Management Accounting Report: ABC Ltd Costing, Budgeting and Variance

VerifiedAdded on 2020/06/04

|25

|4645

|39

Report

AI Summary

This report delves into management accounting, focusing on costing methods, budgeting processes, and variance analysis for ABC Ltd. It begins with an introduction to management accounting and its tools, including costing, budgeting, and variance analysis. Task 1 explores different types of costs (fixed, variable, semi-variable) and various costing methods (job, batch, process, contract). It includes cost calculations using FIFO, LIFO, and AVCO methods. Task 2 covers the preparation and analysis of routine cost reports and performance indicators to identify potential improvements for ABC Ltd. Task 3 examines the purpose and nature of the budgeting process, proposing budgeting methods and preparing budgets, including a cash budget. Task 4 focuses on calculating variances, identifying causes, and providing recommendations, along with an operating statement reconciling budgeted and actual results, and identifying responsibility centers. The report concludes with a summary of findings and recommendations for ABC Ltd.

MANAGEMENT

ACCOUNTING COSTING

AND BUDGETING

ACCOUNTING COSTING

AND BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

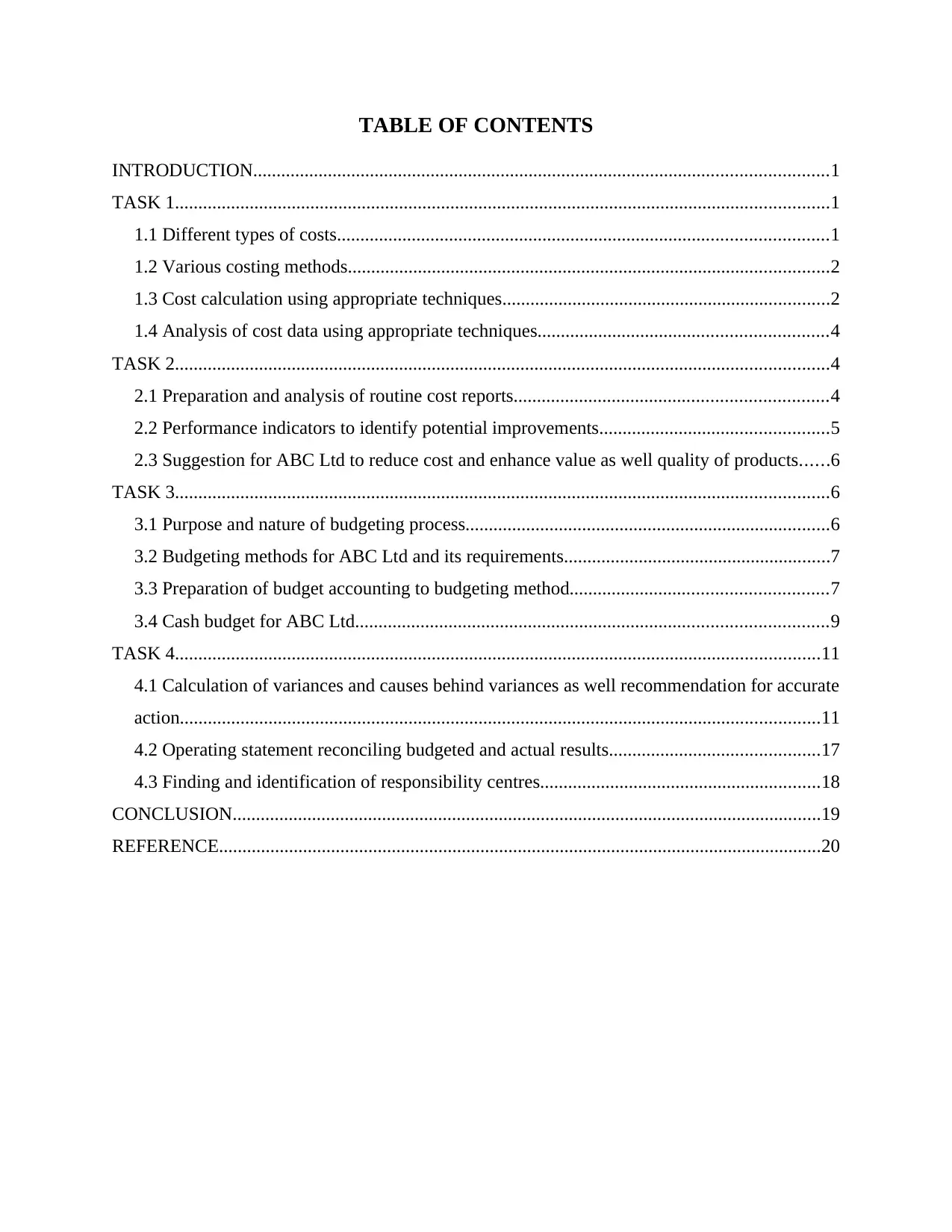

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different types of costs.........................................................................................................1

1.2 Various costing methods.......................................................................................................2

1.3 Cost calculation using appropriate techniques......................................................................2

1.4 Analysis of cost data using appropriate techniques..............................................................4

TASK 2............................................................................................................................................4

2.1 Preparation and analysis of routine cost reports...................................................................4

2.2 Performance indicators to identify potential improvements.................................................5

2.3 Suggestion for ABC Ltd to reduce cost and enhance value as well quality of products......6

TASK 3............................................................................................................................................6

3.1 Purpose and nature of budgeting process..............................................................................6

3.2 Budgeting methods for ABC Ltd and its requirements.........................................................7

3.3 Preparation of budget accounting to budgeting method.......................................................7

3.4 Cash budget for ABC Ltd.....................................................................................................9

TASK 4..........................................................................................................................................11

4.1 Calculation of variances and causes behind variances as well recommendation for accurate

action.........................................................................................................................................11

4.2 Operating statement reconciling budgeted and actual results.............................................17

4.3 Finding and identification of responsibility centres............................................................18

CONCLUSION..............................................................................................................................19

REFERENCE.................................................................................................................................20

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different types of costs.........................................................................................................1

1.2 Various costing methods.......................................................................................................2

1.3 Cost calculation using appropriate techniques......................................................................2

1.4 Analysis of cost data using appropriate techniques..............................................................4

TASK 2............................................................................................................................................4

2.1 Preparation and analysis of routine cost reports...................................................................4

2.2 Performance indicators to identify potential improvements.................................................5

2.3 Suggestion for ABC Ltd to reduce cost and enhance value as well quality of products......6

TASK 3............................................................................................................................................6

3.1 Purpose and nature of budgeting process..............................................................................6

3.2 Budgeting methods for ABC Ltd and its requirements.........................................................7

3.3 Preparation of budget accounting to budgeting method.......................................................7

3.4 Cash budget for ABC Ltd.....................................................................................................9

TASK 4..........................................................................................................................................11

4.1 Calculation of variances and causes behind variances as well recommendation for accurate

action.........................................................................................................................................11

4.2 Operating statement reconciling budgeted and actual results.............................................17

4.3 Finding and identification of responsibility centres............................................................18

CONCLUSION..............................................................................................................................19

REFERENCE.................................................................................................................................20

