Comprehensive Management Accounting Report for Imda Tech

VerifiedAdded on 2020/07/22

|13

|3516

|482

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles and their application within the context of Imda Tech, a company manufacturing chargers and electronic gadgets. The report begins with an introduction to management accounting, differentiating it from financial accounting and highlighting its significance in making effective business decisions. It then delves into various management accounting systems, including cost accounting, inventory management, job costing, and price optimization. The report further explores financial statement analysis, comparing income statements prepared using absorption and marginal costing methods. Additionally, it examines different budgeting techniques, including cash and sales budgets, along with their merits, demerits, and the procedure for budget preparation. The report also covers different pricing tactics used by Imda Tech. Finally, the report concludes with an analysis of the Balanced Scorecard (BSC) and its application in identifying financial issues and enhancing financial governance. The report offers a practical understanding of management accounting concepts and their implications for business decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. i. Defining management accounting and differentiate with financial accounting.............1

A. ii. Significance of MA in order to make effective business decisions..............................2

B. Various kinds of systems of MA and their use in departments.........................................2

Cost accounting system..........................................................................................................2

Inventory management system...............................................................................................3

Job costing system..................................................................................................................3

Price optimisation system.......................................................................................................3

TASK 2............................................................................................................................................4

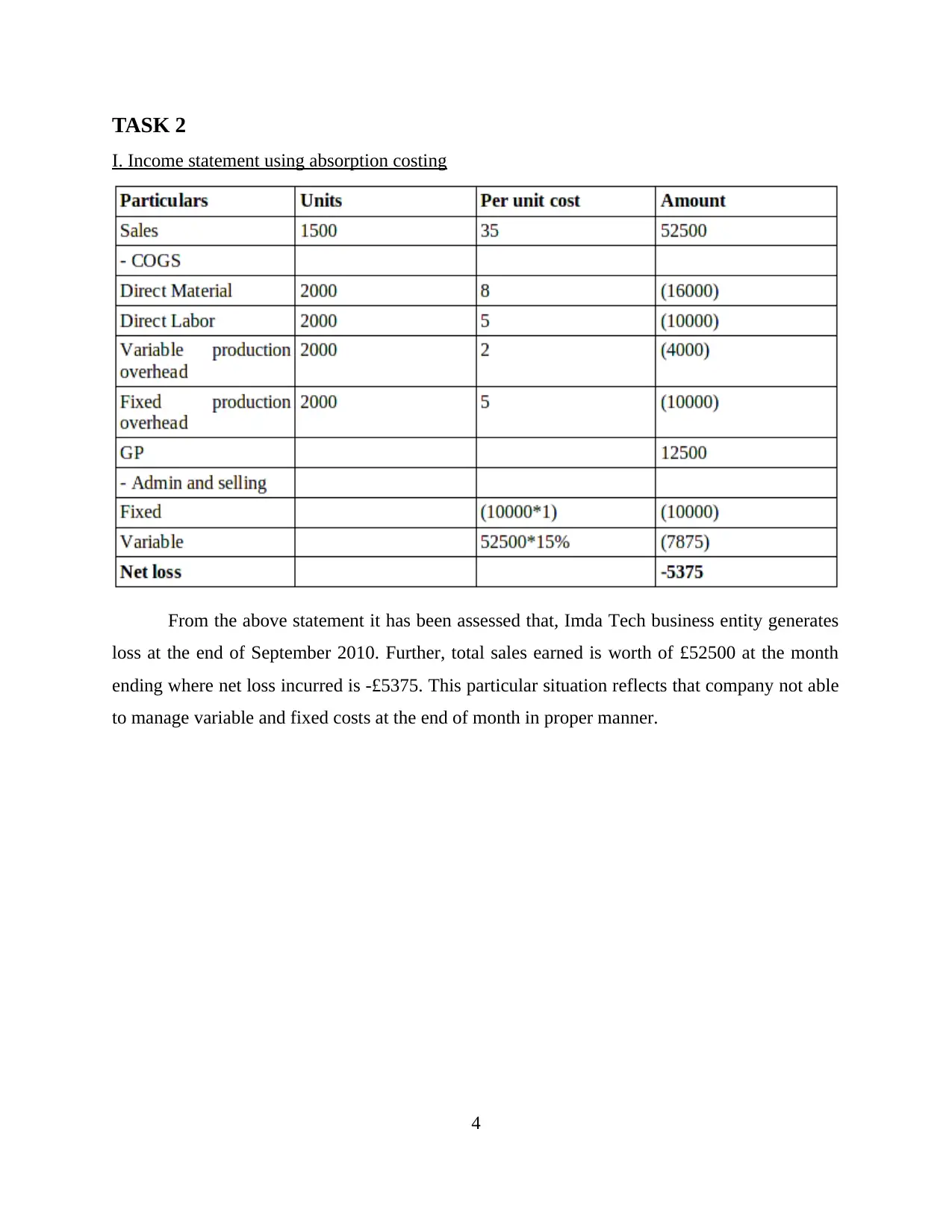

I. Income statement using absorption costing........................................................................4

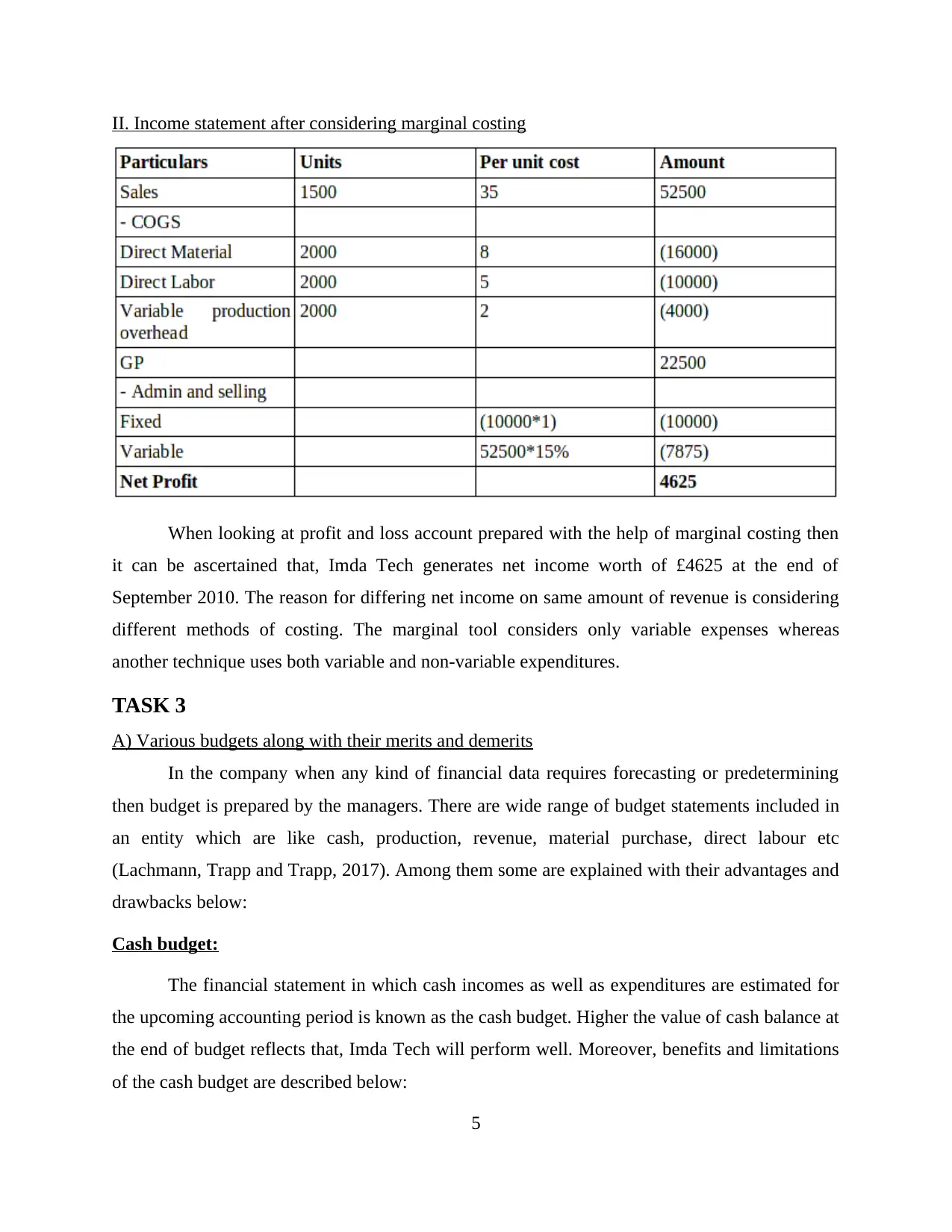

II. Income statement after considering marginal costing.......................................................5

TASK 3............................................................................................................................................5

A) Various budgets along with their merits and demerits......................................................5

B) Procedure in order to prepare budgets...............................................................................6

C) Different pricing tactics.....................................................................................................7

TASK 4............................................................................................................................................8

