Management Accounting Report: Airdri's Financial Analysis

VerifiedAdded on 2021/02/19

|13

|3730

|18

Report

AI Summary

This report provides a detailed analysis of Airdri's management accounting practices, covering various aspects such as cost accounting, inventory management, and budgetary control. The report begins with an introduction to management accounting and its requirements within an organization, followed by an explanation of different management accounting reporting methods, including budget reports, account receivable aging reports, cost reports, performance reports, and inventory management reports. The report then delves into income statements, comparing absorption costing and marginal costing methods. Furthermore, it examines the benefits and weaknesses of various planning tools used in budgetary control, such as operational budgets and master budgets. Finally, the report concludes with a comparison of companies in resolving financial issues, providing a comprehensive overview of Airdri's financial management strategies and performance.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1.Management accounting and its requirements in an organisation:........................................4

P2: Explain different methods used for management accounting reporting...............................5

TASK 2............................................................................................................................................7

P3.Income statements by absorption costing and marginal costing:...........................................7

TASK 3............................................................................................................................................8

P4.Benefits and weaknesses of different types of panning tools used in budgetary control:.....8

TASK 4..........................................................................................................................................10

P5.Comparison of companies in resolving the financial issues:...............................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................14

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................4

P1.Management accounting and its requirements in an organisation:........................................4

P2: Explain different methods used for management accounting reporting...............................5

TASK 2............................................................................................................................................7

P3.Income statements by absorption costing and marginal costing:...........................................7

TASK 3............................................................................................................................................8

P4.Benefits and weaknesses of different types of panning tools used in budgetary control:.....8

TASK 4..........................................................................................................................................10

P5.Comparison of companies in resolving the financial issues:...............................................10

CONCLUSION..............................................................................................................................11

REFERENCES .............................................................................................................................14

INTRODUCTION

Management accounting that also known as managerial accounting which is a chain of

activities for analysing cost of a business and operations for building financial reports, records

that helps in taking important decisions in achieving financial goals and objectives. It is very

much important for organisation to translate data and statistics into meaningful information from

it. This report is based Airdri which is a hand drying industry founded in Oxfordshire in year

1974 to give best experience to their consumer base by giving best products and services. This

report is based on management accounting and essential requirement of various kinds of

management accounting systems. With various kinds of methods of management accounting

reporting to get reliable outcomes in an organisation. Further it includes varied costs with help of

techniques for preparing income statement with advantages and disadvantages of various kinds

of planning tools for budgetary control. At last comparison in between organisations for adapting

management accounting systems to respond with financial problems or concerns.

TASK 1

P1.Management accounting and its requirements in an organisation:

In management accounting involves building and providing timely financial with statical

data and information to managers of business for taking day to day decisions for accomplishing

organisational goals and objectives (Banerjee, 2012). Information and data which founded in

management accounting is vast in nature and helps to managers in formulating business policies

and plans in taking effective decisions.

There are various types of management accounting systems that are as follows:

Inventory management system:

Cost accounting system:

Management accounting that also known as managerial accounting which is a chain of

activities for analysing cost of a business and operations for building financial reports, records

that helps in taking important decisions in achieving financial goals and objectives. It is very

much important for organisation to translate data and statistics into meaningful information from

it. This report is based Airdri which is a hand drying industry founded in Oxfordshire in year

1974 to give best experience to their consumer base by giving best products and services. This

report is based on management accounting and essential requirement of various kinds of

management accounting systems. With various kinds of methods of management accounting

reporting to get reliable outcomes in an organisation. Further it includes varied costs with help of

techniques for preparing income statement with advantages and disadvantages of various kinds

of planning tools for budgetary control. At last comparison in between organisations for adapting

management accounting systems to respond with financial problems or concerns.

TASK 1

P1.Management accounting and its requirements in an organisation:

In management accounting involves building and providing timely financial with statical

data and information to managers of business for taking day to day decisions for accomplishing

organisational goals and objectives (Banerjee, 2012). Information and data which founded in

management accounting is vast in nature and helps to managers in formulating business policies

and plans in taking effective decisions.

