Management Accounting Analysis for R.L. Maynard Company Report

VerifiedAdded on 2020/01/28

|16

|3860

|104

Report

AI Summary

This report analyzes management accounting practices within the context of the R.L. Maynard Company. It begins with an explanation of management accounting, its types (lean, traditional, throughput, and transfer pricing), and its role in decision-making. The report then details various management accounting reporting methods, including sales reports, cost accounting, and budgetary reports. A significant portion of the report focuses on calculating net profit using both marginal and absorption costing methods, providing income statements for each method and comparing their outcomes. The report also examines the advantages and disadvantages of different planning tools used for budgetary control, and it concludes with a comparison of how organizations respond to financial problems. The analysis highlights the importance of management accounting in financial planning, cost control, and strategic decision-making, with a specific focus on the application of these concepts within the R.L. Maynard Company.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and its types......................................................................3

P2 Explain different methods used for management accounting reporting................................5

TASK 2............................................................................................................................................6

P3 Calculate of net profit by using various costing methods......................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of various types of planning tools .......................................9

TASK 4..........................................................................................................................................12

P5 Comparison how organisation and how they respond to financial problems......................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Explain management accounting and its types......................................................................3

P2 Explain different methods used for management accounting reporting................................5

TASK 2............................................................................................................................................6

P3 Calculate of net profit by using various costing methods......................................................6

TASK 3............................................................................................................................................9

P4 Advantages and disadvantages of various types of planning tools .......................................9

TASK 4..........................................................................................................................................12

P5 Comparison how organisation and how they respond to financial problems......................12

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Managerial decisions are very vital for the organisation that gives the new blood to the

organisation. It manages all the resources, minimizing cost, control budgets and planning regard

to business. It can be possible through the information that are provided in the management

accounting that facilitate them in to making financial decisions regard to finance. The research

project is context to the R.L. Maynard company in which it manager adopt various planning

tools, management accounting system and reporting (Burritt, Schaltegger and Zvezdov, 2011).

There is a mainly discussion on the management accounting and study on the different types of

management of accounting system that easily responding financial problem. Thereafter, it there

is discussion on marginal costing and absorption costing techniques that are adopted by company

to prepared net profit. Further, there is a study on the explanation on advantages and

disadvantages of various types of planning tools that can be used for budgetary control.

TASK 1

P1 Explain management accounting and its types

Management accounting is used by the managers in order to make effective decisions

regard to firm. The information includes in it are helpful for the manager to run their day to day

business operation in effective manner. Thus, it involves a accounting information that are useful

for the management for the main purpose of performance management system, devising planning

and also controlling in formulation of business's strategy. The main aim of these type of

accounting is that to give proper advice to the managers regard to financial consequences of

firms decisions, help in controlling financial aspects, also describe the effects of the competitive

landscape (Elbashir, Collier and Sutton, 2011). Therefore, it is different from the financial

accounting as it is always looking for future rather than historical data. R.L. Maynard company

used management accounting and it provide essential requirements of different type of

management accounting system that are described below-

Lean accounting- It together brings the control, performance measurement methods and

accounting which supporting the lean manufacturing introduction. It does not support the

lean manufacturing but employed the lean methods. It mainly focusses on minimizing the

cost of goods sold rather than determining the cost that are incur are the time of

manufacturing process. There are several functions in these accounting that are perform

by the lean accounting that includes removing non-value -add procedure in reporting as

Managerial decisions are very vital for the organisation that gives the new blood to the

organisation. It manages all the resources, minimizing cost, control budgets and planning regard

to business. It can be possible through the information that are provided in the management

accounting that facilitate them in to making financial decisions regard to finance. The research

project is context to the R.L. Maynard company in which it manager adopt various planning

tools, management accounting system and reporting (Burritt, Schaltegger and Zvezdov, 2011).

There is a mainly discussion on the management accounting and study on the different types of

management of accounting system that easily responding financial problem. Thereafter, it there

is discussion on marginal costing and absorption costing techniques that are adopted by company

to prepared net profit. Further, there is a study on the explanation on advantages and

disadvantages of various types of planning tools that can be used for budgetary control.

TASK 1

P1 Explain management accounting and its types

Management accounting is used by the managers in order to make effective decisions

regard to firm. The information includes in it are helpful for the manager to run their day to day

business operation in effective manner. Thus, it involves a accounting information that are useful

for the management for the main purpose of performance management system, devising planning

and also controlling in formulation of business's strategy. The main aim of these type of

accounting is that to give proper advice to the managers regard to financial consequences of

firms decisions, help in controlling financial aspects, also describe the effects of the competitive

landscape (Elbashir, Collier and Sutton, 2011). Therefore, it is different from the financial

accounting as it is always looking for future rather than historical data. R.L. Maynard company

used management accounting and it provide essential requirements of different type of

management accounting system that are described below-

Lean accounting- It together brings the control, performance measurement methods and

accounting which supporting the lean manufacturing introduction. It does not support the

lean manufacturing but employed the lean methods. It mainly focusses on minimizing the

cost of goods sold rather than determining the cost that are incur are the time of

manufacturing process. There are several functions in these accounting that are perform

by the lean accounting that includes removing non-value -add procedure in reporting as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

well as accounting. Further, give a clear understanding of probability in apposition to

product lines and it generate a real-time report on regular basis. Thus, ignore the months

end as well as historical week reports.

Traditional cost accounting- It can be defining as a allocating the production expenses

that are produced at the time of manufacturing a goods. It is also known as a conventional

method as it assigning the indirect cost incur in factory at the time of manufacturing an

item. It includes mainly in it are the production machine hours, number of units produced

and direct labour hours etc. R.L. Maynard adopts the traditional costing method in which

it assigns the manufacturing cost and it fails in allocating the non-manufacturing. The

main advantages from it is that to generate the financial reports as it assists them in

providing a value for COGS. Apart from this, with the advancement of computer and

machines now this system becomes outdated. It is bad for the management in their

decisions-making process as it does non-consider the non-manufacturing expense.