A. I. Ways through which BSC used for identifying and responding financial issues..........8

A. II. Use of BSC in order to enhance financial governance and frame effectual strategies. 9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. i. Defining management accounting and differentiate with financial accounting.............1

A. ii. Significance of MA in order to make effective business decisions..............................2

B. Various kinds of systems of MA and their use in departments.........................................2

Cost accounting system..........................................................................................................2

Inventory management system...............................................................................................3

Job costing system..................................................................................................................3

Price optimisation system.......................................................................................................3

TASK 2............................................................................................................................................4

I. Income statement using absorption costing........................................................................4

II. Income statement after considering marginal costing.......................................................5

TASK 3............................................................................................................................................5

A) Various budgets along with their merits and demerits......................................................5

B) Procedure in order to prepare budgets...............................................................................6

C) Different pricing tactics.....................................................................................................7

TASK 4............................................................................................................................................8

A. I. Ways through which BSC used for identifying and responding financial issues..........8

A. II. Use of BSC in order to enhance financial governance and frame effectual strategies. 9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION

The system under which management reports as well as accounts are framed for taking

internal business decisions, considered as the management accounting (MA). The present report

focuses on the Imda Tech company which manufactures special charger as well as some

electronic gadgets. The study describes about management accounting, its importance in the

company along with its several systems. Further, income statements are prepared on the basis of

two methods like marginal and absorption. Beside this, about the different budgets, process of

preparing such statements as well as various pricing strategies are explained in the present

project. At the end of report, Balanced Scorecard (BSC) is described along with its uses within

workplace of the Imda Tech firm.

TASK 1

A. i. Defining management accounting and differentiate with financial accounting

A process in which financial data planned, implemented, organised as well as controlled

within workplace in order to make it financially sound is considered as the management

accounting. In context to this, as the managers of Imda Tech entity considers this particular

system within workplace then able to enhance financial performance in the relevant industry. It

differs from the financial accounting which stated as below:

Management accounting Financial accounting

The system which focuses on financial plans as

well as tactics for operating business in

profitable direction is known as management

accounting (Granlund and Lukka, 2017).

An approach of accounting where financial

statements are prepared for assessing business

performance is considered as financial

accounting (FA).

For the entities it is not necessary to use MA in

the firm.

On the other hand, it is mandatory for Imda

Tech to use FA within working environment.

Users of the MA are only internal stakeholders

or management of the cited firm.

The financial accounting used by both external

and internal stakeholders.

1

The system under which management reports as well as accounts are framed for taking

internal business decisions, considered as the management accounting (MA). The present report

focuses on the Imda Tech company which manufactures special charger as well as some

electronic gadgets. The study describes about management accounting, its importance in the

company along with its several systems. Further, income statements are prepared on the basis of

two methods like marginal and absorption. Beside this, about the different budgets, process of

preparing such statements as well as various pricing strategies are explained in the present

project. At the end of report, Balanced Scorecard (BSC) is described along with its uses within

workplace of the Imda Tech firm.

TASK 1

A. i. Defining management accounting and differentiate with financial accounting

A process in which financial data planned, implemented, organised as well as controlled

within workplace in order to make it financially sound is considered as the management

accounting. In context to this, as the managers of Imda Tech entity considers this particular

system within workplace then able to enhance financial performance in the relevant industry. It

differs from the financial accounting which stated as below:

Management accounting Financial accounting

The system which focuses on financial plans as

well as tactics for operating business in

profitable direction is known as management

accounting (Granlund and Lukka, 2017).

An approach of accounting where financial

statements are prepared for assessing business

performance is considered as financial

accounting (FA).

For the entities it is not necessary to use MA in

the firm.

On the other hand, it is mandatory for Imda

Tech to use FA within working environment.

Users of the MA are only internal stakeholders

or management of the cited firm.

The financial accounting used by both external

and internal stakeholders.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Through this, upcoming financial information

determined with the help of budget

preparation.

While, FA provides past financial data which

supports to analyse past business performance.

Any specified formates are not used while

framing reports under the MA.

In order to prepare reports under FA, specified

formates taken into consideration.

Not required to consider auditing as well as

publishing system in the management

accounting.

Under the financial accounting, it is mandatory

to publish final accounts along with the

auditing procedure.

A. ii. Significance of MA in order to make effective business decisions

Management accounting is basically considered at the internal business level in order to

make fruitful decisions. Further, its importance for Imda Tech as a tool of decision-making

within workplace is described below:

The management accounting system supports to the firm for preparing budgets and

forecast future financial information in an appropriate direction. On the basis of different

budget statements, the manager frames strategies for making changes or modifications in

the firm (Ax and Greve, 2017). Moreover, when financial performance predetermined

then highly fruitful as well as the profitable business decisions are made.