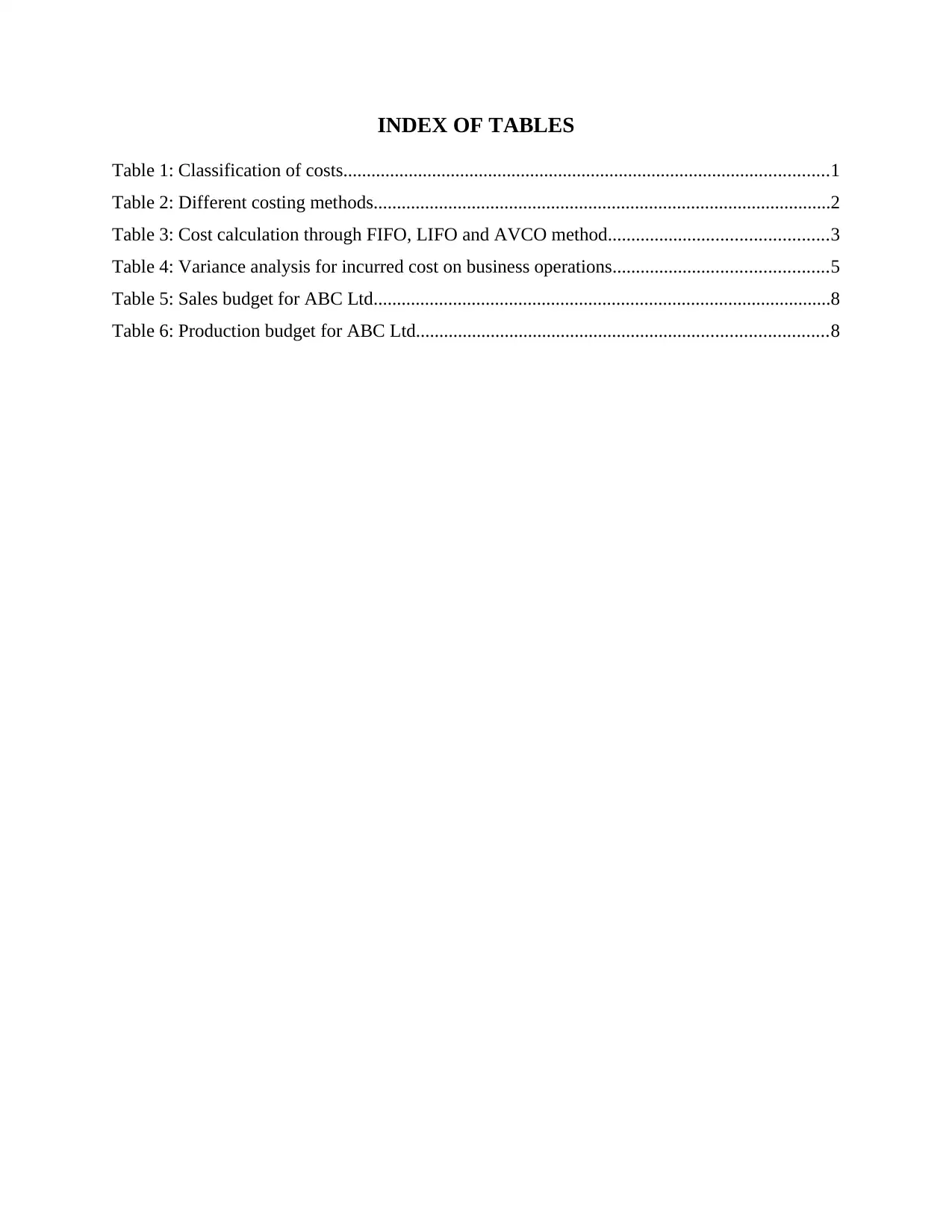

INDEX OF TABLES

Table 1: Classification of costs........................................................................................................1

Table 2: Different costing methods..................................................................................................2

Table 3: Cost calculation through FIFO, LIFO and AVCO method...............................................3

Table 4: Variance analysis for incurred cost on business operations..............................................5

Table 5: Sales budget for ABC Ltd..................................................................................................8

Table 6: Production budget for ABC Ltd........................................................................................8

Table 1: Classification of costs........................................................................................................1

Table 2: Different costing methods..................................................................................................2

Table 3: Cost calculation through FIFO, LIFO and AVCO method...............................................3

Table 4: Variance analysis for incurred cost on business operations..............................................5

Table 5: Sales budget for ABC Ltd..................................................................................................8

Table 6: Production budget for ABC Ltd........................................................................................8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

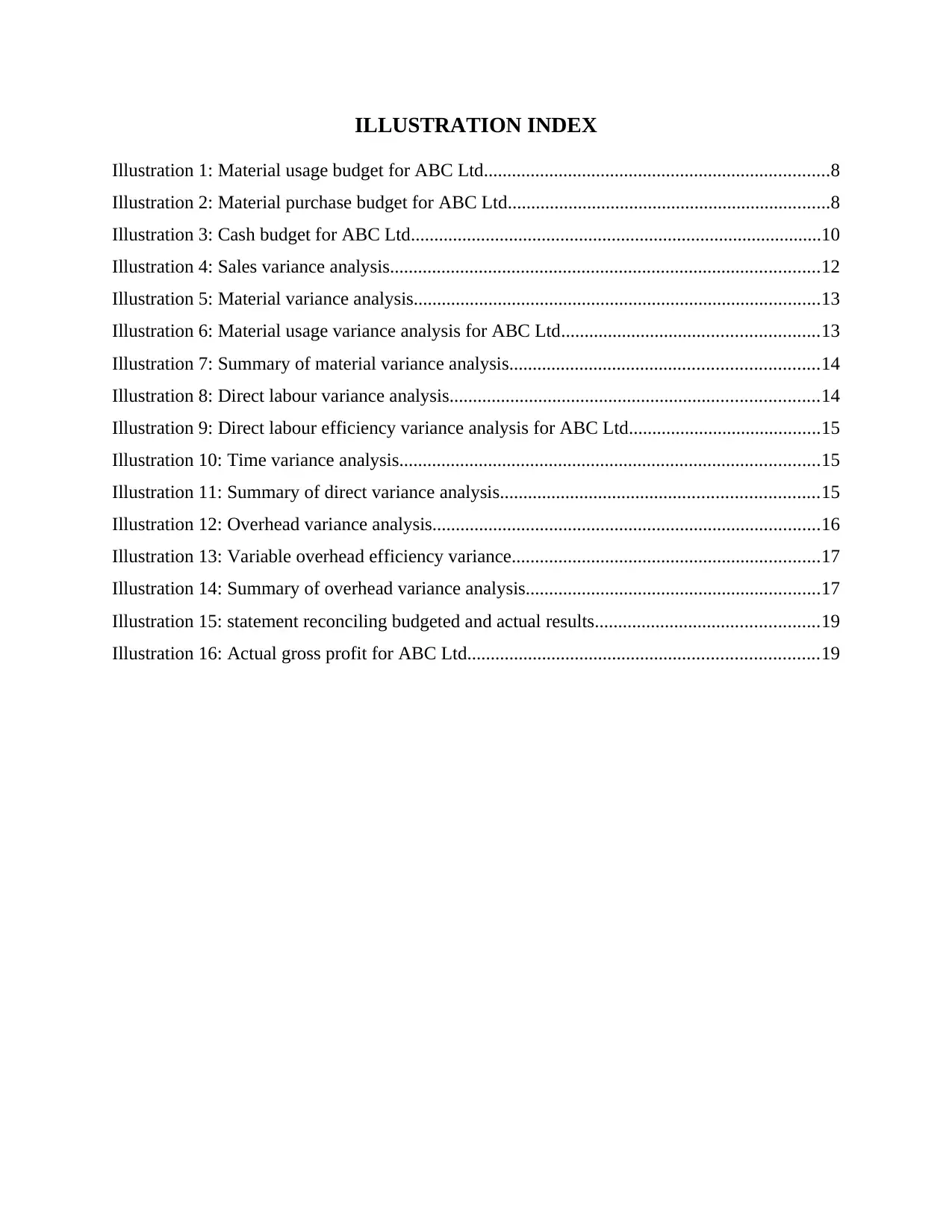

ILLUSTRATION INDEX

Illustration 1: Material usage budget for ABC Ltd..........................................................................8

Illustration 2: Material purchase budget for ABC Ltd.....................................................................8

Illustration 3: Cash budget for ABC Ltd........................................................................................10

Illustration 4: Sales variance analysis............................................................................................12

