Report on Management Accounting for Captify Manufacturing, UK

VerifiedAdded on 2020/10/23

|14

|3963

|336

Report

AI Summary

This report, prepared by an assistant accountant for Captify, a UK-based manufacturing company, explores key aspects of management accounting. It begins by defining management accounting and its essential requirements, including cost accounting and inventory management systems. The report then details various management accounting reporting methods, such as budget, financial, performance, and cost reports. It critically evaluates the management accounting system and reporting, highlighting their importance for financial efficiency. Furthermore, the report presents the preparation of income statements using different management accounting techniques, specifically marginal costing and absorption costing, illustrating the varying profit results. The report also includes calculations and interpretations of both costing methods, offering a comprehensive analysis of financial reporting in a business context.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

1. Management accounting and its essential requirement of the management accounting

system..........................................................................................................................................1

2. Explaining different methods of the management accounting reporting................................3

LO 2.................................................................................................................................................5

3. Preparation of income statement using different management accounting techniques..........5

LO 3.................................................................................................................................................6

4. Explaining advantages and disadvantages of various planning tools of the budgetary control

system .........................................................................................................................................7

5. Explaining various management accounting system as to help the company in responding

to various financial problems......................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

1. Management accounting and its essential requirement of the management accounting

system..........................................................................................................................................1

2. Explaining different methods of the management accounting reporting................................3

LO 2.................................................................................................................................................5

3. Preparation of income statement using different management accounting techniques..........5

LO 3.................................................................................................................................................6

4. Explaining advantages and disadvantages of various planning tools of the budgetary control

system .........................................................................................................................................7

5. Explaining various management accounting system as to help the company in responding

to various financial problems......................................................................................................9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is a branch of accounting that is concerned with providing all

the relevant information to the managers of the company. It is a process which requires

professional skills of the accountants so that they can provide all the relevant financial

information to the managers and helping them in their decision making procedure. Captify is a

middle sized manufacturing company of UK. It was established in 2011. The present assignment

shows a report of an assistant accountant of the Captify, that provides a brief information about

the management accounting its essential requirement in the business along with the benefits of

various management accounting systems and their applications within the business. Further, the

study also shows numerous methods to be used for the management accounting reporting. An

explanation about various planning tools of the budgetary control system and about adoption of

various management accounting system and their usefulness in the business as to resolve various

financial problems of the company. In addition, the study also shows preparation of the income

statement of the company using different techniques of the management accounting

LO 1

1. Management accounting and its essential requirement of the management accounting system

Captify

To,

the line manager,

subject: For providing information about the role and functions of management accounts

department.

Management accounting

“The management accounting system can be defined as a process of analysing the cost

and financial activities of the business and preparing financial reports from those informations

as to help the managers in taking their decisions relating to the cost and financial activities of

the business, as to strengthen the financial capacity of the business. (Otley, 2016)”

In other words, it can also be defined as a systematic procedure through which the

business can develop effectiveness and efficiency in the business as to make the best use of the

financial resources like cash, inventories, etc. of the business.”

Management accounting system

“Management accounting system refers to a process in which the financial managers

1

Management accounting is a branch of accounting that is concerned with providing all

the relevant information to the managers of the company. It is a process which requires

professional skills of the accountants so that they can provide all the relevant financial

information to the managers and helping them in their decision making procedure. Captify is a

middle sized manufacturing company of UK. It was established in 2011. The present assignment

shows a report of an assistant accountant of the Captify, that provides a brief information about

the management accounting its essential requirement in the business along with the benefits of

various management accounting systems and their applications within the business. Further, the

study also shows numerous methods to be used for the management accounting reporting. An

explanation about various planning tools of the budgetary control system and about adoption of

various management accounting system and their usefulness in the business as to resolve various

financial problems of the company. In addition, the study also shows preparation of the income

statement of the company using different techniques of the management accounting

LO 1

1. Management accounting and its essential requirement of the management accounting system

Captify

To,

the line manager,

subject: For providing information about the role and functions of management accounts

department.

Management accounting

“The management accounting system can be defined as a process of analysing the cost

and financial activities of the business and preparing financial reports from those informations

as to help the managers in taking their decisions relating to the cost and financial activities of

the business, as to strengthen the financial capacity of the business. (Otley, 2016)”

In other words, it can also be defined as a systematic procedure through which the

business can develop effectiveness and efficiency in the business as to make the best use of the

financial resources like cash, inventories, etc. of the business.”

Management accounting system

“Management accounting system refers to a process in which the financial managers

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

analyse and evaluate all the financial activities of the business and prepares a detailed report

that

can provide all the detailed information to both internal and external users of the company.”

There are various management accounting systems like cost accounting

system,inventory management system, job costing system, etc. that can be adopted by the

company for the purpose of developing effectiveness in the overall business organisation.

Essential requirements of management accounting system

Cost accounting system: Cost accounting system is that type of management

accounting system that helps the overall business in estimating the cost to be incurred by

the business and determine the actual cost of the business as well. This system helps the

company in developing the cost effectiveness in the overall business operations. This

system is required by the those business that are engaged in manufacturing products or

renderning services to the customers.

Requirements

▪ This system helps the business in making the company more cost effective.

▪ It helps the managers in having effective analysis of the cost related activities

and develop more strong strategies for the company accordingly.

