HND Business - Management Accounting: Costing and Budgeting Report

VerifiedAdded on 2020/01/06

|19

|5475

|426

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on cost analysis, costing methods, and budgeting techniques. The report examines different types of costs, including fixed, variable, direct, and indirect costs, as well as various costing methods such as unit costing, job costing, and process costing. It further analyzes cost data, comparing variable and absorption costing methods under different production and sales scenarios. The report also delves into performance indicators, ways to reduce costs, enhance value and quality, and the purpose and nature of the budgeting process. It includes a detailed cash budget for Antonio Ltd, variance calculations, and an operating statement to deduce budget profit. Finally, it provides recommendations for corrective actions and presents findings to management, offering valuable insights into financial accounting and reporting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different types of costs.........................................................................................................1

1.2 Different types of costing methods.......................................................................................2

1.3 Costing techniques................................................................................................................2

1.4 Analyse the cost data.............................................................................................................3

TASK 2............................................................................................................................................5

2.1 Cost report and analysis........................................................................................................5

2.2 Various performance indicators used to identify potential improvements...........................6

2.3 Ways to reduce costs, enhance value and quality.................................................................6

TASK 3 ...........................................................................................................................................7

3.1 Purpose and nature of budgeting process..............................................................................7

3.2 Budgeting method and its need.............................................................................................8

3.3 Budget preparation................................................................................................................9

3.4 Preparation of cash budget for Antonio Ltd........................................................................10

TASK 4..........................................................................................................................................11

4.1 Variance calculation, identify possible causes and recommend corrective actions............11

4.2 Operating statement to deduce budget profit for the month of May...................................12

1.3 Report the findings to management....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Different types of costs.........................................................................................................1

1.2 Different types of costing methods.......................................................................................2

1.3 Costing techniques................................................................................................................2

1.4 Analyse the cost data.............................................................................................................3

TASK 2............................................................................................................................................5

2.1 Cost report and analysis........................................................................................................5

2.2 Various performance indicators used to identify potential improvements...........................6

2.3 Ways to reduce costs, enhance value and quality.................................................................6

TASK 3 ...........................................................................................................................................7

3.1 Purpose and nature of budgeting process..............................................................................7

3.2 Budgeting method and its need.............................................................................................8

3.3 Budget preparation................................................................................................................9

3.4 Preparation of cash budget for Antonio Ltd........................................................................10

TASK 4..........................................................................................................................................11

4.1 Variance calculation, identify possible causes and recommend corrective actions............11

4.2 Operating statement to deduce budget profit for the month of May...................................12

1.3 Report the findings to management....................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................15

Index of Tables

Table 1: Variable costing for Bittern Ltd.........................................................................................3

Table 2: Absorption costing for Bittern Ltd....................................................................................3

Table 3: Variable costing for Bittern Ltd.........................................................................................4

Table 4: Absorption costing for Bittern Ltd....................................................................................4

Table 5: Variable costing for Bittern Ltd.........................................................................................5

Table 6: Absorption costing for Bittern Ltd....................................................................................5

Table 7: Material purchase budget...................................................................................................9

Table 8: Trade payable budgets.......................................................................................................9

Table 9: Cash budget of Antonio for six months...........................................................................10

Table 10: Standard and actual results............................................................................................11

Table 11: Calculation of variances................................................................................................11

Table 12: Operating statement to deduce budget profit for May...................................................12

Table 1: Variable costing for Bittern Ltd.........................................................................................3

Table 2: Absorption costing for Bittern Ltd....................................................................................3

Table 3: Variable costing for Bittern Ltd.........................................................................................4

Table 4: Absorption costing for Bittern Ltd....................................................................................4

Table 5: Variable costing for Bittern Ltd.........................................................................................5

Table 6: Absorption costing for Bittern Ltd....................................................................................5

Table 7: Material purchase budget...................................................................................................9

Table 8: Trade payable budgets.......................................................................................................9

Table 9: Cash budget of Antonio for six months...........................................................................10

Table 10: Standard and actual results............................................................................................11

Table 11: Calculation of variances................................................................................................11

Table 12: Operating statement to deduce budget profit for May...................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Cost accounting is a process of analysing and evaluating other alternatives in a business.

It provides detailed information about a product which can be used by the management for

making decisions. It can be helpful in managing and controlling cost in the organisation. In cost

accounting, the activities are generally classified on the basis of products, process and functions

(Costing methods, 2015). The report is based on cost accounting system of Bittern Ltd. The

company has decided to review its system and improve the profitability of their business.

Furthermore, analysis of cost information, methods to reduce costs, forecasting, budgeting and

monitoring techniques used by Bittern Ltd has also been included in the report.

TASK 1

1.1 Different types of costs

The costs can be classified into different categories:

Fixed and variable costs: Fixed costs remain same even if the production increases or

decreases. For example, rent, salaries, insurgence etc. While variable costs change according to

the change in the production volume (DRURY, 2013). It includes wages, inventory, packaging

costs etc. Bittern Ltd. is a manufacturing company so they have to consider both the costs

because it may affect price of the product.

Direct and indirect costs: The costs which can be directly associated to the product,

project or department are called direct costs (Kaplan and Atkinson, 2015). On the other hand,

indirect costs cannot be directly associated to any cost object. For example, salaries, quality

control costs, depreciation etc.

Material, labour and overhead costs: The cost to buy raw material for Bittern Ltd is

called as material cost. On the other hand the cost of labour includes wages, payrolls and other

benefits of the employees (Ellul and et.al., 2015). Overhead costs include all the other costs apart

from material and labour costs. For example, legal fees, taxes, repairs, utilities and travel

expenditures.

