Management Accounting Report: Costing, Planning and Analysis

VerifiedAdded on 2020/11/12

|19

|5192

|413

Report

AI Summary

This report delves into the core concepts of management accounting, exploring various systems, and their reporting requirements. It examines costing methods, specifically marginal and absorption costing, calculating net profit and highlighting their differences. The report also analyzes planning tools, such as budgetary control, discussing their advantages and disadvantages. Furthermore, it addresses financial problem-solving by adapting management accounting systems and critically evaluating data collected from income statements. The report covers topics like planning, organizing, decision making, and controlling, emphasizing the importance of managerial reports for internal decision-making and financial analysis. It also reviews inventory management systems and costing systems like actual costing and standard costing, and how they can be applied to various scenarios to reduce costs and improve efficiency. The report provides a comprehensive overview of management accounting principles and their practical applications within organizations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting concept and related requirements of different types of system....1

D1: Critical evaluation of accounting system reporting.............................................................4

M1: Benefits of management accounting system.......................................................................4

P2: Various types of methods used in management accounting reports.....................................4

TASK 2:...........................................................................................................................................6

P3: Calculate net profit using marginal and absorption costing and explain difference between

these two management technique................................................................................................6

M2 Various types of management accounting techniques..........................................................1

D2: Critically analyse the data collected from the Income statements.......................................1

TASK 3:...........................................................................................................................................1

P4: Advantages and Disadvantages of various planning tools used for budgetary control........1

M3 Analysis of use planning tools..............................................................................................4

D3: Critical evaluation to reduce the financial issues of the company.......................................4

TASK 4............................................................................................................................................4

P5: Responding to financial problems by adapting management accounting systems...............4

M4: Analysis of financial problems............................................................................................5

CONCLUSION................................................................................................................................5

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting concept and related requirements of different types of system....1

D1: Critical evaluation of accounting system reporting.............................................................4

M1: Benefits of management accounting system.......................................................................4

P2: Various types of methods used in management accounting reports.....................................4

TASK 2:...........................................................................................................................................6

P3: Calculate net profit using marginal and absorption costing and explain difference between

these two management technique................................................................................................6

M2 Various types of management accounting techniques..........................................................1

D2: Critically analyse the data collected from the Income statements.......................................1

TASK 3:...........................................................................................................................................1

P4: Advantages and Disadvantages of various planning tools used for budgetary control........1

M3 Analysis of use planning tools..............................................................................................4

D3: Critical evaluation to reduce the financial issues of the company.......................................4

TASK 4............................................................................................................................................4

P5: Responding to financial problems by adapting management accounting systems...............4

M4: Analysis of financial problems............................................................................................5

CONCLUSION................................................................................................................................5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is the process that is undertaken by the accountants of the company for the

purpose of recording, classifying, summarising , analysing and interpreting the transactions of

the business. Accounting also deals with preparations of the financial statements of the company

such as statement of profit and loss account, balance sheet, and cash flow statements. This part of

accounting is called financial accounting. In the modern era, the accounting has been divided

under two major heads which is financial accounting and management accounting (Yeshmin, and

Fowzia, 2010) Management accounting is the form of accounting which is done for the internal

management of the company so that they can make efficient decision for the operations of the

company. Management accounting plays an important role in the organisations like “Rowlinson

Knitwear” in the modern world. This project report deals with the discussion regarding

managerial accounting and various systems of accounting and their reporting systems. The

discussion regarding various costing systems of accounting such as marginal and absorption

costing has also been performed here with the practical examples. The role of budgets as

planning tool for controlling the performances and operations of company has been undertaken.

TASK 1

P1: Explain management accounting and give the essential requirements of different types of

management accounting system

In modern world, management accounting plays a significant role because it provides the

managers of the company with the relevant information which assists them in formulation of

policies of company. Managerial accounting is the process of summarising the information

contained in the financial statements of the company and also the other relevant information that

is contained in the footnotes of those statements. ( Nakajima, 2010)The managerial accounting

information also includes the future economic and non-economic policies of the country that is

going to be prevalent in the coming period. The managers of the company use these managerial

reports made by the accountants and then make the policies of the company for making the

objectives and policies of the company so that the future economic condition that will be

prevalent in the economy does not hinder the operations of the organisation. The significant

accounting systems are as follows:

1

Accounting is the process that is undertaken by the accountants of the company for the

purpose of recording, classifying, summarising , analysing and interpreting the transactions of

the business. Accounting also deals with preparations of the financial statements of the company

such as statement of profit and loss account, balance sheet, and cash flow statements. This part of

accounting is called financial accounting. In the modern era, the accounting has been divided

under two major heads which is financial accounting and management accounting (Yeshmin, and

Fowzia, 2010) Management accounting is the form of accounting which is done for the internal

management of the company so that they can make efficient decision for the operations of the

company. Management accounting plays an important role in the organisations like “Rowlinson

Knitwear” in the modern world. This project report deals with the discussion regarding

managerial accounting and various systems of accounting and their reporting systems. The

discussion regarding various costing systems of accounting such as marginal and absorption

costing has also been performed here with the practical examples. The role of budgets as

planning tool for controlling the performances and operations of company has been undertaken.

