Management Accounting Report for Johnson Jewellers Ltd

VerifiedAdded on 2020/12/24

|15

|5060

|186

Report

AI Summary

This report delves into management accounting, specifically examining its application within Johnson Jewellers Ltd. It explores various management accounting systems, including cost accounting, price optimization, inventory management, and job costing, highlighting their benefits in financial forecasting, profitability enhancement, and customer relationship management. The report details different types of accounting reporting systems like performance reports, account receivable reports, and inventory management reports, emphasizing their role in providing stakeholders with insights into a company's financial position. Furthermore, it analyzes the merits and demerits of using accounting systems, different costing methods for determining net profitability, and the advantages and disadvantages of planning tools used in budgeting. The assignment also addresses financial issues and proposes measures for their resolution, culminating in an analysis of management accounting techniques that can lead to sustainable success. The report uses the case of Johnson Jewellers Ltd. to illustrate practical applications of these concepts.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various management accounting systems and its benefits to an organisation.................1

P2: Various types of accounting reporting system.................................................................3

M1: Merits and demerits of using accounting systems .........................................................5

D1: Critical analysis of reporting system...............................................................................6

TASK 2............................................................................................................................................6

P3: Different types of costing method in determining net profitability of company.............6

M2. Application of management accounting techniques:......................................................8

D2 Costing techniques helpful in providing financial reports that accurately apply and inter

prate data for a range of business activities............................................................................9

TASK 3............................................................................................................................................9

P4: Advantage and disadvantage of using planning tools use in budget................................9

M3 Use of different planning tools and their application.....................................................10

TASK 4..........................................................................................................................................10

P5: Various financial issues and measure to resolve it.........................................................10

M4 Analyses of management accounting which can lead towards sustainable success......11

D3 Use of planning tools to solve financial problems.........................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Various management accounting systems and its benefits to an organisation.................1

P2: Various types of accounting reporting system.................................................................3

M1: Merits and demerits of using accounting systems .........................................................5

D1: Critical analysis of reporting system...............................................................................6

TASK 2............................................................................................................................................6

P3: Different types of costing method in determining net profitability of company.............6

M2. Application of management accounting techniques:......................................................8

D2 Costing techniques helpful in providing financial reports that accurately apply and inter

prate data for a range of business activities............................................................................9

TASK 3............................................................................................................................................9

P4: Advantage and disadvantage of using planning tools use in budget................................9

M3 Use of different planning tools and their application.....................................................10

TASK 4..........................................................................................................................................10

P5: Various financial issues and measure to resolve it.........................................................10

M4 Analyses of management accounting which can lead towards sustainable success......11

D3 Use of planning tools to solve financial problems.........................................................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is an activity of preparing managerial reports in order to

facilitate management to make an effective decisions and plans for achievement of desired goals

and objectives. Managerial reports include Profit & Loss a/c, Balance sheet, Cash flow statement

etc. that shows true and fair financial position of company which directs management to make

changes in their existing policies so as to attain a good financial position of company in

competitive market. For this, the manager is required to take responsibility of collecting data

from various managerial reports and take an effective decision for the purpose of increasing

profitability of an organisation (Amidu, Effah and Abor, 2011).

The present assignment is based on Johnson Jewellers Ltd. which is engaged in

manufacturing and selling different deigns of jewellery items to the people of UK. The project

explains various management accounting systems along with their benefit to an organisation. In

addition, with this, management accounting reporting systems, methods of calculation of net

profitability are briefly described under the report. The project also summarises different

planning tools to control budget and other tools to resolve financial issues of an organisation.

TASK 1

P1: Various management accounting systems and its benefits to an organisation

Management accounting: It is a profession that requires specific skills and knowledge

which assist management in collecting relevant information from the managerial reports in order

to make an effective decisions and suitable plans for the betterment of an organisation. Such

managerial reports include Profit & Loss a/c, Balance sheet, Cash flow statement etc. which is

prepared on annual basis.

Benefits of management accounting systems:

Forecasting cash flows: With the help of using various accounting systems, the

accounting managers are able to prepare various kind of reports which makes easy for them to

acquire knowledge about inflow and outflow of cash during an accounting period. This will

assist management to execute business operations without fearing any shortage of funds

(Carlsson-Wall, Kraus and Lind, 2015).

1

Management accounting is an activity of preparing managerial reports in order to

facilitate management to make an effective decisions and plans for achievement of desired goals

and objectives. Managerial reports include Profit & Loss a/c, Balance sheet, Cash flow statement

etc. that shows true and fair financial position of company which directs management to make

changes in their existing policies so as to attain a good financial position of company in

competitive market. For this, the manager is required to take responsibility of collecting data

from various managerial reports and take an effective decision for the purpose of increasing

profitability of an organisation (Amidu, Effah and Abor, 2011).

The present assignment is based on Johnson Jewellers Ltd. which is engaged in

manufacturing and selling different deigns of jewellery items to the people of UK. The project

explains various management accounting systems along with their benefit to an organisation. In

addition, with this, management accounting reporting systems, methods of calculation of net

profitability are briefly described under the report. The project also summarises different

planning tools to control budget and other tools to resolve financial issues of an organisation.

TASK 1

P1: Various management accounting systems and its benefits to an organisation

Management accounting: It is a profession that requires specific skills and knowledge

which assist management in collecting relevant information from the managerial reports in order

to make an effective decisions and suitable plans for the betterment of an organisation. Such

managerial reports include Profit & Loss a/c, Balance sheet, Cash flow statement etc. which is

prepared on annual basis.