Throughput accounting- It is based upon principle and it is very new in the

management accounting. It is an accounting through it identifies factor that facilitate

them in achieve its goals and objectives in effective manner. It mainly focusses on cash

transaction and ignore the costing as well as cost accounting. It does not assign all the

expenses such as variable and fixed cost as well as it also involves overheads related to

goods that are offer by company (Elbashir, Collier and Sutton, 2011). It is a theory of

constraints through which manager of a company can easily make decisions that are

relate to growth purpose.

Transfer pricing- It is that price in which a government formulating the rules when one

enterprises transfer any kind of goods across borders. Therefore,it is used by the

management accountant to determine the cost that are incur at the time of transaction

among division. Furthermore, these prices are normally set for the intermediate goods

which are supplied through selling to buying division. The main advantage of this is that

it provides accuracy as well as fairness about the business entities as there are various

regulation are formulated in transfer price.

product lines and it generate a real-time report on regular basis. Thus, ignore the months

end as well as historical week reports.

Traditional cost accounting- It can be defining as a allocating the production expenses

that are produced at the time of manufacturing a goods. It is also known as a conventional

method as it assigning the indirect cost incur in factory at the time of manufacturing an

item. It includes mainly in it are the production machine hours, number of units produced

and direct labour hours etc. R.L. Maynard adopts the traditional costing method in which

it assigns the manufacturing cost and it fails in allocating the non-manufacturing. The

main advantages from it is that to generate the financial reports as it assists them in

providing a value for COGS. Apart from this, with the advancement of computer and

machines now this system becomes outdated. It is bad for the management in their

decisions-making process as it does non-consider the non-manufacturing expense.

Throughput accounting- It is based upon principle and it is very new in the

management accounting. It is an accounting through it identifies factor that facilitate

them in achieve its goals and objectives in effective manner. It mainly focusses on cash

transaction and ignore the costing as well as cost accounting. It does not assign all the

expenses such as variable and fixed cost as well as it also involves overheads related to

goods that are offer by company (Elbashir, Collier and Sutton, 2011). It is a theory of

constraints through which manager of a company can easily make decisions that are

relate to growth purpose.

Transfer pricing- It is that price in which a government formulating the rules when one

enterprises transfer any kind of goods across borders. Therefore,it is used by the

management accountant to determine the cost that are incur at the time of transaction

among division. Furthermore, these prices are normally set for the intermediate goods

which are supplied through selling to buying division. The main advantage of this is that

it provides accuracy as well as fairness about the business entities as there are various

regulation are formulated in transfer price.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P2 Explain different methods used for management accounting reporting

The R.L. Maynard adopts the various types of management accounting reporting that are

as discussed below-

Sales report- The report is based upon the sales activities that are carried out by each and

every business firm for some particular time period. It summarizing the sales of products

or services to a customers, performance of salesperson and profit of a company etc.

Furthermore, there is an also information of e-mail,customer meeting, conversation,

outbound calls that are created on daily as well as weekly and monthly basis. The main

advantages of sales report is that it can be used by company for the purpose of knowing

financial performance (Garrison and et.al., 2010). It is possible through comparison

among past financial performance with the current profits. For this, they can make

marketing plan accordingly to deliver the product or services as per the customer’s

expectation. The sales report is used by the managers to finding out the market

opportunities and trends so, they can easily increase sales volume of product or services

in the particular area.

Cost accounting- It is useful for the management in order to provide a accurate amount

on financial statements as it determined the cost of projects, process and products etc. It

is also assist the manager in taking decision in effective way, controlling the organisation

functions etc. Therefore, it is best management accounting system that are used by most

of the manufacturing companies in computing the unit cost of products that are

manufactured (Ward, 2012). For the purpose of reporting the inventory cost on its B/S

and COGS on the income statement. R.L. Maynard used cost accounting to determine

cost, control cost and give the future decisions related to cost that are based upon

historical cost data.

Budgetary report- It is a detailed information that are mainly comprised into two

columns are the budgeted outlays and actual. It facilitates them in determine the budget

variance among budgeted and actual amount over an accounting period. It is a internal

report in which it can easily designed budget for a future through comparison estimated

and comparison budgeted. The report has a two uses one is that when any issues arise

within the workplace regard to finance that are be easily reviewing through budget report.

The R.L. Maynard adopts the various types of management accounting reporting that are

as discussed below-

Sales report- The report is based upon the sales activities that are carried out by each and

every business firm for some particular time period. It summarizing the sales of products

or services to a customers, performance of salesperson and profit of a company etc.

Furthermore, there is an also information of e-mail,customer meeting, conversation,

outbound calls that are created on daily as well as weekly and monthly basis. The main

advantages of sales report is that it can be used by company for the purpose of knowing

financial performance (Garrison and et.al., 2010). It is possible through comparison

among past financial performance with the current profits. For this, they can make

marketing plan accordingly to deliver the product or services as per the customer’s

expectation. The sales report is used by the managers to finding out the market

opportunities and trends so, they can easily increase sales volume of product or services

in the particular area.

Cost accounting- It is useful for the management in order to provide a accurate amount

on financial statements as it determined the cost of projects, process and products etc. It

is also assist the manager in taking decision in effective way, controlling the organisation

functions etc. Therefore, it is best management accounting system that are used by most

of the manufacturing companies in computing the unit cost of products that are

manufactured (Ward, 2012). For the purpose of reporting the inventory cost on its B/S

and COGS on the income statement. R.L. Maynard used cost accounting to determine

cost, control cost and give the future decisions related to cost that are based upon

historical cost data.

Budgetary report- It is a detailed information that are mainly comprised into two

columns are the budgeted outlays and actual. It facilitates them in determine the budget

variance among budgeted and actual amount over an accounting period. It is a internal

report in which it can easily designed budget for a future through comparison estimated

and comparison budgeted. The report has a two uses one is that when any issues arise

within the workplace regard to finance that are be easily reviewing through budget report.

Furthermore, it has a one more purpose in which they can easily make prediction and

evaluating the company's financial performance.

