Oshodi Plc: Management Accounting Systems and Techniques Report

VerifiedAdded on 2021/02/20

|14

|4661

|41

Report

AI Summary

This report provides a comprehensive analysis of management accounting systems and techniques applied to Oshodi Plc, a manufacturing company producing JOJO fruit juice. The report begins with an introduction to management accounting, defining its role in financial statement preparation and stakeholder analysis. It explores various management accounting systems, including job costing, cost accounting, and inventory systems, evaluating their advantages and disadvantages. The report further discusses different methods used for management accounting reporting, such as budget reports, job cost reports, and accounts receivable reports, and highlights the benefits of these systems within an organization. Additionally, the report provides a detailed calculation of income statements under both marginal costing and absorption costing methods, offering a comparative analysis of these costing techniques. The report also includes calculations for March and April using both marginal and absorption costing.

Management Accounting

Systems and Techniques

Systems and Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

It can be defined as those systems which help in preparation of Financial Statements. These

systems are generally used in order to prepare various financial reports for the company's

stakeholders. These reports are needed by stakeholders of company to analyse financial

performance. There are various tools and techniques are used in preparation of various financial

reports (Management Accounting Systems, 2019). There are several systems such as cost accounting

systems, financial accounting systems, Business accounting system etc. Oshodi Plc is a

manufacturing company who is engaged in mainly production of JOJO fruit juice. Company wants

to prepare financial reports to evaluate financial position of company at time of production of JOJO

fruit juice. The report includes all the Budgetary control planning can be used by company to

control the extra cost allocation by setting up standard budgets. It also includes the various

techniques to resolve the financial issues in company by using the best technique for company. It

also help in knowing Oshodi that which costing method will be presenting better net profits for

company. Thus, report covers all the management accounting tools and techniques can be used by

company to know the financial condition of company. It will also help investors in evaluating and

making analysis on company's financial position.

LO 1

P 1 Definition of MA and requirement of different types of MA systems

It is defined as the method where financial statements are prepared by company to analyse

their financial performance. It main aim is to record all the monetary transactions in books of

accounts (Kaplan, 2015). MA is the method where all transactions related to finance are identified,

analysed, summarized and recorded in the books of accounts to interpret it and develop annual

reports. It helps management in taking short term or long term decisions for Oshodi Plc. There are

three types of financial management such as tac, financial and management accounting. It also helps

management in taking decision related to cost reduction and cost elimination. By examining where

the extra are more and it is necessary or not to allocate the expense in that particular department.

This also help in preparation of various strategies and business growth models.

Management Accounting systems are required in oshodi Plc in order to prepare Financial

Statements by using suitable systems. The various systems are described below:-

Job Costing System

This system helps in knowing the various calculation of job departments in company. It

helps in allocation of different costs in particular department as per the need of cost in that

department. It also help in examining extra cost allocated in different department and avoid that

It can be defined as those systems which help in preparation of Financial Statements. These

systems are generally used in order to prepare various financial reports for the company's

stakeholders. These reports are needed by stakeholders of company to analyse financial

performance. There are various tools and techniques are used in preparation of various financial

reports (Management Accounting Systems, 2019). There are several systems such as cost accounting

systems, financial accounting systems, Business accounting system etc. Oshodi Plc is a

manufacturing company who is engaged in mainly production of JOJO fruit juice. Company wants

to prepare financial reports to evaluate financial position of company at time of production of JOJO

fruit juice. The report includes all the Budgetary control planning can be used by company to

control the extra cost allocation by setting up standard budgets. It also includes the various

techniques to resolve the financial issues in company by using the best technique for company. It

also help in knowing Oshodi that which costing method will be presenting better net profits for

company. Thus, report covers all the management accounting tools and techniques can be used by

company to know the financial condition of company. It will also help investors in evaluating and

making analysis on company's financial position.

LO 1

P 1 Definition of MA and requirement of different types of MA systems

It is defined as the method where financial statements are prepared by company to analyse

their financial performance. It main aim is to record all the monetary transactions in books of

accounts (Kaplan, 2015). MA is the method where all transactions related to finance are identified,

analysed, summarized and recorded in the books of accounts to interpret it and develop annual

reports. It helps management in taking short term or long term decisions for Oshodi Plc. There are

three types of financial management such as tac, financial and management accounting. It also helps

management in taking decision related to cost reduction and cost elimination. By examining where

the extra are more and it is necessary or not to allocate the expense in that particular department.

This also help in preparation of various strategies and business growth models.

Management Accounting systems are required in oshodi Plc in order to prepare Financial

Statements by using suitable systems. The various systems are described below:-

Job Costing System

This system helps in knowing the various calculation of job departments in company. It

helps in allocation of different costs in particular department as per the need of cost in that

department. It also help in examining extra cost allocated in different department and avoid that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

extra cost if it is not beneficial to company.

Advantages Disadvantages

This system help in examining extra cost

in every department (Kavanagh, 2017);

It is a basis for cost elimination or cost

reduction in all department of Oshodi

Plc;

It provides brief information about direct

material, direct labour, fixed and variable

overhead charged in the different

departments.

It is not suitable in small organization

where there are less number of

departments;

This system is very expensive and also

very expensive to implement in Oshodi

Plc;

Under this method, there is lack of job

standardization;

It needs more professional experts in

order to apply this method in any

organization.

Cost Accounting System

This is used under which total cost used in every department and total production cost of

products are been calculated. There is preparation of different types of cost sheets for every

department in order to know where is need of extra cost allocation. It help in cost effective in

Oshodi Plc. Thus, it helps in identifying direct and indirect expenses related to production of each

product is calculated.

Advantages Disadvantages

It helps in cost reduction in company by

evaluating extra cost allocated in every

department;

The method help in knowing under

which department there is under

absorbed or over absorbed cost;

It help in setting up the new price for

new products;

Facilitates determining of production

cost per unit.

This method very complex in nature and

takes a lot of time preparation of cost

sheets for each department (Fleischman,

2017);

It is very lengthy process for preparation

of cost sheets for each department;

It needs professional to prepare various

cost sheets for every department in

Oshodi Plc.

Inventory System

Inventory System refers to that system where different ledgers are preprepared for knowing

Advantages Disadvantages

This system help in examining extra cost

in every department (Kavanagh, 2017);

It is a basis for cost elimination or cost

reduction in all department of Oshodi

Plc;

It provides brief information about direct

material, direct labour, fixed and variable

overhead charged in the different

departments.

It is not suitable in small organization

where there are less number of

departments;

This system is very expensive and also

very expensive to implement in Oshodi

Plc;

Under this method, there is lack of job

standardization;

It needs more professional experts in

order to apply this method in any

organization.

Cost Accounting System

This is used under which total cost used in every department and total production cost of

products are been calculated. There is preparation of different types of cost sheets for every

department in order to know where is need of extra cost allocation. It help in cost effective in

Oshodi Plc. Thus, it helps in identifying direct and indirect expenses related to production of each

product is calculated.

Advantages Disadvantages

It helps in cost reduction in company by

evaluating extra cost allocated in every

department;

The method help in knowing under

which department there is under

absorbed or over absorbed cost;

It help in setting up the new price for

new products;

Facilitates determining of production

cost per unit.

This method very complex in nature and

takes a lot of time preparation of cost

sheets for each department (Fleischman,

2017);

It is very lengthy process for preparation

of cost sheets for each department;

It needs professional to prepare various

cost sheets for every department in

Oshodi Plc.

