Management Accounting Report: Analysis for Excite Entertainment Ltd.

VerifiedAdded on 2020/12/29

|19

|5378

|470

Report

AI Summary

This report offers a comprehensive analysis of management accounting principles and their application within Excite Entertainment Ltd. It begins by defining management accounting and differentiating it from financial accounting, emphasizing its role in internal decision-making, planning, and performance management. The report then explores various management accounting systems, including cost accounting, inventory management, and job costing, highlighting their benefits for operational efficiency and profitability. Furthermore, the report delves into management accounting reporting methods such as budgeting, cost reports, and performance reports, illustrating how these tools support financial planning and problem-solving. The report also covers the preparation of income statements using absorption and marginal costing, discusses the advantages and disadvantages of planning tools, and outlines strategies for adapting management accounting systems to address financial challenges. The report provides a detailed examination of the financial aspects of Excite Entertainment Ltd., making it a valuable resource for understanding management accounting in practice.

MANAGEMENT

ACCOUNTING

REPORT FOR EXCITE

ENTERTAINMENT

LTD

ACCOUNTING

REPORT FOR EXCITE

ENTERTAINMENT

LTD

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 Management Accounting and its requirements......................................................................1

P2 Methods for management accounting reporting....................................................................5

LO 2.................................................................................................................................................7

P3 Preparation of Income Statement using Absorption & Marginal Costing..............................7

LO 3.................................................................................................................................................8

P4 Advantage & Disadvantage of Planning Tools......................................................................8

LO 4.................................................................................................................................................8

P5 Adaption of management accounting system to resolve financial problems.........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

LO 1.................................................................................................................................................1

P1 Management Accounting and its requirements......................................................................1

P2 Methods for management accounting reporting....................................................................5

LO 2.................................................................................................................................................7

P3 Preparation of Income Statement using Absorption & Marginal Costing..............................7

LO 3.................................................................................................................................................8

P4 Advantage & Disadvantage of Planning Tools......................................................................8

LO 4.................................................................................................................................................8

P5 Adaption of management accounting system to resolve financial problems.........................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management Accounting enable managers of organisations in evaluating its internal

information and making various important decisions so that company can achieve its objectives.

The below report elaborate meaning of management accounting and difference between financial

and management accounting. Further, this report explain different types of management

accounting system. Furthermore, this report include various methods of management accounting

reporting. Moreover, this prepare Income Statement by using Absorption and Marginal Costing.

After that, the below report gives advantage and disadvantage of planning tools. At alst this

report include various methods to resolve financial problems.

LO 1

P1 Management Accounting and its requirements

Financial Accounting and Management Accounting are two methods of accounting used

by business organizations to monitor and control their financial position. Excite Limited is an

UK based company offer services of event management and organises concerts at different

location in the country. As company is operating its business at a large scale it is required by the

accountant of company to manage its accounts and all the other financial transactions and it

becomes possible only when company uses an effective accounting system manage its business

transactions(Boučková, 2015).

Management Accounting

Management Accounting provides all the relevant information related to company to its

managers. Thus, Management Accounting is a process of accounting which is used by managers

of a business firm in decision making, planning and performance management. This accounting

method also enable managers resolving financial problems.

Financial Accounting

Financial Accounting is an activity through which a business firm can record, analyse and

interpret all its financial transactions. With this accounting method Excite Limited can use its

present its financial information in statements and disclose them to its Internal &External Users.

Difference between Management Accounting and Financial Accounting:

Factors Management Accounting Financial accounting

Format of Presentation This accounting method Financial statements are

1

Management Accounting enable managers of organisations in evaluating its internal

information and making various important decisions so that company can achieve its objectives.

The below report elaborate meaning of management accounting and difference between financial

and management accounting. Further, this report explain different types of management

accounting system. Furthermore, this report include various methods of management accounting

reporting. Moreover, this prepare Income Statement by using Absorption and Marginal Costing.

After that, the below report gives advantage and disadvantage of planning tools. At alst this

report include various methods to resolve financial problems.

LO 1

P1 Management Accounting and its requirements

Financial Accounting and Management Accounting are two methods of accounting used

by business organizations to monitor and control their financial position. Excite Limited is an

UK based company offer services of event management and organises concerts at different

location in the country. As company is operating its business at a large scale it is required by the

accountant of company to manage its accounts and all the other financial transactions and it

becomes possible only when company uses an effective accounting system manage its business

transactions(Boučková, 2015).

Management Accounting

Management Accounting provides all the relevant information related to company to its

managers. Thus, Management Accounting is a process of accounting which is used by managers

of a business firm in decision making, planning and performance management. This accounting

method also enable managers resolving financial problems.