Illustration 5: Material variance analysis.......................................................................................13

Illustration 6: Material usage variance analysis for ABC Ltd.......................................................13

Illustration 7: Summary of material variance analysis..................................................................14

Illustration 8: Direct labour variance analysis...............................................................................14

Illustration 9: Direct labour efficiency variance analysis for ABC Ltd.........................................15

Illustration 10: Time variance analysis..........................................................................................15

Illustration 11: Summary of direct variance analysis....................................................................15

Illustration 12: Overhead variance analysis...................................................................................16

Illustration 13: Variable overhead efficiency variance..................................................................17

Illustration 14: Summary of overhead variance analysis...............................................................17

Illustration 15: statement reconciling budgeted and actual results................................................19

Illustration 16: Actual gross profit for ABC Ltd...........................................................................19

Illustration 1: Material usage budget for ABC Ltd..........................................................................8

Illustration 2: Material purchase budget for ABC Ltd.....................................................................8

Illustration 3: Cash budget for ABC Ltd........................................................................................10

Illustration 4: Sales variance analysis............................................................................................12

Illustration 5: Material variance analysis.......................................................................................13

Illustration 6: Material usage variance analysis for ABC Ltd.......................................................13

Illustration 7: Summary of material variance analysis..................................................................14

Illustration 8: Direct labour variance analysis...............................................................................14

Illustration 9: Direct labour efficiency variance analysis for ABC Ltd.........................................15

Illustration 10: Time variance analysis..........................................................................................15

Illustration 11: Summary of direct variance analysis....................................................................15

Illustration 12: Overhead variance analysis...................................................................................16

Illustration 13: Variable overhead efficiency variance..................................................................17

Illustration 14: Summary of overhead variance analysis...............................................................17

Illustration 15: statement reconciling budgeted and actual results................................................19

Illustration 16: Actual gross profit for ABC Ltd...........................................................................19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

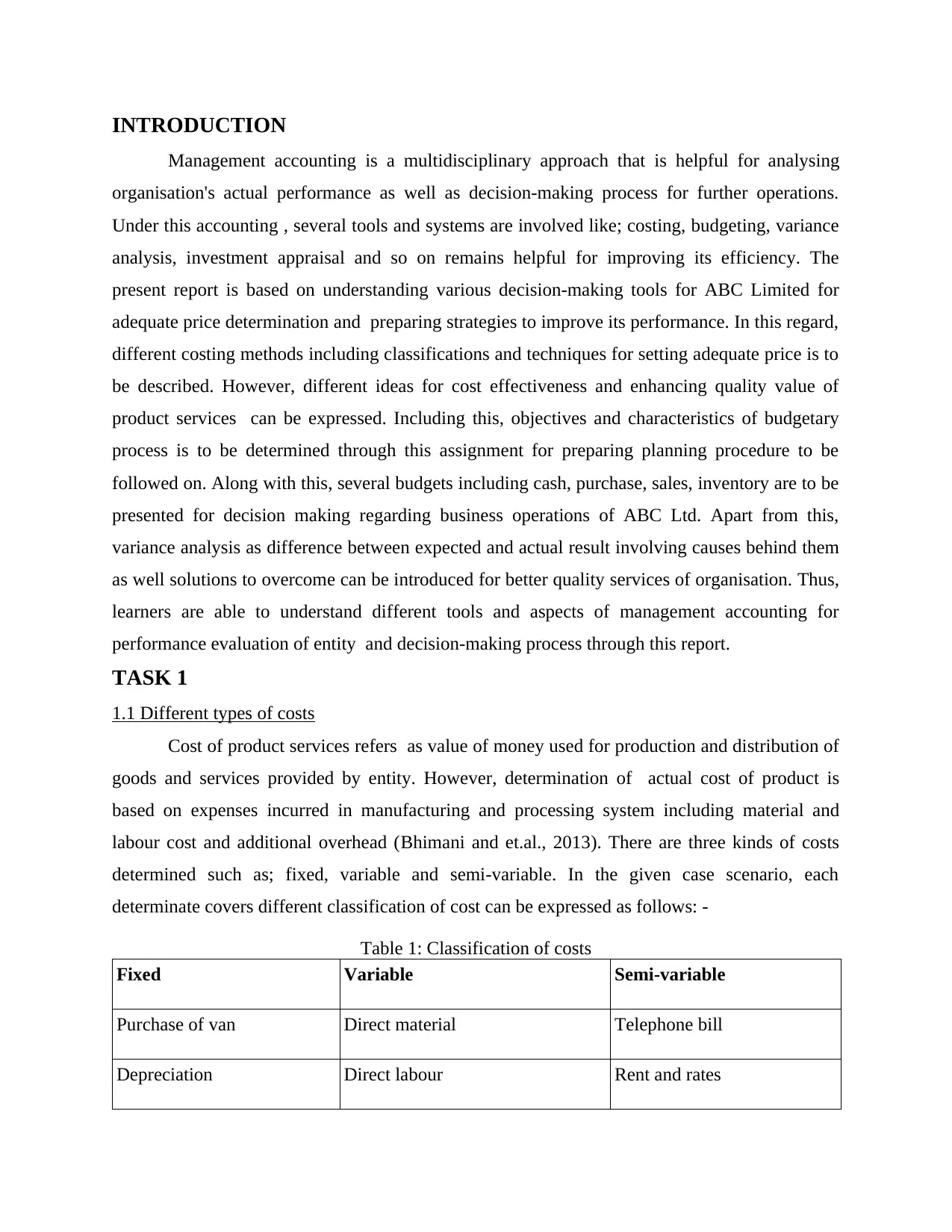

INTRODUCTION

Management accounting is a multidisciplinary approach that is helpful for analysing

organisation's actual performance as well as decision-making process for further operations.

Under this accounting , several tools and systems are involved like; costing, budgeting, variance

analysis, investment appraisal and so on remains helpful for improving its efficiency. The

present report is based on understanding various decision-making tools for ABC Limited for

adequate price determination and preparing strategies to improve its performance. In this regard,

different costing methods including classifications and techniques for setting adequate price is to

be described. However, different ideas for cost effectiveness and enhancing quality value of

product services can be expressed. Including this, objectives and characteristics of budgetary

process is to be determined through this assignment for preparing planning procedure to be

followed on. Along with this, several budgets including cash, purchase, sales, inventory are to be

presented for decision making regarding business operations of ABC Ltd. Apart from this,

variance analysis as difference between expected and actual result involving causes behind them

as well solutions to overcome can be introduced for better quality services of organisation. Thus,

learners are able to understand different tools and aspects of management accounting for

performance evaluation of entity and decision-making process through this report.

TASK 1

1.1 Different types of costs

Cost of product services refers as value of money used for production and distribution of

goods and services provided by entity. However, determination of actual cost of product is

based on expenses incurred in manufacturing and processing system including material and

labour cost and additional overhead (Bhimani and et.al., 2013). There are three kinds of costs

determined such as; fixed, variable and semi-variable. In the given case scenario, each

determinate covers different classification of cost can be expressed as follows: -

