Management Accounting Systems and Techniques Analysis

VerifiedAdded on 2021/02/20

|18

|4759

|40

Report

AI Summary

This report provides a comprehensive overview of management accounting systems and techniques, focusing on their application within the context of ITW Construction Products. It begins with an introduction to management accounting, its role, origin, and principles, differentiating it from financial accounting. The report then delves into various management accounting systems, including job costing, price optimization, cost accounting, and inventory management. It discusses the significance of integrating these systems within a business organization. The report further explores management accounting reports, such as account receivable aging reports, performance reports, and job cost reports, highlighting their importance in decision-making. Additionally, it examines costing techniques used to prepare income statements, including cost-volume-profit analysis, flexible budgeting, and cost variances. The report also covers marginal costing, absorption costing, and cost allocation methods. Finally, the report touches on the advantages and disadvantages of planning tools used for budgetary control and compares how different business entities apply management accounting systems to address financial problems. The conclusion summarizes the key findings, emphasizing the role of management accounting in providing crucial information for managerial decision-making and achieving organizational goals.

Management

Accounting Systems

&

Techniques

Accounting Systems

&

Techniques

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Management Accounting and its systems:...................................................................................4

Management Accounting Reports:..............................................................................................7

TASK 2............................................................................................................................................8

Costing Techniques to prepare income statements:.....................................................................8

TASK 3..........................................................................................................................................16

Advantages and disadvantages of different types of planning tools used for budgetary control:

....................................................................................................................................................16

TASK 4..........................................................................................................................................19

Comparison of business entities applying management accounting systems for responding

different financial problems:.....................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

Management Accounting and its systems:...................................................................................4

Management Accounting Reports:..............................................................................................7

TASK 2............................................................................................................................................8

Costing Techniques to prepare income statements:.....................................................................8

TASK 3..........................................................................................................................................16

Advantages and disadvantages of different types of planning tools used for budgetary control:

....................................................................................................................................................16

TASK 4..........................................................................................................................................19

Comparison of business entities applying management accounting systems for responding

different financial problems:.....................................................................................................19

CONCLUSION..............................................................................................................................20

REFERENCES..............................................................................................................................22

INTRODUCTION

In current business environment, every business entities want to establish a structure to

develop a source of information for managerial decision-making. Management accounting is

only a way that provides a systematic way to create structure within business entity, because it

contains functions and task directly related to providing information for taking vital decisions

(Bagautdinova, Kundakchyan and Malakhov, 2013). In this context a consultancy firm named

Alfa consultancy company. Report contains an exhaustive definition along with different aspects

like role, origin etc. of management accounting, clear distinction between financial accounting

and management accounting and, presentation of financial information under management

accounting reporting and systems in context of client company ITW Construction Products. It is

UK's manufacturing company engaged in manufacturing of fixing, fastening and drilling systems

for wood, steel and concrete applications. This report also includes pricing strategies, PEST

analysis, SWOT analysis and other different kind of reports of management accounting.

TASK 1

Management Accounting and its systems:

Management Accounting: Management accounting is the process in which the financial

information is utilised by the management in systematic manner in order to achieve financial as

well as operational goals (Collis and Hussey, 2017). Management Accounting comprises of all

technical aspects of financial accounting and cost accounting which assists management with

constructive data set which helps the ITW Construction Product's management in formulating

financial and operational policies which further provides the management with a strong set of

parameters to build robust decision-making systems. Under the aegis of management accounting,

accounting information is utilised judiciously by the management to improve the continuous

financial health of the organisation and devising further measures to minimise losses.

Management Accounting System: Management accounting systems refers to systematised use

of accounting information to achieve targeted goals in harmony with the organisational policies.

There are various management accounting systems which works in unison to integrate the

overall managerial processes which attributes to the substantial framework of policy making like

cost accounting, inventory management etc.

Significance of integration of systems within business organisation:

In current business environment, every business entities want to establish a structure to

develop a source of information for managerial decision-making. Management accounting is

only a way that provides a systematic way to create structure within business entity, because it

contains functions and task directly related to providing information for taking vital decisions

(Bagautdinova, Kundakchyan and Malakhov, 2013). In this context a consultancy firm named

Alfa consultancy company. Report contains an exhaustive definition along with different aspects

like role, origin etc. of management accounting, clear distinction between financial accounting

and management accounting and, presentation of financial information under management

accounting reporting and systems in context of client company ITW Construction Products. It is

UK's manufacturing company engaged in manufacturing of fixing, fastening and drilling systems

for wood, steel and concrete applications. This report also includes pricing strategies, PEST

analysis, SWOT analysis and other different kind of reports of management accounting.