TASK 2

P3 Calculate of net profit by using various costing methods

Income statements is a financial position of a firm that can be categorised into two parts

revenue and expenditure. It is a financial statement of a company that are prepared in specific

accounting period that can be judge firm's financial performance based on net profit or net loss.

The accountant put all the activities that are related to operating and non-operating activities on

the debit and credit side (Zimmerman and Yahya-Zadeh, 2011). It can be prepared by company's

accountant by adopting management costing techniques either marginal and absorption costing.

R.L Maynard management accountant prepared income statement by adopting both techniques to

finding out the net profit or loss of firm. It has been shown in the table 1 and table 2 in which Net

profit/ loss prepared by both management costing techniques are as follows-

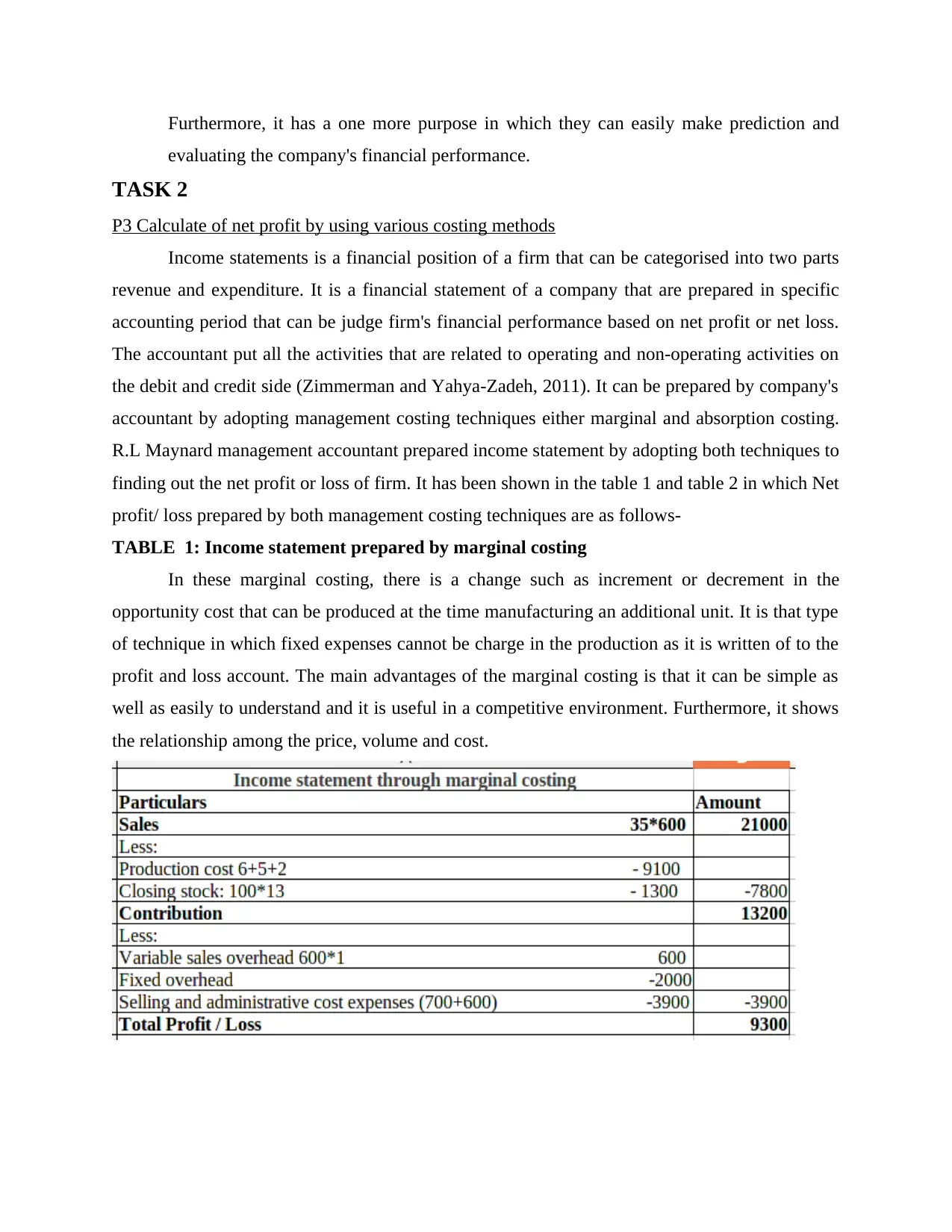

TABLE 1: Income statement prepared by marginal costing

In these marginal costing, there is a change such as increment or decrement in the

opportunity cost that can be produced at the time manufacturing an additional unit. It is that type

of technique in which fixed expenses cannot be charge in the production as it is written of to the

profit and loss account. The main advantages of the marginal costing is that it can be simple as

well as easily to understand and it is useful in a competitive environment. Furthermore, it shows

the relationship among the price, volume and cost.

evaluating the company's financial performance.

TASK 2

P3 Calculate of net profit by using various costing methods

Income statements is a financial position of a firm that can be categorised into two parts

revenue and expenditure. It is a financial statement of a company that are prepared in specific

accounting period that can be judge firm's financial performance based on net profit or net loss.

The accountant put all the activities that are related to operating and non-operating activities on

the debit and credit side (Zimmerman and Yahya-Zadeh, 2011). It can be prepared by company's

accountant by adopting management costing techniques either marginal and absorption costing.