TASK 1

P1: Explain management accounting and give the essential requirements of different types of

management accounting system

In modern world, management accounting plays a significant role because it provides the

managers of the company with the relevant information which assists them in formulation of

policies of company. Managerial accounting is the process of summarising the information

contained in the financial statements of the company and also the other relevant information that

is contained in the footnotes of those statements. ( Nakajima, 2010)The managerial accounting

information also includes the future economic and non-economic policies of the country that is

going to be prevalent in the coming period. The managers of the company use these managerial

reports made by the accountants and then make the policies of the company for making the

objectives and policies of the company so that the future economic condition that will be

prevalent in the economy does not hinder the operations of the organisation. The significant

accounting systems are as follows:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Planning: Planning process is undertaken by every company in order to achieve the

targets and objectives of the company in an efficient manner. Planning is done for the

achievements of both long term and short term objectives of the company. The managerial

accounting process assists the managers of the company in setting objectives and formulating

policies according to the requirements of the company and as per the external environment.

Organising: This tool deals with the management of the employees and other people of

the organization according to a well-defined framework that is formulated by the managers. In

this process the managers define the role and responsibilities of personnels and different

departments of the organisation.

Decision making: The main purpose behind managerial accounting reports is to assist

the management of the company in the process of decision making. Managerial reports provide

the internal management with the relevant information regarding the financial health of the

company and also about the external economic environment which may impact the functioning

of the business so that they can make decisions by using these trends.

Controlling: In this process the budgets and performance standards are used to measure

the performances of the individual employees and the whole departments so that the managers

can take corrective actions if necessary on the persons which are not working according to pre-

defined standards. These budgets and performance standards are created by the managers using

the managerial accounting reports.

Various costing systems:

Actual costing: According to this costing system, accountants considers the

measurement of actual expenditure that is occurred in the process of production and other

operations of the company. In this method of costing, the actual cost related to all the job

activities are taken into consideration such as direct material cost, labour cost and other

production overheads. ( Victoravich, 2010)

Standard costing: In this costing process, the estimation of the standard cost is

determined that should be incurred in the process of production that will be done in the future.

The department heads then have to consider these standards for incurring expenses, if the cost

goes higher then these set standards then the managers are held responsible for that.

Inventory management system: this system is undertaken by the managers of the company for

the purpose of solving the issues related to the management of the inventory. This system assists

2

targets and objectives of the company in an efficient manner. Planning is done for the

achievements of both long term and short term objectives of the company. The managerial

accounting process assists the managers of the company in setting objectives and formulating

policies according to the requirements of the company and as per the external environment.

Organising: This tool deals with the management of the employees and other people of

the organization according to a well-defined framework that is formulated by the managers. In

this process the managers define the role and responsibilities of personnels and different

departments of the organisation.

Decision making: The main purpose behind managerial accounting reports is to assist

the management of the company in the process of decision making. Managerial reports provide

the internal management with the relevant information regarding the financial health of the

company and also about the external economic environment which may impact the functioning

of the business so that they can make decisions by using these trends.

Controlling: In this process the budgets and performance standards are used to measure

the performances of the individual employees and the whole departments so that the managers

can take corrective actions if necessary on the persons which are not working according to pre-

defined standards. These budgets and performance standards are created by the managers using

the managerial accounting reports.

Various costing systems:

Actual costing: According to this costing system, accountants considers the

measurement of actual expenditure that is occurred in the process of production and other

operations of the company. In this method of costing, the actual cost related to all the job

activities are taken into consideration such as direct material cost, labour cost and other

production overheads. ( Victoravich, 2010)

Standard costing: In this costing process, the estimation of the standard cost is

determined that should be incurred in the process of production that will be done in the future.

The department heads then have to consider these standards for incurring expenses, if the cost

goes higher then these set standards then the managers are held responsible for that.

Inventory management system: this system is undertaken by the managers of the company for

the purpose of solving the issues related to the management of the inventory. This system assists

2

the company in maintaining optimum stocks of raw material and finished goods such that there is

hindrance occurred in the process of production as well as the demands of the consumers are met

in an efficient way. There are various inventory management systems that are adopted by the

organisations for efficient management of inventory, these are discussed as under in brief:

FIFO: This techniques of inventory management means First in first out. According to

this system, the inventories which came into the stocks of the companies are supposed to be sold

first and the rest of unsold inventory is transferred into the closing stock of the company. In this

the COGS represents those goods which were purchased first, and closing inventory includes

goods which were purchased later.

LIFO: In this inventory management system, the goods that were purchased in the end

by the company are sold or utilised firstly. The full form of LIFO is last in first out which

interprets its procedure. In this method, COGS represents the goods which were manufactured

recently by the company and earlier purchased goods goes into closing inventory.

Weighted average cost method: Under this method of inventory management, the

weighted average cost of all the purchased goods that is in the inventory of the company is find

out using a formula, which equates the prices of all the goods that is existing in the stocks of the

company and then the goods are transferred into COGS and closing inventory. Under this

method the price of inventory is same in cost of goods sold and the ending inventory of the

company.

Job costing system: this system represents and allocates the cost of production of for a specific

product or the cost related to particular job. This system of job costing takes into consideration

the cost of direct labour and direct material that is incurred in the process of producing that

product or cost related to a specific job. The managers of the company determines the earnings

that the company can earn from a job and accordingly the management decides the expenditure

that can be incurred in the process.(Abdel-Kader, 2011)

Batch costing: this kind of costing considers the cost that in incurred in producing a

particular batch of products.