Inventory System

Inventory System refers to that system where different ledgers are preprepared for knowing

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

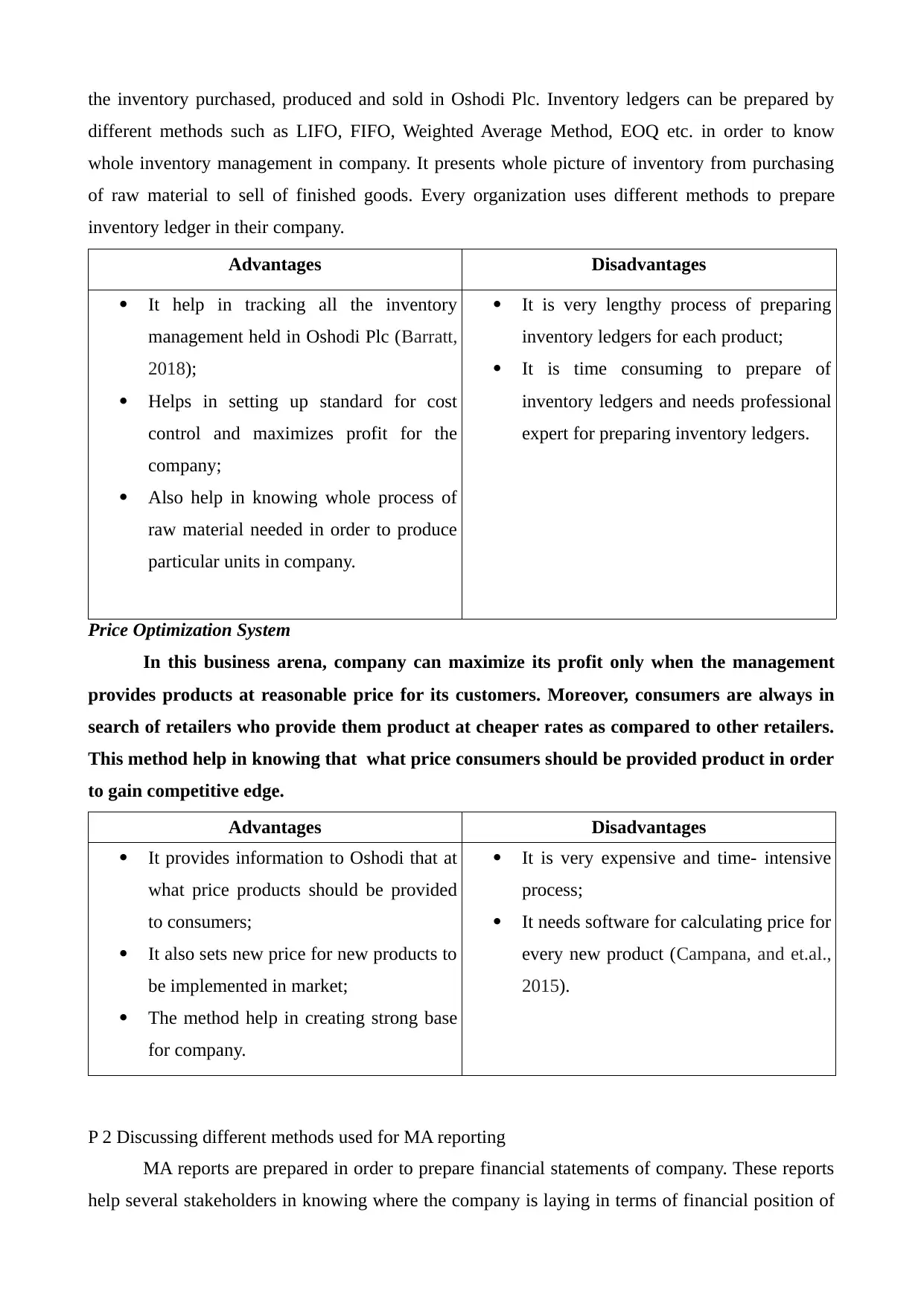

the inventory purchased, produced and sold in Oshodi Plc. Inventory ledgers can be prepared by

different methods such as LIFO, FIFO, Weighted Average Method, EOQ etc. in order to know

whole inventory management in company. It presents whole picture of inventory from purchasing

of raw material to sell of finished goods. Every organization uses different methods to prepare

inventory ledger in their company.

Advantages Disadvantages

It help in tracking all the inventory

management held in Oshodi Plc (Barratt,

2018);

Helps in setting up standard for cost

control and maximizes profit for the

company;

Also help in knowing whole process of

raw material needed in order to produce

particular units in company.

It is very lengthy process of preparing

inventory ledgers for each product;

It is time consuming to prepare of

inventory ledgers and needs professional

expert for preparing inventory ledgers.

Price Optimization System

In this business arena, company can maximize its profit only when the management

provides products at reasonable price for its customers. Moreover, consumers are always in

search of retailers who provide them product at cheaper rates as compared to other retailers.

This method help in knowing that what price consumers should be provided product in order

to gain competitive edge.

Advantages Disadvantages

It provides information to Oshodi that at

what price products should be provided

to consumers;

It also sets new price for new products to

be implemented in market;

The method help in creating strong base

for company.

It is very expensive and time- intensive

process;

It needs software for calculating price for

every new product (Campana, and et.al.,

2015).

P 2 Discussing different methods used for MA reporting

MA reports are prepared in order to prepare financial statements of company. These reports

help several stakeholders in knowing where the company is laying in terms of financial position of

different methods such as LIFO, FIFO, Weighted Average Method, EOQ etc. in order to know

whole inventory management in company. It presents whole picture of inventory from purchasing

of raw material to sell of finished goods. Every organization uses different methods to prepare

inventory ledger in their company.

Advantages Disadvantages

It help in tracking all the inventory

management held in Oshodi Plc (Barratt,

2018);

Helps in setting up standard for cost

control and maximizes profit for the

company;

Also help in knowing whole process of

raw material needed in order to produce

particular units in company.

It is very lengthy process of preparing

inventory ledgers for each product;

It is time consuming to prepare of

inventory ledgers and needs professional

expert for preparing inventory ledgers.

Price Optimization System

In this business arena, company can maximize its profit only when the management

provides products at reasonable price for its customers. Moreover, consumers are always in

search of retailers who provide them product at cheaper rates as compared to other retailers.

This method help in knowing that what price consumers should be provided product in order

to gain competitive edge.

Advantages Disadvantages

It provides information to Oshodi that at

what price products should be provided

to consumers;

It also sets new price for new products to

be implemented in market;

The method help in creating strong base

for company.

It is very expensive and time- intensive

process;

It needs software for calculating price for

every new product (Campana, and et.al.,

2015).