Production, administration and distribution costs: The costs which are related to

production of goods are called as the production costs. On the other hand, administration

expenses include cost of management and their activities like stationery, telephone etc (Salako

and Yusuf, 2016). Distribution costs include all the cost which is incurred to sell the product. For

example, discounts, market research and commission.

1

Cost accounting is a process of analysing and evaluating other alternatives in a business.

It provides detailed information about a product which can be used by the management for

making decisions. It can be helpful in managing and controlling cost in the organisation. In cost

accounting, the activities are generally classified on the basis of products, process and functions

(Costing methods, 2015). The report is based on cost accounting system of Bittern Ltd. The

company has decided to review its system and improve the profitability of their business.

Furthermore, analysis of cost information, methods to reduce costs, forecasting, budgeting and

monitoring techniques used by Bittern Ltd has also been included in the report.

TASK 1

1.1 Different types of costs

The costs can be classified into different categories:

Fixed and variable costs: Fixed costs remain same even if the production increases or

decreases. For example, rent, salaries, insurgence etc. While variable costs change according to

the change in the production volume (DRURY, 2013). It includes wages, inventory, packaging

costs etc. Bittern Ltd. is a manufacturing company so they have to consider both the costs

because it may affect price of the product.

Direct and indirect costs: The costs which can be directly associated to the product,

project or department are called direct costs (Kaplan and Atkinson, 2015). On the other hand,

indirect costs cannot be directly associated to any cost object. For example, salaries, quality

control costs, depreciation etc.

Material, labour and overhead costs: The cost to buy raw material for Bittern Ltd is

called as material cost. On the other hand the cost of labour includes wages, payrolls and other

benefits of the employees (Ellul and et.al., 2015). Overhead costs include all the other costs apart

from material and labour costs. For example, legal fees, taxes, repairs, utilities and travel

expenditures.

Production, administration and distribution costs: The costs which are related to

production of goods are called as the production costs. On the other hand, administration

expenses include cost of management and their activities like stationery, telephone etc (Salako

and Yusuf, 2016). Distribution costs include all the cost which is incurred to sell the product. For

example, discounts, market research and commission.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

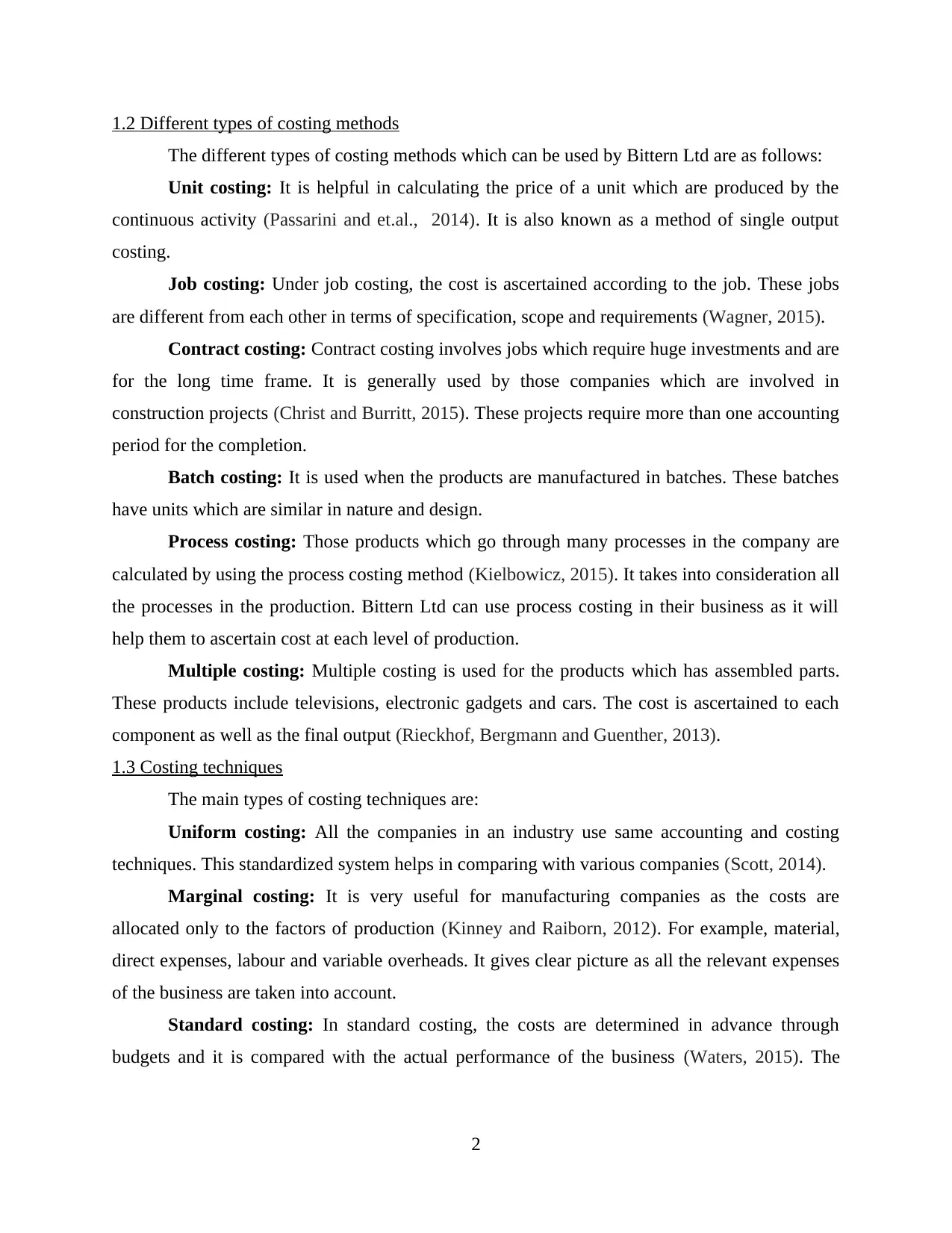

1.2 Different types of costing methods

The different types of costing methods which can be used by Bittern Ltd are as follows:

Unit costing: It is helpful in calculating the price of a unit which are produced by the

continuous activity (Passarini and et.al., 2014). It is also known as a method of single output

costing.