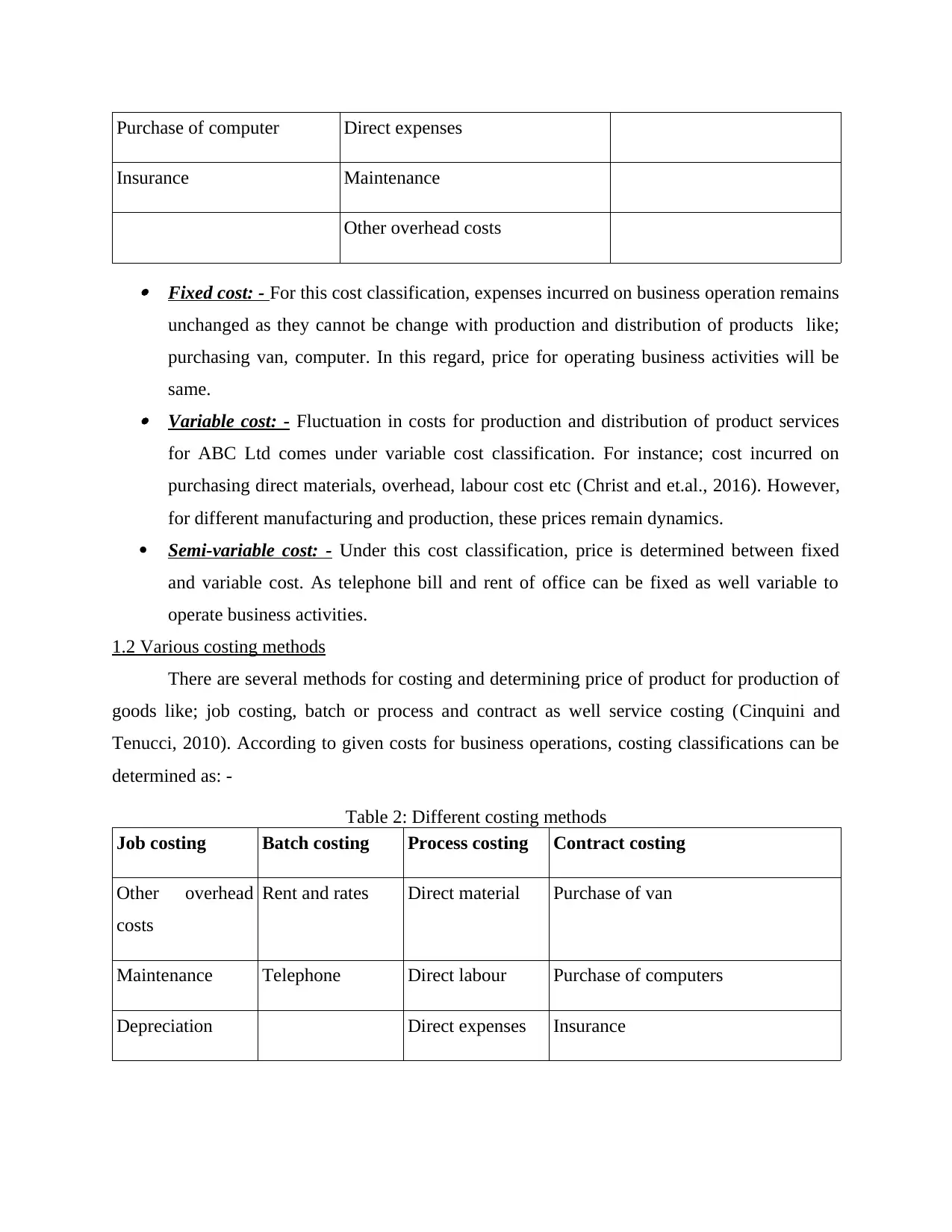

Table 1: Classification of costs

Fixed Variable Semi-variable

Purchase of van Direct material Telephone bill

Depreciation Direct labour Rent and rates

Management accounting is a multidisciplinary approach that is helpful for analysing

organisation's actual performance as well as decision-making process for further operations.

Under this accounting , several tools and systems are involved like; costing, budgeting, variance

analysis, investment appraisal and so on remains helpful for improving its efficiency. The

present report is based on understanding various decision-making tools for ABC Limited for

adequate price determination and preparing strategies to improve its performance. In this regard,

different costing methods including classifications and techniques for setting adequate price is to

be described. However, different ideas for cost effectiveness and enhancing quality value of

product services can be expressed. Including this, objectives and characteristics of budgetary

process is to be determined through this assignment for preparing planning procedure to be

followed on. Along with this, several budgets including cash, purchase, sales, inventory are to be

presented for decision making regarding business operations of ABC Ltd. Apart from this,

variance analysis as difference between expected and actual result involving causes behind them

as well solutions to overcome can be introduced for better quality services of organisation. Thus,

learners are able to understand different tools and aspects of management accounting for

performance evaluation of entity and decision-making process through this report.

TASK 1

1.1 Different types of costs

Cost of product services refers as value of money used for production and distribution of

goods and services provided by entity. However, determination of actual cost of product is

based on expenses incurred in manufacturing and processing system including material and

labour cost and additional overhead (Bhimani and et.al., 2013). There are three kinds of costs

determined such as; fixed, variable and semi-variable. In the given case scenario, each

determinate covers different classification of cost can be expressed as follows: -

Table 1: Classification of costs

Fixed Variable Semi-variable

Purchase of van Direct material Telephone bill

Depreciation Direct labour Rent and rates

Purchase of computer Direct expenses

Insurance Maintenance

Other overhead costs

Fixed cost: - For this cost classification, expenses incurred on business operation remains

unchanged as they cannot be change with production and distribution of products like;

purchasing van, computer. In this regard, price for operating business activities will be

same. Variable cost: - Fluctuation in costs for production and distribution of product services

for ABC Ltd comes under variable cost classification. For instance; cost incurred on

purchasing direct materials, overhead, labour cost etc (Christ and et.al., 2016). However,

for different manufacturing and production, these prices remain dynamics.

Semi-variable cost: - Under this cost classification, price is determined between fixed

and variable cost. As telephone bill and rent of office can be fixed as well variable to

operate business activities.

1.2 Various costing methods

There are several methods for costing and determining price of product for production of

goods like; job costing, batch or process and contract as well service costing (Cinquini and

Tenucci, 2010). According to given costs for business operations, costing classifications can be

