Management Accounting Systems and Techniques: A Comprehensive Report

VerifiedAdded on 2021/02/19

|21

|5858

|15

Report

AI Summary

This report provides a comprehensive overview of management accounting, exploring its core concepts, techniques, and applications. It begins by defining management accounting and distinguishing it from financial accounting, highlighting its internal focus and the diverse systems employed, such as job costing and inventory management. The report then delves into different methods used for management accounting reporting, including budgeting, cost reports, and performance evaluations. It emphasizes the importance of these reports in informed decision-making and financial risk assessment. A significant portion of the report is dedicated to cost analysis, with detailed explanations of fixed, variable, opportunity, and marginal costs. It demonstrates the preparation of income statements using both marginal and absorption costing methods, complete with cost calculations. The report also examines planning tools used in management accounting, such as budgeting, and how organizations can use management accounting to respond to financial problems. The assignment uses a case study of ABC LTD, a UK-based manufacturing company, to illustrate these concepts and their practical application.

Management Accounting

Systems & Techniques

Systems & Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting. .................................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2. Explain different methods used for management accounting reporting...............................7

LO2. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs ..............................................................................7

P3. ..............................................................................................................................................7

LO3. Explain the use of planning tools used in management accounting.....................................11

P4. ............................................................................................................................................11

LO4. Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems....................................................................................................................16

CONCLUSION.............................................................................................................................19

INTRODUCTION...........................................................................................................................3

LO1. Demonstrate an understanding of management accounting. .................................................4

P1. Explain management accounting and give the essential requirements of different types of

management accounting systems................................................................................................4

P2. Explain different methods used for management accounting reporting...............................7

LO2. Calculate costs using appropriate techniques of cost analysis to prepare an income

statement using marginal and absorption costs ..............................................................................7

P3. ..............................................................................................................................................7

LO3. Explain the use of planning tools used in management accounting.....................................11

P4. ............................................................................................................................................11

LO4. Compare ways in which organizations could use management accounting to respond to

financial problems.........................................................................................................................16

P5. Compare how organizations are adapting management accounting systems to respond to

financial problems....................................................................................................................16

CONCLUSION.............................................................................................................................19

INTRODUCTION

The Management accounting assignment includes a discussion about methods as a

planning and measurement tool for the enterprise to evaluate its performance also includes the

explanations about various management accounting systems. This will create an understanding

of the management accounting system which includes preparation of income statement of basis

of absorption costing and marginal costing.

A comparison has been made to show how the organization can use management accounting in

responding to financial problems.

ABC LTD is a medium size radiators and fan manufacturing company in the UK.

LO1. Demonstrate an understanding of management

accounting.

P1. Explain management accounting and give the essential requirements of different

types of management accounting systems.

Management Accounting, is the process of analysing business costs and operations to prepare

internal financial report, records, and account to aid managers in making decisions in achieving

business goals.

Management accounting is defined as:

Measurement of performance – it helps the organization in measuring employee

performance and efficiency measurement.

Assessment of risk – it identifies and assesses the risk factors within the enterprise

which can be minimised through effective management

Allocation of resources – this ensures fulfilment of organisational objectives while

efforts have been made for long-term sustainability;

Financial statement presentation – Management accounting provides a presentation of

the financial position of the enterprise. Various cost data and financial data makes it easy

for the enterprise to present good and precise financial report in order to take a good

decision.

There are a few roles and principles of management accounting which are explained below;

Influence – Communication is the main source which provides insight that is influential

Management accounting is concerned with effective communication as it improves

decision making;

Relevance – Management accounting takes into consideration the best available relevant

information available with the enterprise.

The Management accounting assignment includes a discussion about methods as a

planning and measurement tool for the enterprise to evaluate its performance also includes the

explanations about various management accounting systems. This will create an understanding

of the management accounting system which includes preparation of income statement of basis

of absorption costing and marginal costing.

A comparison has been made to show how the organization can use management accounting in

responding to financial problems.

ABC LTD is a medium size radiators and fan manufacturing company in the UK.

LO1. Demonstrate an understanding of management

accounting.

P1. Explain management accounting and give the essential requirements of different

types of management accounting systems.

Management Accounting, is the process of analysing business costs and operations to prepare

internal financial report, records, and account to aid managers in making decisions in achieving

business goals.

Management accounting is defined as:

Measurement of performance – it helps the organization in measuring employee

performance and efficiency measurement.

Assessment of risk – it identifies and assesses the risk factors within the enterprise

which can be minimised through effective management

Allocation of resources – this ensures fulfilment of organisational objectives while

efforts have been made for long-term sustainability;

Financial statement presentation – Management accounting provides a presentation of

the financial position of the enterprise. Various cost data and financial data makes it easy

for the enterprise to present good and precise financial report in order to take a good

decision.

There are a few roles and principles of management accounting which are explained below;

Influence – Communication is the main source which provides insight that is influential

Management accounting is concerned with effective communication as it improves

decision making;

Relevance – Management accounting takes into consideration the best available relevant

information available with the enterprise.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Value Generation – Management accounting considers analysis information along with

the value generation path while exploiting opportunities and focuses on costs, risk and

Value generation opportunities;

Trust – the professionals involved in management accounting processes are expected to

be skilful, ethical, and accountable while ensuring governance and social requirements.

The main difference between financial and managerial accounting whether there is an internal

or external focus; financial accounting focuses on creating and evaluating financial statements

that will be reported externally, like creditors and investors and managerial accounting analyses

and reports to business leaders in order to make decision to run the business effectively.

The various distinctions between management and financial accounting are presented bellow;

Users: The use of management accounting is internal mainly with managers and employees

whereas external users are concerned with financial accounting including shareholders, creditors,

banks;

Set of regulations: No application of accounting standard or external rules is imposed in

management accounting where a financial accounting is concerned with a various set of

regulations and standards as applicable to the company.

Sources: Financial as well as non-financial data, is used in management accounting however

financial accounting uses financial data utilized and drawn from the organization core

transaction-based accounting system.

Nature: The nature of information is mainly historical, current and future-oriented in

management accounting while the source of information and nature is historical related to the

past performance in financial accounting.