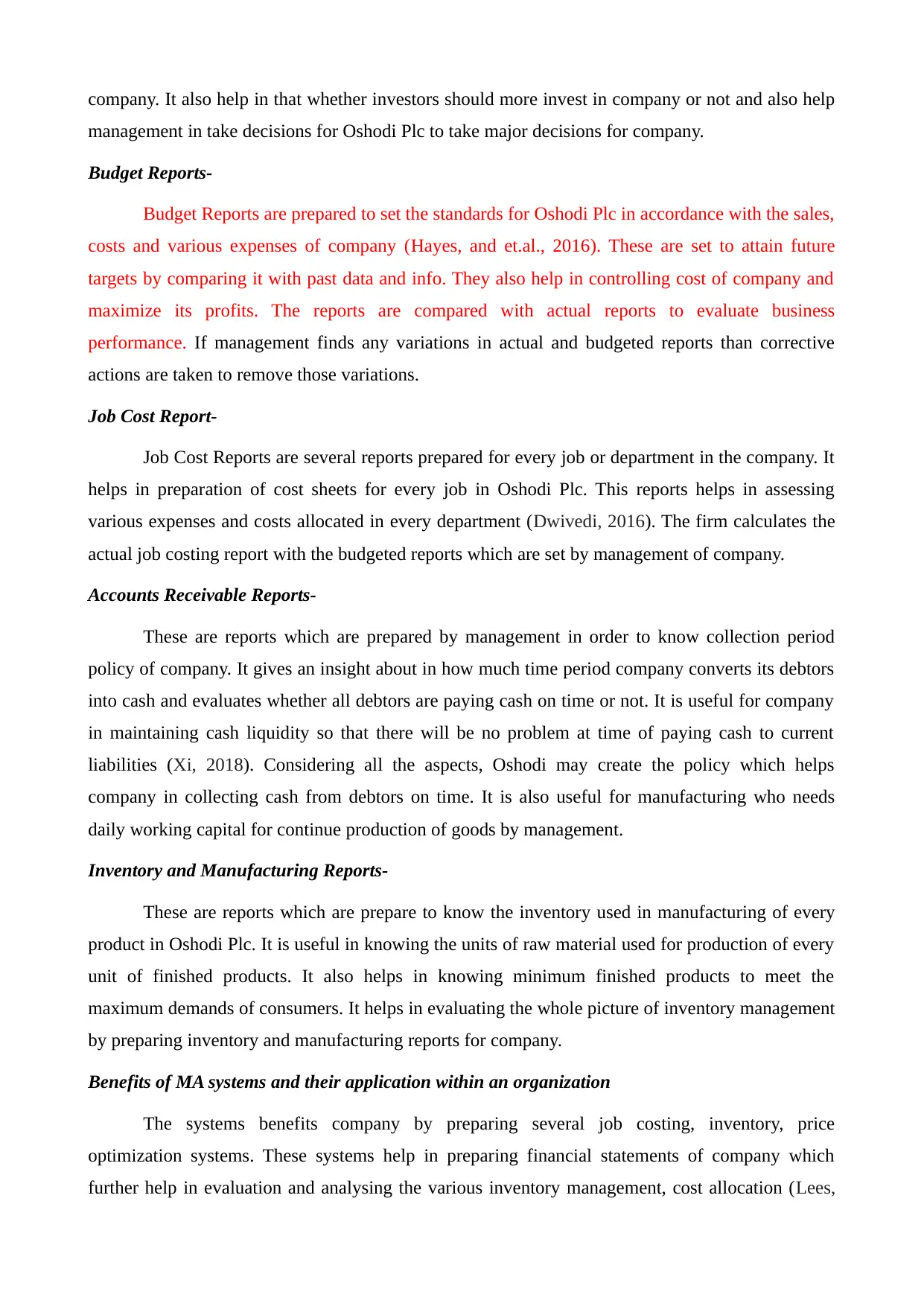

P 2 Discussing different methods used for MA reporting

MA reports are prepared in order to prepare financial statements of company. These reports

help several stakeholders in knowing where the company is laying in terms of financial position of

company. It also help in that whether investors should more invest in company or not and also help

management in take decisions for Oshodi Plc to take major decisions for company.

Budget Reports-

Budget Reports are prepared to set the standards for Oshodi Plc in accordance with the sales,

costs and various expenses of company (Hayes, and et.al., 2016). These are set to attain future

targets by comparing it with past data and info. They also help in controlling cost of company and

maximize its profits. The reports are compared with actual reports to evaluate business

performance. If management finds any variations in actual and budgeted reports than corrective

actions are taken to remove those variations.

Job Cost Report-

Job Cost Reports are several reports prepared for every job or department in the company. It

helps in preparation of cost sheets for every job in Oshodi Plc. This reports helps in assessing

various expenses and costs allocated in every department (Dwivedi, 2016). The firm calculates the

actual job costing report with the budgeted reports which are set by management of company.

Accounts Receivable Reports-

These are reports which are prepared by management in order to know collection period

policy of company. It gives an insight about in how much time period company converts its debtors

into cash and evaluates whether all debtors are paying cash on time or not. It is useful for company

in maintaining cash liquidity so that there will be no problem at time of paying cash to current

liabilities (Xi, 2018). Considering all the aspects, Oshodi may create the policy which helps

company in collecting cash from debtors on time. It is also useful for manufacturing who needs

daily working capital for continue production of goods by management.

Inventory and Manufacturing Reports-

These are reports which are prepare to know the inventory used in manufacturing of every

product in Oshodi Plc. It is useful in knowing the units of raw material used for production of every

unit of finished products. It also helps in knowing minimum finished products to meet the

maximum demands of consumers. It helps in evaluating the whole picture of inventory management

by preparing inventory and manufacturing reports for company.

Benefits of MA systems and their application within an organization

The systems benefits company by preparing several job costing, inventory, price

optimization systems. These systems help in preparing financial statements of company which

further help in evaluation and analysing the various inventory management, cost allocation (Lees,

management in take decisions for Oshodi Plc to take major decisions for company.

Budget Reports-

Budget Reports are prepared to set the standards for Oshodi Plc in accordance with the sales,

costs and various expenses of company (Hayes, and et.al., 2016). These are set to attain future

targets by comparing it with past data and info. They also help in controlling cost of company and

maximize its profits. The reports are compared with actual reports to evaluate business

performance. If management finds any variations in actual and budgeted reports than corrective

actions are taken to remove those variations.

Job Cost Report-

Job Cost Reports are several reports prepared for every job or department in the company. It

helps in preparation of cost sheets for every job in Oshodi Plc. This reports helps in assessing

various expenses and costs allocated in every department (Dwivedi, 2016). The firm calculates the

actual job costing report with the budgeted reports which are set by management of company.

Accounts Receivable Reports-

These are reports which are prepared by management in order to know collection period

policy of company. It gives an insight about in how much time period company converts its debtors

into cash and evaluates whether all debtors are paying cash on time or not. It is useful for company

in maintaining cash liquidity so that there will be no problem at time of paying cash to current

liabilities (Xi, 2018). Considering all the aspects, Oshodi may create the policy which helps

company in collecting cash from debtors on time. It is also useful for manufacturing who needs

daily working capital for continue production of goods by management.

Inventory and Manufacturing Reports-

These are reports which are prepare to know the inventory used in manufacturing of every

product in Oshodi Plc. It is useful in knowing the units of raw material used for production of every

unit of finished products. It also helps in knowing minimum finished products to meet the

maximum demands of consumers. It helps in evaluating the whole picture of inventory management

by preparing inventory and manufacturing reports for company.

Benefits of MA systems and their application within an organization

The systems benefits company by preparing several job costing, inventory, price

optimization systems. These systems help in preparing financial statements of company which

further help in evaluation and analysing the various inventory management, cost allocation (Lees,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2017). These systems are useful to apply in company so that Oshodi' s management can take short

term and long term decisions for company. They are also helpful in cost allocation and pricing new

products which are going to be introduced in market. These are applied in organization to have

information about every department and about every system in company.