Contract costing: this costing process involves that cost which is incurred in the specific

contracts undertaken by the company.

3

hindrance occurred in the process of production as well as the demands of the consumers are met

in an efficient way. There are various inventory management systems that are adopted by the

organisations for efficient management of inventory, these are discussed as under in brief:

FIFO: This techniques of inventory management means First in first out. According to

this system, the inventories which came into the stocks of the companies are supposed to be sold

first and the rest of unsold inventory is transferred into the closing stock of the company. In this

the COGS represents those goods which were purchased first, and closing inventory includes

goods which were purchased later.

LIFO: In this inventory management system, the goods that were purchased in the end

by the company are sold or utilised firstly. The full form of LIFO is last in first out which

interprets its procedure. In this method, COGS represents the goods which were manufactured

recently by the company and earlier purchased goods goes into closing inventory.

Weighted average cost method: Under this method of inventory management, the

weighted average cost of all the purchased goods that is in the inventory of the company is find

out using a formula, which equates the prices of all the goods that is existing in the stocks of the

company and then the goods are transferred into COGS and closing inventory. Under this

method the price of inventory is same in cost of goods sold and the ending inventory of the

company.

Job costing system: this system represents and allocates the cost of production of for a specific

product or the cost related to particular job. This system of job costing takes into consideration

the cost of direct labour and direct material that is incurred in the process of producing that

product or cost related to a specific job. The managers of the company determines the earnings

that the company can earn from a job and accordingly the management decides the expenditure

that can be incurred in the process.(Abdel-Kader, 2011)

Batch costing: this kind of costing considers the cost that in incurred in producing a

particular batch of products.

Contract costing: this costing process involves that cost which is incurred in the specific

contracts undertaken by the company.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Normal costing: This costing process is used to in deciding the cost of production of

goods. In this the cost of material, cost of labour and other production overheads are prices

according to the pre-determined rates that were decided at the initial stage of accounting year.

D1: Critical evaluation of accounting system reporting

As per the above, accounting reports this has been examined that it plays an crucial role

in incurring the maximum outcomes of the business. The main purpose behind this is to achieve

all the objectives and targets that are being set by the company. According to this the

performance reports will be evaluated in more efficient manner.

M1: Benefits of management accounting system

The managerial accounting process helps the internal management of the company in the

formulation of policies and setting the objectives of the business by using the information that is

de scripted in the reports made by the accountants. The certain benefit of management

accounting report is determining the aims and objectives that are to be achieved by the

organisation in the upcoming period. Reducing the cost of production and increasing the

efficiency of the organisation is the primary motive of any finance manager. Every accounting

system is valuable and have their own benefits in the organisation. To increase the profitability

of the company, cost accounting system is effectively used. (Smith, 2017)

P2: Explain different methods used for management accounting reporting

The managerial reports made by the accountants of the company records every

transaction whether it is non financial or financial are included in these reports. The managerial

reports also involve all the future economic and non-economic policies that will be prevalent in

the economy which will affect the functioning of the business. Because of these reasons there is

a significant importance of managerial reports for improving the operations of the company.

These reports are discussed as below:

Budget reports: Every company prepares budgets whether it is big or small. The budgets

are prepared for every department and for every function of the company. These budgets assist

the company in estimating the total cost that will be incurred in the operations and also helps in

setting the performance standards for the employees and each department. Therefore, these

reports also help the stakeholders of the company in checking the future scenario regarding the

functioning of the business.

4

goods. In this the cost of material, cost of labour and other production overheads are prices

according to the pre-determined rates that were decided at the initial stage of accounting year.

D1: Critical evaluation of accounting system reporting

As per the above, accounting reports this has been examined that it plays an crucial role

in incurring the maximum outcomes of the business. The main purpose behind this is to achieve

all the objectives and targets that are being set by the company. According to this the

performance reports will be evaluated in more efficient manner.

M1: Benefits of management accounting system

The managerial accounting process helps the internal management of the company in the

formulation of policies and setting the objectives of the business by using the information that is

de scripted in the reports made by the accountants. The certain benefit of management

accounting report is determining the aims and objectives that are to be achieved by the

organisation in the upcoming period. Reducing the cost of production and increasing the

efficiency of the organisation is the primary motive of any finance manager. Every accounting

system is valuable and have their own benefits in the organisation. To increase the profitability

of the company, cost accounting system is effectively used. (Smith, 2017)

P2: Explain different methods used for management accounting reporting

The managerial reports made by the accountants of the company records every

transaction whether it is non financial or financial are included in these reports. The managerial

reports also involve all the future economic and non-economic policies that will be prevalent in

the economy which will affect the functioning of the business. Because of these reasons there is

a significant importance of managerial reports for improving the operations of the company.

These reports are discussed as below:

Budget reports: Every company prepares budgets whether it is big or small. The budgets

are prepared for every department and for every function of the company. These budgets assist

the company in estimating the total cost that will be incurred in the operations and also helps in

setting the performance standards for the employees and each department. Therefore, these

reports also help the stakeholders of the company in checking the future scenario regarding the

functioning of the business.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Accounts receivable report: the AR report makes an analysis regarding the total account

receivables that the company currently have in the balance sheet. This report measures the

amount of debtors from the company has to receive the payments and when the amount is due to

be received. These report also tells about the bad and doubtful debts of the company from which

the receiving of payments are uncertain. With the help of the AR report company losens or

tightens it collection period policy.

