Management Accounting Report: Costing, Budgeting and Variance Analysis

VerifiedAdded on 2020/06/06

|20

|3237

|50

Report

AI Summary

This report presents a comprehensive analysis of management accounting principles, focusing on costing methods, budgeting techniques, and variance analysis within the context of ABC Ltd. The report begins by explaining various cost classifications (variable, fixed, and semi-variable) and different costing methods (batch, job, service, contract, and process costing). It then delves into inventory valuation using LIFO, FIFO, and AVCO methods, evaluating their impact on profitability. The report proceeds to calculate a routine cost report with variance analysis, identifies potential improvements using key performance indicators, and suggests cost reduction and quality enhancement strategies. Furthermore, the report explores the budgeting process, analyzes appropriate budgeting techniques, and calculates a cash budget for ABC Ltd. Finally, it measures variances, prepares an operating statement, and identifies responsibility centers of management, providing a holistic view of financial performance and management control within the organization.

MANAGEMENT ACCOUNTING COSTING

AND

BUDGETING

AND

BUDGETING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explaining various kinds of costs.....................................................................................1

1.2 Explaining different kinds of costing methods.................................................................2

1.3 Measuring costs for closing inventories by various methods...........................................2

1.4 Appropriate techniques for analysing the cost data..........................................................4

TASK 2............................................................................................................................................5

2.1 Calculating the routine cost report with variance analysis...............................................5

2.2 Potential improvements for ABC Ltd with the help of performance indicators..............6

2.3 Suggestion for reducing costs as well as improving quality and value............................6

TASK 3............................................................................................................................................6

3.1 Explaining budgeting process and its nature as well as objective....................................6

3.2 Appropriate budgeting technique for the organisation and its needs...............................7

3.3 Analysis of various budgets for ABC Ltd........................................................................7

3.4 Calculation cash budget for ABC Ltd..............................................................................9

TASK 4............................................................................................................................................9

4.1 Measuring variances.........................................................................................................9

4.2 Calculations for operating statement..............................................................................14

4.3 Report finding in context with identifying responsibility centres of management........15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explaining various kinds of costs.....................................................................................1

1.2 Explaining different kinds of costing methods.................................................................2

1.3 Measuring costs for closing inventories by various methods...........................................2

1.4 Appropriate techniques for analysing the cost data..........................................................4

TASK 2............................................................................................................................................5

2.1 Calculating the routine cost report with variance analysis...............................................5

2.2 Potential improvements for ABC Ltd with the help of performance indicators..............6

2.3 Suggestion for reducing costs as well as improving quality and value............................6

TASK 3............................................................................................................................................6

3.1 Explaining budgeting process and its nature as well as objective....................................6

3.2 Appropriate budgeting technique for the organisation and its needs...............................7

3.3 Analysis of various budgets for ABC Ltd........................................................................7

3.4 Calculation cash budget for ABC Ltd..............................................................................9

TASK 4............................................................................................................................................9

4.1 Measuring variances.........................................................................................................9

4.2 Calculations for operating statement..............................................................................14

4.3 Report finding in context with identifying responsibility centres of management........15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

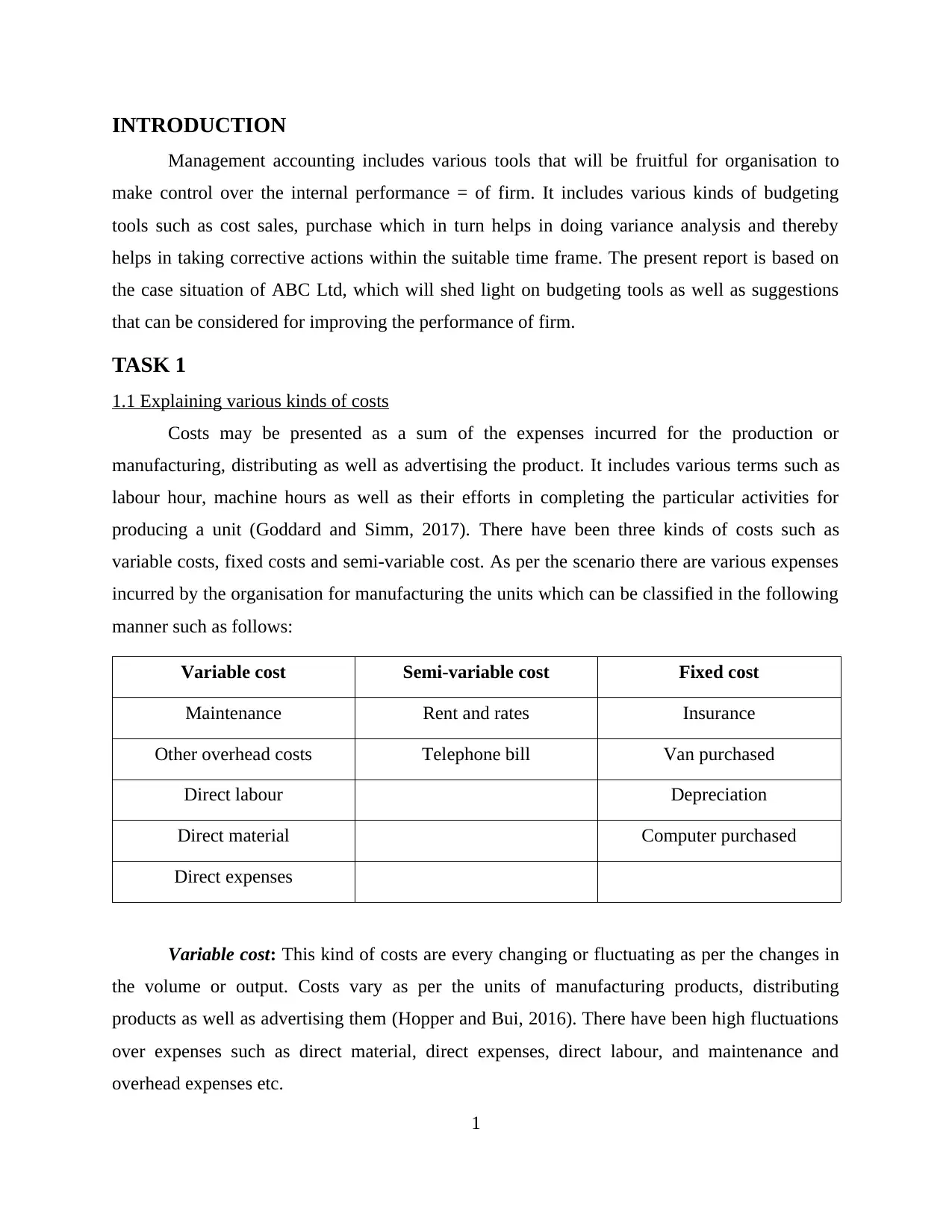

INTRODUCTION

Management accounting includes various tools that will be fruitful for organisation to

make control over the internal performance = of firm. It includes various kinds of budgeting

tools such as cost sales, purchase which in turn helps in doing variance analysis and thereby

helps in taking corrective actions within the suitable time frame. The present report is based on

the case situation of ABC Ltd, which will shed light on budgeting tools as well as suggestions

that can be considered for improving the performance of firm.