determined as: -

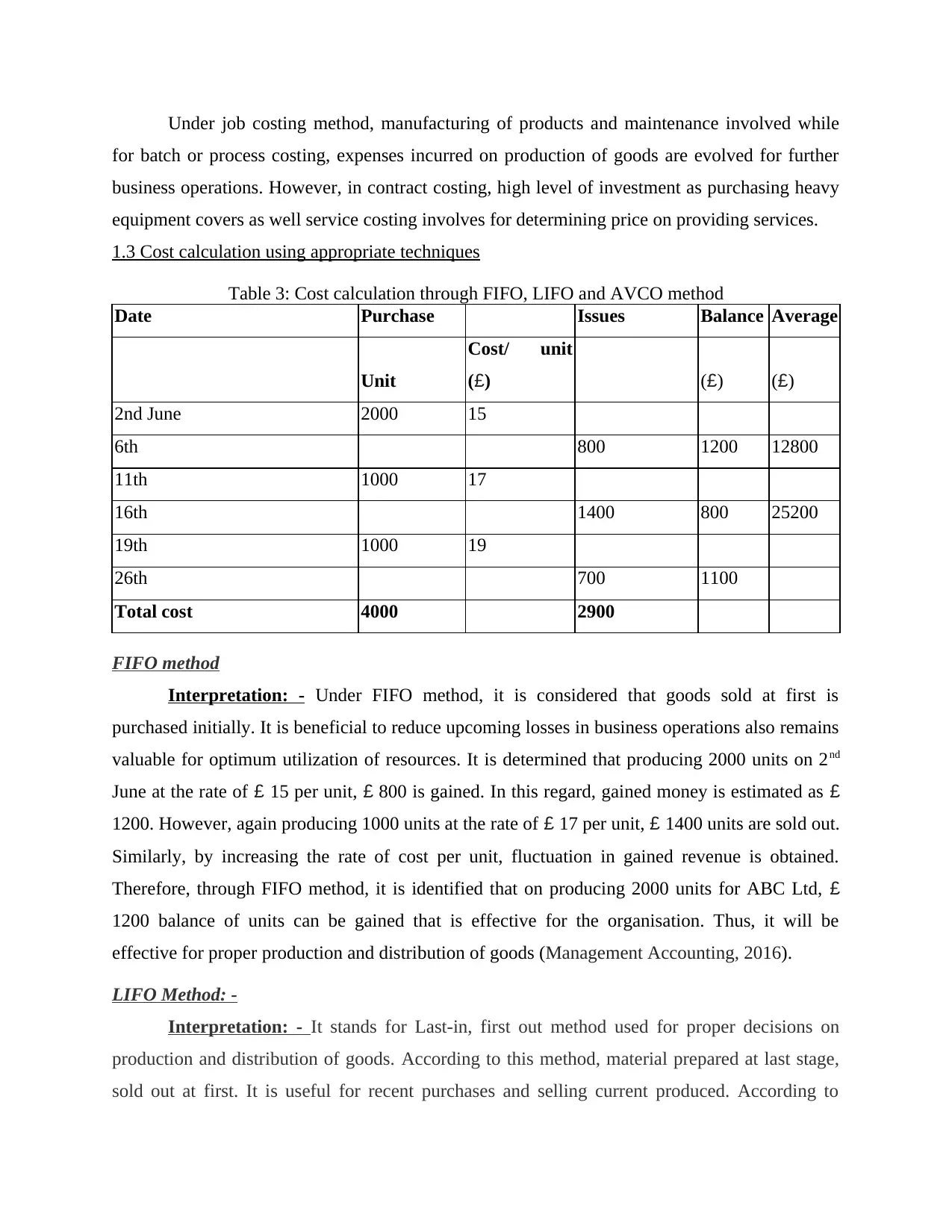

Table 2: Different costing methods

Job costing Batch costing Process costing Contract costing

Other overhead

costs

Rent and rates Direct material Purchase of van

Maintenance Telephone Direct labour Purchase of computers

Depreciation Direct expenses Insurance

Insurance Maintenance

Other overhead costs

Fixed cost: - For this cost classification, expenses incurred on business operation remains

unchanged as they cannot be change with production and distribution of products like;

purchasing van, computer. In this regard, price for operating business activities will be

same. Variable cost: - Fluctuation in costs for production and distribution of product services

for ABC Ltd comes under variable cost classification. For instance; cost incurred on

purchasing direct materials, overhead, labour cost etc (Christ and et.al., 2016). However,

for different manufacturing and production, these prices remain dynamics.

Semi-variable cost: - Under this cost classification, price is determined between fixed

and variable cost. As telephone bill and rent of office can be fixed as well variable to

operate business activities.

1.2 Various costing methods

There are several methods for costing and determining price of product for production of

goods like; job costing, batch or process and contract as well service costing (Cinquini and

Tenucci, 2010). According to given costs for business operations, costing classifications can be

determined as: -

Table 2: Different costing methods

Job costing Batch costing Process costing Contract costing

Other overhead

costs

Rent and rates Direct material Purchase of van

Maintenance Telephone Direct labour Purchase of computers

Depreciation Direct expenses Insurance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under job costing method, manufacturing of products and maintenance involved while

for batch or process costing, expenses incurred on production of goods are evolved for further

business operations. However, in contract costing, high level of investment as purchasing heavy

equipment covers as well service costing involves for determining price on providing services.

1.3 Cost calculation using appropriate techniques

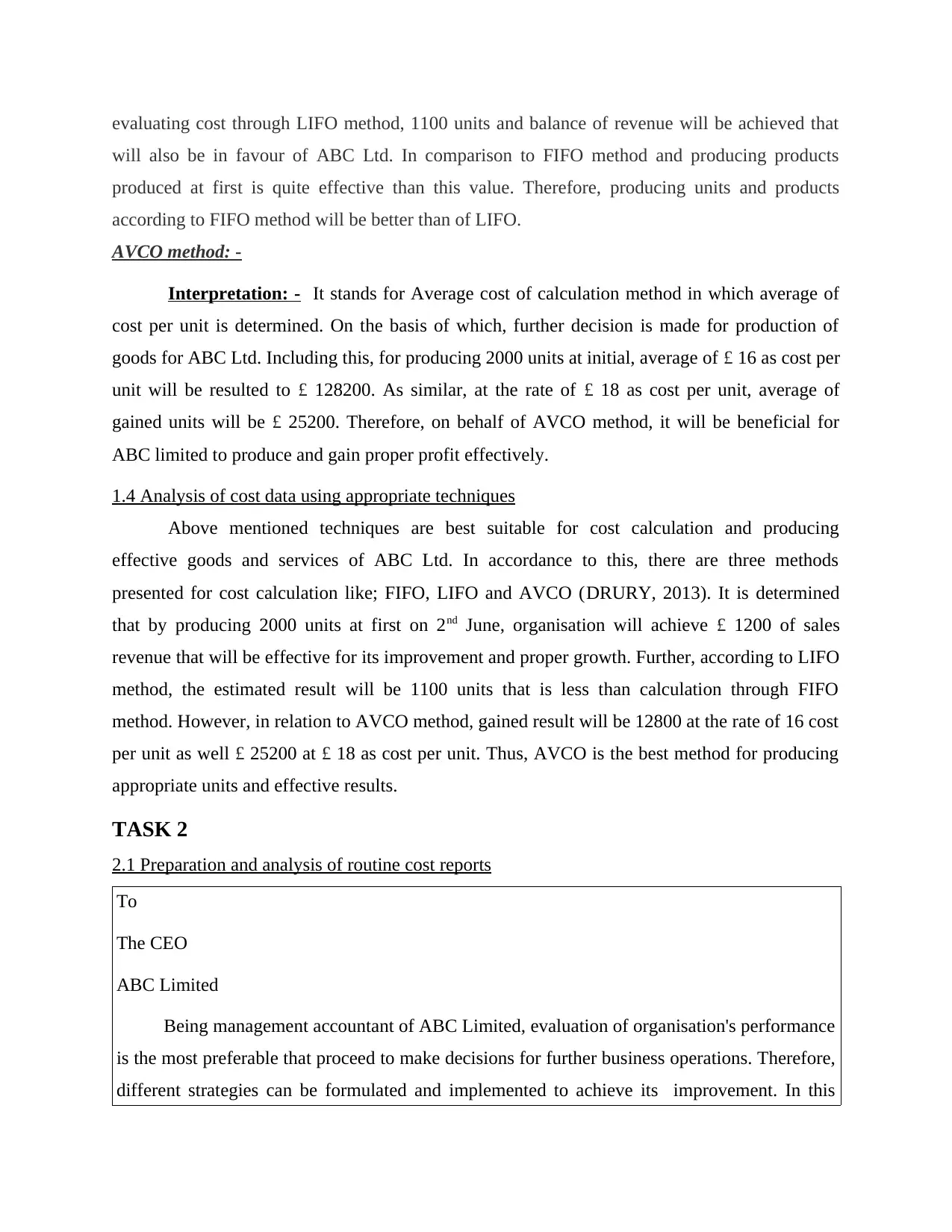

Table 3: Cost calculation through FIFO, LIFO and AVCO method

Date Purchase Issues Balance Average

Unit

Cost/ unit

(£) (£) (£)

2nd June 2000 15

6th 800 1200 12800

11th 1000 17

16th 1400 800 25200

19th 1000 19

26th 700 1100

Total cost 4000 2900

FIFO method

Interpretation: - Under FIFO method, it is considered that goods sold at first is

purchased initially. It is beneficial to reduce upcoming losses in business operations also remains

valuable for optimum utilization of resources. It is determined that producing 2000 units on 2nd

June at the rate of £ 15 per unit, £ 800 is gained. In this regard, gained money is estimated as £

1200. However, again producing 1000 units at the rate of £ 17 per unit, £ 1400 units are sold out.

Similarly, by increasing the rate of cost per unit, fluctuation in gained revenue is obtained.