Financial Accounting

Financial Accounting is an activity through which a business firm can record, analyse and

interpret all its financial transactions. With this accounting method Excite Limited can use its

present its financial information in statements and disclose them to its Internal &External Users.

Difference between Management Accounting and Financial Accounting:

Factors Management Accounting Financial accounting

Format of Presentation This accounting method Financial statements are

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

provides internal information

of business operations to its

managers such as information

related to Future Financial

Plan or Details of Cost.

E.g. Budget is presented in a

proper format by segregating

Income &

Expenditures(Bromwich and

Scapens, 2016).

prepared by using this

accounting methods such as

Balance Sheet, Income

Statement and Statement of

Cash Flow.

E.g. Balance Sheet is

presented in a prescribed

manner which gives detailed

information of all the assets

and liabilities.

Legal Requirements Not rules and guidelines are

set by government fro the

disclose and presentation of

information related to

management accounting.

Excite Limited can present its

internal information to its

managers in any format which

can be easily understand by the

managers.

All the financial statements

are mandatorily prepared and

presented in the prescribed

format. Excite Limited cannot

prepare its Balance Sheet in

any other format which is not

regulated by government of

UK. Further, it is essential for

the companies to disclose its

financial information to

general public(Carlsson-Wall,

Kraus and Lind, 2015).

Areas of Coverage within the

Organization

This Accounting method

manager all the operational

activities required in

production of companies

products & services. For

Example- Cost Minimization,

Preparation of Production

Budget or Sales Budget and

Financial Accounting control

and manage over all business

performance such as managing

and enhancing financial

performance by disclosing

factual data to investors and

creditors so that investors can

make investment decisions and

2

of business operations to its

managers such as information

related to Future Financial

Plan or Details of Cost.

E.g. Budget is presented in a

proper format by segregating

Income &

Expenditures(Bromwich and

Scapens, 2016).

prepared by using this

accounting methods such as

Balance Sheet, Income

Statement and Statement of

Cash Flow.

E.g. Balance Sheet is

presented in a prescribed

manner which gives detailed

information of all the assets

and liabilities.

Legal Requirements Not rules and guidelines are

set by government fro the

disclose and presentation of

information related to

management accounting.

Excite Limited can present its

internal information to its

managers in any format which

can be easily understand by the

managers.

All the financial statements

are mandatorily prepared and

presented in the prescribed

format. Excite Limited cannot

prepare its Balance Sheet in

any other format which is not

regulated by government of

UK. Further, it is essential for

the companies to disclose its

financial information to

general public(Carlsson-Wall,

Kraus and Lind, 2015).