TASK 1

1.1 Explaining various kinds of costs

Costs may be presented as a sum of the expenses incurred for the production or

manufacturing, distributing as well as advertising the product. It includes various terms such as

labour hour, machine hours as well as their efforts in completing the particular activities for

producing a unit (Goddard and Simm, 2017). There have been three kinds of costs such as

variable costs, fixed costs and semi-variable cost. As per the scenario there are various expenses

incurred by the organisation for manufacturing the units which can be classified in the following

manner such as follows:

Variable cost Semi-variable cost Fixed cost

Maintenance Rent and rates Insurance

Other overhead costs Telephone bill Van purchased

Direct labour Depreciation

Direct material Computer purchased

Direct expenses

Variable cost: This kind of costs are every changing or fluctuating as per the changes in

the volume or output. Costs vary as per the units of manufacturing products, distributing

products as well as advertising them (Hopper and Bui, 2016). There have been high fluctuations

over expenses such as direct material, direct expenses, direct labour, and maintenance and

overhead expenses etc.

1

Management accounting includes various tools that will be fruitful for organisation to

make control over the internal performance = of firm. It includes various kinds of budgeting

tools such as cost sales, purchase which in turn helps in doing variance analysis and thereby

helps in taking corrective actions within the suitable time frame. The present report is based on

the case situation of ABC Ltd, which will shed light on budgeting tools as well as suggestions

that can be considered for improving the performance of firm.

TASK 1

1.1 Explaining various kinds of costs

Costs may be presented as a sum of the expenses incurred for the production or

manufacturing, distributing as well as advertising the product. It includes various terms such as

labour hour, machine hours as well as their efforts in completing the particular activities for

producing a unit (Goddard and Simm, 2017). There have been three kinds of costs such as

variable costs, fixed costs and semi-variable cost. As per the scenario there are various expenses

incurred by the organisation for manufacturing the units which can be classified in the following

manner such as follows:

Variable cost Semi-variable cost Fixed cost

Maintenance Rent and rates Insurance

Other overhead costs Telephone bill Van purchased

Direct labour Depreciation

Direct material Computer purchased

Direct expenses

Variable cost: This kind of costs are every changing or fluctuating as per the changes in

the volume or output. Costs vary as per the units of manufacturing products, distributing

products as well as advertising them (Hopper and Bui, 2016). There have been high fluctuations

over expenses such as direct material, direct expenses, direct labour, and maintenance and

overhead expenses etc.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Semi-variable cost: These cost has the variable of both the costs fixed and variable which

is facilitates professionals deciding the favourable costs for production (Aouni, McGillis and

Abdulkarim, 2017). The expenses like telephone and rent will remain fixed or will be fluctuate

as per changing conditions.

Fixed cost: It denoted as the costs of product which remains same or unchanged at each

level of output. It will be same in every aspect of business operations like office rent, salary of

workers etc.

1.2 Explaining different kinds of costing methods.

Categorization of cost is based on the different kinds of business operations which is going to be

held in the organisation (Bathurst and Schwartz, 2017). Each process and piece of work has its

own costs or expenses which are need to be done as to give the proper outcome. ABC ltd.

Company has incurred various expenses which are to be categorised in the various costing

techniques such as:

Batch costing Job costing Service costing Contract costing Process costing

Telephone Overhead

expenses

Maintenance Computer

purchased

Direct labour

Rent Depreciation Van purchased Direct Material

Insurance Direct expenses

There has been classification of various expenses into these five costing categories. Batch

costing includes rents and rates as well as telephone expenses. Services costing have

maintenance, depreciation as well as insurance expenses which are the services that have been

provided by organisation apart from main functional operations (Kabinlapat and Sutthachai,

2017). Contract costing includes purchase of Van as well as Computer. For production of units

there has been use of various direct costs such as labour machinery that helps in manufacturing

the particular units.

1.3 Measuring costs for closing inventories by various methods

LIFO technique: This method helps in dispatching units at first which has last input

transaction in organisation (Mo and et.al., 2017). It will be beneficial for selling units at higher

2

is facilitates professionals deciding the favourable costs for production (Aouni, McGillis and

Abdulkarim, 2017). The expenses like telephone and rent will remain fixed or will be fluctuate

as per changing conditions.

Fixed cost: It denoted as the costs of product which remains same or unchanged at each

level of output. It will be same in every aspect of business operations like office rent, salary of

workers etc.

1.2 Explaining different kinds of costing methods.

Categorization of cost is based on the different kinds of business operations which is going to be

held in the organisation (Bathurst and Schwartz, 2017). Each process and piece of work has its

own costs or expenses which are need to be done as to give the proper outcome. ABC ltd.

Company has incurred various expenses which are to be categorised in the various costing

techniques such as:

Batch costing Job costing Service costing Contract costing Process costing

Telephone Overhead

expenses

Maintenance Computer

purchased

Direct labour

Rent Depreciation Van purchased Direct Material

Insurance Direct expenses

There has been classification of various expenses into these five costing categories. Batch

costing includes rents and rates as well as telephone expenses. Services costing have

maintenance, depreciation as well as insurance expenses which are the services that have been

provided by organisation apart from main functional operations (Kabinlapat and Sutthachai,

2017). Contract costing includes purchase of Van as well as Computer. For production of units

there has been use of various direct costs such as labour machinery that helps in manufacturing

the particular units.