Job cost reports: The job cost reports provides the information to the management

regarding the total revenues that is generated from production of batch of product or specific

product. The report tells about the the revenues or profits that is generated by undertaking a

specific product or job function and accordingly how much cost is incurred in that process. This

helps the managers of the company in choosing those products or job functions which provide

maximum profits to the company. (Harris, and Durden, 2012)

Significance of details of management accounting reports:

Increased financial returns: These reports of management accounting provides details

about the financial statements of the company and also about the future economic polices that

will be prevalent in economy, which helps the managers in the formulation of the budgets for

analysing and interpreting the projects that are more profitable for the company. Such projects

increase the overall revenues of the company and also increases the wealth of shareholders.

Cost reduction: The managerial reports prepared by the company provide guidance to

the managers in the prediction of the issues that can faced by the company in the future period.

The management identifies and eliminate these issues by using the managerial reports which in

turn reduces the cost of the operations in the future period.

5

receivables that the company currently have in the balance sheet. This report measures the

amount of debtors from the company has to receive the payments and when the amount is due to

be received. These report also tells about the bad and doubtful debts of the company from which

the receiving of payments are uncertain. With the help of the AR report company losens or

tightens it collection period policy.

Job cost reports: The job cost reports provides the information to the management

regarding the total revenues that is generated from production of batch of product or specific

product. The report tells about the the revenues or profits that is generated by undertaking a

specific product or job function and accordingly how much cost is incurred in that process. This

helps the managers of the company in choosing those products or job functions which provide

maximum profits to the company. (Harris, and Durden, 2012)

Significance of details of management accounting reports:

Increased financial returns: These reports of management accounting provides details

about the financial statements of the company and also about the future economic polices that

will be prevalent in economy, which helps the managers in the formulation of the budgets for

analysing and interpreting the projects that are more profitable for the company. Such projects

increase the overall revenues of the company and also increases the wealth of shareholders.

Cost reduction: The managerial reports prepared by the company provide guidance to

the managers in the prediction of the issues that can faced by the company in the future period.

The management identifies and eliminate these issues by using the managerial reports which in

turn reduces the cost of the operations in the future period.