TASK 1

Management Accounting and its systems:

Management Accounting: Management accounting is the process in which the financial

information is utilised by the management in systematic manner in order to achieve financial as

well as operational goals (Collis and Hussey, 2017). Management Accounting comprises of all

technical aspects of financial accounting and cost accounting which assists management with

constructive data set which helps the ITW Construction Product's management in formulating

financial and operational policies which further provides the management with a strong set of

parameters to build robust decision-making systems. Under the aegis of management accounting,

accounting information is utilised judiciously by the management to improve the continuous

financial health of the organisation and devising further measures to minimise losses.

Management Accounting System: Management accounting systems refers to systematised use

of accounting information to achieve targeted goals in harmony with the organisational policies.

There are various management accounting systems which works in unison to integrate the

overall managerial processes which attributes to the substantial framework of policy making like

cost accounting, inventory management etc.

Significance of integration of systems within business organisation:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Efficiency and effectiveness in organisational functions is main aim of ITW Construction

Products, so managerial person always tries to integrate systems like inventory management, cost

accounting, price optimisation etc. with numerous activities of company. Such systems act as a

framework for business enterprise to run their business tasks smoothly (Demski, 2013). For

example company has integrated inventory management system with inventory process which

assist them in optimising expenses of inventory handling, warehouse expenses, storage expenses

etc.

Role, Origin and principle of management accounting:

There are no common view about management accounting's origin. The term

Management Accounting is initially used in approx 1959s. It is also considered as cost

accounting but afterwards management accounting becomes a filed of accounting (Management

Accounting. 2019). In business context it play role in safeguarding of financial resources of

business enterprise. It assist managers in quick and effective accomplishment of task of decision-

making. Following are some significant management accounting principles:

Influence:

Management accounting require to generate

informations that can persuasion potential

decisions.

Relevance:

Information must be consistent and applicable

or usable for different users.

Values:

Functions of management accounting

required to be combine an analysis which

exhibits effect on values determined by

business organisation (Thomas, 2016).

Trust:

Information generated from reporting of result

of management accounting system require to

be reliable and with a motive to develop trust

in individual.

Differences: Financial Accounting v/s Management Accounting:

Management Accounting Financial Accounting

Main objective of adopting of management

accounting is to circulate compatible

information for managerial and business

decisions.

Financial Accounting is adopted by entities to

communicate performance of company to

various interested parties and stakeholders.

Products, so managerial person always tries to integrate systems like inventory management, cost

accounting, price optimisation etc. with numerous activities of company. Such systems act as a

framework for business enterprise to run their business tasks smoothly (Demski, 2013). For

example company has integrated inventory management system with inventory process which

assist them in optimising expenses of inventory handling, warehouse expenses, storage expenses

etc.

Role, Origin and principle of management accounting:

There are no common view about management accounting's origin. The term

Management Accounting is initially used in approx 1959s. It is also considered as cost

accounting but afterwards management accounting becomes a filed of accounting (Management

Accounting. 2019). In business context it play role in safeguarding of financial resources of

business enterprise. It assist managers in quick and effective accomplishment of task of decision-

making. Following are some significant management accounting principles:

Influence:

Management accounting require to generate

informations that can persuasion potential

decisions.

Relevance:

Information must be consistent and applicable

or usable for different users.

Values:

Functions of management accounting

required to be combine an analysis which

exhibits effect on values determined by

business organisation (Thomas, 2016).

Trust:

Information generated from reporting of result

of management accounting system require to

be reliable and with a motive to develop trust

in individual.

Differences: Financial Accounting v/s Management Accounting:

Management Accounting Financial Accounting

Main objective of adopting of management

accounting is to circulate compatible

information for managerial and business

decisions.

Financial Accounting is adopted by entities to

communicate performance of company to

various interested parties and stakeholders.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

No legal or statutory requirement for adoption. In almost all countries financial accounting is

statutory requirement.

Qualitative and Numerical facts and elements

are considered in management accounting.

It emphasises on numerical figures and fact

only.

Type of management accounting systems:

Job costing system

The job costing system is the method of accumulating cost information associated with specific

service or production job. Job costing helps in determining manufacturing costs in a systematic

manner by dividing them under direct material, direct labour and overhead costs by individually

estimating them at their actual costs (Kanellou and Spathis, 2013). Manufacturing firms such as

ITW Construction Products use job costing method to regulate the use of raw materials, labour

hours and equipments by allocation of cost to every customer order separately. Job costing

method is useful for the firms who manufacture goods and services based on customer

specifications or in distinguished batches.