LO 2

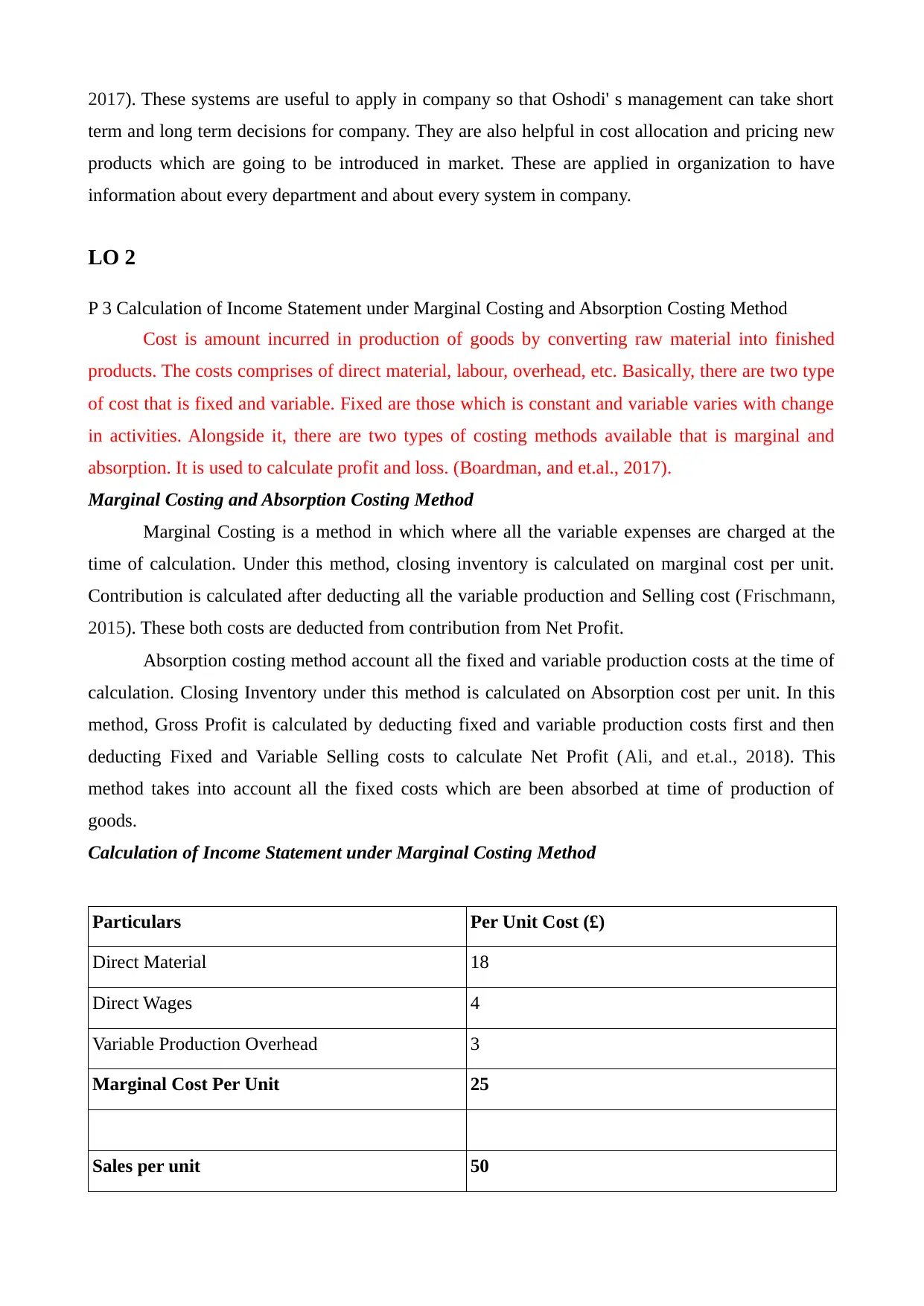

P 3 Calculation of Income Statement under Marginal Costing and Absorption Costing Method

Cost is amount incurred in production of goods by converting raw material into finished

products. The costs comprises of direct material, labour, overhead, etc. Basically, there are two type

of cost that is fixed and variable. Fixed are those which is constant and variable varies with change

in activities. Alongside it, there are two types of costing methods available that is marginal and

absorption. It is used to calculate profit and loss. (Boardman, and et.al., 2017).

Marginal Costing and Absorption Costing Method

Marginal Costing is a method in which where all the variable expenses are charged at the

time of calculation. Under this method, closing inventory is calculated on marginal cost per unit.

Contribution is calculated after deducting all the variable production and Selling cost (Frischmann,

2015). These both costs are deducted from contribution from Net Profit.

Absorption costing method account all the fixed and variable production costs at the time of

calculation. Closing Inventory under this method is calculated on Absorption cost per unit. In this

method, Gross Profit is calculated by deducting fixed and variable production costs first and then

deducting Fixed and Variable Selling costs to calculate Net Profit (Ali, and et.al., 2018). This

method takes into account all the fixed costs which are been absorbed at time of production of

goods.

Calculation of Income Statement under Marginal Costing Method

Particulars Per Unit Cost (£)

Direct Material 18

Direct Wages 4

Variable Production Overhead 3

Marginal Cost Per Unit 25

Sales per unit 50

term and long term decisions for company. They are also helpful in cost allocation and pricing new

products which are going to be introduced in market. These are applied in organization to have

information about every department and about every system in company.

LO 2

P 3 Calculation of Income Statement under Marginal Costing and Absorption Costing Method

Cost is amount incurred in production of goods by converting raw material into finished

products. The costs comprises of direct material, labour, overhead, etc. Basically, there are two type

of cost that is fixed and variable. Fixed are those which is constant and variable varies with change

in activities. Alongside it, there are two types of costing methods available that is marginal and

absorption. It is used to calculate profit and loss. (Boardman, and et.al., 2017).

Marginal Costing and Absorption Costing Method

Marginal Costing is a method in which where all the variable expenses are charged at the

time of calculation. Under this method, closing inventory is calculated on marginal cost per unit.

Contribution is calculated after deducting all the variable production and Selling cost (Frischmann,

2015). These both costs are deducted from contribution from Net Profit.

Absorption costing method account all the fixed and variable production costs at the time of

calculation. Closing Inventory under this method is calculated on Absorption cost per unit. In this

method, Gross Profit is calculated by deducting fixed and variable production costs first and then

deducting Fixed and Variable Selling costs to calculate Net Profit (Ali, and et.al., 2018). This

method takes into account all the fixed costs which are been absorbed at time of production of

goods.

Calculation of Income Statement under Marginal Costing Method

Particulars Per Unit Cost (£)