Job costing: Under job costing, the cost is ascertained according to the job. These jobs

are different from each other in terms of specification, scope and requirements (Wagner, 2015).

Contract costing: Contract costing involves jobs which require huge investments and are

for the long time frame. It is generally used by those companies which are involved in

construction projects (Christ and Burritt, 2015). These projects require more than one accounting

period for the completion.

Batch costing: It is used when the products are manufactured in batches. These batches

have units which are similar in nature and design.

Process costing: Those products which go through many processes in the company are

calculated by using the process costing method (Kielbowicz, 2015). It takes into consideration all

the processes in the production. Bittern Ltd can use process costing in their business as it will

help them to ascertain cost at each level of production.

Multiple costing: Multiple costing is used for the products which has assembled parts.

These products include televisions, electronic gadgets and cars. The cost is ascertained to each

component as well as the final output (Rieckhof, Bergmann and Guenther, 2013).

1.3 Costing techniques

The main types of costing techniques are:

Uniform costing: All the companies in an industry use same accounting and costing

techniques. This standardized system helps in comparing with various companies (Scott, 2014).

Marginal costing: It is very useful for manufacturing companies as the costs are

allocated only to the factors of production (Kinney and Raiborn, 2012). For example, material,

direct expenses, labour and variable overheads. It gives clear picture as all the relevant expenses

of the business are taken into account.

Standard costing: In standard costing, the costs are determined in advance through

budgets and it is compared with the actual performance of the business (Waters, 2015). The

2

The different types of costing methods which can be used by Bittern Ltd are as follows:

Unit costing: It is helpful in calculating the price of a unit which are produced by the

continuous activity (Passarini and et.al., 2014). It is also known as a method of single output

costing.

Job costing: Under job costing, the cost is ascertained according to the job. These jobs

are different from each other in terms of specification, scope and requirements (Wagner, 2015).

Contract costing: Contract costing involves jobs which require huge investments and are

for the long time frame. It is generally used by those companies which are involved in

construction projects (Christ and Burritt, 2015). These projects require more than one accounting

period for the completion.

Batch costing: It is used when the products are manufactured in batches. These batches

have units which are similar in nature and design.

Process costing: Those products which go through many processes in the company are

calculated by using the process costing method (Kielbowicz, 2015). It takes into consideration all

the processes in the production. Bittern Ltd can use process costing in their business as it will

help them to ascertain cost at each level of production.

Multiple costing: Multiple costing is used for the products which has assembled parts.

These products include televisions, electronic gadgets and cars. The cost is ascertained to each

component as well as the final output (Rieckhof, Bergmann and Guenther, 2013).

1.3 Costing techniques

The main types of costing techniques are:

Uniform costing: All the companies in an industry use same accounting and costing

techniques. This standardized system helps in comparing with various companies (Scott, 2014).

Marginal costing: It is very useful for manufacturing companies as the costs are

allocated only to the factors of production (Kinney and Raiborn, 2012). For example, material,

direct expenses, labour and variable overheads. It gives clear picture as all the relevant expenses

of the business are taken into account.

Standard costing: In standard costing, the costs are determined in advance through

budgets and it is compared with the actual performance of the business (Waters, 2015). The