Areas of Coverage within the

Organization

This Accounting method

manager all the operational

activities required in

production of companies

products & services. For

Example- Cost Minimization,

Preparation of Production

Budget or Sales Budget and

Financial Accounting control

and manage over all business

performance such as managing

and enhancing financial

performance by disclosing

factual data to investors and

creditors so that investors can

make investment decisions and

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

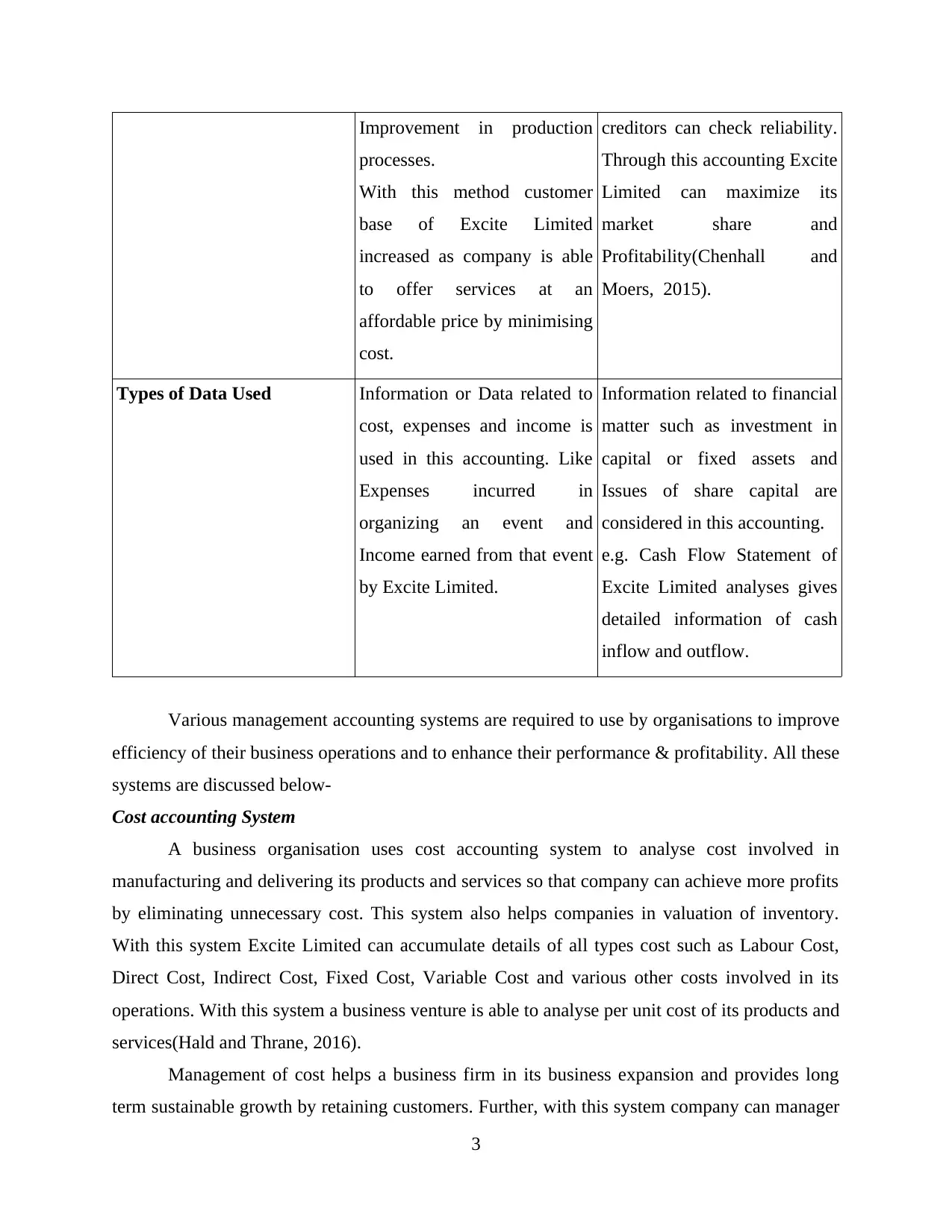

Improvement in production

processes.

With this method customer

base of Excite Limited

increased as company is able

to offer services at an

affordable price by minimising

cost.

creditors can check reliability.

Through this accounting Excite

Limited can maximize its

market share and

Profitability(Chenhall and

Moers, 2015).

Types of Data Used Information or Data related to

cost, expenses and income is

used in this accounting. Like

Expenses incurred in

organizing an event and

Income earned from that event

by Excite Limited.

Information related to financial

matter such as investment in

capital or fixed assets and

Issues of share capital are

considered in this accounting.

e.g. Cash Flow Statement of

Excite Limited analyses gives

detailed information of cash

inflow and outflow.

Various management accounting systems are required to use by organisations to improve

efficiency of their business operations and to enhance their performance & profitability. All these

systems are discussed below-

Cost accounting System

A business organisation uses cost accounting system to analyse cost involved in

manufacturing and delivering its products and services so that company can achieve more profits

by eliminating unnecessary cost. This system also helps companies in valuation of inventory.

With this system Excite Limited can accumulate details of all types cost such as Labour Cost,

Direct Cost, Indirect Cost, Fixed Cost, Variable Cost and various other costs involved in its

operations. With this system a business venture is able to analyse per unit cost of its products and

services(Hald and Thrane, 2016).

Management of cost helps a business firm in its business expansion and provides long

term sustainable growth by retaining customers. Further, with this system company can manager

3

processes.

With this method customer

base of Excite Limited

increased as company is able

to offer services at an

affordable price by minimising

cost.

creditors can check reliability.

Through this accounting Excite

Limited can maximize its

market share and

Profitability(Chenhall and

Moers, 2015).

Types of Data Used Information or Data related to

cost, expenses and income is

used in this accounting. Like

Expenses incurred in

organizing an event and

Income earned from that event

by Excite Limited.

Information related to financial

matter such as investment in

capital or fixed assets and

Issues of share capital are

considered in this accounting.

e.g. Cash Flow Statement of

Excite Limited analyses gives

detailed information of cash

inflow and outflow.

Various management accounting systems are required to use by organisations to improve

efficiency of their business operations and to enhance their performance & profitability. All these

systems are discussed below-

Cost accounting System

A business organisation uses cost accounting system to analyse cost involved in

manufacturing and delivering its products and services so that company can achieve more profits

by eliminating unnecessary cost. This system also helps companies in valuation of inventory.

With this system Excite Limited can accumulate details of all types cost such as Labour Cost,

Direct Cost, Indirect Cost, Fixed Cost, Variable Cost and various other costs involved in its

operations. With this system a business venture is able to analyse per unit cost of its products and

services(Hald and Thrane, 2016).

Management of cost helps a business firm in its business expansion and provides long

term sustainable growth by retaining customers. Further, with this system company can manager

3

its cash inflows and outflows so that it can make further investment decisions. With this system a

company can track its raw material, labour efficiency and inventory level.