There are various types of management accounting systems that are as follows:

Inventory management system:

Cost accounting system:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost accounting system or costing is an accounting framework that applied in an

organisation to predict or approximate cost of their products for motive of valuation of inventory,

analysis of profitability and controlling cost (Cadez and Guilding, 2012.). In cost accounting

system allocation of the cost should be performed on basis of activity based costing system or by

using traditional costing system. Estimation of actual cost is very much potential for organisation

for effective functioning of various activities. It is an kind of accounting system with motive of

capture and evaluate organisational production cost by weighing inputs cost and includes fixed

cost for taking crucial decisions. In context of Airdri they use cost accounting framework for

evaluation of cost of products and services by evaluating each and every factor associated with it.

Inventory management system:

Inventory management consist of methods or tools to control and evaluate the overseeing

of ordering, usage and storage of various components that are applied in organisation to produce

goods and services that they want to sell (DRURY, 2013. ). It helps in combining various

applications of barcode scanner, desktop software's and mobile devices by streamlining the

management of inventory that are consumables, goods and services and supplier products and

services. It is a important practice for controlling and overseeing quantities of finished products

and services in proper way. In context of Airdri by using inventory management they evaluate

and measure factors that affect inventory in proper by so that effective results should be

accomplished.

Job costing system:

Job costing is an system refers to allocating the cost of manufacturing for an individual

product or batch of a products to get right kind of inputs (Fullerton, Kennedy and Widener,

2014.). For job costing system information should be needed to submit data to ultimate

consumers as per the contract in which costs should be refunded. That kind of information is

very much essential for determining accuracy of system that should be capable for quoting

pricing that reasonable for pricing. In context of Airdri they by using job costing system by

collecting and allocating manufacturing and their resourcing.

Price optimisation system:

Price optimisation system refers to the mathematical application to determine reaction of

consumers to their various price levels regarding their goods and services. It basically applied for

determining of pricing that helps to organisation for fulfilling their goals and objectives to

organisation to predict or approximate cost of their products for motive of valuation of inventory,

analysis of profitability and controlling cost (Cadez and Guilding, 2012.). In cost accounting

system allocation of the cost should be performed on basis of activity based costing system or by

using traditional costing system. Estimation of actual cost is very much potential for organisation

for effective functioning of various activities. It is an kind of accounting system with motive of

capture and evaluate organisational production cost by weighing inputs cost and includes fixed

cost for taking crucial decisions. In context of Airdri they use cost accounting framework for

evaluation of cost of products and services by evaluating each and every factor associated with it.

Inventory management system:

Inventory management consist of methods or tools to control and evaluate the overseeing

of ordering, usage and storage of various components that are applied in organisation to produce

goods and services that they want to sell (DRURY, 2013. ). It helps in combining various

applications of barcode scanner, desktop software's and mobile devices by streamlining the

management of inventory that are consumables, goods and services and supplier products and

services. It is a important practice for controlling and overseeing quantities of finished products

and services in proper way. In context of Airdri by using inventory management they evaluate

and measure factors that affect inventory in proper by so that effective results should be

accomplished.

Job costing system:

Job costing is an system refers to allocating the cost of manufacturing for an individual

product or batch of a products to get right kind of inputs (Fullerton, Kennedy and Widener,

2014.). For job costing system information should be needed to submit data to ultimate

consumers as per the contract in which costs should be refunded. That kind of information is

very much essential for determining accuracy of system that should be capable for quoting

pricing that reasonable for pricing. In context of Airdri they by using job costing system by

collecting and allocating manufacturing and their resourcing.

Price optimisation system:

Price optimisation system refers to the mathematical application to determine reaction of

consumers to their various price levels regarding their goods and services. It basically applied for

determining of pricing that helps to organisation for fulfilling their goals and objectives to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

maximise profit in proper way. In context of Airdri by using they fix optimum pricing that

proved beneficial to reach at large no. of consumer base.

Difference in management and financial accounting:

Management accounting majorly provides information to the people in their organisation

on other hand financial accounting gives information to outsiders such as shareholders to occupy

best results. On other hand financial accounting required by the law and regulations on other

hand management accounting does not required any kind of laws.