Various types of management accounting for the chosen company means:

- Job costing system: this is a system to assign manufacturing cost to each individual

product while keeping track on expense monitoring.

Job costing accounting procedure consist of: - receiving enquiry, estimate price of job,

order receiving, production order, cost recording, completion of the job.

- Price optimising system: Price optimizing system is used o take control of the prices of

resources. ABC will use this type of management accounting system as it will help tthem

in determining price structures for promotional pricing, initial pricing, and discount

pricing.

- Cost accounting system: The system helps the organisation to estimate the cost of the

product while analysis can be made of organisational profitability, inventory and cost

control.

the value generation path while exploiting opportunities and focuses on costs, risk and

Value generation opportunities;

Trust – the professionals involved in management accounting processes are expected to

be skilful, ethical, and accountable while ensuring governance and social requirements.

The main difference between financial and managerial accounting whether there is an internal

or external focus; financial accounting focuses on creating and evaluating financial statements

that will be reported externally, like creditors and investors and managerial accounting analyses

and reports to business leaders in order to make decision to run the business effectively.

The various distinctions between management and financial accounting are presented bellow;

Users: The use of management accounting is internal mainly with managers and employees

whereas external users are concerned with financial accounting including shareholders, creditors,

banks;

Set of regulations: No application of accounting standard or external rules is imposed in

management accounting where a financial accounting is concerned with a various set of

regulations and standards as applicable to the company.

Sources: Financial as well as non-financial data, is used in management accounting however

financial accounting uses financial data utilized and drawn from the organization core

transaction-based accounting system.

Nature: The nature of information is mainly historical, current and future-oriented in

management accounting while the source of information and nature is historical related to the

past performance in financial accounting.

Various types of management accounting for the chosen company means:

- Job costing system: this is a system to assign manufacturing cost to each individual

product while keeping track on expense monitoring.

Job costing accounting procedure consist of: - receiving enquiry, estimate price of job,

order receiving, production order, cost recording, completion of the job.

- Price optimising system: Price optimizing system is used o take control of the prices of

resources. ABC will use this type of management accounting system as it will help tthem

in determining price structures for promotional pricing, initial pricing, and discount

pricing.

- Cost accounting system: The system helps the organisation to estimate the cost of the

product while analysis can be made of organisational profitability, inventory and cost

control.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

- Inventory management system : The system can be used to achieve efficient and

effective flow of inventory within the organization and at the point of sales.

The various advantages of management accounting systems in context of ABC is presented

below:

- Cost accounting system.

Advantages

o ABC Ltd can measure the efficiency in processes and then assist in making with

the use of this system;

o it will help the company in fixation and reduction of prices

o provides necessary information required for planning.

- Inventory management systems:

o ABC can improve the accuracy of its inventory orders which means efficiency

and saving time and money;

- Job costing system:

o It will help ABC in the estimations of all types of cost throughout the

manufacturing process;

o It will prevent duplication and it helps in the evaluation of the quality of work

done.

- Price optimising systems

o ABC can determine the attitude of customers based on different prices, and helps

in maximizations of operating profit with best prices.