Cost Accounting System is an essential requirement of Management Accounting as this

system helps managers in making decisions regarding allocation of cost to the different

departments and helps in planning of next years production budget and other types of budgets.

Direct Cost- Direct Cost is cost specifically incurred in manufacturing of products and

services such as cost of raw material, labour, power consumption and fuel. Direct cost is variable

in accordance with production quantity(Jansen, 2018.).

Standard Cost- Standard cost is an estimated cost that should be incurred in the process

of production. Standard Cost Accounting System is a system with which a company and its

production manager can compare actual cost and estimated cost of production. Further, it helps

company in identifying reason behind the actual and standard cost. E.g. Excite Limited standard

cost that should be involved in organising an event is 1000 Us Dollars and Actual Cost incurred

is 1020 US Dollar than this difference can be analysed with the help of Standard Costing

System(Standard Costing. 2019).

Various Cost Accounting Techniques such as Job Costing, Process Costing, Contract

Costing, Marginal Costing and Services Costing are used by companies to evaluate and measure

cost of different department and different operations. If a company is including variety of

products & services in its portfolio than this techniques benefits it in analysing cost. For

Example- Excite Entertainment Limited is offering event management services than company

can use Service Cost Technique to determine cost of services provided by it. Contract Costing is

also used in case of a big contract related to wedding or any popular event such as

Olympic(Kaplan and Atkinson, 2015).

Inventory Management System

Its is an another requirement of Management Accounting as it helps organisations in

managing their inventory level according to the production demand. Further, Inventory is an

important element with which a company can enhance its production capacity. Supply Chain of a

a company is dependent on the availability of inventory thus, it is necessary for companies to use

Inventory Management System.

With this system managers of company can make decision related to purchase of raw

material and plan production with the available stock. For Example- If managers of Excite

4

company can track its raw material, labour efficiency and inventory level.

Cost Accounting System is an essential requirement of Management Accounting as this

system helps managers in making decisions regarding allocation of cost to the different

departments and helps in planning of next years production budget and other types of budgets.

Direct Cost- Direct Cost is cost specifically incurred in manufacturing of products and

services such as cost of raw material, labour, power consumption and fuel. Direct cost is variable

in accordance with production quantity(Jansen, 2018.).

Standard Cost- Standard cost is an estimated cost that should be incurred in the process

of production. Standard Cost Accounting System is a system with which a company and its

production manager can compare actual cost and estimated cost of production. Further, it helps

company in identifying reason behind the actual and standard cost. E.g. Excite Limited standard

cost that should be involved in organising an event is 1000 Us Dollars and Actual Cost incurred

is 1020 US Dollar than this difference can be analysed with the help of Standard Costing

System(Standard Costing. 2019).

Various Cost Accounting Techniques such as Job Costing, Process Costing, Contract

Costing, Marginal Costing and Services Costing are used by companies to evaluate and measure

cost of different department and different operations. If a company is including variety of

products & services in its portfolio than this techniques benefits it in analysing cost. For

Example- Excite Entertainment Limited is offering event management services than company

can use Service Cost Technique to determine cost of services provided by it. Contract Costing is

also used in case of a big contract related to wedding or any popular event such as

Olympic(Kaplan and Atkinson, 2015).

Inventory Management System

Its is an another requirement of Management Accounting as it helps organisations in

managing their inventory level according to the production demand. Further, Inventory is an

important element with which a company can enhance its production capacity. Supply Chain of a

a company is dependent on the availability of inventory thus, it is necessary for companies to use

Inventory Management System.

With this system managers of company can make decision related to purchase of raw

material and plan production with the available stock. For Example- If managers of Excite

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limited are able to manage its inventory than it can fulfil its customers demand easily which in

turn helps in increasing customer base of a company. Further, this system also helps in optimum

utilisation of available resources and it also enable manager in taking decision as to what type of

inventory is used at first.

This system also supports managers in making decision related to what type of inventory

is used like FIFO or LIFO which in turn enhances production efficiency and output of business

firm. For Example- A company is using FIFO method than goods or raw material which is

recently placed in warehouse are sold first whereas according to LIFO method last added

inventory is used first(Maas, Schaltegger and Crutzen, 2016).

Job Costing System

Job Costing System provides detail information related to cost involved in manufacturing

of each job separately. This system is most widely used by Event Management Companies and

Furniture Manufacturers. Thus, this system is appropriate for Excite Entertainment Limited and

with this this company can track cost of each of its events and concerts.

For Example- Excite Limited is organising three events in a day in different city than

with this system managers of company are able measure cost involved in each of its job offered

or events. Thus, this system is also required in management accounting(Cost Accounting

Systems. 2019).