▪ With the help of it, company can determine the cost incurred by the business for

manufacturing each product or rendering each services to the customers (Maas,

Schaltegger and Crutzen, 2016). In this regard, the firm can determine the

appropriate price of the product or services.

▪ Further, this system also helps the managers in predicting the requirement of

resources in the firm in the near future. With the help of which they can maintain

sufficiency of the various financial resources of the business.

Inventory management system: Inventory management system can be defined as a

process of management in which they monitors the usage of inventories of the business

and develop strategies and plans for the business. This system helps the managers in

developing effectiveness in the business for using its inventories. This system is Useful

for those businesses that needs to maintain the inventories either for the further

processing and manufacturing goods or for their further sale.

Requirements

2

that

can provide all the detailed information to both internal and external users of the company.”

There are various management accounting systems like cost accounting

system,inventory management system, job costing system, etc. that can be adopted by the

company for the purpose of developing effectiveness in the overall business organisation.

Essential requirements of management accounting system

Cost accounting system: Cost accounting system is that type of management

accounting system that helps the overall business in estimating the cost to be incurred by

the business and determine the actual cost of the business as well. This system helps the

company in developing the cost effectiveness in the overall business operations. This

system is required by the those business that are engaged in manufacturing products or

renderning services to the customers.

Requirements

▪ This system helps the business in making the company more cost effective.

▪ It helps the managers in having effective analysis of the cost related activities

and develop more strong strategies for the company accordingly.

▪ With the help of it, company can determine the cost incurred by the business for

manufacturing each product or rendering each services to the customers (Maas,

Schaltegger and Crutzen, 2016). In this regard, the firm can determine the

appropriate price of the product or services.

▪ Further, this system also helps the managers in predicting the requirement of

resources in the firm in the near future. With the help of which they can maintain

sufficiency of the various financial resources of the business.

Inventory management system: Inventory management system can be defined as a

process of management in which they monitors the usage of inventories of the business

and develop strategies and plans for the business. This system helps the managers in

developing effectiveness in the business for using its inventories. This system is Useful

for those businesses that needs to maintain the inventories either for the further

processing and manufacturing goods or for their further sale.

Requirements

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

▪ It enables the managers in monitoring the use of inventories in the business.

▪ With the help of this system, managers can maintain the sufficiency of the

inventory in the business by determining the minimum need of the stock in the

firm.

▪ Further, this system also result in elimination of the excess or shortage of the

inventory in the business.

▪ The inventory management system also leads in eliminating wastage of the stock

from the business by monitoring each flow of the inventory in the company.

Price optimisation system: Adoption of this system of the management accounting can

help the managers in effectively setting the price of their products or services. In this

system, the managers analyses the cost of each product and sets the price in such a way

so that the company could generate enough profit from its selling and customers also

gets ready to pay such price for the product (Modugno and Di Carlo, 2019). This

system is required by all the businesses, as each company needs to set the price of their

product or services.

Requirements

▪ It helps the company in generating sufficient profit from the business operations.

▪ This system may result in attracting the customers towards the company's

product due to setting of the most appropriate price of the product.

▪ It may result in improving the profit making policies of the firm.

2. Explaining different methods of the management accounting reporting

Management accounting reporting

management accounting reporting is a part of management accounting in which various

financial accounting reports are prepared by the business in order to summerise all the financial

transactions of the company.

The management accounting reporting is required by all the firms as to provide all the

relevant information to the internal and external users of the financial reports. With the help of

these reports, the internal users of the company i.e. managers can effectively analyze the actual

position of the company and develop[p their strategies accordingly. Further, with the help of

these reports the external users like creditors, suppliers, investors, etc. can take their decisions

for the company.

3

▪ With the help of this system, managers can maintain the sufficiency of the

inventory in the business by determining the minimum need of the stock in the

firm.

▪ Further, this system also result in elimination of the excess or shortage of the

inventory in the business.

▪ The inventory management system also leads in eliminating wastage of the stock

from the business by monitoring each flow of the inventory in the company.

Price optimisation system: Adoption of this system of the management accounting can

help the managers in effectively setting the price of their products or services. In this

system, the managers analyses the cost of each product and sets the price in such a way

so that the company could generate enough profit from its selling and customers also

gets ready to pay such price for the product (Modugno and Di Carlo, 2019). This

system is required by all the businesses, as each company needs to set the price of their

product or services.

Requirements

▪ It helps the company in generating sufficient profit from the business operations.

▪ This system may result in attracting the customers towards the company's

product due to setting of the most appropriate price of the product.

▪ It may result in improving the profit making policies of the firm.

2. Explaining different methods of the management accounting reporting

Management accounting reporting

management accounting reporting is a part of management accounting in which various

financial accounting reports are prepared by the business in order to summerise all the financial

transactions of the company.

The management accounting reporting is required by all the firms as to provide all the

relevant information to the internal and external users of the financial reports. With the help of

these reports, the internal users of the company i.e. managers can effectively analyze the actual

position of the company and develop[p their strategies accordingly. Further, with the help of

these reports the external users like creditors, suppliers, investors, etc. can take their decisions

for the company.

3

Methods of management accounting reporting

There are various methods through with the help of which the managers can prepare

various management accounting reports (Hopper and Bui, 2016). Some of the important

methods of management accounting reporting are as under:

Budget reports: These are the reports that provides the information about the estimated

activities of the company. With the help of these reports the managers can maintain

sufficiency of each resources of the company. Further, by comparing these reports with

the actual performance of the firm, the managers can analyse the efficiency of the

business and develop more effective strategies and plan for the company as well.