Direct Material 18

Direct Wages 4

Variable Production Overhead 3

Marginal Cost Per Unit 25

Sales per unit 50

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

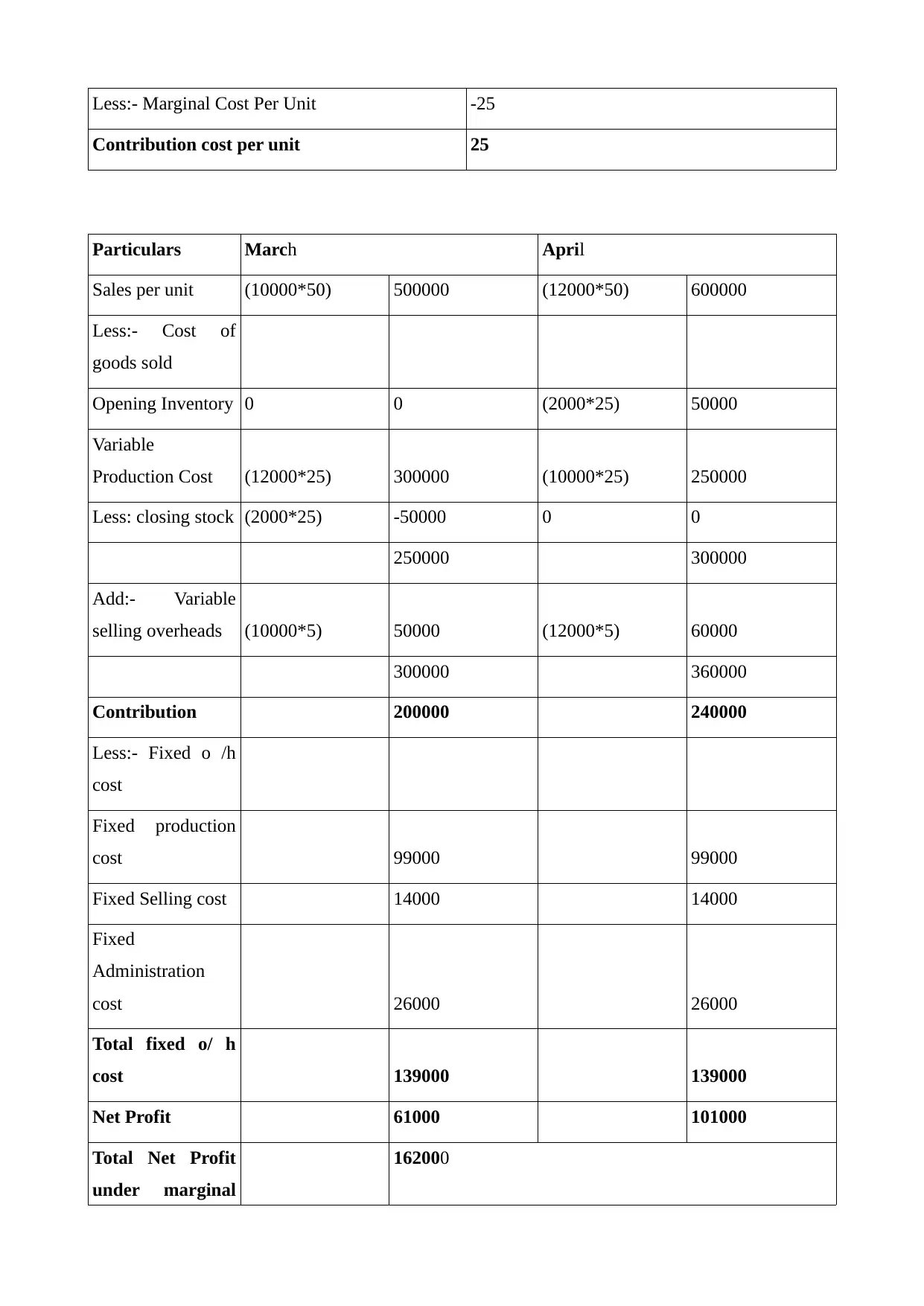

Less:- Marginal Cost Per Unit -25

Contribution cost per unit 25

Particulars March April

Sales per unit (10000*50) 500000 (12000*50) 600000

Less:- Cost of

goods sold

Opening Inventory 0 0 (2000*25) 50000

Variable

Production Cost (12000*25) 300000 (10000*25) 250000

Less: closing stock (2000*25) -50000 0 0

250000 300000

Add:- Variable

selling overheads (10000*5) 50000 (12000*5) 60000

300000 360000

Contribution 200000 240000

Less:- Fixed o /h

cost

Fixed production

cost 99000 99000

Fixed Selling cost 14000 14000

Fixed

Administration

cost 26000 26000

Total fixed o/ h

cost 139000 139000

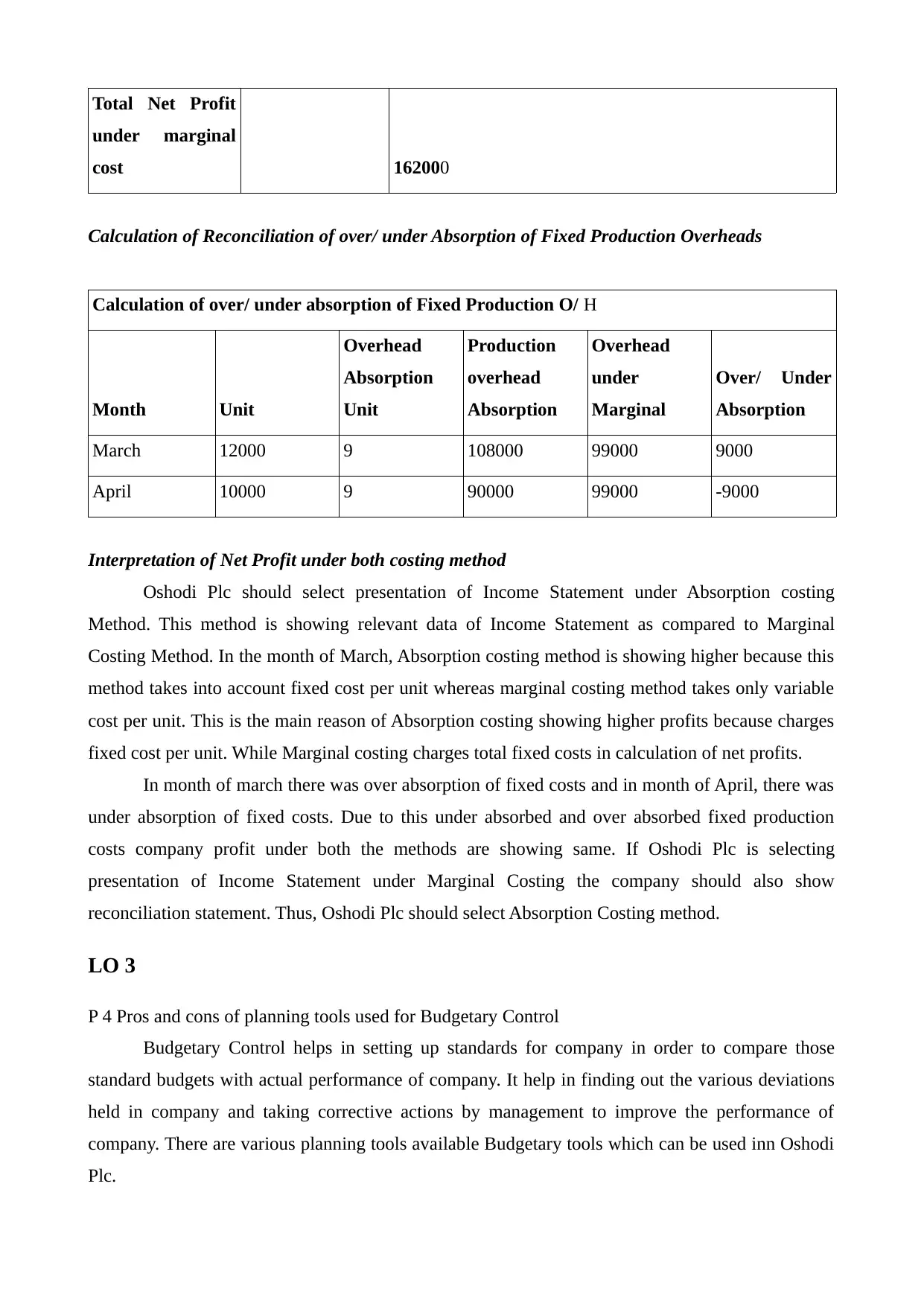

Net Profit 61000 101000

Total Net Profit

under marginal

162000

Contribution cost per unit 25

Particulars March April

Sales per unit (10000*50) 500000 (12000*50) 600000

Less:- Cost of

goods sold

Opening Inventory 0 0 (2000*25) 50000

Variable

Production Cost (12000*25) 300000 (10000*25) 250000

Less: closing stock (2000*25) -50000 0 0

250000 300000

Add:- Variable

selling overheads (10000*5) 50000 (12000*5) 60000

300000 360000

Contribution 200000 240000

Less:- Fixed o /h

cost

Fixed production

cost 99000 99000

Fixed Selling cost 14000 14000

Fixed

Administration

cost 26000 26000

Total fixed o/ h

cost 139000 139000

Net Profit 61000 101000

Total Net Profit

under marginal

162000

cost

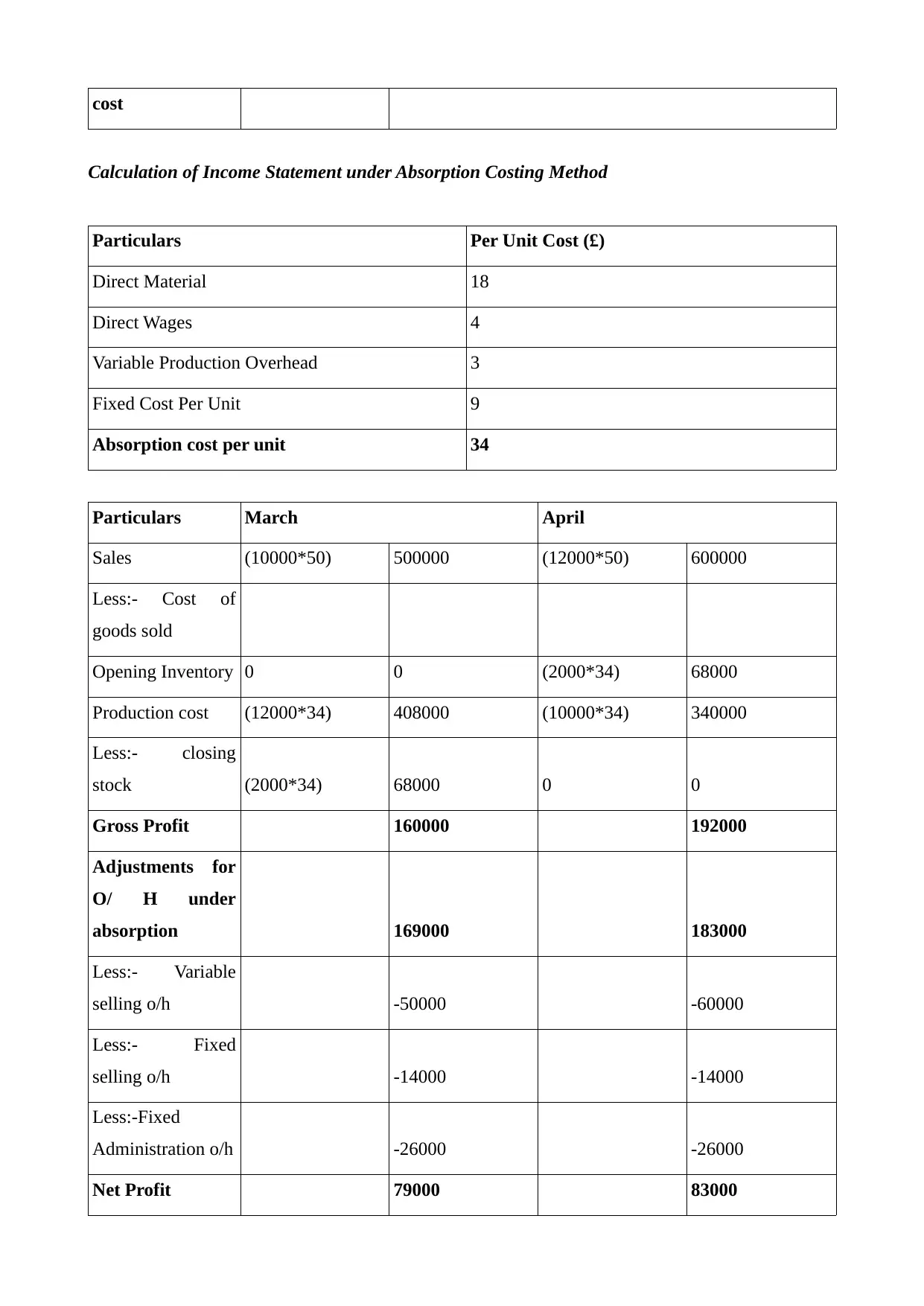

Calculation of Income Statement under Absorption Costing Method

Particulars Per Unit Cost (£)

Direct Material 18

Direct Wages 4

Variable Production Overhead 3

Fixed Cost Per Unit 9

Absorption cost per unit 34

Particulars March April

Sales (10000*50) 500000 (12000*50) 600000

Less:- Cost of

goods sold

Opening Inventory 0 0 (2000*34) 68000

Production cost (12000*34) 408000 (10000*34) 340000

Less:- closing

stock (2000*34) 68000 0 0

Gross Profit 160000 192000

Adjustments for

O/ H under

absorption 169000 183000

Less:- Variable

selling o/h -50000 -60000

Less:- Fixed

selling o/h -14000 -14000

Less:-Fixed