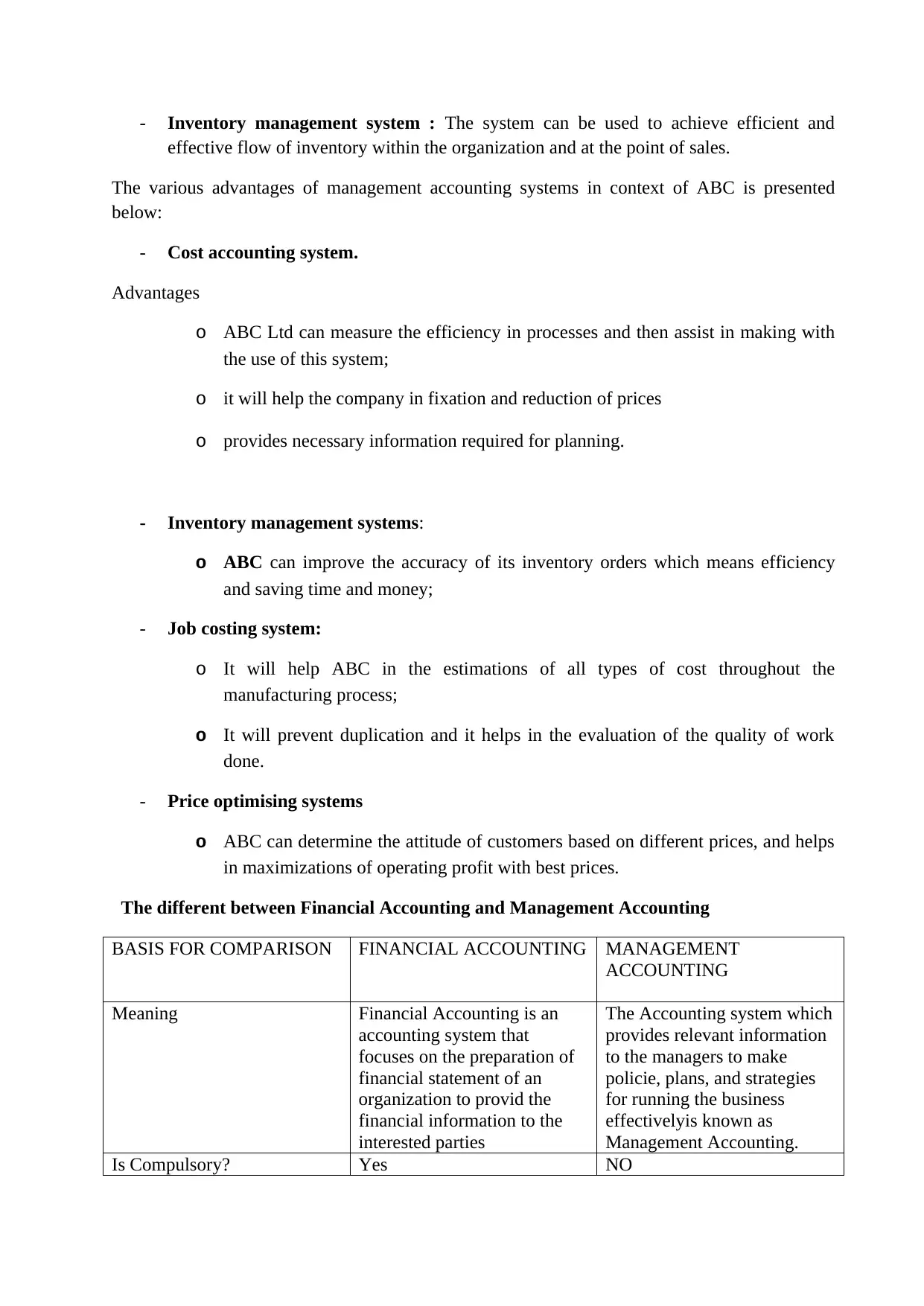

The different between Financial Accounting and Management Accounting

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

Meaning Financial Accounting is an

accounting system that

focuses on the preparation of

financial statement of an

organization to provid the

financial information to the

interested parties

The Accounting system which

provides relevant information

to the managers to make

policie, plans, and strategies

for running the business

effectivelyis known as

Management Accounting.

Is Compulsory? Yes NO

effective flow of inventory within the organization and at the point of sales.

The various advantages of management accounting systems in context of ABC is presented

below:

- Cost accounting system.

Advantages

o ABC Ltd can measure the efficiency in processes and then assist in making with

the use of this system;

o it will help the company in fixation and reduction of prices

o provides necessary information required for planning.

- Inventory management systems:

o ABC can improve the accuracy of its inventory orders which means efficiency

and saving time and money;

- Job costing system:

o It will help ABC in the estimations of all types of cost throughout the

manufacturing process;

o It will prevent duplication and it helps in the evaluation of the quality of work

done.

- Price optimising systems

o ABC can determine the attitude of customers based on different prices, and helps

in maximizations of operating profit with best prices.

The different between Financial Accounting and Management Accounting

BASIS FOR COMPARISON FINANCIAL ACCOUNTING MANAGEMENT

ACCOUNTING

Meaning Financial Accounting is an

accounting system that

focuses on the preparation of

financial statement of an

organization to provid the

financial information to the

interested parties

The Accounting system which

provides relevant information

to the managers to make

policie, plans, and strategies

for running the business

effectivelyis known as

Management Accounting.

Is Compulsory? Yes NO

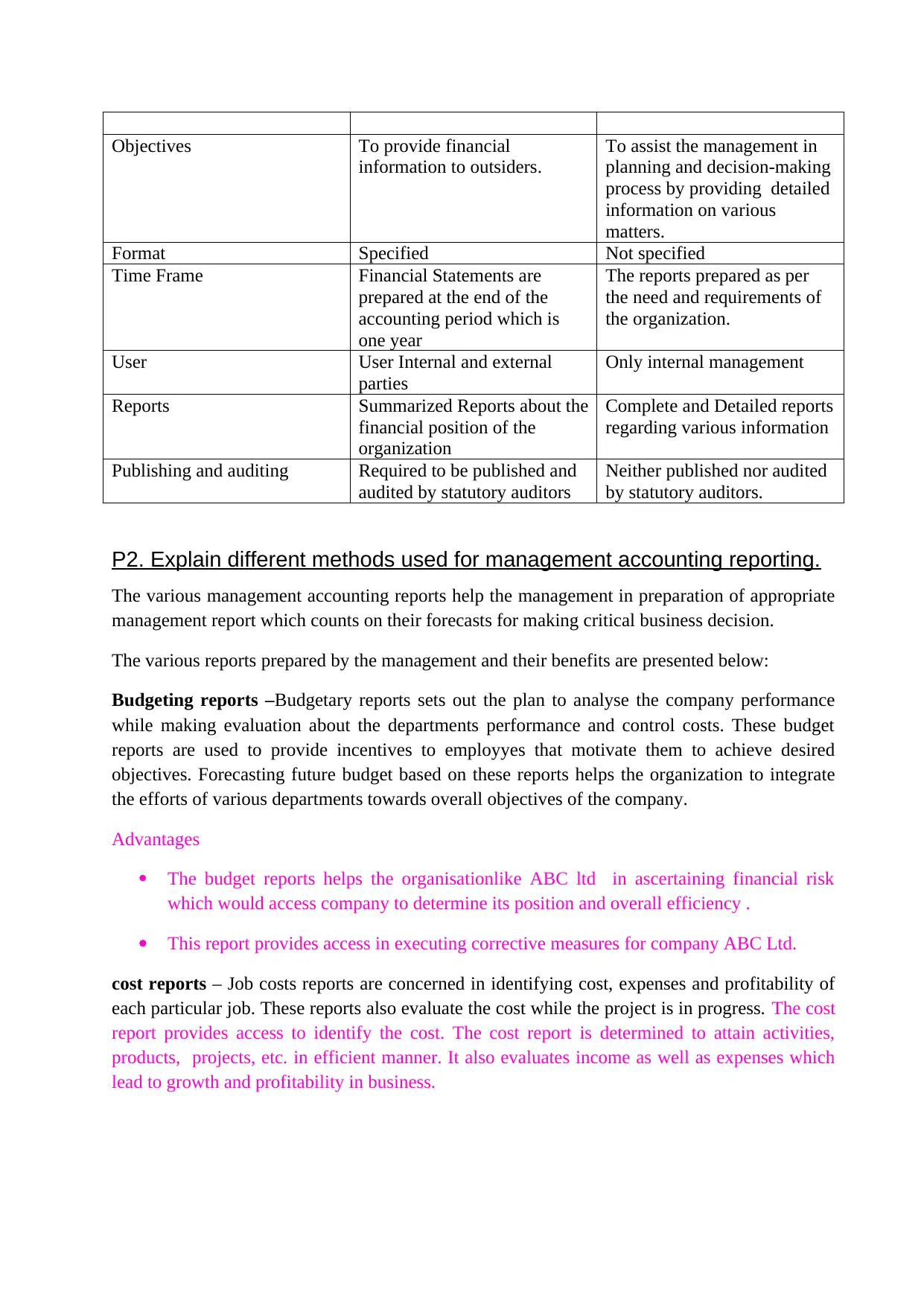

Objectives To provide financial

information to outsiders.