Apart from this, MA helps to make analysis of the costs associated with each and every

activity of business procedures. During this, if Imda Tech founds that expenses incurred

in higher amount at specific stage or activity then take corrective actions for reducing the

issue. Therefore, it can be said that MA is an important to make cost decisions and

strategies within working environment.

Another significance of the management accounting is for utilising available resources

and data in the firm properly. On the basis of financial projections upcoming performance

is easily assessed by which manager decides that which data needs to utilise in optimum

manner (Lapsley and Rekers, 2017).

2

determined with the help of budget

preparation.

While, FA provides past financial data which

supports to analyse past business performance.

Any specified formates are not used while

framing reports under the MA.

In order to prepare reports under FA, specified

formates taken into consideration.

Not required to consider auditing as well as

publishing system in the management

accounting.

Under the financial accounting, it is mandatory

to publish final accounts along with the

auditing procedure.

A. ii. Significance of MA in order to make effective business decisions

Management accounting is basically considered at the internal business level in order to

make fruitful decisions. Further, its importance for Imda Tech as a tool of decision-making

within workplace is described below:

The management accounting system supports to the firm for preparing budgets and

forecast future financial information in an appropriate direction. On the basis of different

budget statements, the manager frames strategies for making changes or modifications in

the firm (Ax and Greve, 2017). Moreover, when financial performance predetermined

then highly fruitful as well as the profitable business decisions are made.

Apart from this, MA helps to make analysis of the costs associated with each and every

activity of business procedures. During this, if Imda Tech founds that expenses incurred

in higher amount at specific stage or activity then take corrective actions for reducing the

issue. Therefore, it can be said that MA is an important to make cost decisions and

strategies within working environment.

Another significance of the management accounting is for utilising available resources

and data in the firm properly. On the basis of financial projections upcoming performance

is easily assessed by which manager decides that which data needs to utilise in optimum

manner (Lapsley and Rekers, 2017).

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

B. Various kinds of systems of MA and their use in departments

Under the management accounting different kinds of approaches and systems are

included which helps to various departments. Further, such systems are described below:

Cost accounting system

An approach in which various kinds of expenditures associated within workplace of a

company are analysed is known as cost accounting system. It generally used by the cost centre

and accounting department of the company where expenses related data transacted. Further,

basic use of this system is to assess production cost which supports to make pricing decisions.

Inventory management system

According to this framework, stock available in the workplace are managed in order to

boost up total financial performance at the end of year. As the level of stock is properly managed

and reduced in Imda Tech then it will support to increase sales. Under this, valuation of

inventory is also analysed by the manager where basically three methods used like FIFO, LIFO

and weighted average (Soderstrom, Soderstrom and Stewart, 2017).

Job costing system

When costs and expenses of products on the basis of job are needed to analyse in the

company then job costing system is undertaken by the management. The Imda Tech business

produces products in basically two job order like special charges for mobile phone and other

electronic gadgets. Moreover, for determining cost of each job product this method is taken into

consideration.

Price optimisation system

Another system of management accounting is price optimisation which helps to the entity

bin order to make profitable pricing decisions while selling products and services. The Imda

Tech firm charges different price level where number of customers also varied. Further, this

system helps to it for analysing a specific price at which more number of consumers respond and

used for selling in the market.

3

Under the management accounting different kinds of approaches and systems are

included which helps to various departments. Further, such systems are described below:

Cost accounting system

An approach in which various kinds of expenditures associated within workplace of a

company are analysed is known as cost accounting system. It generally used by the cost centre

and accounting department of the company where expenses related data transacted. Further,

basic use of this system is to assess production cost which supports to make pricing decisions.

Inventory management system

According to this framework, stock available in the workplace are managed in order to

boost up total financial performance at the end of year. As the level of stock is properly managed

and reduced in Imda Tech then it will support to increase sales. Under this, valuation of

inventory is also analysed by the manager where basically three methods used like FIFO, LIFO

and weighted average (Soderstrom, Soderstrom and Stewart, 2017).

Job costing system

When costs and expenses of products on the basis of job are needed to analyse in the

company then job costing system is undertaken by the management. The Imda Tech business

produces products in basically two job order like special charges for mobile phone and other

electronic gadgets. Moreover, for determining cost of each job product this method is taken into

consideration.

Price optimisation system

Another system of management accounting is price optimisation which helps to the entity

bin order to make profitable pricing decisions while selling products and services. The Imda

Tech firm charges different price level where number of customers also varied. Further, this

system helps to it for analysing a specific price at which more number of consumers respond and

used for selling in the market.