Administration o/h -26000 -26000

Net Profit 79000 83000

Calculation of Income Statement under Absorption Costing Method

Particulars Per Unit Cost (£)

Direct Material 18

Direct Wages 4

Variable Production Overhead 3

Fixed Cost Per Unit 9

Absorption cost per unit 34

Particulars March April

Sales (10000*50) 500000 (12000*50) 600000

Less:- Cost of

goods sold

Opening Inventory 0 0 (2000*34) 68000

Production cost (12000*34) 408000 (10000*34) 340000

Less:- closing

stock (2000*34) 68000 0 0

Gross Profit 160000 192000

Adjustments for

O/ H under

absorption 169000 183000

Less:- Variable

selling o/h -50000 -60000

Less:- Fixed

selling o/h -14000 -14000

Less:-Fixed

Administration o/h -26000 -26000

Net Profit 79000 83000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Total Net Profit

under marginal

cost 162000

Calculation of Reconciliation of over/ under Absorption of Fixed Production Overheads

Calculation of over/ under absorption of Fixed Production O/ H

Month Unit

Overhead

Absorption

Unit

Production

overhead

Absorption

Overhead

under

Marginal

Over/ Under

Absorption

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

Interpretation of Net Profit under both costing method

Oshodi Plc should select presentation of Income Statement under Absorption costing

Method. This method is showing relevant data of Income Statement as compared to Marginal

Costing Method. In the month of March, Absorption costing method is showing higher because this

method takes into account fixed cost per unit whereas marginal costing method takes only variable

cost per unit. This is the main reason of Absorption costing showing higher profits because charges

fixed cost per unit. While Marginal costing charges total fixed costs in calculation of net profits.

In month of march there was over absorption of fixed costs and in month of April, there was

under absorption of fixed costs. Due to this under absorbed and over absorbed fixed production

costs company profit under both the methods are showing same. If Oshodi Plc is selecting

presentation of Income Statement under Marginal Costing the company should also show

reconciliation statement. Thus, Oshodi Plc should select Absorption Costing method.