2

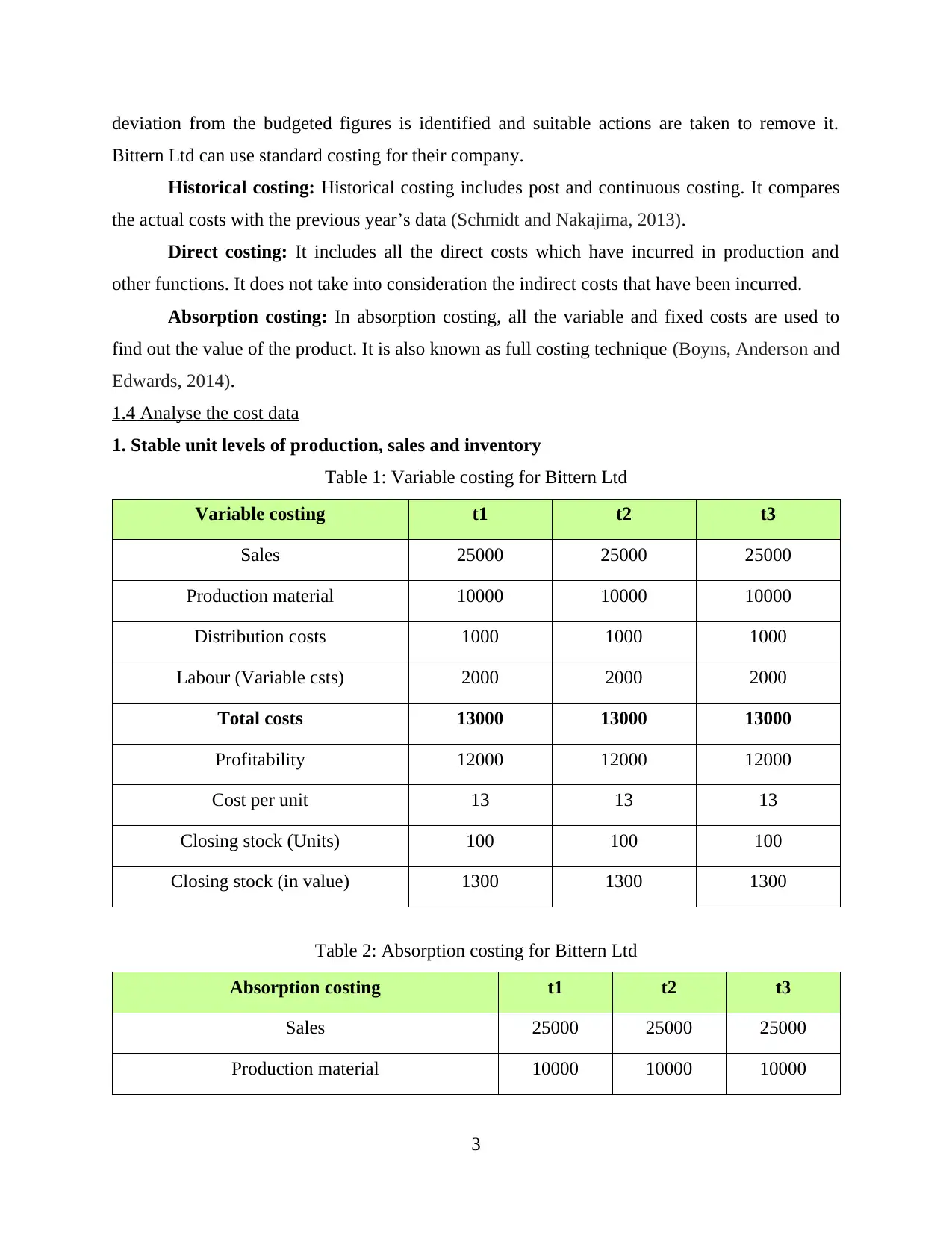

deviation from the budgeted figures is identified and suitable actions are taken to remove it.

Bittern Ltd can use standard costing for their company.

Historical costing: Historical costing includes post and continuous costing. It compares

the actual costs with the previous year’s data (Schmidt and Nakajima, 2013).

Direct costing: It includes all the direct costs which have incurred in production and

other functions. It does not take into consideration the indirect costs that have been incurred.

Absorption costing: In absorption costing, all the variable and fixed costs are used to

find out the value of the product. It is also known as full costing technique (Boyns, Anderson and

Edwards, 2014).

1.4 Analyse the cost data

1. Stable unit levels of production, sales and inventory

Table 1: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable csts) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Absorption costing for Bittern Ltd

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

3

Bittern Ltd can use standard costing for their company.

Historical costing: Historical costing includes post and continuous costing. It compares

the actual costs with the previous year’s data (Schmidt and Nakajima, 2013).

Direct costing: It includes all the direct costs which have incurred in production and

other functions. It does not take into consideration the indirect costs that have been incurred.

Absorption costing: In absorption costing, all the variable and fixed costs are used to

find out the value of the product. It is also known as full costing technique (Boyns, Anderson and

Edwards, 2014).