R.L Maynard management accountant prepared income statement by adopting both techniques to

finding out the net profit or loss of firm. It has been shown in the table 1 and table 2 in which Net

profit/ loss prepared by both management costing techniques are as follows-

TABLE 1: Income statement prepared by marginal costing

In these marginal costing, there is a change such as increment or decrement in the

opportunity cost that can be produced at the time manufacturing an additional unit. It is that type

of technique in which fixed expenses cannot be charge in the production as it is written of to the

profit and loss account. The main advantages of the marginal costing is that it can be simple as

well as easily to understand and it is useful in a competitive environment. Furthermore, it shows

the relationship among the price, volume and cost.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

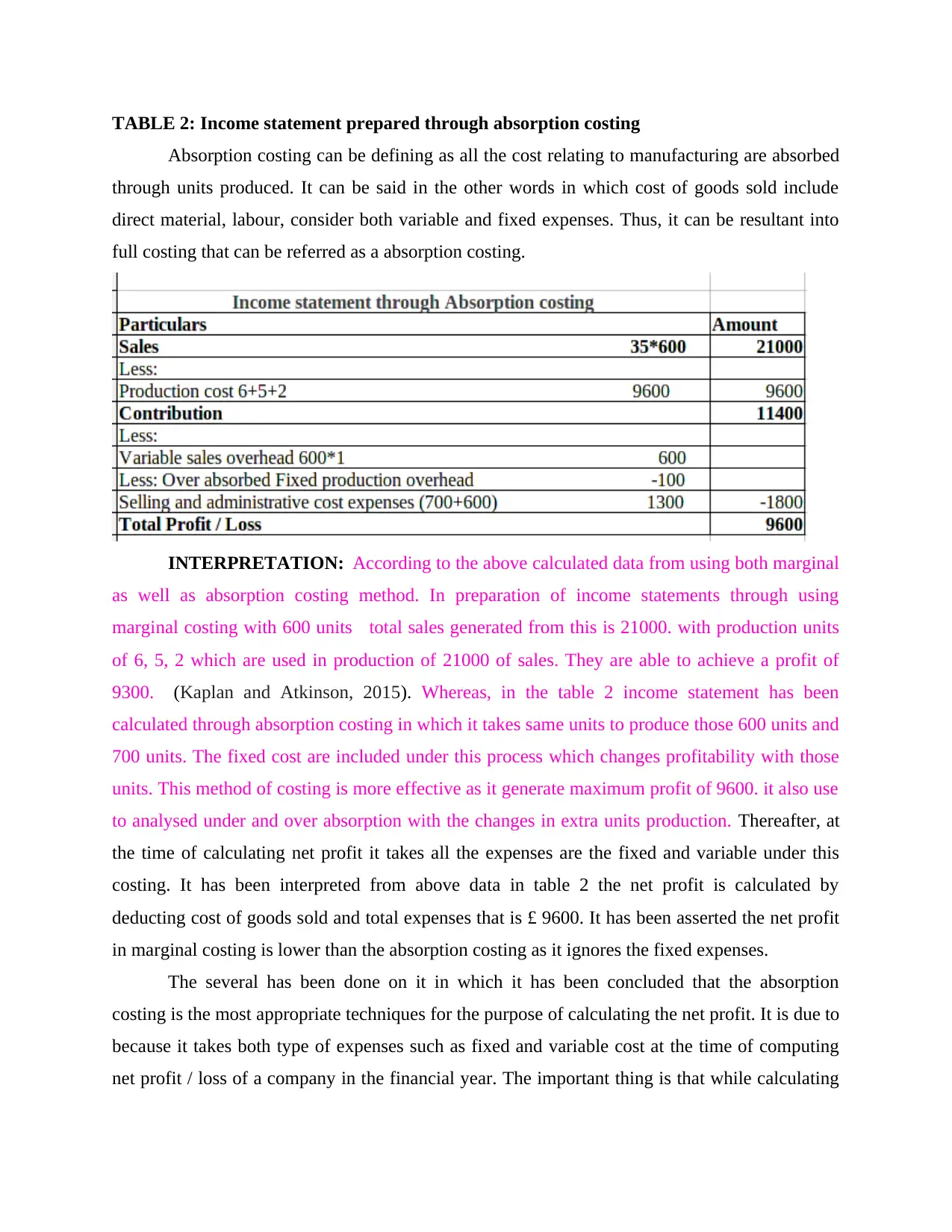

TABLE 2: Income statement prepared through absorption costing

Absorption costing can be defining as all the cost relating to manufacturing are absorbed

through units produced. It can be said in the other words in which cost of goods sold include

direct material, labour, consider both variable and fixed expenses. Thus, it can be resultant into

full costing that can be referred as a absorption costing.

INTERPRETATION: According to the above calculated data from using both marginal

as well as absorption costing method. In preparation of income statements through using

marginal costing with 600 units total sales generated from this is 21000. with production units

of 6, 5, 2 which are used in production of 21000 of sales. They are able to achieve a profit of

9300. (Kaplan and Atkinson, 2015). Whereas, in the table 2 income statement has been

calculated through absorption costing in which it takes same units to produce those 600 units and

700 units. The fixed cost are included under this process which changes profitability with those

units. This method of costing is more effective as it generate maximum profit of 9600. it also use

to analysed under and over absorption with the changes in extra units production. Thereafter, at

the time of calculating net profit it takes all the expenses are the fixed and variable under this

costing. It has been interpreted from above data in table 2 the net profit is calculated by

deducting cost of goods sold and total expenses that is £ 9600. It has been asserted the net profit

in marginal costing is lower than the absorption costing as it ignores the fixed expenses.

The several has been done on it in which it has been concluded that the absorption

costing is the most appropriate techniques for the purpose of calculating the net profit. It is due to

because it takes both type of expenses such as fixed and variable cost at the time of computing

net profit / loss of a company in the financial year. The important thing is that while calculating

Absorption costing can be defining as all the cost relating to manufacturing are absorbed

through units produced. It can be said in the other words in which cost of goods sold include

direct material, labour, consider both variable and fixed expenses. Thus, it can be resultant into

full costing that can be referred as a absorption costing.