P2: Explain different methods used for management accounting reporting.

For an organisation management accounting reporting is very much crucial to gain

desirable outcomes that are as follows:

Budget reports:

Budget managerial accounting reporting is very critical to measure performance of an

organisation and created for organisation as a whole, department wise and for the large

organisation (Herbert and Seal, 2012). Each and every organisation builds or create their own

budget which is a grand plan of a business. A budget should be based on their previous

experiences and from unforeseen circumstances that arise. In context of Airdri they list out all

their major income and expenditures that helps in get accurate results to accumulate right kind of

knowledge and information. Airdri always tries to achieve their goals and objectives as per their

budgeted amount.

Account receivable aging reports:

If an organisation majorly rely on the extending credits then account receivable aging

reports is very much crucial for them (Hilton and Platt, 2013..). Breaking down the balance of

an organisation as per specific time period helps to managers to find out their defaulters by

finding out their issues or problems by collection process of an organisation. After that company

find out kinds of defaulters then organisation tighter their policies to get their money back that is

very much critical for their business. In context of Airdri they use account aging reports to find

out their bad debts and money they have to get from their defaulters.

Cost managerial accounting reports:

Managerial accounting helps in compute the cost of various articles that are come into

manufacturing. In that all raw material cost, overhead cost and labour with another kinds of cost

proved beneficial to reach at large no. of consumer base.

Difference in management and financial accounting:

Management accounting majorly provides information to the people in their organisation

on other hand financial accounting gives information to outsiders such as shareholders to occupy

best results. On other hand financial accounting required by the law and regulations on other

hand management accounting does not required any kind of laws.

P2: Explain different methods used for management accounting reporting.

For an organisation management accounting reporting is very much crucial to gain

desirable outcomes that are as follows:

Budget reports:

Budget managerial accounting reporting is very critical to measure performance of an

organisation and created for organisation as a whole, department wise and for the large

organisation (Herbert and Seal, 2012). Each and every organisation builds or create their own

budget which is a grand plan of a business. A budget should be based on their previous

experiences and from unforeseen circumstances that arise. In context of Airdri they list out all

their major income and expenditures that helps in get accurate results to accumulate right kind of

knowledge and information. Airdri always tries to achieve their goals and objectives as per their

budgeted amount.

Account receivable aging reports:

If an organisation majorly rely on the extending credits then account receivable aging

reports is very much crucial for them (Hilton and Platt, 2013..). Breaking down the balance of

an organisation as per specific time period helps to managers to find out their defaulters by

finding out their issues or problems by collection process of an organisation. After that company

find out kinds of defaulters then organisation tighter their policies to get their money back that is

very much critical for their business. In context of Airdri they use account aging reports to find

out their bad debts and money they have to get from their defaulters.

Cost managerial accounting reports:

Managerial accounting helps in compute the cost of various articles that are come into

manufacturing. In that all raw material cost, overhead cost and labour with another kinds of cost

comes under it. In cost report all kinds of summary of information consisted and gives the

capacity to managers in realisation of costs of various products in against selling prices. In

context of Airdri which estimates profit margins with help of these reports as they provide clear

picture in front of the manager for predicting accurate cost (Strauss, Kristandl and Quinn, 2015).

Performance reports:

Performance reports are very much crucial for an organisation to review the performance

of an organisation as well as performance of each and every employees as per the set standards.

In context of Airdri where departmental performance reports should be generated to measure the

performance of the whole organisation. Managers avails performance reports for taking

important strategic decisions regarding future of an organisation. In that individuals are rewarded

for their performance and commitments and underperformed should be remarked as separately.

These kinds of reports have deep insights regarding working of an organisation in giving their

best for organisational growth and enhancement (Kaplan and Atkinson, 2015). So it is one of

most important report to measure and evaluate performance of each and every individual to get

right kind of results while reviewing performance of an individual to get right outputs.

