and assist in improving its efficiency and effectiveness. This report contains

routine income and revenues information, rigid and elastic costs, net worth of the organisation,

including assets and liabilities. The executive managers of chosen entity are capable to measure

adverse or favourable variances (deviations) with help of such report and determine the action to

be taken according to each circumstances. Budget report provides way the board to minimise

expenses. It also assists in moderating or updating standards in budgets, if required.

Performance Reports: This report provides about the performances of its various

business activities along with its working staff to the board of directors. With the help of such

report, an entity's executive managers may assess the weaknesses and strengths of its current

business activities and accordingly it makes take sufficient and appropriate actions within the

internal environment of an entity. This may in various types according to the need of the

organisation such as progress report, forecasting report, trend report and so on.

Accounts Receivable Reports: Such report assists the company in providing information

related to its account receivable (debtors) that are very useful for evaluating the performances of

its debtors. It provides the details that how many amount is pending from the debtors after the

due date and also provides details about amount of interest which a company shall require to

recovered from the it accounts receivable due to delayed payments (McVay, Kennedy and

Fullerton, 2016). Such report provides the details about unpaid debtors list along with utilised

cash memos and it may be defined as collection tool for management personnel.

Inventory Management Report: For further move, process of inventory management

system, this report is prepared. Information and estimations delivered by the system provides a

Management Accounting Reporting: It covers evaluation, analysis and verdict

preparing technique with benefit of data furnished by the management and statements. This

process gives a opinion of operational structure to the executive managers to implement several

plans. The main function of these reports is to calculate variance between real and estimated

budgets or outcomes. In business environment, several reports utilised by staff of Hewland

Engineering limited to develop management reporting system. Few are as follows:

Budget Reports: It consists information regarding several business activities of an

organisation and accordingly preparation of various budgets for different activities of various

department. It helps the company in comparing its actual results of business activities with such

budgeted report and assist in improving its efficiency and effectiveness. This report contains

routine income and revenues information, rigid and elastic costs, net worth of the organisation,

including assets and liabilities. The executive managers of chosen entity are capable to measure

adverse or favourable variances (deviations) with help of such report and determine the action to

be taken according to each circumstances. Budget report provides way the board to minimise

expenses. It also assists in moderating or updating standards in budgets, if required.

Performance Reports: This report provides about the performances of its various

business activities along with its working staff to the board of directors. With the help of such

report, an entity's executive managers may assess the weaknesses and strengths of its current

business activities and accordingly it makes take sufficient and appropriate actions within the

internal environment of an entity. This may in various types according to the need of the

organisation such as progress report, forecasting report, trend report and so on.

Accounts Receivable Reports: Such report assists the company in providing information

related to its account receivable (debtors) that are very useful for evaluating the performances of

its debtors. It provides the details that how many amount is pending from the debtors after the

due date and also provides details about amount of interest which a company shall require to

recovered from the it accounts receivable due to delayed payments (McVay, Kennedy and

Fullerton, 2016). Such report provides the details about unpaid debtors list along with utilised

cash memos and it may be defined as collection tool for management personnel.

Inventory Management Report: For further move, process of inventory management

system, this report is prepared. Information and estimations delivered by the system provides a