Benefits of management accounting systems:

Forecasting cash flows: With the help of using various accounting systems, the

accounting managers are able to prepare various kind of reports which makes easy for them to

acquire knowledge about inflow and outflow of cash during an accounting period. This will

assist management to execute business operations without fearing any shortage of funds

(Carlsson-Wall, Kraus and Lind, 2015).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increase profitability: Using cost accounting system help in preparation of budget for

execution of each business activities and allocate cost accordingly. This will minimise the cost of

operations which directly makes positive impact on the profitability of company as well.

Increase customer’s strength: Using price optimisation system help in identifying the

actual perception of buyers towards the pricing strategies made by company on their products

and services. This will enable management to make changes in existing pricing policies in order

to influence buying behaviour of customers in favour of their offerings. Therefore, using such

system provides an opportunity to company to achieve loyalty of targeted people and attain huge

customer strength.

Every organisation irrespective of the size whether small, medium or large always try to

enhance their business operations which can be possible through maintaining managerial reports

on specific time period. The management is held responsible to prepare managerial reports which

contains the information related with accounting transactions which were made during the

accounting period. It assists them to make an effective decisions and plans for the growth and

success of an organisation. Therefore, the management of Johnson Jewellers Ltd. is required to

prepare various kinds of managerial reports with the help of different management accounting

systems such as cost accounting systems, price optimisation system etc (Granlund, 2011). which

provides relevant information about the current position of company in competitive market. Here

are the brief explanation of various management accounting systems along with their benefits:

Cost accounting system: It refers to such accounting system which help in providing

information about the total cost invested in the execution of different business activities. It

assists management to prepare budget and accordingly allocate cost to different department

which minimises the chances of wastage of money. The main aim of using such system is to

reduce cost of operations so as to make positive impact on the profitability of an

organisation. Therefore, it is very important for Johnson Jewellers Ltd. to adopt such system

in order to identify the total cost incurred in business activities so that it can be recover from

the customers along with their certain percentage of margin. For example, manufacturing and

designing jewellery items requires huge amount to incur which enable management to

identify the total coast and on the basis of which set pricing strategies including their margin

for their targeted customers.

2

execution of each business activities and allocate cost accordingly. This will minimise the cost of

operations which directly makes positive impact on the profitability of company as well.

Increase customer’s strength: Using price optimisation system help in identifying the

actual perception of buyers towards the pricing strategies made by company on their products

and services. This will enable management to make changes in existing pricing policies in order

to influence buying behaviour of customers in favour of their offerings. Therefore, using such

system provides an opportunity to company to achieve loyalty of targeted people and attain huge

customer strength.

Every organisation irrespective of the size whether small, medium or large always try to

enhance their business operations which can be possible through maintaining managerial reports

on specific time period. The management is held responsible to prepare managerial reports which

contains the information related with accounting transactions which were made during the

accounting period. It assists them to make an effective decisions and plans for the growth and

success of an organisation. Therefore, the management of Johnson Jewellers Ltd. is required to

prepare various kinds of managerial reports with the help of different management accounting

systems such as cost accounting systems, price optimisation system etc (Granlund, 2011). which

provides relevant information about the current position of company in competitive market. Here

are the brief explanation of various management accounting systems along with their benefits:

Cost accounting system: It refers to such accounting system which help in providing

information about the total cost invested in the execution of different business activities. It

assists management to prepare budget and accordingly allocate cost to different department

which minimises the chances of wastage of money. The main aim of using such system is to

reduce cost of operations so as to make positive impact on the profitability of an

organisation. Therefore, it is very important for Johnson Jewellers Ltd. to adopt such system

in order to identify the total cost incurred in business activities so that it can be recover from

the customers along with their certain percentage of margin. For example, manufacturing and

designing jewellery items requires huge amount to incur which enable management to

identify the total coast and on the basis of which set pricing strategies including their margin

for their targeted customers.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price optimisation system: It is such accounting system which help management in

identify the perception of targeted people towards the pricing strategies made by the

company on their products and services. It assists management to analyse the satisfaction

level of customers after buying their products and services on certain price. This will make

easy for management to set an effective pricing policies for their products and services which

can maximises the satisfaction level of customers and can easily attract them towards

purchasing their products and services. Therefore, Johnson Jewellers Ltd. is required to adopt

such accounting system as it help in achieving huge customer strength through charging an

appropriate amount from them on their product and services (Johnson, 2013).

Inventory management system: It is such accounting system which facilitate

management to maintain the sufficient amount of inventory with company so as to meet the

customer requirements on time. It assists management to decide whether to place an order for

further inventory to meet future requirements or not. Therefore, it helps in allocating

resources to different departments after identifying the shortage. Johnson Jewellers Ltd. is

engaged in manufacturing jeweller items which are always more in demand therefore it is

necessary for management to maintain the adequate level of inventory with company to meet

customers’ requirements which can be possible through implementing such accounting

system.

Job costing system: It is mostly used by every organisation which facilitate management

to identify the cost incurred in producing individual product or bunch of products at

particular period of time. This will help in identification of cost invested in particular

products which can be helpful in determining the net profit earned after selling such products

into market. It assist management to decide that which product will bring profitable outcome

to company after analysing their cost and profitability. Therefore, Johnson Jewellers Ltd.

must required to adopt such accounting system due to dealing with selling different design of

jewellery items.