Inventory management report:

For an organisation inventory management report works to evaluate overall health of an

organisation it helps in gaining important insights about profitability regarding products and

services to evaluate performance at optimum level (Kotas, 2014.). With help of these reports

organisation can by using item fill rate and for getting inventory accuracy to get right kinds of

outputs. It also helps in reducing inventory turnover by calculating it in proper way. In context of

Airdri they uses inventory management report to control each and every attribute related with

inventory so that they can get desirable outcomes.

TASK 2

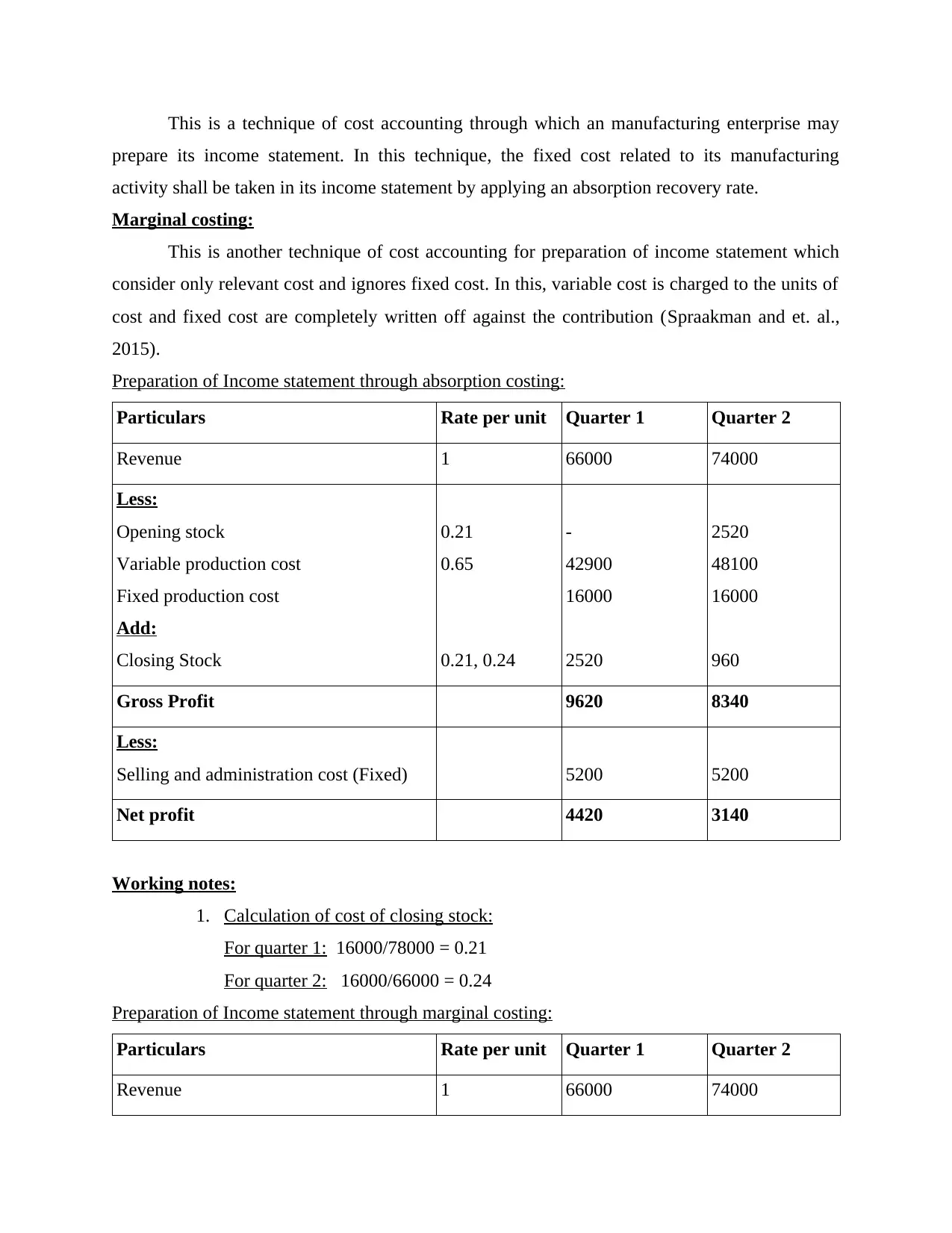

P3.Income statements by absorption costing and marginal costing:

Income statement may be prepared with the help of two techniques of the management

accounting system, the meaning and practical solution for preparation of income statement is

discussed in detail which are as follows:

Absorption costing:

capacity to managers in realisation of costs of various products in against selling prices. In

context of Airdri which estimates profit margins with help of these reports as they provide clear

picture in front of the manager for predicting accurate cost (Strauss, Kristandl and Quinn, 2015).