Benefits of Management Accounting System

Management Accounting system provides stability and long term growth for the

company by minimising different types of risk as this method of accounting is having various

benefits. As with this accounting system Excite Limited can increase its profits by managing

cost and other operational activities. It enable business ventures in producing more products with

which company can get more customers(Malina, 2018).

Further, this system is also beneficial in reducing wastage as all the decisions are made

by the managers by evaluating all the resources and cost which provides optimum utilisation.

Further, it also benefits companies managing inventory by suggesting it an appropriate

inventory management method according to the business of company. Moreover, management

accounting system helps Excite Limited in scheduling all of its operating activities.

5

turn helps in increasing customer base of a company. Further, this system also helps in optimum

utilisation of available resources and it also enable manager in taking decision as to what type of

inventory is used at first.

This system also supports managers in making decision related to what type of inventory

is used like FIFO or LIFO which in turn enhances production efficiency and output of business

firm. For Example- A company is using FIFO method than goods or raw material which is

recently placed in warehouse are sold first whereas according to LIFO method last added

inventory is used first(Maas, Schaltegger and Crutzen, 2016).

Job Costing System

Job Costing System provides detail information related to cost involved in manufacturing

of each job separately. This system is most widely used by Event Management Companies and

Furniture Manufacturers. Thus, this system is appropriate for Excite Entertainment Limited and

with this this company can track cost of each of its events and concerts.

For Example- Excite Limited is organising three events in a day in different city than

with this system managers of company are able measure cost involved in each of its job offered

or events. Thus, this system is also required in management accounting(Cost Accounting

Systems. 2019).

Benefits of Management Accounting System

Management Accounting system provides stability and long term growth for the

company by minimising different types of risk as this method of accounting is having various

benefits. As with this accounting system Excite Limited can increase its profits by managing

cost and other operational activities. It enable business ventures in producing more products with

which company can get more customers(Malina, 2018).

Further, this system is also beneficial in reducing wastage as all the decisions are made

by the managers by evaluating all the resources and cost which provides optimum utilisation.

Further, it also benefits companies managing inventory by suggesting it an appropriate

inventory management method according to the business of company. Moreover, management

accounting system helps Excite Limited in scheduling all of its operating activities.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Methods for management accounting reporting

Managers Accounting Reports are prepared by companies with the purpose of resolving

various organizational problems as with this reports managers make plans of improving their

production process and make decisions so that they can achieve more profits in future. Different

types of management accounting reports are discussed below-

Budget- Budget Report is prepared for projecting future expenses and income of a

company. This report includes details of future financial plan of company and it helps firm in

operating its business in accordance with the budget report so that it can achieve its future

objective. Thus, it benefits managers of business ventures in analysing their performance and

also support production department by controlling cost. Usually Budget Report is prepared by

business organisation on the basis of their past years budget which gives more accuracy and

profits. For Example- With the help of Budget managers of Excite Limited are able to decide

salary and incentives for its employees(Messner, 2016).

Cost Report- Cost Accounting Reports enable manufacturers in computing various types

of costs involved in production process. This report contains information related to cost which

helps managers in determining prices of products and services offered by company by deciding

profit margin. Further, managers also can revise price of products according to the change in

cost. This report also helps managers of Excite Limited in resolving problem of wastage by

providing optimum utilisation of resources.

Performance Report- This report is prepared to analyse performance of company with

which managers can formulate various strategies to achieve future goals. With this report

managers can analyse that companies operations are in accordance with the estimation made in

Budget Report or not and if company is not performing its business activities according to the

budget than managers make a revise budget. With this report HR managers of Excite Limited can

appreciate performance of its employees which also beneficial in retaining and acquiring talented

employees at work place(Tucker and Schaltegger, 2016).

All the information presented in managerial accounting reports should be accurate,

reliable and relevant the to user so that manager can make appropriate decisions and

stakeholders such as shareholders, government, suppliers and creditors so that share holder can

make investment decisions and creditors & government can provide loans to raise capital of

company. Because, if stakeholders of company shows interest in its business than directly

6

Managers Accounting Reports are prepared by companies with the purpose of resolving

various organizational problems as with this reports managers make plans of improving their

production process and make decisions so that they can achieve more profits in future. Different

types of management accounting reports are discussed below-

Budget- Budget Report is prepared for projecting future expenses and income of a

company. This report includes details of future financial plan of company and it helps firm in

operating its business in accordance with the budget report so that it can achieve its future

objective. Thus, it benefits managers of business ventures in analysing their performance and

also support production department by controlling cost. Usually Budget Report is prepared by

business organisation on the basis of their past years budget which gives more accuracy and

profits. For Example- With the help of Budget managers of Excite Limited are able to decide

salary and incentives for its employees(Messner, 2016).