1.3 Measuring costs for closing inventories by various methods

LIFO technique: This method helps in dispatching units at first which has last input

transaction in organisation (Mo and et.al., 2017). It will be beneficial for selling units at higher

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

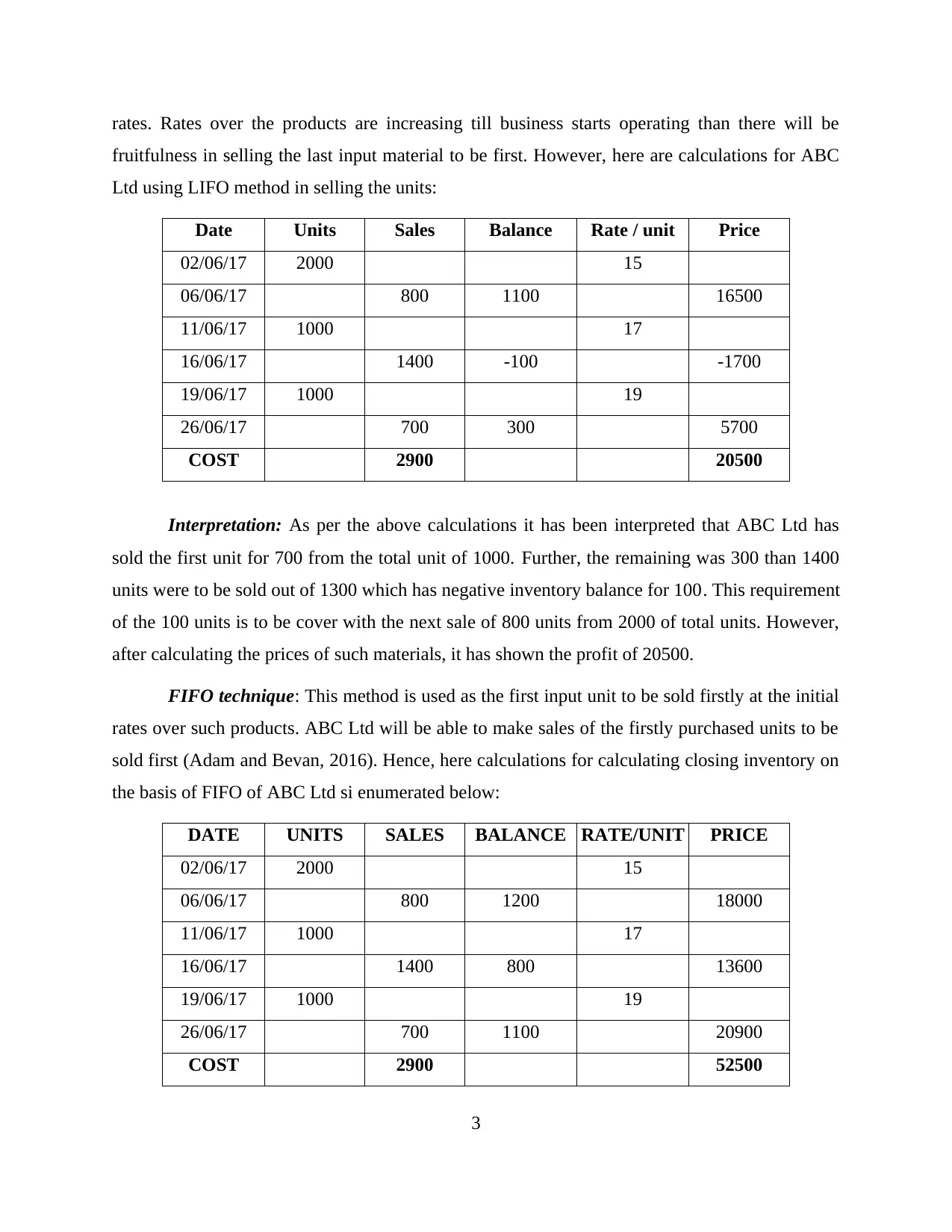

rates. Rates over the products are increasing till business starts operating than there will be

fruitfulness in selling the last input material to be first. However, here are calculations for ABC

Ltd using LIFO method in selling the units:

Date Units Sales Balance Rate / unit Price

02/06/17 2000 15

06/06/17 800 1100 16500

11/06/17 1000 17

16/06/17 1400 -100 -1700

19/06/17 1000 19

26/06/17 700 300 5700

COST 2900 20500

Interpretation: As per the above calculations it has been interpreted that ABC Ltd has

sold the first unit for 700 from the total unit of 1000. Further, the remaining was 300 than 1400

units were to be sold out of 1300 which has negative inventory balance for 100. This requirement

of the 100 units is to be cover with the next sale of 800 units from 2000 of total units. However,

after calculating the prices of such materials, it has shown the profit of 20500.

FIFO technique: This method is used as the first input unit to be sold firstly at the initial

rates over such products. ABC Ltd will be able to make sales of the firstly purchased units to be

sold first (Adam and Bevan, 2016). Hence, here calculations for calculating closing inventory on

the basis of FIFO of ABC Ltd si enumerated below:

DATE UNITS SALES BALANCE RATE/UNIT PRICE

02/06/17 2000 15

06/06/17 800 1200 18000

11/06/17 1000 17

16/06/17 1400 800 13600

19/06/17 1000 19

26/06/17 700 1100 20900

COST 2900 52500

3

fruitfulness in selling the last input material to be first. However, here are calculations for ABC

Ltd using LIFO method in selling the units:

Date Units Sales Balance Rate / unit Price

02/06/17 2000 15

06/06/17 800 1100 16500

11/06/17 1000 17

16/06/17 1400 -100 -1700

19/06/17 1000 19

26/06/17 700 300 5700

COST 2900 20500

Interpretation: As per the above calculations it has been interpreted that ABC Ltd has

sold the first unit for 700 from the total unit of 1000. Further, the remaining was 300 than 1400

units were to be sold out of 1300 which has negative inventory balance for 100. This requirement

of the 100 units is to be cover with the next sale of 800 units from 2000 of total units. However,

after calculating the prices of such materials, it has shown the profit of 20500.

FIFO technique: This method is used as the first input unit to be sold firstly at the initial

rates over such products. ABC Ltd will be able to make sales of the firstly purchased units to be

sold first (Adam and Bevan, 2016). Hence, here calculations for calculating closing inventory on

the basis of FIFO of ABC Ltd si enumerated below:

DATE UNITS SALES BALANCE RATE/UNIT PRICE

02/06/17 2000 15

06/06/17 800 1200 18000

11/06/17 1000 17

16/06/17 1400 800 13600

19/06/17 1000 19

26/06/17 700 1100 20900

COST 2900 52500

3

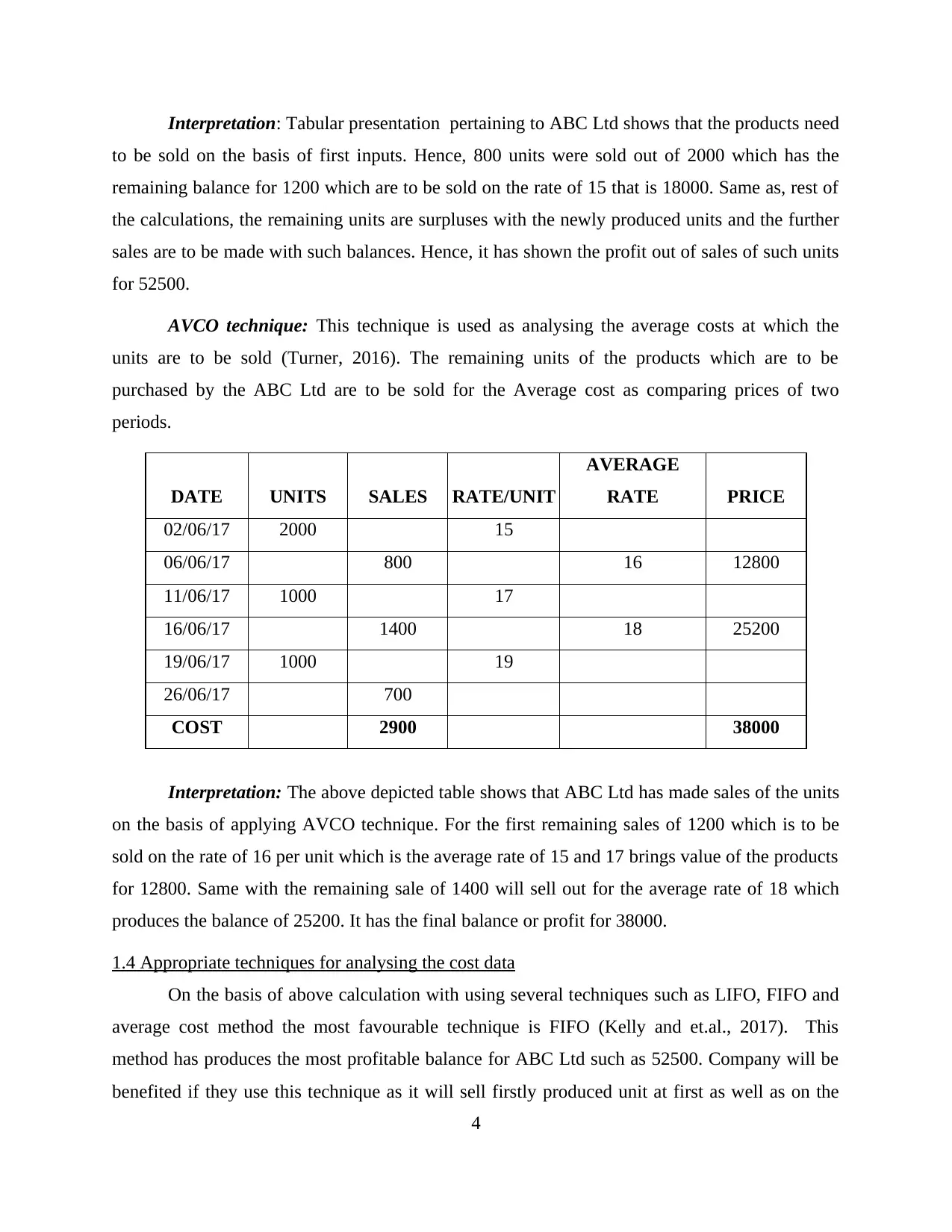

Interpretation: Tabular presentation pertaining to ABC Ltd shows that the products need

to be sold on the basis of first inputs. Hence, 800 units were sold out of 2000 which has the

remaining balance for 1200 which are to be sold on the rate of 15 that is 18000. Same as, rest of

the calculations, the remaining units are surpluses with the newly produced units and the further

sales are to be made with such balances. Hence, it has shown the profit out of sales of such units

for 52500.

AVCO technique: This technique is used as analysing the average costs at which the

units are to be sold (Turner, 2016). The remaining units of the products which are to be

purchased by the ABC Ltd are to be sold for the Average cost as comparing prices of two

periods.

DATE UNITS SALES RATE/UNIT

AVERAGE

RATE PRICE

02/06/17 2000 15

06/06/17 800 16 12800

11/06/17 1000 17

16/06/17 1400 18 25200

19/06/17 1000 19

26/06/17 700

COST 2900 38000

Interpretation: The above depicted table shows that ABC Ltd has made sales of the units

on the basis of applying AVCO technique. For the first remaining sales of 1200 which is to be

sold on the rate of 16 per unit which is the average rate of 15 and 17 brings value of the products

for 12800. Same with the remaining sale of 1400 will sell out for the average rate of 18 which

produces the balance of 25200. It has the final balance or profit for 38000.

1.4 Appropriate techniques for analysing the cost data

On the basis of above calculation with using several techniques such as LIFO, FIFO and

average cost method the most favourable technique is FIFO (Kelly and et.al., 2017). This

method has produces the most profitable balance for ABC Ltd such as 52500. Company will be

benefited if they use this technique as it will sell firstly produced unit at first as well as on the

4

to be sold on the basis of first inputs. Hence, 800 units were sold out of 2000 which has the

remaining balance for 1200 which are to be sold on the rate of 15 that is 18000. Same as, rest of

the calculations, the remaining units are surpluses with the newly produced units and the further

sales are to be made with such balances. Hence, it has shown the profit out of sales of such units

for 52500.

AVCO technique: This technique is used as analysing the average costs at which the

units are to be sold (Turner, 2016). The remaining units of the products which are to be

purchased by the ABC Ltd are to be sold for the Average cost as comparing prices of two

periods.

DATE UNITS SALES RATE/UNIT

AVERAGE

RATE PRICE

02/06/17 2000 15

06/06/17 800 16 12800

11/06/17 1000 17

16/06/17 1400 18 25200

19/06/17 1000 19

26/06/17 700

COST 2900 38000

Interpretation: The above depicted table shows that ABC Ltd has made sales of the units

on the basis of applying AVCO technique. For the first remaining sales of 1200 which is to be

sold on the rate of 16 per unit which is the average rate of 15 and 17 brings value of the products

for 12800. Same with the remaining sale of 1400 will sell out for the average rate of 18 which

produces the balance of 25200. It has the final balance or profit for 38000.

1.4 Appropriate techniques for analysing the cost data

On the basis of above calculation with using several techniques such as LIFO, FIFO and

average cost method the most favourable technique is FIFO (Kelly and et.al., 2017). This

method has produces the most profitable balance for ABC Ltd such as 52500. Company will be

benefited if they use this technique as it will sell firstly produced unit at first as well as on the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

initial rates applied over it. As compare with other techniques such as LIFO and AVCO, there is

not such appreciable balance.