Performance reports:

Performance reports are very much crucial for an organisation to review the performance

of an organisation as well as performance of each and every employees as per the set standards.

In context of Airdri where departmental performance reports should be generated to measure the

performance of the whole organisation. Managers avails performance reports for taking

important strategic decisions regarding future of an organisation. In that individuals are rewarded

for their performance and commitments and underperformed should be remarked as separately.

These kinds of reports have deep insights regarding working of an organisation in giving their

best for organisational growth and enhancement (Kaplan and Atkinson, 2015). So it is one of

most important report to measure and evaluate performance of each and every individual to get

right kind of results while reviewing performance of an individual to get right outputs.

Inventory management report:

For an organisation inventory management report works to evaluate overall health of an

organisation it helps in gaining important insights about profitability regarding products and

services to evaluate performance at optimum level (Kotas, 2014.). With help of these reports

organisation can by using item fill rate and for getting inventory accuracy to get right kinds of

outputs. It also helps in reducing inventory turnover by calculating it in proper way. In context of

Airdri they uses inventory management report to control each and every attribute related with

inventory so that they can get desirable outcomes.

TASK 2

P3.Income statements by absorption costing and marginal costing:

Income statement may be prepared with the help of two techniques of the management

accounting system, the meaning and practical solution for preparation of income statement is

discussed in detail which are as follows:

Absorption costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This is a technique of cost accounting through which an manufacturing enterprise may

prepare its income statement. In this technique, the fixed cost related to its manufacturing

activity shall be taken in its income statement by applying an absorption recovery rate.

Marginal costing:

This is another technique of cost accounting for preparation of income statement which

consider only relevant cost and ignores fixed cost. In this, variable cost is charged to the units of

cost and fixed cost are completely written off against the contribution (Spraakman and et. al.,

2015).

Preparation of Income statement through absorption costing:

Particulars Rate per unit Quarter 1 Quarter 2

Revenue 1 66000 74000

Less:

Opening stock

Variable production cost

Fixed production cost

Add:

Closing Stock

0.21

0.65

0.21, 0.24

-

42900

16000

2520

2520

48100

16000

960

Gross Profit 9620 8340

Less:

Selling and administration cost (Fixed) 5200 5200

Net profit 4420 3140

Working notes:

1. Calculation of cost of closing stock:

For quarter 1: 16000/78000 = 0.21

For quarter 2: 16000/66000 = 0.24

Preparation of Income statement through marginal costing:

Particulars Rate per unit Quarter 1 Quarter 2

Revenue 1 66000 74000

prepare its income statement. In this technique, the fixed cost related to its manufacturing

activity shall be taken in its income statement by applying an absorption recovery rate.

Marginal costing:

This is another technique of cost accounting for preparation of income statement which

consider only relevant cost and ignores fixed cost. In this, variable cost is charged to the units of

cost and fixed cost are completely written off against the contribution (Spraakman and et. al.,

2015).

Preparation of Income statement through absorption costing:

Particulars Rate per unit Quarter 1 Quarter 2

Revenue 1 66000 74000

Less:

Opening stock

Variable production cost

Fixed production cost

Add:

Closing Stock

0.21

0.65

0.21, 0.24

-

42900

16000

2520

2520

48100

16000

960

Gross Profit 9620 8340

Less:

Selling and administration cost (Fixed) 5200 5200

Net profit 4420 3140

Working notes:

1. Calculation of cost of closing stock:

For quarter 1: 16000/78000 = 0.21

For quarter 2: 16000/66000 = 0.24

Preparation of Income statement through marginal costing:

Particulars Rate per unit Quarter 1 Quarter 2

Revenue 1 66000 74000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Less:

Variable production cost 0.65 42900 48100

Gross Profit 23100 25900

Less:

Fixed production cost

Selling and administration cost (Fixed)

16000

5200

16000

5200

Net profit 1900 4700

Interpretation:

After observing the above solution related to income statements, it is evident that profits

under absorption costing is higher in quarter 1 and lower in quarter 2 as compared to marginal

costing approach, this is because marginal costing approach provides correct profitability of an

enterprises. Therefore, enterprise shall follow the marginal costing approach in preparing its

income statement.

TASK 3

P4.Benefits and weaknesses of different types of panning tools used in budgetary control:

Budget may be defined as a financial plan which is prepared by the manufacturing

enterprise like Nero Ltd. for its future business operations to provide guidance to management

staff and working staff. Budgetary control may be defined as process for setting goals by the

mangers within various budget. In other words, it is an control activity in which actual results are

compared with budgets (Christ and Burritt, 2017).

The various planning tools which are used in budgetary control are as follows:

Operational budget:

This budget assist the companies like Nero Ltd. in performing its day to day operations in

effective and efficient manner.

Benefits: This type of budget helps the company in analysing and evaluating the

different processes such as worker performances related to a specific task and so on.

Variable production cost 0.65 42900 48100

Gross Profit 23100 25900

Less:

Fixed production cost

Selling and administration cost (Fixed)

16000

5200

16000

5200

Net profit 1900 4700

Interpretation:

After observing the above solution related to income statements, it is evident that profits

under absorption costing is higher in quarter 1 and lower in quarter 2 as compared to marginal

costing approach, this is because marginal costing approach provides correct profitability of an

enterprises. Therefore, enterprise shall follow the marginal costing approach in preparing its

income statement.

TASK 3

P4.Benefits and weaknesses of different types of panning tools used in budgetary control:

Budget may be defined as a financial plan which is prepared by the manufacturing

enterprise like Nero Ltd. for its future business operations to provide guidance to management

staff and working staff. Budgetary control may be defined as process for setting goals by the

mangers within various budget. In other words, it is an control activity in which actual results are

compared with budgets (Christ and Burritt, 2017).

The various planning tools which are used in budgetary control are as follows:

Operational budget:

This budget assist the companies like Nero Ltd. in performing its day to day operations in

effective and efficient manner.

Benefits: This type of budget helps the company in analysing and evaluating the

different processes such as worker performances related to a specific task and so on.

Weaknesses: It needs more time and cost in preparation process that makes this budget a

little ineffective and inefficient.

Master budget:

Management accountant of an organisation like Nero Ltd. has responsibility to prepare

this budget which provides the details about the performances of a specific division (department)

of the company.

Benefits: By creating budget related to the performance of a specific budget, it helps the

company in planning the future operations related to such division for improving its

effectiveness and efficiency for increase the

Weaknesses: The important disadvantage of using master budget is non cooperation for

the working staff which may lead to ineffective preparation of this budget that are not

provided any support in growth of an organisation like Nero Ltd (Collis and Hussey,

2017).

Zero-based budget:

It starts in all the department with zero level for their financial requirements. In this

budget, company does not consider previous budget's figures.

Benefits: Preparation of this budget has justified spending, identify redundancies and

focuses on use of resources.

Weaknesses: It includes lot of money and time to prepare this budget and there is loss of

long-term planning (Edwards, 2013).

SWOT analysis:

This is a techniques which is used by the companies like Nero Ltd. the for assessing its

internal and external environment at micro level that support the company in its growth and its

long term survival in such industry. Swot analysis includes the following stages:

Strengths; By using this analysis, company can identify its strengths which are existed in

the internal environment of an business organisation that may help such company in

developing its competitive advantages (Pavlatos, 2015).

Weaknesses: SWOT analysis assists an organisation in identifying its weaknesses which

should be necessary for the company for long term survival without any interruption.

little ineffective and inefficient.

Master budget:

Management accountant of an organisation like Nero Ltd. has responsibility to prepare

this budget which provides the details about the performances of a specific division (department)

of the company.