Cost Report- Cost Accounting Reports enable manufacturers in computing various types

of costs involved in production process. This report contains information related to cost which

helps managers in determining prices of products and services offered by company by deciding

profit margin. Further, managers also can revise price of products according to the change in

cost. This report also helps managers of Excite Limited in resolving problem of wastage by

providing optimum utilisation of resources.

Performance Report- This report is prepared to analyse performance of company with

which managers can formulate various strategies to achieve future goals. With this report

managers can analyse that companies operations are in accordance with the estimation made in

Budget Report or not and if company is not performing its business activities according to the

budget than managers make a revise budget. With this report HR managers of Excite Limited can

appreciate performance of its employees which also beneficial in retaining and acquiring talented

employees at work place(Tucker and Schaltegger, 2016).

All the information presented in managerial accounting reports should be accurate,

reliable and relevant the to user so that manager can make appropriate decisions and

stakeholders such as shareholders, government, suppliers and creditors so that share holder can

make investment decisions and creditors & government can provide loans to raise capital of

company. Because, if stakeholders of company shows interest in its business than directly

6

contributes in maximisation of market share and performance. Further, disclosing accurate

information helps managers in making future budget and plans which leads to long term success.

It is also advantageous as with this business can analyse its accurate position in the market. Thus,

it is also necessary fro Excite Limited to disclose all the internal information of company to its

directors, managers and employees if required.

LO 2

P3 Preparation of Income Statement using Absorption & Marginal Costing

Absorption Costing

Absorption Costing is a method of determining cost involved in manufacturing of

products and services by considering both direct as well as Indirect Cost. Direct cost includes

cost of labour, material and direct overheads whereas indirect cost includes cost of

administration, interest and other non operating expenses. This costing is beneficial in filling

income tax returns as it gives net profit after deduction of interest and tax(Management

Accounting – Meaning, Advantages and Limitation. 2019).

Advantage

Most important advantage of absorption cost consider fixed of overhead involved in

manufacturing process.

This method gives actual profits and which helps company in identifying its actual

growth and profitability. Absorption Costing benefits business firms in preparation of financial statements such as

Income Statement, Cash Flow Statement and Balance Sheet.

Disadvantage

With absorption costing managers of business firm cannot monitor and control its

production process as it also includes non operating cost. This method is also not useful for managers in decision making process.

Marginal Costing

Marginal Cost includes cost of additional units manufactured of added thus, this cost is

vary according to change in number of sales units. Thus, Marginal Costing is method which

consider extra cost incurred in manufacturing of additional units and this method is having a

direct impact on profit(Smith and Driscoll, 2017).

Advantage

7

information helps managers in making future budget and plans which leads to long term success.

It is also advantageous as with this business can analyse its accurate position in the market. Thus,

it is also necessary fro Excite Limited to disclose all the internal information of company to its

directors, managers and employees if required.

LO 2

P3 Preparation of Income Statement using Absorption & Marginal Costing

Absorption Costing

Absorption Costing is a method of determining cost involved in manufacturing of

products and services by considering both direct as well as Indirect Cost. Direct cost includes

cost of labour, material and direct overheads whereas indirect cost includes cost of

administration, interest and other non operating expenses. This costing is beneficial in filling

income tax returns as it gives net profit after deduction of interest and tax(Management

Accounting – Meaning, Advantages and Limitation. 2019).

Advantage

Most important advantage of absorption cost consider fixed of overhead involved in

manufacturing process.

This method gives actual profits and which helps company in identifying its actual

growth and profitability. Absorption Costing benefits business firms in preparation of financial statements such as

Income Statement, Cash Flow Statement and Balance Sheet.

Disadvantage

With absorption costing managers of business firm cannot monitor and control its

production process as it also includes non operating cost. This method is also not useful for managers in decision making process.

Marginal Costing

Marginal Cost includes cost of additional units manufactured of added thus, this cost is

vary according to change in number of sales units. Thus, Marginal Costing is method which

consider extra cost incurred in manufacturing of additional units and this method is having a

direct impact on profit(Smith and Driscoll, 2017).

Advantage

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This method is beneficial in short term decision making. With this method managers can control the cost and in this method it is necessary for the

managers to monitor the cost as it keeps changing with the output.

Disadvantage

This method does not consider fixed overheads involved in manufacturing.

This method uses past years data while making estimation related to output which does

not give appropriate results sometimes.