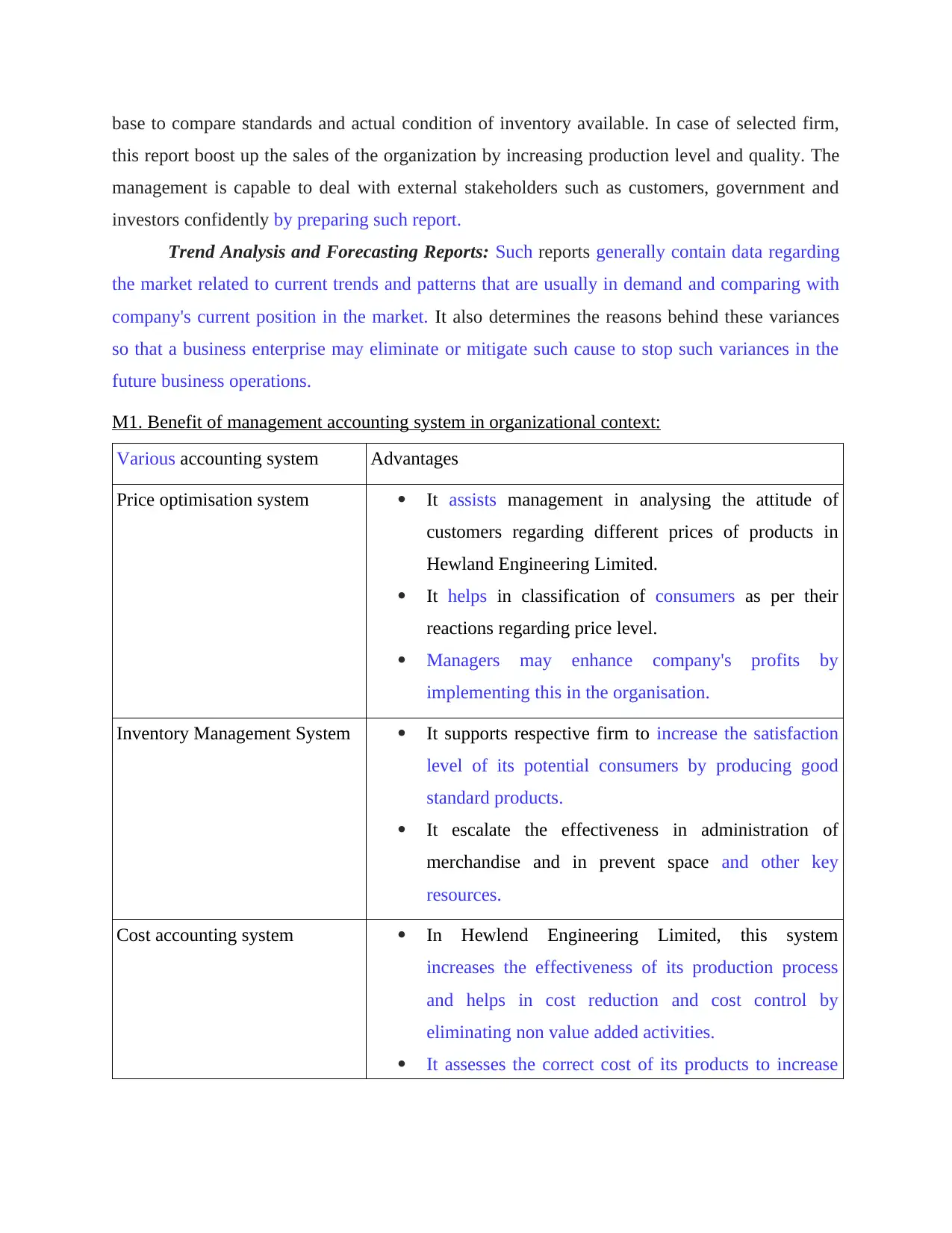

base to compare standards and actual condition of inventory available. In case of selected firm,

this report boost up the sales of the organization by increasing production level and quality. The

management is capable to deal with external stakeholders such as customers, government and

investors confidently by preparing such report.

Trend Analysis and Forecasting Reports: Such reports generally contain data regarding

the market related to current trends and patterns that are usually in demand and comparing with

company's current position in the market. It also determines the reasons behind these variances

so that a business enterprise may eliminate or mitigate such cause to stop such variances in the

future business operations.

M1. Benefit of management accounting system in organizational context:

Various accounting system Advantages

Price optimisation system It assists management in analysing the attitude of

customers regarding different prices of products in

Hewland Engineering Limited.

It helps in classification of consumers as per their

reactions regarding price level.

Managers may enhance company's profits by

implementing this in the organisation.

Inventory Management System It supports respective firm to increase the satisfaction

level of its potential consumers by producing good

standard products.

It escalate the effectiveness in administration of

merchandise and in prevent space and other key

resources.

Cost accounting system In Hewlend Engineering Limited, this system

increases the effectiveness of its production process

and helps in cost reduction and cost control by

eliminating non value added activities.

It assesses the correct cost of its products to increase

this report boost up the sales of the organization by increasing production level and quality. The

management is capable to deal with external stakeholders such as customers, government and

investors confidently by preparing such report.