3

TASK 2

I. Income statement using absorption costing

From the above statement it has been assessed that, Imda Tech business entity generates

loss at the end of September 2010. Further, total sales earned is worth of £52500 at the month

ending where net loss incurred is -£5375. This particular situation reflects that company not able

to manage variable and fixed costs at the end of month in proper manner.

4

I. Income statement using absorption costing

From the above statement it has been assessed that, Imda Tech business entity generates

loss at the end of September 2010. Further, total sales earned is worth of £52500 at the month

ending where net loss incurred is -£5375. This particular situation reflects that company not able

to manage variable and fixed costs at the end of month in proper manner.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

II. Income statement after considering marginal costing

When looking at profit and loss account prepared with the help of marginal costing then

it can be ascertained that, Imda Tech generates net income worth of £4625 at the end of

September 2010. The reason for differing net income on same amount of revenue is considering

different methods of costing. The marginal tool considers only variable expenses whereas

another technique uses both variable and non-variable expenditures.

TASK 3

A) Various budgets along with their merits and demerits

In the company when any kind of financial data requires forecasting or predetermining

then budget is prepared by the managers. There are wide range of budget statements included in

an entity which are like cash, production, revenue, material purchase, direct labour etc

(Lachmann, Trapp and Trapp, 2017). Among them some are explained with their advantages and

drawbacks below:

Cash budget:

The financial statement in which cash incomes as well as expenditures are estimated for

the upcoming accounting period is known as the cash budget. Higher the value of cash balance at

the end of budget reflects that, Imda Tech will perform well. Moreover, benefits and limitations

of the cash budget are described below:

5

When looking at profit and loss account prepared with the help of marginal costing then

it can be ascertained that, Imda Tech generates net income worth of £4625 at the end of

September 2010. The reason for differing net income on same amount of revenue is considering

different methods of costing. The marginal tool considers only variable expenses whereas

another technique uses both variable and non-variable expenditures.

TASK 3

A) Various budgets along with their merits and demerits

In the company when any kind of financial data requires forecasting or predetermining

then budget is prepared by the managers. There are wide range of budget statements included in

an entity which are like cash, production, revenue, material purchase, direct labour etc

(Lachmann, Trapp and Trapp, 2017). Among them some are explained with their advantages and

drawbacks below:

Cash budget:

The financial statement in which cash incomes as well as expenditures are estimated for

the upcoming accounting period is known as the cash budget. Higher the value of cash balance at

the end of budget reflects that, Imda Tech will perform well. Moreover, benefits and limitations

of the cash budget are described below:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The cash budget supports to management of Imda Tech in order to concentrate on the

financials after considering to the plan prepared. For enhancing effective communication within

workplace and establishing better coordination among employees it is one of the importance tool.

Along with this, it helps to make allocate financial resources in an adequate and proper direction

among organisational functions (Smith and Driscoll, 2017).

However, a big demerit of cash budget is reliance on the assumptions and estimations

made for preparing it within workplace of the Imda Tech. When this budget incorporated in the

firm then imposes expense burden.

Sales budget:

A forecasted statement which refers to the revenue needs to generate the company at the

end of next fiscal period is considered as the sale budget in management accounting. On the

basis of this, Imda Tech able to determine that how much amount requires earning for achieving

objectives. Further, sale budget has some advantages and demerits which are such as follows:

It is an important budget which drives other stated budgets within Imda Tech like labour,

cash, manufacturing, production etc. It helps to make raw materials purchasing decisions by

which stock can be managed properly (Duff, 2016). Along with this, plan for earning estimated

revenue can be framed in fruitful direction.

On the other side, if the market situations not analysed appropriately then issue of stock

increasing will be occurred in the cited company. Further, in case demand of the products

fluctuate then goal of revenue generated cannot meet by the firm (Mack, 2016).

B) Procedure in order to prepare budgets

In the workplace of Imda Tech when budgets are preparing then particular procedure is to

be followed. Further, stages involved in the budget preparation process are such as follows:

At the very first and foremost stage of budget preparation, data which needed in order to

frame the budgets obtained and estimated. For completing this particular step past

financial data or statements taken as a base by the management. Further, each department

is considered while obtaining data and estimating in the company (Agarwal, 2016).

At the second stage, all the above stated estimations are coordinated with the budget

committee of Imda Tech company. Further, all the estimating are reviewed and evaluated

6

financials after considering to the plan prepared. For enhancing effective communication within

workplace and establishing better coordination among employees it is one of the importance tool.