Financial reports: Financial reports of the company contains information about all the

financial transactions of the business. With the help of these reports, the managers can

analyse all the activities of the business (TYPES OF MANAGERIAL ACCOUNTING

REPORTS, 2019). These provides all the relevant information to the managers which

are required by them as to analyse overall performance of the business.

Performance reports: These reports includes information about the overall

performance of the business. These reports are prepared by comparing the actual

performance of the business with the budgeted performance.

Cost reports: Cost reports are those reports that provides information about all the costs

incurred by the business in performing its normal course of actions. Cost reports are

useful for the managers to determine the need of the funds and other financial resources

in the business and developing their strategies to make the company more cost effective.

In this regard, the management accounting reporting is also an essential part of the

management accounting.

Critical evaluation of management accounting system and management accounting

reporting

Both management accounting system and management accounting reporting helps the

business in maintaining the efficiency in all the operations of the company. Adoption of

management accounting system and preparing management accounting reports can help the

managers in enhancing its financial position in the market.

On the other hand, if the company wants involve the management accounting system

and management accounting reporting in the business, it has to incur a huge expenditure in this

4

There are various methods through with the help of which the managers can prepare

various management accounting reports (Hopper and Bui, 2016). Some of the important

methods of management accounting reporting are as under:

Budget reports: These are the reports that provides the information about the estimated

activities of the company. With the help of these reports the managers can maintain

sufficiency of each resources of the company. Further, by comparing these reports with

the actual performance of the firm, the managers can analyse the efficiency of the

business and develop more effective strategies and plan for the company as well.

Financial reports: Financial reports of the company contains information about all the

financial transactions of the business. With the help of these reports, the managers can

analyse all the activities of the business (TYPES OF MANAGERIAL ACCOUNTING

REPORTS, 2019). These provides all the relevant information to the managers which

are required by them as to analyse overall performance of the business.

Performance reports: These reports includes information about the overall

performance of the business. These reports are prepared by comparing the actual

performance of the business with the budgeted performance.

Cost reports: Cost reports are those reports that provides information about all the costs

incurred by the business in performing its normal course of actions. Cost reports are

useful for the managers to determine the need of the funds and other financial resources

in the business and developing their strategies to make the company more cost effective.

In this regard, the management accounting reporting is also an essential part of the

management accounting.

Critical evaluation of management accounting system and management accounting

reporting

Both management accounting system and management accounting reporting helps the

business in maintaining the efficiency in all the operations of the company. Adoption of

management accounting system and preparing management accounting reports can help the

managers in enhancing its financial position in the market.

On the other hand, if the company wants involve the management accounting system

and management accounting reporting in the business, it has to incur a huge expenditure in this

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

regard.

From the above analysis it can be evaluated that although management accounting

reporting and management accounting system needs a huge cost and time of the managers as

well, but with the help of these systems, the company can enhance its ability to generate more

profit from the business operations through which the even the extra cost incurred by the

business could be easily recovered.

LO 2

3. Preparation of income statement using different management accounting techniques

There are different techniques that can be adopted by the finance managers for the

purpose of preparing their financial reports. Although, due to the difference in the methods of

calculations, each technique may provide different result of profit for the business.

The main techniques of management accounting for preparation of financial reports are

as under:

Marginal costing: It is the method in which while determining the cost of production,

each variable cost incurred by the business are considered as the product cost and all the

fixed costs are considered as the period cost (George, 2016). Due to exclusion of fixed

cost from the product cost, this methods results in providing higher amount of profit for

the business.

Absorption costing: Absorption costing is that method of management accounting in

which each cost incurred by the business while producing the products or services are

being considered as the product cost and included in the calculation of the cost of

production. In this regard, this method provided lower amount of profit to the company.