To assist the management in

planning and decision-making

process by providing detailed

information on various

matters.

Format Specified Not specified

Time Frame Financial Statements are

prepared at the end of the

accounting period which is

one year

The reports prepared as per

the need and requirements of

the organization.

User User Internal and external

parties

Only internal management

Reports Summarized Reports about the

financial position of the

organization

Complete and Detailed reports

regarding various information

Publishing and auditing Required to be published and

audited by statutory auditors

Neither published nor audited

by statutory auditors.

P2. Explain different methods used for management accounting reporting.

The various management accounting reports help the management in preparation of appropriate

management report which counts on their forecasts for making critical business decision.

The various reports prepared by the management and their benefits are presented below:

Budgeting reports –Budgetary reports sets out the plan to analyse the company performance

while making evaluation about the departments performance and control costs. These budget

reports are used to provide incentives to employyes that motivate them to achieve desired

objectives. Forecasting future budget based on these reports helps the organization to integrate

the efforts of various departments towards overall objectives of the company.

Advantages

The budget reports helps the organisationlike ABC ltd in ascertaining financial risk

which would access company to determine its position and overall efficiency .

This report provides access in executing corrective measures for company ABC Ltd.

cost reports – Job costs reports are concerned in identifying cost, expenses and profitability of

each particular job. These reports also evaluate the cost while the project is in progress. The cost

report provides access to identify the cost. The cost report is determined to attain activities,

products, projects, etc. in efficient manner. It also evaluates income as well as expenses which

lead to growth and profitability in business.

information to outsiders.

To assist the management in

planning and decision-making

process by providing detailed

information on various

matters.

Format Specified Not specified

Time Frame Financial Statements are

prepared at the end of the

accounting period which is

one year

The reports prepared as per

the need and requirements of

the organization.

User User Internal and external

parties

Only internal management

Reports Summarized Reports about the

financial position of the

organization

Complete and Detailed reports

regarding various information

Publishing and auditing Required to be published and

audited by statutory auditors

Neither published nor audited

by statutory auditors.

P2. Explain different methods used for management accounting reporting.

The various management accounting reports help the management in preparation of appropriate

management report which counts on their forecasts for making critical business decision.

The various reports prepared by the management and their benefits are presented below:

Budgeting reports –Budgetary reports sets out the plan to analyse the company performance

while making evaluation about the departments performance and control costs. These budget

reports are used to provide incentives to employyes that motivate them to achieve desired

objectives. Forecasting future budget based on these reports helps the organization to integrate

the efforts of various departments towards overall objectives of the company.

Advantages

The budget reports helps the organisationlike ABC ltd in ascertaining financial risk

which would access company to determine its position and overall efficiency .

This report provides access in executing corrective measures for company ABC Ltd.

cost reports – Job costs reports are concerned in identifying cost, expenses and profitability of

each particular job. These reports also evaluate the cost while the project is in progress. The cost

report provides access to identify the cost. The cost report is determined to attain activities,

products, projects, etc. in efficient manner. It also evaluates income as well as expenses which

lead to growth and profitability in business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory and manufacturing reports - These reports contain labour cost, per unit overhead

cost and wastages with inventory which provides managers a good comparison between different

assembly line.

Performance reports: this is a comparison of actual results with budgeted performances and

analysed. These are generally prepared yearly however they can be prepared monthly or

quarterly. This report is prepared for reviewing the business performance such as ABC Ltd. The

members of staff which executes decision making in relation to appraisal. This report is prepared

mostly in large organisation for their department in order to analyse its performance for attaining

set goals and objectives

Advantages

The report is helpful while conducting training programme in ABC Ltd. By analysing

performance of the employees.

Also, this report is helpful in determining category of employees regarding promotion,

termination, transfer, etc. for employees working in ABC ltd.

Order information report: The order information report helps management to see th trends in

their business efficiently and effectively. Various types of reports prepared in this type of

reporting help integrating management operations to achieve low cost on placing of orders and

their management.

LO2. Calculate costs using appropriate techniques of cost

analysis to prepare an income statement using marginal

and absorption costs

P3.

1) Explain the different types of costs.

Cost refers to the value of money which has been used to produce anything and represents the

monitory evaluation of materials, resources, efforts, risks incurred, time and utilities consumed

and the opportunity in production and delivery of product (Drury 2013).

There are a few types of costs:

Fixed and variable costs – Fixed costs represents that part of the cost that remains constant for

a certain level of output and does not get fluctuated.

Variable costs represents that part of the costs that varies with the variation in production

directly like raw material, labour (Weygandt, et.al.,2015).

Opportunity and outlay costs – Outlay or actual cost are the real or actual expenses incurred by

the firm for machinery, labour, material.

cost and wastages with inventory which provides managers a good comparison between different

assembly line.

Performance reports: this is a comparison of actual results with budgeted performances and

analysed. These are generally prepared yearly however they can be prepared monthly or

quarterly. This report is prepared for reviewing the business performance such as ABC Ltd. The

members of staff which executes decision making in relation to appraisal. This report is prepared

mostly in large organisation for their department in order to analyse its performance for attaining

set goals and objectives

Advantages

The report is helpful while conducting training programme in ABC Ltd. By analysing

performance of the employees.

Also, this report is helpful in determining category of employees regarding promotion,

termination, transfer, etc. for employees working in ABC ltd.

Order information report: The order information report helps management to see th trends in

their business efficiently and effectively. Various types of reports prepared in this type of

reporting help integrating management operations to achieve low cost on placing of orders and

their management.

LO2. Calculate costs using appropriate techniques of cost

analysis to prepare an income statement using marginal

and absorption costs

P3.

1) Explain the different types of costs.

Cost refers to the value of money which has been used to produce anything and represents the

monitory evaluation of materials, resources, efforts, risks incurred, time and utilities consumed

and the opportunity in production and delivery of product (Drury 2013).