P2: Various types of accounting reporting system

Management accounting reporting systems contains the relevant information about the

present situation of company in competitive market which provides an opportunity to

management to maintain through implementing corrective actions and suitable plans. Such

accounting reports includes performance report, inventory management report, account

3

identify the perception of targeted people towards the pricing strategies made by the

company on their products and services. It assists management to analyse the satisfaction

level of customers after buying their products and services on certain price. This will make

easy for management to set an effective pricing policies for their products and services which

can maximises the satisfaction level of customers and can easily attract them towards

purchasing their products and services. Therefore, Johnson Jewellers Ltd. is required to adopt

such accounting system as it help in achieving huge customer strength through charging an

appropriate amount from them on their product and services (Johnson, 2013).

Inventory management system: It is such accounting system which facilitate

management to maintain the sufficient amount of inventory with company so as to meet the

customer requirements on time. It assists management to decide whether to place an order for

further inventory to meet future requirements or not. Therefore, it helps in allocating

resources to different departments after identifying the shortage. Johnson Jewellers Ltd. is

engaged in manufacturing jeweller items which are always more in demand therefore it is

necessary for management to maintain the adequate level of inventory with company to meet

customers’ requirements which can be possible through implementing such accounting

system.

Job costing system: It is mostly used by every organisation which facilitate management

to identify the cost incurred in producing individual product or bunch of products at

particular period of time. This will help in identification of cost invested in particular

products which can be helpful in determining the net profit earned after selling such products

into market. It assist management to decide that which product will bring profitable outcome

to company after analysing their cost and profitability. Therefore, Johnson Jewellers Ltd.

must required to adopt such accounting system due to dealing with selling different design of

jewellery items.

P2: Various types of accounting reporting system

Management accounting reporting systems contains the relevant information about the

present situation of company in competitive market which provides an opportunity to

management to maintain through implementing corrective actions and suitable plans. Such

accounting reports includes performance report, inventory management report, account

3

receivable report etc. The growth and success of an organisation is very much depending on their

stakeholders who have rights to know actual financial position of company in market at present

times. Therefore, it is essential for management of Johnson Jewellers Ltd. to prepare such kinds

of reports on annual basis so to acquire knowledge about current position of company and

accordingly make further actions to improve in order to compete with their rivals in competitive

market (JOSHI and et. al., 2011). It can be further understood through describing the various

types of management accounting reports in detailed manner:

Performance report: This is the report which contains the information related with

performance of each and every department of an organisation. It assists management in identify

the deviations if any, which restricts departments to achieve their target within allotted time

period. The overall performance of an organisation is very much based on the performance of

various departments due to which it important for company to proper analyse the performance of

each department with the help of such reporting system. It will also help management to

distribute funds to departments on the basis of their performance and outcomes so that maximum

predictability can be achieved by company during an accounting period.

Account receivable report: It is such accounting report which contain the information

about the list of debtors with their unpaid amount to company for the products and services they

received from company in previous time. This will help management in making strict actions to

recover the unpaid amount from the debtors along with the pre-determined rate of interest.

Therefore, it more useful for Johnson Jewellers Ltd. to prepare such reports in order to prevent

the loss as bad debts. It further assist management make decision related with changing existing

credit policies so as to make easy for company to receive the amount from debtors on due date

(Klychova, Faskhutdinova and Sadrieva, 2014).

Inventory management report: It is such accounting report which provides sufficient

information about the current level of inventory the company have at present so that further order

can be taken from the customers. Johnson Jewellers Ltd. is engaged in manufacturing jewellery

items which are more in demand in every season therefore it is important for company to

maintain the adequate level of inventory at all time so as to meet customers’ demands on time. It

can be possible through preparing such report as it assists management on accounting knowledge

of present inventory which drives them to place an order from suppliers of any shortage found.

4

stakeholders who have rights to know actual financial position of company in market at present

times. Therefore, it is essential for management of Johnson Jewellers Ltd. to prepare such kinds

of reports on annual basis so to acquire knowledge about current position of company and

accordingly make further actions to improve in order to compete with their rivals in competitive

market (JOSHI and et. al., 2011). It can be further understood through describing the various

types of management accounting reports in detailed manner:

Performance report: This is the report which contains the information related with

performance of each and every department of an organisation. It assists management in identify

the deviations if any, which restricts departments to achieve their target within allotted time

period. The overall performance of an organisation is very much based on the performance of

various departments due to which it important for company to proper analyse the performance of

each department with the help of such reporting system. It will also help management to

distribute funds to departments on the basis of their performance and outcomes so that maximum

predictability can be achieved by company during an accounting period.

Account receivable report: It is such accounting report which contain the information

about the list of debtors with their unpaid amount to company for the products and services they

received from company in previous time. This will help management in making strict actions to

recover the unpaid amount from the debtors along with the pre-determined rate of interest.

Therefore, it more useful for Johnson Jewellers Ltd. to prepare such reports in order to prevent

the loss as bad debts. It further assist management make decision related with changing existing

credit policies so as to make easy for company to receive the amount from debtors on due date

(Klychova, Faskhutdinova and Sadrieva, 2014).