Therefore, through FIFO method, it is identified that on producing 2000 units for ABC Ltd, £

1200 balance of units can be gained that is effective for the organisation. Thus, it will be

effective for proper production and distribution of goods (Management Accounting, 2016).

LIFO Method: -

Interpretation: - It stands for Last-in, first out method used for proper decisions on

production and distribution of goods. According to this method, material prepared at last stage,

sold out at first. It is useful for recent purchases and selling current produced. According to

for batch or process costing, expenses incurred on production of goods are evolved for further

business operations. However, in contract costing, high level of investment as purchasing heavy

equipment covers as well service costing involves for determining price on providing services.

1.3 Cost calculation using appropriate techniques

Table 3: Cost calculation through FIFO, LIFO and AVCO method

Date Purchase Issues Balance Average

Unit

Cost/ unit

(£) (£) (£)

2nd June 2000 15

6th 800 1200 12800

11th 1000 17

16th 1400 800 25200

19th 1000 19

26th 700 1100

Total cost 4000 2900

FIFO method

Interpretation: - Under FIFO method, it is considered that goods sold at first is

purchased initially. It is beneficial to reduce upcoming losses in business operations also remains

valuable for optimum utilization of resources. It is determined that producing 2000 units on 2nd

June at the rate of £ 15 per unit, £ 800 is gained. In this regard, gained money is estimated as £

1200. However, again producing 1000 units at the rate of £ 17 per unit, £ 1400 units are sold out.

Similarly, by increasing the rate of cost per unit, fluctuation in gained revenue is obtained.

Therefore, through FIFO method, it is identified that on producing 2000 units for ABC Ltd, £

1200 balance of units can be gained that is effective for the organisation. Thus, it will be

effective for proper production and distribution of goods (Management Accounting, 2016).

LIFO Method: -

Interpretation: - It stands for Last-in, first out method used for proper decisions on

production and distribution of goods. According to this method, material prepared at last stage,

sold out at first. It is useful for recent purchases and selling current produced. According to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

evaluating cost through LIFO method, 1100 units and balance of revenue will be achieved that

will also be in favour of ABC Ltd. In comparison to FIFO method and producing products

produced at first is quite effective than this value. Therefore, producing units and products

according to FIFO method will be better than of LIFO.

AVCO method: -

Interpretation: - It stands for Average cost of calculation method in which average of

cost per unit is determined. On the basis of which, further decision is made for production of

goods for ABC Ltd. Including this, for producing 2000 units at initial, average of £ 16 as cost per

unit will be resulted to £ 128200. As similar, at the rate of £ 18 as cost per unit, average of

gained units will be £ 25200. Therefore, on behalf of AVCO method, it will be beneficial for

ABC limited to produce and gain proper profit effectively.

1.4 Analysis of cost data using appropriate techniques

Above mentioned techniques are best suitable for cost calculation and producing

effective goods and services of ABC Ltd. In accordance to this, there are three methods

presented for cost calculation like; FIFO, LIFO and AVCO (DRURY, 2013). It is determined

that by producing 2000 units at first on 2nd June, organisation will achieve £ 1200 of sales

revenue that will be effective for its improvement and proper growth. Further, according to LIFO

method, the estimated result will be 1100 units that is less than calculation through FIFO

method. However, in relation to AVCO method, gained result will be 12800 at the rate of 16 cost

per unit as well £ 25200 at £ 18 as cost per unit. Thus, AVCO is the best method for producing

appropriate units and effective results.

TASK 2

2.1 Preparation and analysis of routine cost reports

To

The CEO

ABC Limited

Being management accountant of ABC Limited, evaluation of organisation's performance

is the most preferable that proceed to make decisions for further business operations. Therefore,

different strategies can be formulated and implemented to achieve its improvement. In this

will also be in favour of ABC Ltd. In comparison to FIFO method and producing products

produced at first is quite effective than this value. Therefore, producing units and products

according to FIFO method will be better than of LIFO.

AVCO method: -

Interpretation: - It stands for Average cost of calculation method in which average of

cost per unit is determined. On the basis of which, further decision is made for production of

goods for ABC Ltd. Including this, for producing 2000 units at initial, average of £ 16 as cost per

unit will be resulted to £ 128200. As similar, at the rate of £ 18 as cost per unit, average of

gained units will be £ 25200. Therefore, on behalf of AVCO method, it will be beneficial for

ABC limited to produce and gain proper profit effectively.

1.4 Analysis of cost data using appropriate techniques

Above mentioned techniques are best suitable for cost calculation and producing

effective goods and services of ABC Ltd. In accordance to this, there are three methods

presented for cost calculation like; FIFO, LIFO and AVCO (DRURY, 2013). It is determined

that by producing 2000 units at first on 2nd June, organisation will achieve £ 1200 of sales

revenue that will be effective for its improvement and proper growth. Further, according to LIFO

method, the estimated result will be 1100 units that is less than calculation through FIFO

method. However, in relation to AVCO method, gained result will be 12800 at the rate of 16 cost

per unit as well £ 25200 at £ 18 as cost per unit. Thus, AVCO is the best method for producing

appropriate units and effective results.

TASK 2

2.1 Preparation and analysis of routine cost reports

To

The CEO

ABC Limited

Being management accountant of ABC Limited, evaluation of organisation's performance

is the most preferable that proceed to make decisions for further business operations. Therefore,

different strategies can be formulated and implemented to achieve its improvement. In this

regard, cost expected to be incurred and actual expenses incurred on business operations can be

comprised. However, in the given case scenario, units incurred on operations can be recognized

through following routine cost report that is to mention variance analysis for April 2016: -