INTERPRETATION: According to the above calculated data from using both marginal

as well as absorption costing method. In preparation of income statements through using

marginal costing with 600 units total sales generated from this is 21000. with production units

of 6, 5, 2 which are used in production of 21000 of sales. They are able to achieve a profit of

9300. (Kaplan and Atkinson, 2015). Whereas, in the table 2 income statement has been

calculated through absorption costing in which it takes same units to produce those 600 units and

700 units. The fixed cost are included under this process which changes profitability with those

units. This method of costing is more effective as it generate maximum profit of 9600. it also use

to analysed under and over absorption with the changes in extra units production. Thereafter, at

the time of calculating net profit it takes all the expenses are the fixed and variable under this

costing. It has been interpreted from above data in table 2 the net profit is calculated by

deducting cost of goods sold and total expenses that is £ 9600. It has been asserted the net profit

in marginal costing is lower than the absorption costing as it ignores the fixed expenses.

The several has been done on it in which it has been concluded that the absorption

costing is the most appropriate techniques for the purpose of calculating the net profit. It is due to

because it takes both type of expenses such as fixed and variable cost at the time of computing

net profit / loss of a company in the financial year. The important thing is that while calculating

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profit is that the expenses that are taken must be validate and reliable data. Furthermore, most of

the manufacturing organisation adopt absorption costing methods in preparation of income

statement.

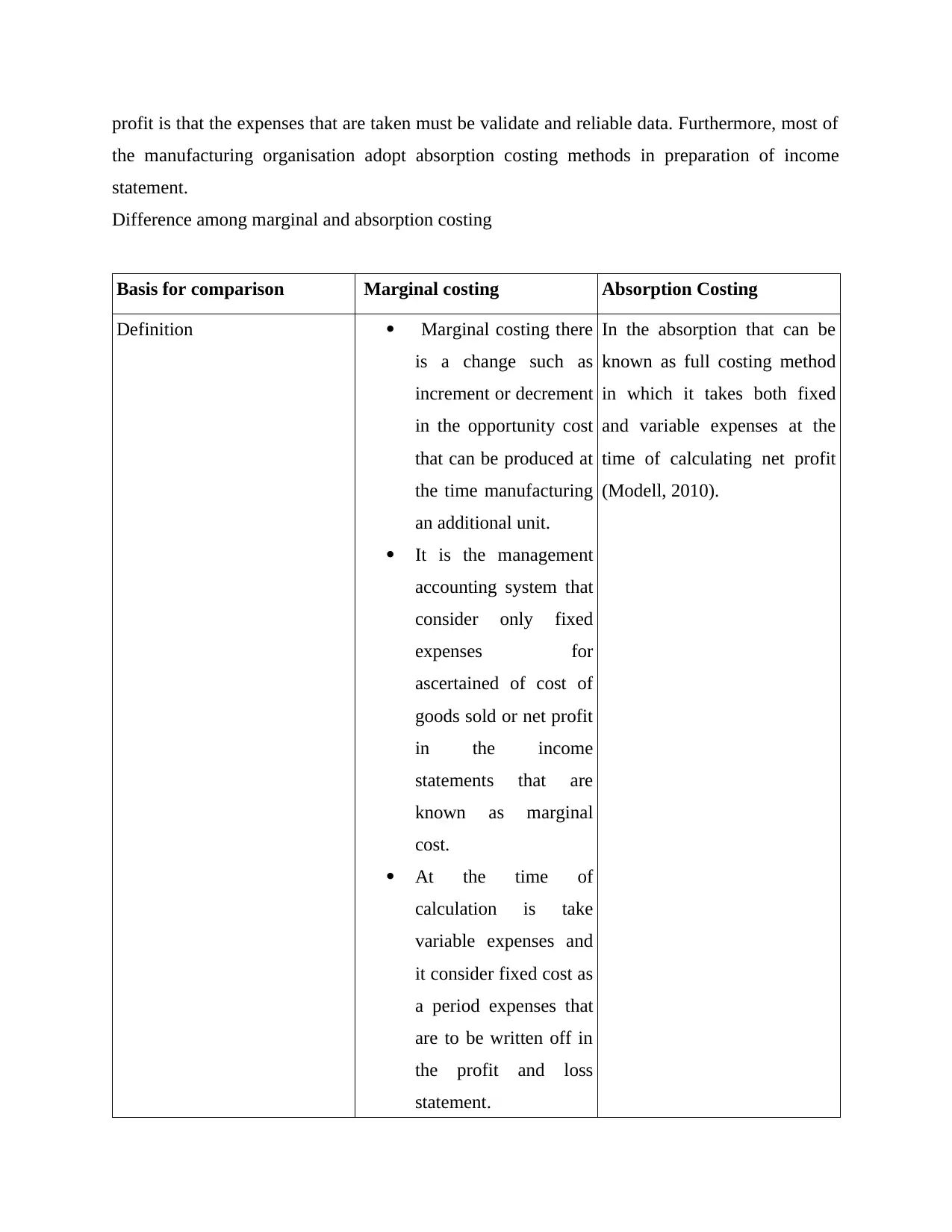

Difference among marginal and absorption costing

Basis for comparison Marginal costing Absorption Costing

Definition Marginal costing there

is a change such as

increment or decrement

in the opportunity cost

that can be produced at

the time manufacturing

an additional unit.

It is the management

accounting system that

consider only fixed

expenses for

ascertained of cost of

goods sold or net profit

in the income

statements that are

known as marginal

cost.

At the time of

calculation is take

variable expenses and

it consider fixed cost as

a period expenses that

are to be written off in

the profit and loss

statement.

In the absorption that can be

known as full costing method

in which it takes both fixed

and variable expenses at the

time of calculating net profit

(Modell, 2010).

the manufacturing organisation adopt absorption costing methods in preparation of income

statement.

Difference among marginal and absorption costing

Basis for comparison Marginal costing Absorption Costing

Definition Marginal costing there

is a change such as

increment or decrement

in the opportunity cost

that can be produced at

the time manufacturing

an additional unit.

It is the management

accounting system that

consider only fixed

expenses for

ascertained of cost of

goods sold or net profit

in the income

statements that are

known as marginal

cost.

At the time of

calculation is take

variable expenses and

it consider fixed cost as

a period expenses that

are to be written off in

the profit and loss

statement.

In the absorption that can be

known as full costing method

in which it takes both fixed

and variable expenses at the

time of calculating net profit

(Modell, 2010).