TASK 2

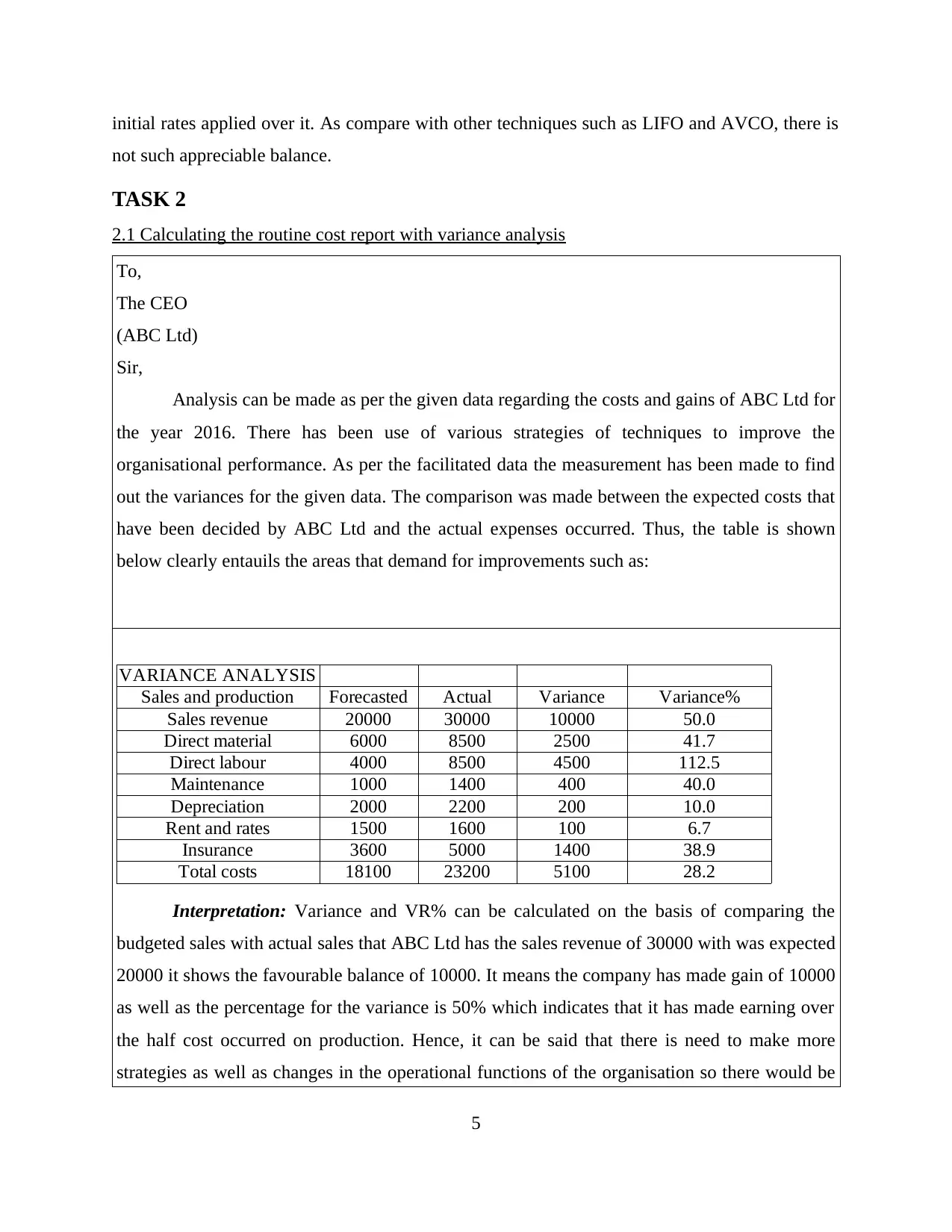

2.1 Calculating the routine cost report with variance analysis

To,

The CEO

(ABC Ltd)

Sir,

Analysis can be made as per the given data regarding the costs and gains of ABC Ltd for

the year 2016. There has been use of various strategies of techniques to improve the

organisational performance. As per the facilitated data the measurement has been made to find

out the variances for the given data. The comparison was made between the expected costs that

have been decided by ABC Ltd and the actual expenses occurred. Thus, the table is shown

below clearly entauils the areas that demand for improvements such as:

VARIANCE ANALYSIS

Sales and production Forecasted Actual Variance Variance%

Sales revenue 20000 30000 10000 50.0

Direct material 6000 8500 2500 41.7

Direct labour 4000 8500 4500 112.5

Maintenance 1000 1400 400 40.0

Depreciation 2000 2200 200 10.0

Rent and rates 1500 1600 100 6.7

Insurance 3600 5000 1400 38.9

Total costs 18100 23200 5100 28.2

Interpretation: Variance and VR% can be calculated on the basis of comparing the

budgeted sales with actual sales that ABC Ltd has the sales revenue of 30000 with was expected

20000 it shows the favourable balance of 10000. It means the company has made gain of 10000

as well as the percentage for the variance is 50% which indicates that it has made earning over

the half cost occurred on production. Hence, it can be said that there is need to make more

strategies as well as changes in the operational functions of the organisation so there would be

5

not such appreciable balance.

TASK 2

2.1 Calculating the routine cost report with variance analysis

To,

The CEO

(ABC Ltd)

Sir,

Analysis can be made as per the given data regarding the costs and gains of ABC Ltd for

the year 2016. There has been use of various strategies of techniques to improve the

organisational performance. As per the facilitated data the measurement has been made to find

out the variances for the given data. The comparison was made between the expected costs that

have been decided by ABC Ltd and the actual expenses occurred. Thus, the table is shown

below clearly entauils the areas that demand for improvements such as:

VARIANCE ANALYSIS

Sales and production Forecasted Actual Variance Variance%

Sales revenue 20000 30000 10000 50.0

Direct material 6000 8500 2500 41.7

Direct labour 4000 8500 4500 112.5

Maintenance 1000 1400 400 40.0

Depreciation 2000 2200 200 10.0

Rent and rates 1500 1600 100 6.7

Insurance 3600 5000 1400 38.9

Total costs 18100 23200 5100 28.2

Interpretation: Variance and VR% can be calculated on the basis of comparing the

budgeted sales with actual sales that ABC Ltd has the sales revenue of 30000 with was expected

20000 it shows the favourable balance of 10000. It means the company has made gain of 10000

as well as the percentage for the variance is 50% which indicates that it has made earning over

the half cost occurred on production. Hence, it can be said that there is need to make more

strategies as well as changes in the operational functions of the organisation so there would be

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

better profitability in the future.

Thanks and Regards,

Management Accountant

(ABC Ltd.)