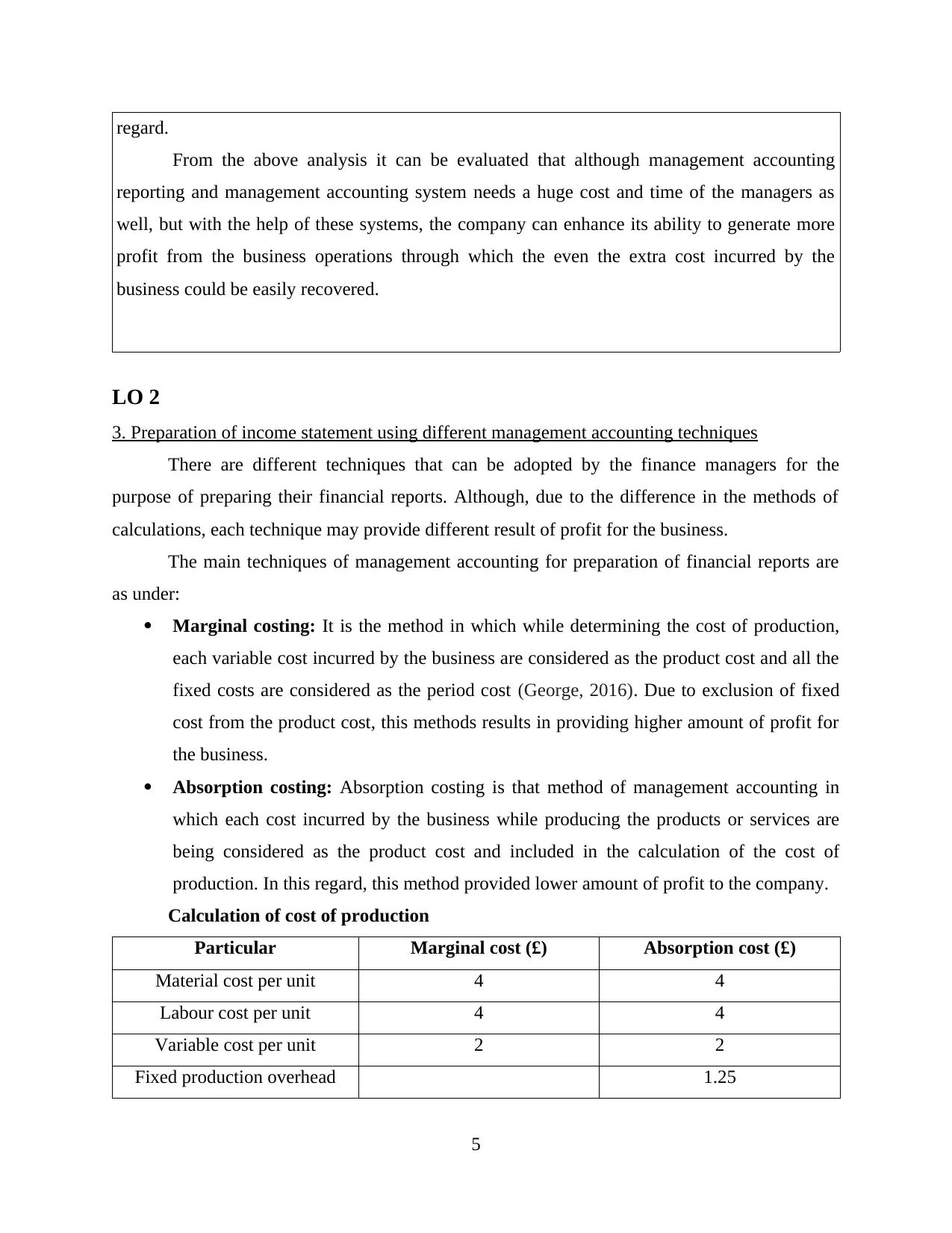

Calculation of cost of production

Particular Marginal cost (£) Absorption cost (£)

Material cost per unit 4 4

Labour cost per unit 4 4

Variable cost per unit 2 2

Fixed production overhead 1.25

5

From the above analysis it can be evaluated that although management accounting

reporting and management accounting system needs a huge cost and time of the managers as

well, but with the help of these systems, the company can enhance its ability to generate more

profit from the business operations through which the even the extra cost incurred by the

business could be easily recovered.

LO 2

3. Preparation of income statement using different management accounting techniques

There are different techniques that can be adopted by the finance managers for the

purpose of preparing their financial reports. Although, due to the difference in the methods of

calculations, each technique may provide different result of profit for the business.

The main techniques of management accounting for preparation of financial reports are

as under:

Marginal costing: It is the method in which while determining the cost of production,

each variable cost incurred by the business are considered as the product cost and all the

fixed costs are considered as the period cost (George, 2016). Due to exclusion of fixed

cost from the product cost, this methods results in providing higher amount of profit for

the business.

Absorption costing: Absorption costing is that method of management accounting in

which each cost incurred by the business while producing the products or services are

being considered as the product cost and included in the calculation of the cost of

production. In this regard, this method provided lower amount of profit to the company.

Calculation of cost of production

Particular Marginal cost (£) Absorption cost (£)

Material cost per unit 4 4

Labour cost per unit 4 4

Variable cost per unit 2 2

Fixed production overhead 1.25

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Other fixed overheads 2.5

10 13.75

Income statement from marginal costing technique

Particulars Amount

Sales £600,000.00

Less: Material cost £160,000.00

Labour cost £160,000.00

£280,000.00

Variable cost £80,000.00

Contribution £200,000.00

income statement from absorption costing technique

Particulars Amount

Sales £600,000.00

Less: Material cost £160,000.00

Labour cost £160,000.00

Gross profit £280,000.00

Variable cost £80,000.00

Fixed production cost £50,000.00

Other fixed costs £100,000.00

Net profit £50,000.00

Interpretation

From the above calculations it can be analysed that in the marginal costing method, the

fixed cost are not considered while calculating cost of production. On the other hand all costs od

production are considered while calculating the cost of production in the absorption costing

method. Further, the marginal costing provides higher amount of profit than the absorption

costing technique.

Captify

6

10 13.75

Income statement from marginal costing technique

Particulars Amount

Sales £600,000.00

Less: Material cost £160,000.00

Labour cost £160,000.00

£280,000.00

Variable cost £80,000.00

Contribution £200,000.00

income statement from absorption costing technique

Particulars Amount

Sales £600,000.00

Less: Material cost £160,000.00

Labour cost £160,000.00

Gross profit £280,000.00

Variable cost £80,000.00

Fixed production cost £50,000.00

Other fixed costs £100,000.00

Net profit £50,000.00

Interpretation

From the above calculations it can be analysed that in the marginal costing method, the

fixed cost are not considered while calculating cost of production. On the other hand all costs od

production are considered while calculating the cost of production in the absorption costing

method. Further, the marginal costing provides higher amount of profit than the absorption

costing technique.