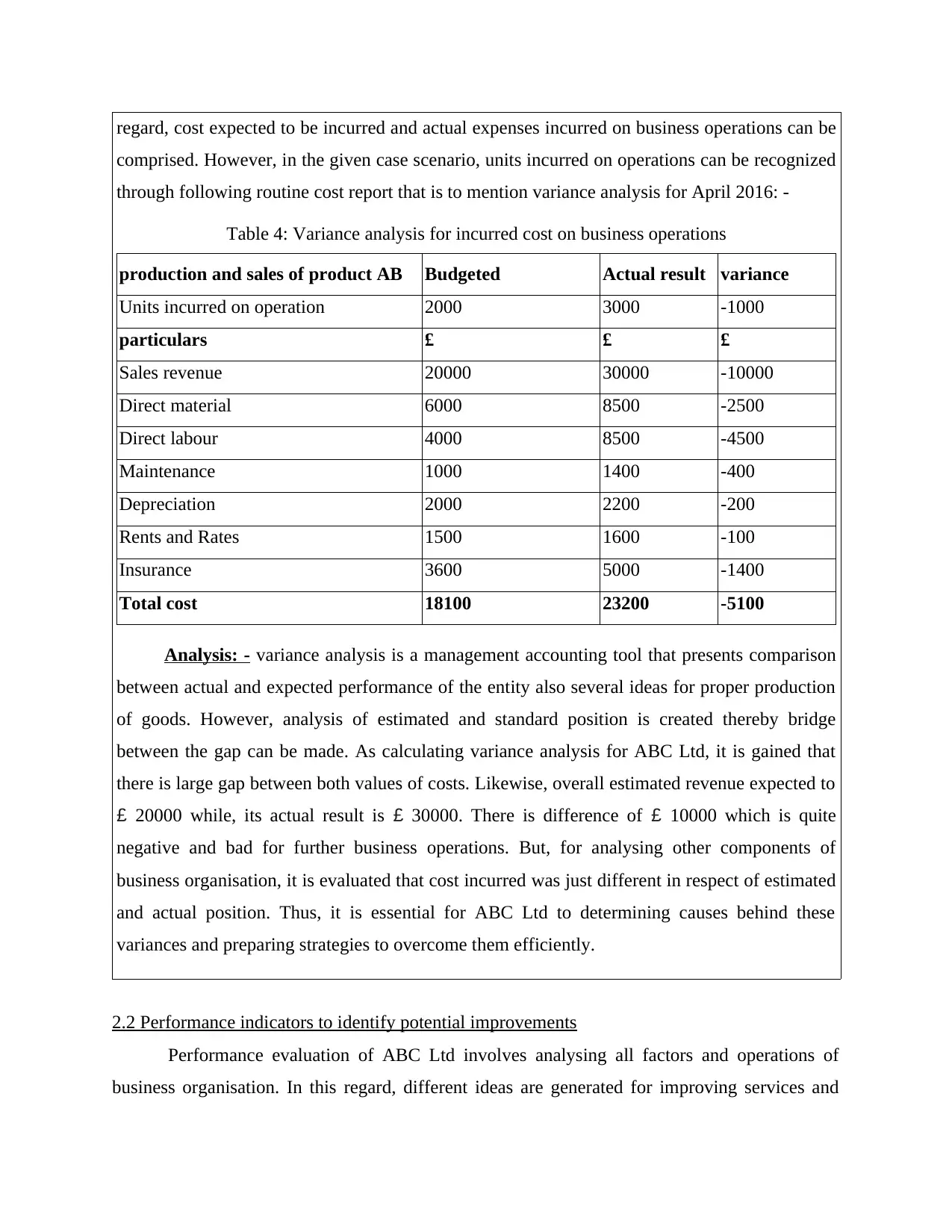

Table 4: Variance analysis for incurred cost on business operations

production and sales of product AB Budgeted Actual result variance

Units incurred on operation 2000 3000 -1000

particulars £ £ £

Sales revenue 20000 30000 -10000

Direct material 6000 8500 -2500

Direct labour 4000 8500 -4500

Maintenance 1000 1400 -400

Depreciation 2000 2200 -200

Rents and Rates 1500 1600 -100

Insurance 3600 5000 -1400

Total cost 18100 23200 -5100

Analysis: - variance analysis is a management accounting tool that presents comparison

between actual and expected performance of the entity also several ideas for proper production

of goods. However, analysis of estimated and standard position is created thereby bridge

between the gap can be made. As calculating variance analysis for ABC Ltd, it is gained that

there is large gap between both values of costs. Likewise, overall estimated revenue expected to

£ 20000 while, its actual result is £ 30000. There is difference of £ 10000 which is quite

negative and bad for further business operations. But, for analysing other components of

business organisation, it is evaluated that cost incurred was just different in respect of estimated

and actual position. Thus, it is essential for ABC Ltd to determining causes behind these

variances and preparing strategies to overcome them efficiently.

2.2 Performance indicators to identify potential improvements

Performance evaluation of ABC Ltd involves analysing all factors and operations of

business organisation. In this regard, different ideas are generated for improving services and

comprised. However, in the given case scenario, units incurred on operations can be recognized

through following routine cost report that is to mention variance analysis for April 2016: -

Table 4: Variance analysis for incurred cost on business operations

production and sales of product AB Budgeted Actual result variance

Units incurred on operation 2000 3000 -1000

particulars £ £ £

Sales revenue 20000 30000 -10000

Direct material 6000 8500 -2500

Direct labour 4000 8500 -4500

Maintenance 1000 1400 -400

Depreciation 2000 2200 -200

Rents and Rates 1500 1600 -100

Insurance 3600 5000 -1400

Total cost 18100 23200 -5100

Analysis: - variance analysis is a management accounting tool that presents comparison

between actual and expected performance of the entity also several ideas for proper production

of goods. However, analysis of estimated and standard position is created thereby bridge

between the gap can be made. As calculating variance analysis for ABC Ltd, it is gained that

there is large gap between both values of costs. Likewise, overall estimated revenue expected to

£ 20000 while, its actual result is £ 30000. There is difference of £ 10000 which is quite

negative and bad for further business operations. But, for analysing other components of

business organisation, it is evaluated that cost incurred was just different in respect of estimated

and actual position. Thus, it is essential for ABC Ltd to determining causes behind these

variances and preparing strategies to overcome them efficiently.

2.2 Performance indicators to identify potential improvements

Performance evaluation of ABC Ltd involves analysing all factors and operations of

business organisation. In this regard, different ideas are generated for improving services and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

providing better-quality services. However, customer satisfaction and demand for different kinds

of kites is identified that leads to make decisions for further business operations (Fullerton,

Kennedy and Widener, 2013). Including this, profit earning capacity of entity is recognized

through this method that influences productivity and profitability of the firm. As per identifying

actual market position and quality services of ABC Ltd, it is recognized that entity required to

focus on all increasing its revenue and utilizing resources and fund in optimum way. It is crucial

for the entity to find out reasons behind variances as well preparing plans to overcome them

efficiently.

2.3 Suggestion for ABC Ltd to reduce cost and enhance value as well quality of products

According to current position of ABC Ltd, it is to suggested that organisation requires to

enhance its revenue and profit earning capacity for competitive advantages and long-term

sustainability. It is needed to create balance of proper production and distribution of kites

produced by the entity (Giovannoni, Maraghini and Riccaboni, 2011). However, for improving

quality services of products and to satisfy customers with them, it is essential to adopt innovative

techniques and enhancing profitability for competitive strategies. Including this, it is crucial for

ABC Ltd to increase profitability through analysing all business operations critically therefore,

actual position of entity can be gained. On the basis of this, several strategies including decision

making can be processed for improving quality services and performance of entity effectively. It

will be helpful for optimum utilization of resources and fund that affects further business

operations to make place in market for long term periodicity.

TASK 3

3.1 Purpose and nature of budgeting process

Nature of budgeting:

At the time of making budget for company, old and past performance is always

considered by the manager.

Budget provide data to the ABC Limited regarding net cash balance or surplus and

deficit. On the basis of this effective strategies and business decisions are made (Kaplan

and Anderson, 2013). By this, decisions of raising fund are to be made because it shows that in further year

whether money will be required or not.

of kites is identified that leads to make decisions for further business operations (Fullerton,

Kennedy and Widener, 2013). Including this, profit earning capacity of entity is recognized

through this method that influences productivity and profitability of the firm. As per identifying

actual market position and quality services of ABC Ltd, it is recognized that entity required to

focus on all increasing its revenue and utilizing resources and fund in optimum way. It is crucial

for the entity to find out reasons behind variances as well preparing plans to overcome them

efficiently.

2.3 Suggestion for ABC Ltd to reduce cost and enhance value as well quality of products

According to current position of ABC Ltd, it is to suggested that organisation requires to

enhance its revenue and profit earning capacity for competitive advantages and long-term

sustainability. It is needed to create balance of proper production and distribution of kites

produced by the entity (Giovannoni, Maraghini and Riccaboni, 2011). However, for improving

quality services of products and to satisfy customers with them, it is essential to adopt innovative

techniques and enhancing profitability for competitive strategies. Including this, it is crucial for

ABC Ltd to increase profitability through analysing all business operations critically therefore,

actual position of entity can be gained. On the basis of this, several strategies including decision

making can be processed for improving quality services and performance of entity effectively. It

will be helpful for optimum utilization of resources and fund that affects further business

operations to make place in market for long term periodicity.

TASK 3

3.1 Purpose and nature of budgeting process

Nature of budgeting:

At the time of making budget for company, old and past performance is always

considered by the manager.

Budget provide data to the ABC Limited regarding net cash balance or surplus and

deficit. On the basis of this effective strategies and business decisions are made (Kaplan

and Anderson, 2013). By this, decisions of raising fund are to be made because it shows that in further year

whether money will be required or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Objectives of budgeting:

Very initial objective of the budgeting is to provide financial data of the next accounting

years to the company in proper manner. After considering this aspect, ABC limited

makes several business decisions to improve its financial health.

Another purpose is to assess business performance using variance analysis method. The

technique under which expected or forecasted data of budget are compared with the

generated is known as variance analysis.