5

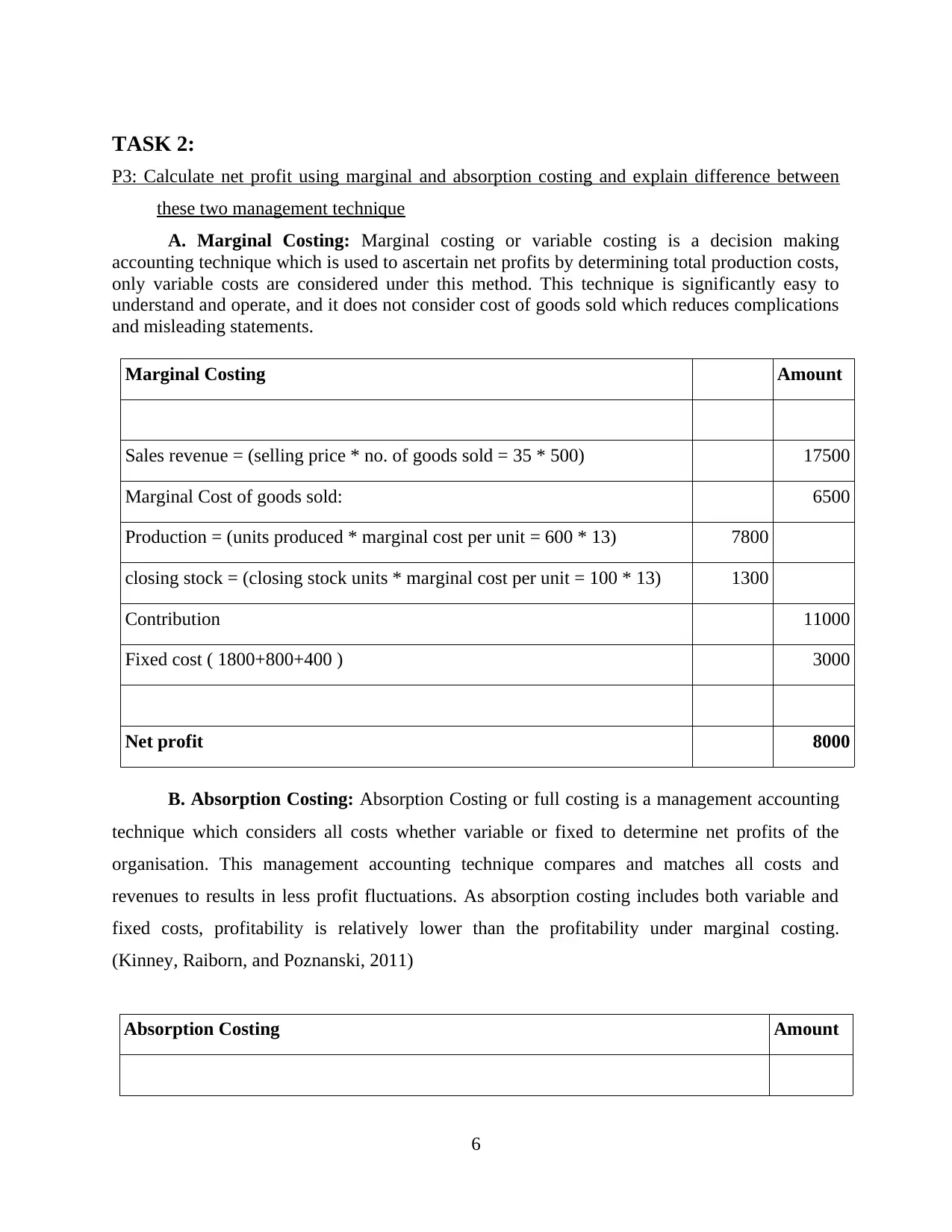

TASK 2:

P3: Calculate net profit using marginal and absorption costing and explain difference between

these two management technique

A. Marginal Costing: Marginal costing or variable costing is a decision making

accounting technique which is used to ascertain net profits by determining total production costs,

only variable costs are considered under this method. This technique is significantly easy to

understand and operate, and it does not consider cost of goods sold which reduces complications

and misleading statements.

Marginal Costing Amount

Sales revenue = (selling price * no. of goods sold = 35 * 500) 17500

Marginal Cost of goods sold: 6500

Production = (units produced * marginal cost per unit = 600 * 13) 7800

closing stock = (closing stock units * marginal cost per unit = 100 * 13) 1300

Contribution 11000

Fixed cost ( 1800+800+400 ) 3000

Net profit 8000

B. Absorption Costing: Absorption Costing or full costing is a management accounting

technique which considers all costs whether variable or fixed to determine net profits of the

organisation. This management accounting technique compares and matches all costs and

revenues to results in less profit fluctuations. As absorption costing includes both variable and

fixed costs, profitability is relatively lower than the profitability under marginal costing.

(Kinney, Raiborn, and Poznanski, 2011)

Absorption Costing Amount

6

P3: Calculate net profit using marginal and absorption costing and explain difference between

these two management technique

A. Marginal Costing: Marginal costing or variable costing is a decision making

accounting technique which is used to ascertain net profits by determining total production costs,

only variable costs are considered under this method. This technique is significantly easy to

understand and operate, and it does not consider cost of goods sold which reduces complications

and misleading statements.

Marginal Costing Amount

Sales revenue = (selling price * no. of goods sold = 35 * 500) 17500

Marginal Cost of goods sold: 6500

Production = (units produced * marginal cost per unit = 600 * 13) 7800

closing stock = (closing stock units * marginal cost per unit = 100 * 13) 1300

Contribution 11000

Fixed cost ( 1800+800+400 ) 3000

Net profit 8000

B. Absorption Costing: Absorption Costing or full costing is a management accounting

technique which considers all costs whether variable or fixed to determine net profits of the

organisation. This management accounting technique compares and matches all costs and

revenues to results in less profit fluctuations. As absorption costing includes both variable and

fixed costs, profitability is relatively lower than the profitability under marginal costing.

(Kinney, Raiborn, and Poznanski, 2011)