Captify

6

To,

the line manager,

subject: For providing information about the role and functions of management accounts

department.

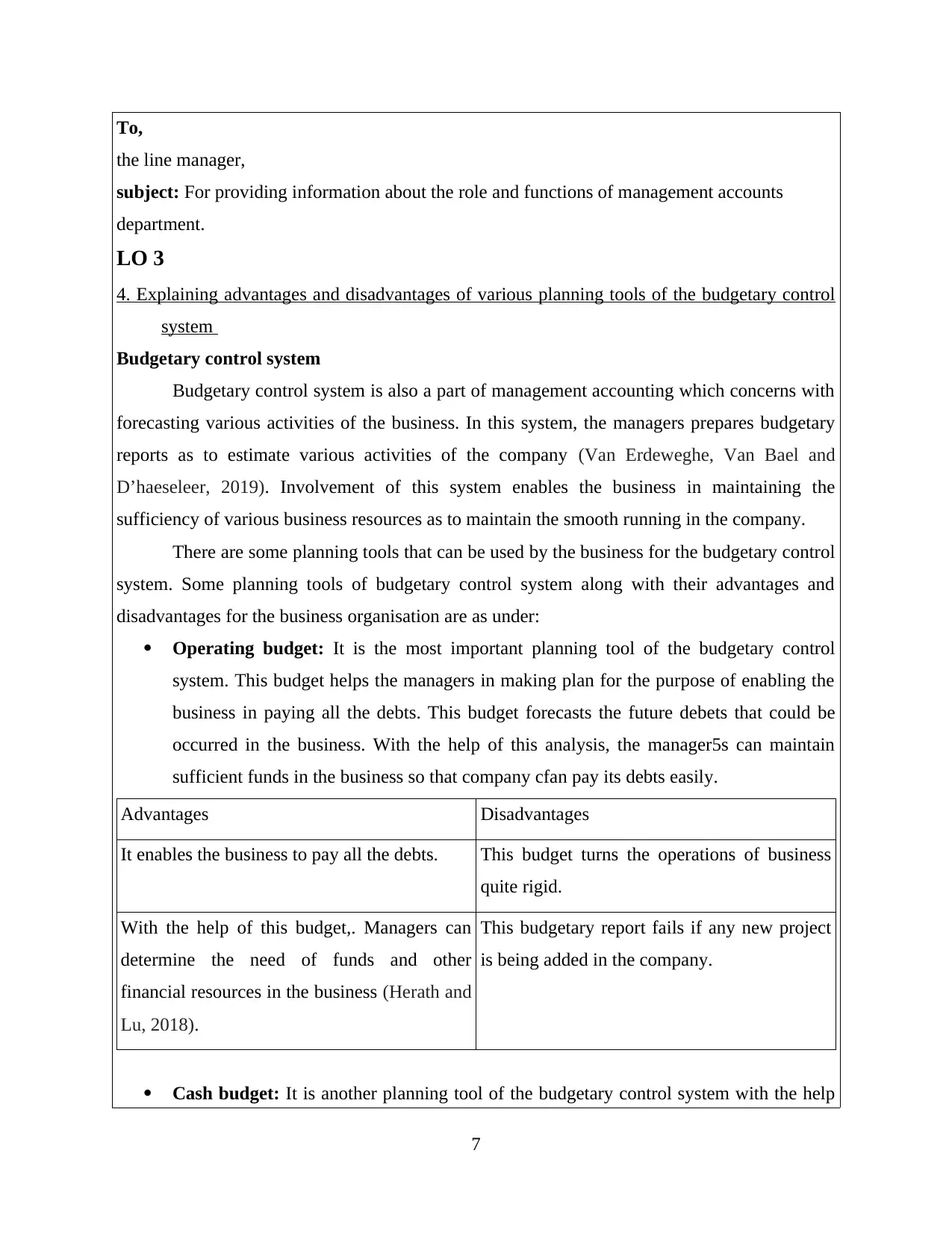

LO 3

4. Explaining advantages and disadvantages of various planning tools of the budgetary control

system

Budgetary control system

Budgetary control system is also a part of management accounting which concerns with

forecasting various activities of the business. In this system, the managers prepares budgetary

reports as to estimate various activities of the company (Van Erdeweghe, Van Bael and

D’haeseleer, 2019). Involvement of this system enables the business in maintaining the

sufficiency of various business resources as to maintain the smooth running in the company.

There are some planning tools that can be used by the business for the budgetary control

system. Some planning tools of budgetary control system along with their advantages and

disadvantages for the business organisation are as under:

Operating budget: It is the most important planning tool of the budgetary control

system. This budget helps the managers in making plan for the purpose of enabling the

business in paying all the debts. This budget forecasts the future debets that could be

occurred in the business. With the help of this analysis, the manager5s can maintain

sufficient funds in the business so that company cfan pay its debts easily.

Advantages Disadvantages

It enables the business to pay all the debts. This budget turns the operations of business

quite rigid.

With the help of this budget,. Managers can

determine the need of funds and other

financial resources in the business (Herath and

Lu, 2018).

This budgetary report fails if any new project

is being added in the company.