Through this, resources are allotted adequately among all the functions and departments

of ABC limited as it was significant for every firm.

By this, various kinds of functions are coordinated with each other in proper ways which

is sign of effective organisational relationship (Henttu-Aho and Järvinen, 2013).

In the different responsibility centres like cost, expense, sales or revenue, profit,

investment etc. budgeting has important place.

Moreover, budgeting is one of the highly supportive tool for ABC Limited in order to

achieve financial objectives.

3.2 Budgeting methods for ABC Ltd and its requirements

When the management is going to prepare budget for the firm then there are several kinds

of techniques or methods are undertaken. The various budgeting methods are used like

traditional, zero based, incremental, fixed, activity based etc. Without considering anyone

method manager of ABC limited not able to forecast future financial information. Very effective

and suitable method to frame budget for ABC Limited entity is activity based budgeting process.

With the help of this, management able to assess costing level of every activity and business

process exist within workplace. Very basic requirement of suggested budgeting method is to

identify problems and constraints regarding to every activity in proper ways (Bierman and Smidt,

2014). Further, fruitful decisions can be made which is sign of enhancing business performance

within the market segment. Along with this, firm can easily allot financial resources to each

business activity adequately.

3.3 Preparation of budget accounting to budgeting method

Sales budget: -

Table 5: Sales budget for ABC Ltd

Very initial objective of the budgeting is to provide financial data of the next accounting

years to the company in proper manner. After considering this aspect, ABC limited

makes several business decisions to improve its financial health.

Another purpose is to assess business performance using variance analysis method. The

technique under which expected or forecasted data of budget are compared with the

generated is known as variance analysis.

Through this, resources are allotted adequately among all the functions and departments

of ABC limited as it was significant for every firm.

By this, various kinds of functions are coordinated with each other in proper ways which

is sign of effective organisational relationship (Henttu-Aho and Järvinen, 2013).

In the different responsibility centres like cost, expense, sales or revenue, profit,

investment etc. budgeting has important place.

Moreover, budgeting is one of the highly supportive tool for ABC Limited in order to

achieve financial objectives.

3.2 Budgeting methods for ABC Ltd and its requirements

When the management is going to prepare budget for the firm then there are several kinds

of techniques or methods are undertaken. The various budgeting methods are used like

traditional, zero based, incremental, fixed, activity based etc. Without considering anyone

method manager of ABC limited not able to forecast future financial information. Very effective

and suitable method to frame budget for ABC Limited entity is activity based budgeting process.

With the help of this, management able to assess costing level of every activity and business

process exist within workplace. Very basic requirement of suggested budgeting method is to

identify problems and constraints regarding to every activity in proper ways (Bierman and Smidt,

2014). Further, fruitful decisions can be made which is sign of enhancing business performance

within the market segment. Along with this, firm can easily allot financial resources to each

business activity adequately.

3.3 Preparation of budget accounting to budgeting method

Sales budget: -

Table 5: Sales budget for ABC Ltd

Product Sales unit

Selling price per

unit

Budgeted sales

revenue

X kite 4000 60 240000

Y kite 12000 80 960000

Z kite 3000 120 360000

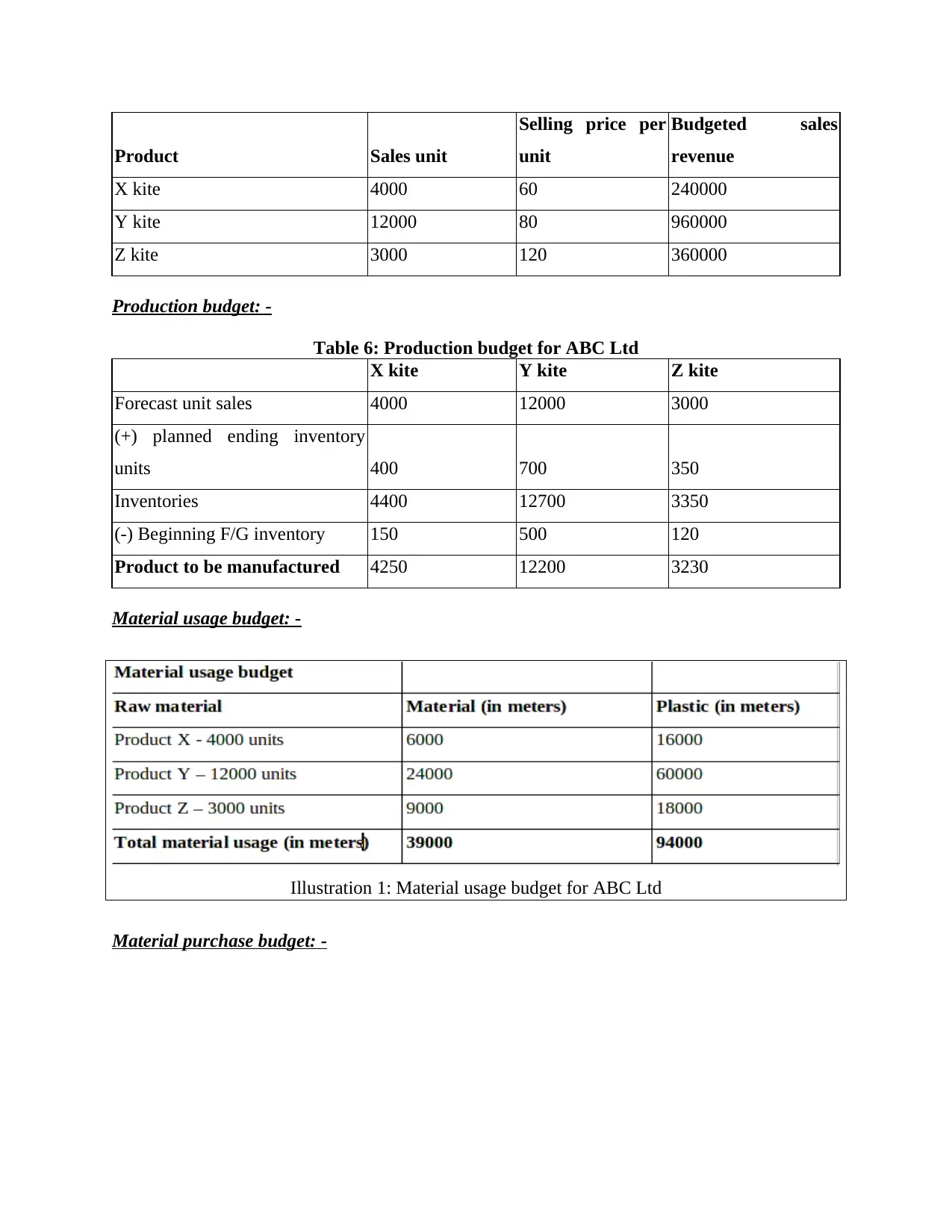

Production budget: -

Table 6: Production budget for ABC Ltd

X kite Y kite Z kite

Forecast unit sales 4000 12000 3000

(+) planned ending inventory

units 400 700 350

Inventories 4400 12700 3350

(-) Beginning F/G inventory 150 500 120

Product to be manufactured 4250 12200 3230

Material usage budget: -

Material purchase budget: -

Illustration 1: Material usage budget for ABC Ltd

Selling price per

unit

Budgeted sales

revenue

X kite 4000 60 240000

Y kite 12000 80 960000

Z kite 3000 120 360000

Production budget: -

Table 6: Production budget for ABC Ltd

X kite Y kite Z kite

Forecast unit sales 4000 12000 3000

(+) planned ending inventory

units 400 700 350

Inventories 4400 12700 3350

(-) Beginning F/G inventory 150 500 120

Product to be manufactured 4250 12200 3230

Material usage budget: -

Material purchase budget: -

Illustration 1: Material usage budget for ABC Ltd

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 25

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.