Cost recognition It take variable expenses as a

product cost and fixed cost as

periodic that are to be written

off in P/L account

It takes both fixed and

variable expenses in the

product cost.

Division of expenses It divides the expenses into

fixed and variable cost

(Macintosh and Quattrone,

2010).

In these it has been divided

into selling & Distribution

administration and production

etc.

Profits Profit can be measured

through profit-volume ratio

Profits get affected due to

intuitionism of fixed cost.

Cost per unit There is no impact on cost per

unit due to change in the

closing and opening inventory.

It influences the cost per unit if

there is an any change in the

closing and opening stock

Objectives The objectives of marginal

costing is that to make an

effective decisions that are

used by the internal member

It provides an information to

the external parties that are

outside the organisation that

are managed the organisation

activities in effective way.

Highlights Contribution per unit ( CPU) Net profit per unit( NPU)

TASK 3

P4 Advantages and disadvantages of various types of planning tools

Budgetary control it is process which shows the actual outcome by make comparison

among standard budget and actual budget over an accounting period. It provides the budget

variance due to which they can easily finding out the deficiency due to they can easily take

remedial actions. They can easily control with the help of various planning tools that are adopted

by the R.L. Maynard which has been described below-

Variance analysis- It is a variation among the standard and actual performance of a firm.

It can be known as a deviation that are categorised into two parts that is favourable and

product cost and fixed cost as

periodic that are to be written

off in P/L account

It takes both fixed and

variable expenses in the

product cost.

Division of expenses It divides the expenses into

fixed and variable cost

(Macintosh and Quattrone,

2010).

In these it has been divided

into selling & Distribution

administration and production

etc.

Profits Profit can be measured

through profit-volume ratio

Profits get affected due to

intuitionism of fixed cost.

Cost per unit There is no impact on cost per

unit due to change in the

closing and opening inventory.

It influences the cost per unit if

there is an any change in the

closing and opening stock

Objectives The objectives of marginal

costing is that to make an

effective decisions that are

used by the internal member

It provides an information to

the external parties that are

outside the organisation that

are managed the organisation

activities in effective way.

Highlights Contribution per unit ( CPU) Net profit per unit( NPU)

TASK 3

P4 Advantages and disadvantages of various types of planning tools

Budgetary control it is process which shows the actual outcome by make comparison

among standard budget and actual budget over an accounting period. It provides the budget

variance due to which they can easily finding out the deficiency due to they can easily take

remedial actions. They can easily control with the help of various planning tools that are adopted

by the R.L. Maynard which has been described below-

Variance analysis- It is a variation among the standard and actual performance of a firm.

It can be known as a deviation that are categorised into two parts that is favourable and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

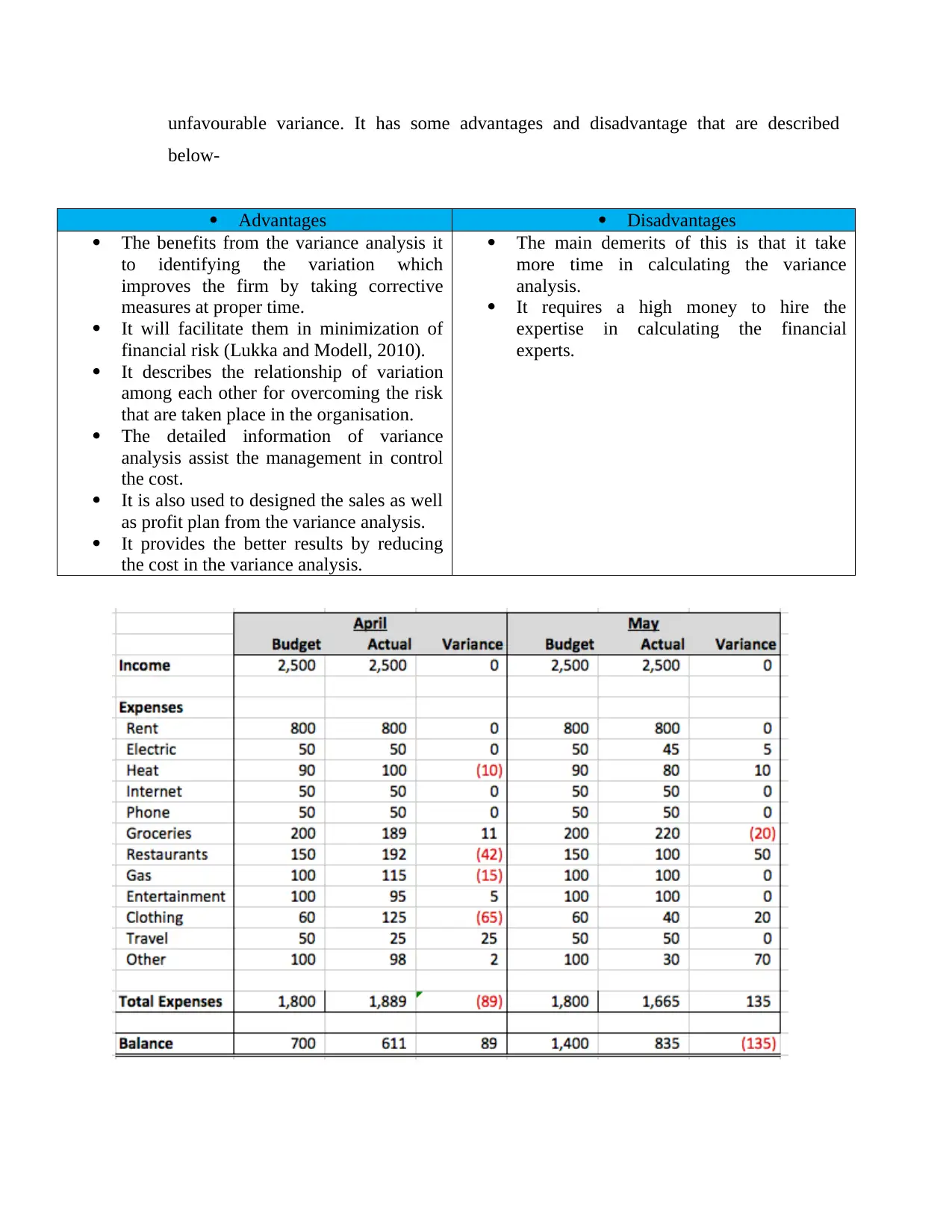

unfavourable variance. It has some advantages and disadvantage that are described

below-

Advantages Disadvantages

The benefits from the variance analysis it

to identifying the variation which

improves the firm by taking corrective

measures at proper time.