Trend Analysis and Forecasting Reports: Such reports generally contain data regarding

the market related to current trends and patterns that are usually in demand and comparing with

company's current position in the market. It also determines the reasons behind these variances

so that a business enterprise may eliminate or mitigate such cause to stop such variances in the

future business operations.

M1. Benefit of management accounting system in organizational context:

Various accounting system Advantages

Price optimisation system It assists management in analysing the attitude of

customers regarding different prices of products in

Hewland Engineering Limited.

It helps in classification of consumers as per their

reactions regarding price level.

Managers may enhance company's profits by

implementing this in the organisation.

Inventory Management System It supports respective firm to increase the satisfaction

level of its potential consumers by producing good

standard products.

It escalate the effectiveness in administration of

merchandise and in prevent space and other key

resources.

Cost accounting system In Hewlend Engineering Limited, this system

increases the effectiveness of its production process

and helps in cost reduction and cost control by

eliminating non value added activities.

It assesses the correct cost of its products to increase

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the profitability of company.

Job Costing System It helps Hewlend Engineering Limited to estimate

correct cost related to particular job.

Job costing system provides company the benefits of

being capable to maintain path of individuals' and

teams' execution power and reward them accordingly

(Schaltegger, 2012).

D1. Evaluation of management accounting systems and management accounting reporting

integration inside organisational systems:

In the absence of MAS, administrative records are useless papers. By utilizing these

records, company has not able to create successful structure with the goal that these may be

utilized for the success of company. MA reporting gives assistance in breaking down execution

of various factors and discover error and create essential framework. Such framework helps in

establishing in accomplishing high execution and increase the profits of company (Schaltegger,

2012).