2.2 Potential improvements for ABC Ltd with the help of performance indicators

For the potential growth of ABC Ltd in the competitive market there is need to measure

the performance of the entity with the expected requirements. With the help of various key

performance indicators, organisation will be benefited to use various techniques. They need to

make various techniques or strategies to focus over several operational activities of the firm like

sales occurred during the financial year (Koochakpour and Tarokh, 2017). Indicating tools such

as marketing matrix, financial analysis etc. will be fruitful to know the actual condition or

standard of the business in competitive market. Company need to develop the distributional

channel as it facilitates in having the best suppliers of direct material.

2.3 Suggestion for reducing costs as well as improving quality and value

On the basis of above listed performances of the organisation it is to be recommend that

ABC Ltd must do focus over improving marketing techniques (Mo and et.al., 2017). With the

help of promotional techniques there will be increment of sales and the business will be fruitful

in reducing the costs incurred while producing a unit. They need to focus over lowering down

the labour costs used for manufacturing goods, in spite of this there must be installation of

various machineries which will lower down the expenses as well as the time consumed in

producing the units.

TASK 3

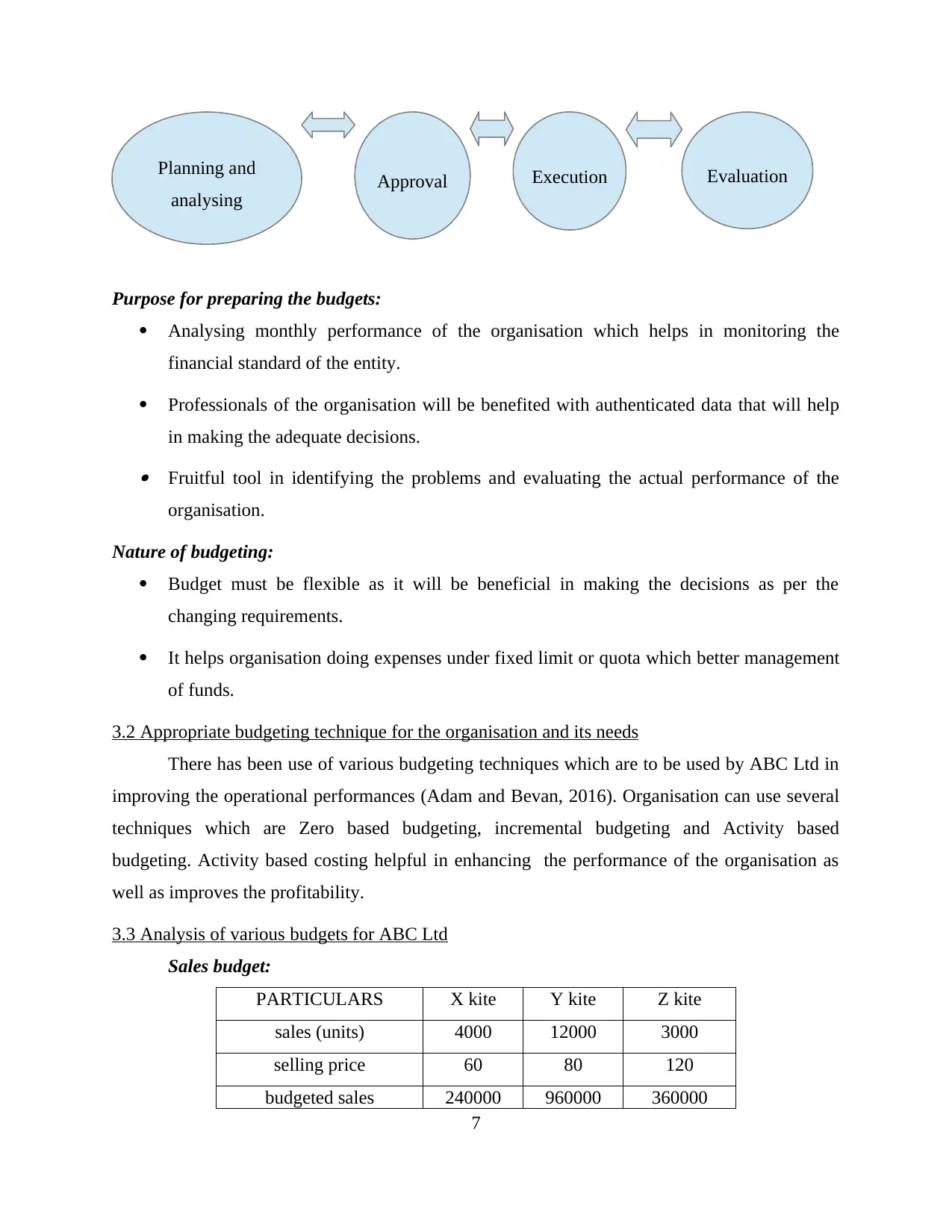

3.1 Explaining budgeting process and its nature as well as objective

Budgets can be prepared on the basis of four terms such as:

6

BUDGET PROCESS

Thanks and Regards,

Management Accountant

(ABC Ltd.)

2.2 Potential improvements for ABC Ltd with the help of performance indicators

For the potential growth of ABC Ltd in the competitive market there is need to measure

the performance of the entity with the expected requirements. With the help of various key

performance indicators, organisation will be benefited to use various techniques. They need to

make various techniques or strategies to focus over several operational activities of the firm like

sales occurred during the financial year (Koochakpour and Tarokh, 2017). Indicating tools such

as marketing matrix, financial analysis etc. will be fruitful to know the actual condition or

standard of the business in competitive market. Company need to develop the distributional

channel as it facilitates in having the best suppliers of direct material.

2.3 Suggestion for reducing costs as well as improving quality and value

On the basis of above listed performances of the organisation it is to be recommend that

ABC Ltd must do focus over improving marketing techniques (Mo and et.al., 2017). With the

help of promotional techniques there will be increment of sales and the business will be fruitful

in reducing the costs incurred while producing a unit. They need to focus over lowering down

the labour costs used for manufacturing goods, in spite of this there must be installation of

various machineries which will lower down the expenses as well as the time consumed in

producing the units.

TASK 3

3.1 Explaining budgeting process and its nature as well as objective

Budgets can be prepared on the basis of four terms such as:

6

BUDGET PROCESS

Purpose for preparing the budgets:

Analysing monthly performance of the organisation which helps in monitoring the

financial standard of the entity.

Professionals of the organisation will be benefited with authenticated data that will help

in making the adequate decisions. Fruitful tool in identifying the problems and evaluating the actual performance of the

organisation.

Nature of budgeting:

Budget must be flexible as it will be beneficial in making the decisions as per the

changing requirements.

It helps organisation doing expenses under fixed limit or quota which better management

of funds.