Along with this, it helps to make allocate financial resources in an adequate and proper direction

among organisational functions (Smith and Driscoll, 2017).

However, a big demerit of cash budget is reliance on the assumptions and estimations

made for preparing it within workplace of the Imda Tech. When this budget incorporated in the

firm then imposes expense burden.

Sales budget:

A forecasted statement which refers to the revenue needs to generate the company at the

end of next fiscal period is considered as the sale budget in management accounting. On the

basis of this, Imda Tech able to determine that how much amount requires earning for achieving

objectives. Further, sale budget has some advantages and demerits which are such as follows:

It is an important budget which drives other stated budgets within Imda Tech like labour,

cash, manufacturing, production etc. It helps to make raw materials purchasing decisions by

which stock can be managed properly (Duff, 2016). Along with this, plan for earning estimated

revenue can be framed in fruitful direction.

On the other side, if the market situations not analysed appropriately then issue of stock

increasing will be occurred in the cited company. Further, in case demand of the products

fluctuate then goal of revenue generated cannot meet by the firm (Mack, 2016).

B) Procedure in order to prepare budgets

In the workplace of Imda Tech when budgets are preparing then particular procedure is to

be followed. Further, stages involved in the budget preparation process are such as follows:

At the very first and foremost stage of budget preparation, data which needed in order to

frame the budgets obtained and estimated. For completing this particular step past

financial data or statements taken as a base by the management. Further, each department

is considered while obtaining data and estimating in the company (Agarwal, 2016).

At the second stage, all the above stated estimations are coordinated with the budget

committee of Imda Tech company. Further, all the estimating are reviewed and evaluated

6

by the authorised party. It is one of the significant stage because after completion of the

evolution by committee next step is used.

Once the estimations are coordinated then communicated with the managers of

department of the firm. Under this, managers of the respective organisational function

assess that whether the resources are adequate for them or not. Moreover, when they all

agreed on the estimations then move towards next step.

At the fourth stage, the above communicated and approved budget plan is implemented

within working environment of the Imda Tech company. After implementation, within

specific period of time reviewed by the relevant authorised party and budget committee.

At the end of budget preparation process, progress report is reviewed and assessed that

whether all the budgeted objectives are completed as well as achieved in an appropriate

direction or not (Otley, 2016). On the basis of this analysis, corrective actions taken by

the management in the Imda Tech enterprise.

C) Different pricing tactics

Price is one of an important aspect within each and every business enterprise. In order to

determine charges of electronic gadgets and phone chargers the Imda Tech firm uses come

strategies which are explained below: Cost plus pricing strategy: The method in which initially total cost of production in the

company is calculated and then determined by the management. Once overall expenses

and costs are assessed then profit margin added on that value. As per this method

percentage of desired profit are included in cost and whatever outcome comes is

considered as the price of phone charger in Imda Tech. Competition based: Another strategy of pricing in which level of prices of the

competitors are analysed firstly and then go for determine product charges. When rivalry

firm of the selected company charges high price of products then management of Imda

Tech derive low prices of the mobile phone chargers. Due to this strategy, customers of

the competitor company will switch towards Imda Tech (Quattrone, 2016). Market perpetration: According to this tool, at the time of existing in the market low

prices are charged from the customers. As the company operates in industry and grow

7

evolution by committee next step is used.

Once the estimations are coordinated then communicated with the managers of

department of the firm. Under this, managers of the respective organisational function

assess that whether the resources are adequate for them or not. Moreover, when they all

agreed on the estimations then move towards next step.

At the fourth stage, the above communicated and approved budget plan is implemented

within working environment of the Imda Tech company. After implementation, within

specific period of time reviewed by the relevant authorised party and budget committee.

At the end of budget preparation process, progress report is reviewed and assessed that

whether all the budgeted objectives are completed as well as achieved in an appropriate

direction or not (Otley, 2016). On the basis of this analysis, corrective actions taken by

the management in the Imda Tech enterprise.

C) Different pricing tactics

Price is one of an important aspect within each and every business enterprise. In order to

determine charges of electronic gadgets and phone chargers the Imda Tech firm uses come

strategies which are explained below: Cost plus pricing strategy: The method in which initially total cost of production in the

company is calculated and then determined by the management. Once overall expenses

and costs are assessed then profit margin added on that value. As per this method

percentage of desired profit are included in cost and whatever outcome comes is

considered as the price of phone charger in Imda Tech. Competition based: Another strategy of pricing in which level of prices of the

competitors are analysed firstly and then go for determine product charges. When rivalry

firm of the selected company charges high price of products then management of Imda

Tech derive low prices of the mobile phone chargers. Due to this strategy, customers of

the competitor company will switch towards Imda Tech (Quattrone, 2016). Market perpetration: According to this tool, at the time of existing in the market low

prices are charged from the customers. As the company operates in industry and grow

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

then enhance prices of the products and services. Basic objective behind considering this

particular pricing strategy is to increase market share in the industry and financial

performance as well.