There are a few types of costs:

Fixed and variable costs – Fixed costs represents that part of the cost that remains constant for

a certain level of output and does not get fluctuated.

Variable costs represents that part of the costs that varies with the variation in production

directly like raw material, labour (Weygandt, et.al.,2015).

Opportunity and outlay costs – Outlay or actual cost are the real or actual expenses incurred by

the firm for machinery, labour, material.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Out of pocketbook costs: Out of pocket cost involves current cash payment for the expense

incurred and also known as explicit cost. It represents the cost of self-owned factors of

production and includes unpaid interest, depreciation and salary of owners of business.

Total average and marginal costs: Marginal cost or the cost of marginal unit produced because

it is that cost which gets incurred for producing the additional unit.

2) Present cost calculations to prepare an income statement using marginal and absorption

costs.

Marginal Costing – Marginal costing can be defined as the accounting system in which variable

costs are allocated to the cost units but fixed costs for the period is written off fully o the

aggregate contribution (Delis, 2015).

Absorption costs – Absorption costing takes into consideration all the resources and expenses

related to the cost of production and hence treats all cost of production as product cost. The cost

includes direct material, direct labour and both fixed and variable overhead cost. Going further

in absorption costing a portion of the fixed overhead cost is allocated to each unit of the product

along with the variable manufacturing cost.

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.