3.2 Appropriate budgeting technique for the organisation and its needs

There has been use of various budgeting techniques which are to be used by ABC Ltd in

improving the operational performances (Adam and Bevan, 2016). Organisation can use several

techniques which are Zero based budgeting, incremental budgeting and Activity based

budgeting. Activity based costing helpful in enhancing the performance of the organisation as

well as improves the profitability.

3.3 Analysis of various budgets for ABC Ltd

Sales budget:

PARTICULARS X kite Y kite Z kite

sales (units) 4000 12000 3000

selling price 60 80 120

budgeted sales 240000 960000 360000

7

Planning and

analysing Approval Execution Evaluation

Analysing monthly performance of the organisation which helps in monitoring the

financial standard of the entity.

Professionals of the organisation will be benefited with authenticated data that will help

in making the adequate decisions. Fruitful tool in identifying the problems and evaluating the actual performance of the

organisation.

Nature of budgeting:

Budget must be flexible as it will be beneficial in making the decisions as per the

changing requirements.

It helps organisation doing expenses under fixed limit or quota which better management

of funds.

3.2 Appropriate budgeting technique for the organisation and its needs

There has been use of various budgeting techniques which are to be used by ABC Ltd in

improving the operational performances (Adam and Bevan, 2016). Organisation can use several

techniques which are Zero based budgeting, incremental budgeting and Activity based

budgeting. Activity based costing helpful in enhancing the performance of the organisation as

well as improves the profitability.

3.3 Analysis of various budgets for ABC Ltd

Sales budget:

PARTICULARS X kite Y kite Z kite

sales (units) 4000 12000 3000

selling price 60 80 120

budgeted sales 240000 960000 360000

7

Planning and

analysing Approval Execution Evaluation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

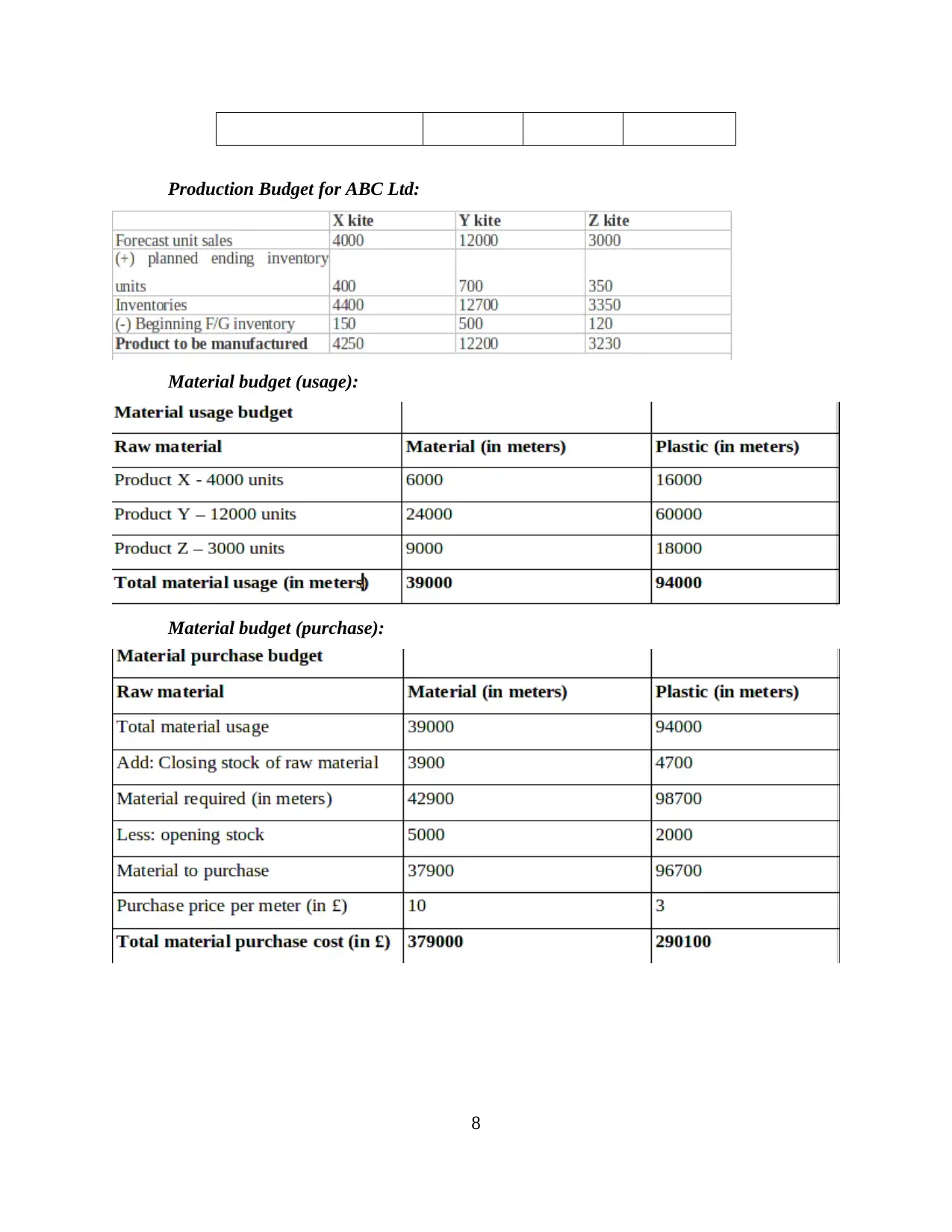

Production Budget for ABC Ltd:

Material budget (usage):

Material budget (purchase):

8

Material budget (usage):

Material budget (purchase):