It will facilitate them in minimization of

financial risk (Lukka and Modell, 2010).

It describes the relationship of variation

among each other for overcoming the risk

that are taken place in the organisation.

The detailed information of variance

analysis assist the management in control

the cost.

It is also used to designed the sales as well

as profit plan from the variance analysis.

It provides the better results by reducing

the cost in the variance analysis.

The main demerits of this is that it take

more time in calculating the variance

analysis.

It requires a high money to hire the

expertise in calculating the financial

experts.

below-

Advantages Disadvantages

The benefits from the variance analysis it

to identifying the variation which

improves the firm by taking corrective

measures at proper time.

It will facilitate them in minimization of

financial risk (Lukka and Modell, 2010).

It describes the relationship of variation

among each other for overcoming the risk

that are taken place in the organisation.

The detailed information of variance

analysis assist the management in control

the cost.

It is also used to designed the sales as well

as profit plan from the variance analysis.

It provides the better results by reducing

the cost in the variance analysis.

The main demerits of this is that it take

more time in calculating the variance

analysis.

It requires a high money to hire the

expertise in calculating the financial

experts.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

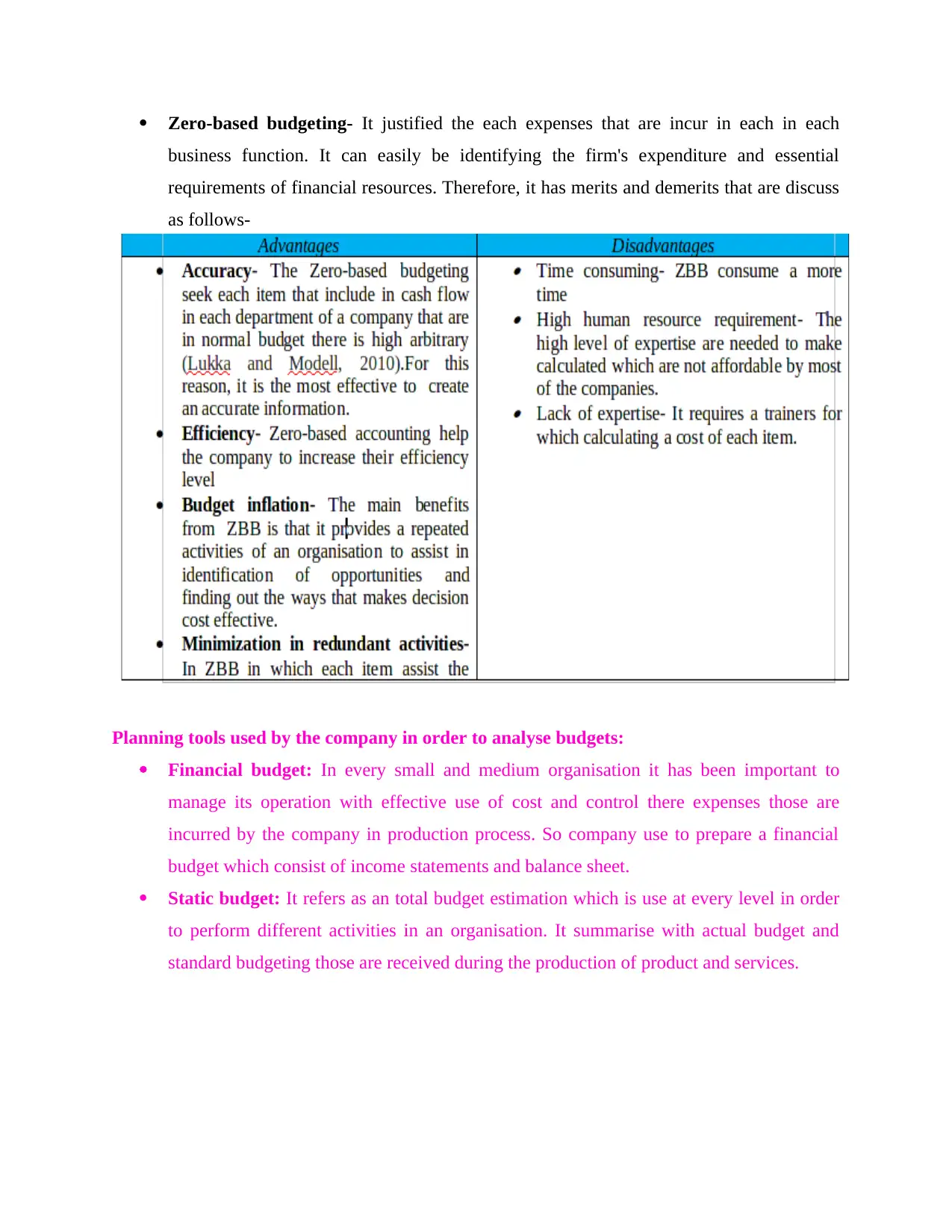

Zero-based budgeting- It justified the each expenses that are incur in each in each

business function. It can easily be identifying the firm's expenditure and essential

requirements of financial resources. Therefore, it has merits and demerits that are discuss

as follows-

Planning tools used by the company in order to analyse budgets:

Financial budget: In every small and medium organisation it has been important to

manage its operation with effective use of cost and control there expenses those are

incurred by the company in production process. So company use to prepare a financial

budget which consist of income statements and balance sheet.