Absorption Costing Amount

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

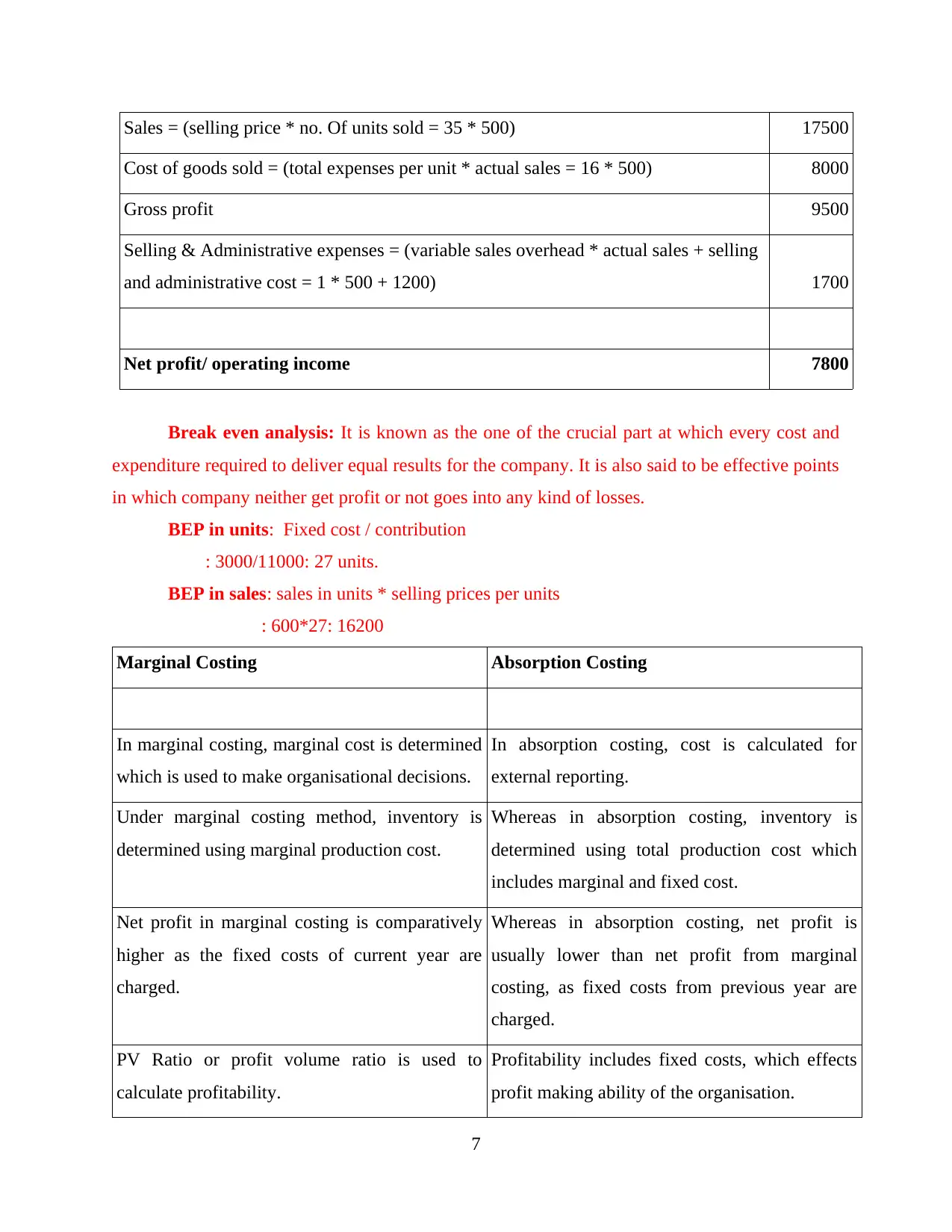

Sales = (selling price * no. Of units sold = 35 * 500) 17500

Cost of goods sold = (total expenses per unit * actual sales = 16 * 500) 8000

Gross profit 9500

Selling & Administrative expenses = (variable sales overhead * actual sales + selling

and administrative cost = 1 * 500 + 1200) 1700

Net profit/ operating income 7800

Break even analysis: It is known as the one of the crucial part at which every cost and

expenditure required to deliver equal results for the company. It is also said to be effective points

in which company neither get profit or not goes into any kind of losses.

BEP in units: Fixed cost / contribution

: 3000/11000: 27 units.

BEP in sales: sales in units * selling prices per units

: 600*27: 16200

Marginal Costing Absorption Costing

In marginal costing, marginal cost is determined

which is used to make organisational decisions.

In absorption costing, cost is calculated for

external reporting.

Under marginal costing method, inventory is

determined using marginal production cost.

Whereas in absorption costing, inventory is

determined using total production cost which

includes marginal and fixed cost.

Net profit in marginal costing is comparatively

higher as the fixed costs of current year are

charged.

Whereas in absorption costing, net profit is

usually lower than net profit from marginal

costing, as fixed costs from previous year are

charged.

PV Ratio or profit volume ratio is used to

calculate profitability.

Profitability includes fixed costs, which effects

profit making ability of the organisation.

7

Cost of goods sold = (total expenses per unit * actual sales = 16 * 500) 8000

Gross profit 9500

Selling & Administrative expenses = (variable sales overhead * actual sales + selling

and administrative cost = 1 * 500 + 1200) 1700

Net profit/ operating income 7800

Break even analysis: It is known as the one of the crucial part at which every cost and

expenditure required to deliver equal results for the company. It is also said to be effective points

in which company neither get profit or not goes into any kind of losses.

BEP in units: Fixed cost / contribution

: 3000/11000: 27 units.

BEP in sales: sales in units * selling prices per units

: 600*27: 16200

Marginal Costing Absorption Costing

In marginal costing, marginal cost is determined

which is used to make organisational decisions.

In absorption costing, cost is calculated for

external reporting.

Under marginal costing method, inventory is

determined using marginal production cost.

Whereas in absorption costing, inventory is

determined using total production cost which

includes marginal and fixed cost.

Net profit in marginal costing is comparatively

higher as the fixed costs of current year are

charged.

Whereas in absorption costing, net profit is

usually lower than net profit from marginal

costing, as fixed costs from previous year are

charged.

PV Ratio or profit volume ratio is used to

calculate profitability.

Profitability includes fixed costs, which effects

profit making ability of the organisation.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