Price optimising system

Price optimisation system is a quantitative tool used by businesses in determining prices for

various products at a given period of time. It helps the management in ascertaining as to how the

demand will fluctuate at various levels and how demand function will behave at various

channels. It is a system of behavioural modelling of potential customers through using specific

data sets , these data sets results into a set of big data for the firms to manipulate the information

for devising price optimisation models for various price levels i.e. initial pricing, promotional

pricing & concessional pricing in ITW Construction Products.

Cost accounting system

A cost accounting system comprises of cost accounting models which are used by businesses to

ascertain the actual cost of their products which aids the organisation in profitability analysis,

stock valuation and cost control. Estimation of correct costs of each and every product is of great

importance to an organisation in order to determine which products are profit making and which

one's are loss making. It is a process of examining the forward flow of goods through each stage

of production namely from raw material stage to passing through production line in batches to

statutory requirement.

Qualitative and Numerical facts and elements

are considered in management accounting.

It emphasises on numerical figures and fact

only.

Type of management accounting systems:

Job costing system

The job costing system is the method of accumulating cost information associated with specific

service or production job. Job costing helps in determining manufacturing costs in a systematic

manner by dividing them under direct material, direct labour and overhead costs by individually

estimating them at their actual costs (Kanellou and Spathis, 2013). Manufacturing firms such as

ITW Construction Products use job costing method to regulate the use of raw materials, labour

hours and equipments by allocation of cost to every customer order separately. Job costing

method is useful for the firms who manufacture goods and services based on customer

specifications or in distinguished batches.

Price optimising system

Price optimisation system is a quantitative tool used by businesses in determining prices for

various products at a given period of time. It helps the management in ascertaining as to how the

demand will fluctuate at various levels and how demand function will behave at various

channels. It is a system of behavioural modelling of potential customers through using specific

data sets , these data sets results into a set of big data for the firms to manipulate the information

for devising price optimisation models for various price levels i.e. initial pricing, promotional

pricing & concessional pricing in ITW Construction Products.

Cost accounting system

A cost accounting system comprises of cost accounting models which are used by businesses to

ascertain the actual cost of their products which aids the organisation in profitability analysis,

stock valuation and cost control. Estimation of correct costs of each and every product is of great

importance to an organisation in order to determine which products are profit making and which

one's are loss making. It is a process of examining the forward flow of goods through each stage

of production namely from raw material stage to passing through production line in batches to

finally converting into finished goods. Under the system when raw materials are put to process

the system credits the raw materials account and debits the goods in process account in ITW

Construction Products.

Inventory management system

Inventory management system combines technology with processes and procedures to ensure the

availability of inventory which consists of raw materials, goods in process and finished goods to

further ensure their availability at all times with the right quality (Bloomfield, 2015). It is often

used at manufacturing firms such as ITW Construction Products, and other concerns by using

asset tags to control the inflow of raw materials and outflow of finished goods as well as

maintaining requisite amount of goods at all times to ensure timely delivery to the clients.

Furthermore, it helps in determining future order requirements in advance which helps in smooth

flow of work processes.

Presentation of financial information:

While applying management accounting systems, main focus of business organisation is

on generation of informations that are reliable, complete, having relevance of various users and

must be accurate. As such kind of information is essential for managers to gain understanding of

facts and data which help in taking strategic decisions. Such information provides a complete

framework for developing action plan and strategies and implement them effectively. A simple,

complete and understandable information is needed in management accounting as managers are

not usual with some technical and financial terms.

Management Accounting Reports:

Account Receivable Aging Report

Account receivable report is vital to the organisation as it provides the information about the

debtors that owe the organisation. These reports are helpful to those organisations which work

heavily on credit basis. In ITW Construction Products, it helps the organisation in tracking

company's collection process simultaneously helping with finding substantial loopholes in

smooth credit flow process. This report provides managers with the inputs to develop robust

credit policy and weed out the probability of generation of bad debts.

Performance Reports

These reports provide information about the asymmetry between the actual execution and the

budgeted execution standards. In this regard, execution or performance can be comprehended as

the system credits the raw materials account and debits the goods in process account in ITW

Construction Products.