Benefits: By creating budget related to the performance of a specific budget, it helps the

company in planning the future operations related to such division for improving its

effectiveness and efficiency for increase the

Weaknesses: The important disadvantage of using master budget is non cooperation for

the working staff which may lead to ineffective preparation of this budget that are not

provided any support in growth of an organisation like Nero Ltd (Collis and Hussey,

2017).

Zero-based budget:

It starts in all the department with zero level for their financial requirements. In this

budget, company does not consider previous budget's figures.

Benefits: Preparation of this budget has justified spending, identify redundancies and

focuses on use of resources.

Weaknesses: It includes lot of money and time to prepare this budget and there is loss of

long-term planning (Edwards, 2013).

SWOT analysis:

This is a techniques which is used by the companies like Nero Ltd. the for assessing its

internal and external environment at micro level that support the company in its growth and its

long term survival in such industry. Swot analysis includes the following stages:

Strengths; By using this analysis, company can identify its strengths which are existed in

the internal environment of an business organisation that may help such company in

developing its competitive advantages (Pavlatos, 2015).

Weaknesses: SWOT analysis assists an organisation in identifying its weaknesses which

should be necessary for the company for long term survival without any interruption.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Opportunities: Opportunities are existed in external environment of an company which

provides various benefits to such company such as increase in the sales and profitability

for permanent state and other related aspects.

Threats: These are existed in external environment that provides interruption in the

function of business operations which should be identifies through applying SWOT

analysis for smooth functioning of business operations in effective and efficient manner

without any delay (Fadzil and Rababah, 2012).

TASK 4

P5.Comparison of companies in resolving the financial issues:

Businesses face challenges in the form of the ways as to how can they adapt to newer

business models, devise new strategies and ascertain modern procedures to reasonably deal with

macro factors while creating value to its shareholders as well as achieving financial success.

Only some established organisation can satisfy the needs of over growing challenges at the wake

of the hour. The major issue is the organisations are failing to address the key benefits which

comes from management accounting imparting wisdom to take robust decisions. Management

accounting provides a broader scope to the whole decision-making mechanism by adding

technical rational to it , helping the managers to be cautious in the future and eliminate the

existing risks in phased manner (Nørreklit, 2017).

Organisational responses to financial problems through management accounting:

The primary objective of a centralised management structure is to identify the key

financial issues which are controlling the flow of decision-maker. These issues disturb the

harmony of an organisation in a way that they devoid systematic flow of processes. However in

order to identify these key financial issues management uses various devices like budgetary

targets control, analysis through key performance indicators, benchmarking techniques,

variances in the budgeted statements by determining the evidential skewness in the budgets etc.

(Farouk, Cherian and Jacob, 2012).

The other issue that arises at the door step of any organisation is the application of ethical

practices. Majority of organisations lack in their pursuit for a good financial governance code.

They lack to seek successful the right use of right thing at the right place at right time. This

disruption in the mechanised flow of financial information creates more disruption in an

provides various benefits to such company such as increase in the sales and profitability

for permanent state and other related aspects.

Threats: These are existed in external environment that provides interruption in the

function of business operations which should be identifies through applying SWOT

analysis for smooth functioning of business operations in effective and efficient manner

without any delay (Fadzil and Rababah, 2012).

TASK 4

P5.Comparison of companies in resolving the financial issues:

Businesses face challenges in the form of the ways as to how can they adapt to newer

business models, devise new strategies and ascertain modern procedures to reasonably deal with

macro factors while creating value to its shareholders as well as achieving financial success.

Only some established organisation can satisfy the needs of over growing challenges at the wake

of the hour. The major issue is the organisations are failing to address the key benefits which

comes from management accounting imparting wisdom to take robust decisions. Management

accounting provides a broader scope to the whole decision-making mechanism by adding

technical rational to it , helping the managers to be cautious in the future and eliminate the

existing risks in phased manner (Nørreklit, 2017).