Inventory management report: It is such accounting report which provides sufficient

information about the current level of inventory the company have at present so that further order

can be taken from the customers. Johnson Jewellers Ltd. is engaged in manufacturing jewellery

items which are more in demand in every season therefore it is important for company to

maintain the adequate level of inventory at all time so as to meet customers’ demands on time. It

can be possible through preparing such report as it assists management on accounting knowledge

of present inventory which drives them to place an order from suppliers of any shortage found.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

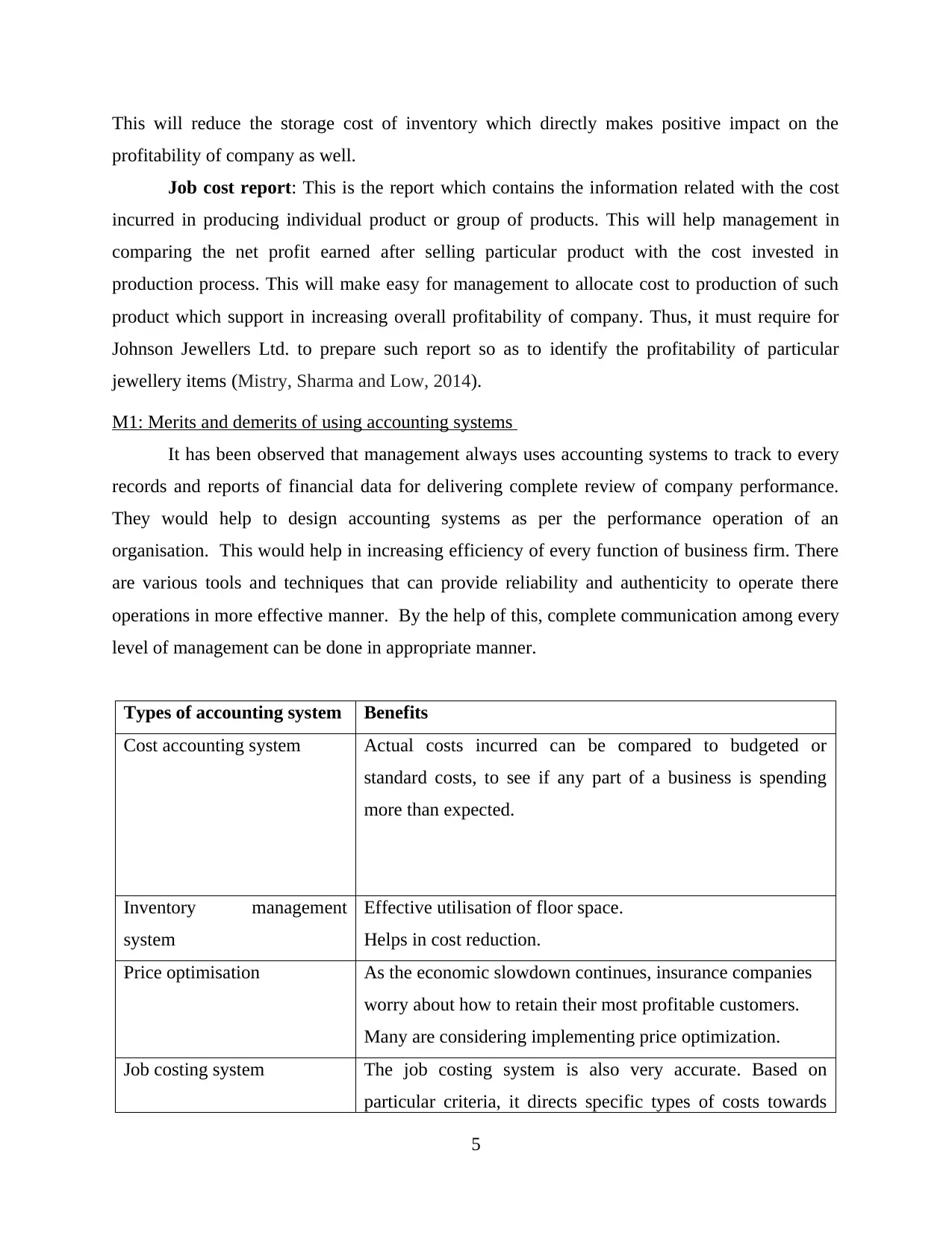

This will reduce the storage cost of inventory which directly makes positive impact on the

profitability of company as well.

Job cost report: This is the report which contains the information related with the cost

incurred in producing individual product or group of products. This will help management in

comparing the net profit earned after selling particular product with the cost invested in

production process. This will make easy for management to allocate cost to production of such

product which support in increasing overall profitability of company. Thus, it must require for

Johnson Jewellers Ltd. to prepare such report so as to identify the profitability of particular

jewellery items (Mistry, Sharma and Low, 2014).

M1: Merits and demerits of using accounting systems

It has been observed that management always uses accounting systems to track to every

records and reports of financial data for delivering complete review of company performance.

They would help to design accounting systems as per the performance operation of an

organisation. This would help in increasing efficiency of every function of business firm. There

are various tools and techniques that can provide reliability and authenticity to operate there

operations in more effective manner. By the help of this, complete communication among every

level of management can be done in appropriate manner.

Types of accounting system Benefits

Cost accounting system Actual costs incurred can be compared to budgeted or

standard costs, to see if any part of a business is spending

more than expected.

Inventory management

system

Effective utilisation of floor space.

Helps in cost reduction.

Price optimisation As the economic slowdown continues, insurance companies

worry about how to retain their most profitable customers.

Many are considering implementing price optimization.

Job costing system The job costing system is also very accurate. Based on

particular criteria, it directs specific types of costs towards

5

profitability of company as well.