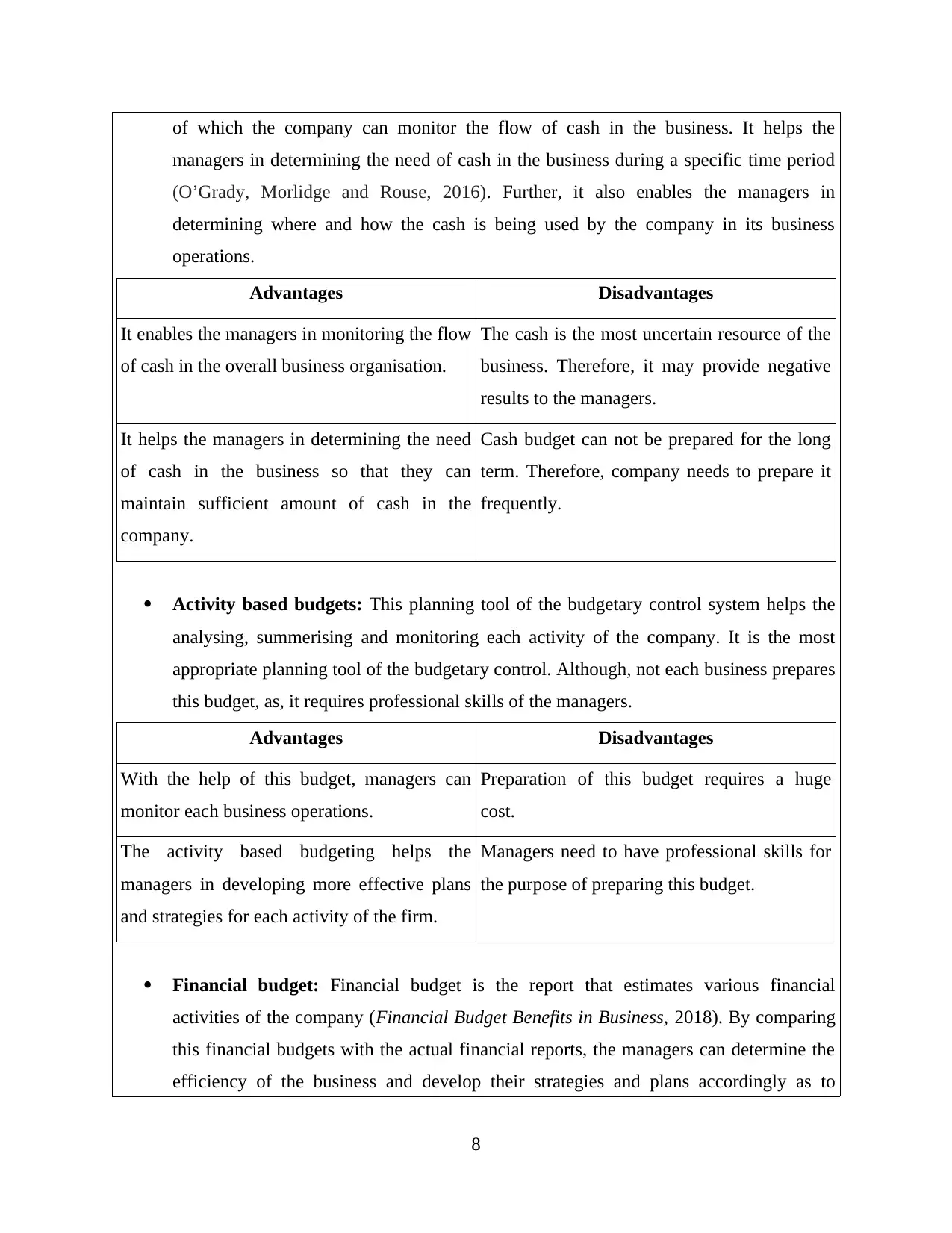

Cash budget: It is another planning tool of the budgetary control system with the help

7

the line manager,

subject: For providing information about the role and functions of management accounts

department.

LO 3

4. Explaining advantages and disadvantages of various planning tools of the budgetary control

system

Budgetary control system

Budgetary control system is also a part of management accounting which concerns with

forecasting various activities of the business. In this system, the managers prepares budgetary

reports as to estimate various activities of the company (Van Erdeweghe, Van Bael and

D’haeseleer, 2019). Involvement of this system enables the business in maintaining the

sufficiency of various business resources as to maintain the smooth running in the company.

There are some planning tools that can be used by the business for the budgetary control

system. Some planning tools of budgetary control system along with their advantages and

disadvantages for the business organisation are as under:

Operating budget: It is the most important planning tool of the budgetary control

system. This budget helps the managers in making plan for the purpose of enabling the

business in paying all the debts. This budget forecasts the future debets that could be

occurred in the business. With the help of this analysis, the manager5s can maintain

sufficient funds in the business so that company cfan pay its debts easily.

Advantages Disadvantages

It enables the business to pay all the debts. This budget turns the operations of business

quite rigid.

With the help of this budget,. Managers can

determine the need of funds and other

financial resources in the business (Herath and

Lu, 2018).

This budgetary report fails if any new project

is being added in the company.

Cash budget: It is another planning tool of the budgetary control system with the help

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of which the company can monitor the flow of cash in the business. It helps the

managers in determining the need of cash in the business during a specific time period

(O’Grady, Morlidge and Rouse, 2016). Further, it also enables the managers in

determining where and how the cash is being used by the company in its business

operations.

Advantages Disadvantages

It enables the managers in monitoring the flow

of cash in the overall business organisation.

The cash is the most uncertain resource of the

business. Therefore, it may provide negative

results to the managers.