Organisational responses to financial problems through management accounting:

The primary objective of a centralised management structure is to identify the key

financial issues which are controlling the flow of decision-maker. These issues disturb the

harmony of an organisation in a way that they devoid systematic flow of processes. However in

order to identify these key financial issues management uses various devices like budgetary

targets control, analysis through key performance indicators, benchmarking techniques,

variances in the budgeted statements by determining the evidential skewness in the budgets etc.

(Farouk, Cherian and Jacob, 2012).

The other issue that arises at the door step of any organisation is the application of ethical

practices. Majority of organisations lack in their pursuit for a good financial governance code.

They lack to seek successful the right use of right thing at the right place at right time. This

disruption in the mechanised flow of financial information creates more disruption in an

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organisation. To come out of this chaotic situation an organisation needs to come out of the

shackles of traditional governance models and to develop robust financial information flow

channels with profound systems to support the flow (Gond, J. P., and et. al., 2012).

Thirdly, an organisation must address the need for management accounting and a good

management accounting system. They must address that applying correct management

accounting principles will only develop the capacity building structure. The organisation needs

to use full disclosure principles through meeting financial reporting standards. The critical steps

to a successful and sustainable business are :

Constantly evaluate the global trends which are impacting the business scenario around

the globe.

Address key determinants in the industry which are determining the shift in the

management style, processing, operations, laws etc.

Build a linkage between various functional areas with the sustainable goals of the

organisation, develop new models which suits the corporate identity of the business,

always keep on building new outlook.

Keep on developing KPI which may play a key role in the development in the decision-

making paving a way for incremental judgement mechanism.

By emancipating key tools and principles of management accounting like carbon foot

printing, lifestyle costing, natural resource premises sustainability, and other factors into

a decision-making model.

Ensure that all matters of financial and non financial nature are met through the

sustainability model of the business. Construct a solid reporting system along with a more

rock solid management accounting system to build an over growing contributory

organisation to the society at large (Huang, Teoh and Zhang, 2013).

CONCLUSION

From the above report it has been concluded that management accounting is very much

important for an organisation to deal in effective manner with financial concerns. In an

organisation various kinds of management accounting systems and tools should be used that are

cost accounting system, job costing system and many more. To coordinate and evaluate various

aspects organisation have to use accounting reporting that are budget reports, performance

reports and many more that are helps in evaluate hidden factors related with finance. These tools

shackles of traditional governance models and to develop robust financial information flow

channels with profound systems to support the flow (Gond, J. P., and et. al., 2012).

Thirdly, an organisation must address the need for management accounting and a good

management accounting system. They must address that applying correct management

accounting principles will only develop the capacity building structure. The organisation needs

to use full disclosure principles through meeting financial reporting standards. The critical steps

to a successful and sustainable business are :

Constantly evaluate the global trends which are impacting the business scenario around

the globe.

Address key determinants in the industry which are determining the shift in the

management style, processing, operations, laws etc.

Build a linkage between various functional areas with the sustainable goals of the

organisation, develop new models which suits the corporate identity of the business,

always keep on building new outlook.

Keep on developing KPI which may play a key role in the development in the decision-

making paving a way for incremental judgement mechanism.

By emancipating key tools and principles of management accounting like carbon foot

printing, lifestyle costing, natural resource premises sustainability, and other factors into

a decision-making model.

Ensure that all matters of financial and non financial nature are met through the

sustainability model of the business. Construct a solid reporting system along with a more

rock solid management accounting system to build an over growing contributory

organisation to the society at large (Huang, Teoh and Zhang, 2013).

CONCLUSION

From the above report it has been concluded that management accounting is very much

important for an organisation to deal in effective manner with financial concerns. In an

organisation various kinds of management accounting systems and tools should be used that are

cost accounting system, job costing system and many more. To coordinate and evaluate various

aspects organisation have to use accounting reporting that are budget reports, performance

reports and many more that are helps in evaluate hidden factors related with finance. These tools

and techniques proved beneficial for eradicating various kinds of financial problems and

concerns that are lack in resources and funds that hinders self interest of an organisation to get

their desirable outcomes.

concerns that are lack in resources and funds that hinders self interest of an organisation to get

their desirable outcomes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.