1.4 Analyse the cost data

1. Stable unit levels of production, sales and inventory

Table 1: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

Distribution costs 1000 1000 1000

Labour (Variable csts) 2000 2000 2000

Total costs 13000 13000 13000

Profitability 12000 12000 12000

Cost per unit 13 13 13

Closing stock (Units) 100 100 100

Closing stock (in value) 1300 1300 1300

Table 2: Absorption costing for Bittern Ltd

Absorption costing t1 t2 t3

Sales 25000 25000 25000

Production material 10000 10000 10000

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

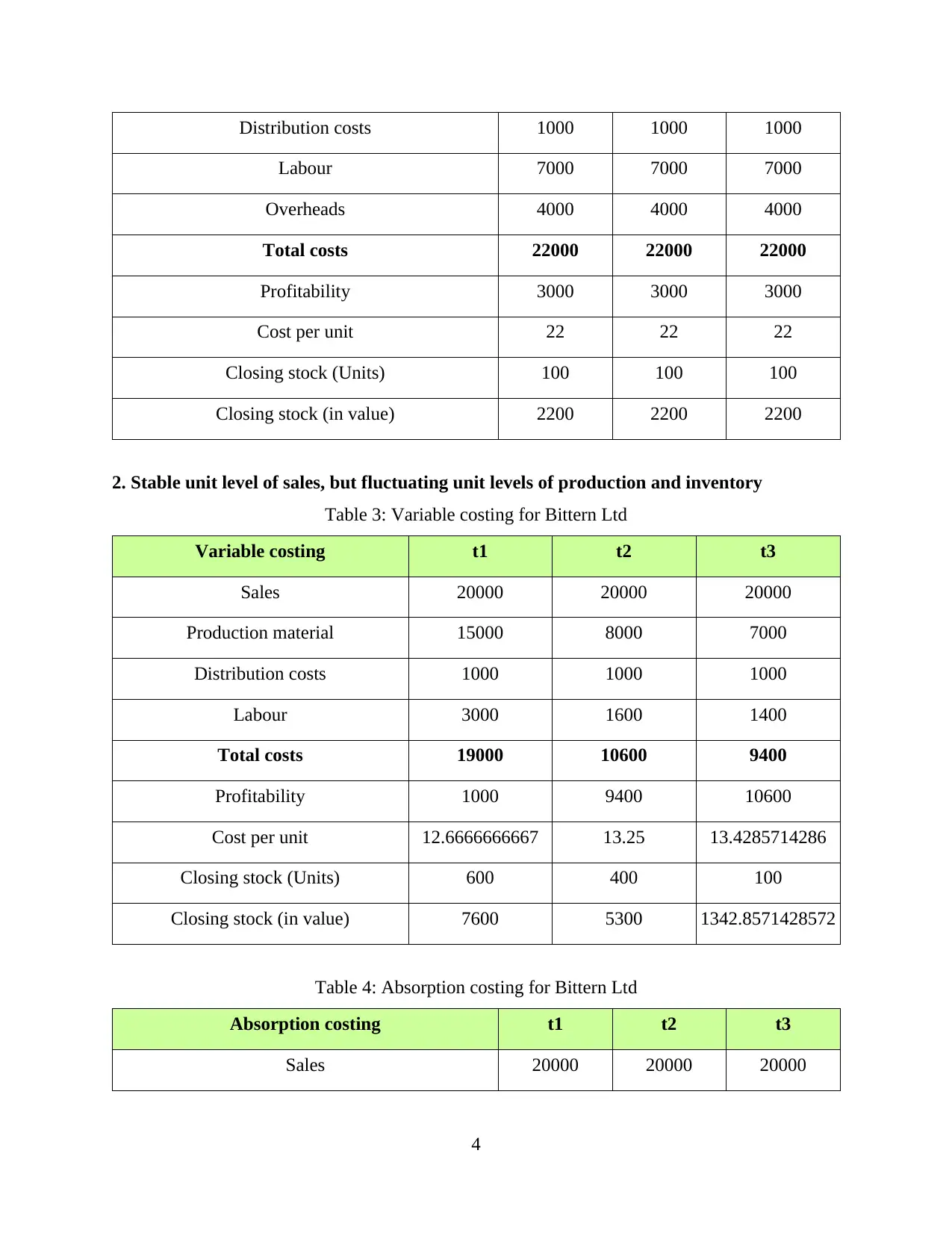

Distribution costs 1000 1000 1000

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

2. Stable unit level of sales, but fluctuating unit levels of production and inventory

Table 3: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Absorption costing for Bittern Ltd

Absorption costing t1 t2 t3

Sales 20000 20000 20000

4

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 22000 22000 22000

Profitability 3000 3000 3000

Cost per unit 22 22 22

Closing stock (Units) 100 100 100

Closing stock (in value) 2200 2200 2200

2. Stable unit level of sales, but fluctuating unit levels of production and inventory

Table 3: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 20000 20000 20000

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 3000 1600 1400

Total costs 19000 10600 9400

Profitability 1000 9400 10600

Cost per unit 12.6666666667 13.25 13.4285714286

Closing stock (Units) 600 400 100

Closing stock (in value) 7600 5300 1342.8571428572

Table 4: Absorption costing for Bittern Ltd

Absorption costing t1 t2 t3

Sales 20000 20000 20000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

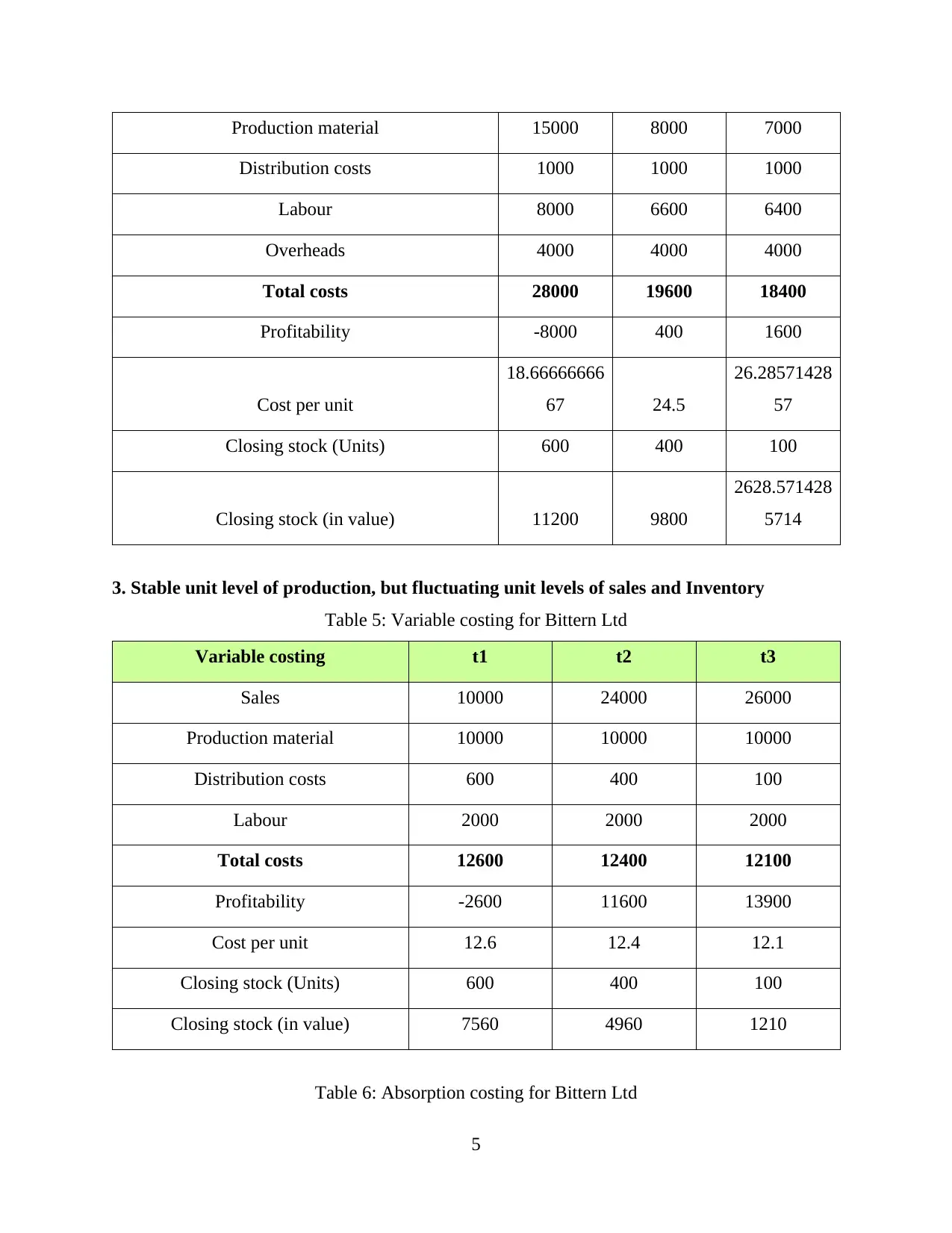

Production material 15000 8000 7000

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Overheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit

18.66666666

67 24.5

26.28571428

57

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.571428

5714

3. Stable unit level of production, but fluctuating unit levels of sales and Inventory

Table 5: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

Closing stock (in value) 7560 4960 1210

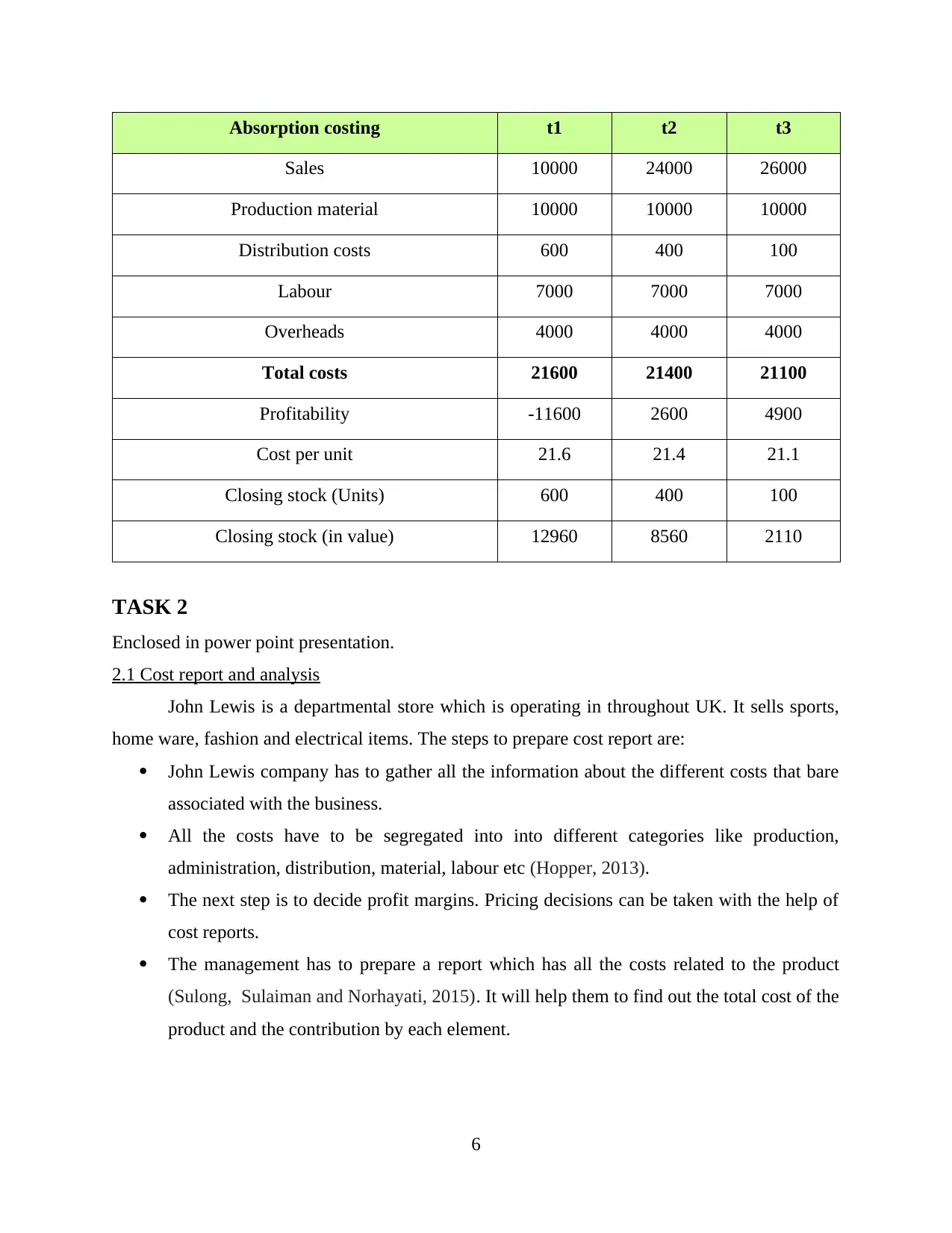

Table 6: Absorption costing for Bittern Ltd

5

Distribution costs 1000 1000 1000

Labour 8000 6600 6400

Overheads 4000 4000 4000

Total costs 28000 19600 18400

Profitability -8000 400 1600

Cost per unit

18.66666666

67 24.5

26.28571428

57

Closing stock (Units) 600 400 100

Closing stock (in value) 11200 9800

2628.571428

5714

3. Stable unit level of production, but fluctuating unit levels of sales and Inventory

Table 5: Variable costing for Bittern Ltd

Variable costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 2000 2000 2000

Total costs 12600 12400 12100

Profitability -2600 11600 13900

Cost per unit 12.6 12.4 12.1

Closing stock (Units) 600 400 100

Closing stock (in value) 7560 4960 1210

Table 6: Absorption costing for Bittern Ltd

5

Absorption costing t1 t2 t3

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 21600 21400 21100

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Enclosed in power point presentation.