Market led pricing method: Under this kind of tactic, the Imda Tech management

researches overall market situation of the electronic and assess demand of the gadgets.

For instance: if the demand of relevant products is high then firm will determine high

prices which lead to increase sales and revenue (Chenhall and Moers, 2015).

TASK 4

A. I. Ways through which BSC used for identifying and responding financial issues

A metric which is used by the companies in order to assess business performance and

improvement is considered as the balanced scorecard (BSC). It is one of the highly concerned

approach for identifying and ascertaining performance of the Imda Tech entity in the industry of

electronics. It has majorly four perspectives which include financial, internal business process,

customers as well as learning and growth. In order to assess those problems of Imda Tech which

are related to the financial aspect then financial perspective of BSC is considered by the

management. Under this, it has been identified that the company is in which extent and manner

utilising the financial resources. When the employees use monetary in an optimum direction then

easily able to raise revenue and productivity.

In the financial perspective of balanced scorecard, different key performance indicators

are applied within workplace. Furthermore, those KPIs considered with respect to BSC are like

cost increasing or decreasing, profitability fluctuations, changes in liquid or cash position etc

(Suomala, Lyly-Yrjänäinen and Lukka, 2014). Along with this, quality or products and services

are also measured against to the expenses made for producing it. For example: when the cost KPI

is used in the working environment then it has been assessed that up to which level expenditures

are associated. In addition to this, total cost of the production and output both compared with the

last year. Therefore, it can be properly diagnosed that at which point along with causes expenses

enhanced and then strategies for eliminating it prepared. Hence, the BSC is one of the effective

approach in order to identify and reducing all the financial issues arisen in Imda Tech.

8

particular pricing strategy is to increase market share in the industry and financial

performance as well.

Market led pricing method: Under this kind of tactic, the Imda Tech management

researches overall market situation of the electronic and assess demand of the gadgets.

For instance: if the demand of relevant products is high then firm will determine high

prices which lead to increase sales and revenue (Chenhall and Moers, 2015).

TASK 4

A. I. Ways through which BSC used for identifying and responding financial issues

A metric which is used by the companies in order to assess business performance and

improvement is considered as the balanced scorecard (BSC). It is one of the highly concerned

approach for identifying and ascertaining performance of the Imda Tech entity in the industry of

electronics. It has majorly four perspectives which include financial, internal business process,

customers as well as learning and growth. In order to assess those problems of Imda Tech which

are related to the financial aspect then financial perspective of BSC is considered by the

management. Under this, it has been identified that the company is in which extent and manner

utilising the financial resources. When the employees use monetary in an optimum direction then

easily able to raise revenue and productivity.

In the financial perspective of balanced scorecard, different key performance indicators

are applied within workplace. Furthermore, those KPIs considered with respect to BSC are like

cost increasing or decreasing, profitability fluctuations, changes in liquid or cash position etc

(Suomala, Lyly-Yrjänäinen and Lukka, 2014). Along with this, quality or products and services

are also measured against to the expenses made for producing it. For example: when the cost KPI

is used in the working environment then it has been assessed that up to which level expenditures

are associated. In addition to this, total cost of the production and output both compared with the

last year. Therefore, it can be properly diagnosed that at which point along with causes expenses

enhanced and then strategies for eliminating it prepared. Hence, the BSC is one of the effective

approach in order to identify and reducing all the financial issues arisen in Imda Tech.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A. II. Use of BSC in order to enhance financial governance and frame effectual strategies

According to the case scenario, at the time of publishing financial statements of Imda

Tech loss of £1.5 million is identified by the management. For resolving this major problem

some tools and techniques are prepared by the financial governance of the selected firm. The

metric of assessing business performance i.e. balanced scorecard used and implemented by the

financial governance. Therefore, it can easily and appropriately ascertain shortfalls incurred in

the company. As time goes, it makes effective and fruitful strategies for responding such kind of

the issues occurred in the chosen electronic manufacturer (Ab Rahman, Hassan and Said, 2015).

Henceforth, it can be stated that by considering financial perspective of BSC adequate tactics

prepared by the financial governance which lead to improve it within workplace.