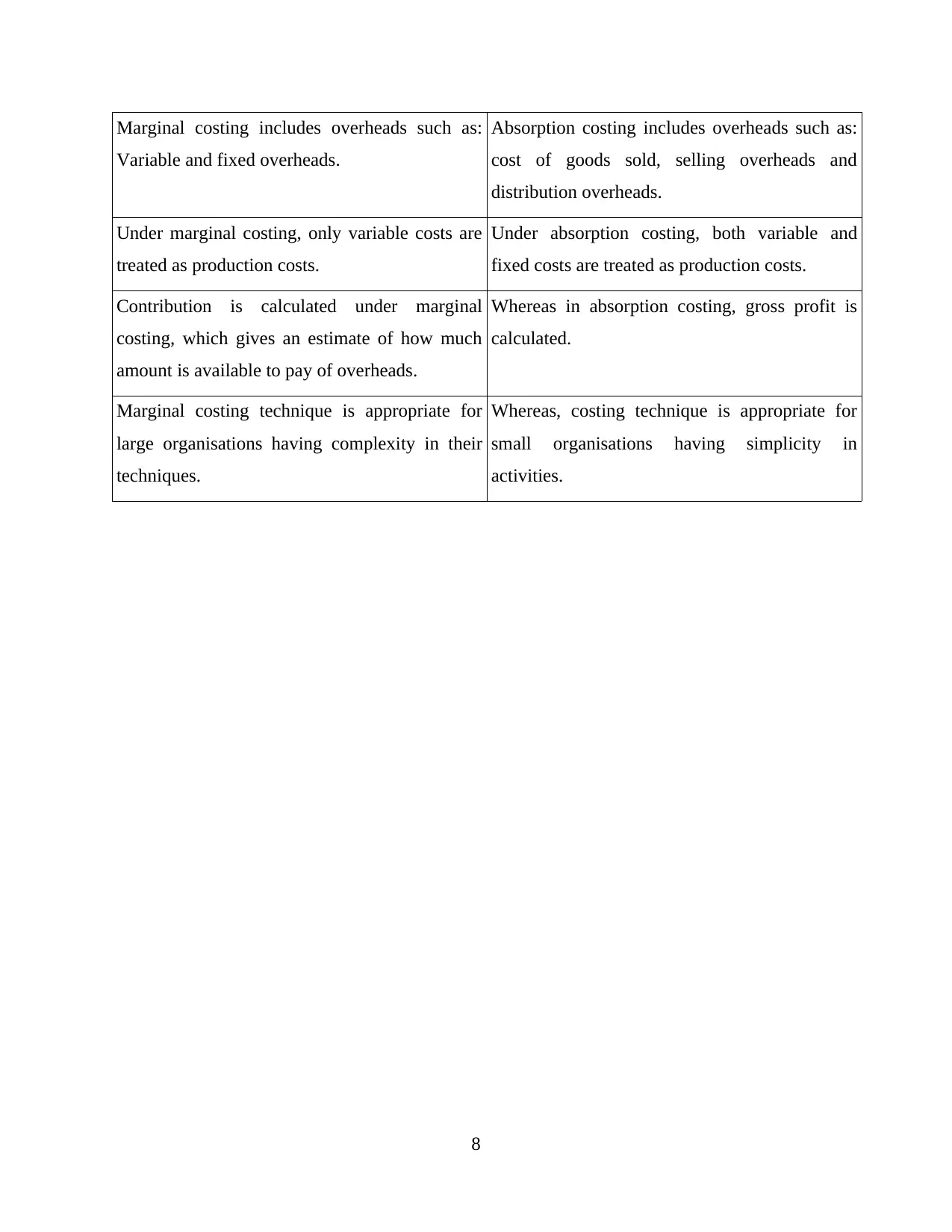

Marginal costing includes overheads such as:

Variable and fixed overheads.

Absorption costing includes overheads such as:

cost of goods sold, selling overheads and

distribution overheads.

Under marginal costing, only variable costs are

treated as production costs.

Under absorption costing, both variable and

fixed costs are treated as production costs.

Contribution is calculated under marginal

costing, which gives an estimate of how much

amount is available to pay of overheads.

Whereas in absorption costing, gross profit is

calculated.

Marginal costing technique is appropriate for

large organisations having complexity in their

techniques.

Whereas, costing technique is appropriate for

small organisations having simplicity in

activities.

8

Variable and fixed overheads.

Absorption costing includes overheads such as:

cost of goods sold, selling overheads and

distribution overheads.

Under marginal costing, only variable costs are

treated as production costs.

Under absorption costing, both variable and

fixed costs are treated as production costs.

Contribution is calculated under marginal

costing, which gives an estimate of how much

amount is available to pay of overheads.

Whereas in absorption costing, gross profit is

calculated.

Marginal costing technique is appropriate for

large organisations having complexity in their

techniques.

Whereas, costing technique is appropriate for

small organisations having simplicity in

activities.

8

M2 Various types of management accounting techniques

There are number of accounting tools and method that must be formulated in corrective

manner so that final results could be accomplished in effective and efficient manner. It is the

responsibility of manager to allocate such management accounting technique so that all resources

that is available with the company in accurate way. The accounting tool delivers the information

that is relevant to measure the performance of company so that corrective actions could be

adopted wherever the improvements are required. Performance measurement is also a important

concept that measures the performance whether it is delivering correct objective or not.( Hülle,

Kaspar, and Möller, 2011)