2.1 Cost report and analysis

John Lewis is a departmental store which is operating in throughout UK. It sells sports,

home ware, fashion and electrical items. The steps to prepare cost report are:

John Lewis company has to gather all the information about the different costs that bare

associated with the business.

All the costs have to be segregated into into different categories like production,

administration, distribution, material, labour etc (Hopper, 2013).

The next step is to decide profit margins. Pricing decisions can be taken with the help of

cost reports.

The management has to prepare a report which has all the costs related to the product

(Sulong, Sulaiman and Norhayati, 2015). It will help them to find out the total cost of the

product and the contribution by each element.

6

Sales 10000 24000 26000

Production material 10000 10000 10000

Distribution costs 600 400 100

Labour 7000 7000 7000

Overheads 4000 4000 4000

Total costs 21600 21400 21100

Profitability -11600 2600 4900

Cost per unit 21.6 21.4 21.1

Closing stock (Units) 600 400 100

Closing stock (in value) 12960 8560 2110

TASK 2

Enclosed in power point presentation.

2.1 Cost report and analysis

John Lewis is a departmental store which is operating in throughout UK. It sells sports,

home ware, fashion and electrical items. The steps to prepare cost report are:

John Lewis company has to gather all the information about the different costs that bare

associated with the business.

All the costs have to be segregated into into different categories like production,

administration, distribution, material, labour etc (Hopper, 2013).

The next step is to decide profit margins. Pricing decisions can be taken with the help of

cost reports.

The management has to prepare a report which has all the costs related to the product

(Sulong, Sulaiman and Norhayati, 2015). It will help them to find out the total cost of the

product and the contribution by each element.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The cost report can be used to compare the data from the previous reports or from the

standard budgets (Kamala and et.al., 2015). If the actual figures of the company is less

than the budgets, it shows that John Lewis company has been efficient in their operations.

2.2 Various performance indicators used to identify potential improvements

Some of the performance indicators which can be used by John Lewis company are:

Profitability: Cost accounting and budgeting can increase the performance of the

company (García-Unanue, Felipe and Gallardo, 2015). it can be an indication for John Lewis

company that they have been performing well.

Costs: John Lewis company can identify the different costs that are associated to the

product. Fixed costs will continue to incur even if there is no production. So, it is important for

the company to compare the cost of their product to find out the difference.

Efficiency: John Lewis company can compare the efficiency of their company from their

previous data. The labour costs and the output difference can be evaluated to see the difference

in performance. Efficiency can be a useful measure of performance for John Lewis company

(Hocke, Meyer and Lorscheid, 2015).

Productivity: Budgeting and standard costing helps a company to keep a track of their

productivity. It ensures that the factors of production yield the maximum results with least of

wastage. If the labour is not productive then it will affect the revenues. So, productivity has to

be maintained to ensure growth of the business (Costing methods, 2015).

Employee satisfaction: If employees are satisfied then they will perform to the best of

their abilities. Costing can allow management to take important decisions about the labour cost.

2.3 Ways to reduce costs, enhance value and quality

A company cannot grow if they are unable to reduce their costs. They have to

continuously develop and grow their business (How to reduce costs, 2015). The quality of the

products have to be maintained and carefully monitored. It is for the same reason that many

companies have Quality control system in their organisation.

Ways to reduce costs:

Ensuring that the sales volume reach to its break even. At this stage the fixed costs starts

declining. It will increase the profits and cost of the products will reduce.

Refining and taking cost cutting decisions in the company (Sulong, Sulaiman and

Norhayati, 2015).

7

standard budgets (Kamala and et.al., 2015). If the actual figures of the company is less

than the budgets, it shows that John Lewis company has been efficient in their operations.

2.2 Various performance indicators used to identify potential improvements

Some of the performance indicators which can be used by John Lewis company are:

Profitability: Cost accounting and budgeting can increase the performance of the

company (García-Unanue, Felipe and Gallardo, 2015). it can be an indication for John Lewis

company that they have been performing well.

Costs: John Lewis company can identify the different costs that are associated to the

product. Fixed costs will continue to incur even if there is no production. So, it is important for

the company to compare the cost of their product to find out the difference.

Efficiency: John Lewis company can compare the efficiency of their company from their

previous data. The labour costs and the output difference can be evaluated to see the difference

in performance. Efficiency can be a useful measure of performance for John Lewis company

(Hocke, Meyer and Lorscheid, 2015).

Productivity: Budgeting and standard costing helps a company to keep a track of their

productivity. It ensures that the factors of production yield the maximum results with least of

wastage. If the labour is not productive then it will affect the revenues. So, productivity has to

be maintained to ensure growth of the business (Costing methods, 2015).

Employee satisfaction: If employees are satisfied then they will perform to the best of

their abilities. Costing can allow management to take important decisions about the labour cost.

2.3 Ways to reduce costs, enhance value and quality

A company cannot grow if they are unable to reduce their costs. They have to

continuously develop and grow their business (How to reduce costs, 2015). The quality of the

products have to be maintained and carefully monitored. It is for the same reason that many

companies have Quality control system in their organisation.

Ways to reduce costs:

Ensuring that the sales volume reach to its break even. At this stage the fixed costs starts

declining. It will increase the profits and cost of the products will reduce.

Refining and taking cost cutting decisions in the company (Sulong, Sulaiman and

Norhayati, 2015).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Rearranging the asset allocation

Budgeting and using standard costing to compare the performance of the business.

The factors of production like material, labour and overheads have to controlled.