Job cost report: This is the report which contains the information related with the cost

incurred in producing individual product or group of products. This will help management in

comparing the net profit earned after selling particular product with the cost invested in

production process. This will make easy for management to allocate cost to production of such

product which support in increasing overall profitability of company. Thus, it must require for

Johnson Jewellers Ltd. to prepare such report so as to identify the profitability of particular

jewellery items (Mistry, Sharma and Low, 2014).

M1: Merits and demerits of using accounting systems

It has been observed that management always uses accounting systems to track to every

records and reports of financial data for delivering complete review of company performance.

They would help to design accounting systems as per the performance operation of an

organisation. This would help in increasing efficiency of every function of business firm. There

are various tools and techniques that can provide reliability and authenticity to operate there

operations in more effective manner. By the help of this, complete communication among every

level of management can be done in appropriate manner.

Types of accounting system Benefits

Cost accounting system Actual costs incurred can be compared to budgeted or

standard costs, to see if any part of a business is spending

more than expected.

Inventory management

system

Effective utilisation of floor space.

Helps in cost reduction.

Price optimisation As the economic slowdown continues, insurance companies

worry about how to retain their most profitable customers.

Many are considering implementing price optimization.

Job costing system The job costing system is also very accurate. Based on

particular criteria, it directs specific types of costs towards

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

appropriate accounts.

D1: Critical analysis of reporting system

This would be vital for every operating business to generate better results with proper

allocation of resources. It is crucial for Nero Ltd to make use of reporting systems in effective

manner to record financial transactions of the company. This happens to be the primary role of

managers to ensure that every data would be properly inserted in to their respective statements.

This will be helpful in analyse performance and their position in more effective manner. Report

are work as useful tool for the managers in order to make plan for the upcoming projects and to

draw the attention of outside investors and stakeholder to make their investments (Moser, 2012).

TASK 2

P3: Different types of costing method in determining net profitability of company

Cost: It refers to the amount which is budgeted to execute different business functions

with the purpose of gaining maximum profitable outcomes. It includes direct cost, indirect cost

and overhead costs. It is valuation of efforts, time, resources etc. which are contributed in

manufacturing products and services.

Johnson Jewellers Ltd. is engaged in manufacturing wide range of jewellery items which

involves huge cost and efforts thus it is important for valuation of such sacrifice resources in

order to gain maximum output. It is important for company to make use of microeconomic

techniques in their business operations so as to achieve more effective results. The management

is held liable to minimises cost of operations in order to maximises the net profitability of

company. For this, it is essential to prepare budget on the basis of estimation and accordingly

allocate funds to each business activity after analysing their return received in near future.

Preparing budget will also reduces the chances of wastage of funds which enhances the

profitability of company as well. To determine the net profitability of company, there are two

costing methods which are mostly used by every organisations. Such methods includes marginal

and absorption costing which are explained as under:

Marginal costing: It refers to the costs which is charged when extra unit is produced

other than main output. It is also known as variable costing methods due to considering

only variable costs and ignoring fixed cost. Due to such, the profitability of company

6

D1: Critical analysis of reporting system

This would be vital for every operating business to generate better results with proper

allocation of resources. It is crucial for Nero Ltd to make use of reporting systems in effective

manner to record financial transactions of the company. This happens to be the primary role of

managers to ensure that every data would be properly inserted in to their respective statements.

This will be helpful in analyse performance and their position in more effective manner. Report

are work as useful tool for the managers in order to make plan for the upcoming projects and to

draw the attention of outside investors and stakeholder to make their investments (Moser, 2012).

TASK 2

P3: Different types of costing method in determining net profitability of company

Cost: It refers to the amount which is budgeted to execute different business functions

with the purpose of gaining maximum profitable outcomes. It includes direct cost, indirect cost

and overhead costs. It is valuation of efforts, time, resources etc. which are contributed in

manufacturing products and services.

Johnson Jewellers Ltd. is engaged in manufacturing wide range of jewellery items which

involves huge cost and efforts thus it is important for valuation of such sacrifice resources in

order to gain maximum output. It is important for company to make use of microeconomic

techniques in their business operations so as to achieve more effective results. The management

is held liable to minimises cost of operations in order to maximises the net profitability of

company. For this, it is essential to prepare budget on the basis of estimation and accordingly

allocate funds to each business activity after analysing their return received in near future.

Preparing budget will also reduces the chances of wastage of funds which enhances the

profitability of company as well. To determine the net profitability of company, there are two

costing methods which are mostly used by every organisations. Such methods includes marginal

and absorption costing which are explained as under:

Marginal costing: It refers to the costs which is charged when extra unit is produced

other than main output. It is also known as variable costing methods due to considering

only variable costs and ignoring fixed cost. Due to such, the profitability of company

6

increases and hence it is adopted by most of the organisation (Schaltegger and Csutora,

2012).

Absorption costing: It refers to such costing methods which determines the overall costs

incurred in manufacturing process. It considers both variable and fixed costs due to which

the net profitability of company decreases. As such costing method is more reliable and

accurate due to containing actual information about the cost incurred in particular

business activity which makes easy for management to determine the cost invested in

each and every business activity.