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

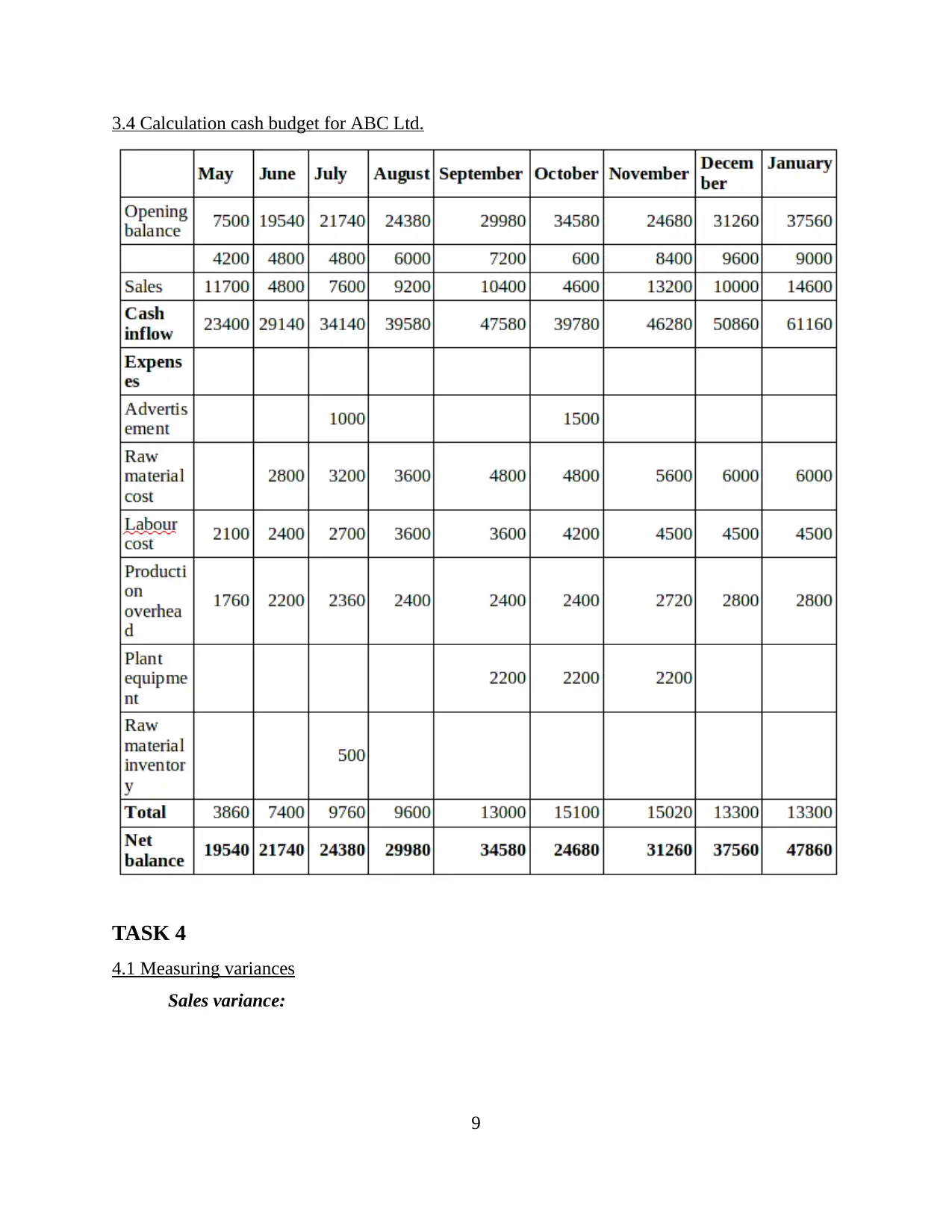

3.4 Calculation cash budget for ABC Ltd.

TASK 4

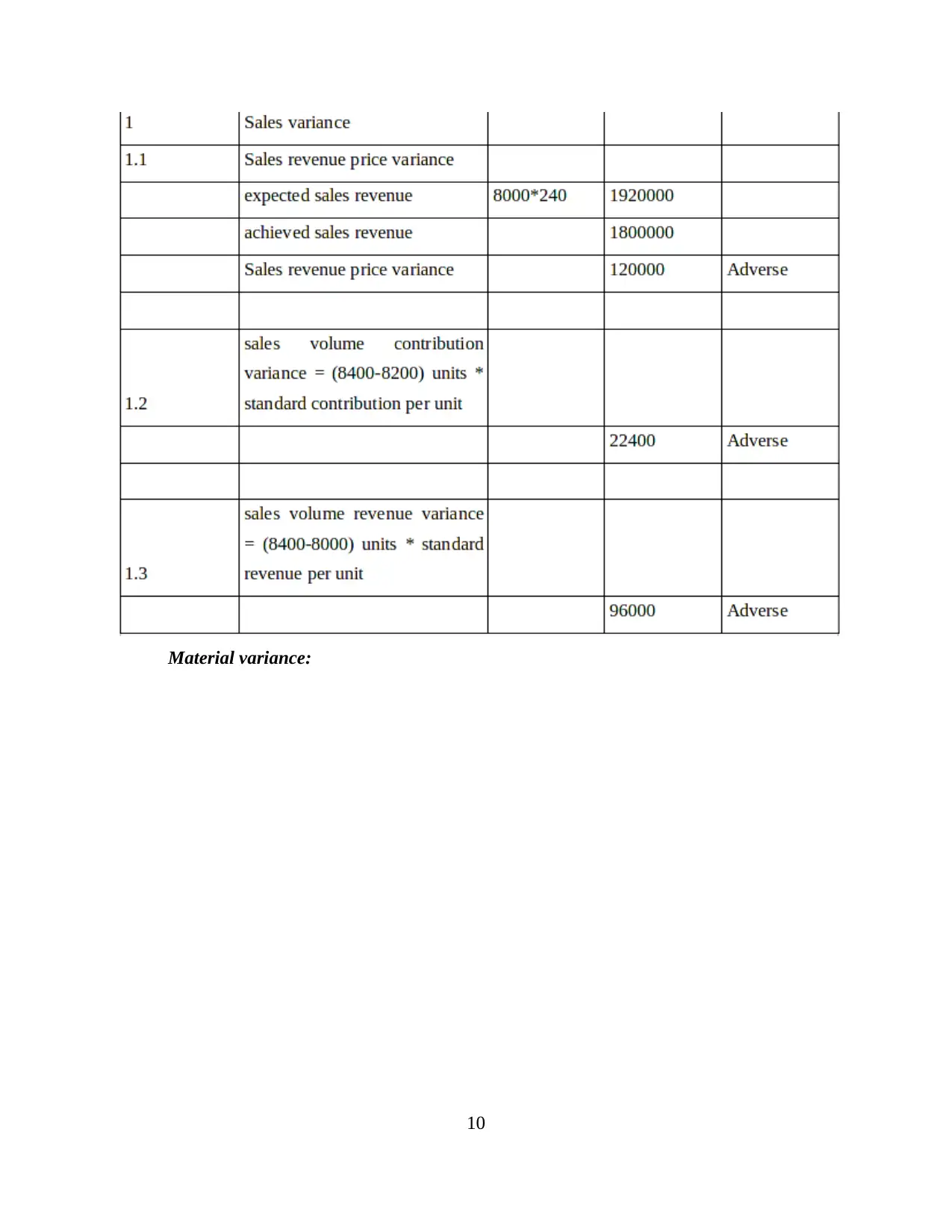

4.1 Measuring variances

Sales variance:

9

TASK 4

4.1 Measuring variances

Sales variance:

9

Material variance:

10

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.