LO 3

P 4 Pros and cons of planning tools used for Budgetary Control

Budgetary Control helps in setting up standards for company in order to compare those

standard budgets with actual performance of company. It help in finding out the various deviations

held in company and taking corrective actions by management to improve the performance of

company. There are various planning tools available Budgetary tools which can be used inn Oshodi

Plc.

under marginal

cost 162000

Calculation of Reconciliation of over/ under Absorption of Fixed Production Overheads

Calculation of over/ under absorption of Fixed Production O/ H

Month Unit

Overhead

Absorption

Unit

Production

overhead

Absorption

Overhead

under

Marginal

Over/ Under

Absorption

March 12000 9 108000 99000 9000

April 10000 9 90000 99000 -9000

Interpretation of Net Profit under both costing method

Oshodi Plc should select presentation of Income Statement under Absorption costing

Method. This method is showing relevant data of Income Statement as compared to Marginal

Costing Method. In the month of March, Absorption costing method is showing higher because this

method takes into account fixed cost per unit whereas marginal costing method takes only variable

cost per unit. This is the main reason of Absorption costing showing higher profits because charges

fixed cost per unit. While Marginal costing charges total fixed costs in calculation of net profits.

In month of march there was over absorption of fixed costs and in month of April, there was

under absorption of fixed costs. Due to this under absorbed and over absorbed fixed production

costs company profit under both the methods are showing same. If Oshodi Plc is selecting

presentation of Income Statement under Marginal Costing the company should also show

reconciliation statement. Thus, Oshodi Plc should select Absorption Costing method.

LO 3

P 4 Pros and cons of planning tools used for Budgetary Control

Budgetary Control helps in setting up standards for company in order to compare those

standard budgets with actual performance of company. It help in finding out the various deviations

held in company and taking corrective actions by management to improve the performance of

company. There are various planning tools available Budgetary tools which can be used inn Oshodi

Plc.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

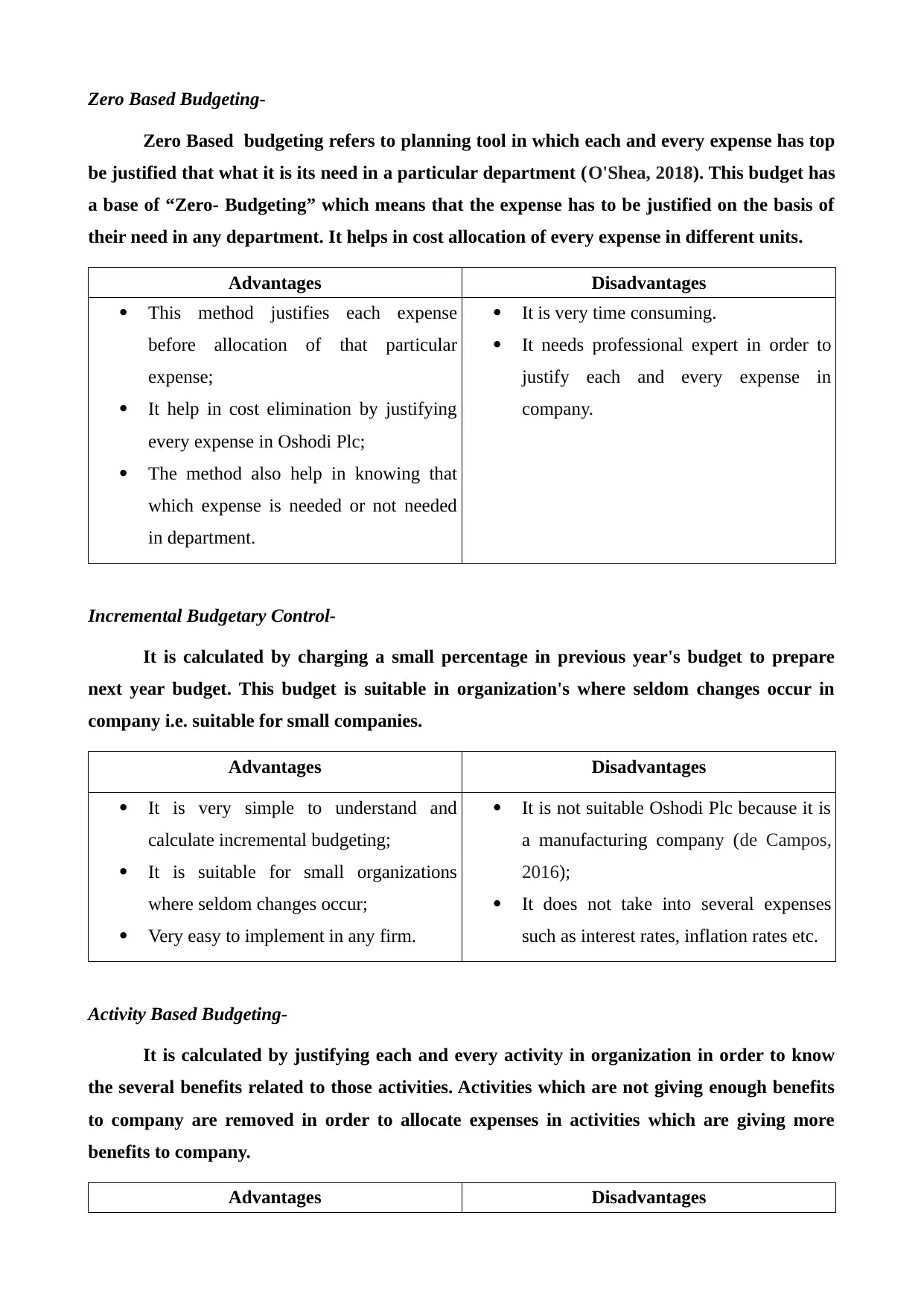

Zero Based Budgeting-

Zero Based budgeting refers to planning tool in which each and every expense has top

be justified that what it is its need in a particular department (O'Shea, 2018). This budget has

a base of “Zero- Budgeting” which means that the expense has to be justified on the basis of

their need in any department. It helps in cost allocation of every expense in different units.

Advantages Disadvantages

This method justifies each expense

before allocation of that particular

expense;

It help in cost elimination by justifying

every expense in Oshodi Plc;

The method also help in knowing that

which expense is needed or not needed

in department.

It is very time consuming.

It needs professional expert in order to

justify each and every expense in

company.

Incremental Budgetary Control-

It is calculated by charging a small percentage in previous year's budget to prepare

next year budget. This budget is suitable in organization's where seldom changes occur in

company i.e. suitable for small companies.

Advantages Disadvantages

It is very simple to understand and

calculate incremental budgeting;

It is suitable for small organizations

where seldom changes occur;

Very easy to implement in any firm.

It is not suitable Oshodi Plc because it is

a manufacturing company (de Campos,

2016);

It does not take into several expenses

such as interest rates, inflation rates etc.

Activity Based Budgeting-

It is calculated by justifying each and every activity in organization in order to know

the several benefits related to those activities. Activities which are not giving enough benefits

to company are removed in order to allocate expenses in activities which are giving more

benefits to company.

Advantages Disadvantages

Zero Based budgeting refers to planning tool in which each and every expense has top

be justified that what it is its need in a particular department (O'Shea, 2018). This budget has

a base of “Zero- Budgeting” which means that the expense has to be justified on the basis of

their need in any department. It helps in cost allocation of every expense in different units.

Advantages Disadvantages

This method justifies each expense

before allocation of that particular

expense;

It help in cost elimination by justifying

every expense in Oshodi Plc;

The method also help in knowing that

which expense is needed or not needed

in department.