CONCLUSION

It can be concluded from the above study that, management accounting is one of the

significant system in order to take profitable and fruitful internal business decisions. Further, the

MA is considered in the working environment as a tool of decision making because it helps to

forecast upcoming financial information. Moreover, there are some systems used by Imda Tech

for enhancing performance which are like cost accounting, stock management, price optimisation

and job costing. It can be ascertained from the income statements that, through marginal and

absorption costing Imda Tech generates net income and loss which is worth of £4625 and -£5375

respectively. Apart from this, cost plus, market based, competition led, market penetration etc.

Pricing strategies are considered by the firm for determining price of the products and services.

Furthermore, financial perspective of BSC is taken into account to assess and eliminate financial

shortfalls within entity.

9

According to the case scenario, at the time of publishing financial statements of Imda

Tech loss of £1.5 million is identified by the management. For resolving this major problem

some tools and techniques are prepared by the financial governance of the selected firm. The

metric of assessing business performance i.e. balanced scorecard used and implemented by the

financial governance. Therefore, it can easily and appropriately ascertain shortfalls incurred in

the company. As time goes, it makes effective and fruitful strategies for responding such kind of

the issues occurred in the chosen electronic manufacturer (Ab Rahman, Hassan and Said, 2015).

Henceforth, it can be stated that by considering financial perspective of BSC adequate tactics

prepared by the financial governance which lead to improve it within workplace.

CONCLUSION

It can be concluded from the above study that, management accounting is one of the

significant system in order to take profitable and fruitful internal business decisions. Further, the

MA is considered in the working environment as a tool of decision making because it helps to

forecast upcoming financial information. Moreover, there are some systems used by Imda Tech

for enhancing performance which are like cost accounting, stock management, price optimisation

and job costing. It can be ascertained from the income statements that, through marginal and

absorption costing Imda Tech generates net income and loss which is worth of £4625 and -£5375

respectively. Apart from this, cost plus, market based, competition led, market penetration etc.

Pricing strategies are considered by the firm for determining price of the products and services.

Furthermore, financial perspective of BSC is taken into account to assess and eliminate financial

shortfalls within entity.

9

REFERENCES

Books and Journals

Ab Rahman, N. A., Hassan, S. and Said, J., 2015. Promoting sustainability of microfinance via

innovation risks, best practices and management accounting practices. Procedia

Economics and Finance. 31. pp. 470-484.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp.1-13.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp. 63-80.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp. 42-58.

Lapsley, I. and Rekers, J. V., 2017. The relevance of strategic management accounting to popular

culture: The world of West End Musicals. Management Accounting Research. 35. pp.47-

55.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp. 45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research. 31. pp. 118-122.

Smith, D. and Driscoll, T., 2017. Key skill sets for management accounting. Strategic Finance.

98(12). pp. 62-64.

Soderstrom, K. M., Soderstrom, N. S. and Stewart, C. R., 2017. Sustainability/CSR research in

management accounting: A review of the literature. In Advances in Management

10

Books and Journals

Ab Rahman, N. A., Hassan, S. and Said, J., 2015. Promoting sustainability of microfinance via

innovation risks, best practices and management accounting practices. Procedia

Economics and Finance. 31. pp. 470-484.

Ax, C. and Greve, J., 2017. Adoption of management accounting innovations: Organizational

culture compatibility and perceived outcomes. Management Accounting Research. 34.

pp.59-74.

Chenhall, R. H. and Moers, F., 2015. The role of innovation in the evolution of management

accounting and its integration into management control. Accounting, Organizations and

Society. 47. pp.1-13.

Granlund, M. and Lukka, K., 2017. Investigating highly established research paradigms:

Reviving contextuality in contingency theory based management accounting research.

Critical Perspectives on Accounting. 45. pp. 63-80.

Lachmann, M., Trapp, I. and Trapp, R., 2017. Diversity and validity in positivist management

accounting research—A longitudinal perspective over four decades. Management

Accounting Research. 34. pp. 42-58.

Lapsley, I. and Rekers, J. V., 2017. The relevance of strategic management accounting to popular

culture: The world of West End Musicals. Management Accounting Research. 35. pp.47-

55.

Otley, D., 2016. The contingency theory of management accounting and control: 1980–2014.

Management accounting research. 31. pp. 45-62.

Quattrone, P., 2016. Management accounting goes digital: Will the move make it wiser?.

Management Accounting Research. 31. pp. 118-122.

Smith, D. and Driscoll, T., 2017. Key skill sets for management accounting. Strategic Finance.

98(12). pp. 62-64.

Soderstrom, K. M., Soderstrom, N. S. and Stewart, C. R., 2017. Sustainability/CSR research in

management accounting: A review of the literature. In Advances in Management

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.