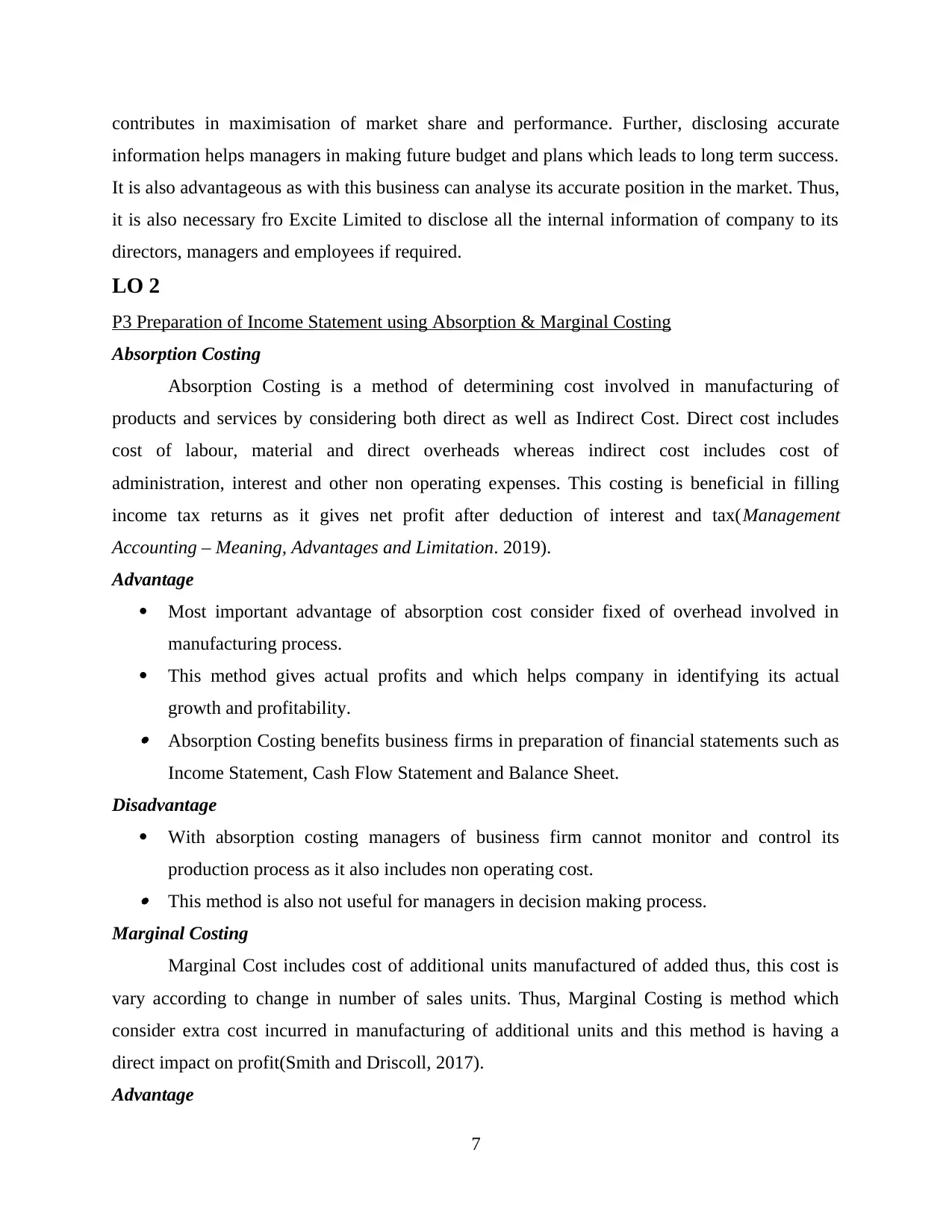

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

Contribution 102000

Less- Fixed Cost -40000

Profit 62000

Income Statement (Absorption Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

8

managers to monitor the cost as it keeps changing with the output.

Disadvantage

This method does not consider fixed overheads involved in manufacturing.

This method uses past years data while making estimation related to output which does

not give appropriate results sometimes.

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

Contribution 102000

Less- Fixed Cost -40000

Profit 62000

Income Statement (Absorption Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less- Fixed Production

Overhead

-40000

Profit 58000

From the above Income Statement it is evaluated that Marginal Costing Method is giving

more profit as compare to adsorption costing.

LO 3

P4 Advantage & Disadvantage of Planning Tools

One of the major planning tool which is used by management is in terms of budgets.

Budgets are the major aspects which helps the companies to prepare their income and

expenditure within a specified periods. This helps the companies to make different strategy by

analysing the particular money left in the company and their technique regarding expansion and

future growth (What is Budget, 2019). Thus, budgets are the financial plan of the company and

usually they are prepared by the management team which is appointed to prepare the complete

budget which recognised their sales, production, actual cost and expenses and total cash flows in

each financial year, Companies uses various planning tool which is used in managing their

accounts are as follows:

Sales Budget: Sales budget means such budget which determines the sales of the

company during the financial years. This budget is mainly prepared to estimated the

profits earned through sales and various other resources which are utilized in sales

activities. As the stability of the company depends upon the sales which they made

during the financial year (Ax and Greve, 2017). So that they can analyse the profits

earned and can prepared the internal team with different products for taking it into sales.