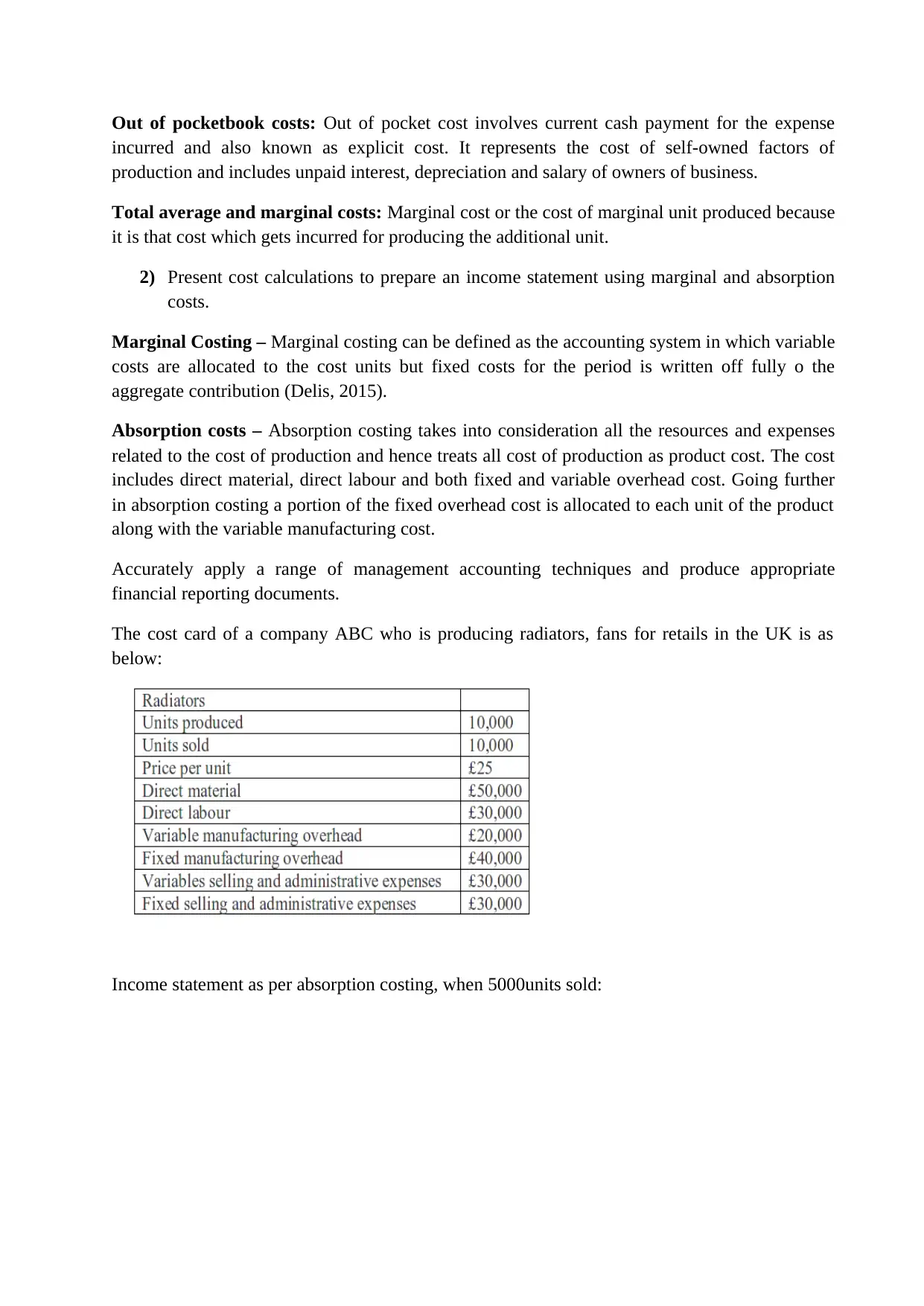

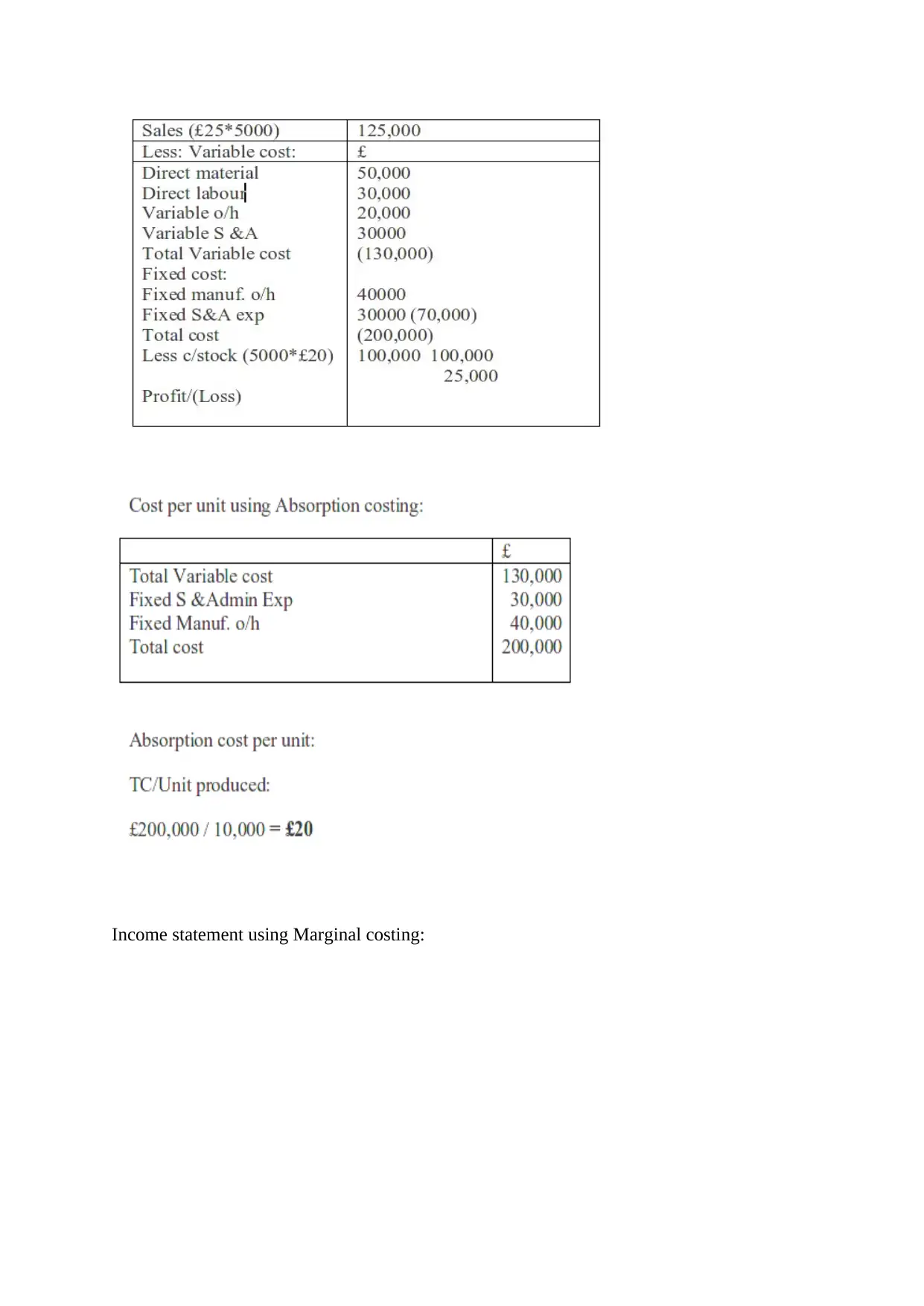

The cost card of a company ABC who is producing radiators, fans for retails in the UK is as

below:

Income statement as per absorption costing, when 5000units sold:

incurred and also known as explicit cost. It represents the cost of self-owned factors of

production and includes unpaid interest, depreciation and salary of owners of business.

Total average and marginal costs: Marginal cost or the cost of marginal unit produced because

it is that cost which gets incurred for producing the additional unit.

2) Present cost calculations to prepare an income statement using marginal and absorption

costs.

Marginal Costing – Marginal costing can be defined as the accounting system in which variable

costs are allocated to the cost units but fixed costs for the period is written off fully o the

aggregate contribution (Delis, 2015).

Absorption costs – Absorption costing takes into consideration all the resources and expenses

related to the cost of production and hence treats all cost of production as product cost. The cost

includes direct material, direct labour and both fixed and variable overhead cost. Going further

in absorption costing a portion of the fixed overhead cost is allocated to each unit of the product

along with the variable manufacturing cost.

Accurately apply a range of management accounting techniques and produce appropriate

financial reporting documents.

The cost card of a company ABC who is producing radiators, fans for retails in the UK is as

below:

Income statement as per absorption costing, when 5000units sold:

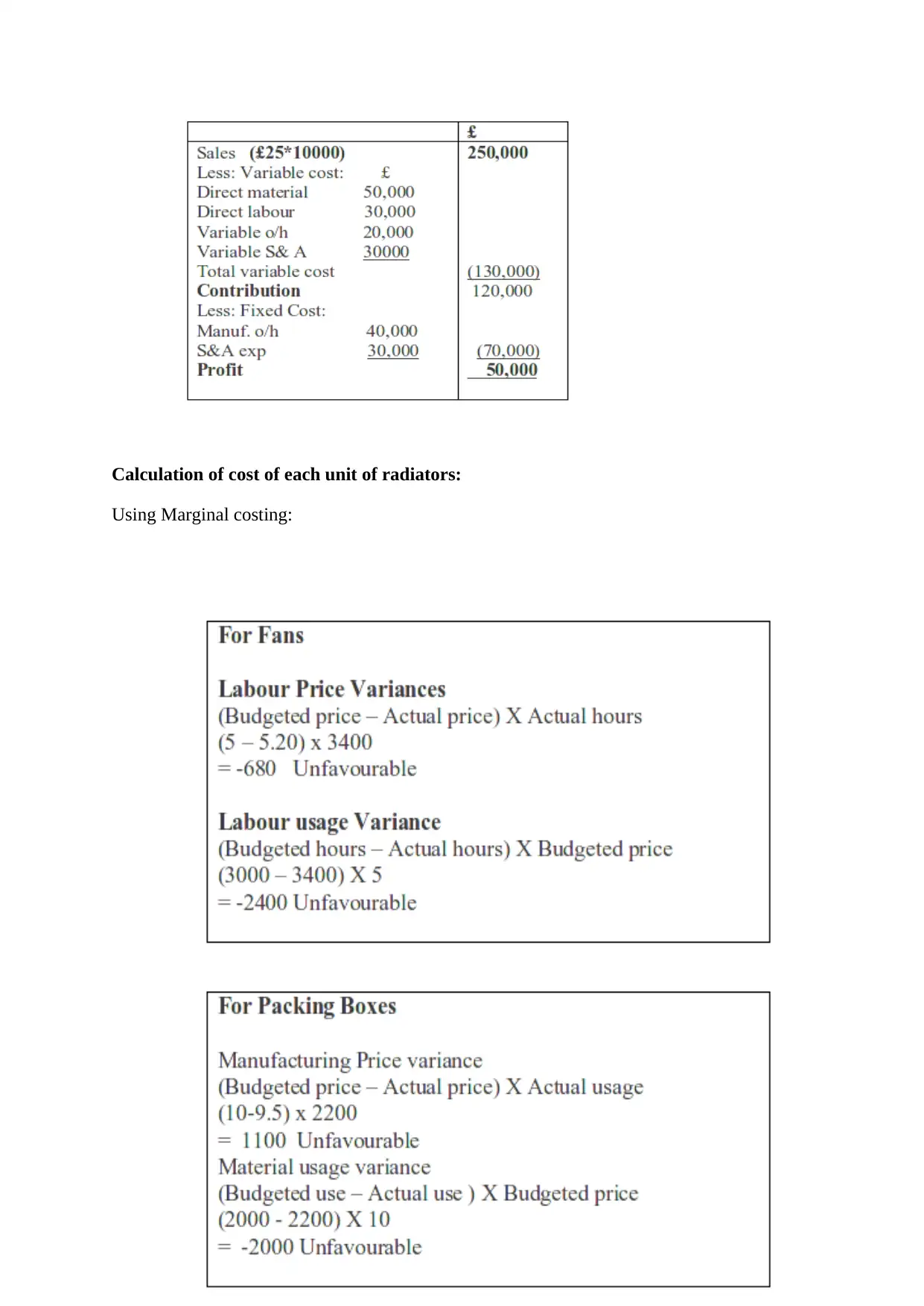

Income statement using Marginal costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Calculation of cost of each unit of radiators:

Using Marginal costing:

Using Marginal costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

LO3. Explain the use of planning tools used in management

accounting

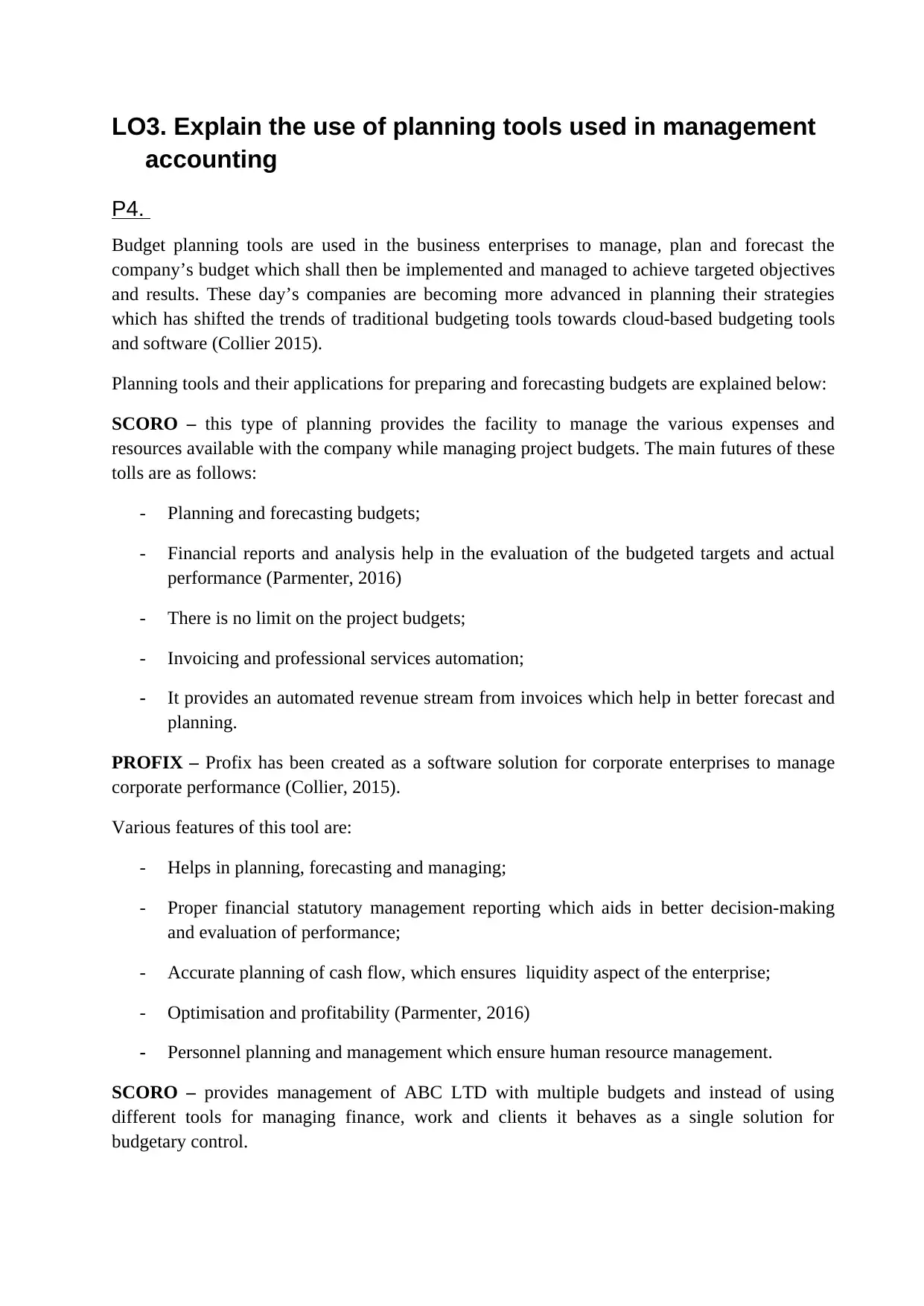

P4.

Budget planning tools are used in the business enterprises to manage, plan and forecast the

company’s budget which shall then be implemented and managed to achieve targeted objectives

and results. These day’s companies are becoming more advanced in planning their strategies

which has shifted the trends of traditional budgeting tools towards cloud-based budgeting tools

and software (Collier 2015).