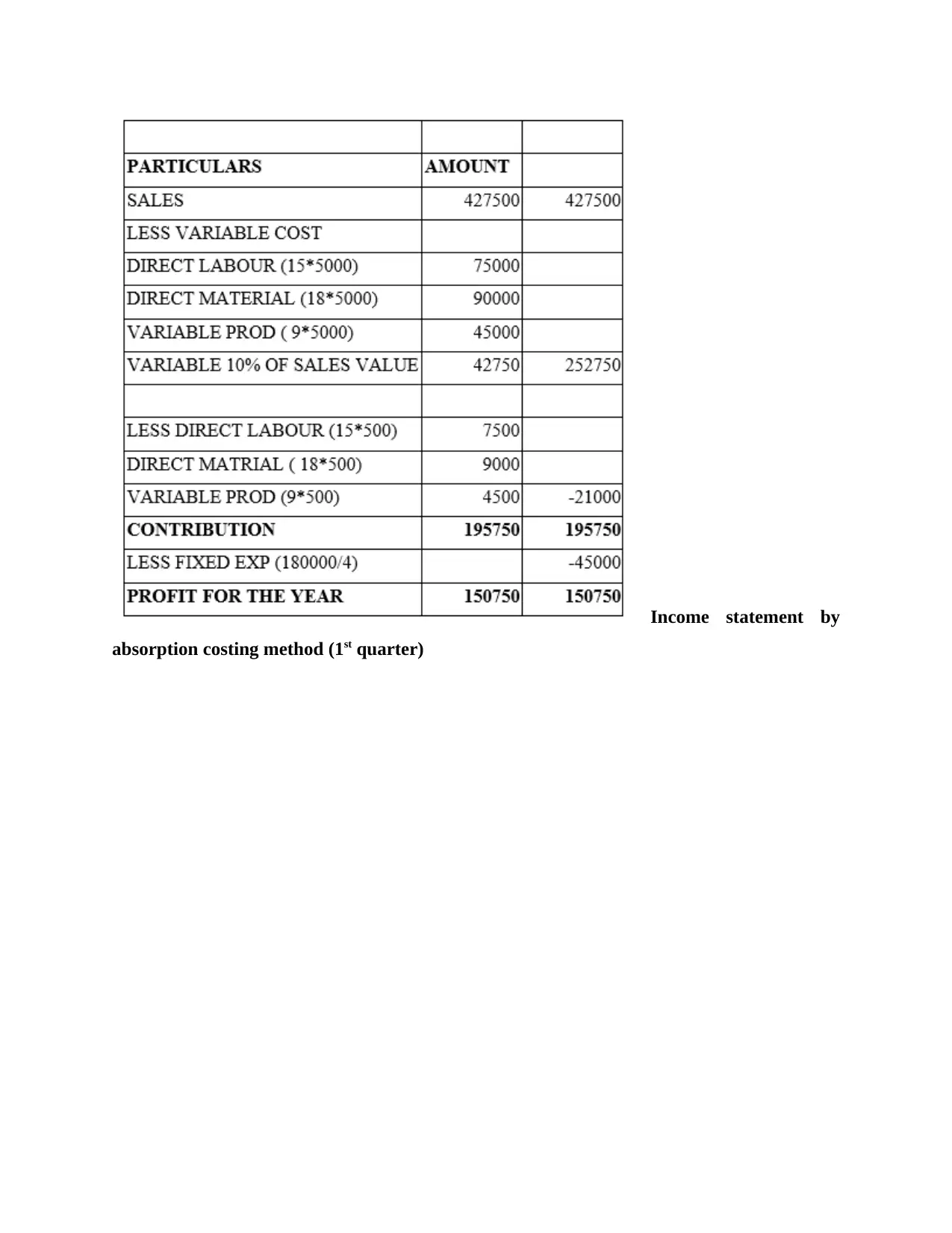

P3. Preparation of income statements using absorption and marginal techniques:

A business organisation may have prepared its income statements by two methods given

as under:

Absorption costing: In this technique of management accounting system, all the cost

which a company incurred is considered whether it is relevant cost or irrelevant cost. In

absorption costing, fixed cost and historical cost is also considered (Flamholtz, 2012).

Marginal costing: This is method in which only relevant cost which is responsible for

manufacturing the particular product is considered. In marginal costing, fixed cost is considered

for amount which is remain after reducing variable cost from sales.

Income statement by marginal costing techniques:

Job Costing System It helps Hewlend Engineering Limited to estimate

correct cost related to particular job.

Job costing system provides company the benefits of

being capable to maintain path of individuals' and

teams' execution power and reward them accordingly

(Schaltegger, 2012).

D1. Evaluation of management accounting systems and management accounting reporting

integration inside organisational systems:

In the absence of MAS, administrative records are useless papers. By utilizing these

records, company has not able to create successful structure with the goal that these may be

utilized for the success of company. MA reporting gives assistance in breaking down execution

of various factors and discover error and create essential framework. Such framework helps in

establishing in accomplishing high execution and increase the profits of company (Schaltegger,

2012).

P3. Preparation of income statements using absorption and marginal techniques:

A business organisation may have prepared its income statements by two methods given

as under:

Absorption costing: In this technique of management accounting system, all the cost

which a company incurred is considered whether it is relevant cost or irrelevant cost. In

absorption costing, fixed cost and historical cost is also considered (Flamholtz, 2012).

Marginal costing: This is method in which only relevant cost which is responsible for

manufacturing the particular product is considered. In marginal costing, fixed cost is considered

for amount which is remain after reducing variable cost from sales.

Income statement by marginal costing techniques:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Income statement by

absorption costing method (1st quarter)

absorption costing method (1st quarter)