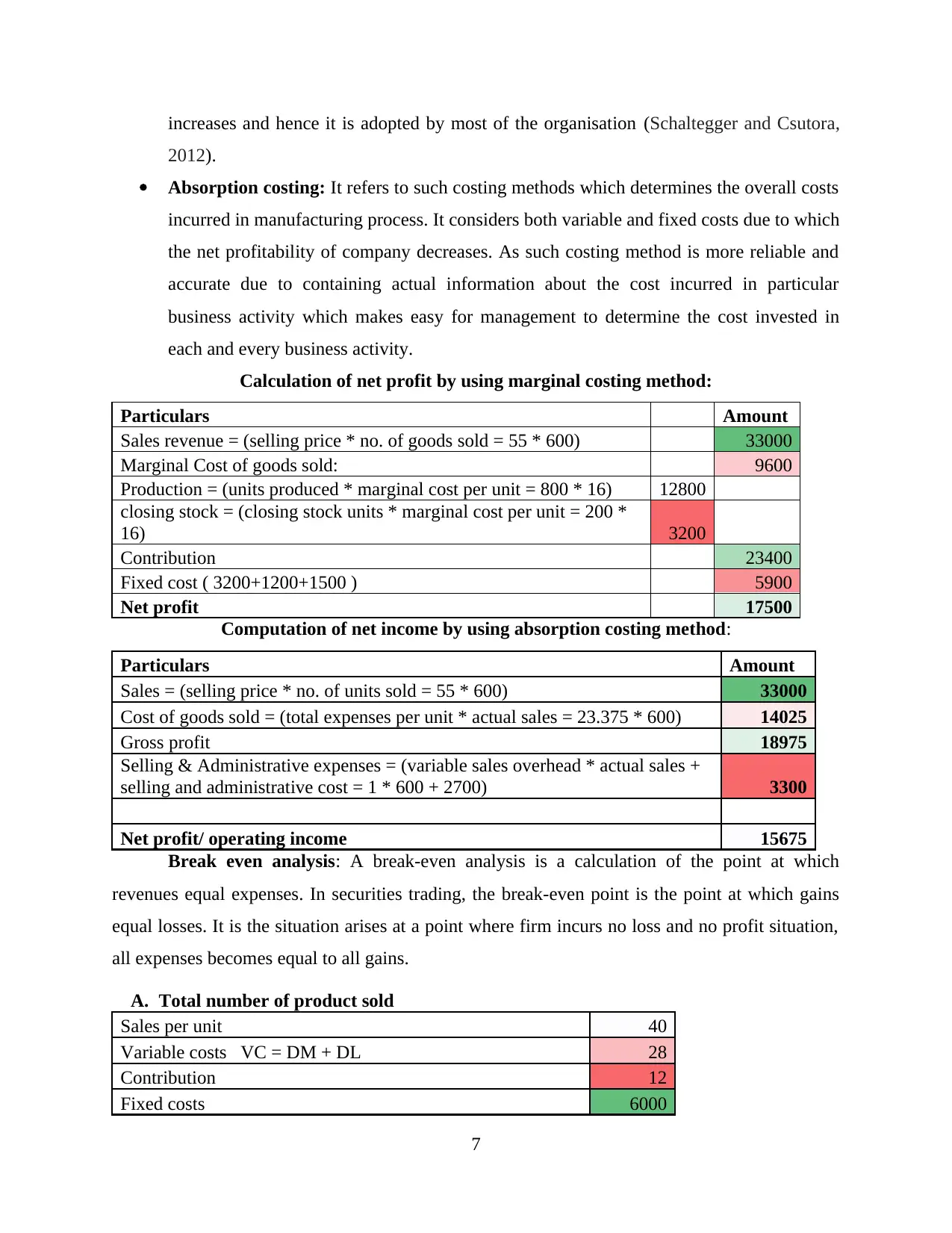

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: A break-even analysis is a calculation of the point at which

revenues equal expenses. In securities trading, the break-even point is the point at which gains

equal losses. It is the situation arises at a point where firm incurs no loss and no profit situation,

all expenses becomes equal to all gains.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

7

2012).

Absorption costing: It refers to such costing methods which determines the overall costs

incurred in manufacturing process. It considers both variable and fixed costs due to which

the net profitability of company decreases. As such costing method is more reliable and

accurate due to containing actual information about the cost incurred in particular

business activity which makes easy for management to determine the cost invested in

each and every business activity.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200+1200+1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: A break-even analysis is a calculation of the point at which

revenues equal expenses. In securities trading, the break-even point is the point at which gains

equal losses. It is the situation arises at a point where firm incurs no loss and no profit situation,

all expenses becomes equal to all gains.