Planning tools and their applications for preparing and forecasting budgets are explained below:

SCORO – this type of planning provides the facility to manage the various expenses and

resources available with the company while managing project budgets. The main futures of these

tolls are as follows:

- Planning and forecasting budgets;

- Financial reports and analysis help in the evaluation of the budgeted targets and actual

performance (Parmenter, 2016)

- There is no limit on the project budgets;

- Invoicing and professional services automation;

- It provides an automated revenue stream from invoices which help in better forecast and

planning.

PROFIX – Profix has been created as a software solution for corporate enterprises to manage

corporate performance (Collier, 2015).

Various features of this tool are:

- Helps in planning, forecasting and managing;

- Proper financial statutory management reporting which aids in better decision-making

and evaluation of performance;

- Accurate planning of cash flow, which ensures liquidity aspect of the enterprise;

- Optimisation and profitability (Parmenter, 2016)

- Personnel planning and management which ensure human resource management.

SCORO – provides management of ABC LTD with multiple budgets and instead of using

different tools for managing finance, work and clients it behaves as a single solution for

budgetary control.

accounting

P4.

Budget planning tools are used in the business enterprises to manage, plan and forecast the

company’s budget which shall then be implemented and managed to achieve targeted objectives

and results. These day’s companies are becoming more advanced in planning their strategies

which has shifted the trends of traditional budgeting tools towards cloud-based budgeting tools

and software (Collier 2015).

Planning tools and their applications for preparing and forecasting budgets are explained below:

SCORO – this type of planning provides the facility to manage the various expenses and

resources available with the company while managing project budgets. The main futures of these

tolls are as follows:

- Planning and forecasting budgets;

- Financial reports and analysis help in the evaluation of the budgeted targets and actual

performance (Parmenter, 2016)

- There is no limit on the project budgets;

- Invoicing and professional services automation;

- It provides an automated revenue stream from invoices which help in better forecast and

planning.

PROFIX – Profix has been created as a software solution for corporate enterprises to manage

corporate performance (Collier, 2015).

Various features of this tool are:

- Helps in planning, forecasting and managing;

- Proper financial statutory management reporting which aids in better decision-making

and evaluation of performance;

- Accurate planning of cash flow, which ensures liquidity aspect of the enterprise;

- Optimisation and profitability (Parmenter, 2016)

- Personnel planning and management which ensure human resource management.

SCORO – provides management of ABC LTD with multiple budgets and instead of using

different tools for managing finance, work and clients it behaves as a single solution for

budgetary control.

PROFIX – the tool will offer ABC LTD with a wholesome product that upgrades and scales

constantly with the growth of the company and forecasting becomes much easier due to

flexibility and adaptability of the tool. The preparation of the budgets will be better and the

resource allocation can be evaluated and analysed in a manner which will ensure that the

company achieves efficiency in operations.

1) Explain different types of common costing systems which can be used for budgetary

control and how costing systems can differ depending of the costing activity.

Costing System Overview Use of system in

budgetary control

Differentiation

Actual costing

system

This is a costing

system which i

concerned with the

recording of cost of

the product based on

actual cost of

material, labour and

overhead incurred

on the product

which is allocated

on the basis of the

actual quantity of

the allocation base

seen during the

reporting period.

This is the simple

costing system

which does not

require any

preplanning of the

standard cost.

The cost estimated

on the basis of

actual costing

system helps the

management to

prepare the budgets

and set targeted

standards in order to

achieve the

objectives of

enterprise which are

practical to achieve.

It does not take into

account any

budgeted amounts or

standards rather it

makes utilisation of

actual cost data.

Normal costing

system

Normal costing

system makes use of

a budgeted amount

of overhead for the

calculation of

product cost. It

makes the use of

smooth long-term

estimated overhead

rate which ensures

the calculation of

cost where sudden

spikes in the cost

are not

The estimation of

production

overheads helps in

calculation of cost

related to a long-

term aspect. This

will help in

preparation of

budgets for the

future aspect of the

enterprise.

Normal costing uses

actual cost for the

material and labour

components but

makes use of

budgeted overhead.

If any difference is

obtained standard

overhead cost and

actual overhead cost

then it can be

charged to cost of

goods sold.

Standard costing This refers to the

cost accounting

Standard costs

allocated to the

The cost accounting

here is concerned

constantly with the growth of the company and forecasting becomes much easier due to

flexibility and adaptability of the tool. The preparation of the budgets will be better and the

resource allocation can be evaluated and analysed in a manner which will ensure that the

company achieves efficiency in operations.

1) Explain different types of common costing systems which can be used for budgetary

control and how costing systems can differ depending of the costing activity.

Costing System Overview Use of system in

budgetary control

Differentiation

Actual costing

system

This is a costing

system which i

concerned with the

recording of cost of

the product based on

actual cost of

material, labour and

overhead incurred

on the product

which is allocated

on the basis of the

actual quantity of

the allocation base

seen during the

reporting period.

This is the simple

costing system

which does not

require any

preplanning of the

standard cost.

The cost estimated

on the basis of

actual costing

system helps the

management to

prepare the budgets

and set targeted

standards in order to

achieve the

objectives of

enterprise which are

practical to achieve.

It does not take into

account any

budgeted amounts or

standards rather it

makes utilisation of

actual cost data.

Normal costing

system

Normal costing

system makes use of

a budgeted amount

of overhead for the

calculation of

product cost. It

makes the use of

smooth long-term

estimated overhead

rate which ensures

the calculation of

cost where sudden

spikes in the cost

are not

The estimation of

production

overheads helps in

calculation of cost

related to a long-

term aspect. This

will help in

preparation of

budgets for the

future aspect of the

enterprise.

Normal costing uses

actual cost for the

material and labour

components but

makes use of

budgeted overhead.

If any difference is

obtained standard

overhead cost and

actual overhead cost

then it can be

charged to cost of

goods sold.

Standard costing This refers to the

cost accounting

Standard costs

allocated to the

The cost accounting

here is concerned

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.