Better utilization of manpower, material and machines. It will help the company to

reduce its cost (Rieckhof, Bergmann and Guenther, 2013).

Ways to enhance quality and value:

Maintaining the same standard of products

Implementation of quality control and budgetary system in the company (Kinney and

Raiborn, 2012).

Use of advanced techniques and technologies for the improving quality of the products.

Effective monitoring and control system should be developed.

Improvements in the efficiency and productivity of the employees.

These steps will allow an organisation to improve their quality, value and their costs will

reduce (Schmidt and Nakajima, 2013). Cost reports can give essential details to the management

so that they can make changes in the policies and functions of the business.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting process allows a business to set standards for revenues and costs for the future.

It has financial goal for the company which they have to achieve in the next one year (Kaplan

and Atkinson, 2015). The major purpose for preparation of budgets by Antonio Ltd are as

follows:

It helps in decision making and management of resources.

Budgets can be used to monitor the performance of the business. The actual expenditure

is compared with the budgeted data to measure the performance (Hocke, Meyer and

Lorscheid, 2015). It allows the company to take decisions against the variations in the

actual performance.

It can be used for financial planning.

It allows the business to forecast their revenues, sales and expenses in the future.

Nature of budgeting process:

Budgeting is a continuous process. It has to be done every year.

It is used to forecast the future revenues and expenses.

8

Budgeting and using standard costing to compare the performance of the business.

The factors of production like material, labour and overheads have to controlled.

Better utilization of manpower, material and machines. It will help the company to

reduce its cost (Rieckhof, Bergmann and Guenther, 2013).

Ways to enhance quality and value:

Maintaining the same standard of products

Implementation of quality control and budgetary system in the company (Kinney and

Raiborn, 2012).

Use of advanced techniques and technologies for the improving quality of the products.

Effective monitoring and control system should be developed.

Improvements in the efficiency and productivity of the employees.

These steps will allow an organisation to improve their quality, value and their costs will

reduce (Schmidt and Nakajima, 2013). Cost reports can give essential details to the management

so that they can make changes in the policies and functions of the business.

TASK 3

3.1 Purpose and nature of budgeting process

Budgeting process allows a business to set standards for revenues and costs for the future.

It has financial goal for the company which they have to achieve in the next one year (Kaplan

and Atkinson, 2015). The major purpose for preparation of budgets by Antonio Ltd are as

follows:

It helps in decision making and management of resources.

Budgets can be used to monitor the performance of the business. The actual expenditure

is compared with the budgeted data to measure the performance (Hocke, Meyer and

Lorscheid, 2015). It allows the company to take decisions against the variations in the

actual performance.

It can be used for financial planning.

It allows the business to forecast their revenues, sales and expenses in the future.

Nature of budgeting process:

Budgeting is a continuous process. It has to be done every year.

It is used to forecast the future revenues and expenses.

8

It is prepared on annual basis (García-Unanue, Felipe and Gallardo, 2015).

Budgets are flexible in nature. They can be altered according to the changes in the

business.

It shows deficits and surplus from the actual expenditure.

Budgets are used as standards of performance.

3.2 Budgeting method and its need

Antonio Ltd can use the following budgeting methods for their company:

Zero based budgeting: Managers considers all the different alternatives to perform an

activity. It requires in depth analysis and evaluation. A manager has to study all the processes of

the business and compare it with other alternatives (Comparing budgeting techniques, 2015).

Many new techniques and methods are introduced with the help of Zero based budgeting. The

main activities in Zero based budgeting are:

Defining an objective

Analysis of cost of various activities

Finding out the alternatives to reach the objective

Formulating the measure of performance

Monitoring and control

Antonio Ltd can use it to make changes in the organisation and start evaluation from a

zero base. They can remove the obsolete and efficient techniques to improve the performance of

the company (Hopper, 2013). Zero based budgeting takes into consideration the changes in the

business environment every year.

Incremental budgeting method: It is a traditional budgeting method. The budgets are

prepared taking the data of the current year's performance and incremental amounts are added to

it. It takes into consideration inflation, planned growth, reductions in costs and expenses.

Incremental budgets are easy to prepare and understand (Boyns, Anderson and Edwards, 2014).

They need less time to prepare and are less expensive than other budgeting process. It is needed

to compare the performance of the business from its past. They give standards of performance

which ensures quality of the products throughout their lives.

9

Budgets are flexible in nature. They can be altered according to the changes in the

business.

It shows deficits and surplus from the actual expenditure.

Budgets are used as standards of performance.

3.2 Budgeting method and its need

Antonio Ltd can use the following budgeting methods for their company:

Zero based budgeting: Managers considers all the different alternatives to perform an

activity. It requires in depth analysis and evaluation. A manager has to study all the processes of

the business and compare it with other alternatives (Comparing budgeting techniques, 2015).

Many new techniques and methods are introduced with the help of Zero based budgeting. The

main activities in Zero based budgeting are:

Defining an objective

Analysis of cost of various activities

Finding out the alternatives to reach the objective

Formulating the measure of performance

Monitoring and control

Antonio Ltd can use it to make changes in the organisation and start evaluation from a

zero base. They can remove the obsolete and efficient techniques to improve the performance of

the company (Hopper, 2013). Zero based budgeting takes into consideration the changes in the

business environment every year.

Incremental budgeting method: It is a traditional budgeting method. The budgets are

prepared taking the data of the current year's performance and incremental amounts are added to

it. It takes into consideration inflation, planned growth, reductions in costs and expenses.

Incremental budgets are easy to prepare and understand (Boyns, Anderson and Edwards, 2014).

They need less time to prepare and are less expensive than other budgeting process. It is needed

to compare the performance of the business from its past. They give standards of performance

which ensures quality of the products throughout their lives.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.