Working note:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

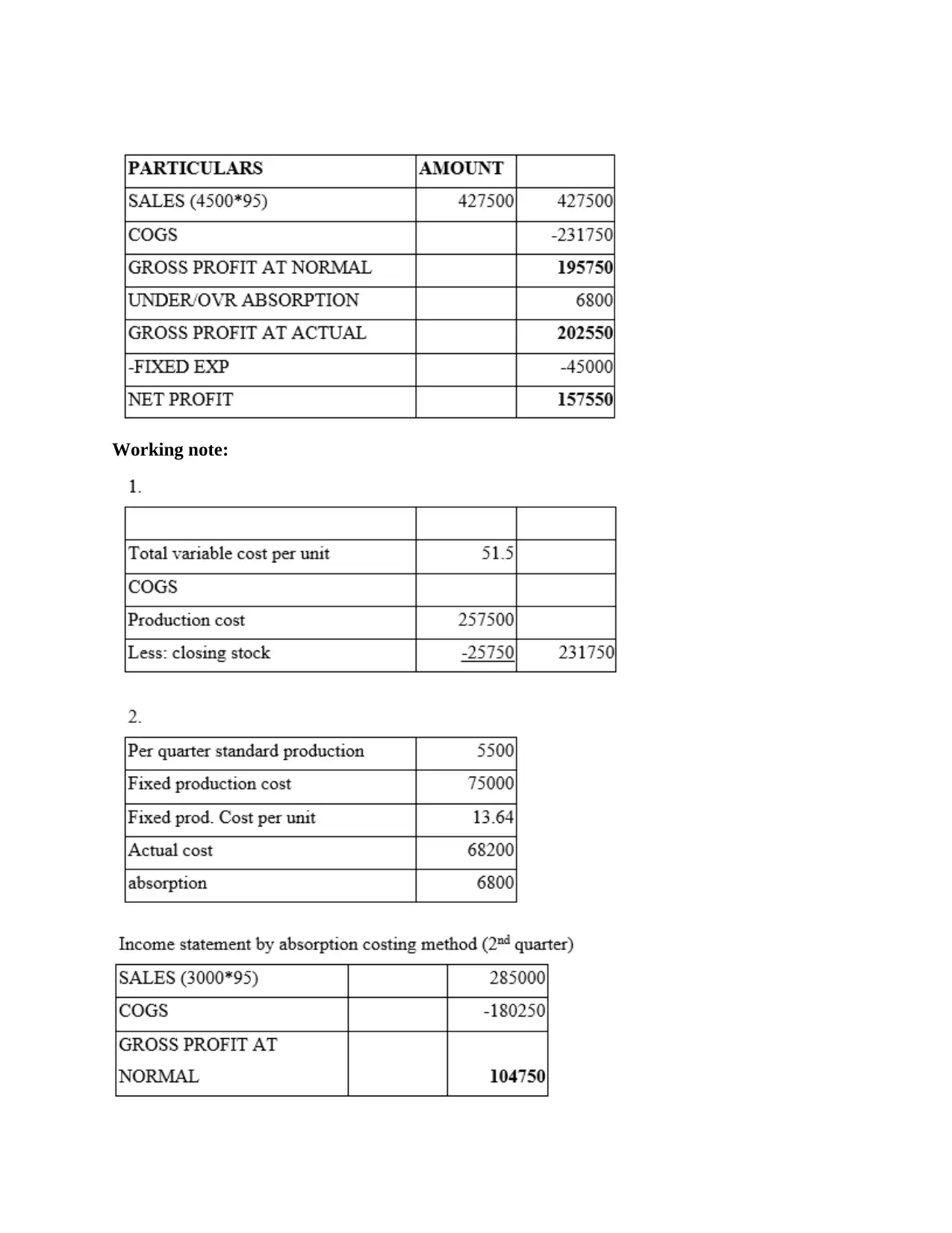

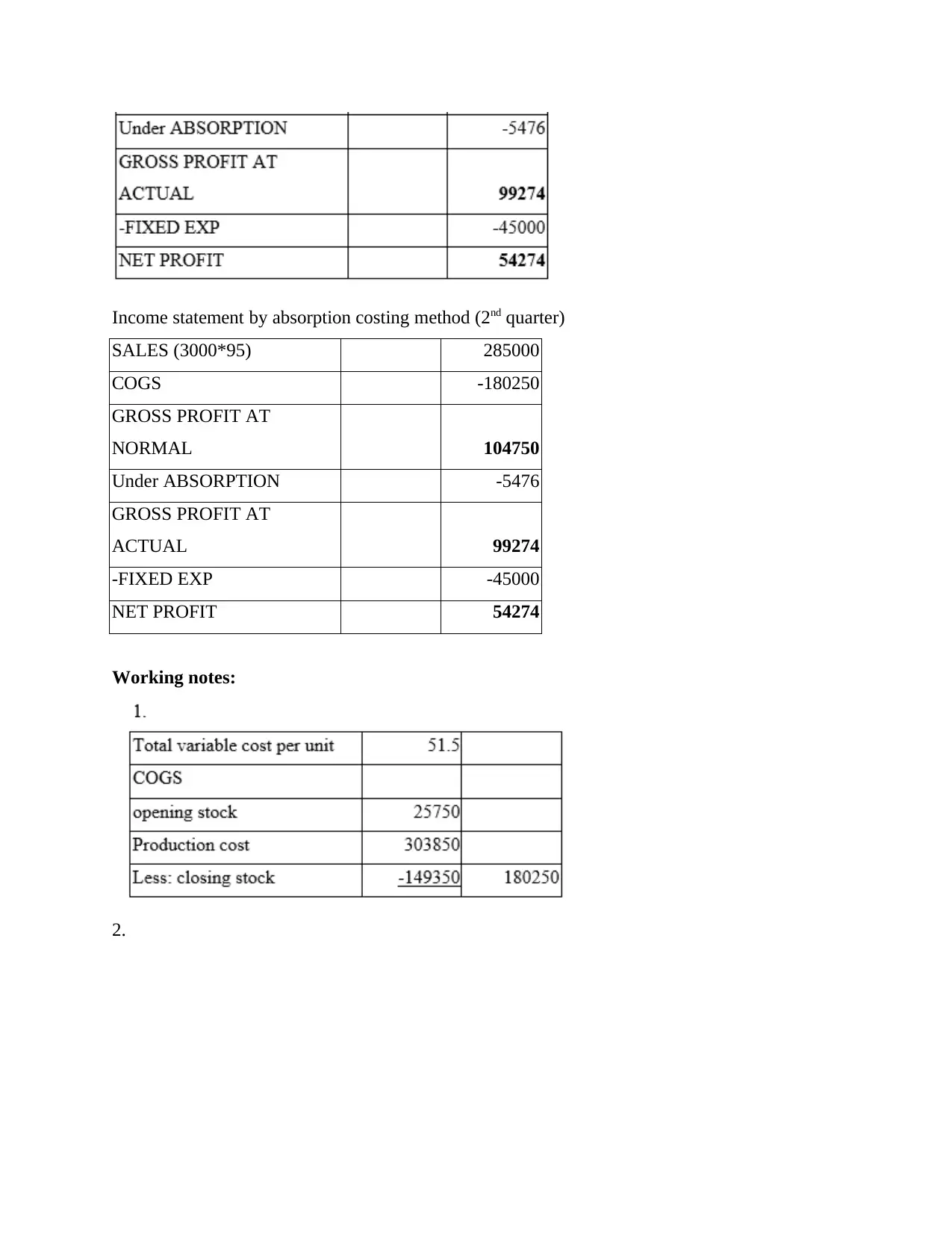

Income statement by absorption costing method (2nd quarter)

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

2.

SALES (3000*95) 285000

COGS -180250

GROSS PROFIT AT

NORMAL 104750

Under ABSORPTION -5476

GROSS PROFIT AT

ACTUAL 99274

-FIXED EXP -45000

NET PROFIT 54274

Working notes:

2.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

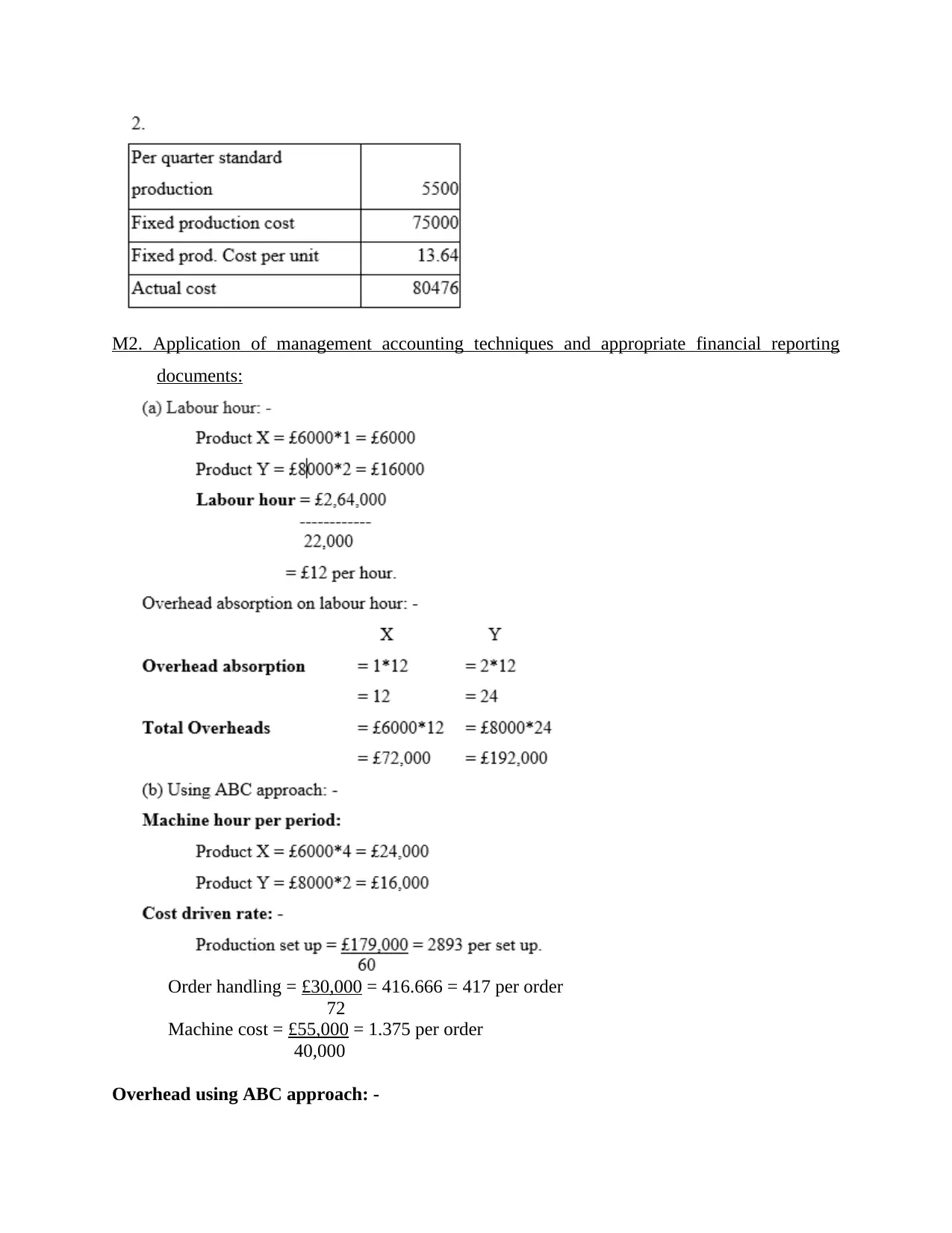

M2. Application of management accounting techniques and appropriate financial reporting

documents:

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

documents:

Order handling = £30,000 = 416.666 = 417 per order

72

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

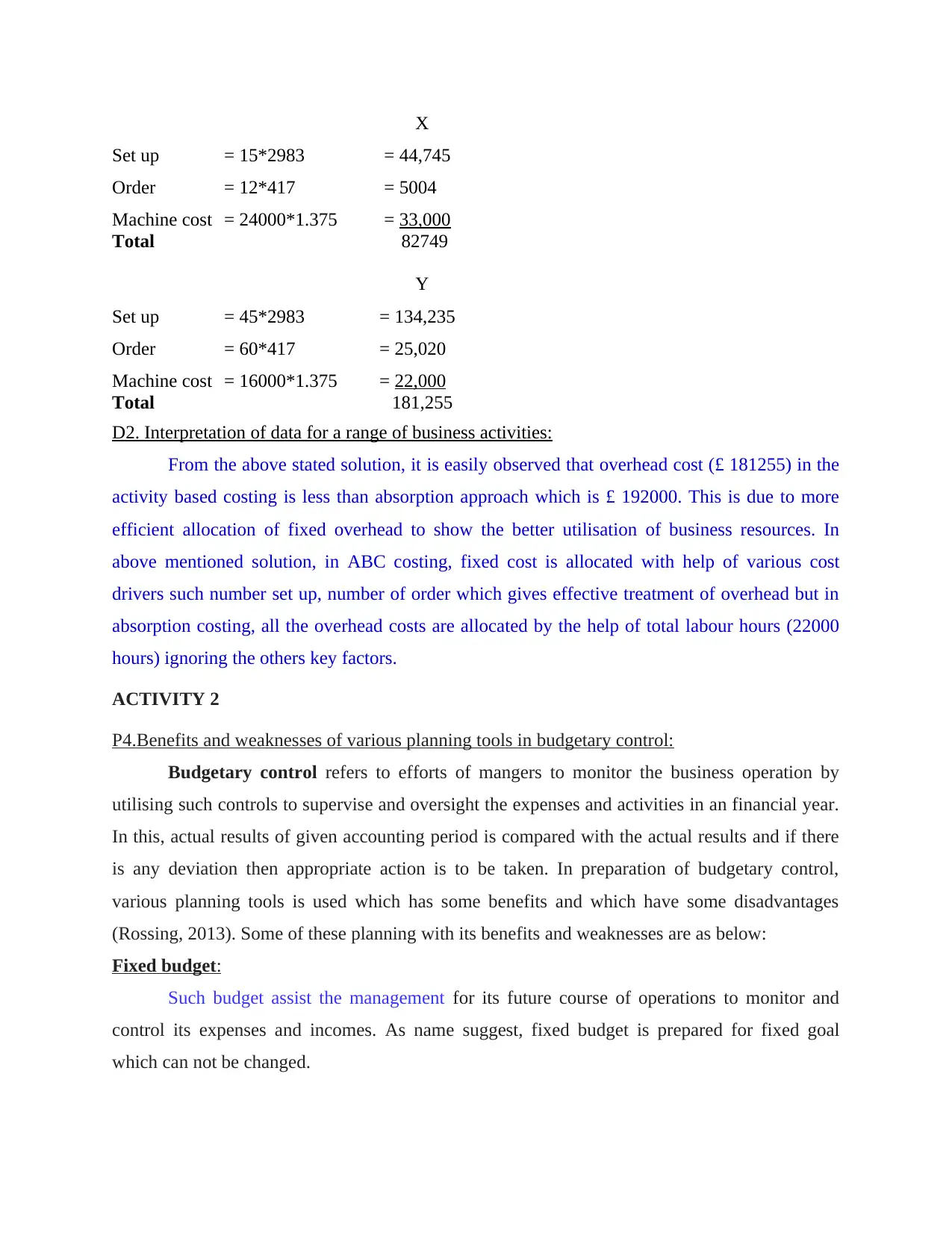

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

D2. Interpretation of data for a range of business activities:

From the above stated solution, it is easily observed that overhead cost (£ 181255) in the

activity based costing is less than absorption approach which is £ 192000. This is due to more

efficient allocation of fixed overhead to show the better utilisation of business resources. In

above mentioned solution, in ABC costing, fixed cost is allocated with help of various cost

drivers such number set up, number of order which gives effective treatment of overhead but in

absorption costing, all the overhead costs are allocated by the help of total labour hours (22000

hours) ignoring the others key factors.

ACTIVITY 2

P4.Benefits and weaknesses of various planning tools in budgetary control:

Budgetary control refers to efforts of mangers to monitor the business operation by

utilising such controls to supervise and oversight the expenses and activities in an financial year.

In this, actual results of given accounting period is compared with the actual results and if there

is any deviation then appropriate action is to be taken. In preparation of budgetary control,

various planning tools is used which has some benefits and which have some disadvantages

(Rossing, 2013). Some of these planning with its benefits and weaknesses are as below:

Fixed budget:

Such budget assist the management for its future course of operations to monitor and

control its expenses and incomes. As name suggest, fixed budget is prepared for fixed goal

which can not be changed.

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

D2. Interpretation of data for a range of business activities:

From the above stated solution, it is easily observed that overhead cost (£ 181255) in the

activity based costing is less than absorption approach which is £ 192000. This is due to more

efficient allocation of fixed overhead to show the better utilisation of business resources. In

above mentioned solution, in ABC costing, fixed cost is allocated with help of various cost

drivers such number set up, number of order which gives effective treatment of overhead but in

absorption costing, all the overhead costs are allocated by the help of total labour hours (22000

hours) ignoring the others key factors.

ACTIVITY 2

P4.Benefits and weaknesses of various planning tools in budgetary control:

Budgetary control refers to efforts of mangers to monitor the business operation by

utilising such controls to supervise and oversight the expenses and activities in an financial year.

In this, actual results of given accounting period is compared with the actual results and if there

is any deviation then appropriate action is to be taken. In preparation of budgetary control,

various planning tools is used which has some benefits and which have some disadvantages

(Rossing, 2013). Some of these planning with its benefits and weaknesses are as below:

Fixed budget:

Such budget assist the management for its future course of operations to monitor and

control its expenses and incomes. As name suggest, fixed budget is prepared for fixed goal

which can not be changed.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.