It helps the managers in determining the need

of cash in the business so that they can

maintain sufficient amount of cash in the

company.

Cash budget can not be prepared for the long

term. Therefore, company needs to prepare it

frequently.

Activity based budgets: This planning tool of the budgetary control system helps the

analysing, summerising and monitoring each activity of the company. It is the most

appropriate planning tool of the budgetary control. Although, not each business prepares

this budget, as, it requires professional skills of the managers.

Advantages Disadvantages

With the help of this budget, managers can

monitor each business operations.

Preparation of this budget requires a huge

cost.

The activity based budgeting helps the

managers in developing more effective plans

and strategies for each activity of the firm.

Managers need to have professional skills for

the purpose of preparing this budget.

Financial budget: Financial budget is the report that estimates various financial

activities of the company (Financial Budget Benefits in Business, 2018). By comparing

this financial budgets with the actual financial reports, the managers can determine the

efficiency of the business and develop their strategies and plans accordingly as to

8

managers in determining the need of cash in the business during a specific time period

(O’Grady, Morlidge and Rouse, 2016). Further, it also enables the managers in

determining where and how the cash is being used by the company in its business

operations.

Advantages Disadvantages

It enables the managers in monitoring the flow

of cash in the overall business organisation.

The cash is the most uncertain resource of the

business. Therefore, it may provide negative

results to the managers.

It helps the managers in determining the need

of cash in the business so that they can

maintain sufficient amount of cash in the

company.

Cash budget can not be prepared for the long

term. Therefore, company needs to prepare it

frequently.

Activity based budgets: This planning tool of the budgetary control system helps the

analysing, summerising and monitoring each activity of the company. It is the most

appropriate planning tool of the budgetary control. Although, not each business prepares

this budget, as, it requires professional skills of the managers.

Advantages Disadvantages

With the help of this budget, managers can

monitor each business operations.

Preparation of this budget requires a huge

cost.

The activity based budgeting helps the

managers in developing more effective plans

and strategies for each activity of the firm.

Managers need to have professional skills for

the purpose of preparing this budget.

Financial budget: Financial budget is the report that estimates various financial

activities of the company (Financial Budget Benefits in Business, 2018). By comparing

this financial budgets with the actual financial reports, the managers can determine the

efficiency of the business and develop their strategies and plans accordingly as to

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

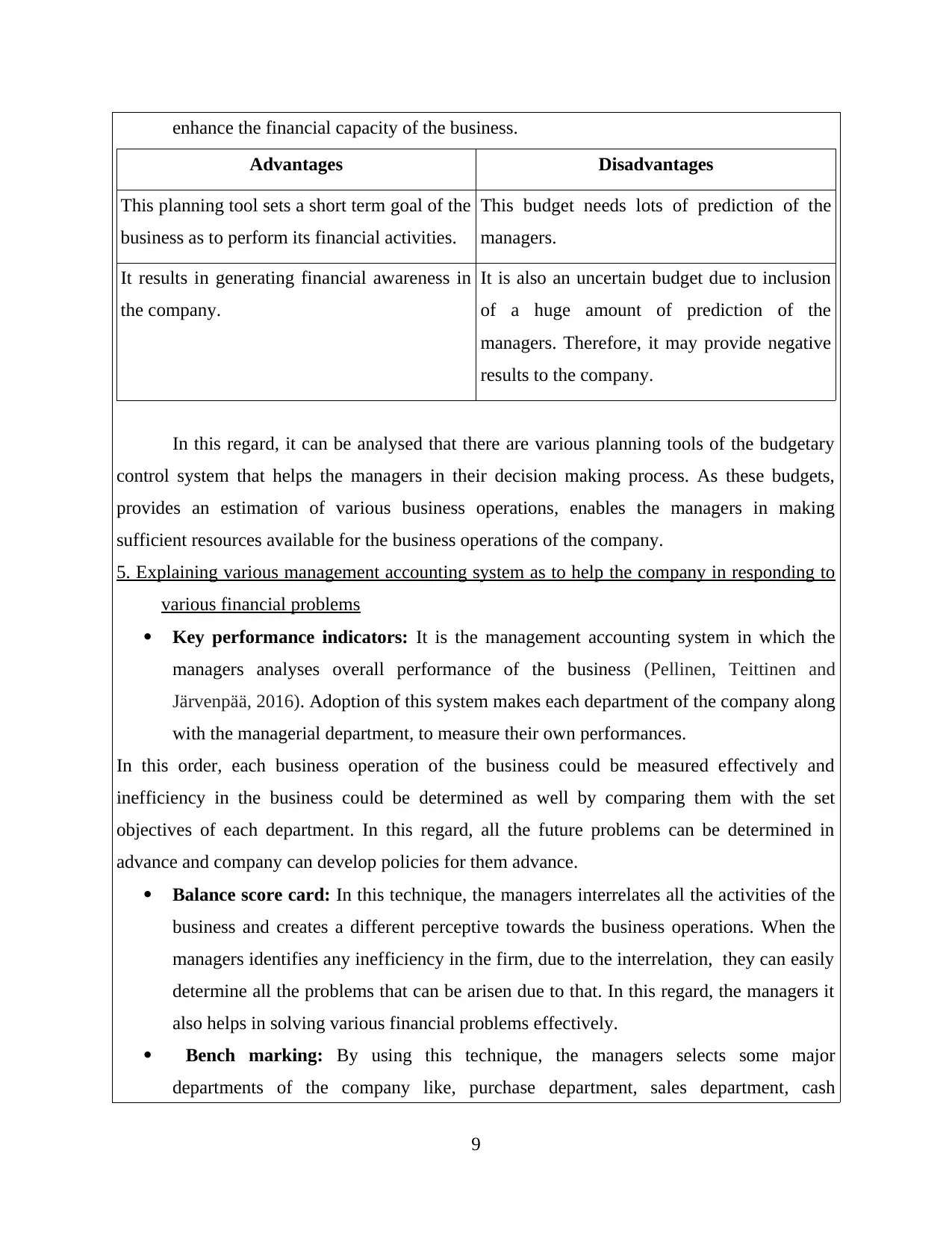

enhance the financial capacity of the business.