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

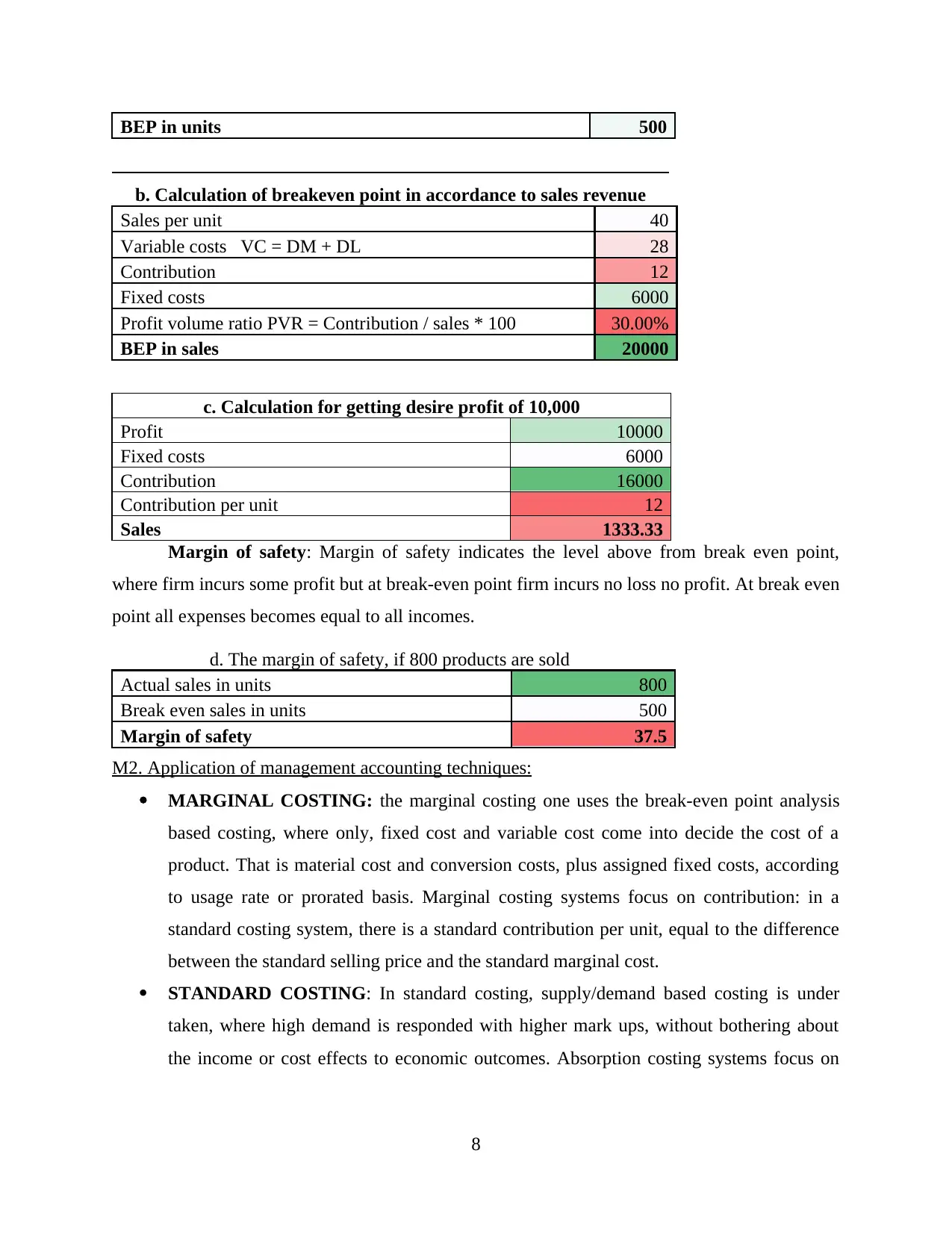

BEP in units 500

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: Margin of safety indicates the level above from break even point,

where firm incurs some profit but at break-even point firm incurs no loss no profit. At break even

point all expenses becomes equal to all incomes.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Application of management accounting techniques:

MARGINAL COSTING: the marginal costing one uses the break-even point analysis

based costing, where only, fixed cost and variable cost come into decide the cost of a

product. That is material cost and conversion costs, plus assigned fixed costs, according

to usage rate or prorated basis. Marginal costing systems focus on contribution: in a

standard costing system, there is a standard contribution per unit, equal to the difference

between the standard selling price and the standard marginal cost.

STANDARD COSTING: In standard costing, supply/demand based costing is under

taken, where high demand is responded with higher mark ups, without bothering about

the income or cost effects to economic outcomes. Absorption costing systems focus on

8

b. Calculation of breakeven point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

BEP in sales 20000

c. Calculation for getting desire profit of 10,000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: Margin of safety indicates the level above from break even point,

where firm incurs some profit but at break-even point firm incurs no loss no profit. At break even

point all expenses becomes equal to all incomes.

d. The margin of safety, if 800 products are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2. Application of management accounting techniques:

MARGINAL COSTING: the marginal costing one uses the break-even point analysis

based costing, where only, fixed cost and variable cost come into decide the cost of a

product. That is material cost and conversion costs, plus assigned fixed costs, according

to usage rate or prorated basis. Marginal costing systems focus on contribution: in a

standard costing system, there is a standard contribution per unit, equal to the difference

between the standard selling price and the standard marginal cost.

STANDARD COSTING: In standard costing, supply/demand based costing is under

taken, where high demand is responded with higher mark ups, without bothering about

the income or cost effects to economic outcomes. Absorption costing systems focus on

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit per unit, and the standard profit per unit of product is the difference between its

standard sales price and standard full cost.

Both the costing techniques are crucial and helpful in providing relevant financial

information regarding costing and also helpful in financial reporting.

D2 Costing techniques helpful in providing financial reports that accurately apply and inter prate

data for a range of business activities.

Under costing, to calculate net profit two techniques where used one is Marginal costing

and another is absorption costing, under marginal costing to calculate contribution all operating

expenses are include but, under absorption costing only those expenses are included which are

related to production only. That is why the profit calculated is different in both techniques. By

marginal costing profit is 17500( in above illustration) and by absorption costing the profit is

15675. Hence, marginal costing is better technique of calculating profit under costing. Because it

depicts the actual profit under costing, but absorption costing minimises the profit unnecessarily.