It is very time consuming.

It needs professional expert in order to

justify each and every expense in

company.

Incremental Budgetary Control-

It is calculated by charging a small percentage in previous year's budget to prepare

next year budget. This budget is suitable in organization's where seldom changes occur in

company i.e. suitable for small companies.

Advantages Disadvantages

It is very simple to understand and

calculate incremental budgeting;

It is suitable for small organizations

where seldom changes occur;

Very easy to implement in any firm.

It is not suitable Oshodi Plc because it is

a manufacturing company (de Campos,

2016);

It does not take into several expenses

such as interest rates, inflation rates etc.

Activity Based Budgeting-

It is calculated by justifying each and every activity in organization in order to know

the several benefits related to those activities. Activities which are not giving enough benefits

to company are removed in order to allocate expenses in activities which are giving more

benefits to company.

Advantages Disadvantages

It justifies each and every activity which

is needed in company;

It help in determining extra cost

allocation for Oshodi Plc (Mahal, 2015);

It is also useful for differencing in

activities which are benefiting company

and which are not benefiting company.

It is expensive and time consuming method.

It needs expert to justify each and every activity

in Oshodi Plc;

This method very rigorous and can be applicable

large firms.

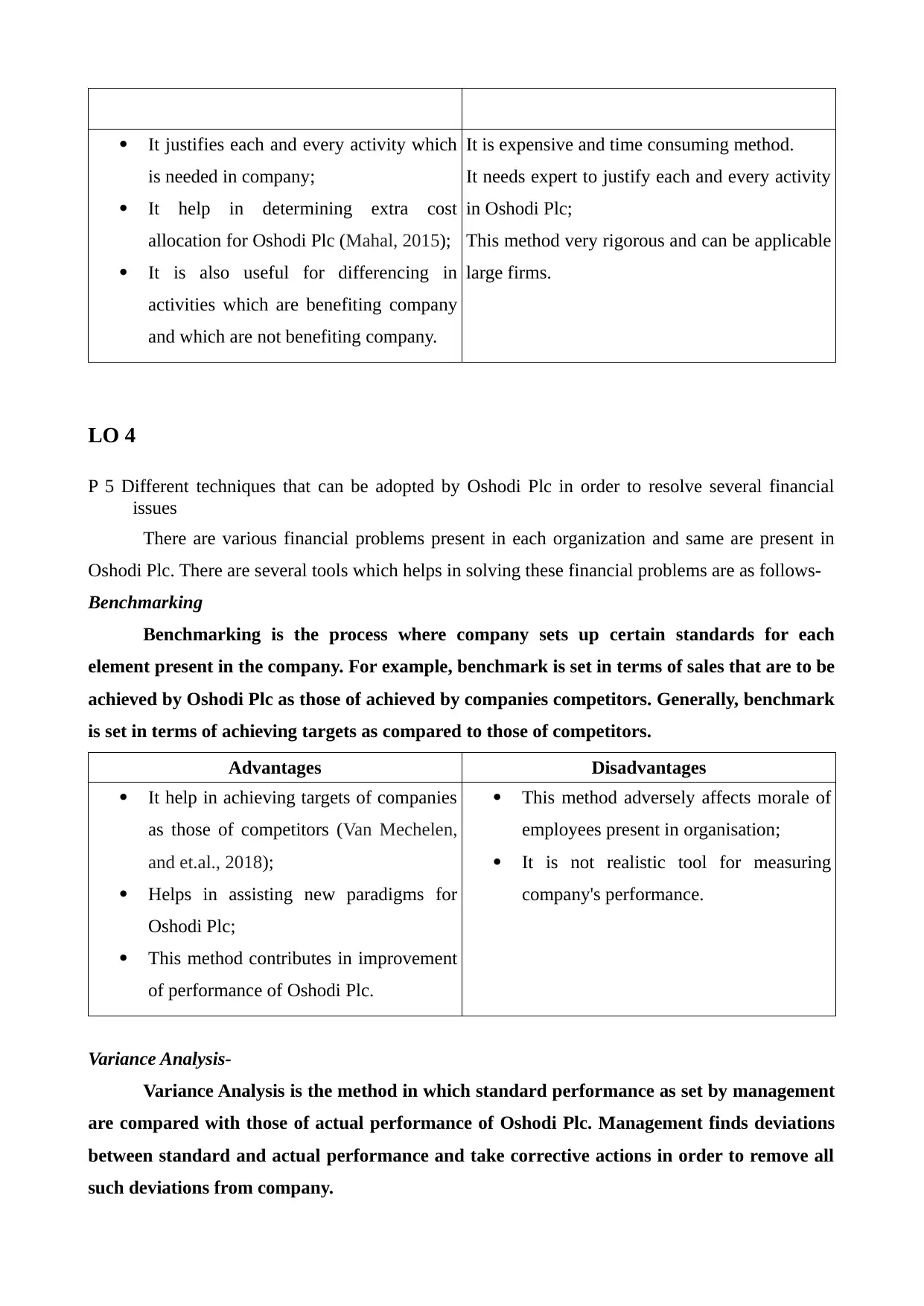

LO 4

P 5 Different techniques that can be adopted by Oshodi Plc in order to resolve several financial

issues

There are various financial problems present in each organization and same are present in

Oshodi Plc. There are several tools which helps in solving these financial problems are as follows-

Benchmarking

Benchmarking is the process where company sets up certain standards for each

element present in the company. For example, benchmark is set in terms of sales that are to be

achieved by Oshodi Plc as those of achieved by companies competitors. Generally, benchmark

is set in terms of achieving targets as compared to those of competitors.

Advantages Disadvantages

It help in achieving targets of companies

as those of competitors (Van Mechelen,

and et.al., 2018);

Helps in assisting new paradigms for

Oshodi Plc;

This method contributes in improvement

of performance of Oshodi Plc.

This method adversely affects morale of

employees present in organisation;

It is not realistic tool for measuring

company's performance.

Variance Analysis-

Variance Analysis is the method in which standard performance as set by management

are compared with those of actual performance of Oshodi Plc. Management finds deviations

between standard and actual performance and take corrective actions in order to remove all

such deviations from company.

is needed in company;

It help in determining extra cost

allocation for Oshodi Plc (Mahal, 2015);

It is also useful for differencing in

activities which are benefiting company

and which are not benefiting company.

It is expensive and time consuming method.

It needs expert to justify each and every activity

in Oshodi Plc;

This method very rigorous and can be applicable

large firms.

LO 4

P 5 Different techniques that can be adopted by Oshodi Plc in order to resolve several financial

issues

There are various financial problems present in each organization and same are present in

Oshodi Plc. There are several tools which helps in solving these financial problems are as follows-

Benchmarking

Benchmarking is the process where company sets up certain standards for each

element present in the company. For example, benchmark is set in terms of sales that are to be

achieved by Oshodi Plc as those of achieved by companies competitors. Generally, benchmark

is set in terms of achieving targets as compared to those of competitors.

Advantages Disadvantages

It help in achieving targets of companies

as those of competitors (Van Mechelen,

and et.al., 2018);

Helps in assisting new paradigms for

Oshodi Plc;

This method contributes in improvement

of performance of Oshodi Plc.

This method adversely affects morale of

employees present in organisation;

It is not realistic tool for measuring

company's performance.

Variance Analysis-

Variance Analysis is the method in which standard performance as set by management

are compared with those of actual performance of Oshodi Plc. Management finds deviations

between standard and actual performance and take corrective actions in order to remove all

such deviations from company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.