Advantages Disadvantages

This planning tool sets a short term goal of the

business as to perform its financial activities.

This budget needs lots of prediction of the

managers.

It results in generating financial awareness in

the company.

It is also an uncertain budget due to inclusion

of a huge amount of prediction of the

managers. Therefore, it may provide negative

results to the company.

In this regard, it can be analysed that there are various planning tools of the budgetary

control system that helps the managers in their decision making process. As these budgets,

provides an estimation of various business operations, enables the managers in making

sufficient resources available for the business operations of the company.

5. Explaining various management accounting system as to help the company in responding to

various financial problems

Key performance indicators: It is the management accounting system in which the

managers analyses overall performance of the business (Pellinen, Teittinen and

Järvenpää, 2016). Adoption of this system makes each department of the company along

with the managerial department, to measure their own performances.

In this order, each business operation of the business could be measured effectively and

inefficiency in the business could be determined as well by comparing them with the set

objectives of each department. In this regard, all the future problems can be determined in

advance and company can develop policies for them advance.

Balance score card: In this technique, the managers interrelates all the activities of the

business and creates a different perceptive towards the business operations. When the

managers identifies any inefficiency in the firm, due to the interrelation, they can easily

determine all the problems that can be arisen due to that. In this regard, the managers it

also helps in solving various financial problems effectively.

Bench marking: By using this technique, the managers selects some major

departments of the company like, purchase department, sales department, cash

9

Advantages Disadvantages

This planning tool sets a short term goal of the

business as to perform its financial activities.

This budget needs lots of prediction of the

managers.

It results in generating financial awareness in

the company.

It is also an uncertain budget due to inclusion

of a huge amount of prediction of the

managers. Therefore, it may provide negative

results to the company.

In this regard, it can be analysed that there are various planning tools of the budgetary

control system that helps the managers in their decision making process. As these budgets,

provides an estimation of various business operations, enables the managers in making

sufficient resources available for the business operations of the company.

5. Explaining various management accounting system as to help the company in responding to

various financial problems

Key performance indicators: It is the management accounting system in which the

managers analyses overall performance of the business (Pellinen, Teittinen and

Järvenpää, 2016). Adoption of this system makes each department of the company along

with the managerial department, to measure their own performances.

In this order, each business operation of the business could be measured effectively and

inefficiency in the business could be determined as well by comparing them with the set

objectives of each department. In this regard, all the future problems can be determined in

advance and company can develop policies for them advance.

Balance score card: In this technique, the managers interrelates all the activities of the

business and creates a different perceptive towards the business operations. When the

managers identifies any inefficiency in the firm, due to the interrelation, they can easily

determine all the problems that can be arisen due to that. In this regard, the managers it

also helps in solving various financial problems effectively.

Bench marking: By using this technique, the managers selects some major

departments of the company like, purchase department, sales department, cash

9

department, etc. and starts managing those selected departments only.

In this order, this technique reduces the burden of managers and enhance and enhance their

efficiency as well (Chiarini and Vagnoni, 2015). Financial problems are detected by

identification if inefficiency in any of the selected department and develop plans and strategies

for that as well.

In this order, these management accounting techniques helps the managers in enabling

the business as to respond to various financial problems by detecting them in advance and

develop plans for them as well.

CONCLUSION

From the above study, it can be analysed that the management accounting system is an

important part of the company. Involvement of management accounting system and management

accounting reporting can help the business in enhancing their financial capabilities. Further, there

are various methods of preparing income statements of management accounting. A business

should choose the most appropriate method to get the best results. Further, there are various

planning tools with the help of which managers can effectively perform their managerial

functions. The study has also concluded that there are numerous techniques with the help of

which the company can effectively identify the inefficiency in the business and become able to

effectively respond to various financial problems.

10

In this order, this technique reduces the burden of managers and enhance and enhance their

efficiency as well (Chiarini and Vagnoni, 2015). Financial problems are detected by

identification if inefficiency in any of the selected department and develop plans and strategies

for that as well.

In this order, these management accounting techniques helps the managers in enabling

the business as to respond to various financial problems by detecting them in advance and

develop plans for them as well.

CONCLUSION

From the above study, it can be analysed that the management accounting system is an

important part of the company. Involvement of management accounting system and management

accounting reporting can help the business in enhancing their financial capabilities. Further, there

are various methods of preparing income statements of management accounting. A business

should choose the most appropriate method to get the best results. Further, there are various

planning tools with the help of which managers can effectively perform their managerial

functions. The study has also concluded that there are numerous techniques with the help of

which the company can effectively identify the inefficiency in the business and become able to

effectively respond to various financial problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.