TASK 3

P4: Advantage and disadvantage of using planning tools use in budget

Planning is essential requirements of every organisation on the basis of which future

business activities are properly executed. The management of Johnson Jewellers Ltd. are held

responsible to prepare an effective budget for each business activity after analysing the profitable

outcomes received future period of time. Budget are prepared to manage and control cost which

is going to use in manufacturing quality products and services. There are various planning tools

which are more useful in controlling budgets which are mentioned under the below:

Forecasting tools: It is considered as more useful tool which is used to identify and

estimating the cost incurred in future project activities after analysing the cost incurred in past. It

is more reliable and accurate as all the data and information are available and collected from

internal and external departments (Ward, 2012).

Merits: It helps in determining the estimation of cost which are going to incurred in

future project activities that makes company ready with the sufficient resources.

Demerits: Estimations are sometimes not accurate due to which the chances of getting

profitable outcomes in ear future will be low.

9

standard sales price and standard full cost.

Both the costing techniques are crucial and helpful in providing relevant financial

information regarding costing and also helpful in financial reporting.

D2 Costing techniques helpful in providing financial reports that accurately apply and inter prate

data for a range of business activities.

Under costing, to calculate net profit two techniques where used one is Marginal costing

and another is absorption costing, under marginal costing to calculate contribution all operating

expenses are include but, under absorption costing only those expenses are included which are

related to production only. That is why the profit calculated is different in both techniques. By

marginal costing profit is 17500( in above illustration) and by absorption costing the profit is

15675. Hence, marginal costing is better technique of calculating profit under costing. Because it

depicts the actual profit under costing, but absorption costing minimises the profit unnecessarily.

TASK 3

P4: Advantage and disadvantage of using planning tools use in budget

Planning is essential requirements of every organisation on the basis of which future

business activities are properly executed. The management of Johnson Jewellers Ltd. are held

responsible to prepare an effective budget for each business activity after analysing the profitable

outcomes received future period of time. Budget are prepared to manage and control cost which

is going to use in manufacturing quality products and services. There are various planning tools

which are more useful in controlling budgets which are mentioned under the below:

Forecasting tools: It is considered as more useful tool which is used to identify and

estimating the cost incurred in future project activities after analysing the cost incurred in past. It

is more reliable and accurate as all the data and information are available and collected from

internal and external departments (Ward, 2012).

Merits: It helps in determining the estimation of cost which are going to incurred in

future project activities that makes company ready with the sufficient resources.

Demerits: Estimations are sometimes not accurate due to which the chances of getting

profitable outcomes in ear future will be low.

9

Contingency tools: Such tools is more useful to deal with contingent condition that may

occur in execution of future business activities. This will help management in determining the

risk which may influence the profitability of company. To deal with them in more effective

manner, suitable contingency tools are required to prepare for the purpose of analysing risk.

Merit: It may not influences even at the time of contingencies which empowered

employees to make an effective decisions in order to cope up with future challenges.

Demerit: It consumes more time and money which affects the profitability of company.

Scenario planning: It is also an effective tool which is used to adopt in order to deal with

flexible situation at may arise in the process of long term business activities. This, such tools are

adopted by every organisation in order to achieve better possible outcomes from future business

activities.

Merit: It brings beneficial result to company through analysing the uncertainties and

complexities which may affects profitably.

Demerit: It is much difficult for management to analyse future contingencies and

flexibilities due to which lots of issues and challenges ay arises in the process of future

business activities (Wickramasinghe, 2012).

M3 Use of different planning tools and their application

Planning tools such as forecasting, contingency and scenario are the techniques which

can be used by an organisation such as Johnson Jewellers Ltd to forecast their future events.

Future is uncertain so their contingencies. Tool like forecasting can be applied to predict future

sales by using trend analyses. Contingency tool should be applied by a company to ascertain

future harmful events and accordingly should prepare budget for future accounting period. Not

only these two, but scenario tool can also be applied to prepare budgets as this tool helps in

ascertaining range of future scenarios.

TASK 4

P5: Various financial issues and measure to resolve it

Every organisation tried to achieve strong financial position in market so as to compete

with the rivals in more effective and efficient manner. For this, it is important for management to

implement various financial tools which can help company resolving financial issues and

10

occur in execution of future business activities. This will help management in determining the

risk which may influence the profitability of company. To deal with them in more effective

manner, suitable contingency tools are required to prepare for the purpose of analysing risk.

Merit: It may not influences even at the time of contingencies which empowered

employees to make an effective decisions in order to cope up with future challenges.

Demerit: It consumes more time and money which affects the profitability of company.

Scenario planning: It is also an effective tool which is used to adopt in order to deal with

flexible situation at may arise in the process of long term business activities. This, such tools are

adopted by every organisation in order to achieve better possible outcomes from future business

activities.

Merit: It brings beneficial result to company through analysing the uncertainties and

complexities which may affects profitably.

Demerit: It is much difficult for management to analyse future contingencies and

flexibilities due to which lots of issues and challenges ay arises in the process of future

business activities (Wickramasinghe, 2012).

M3 Use of different planning tools and their application

Planning tools such as forecasting, contingency and scenario are the techniques which

can be used by an organisation such as Johnson Jewellers Ltd to forecast their future events.

Future is uncertain so their contingencies. Tool like forecasting can be applied to predict future

sales by using trend analyses. Contingency tool should be applied by a company to ascertain

future harmful events and accordingly should prepare budget for future accounting period. Not

only these two, but scenario tool can also be applied to prepare budgets as this tool helps in

ascertaining range of future scenarios.

TASK 4

P5: Various financial issues and measure to resolve it

Every organisation tried to achieve strong financial position in market so as to compete

with the rivals in more effective and efficient manner. For this, it is important for management to

implement various financial tools which can help company resolving financial issues and

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.