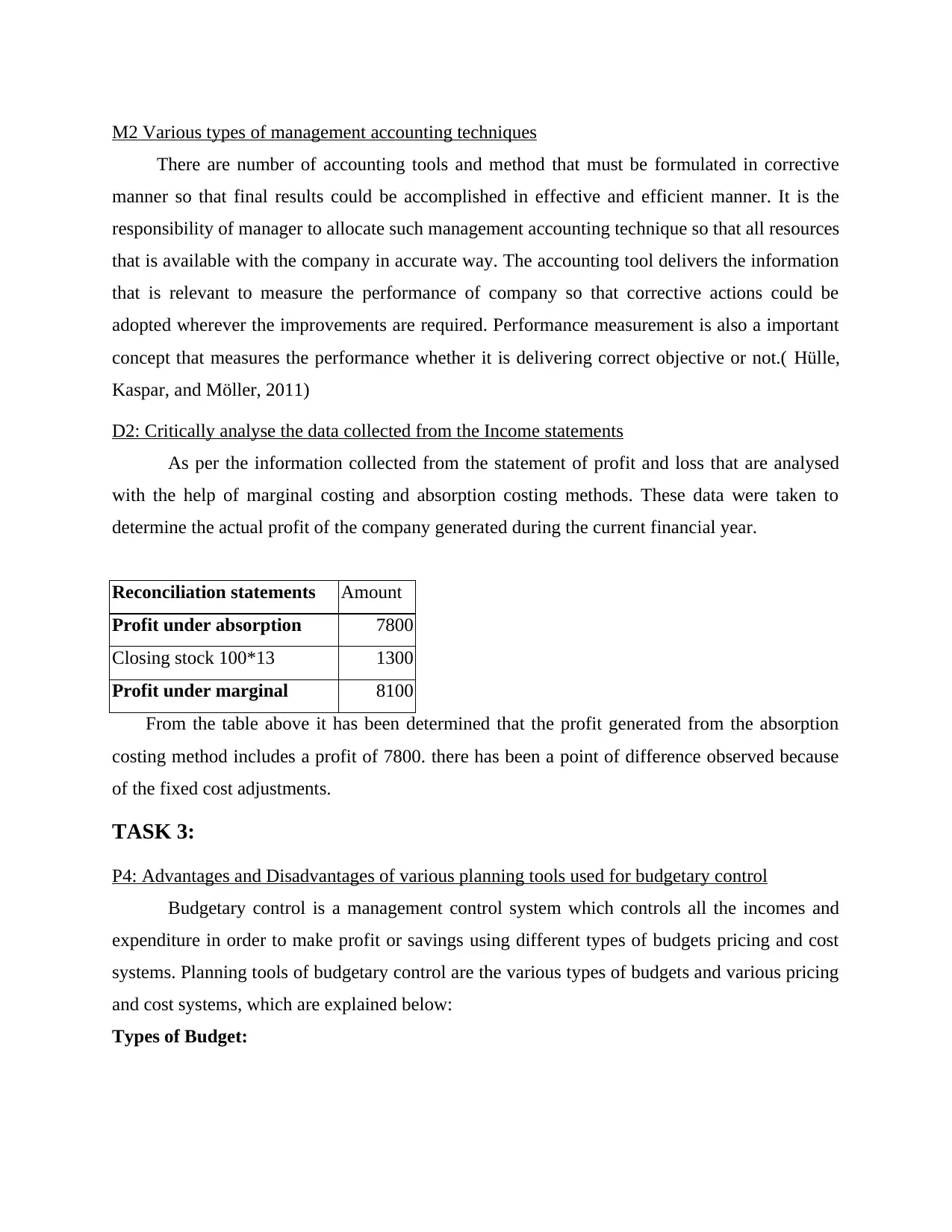

D2: Critically analyse the data collected from the Income statements

As per the information collected from the statement of profit and loss that are analysed

with the help of marginal costing and absorption costing methods. These data were taken to

determine the actual profit of the company generated during the current financial year.

Reconciliation statements Amount

Profit under absorption 7800

Closing stock 100*13 1300

Profit under marginal 8100

From the table above it has been determined that the profit generated from the absorption

costing method includes a profit of 7800. there has been a point of difference observed because

of the fixed cost adjustments.

TASK 3:

P4: Advantages and Disadvantages of various planning tools used for budgetary control

Budgetary control is a management control system which controls all the incomes and

expenditure in order to make profit or savings using different types of budgets pricing and cost

systems. Planning tools of budgetary control are the various types of budgets and various pricing

and cost systems, which are explained below:

Types of Budget:

There are number of accounting tools and method that must be formulated in corrective

manner so that final results could be accomplished in effective and efficient manner. It is the

responsibility of manager to allocate such management accounting technique so that all resources

that is available with the company in accurate way. The accounting tool delivers the information

that is relevant to measure the performance of company so that corrective actions could be

adopted wherever the improvements are required. Performance measurement is also a important

concept that measures the performance whether it is delivering correct objective or not.( Hülle,

Kaspar, and Möller, 2011)

D2: Critically analyse the data collected from the Income statements

As per the information collected from the statement of profit and loss that are analysed

with the help of marginal costing and absorption costing methods. These data were taken to

determine the actual profit of the company generated during the current financial year.

Reconciliation statements Amount

Profit under absorption 7800

Closing stock 100*13 1300

Profit under marginal 8100

From the table above it has been determined that the profit generated from the absorption

costing method includes a profit of 7800. there has been a point of difference observed because

of the fixed cost adjustments.

TASK 3:

P4: Advantages and Disadvantages of various planning tools used for budgetary control

Budgetary control is a management control system which controls all the incomes and

expenditure in order to make profit or savings using different types of budgets pricing and cost

systems. Planning tools of budgetary control are the various types of budgets and various pricing

and cost systems, which are explained below:

Types of Budget:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.