The advantages of Sales budgets are as follows:

It helps the company to plan their activities to bring their products in the market.

Through the sales budget, company know their internal management of the working and

their strategy to adopt the success through such sales process.

By preparing sales budget, company can control their expenses which is incurred without

any providing useful meaning (Carlsson-Wall, Kraus and Lind, 2015).

The disadvantages of sales budget are as follows:

9

Overhead

-40000

Profit 58000

From the above Income Statement it is evaluated that Marginal Costing Method is giving

more profit as compare to adsorption costing.

LO 3

P4 Advantage & Disadvantage of Planning Tools

One of the major planning tool which is used by management is in terms of budgets.

Budgets are the major aspects which helps the companies to prepare their income and

expenditure within a specified periods. This helps the companies to make different strategy by

analysing the particular money left in the company and their technique regarding expansion and

future growth (What is Budget, 2019). Thus, budgets are the financial plan of the company and

usually they are prepared by the management team which is appointed to prepare the complete

budget which recognised their sales, production, actual cost and expenses and total cash flows in

each financial year, Companies uses various planning tool which is used in managing their

accounts are as follows:

Sales Budget: Sales budget means such budget which determines the sales of the

company during the financial years. This budget is mainly prepared to estimated the

profits earned through sales and various other resources which are utilized in sales

activities. As the stability of the company depends upon the sales which they made

during the financial year (Ax and Greve, 2017). So that they can analyse the profits

earned and can prepared the internal team with different products for taking it into sales.

The advantages of Sales budgets are as follows:

It helps the company to plan their activities to bring their products in the market.

Through the sales budget, company know their internal management of the working and

their strategy to adopt the success through such sales process.

By preparing sales budget, company can control their expenses which is incurred without

any providing useful meaning (Carlsson-Wall, Kraus and Lind, 2015).

The disadvantages of sales budget are as follows:

9

1. There are the least chances of flexibility as if the company makes sales budgets which are

not appropriate to actual results then the company while planning is just a waste.

2. Company can't accurately trust on sales budget as they are more fluctuation in

comparison to recent data and previous data (Otley,2016).

In case of excite Entertainment Ltd., Sales budget is mainly prepared by the sales officer

of the company and before making this budget they have to take all the information from various

department such as production, marketing and financial department. After getting all the relevant

information, the sales budget are prepared and this implies the stability of the company to bring

their products in the market.

As under balance score card, it helps the companies to make a strategic management

techniques to identifies the overall activity of the company in internal matters (Qian, Hörisch and

Schaltegger, 2018). As the matters if are sorted with internal activity reflects the external

outcomes regarding the terms of financial matters. If the company finances are strong they can

stable their position in the market.

E.g. As the sales report of 2019, which represents the quarter report of sales relating

activities.

Production Budget: In respect of this budget, companies prepare this budget to

represent the number of units and items which the company is preparing in the financial

year. This determine the working of the company whether it produces some goods or not

deal in any activity(Honggowati and et.al., 2017). This budget is mainly determined

through manufacturing activity and the resources which are utilized to produce a

particular product. The advantages of production budget are as follows:

1. With this budget it helps the companies to know the labour costs and other expense

incurred at the time of production.

10

not appropriate to actual results then the company while planning is just a waste.

2. Company can't accurately trust on sales budget as they are more fluctuation in

comparison to recent data and previous data (Otley,2016).

In case of excite Entertainment Ltd., Sales budget is mainly prepared by the sales officer

of the company and before making this budget they have to take all the information from various

department such as production, marketing and financial department. After getting all the relevant

information, the sales budget are prepared and this implies the stability of the company to bring

their products in the market.

As under balance score card, it helps the companies to make a strategic management

techniques to identifies the overall activity of the company in internal matters (Qian, Hörisch and

Schaltegger, 2018). As the matters if are sorted with internal activity reflects the external

outcomes regarding the terms of financial matters. If the company finances are strong they can

stable their position in the market.

E.g. As the sales report of 2019, which represents the quarter report of sales relating

activities.

Production Budget: In respect of this budget, companies prepare this budget to

represent the number of units and items which the company is preparing in the financial

year. This determine the working of the company whether it produces some goods or not

deal in any activity(Honggowati and et.al., 2017). This budget is mainly determined

through manufacturing activity and the resources which are utilized to produce a

particular product. The advantages of production budget are as follows:

1. With this budget it helps the companies to know the labour costs and other expense

incurred at the time of production.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.