Static budget: It refers as an total budget estimation which is use at every level in order

to perform different activities in an organisation. It summarise with actual budget and

standard budgeting those are received during the production of product and services.

business function. It can easily be identifying the firm's expenditure and essential

requirements of financial resources. Therefore, it has merits and demerits that are discuss

as follows-

Planning tools used by the company in order to analyse budgets:

Financial budget: In every small and medium organisation it has been important to

manage its operation with effective use of cost and control there expenses those are

incurred by the company in production process. So company use to prepare a financial

budget which consist of income statements and balance sheet.

Static budget: It refers as an total budget estimation which is use at every level in order

to perform different activities in an organisation. It summarise with actual budget and

standard budgeting those are received during the production of product and services.

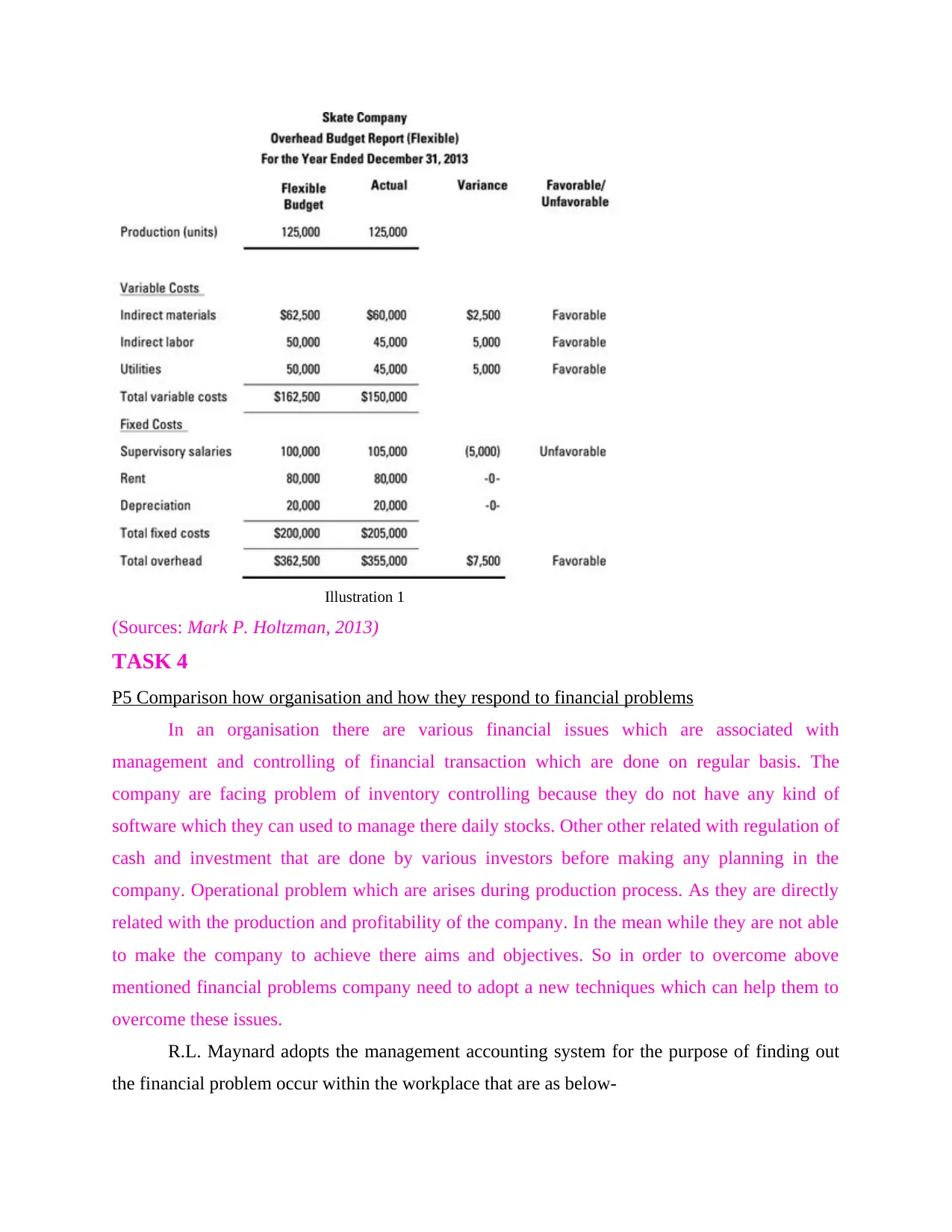

Illustration 1

(Sources: Mark P. Holtzman, 2013)

TASK 4

P5 Comparison how organisation and how they respond to financial problems

In an organisation there are various financial issues which are associated with

management and controlling of financial transaction which are done on regular basis. The

company are facing problem of inventory controlling because they do not have any kind of

software which they can used to manage there daily stocks. Other other related with regulation of

cash and investment that are done by various investors before making any planning in the

company. Operational problem which are arises during production process. As they are directly

related with the production and profitability of the company. In the mean while they are not able

to make the company to achieve there aims and objectives. So in order to overcome above

mentioned financial problems company need to adopt a new techniques which can help them to

overcome these issues.

R.L. Maynard adopts the management accounting system for the purpose of finding out

the financial problem occur within the workplace that are as below-

(Sources: Mark P. Holtzman, 2013)

TASK 4

P5 Comparison how organisation and how they respond to financial problems

In an organisation there are various financial issues which are associated with

management and controlling of financial transaction which are done on regular basis. The

company are facing problem of inventory controlling because they do not have any kind of

software which they can used to manage there daily stocks. Other other related with regulation of

cash and investment that are done by various investors before making any planning in the

company. Operational problem which are arises during production process. As they are directly

related with the production and profitability of the company. In the mean while they are not able

to make the company to achieve there aims and objectives. So in order to overcome above

mentioned financial problems company need to adopt a new techniques which can help them to

overcome these issues.

R.L. Maynard adopts the management accounting system for the purpose of finding out

the financial problem occur within the workplace that are as below-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.