Inventory management system

Inventory management system combines technology with processes and procedures to ensure the

availability of inventory which consists of raw materials, goods in process and finished goods to

further ensure their availability at all times with the right quality (Bloomfield, 2015). It is often

used at manufacturing firms such as ITW Construction Products, and other concerns by using

asset tags to control the inflow of raw materials and outflow of finished goods as well as

maintaining requisite amount of goods at all times to ensure timely delivery to the clients.

Furthermore, it helps in determining future order requirements in advance which helps in smooth

flow of work processes.

Presentation of financial information:

While applying management accounting systems, main focus of business organisation is

on generation of informations that are reliable, complete, having relevance of various users and

must be accurate. As such kind of information is essential for managers to gain understanding of

facts and data which help in taking strategic decisions. Such information provides a complete

framework for developing action plan and strategies and implement them effectively. A simple,

complete and understandable information is needed in management accounting as managers are

not usual with some technical and financial terms.

Management Accounting Reports:

Account Receivable Aging Report

Account receivable report is vital to the organisation as it provides the information about the

debtors that owe the organisation. These reports are helpful to those organisations which work

heavily on credit basis. In ITW Construction Products, it helps the organisation in tracking

company's collection process simultaneously helping with finding substantial loopholes in

smooth credit flow process. This report provides managers with the inputs to develop robust

credit policy and weed out the probability of generation of bad debts.

Performance Reports

These reports provide information about the asymmetry between the actual execution and the

budgeted execution standards. In this regard, execution or performance can be comprehended as

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the effectual and efficiently achievement of business entity’s targets. The difference between the

actual vs budgeted parameters provides critical information about the gap in the execution

standards and the possible key factors which are leading to such differences (McLaren,

Appleyard and Mitchell, 2016). In ITW Construction Products, performance reports are prepared

using key performance indicators (KPI) as tools to assign weights to each function of the

performance evaluation. These reports are instrumental in taking strategic decisions about the

future endeavours.

Job Cost Report

This report is evidential in ascertaining cost, expenses and profit making capacity of each task. It

helps in evaluating the potential earning capacity of each project so that company can increase

more efforts on the potential projects and reduce targeted focus from the loss making projects. In

ITW Construction Products, this report is prepared on the basis of cost estimates, further

arrangement of job cost estimates into the same category of costs that further will be utilised to

generate the in real job cost information. It helps in difference evaluation between actual job cost

to estimated costs.

TASK 2

Costing Techniques to prepare income statements:

Cost: Costs are simply implies to expenses incurred by business enterprises for organisational

purpose. These are necessary for effective accomplishment of operations of business entity.

Costs can also be defined as consideration paid by organisations to acquire something or against

any expense. As ITW Construction Products is a manufacturing company so there are wide range

of expenses are incurred by them. In company costs are classified as variable, semi variable and

fixed. Cost analysis is done by company to increase their manufacturing efficiency. In cost

analysis interconnection of numerous costs and volume of production is evaluated critically.

ITW is using cost analysis to minimise the per unit cost.

Cost-Volume Profit: CVP analysis is used by ITW Construction Products to determine the way

in which volume of production and costs affects organisation's net profit and operational income.

It provide help in optimising price of products to achieve competitive targets.

Flexible budgeting: It is budgeting techniques in which a budget is prepared by accountants and

managers that is flexible and adjustable with changes in level of production and activities. It is

actual vs budgeted parameters provides critical information about the gap in the execution

standards and the possible key factors which are leading to such differences (McLaren,

Appleyard and Mitchell, 2016). In ITW Construction Products, performance reports are prepared

using key performance indicators (KPI) as tools to assign weights to each function of the

performance evaluation. These reports are instrumental in taking strategic decisions about the

future endeavours.

Job Cost Report

This report is evidential in ascertaining cost, expenses and profit making capacity of each task. It

helps in evaluating the potential earning capacity of each project so that company can increase

more efforts on the potential projects and reduce targeted focus from the loss making projects. In

ITW Construction Products, this report is prepared on the basis of cost estimates, further

arrangement of job cost estimates into the same category of costs that further will be utilised to

generate the in real job cost information. It helps in difference evaluation between actual job cost

to estimated costs.

TASK 2

Costing Techniques to prepare income statements:

Cost: Costs are simply implies to expenses incurred by business enterprises for organisational

purpose. These are necessary for effective accomplishment of operations of business entity.

Costs can also be defined as consideration paid by organisations to acquire something or against

any expense. As ITW Construction Products is a manufacturing company so there are wide range

of expenses are incurred by them. In company costs are classified as variable, semi variable and

fixed. Cost analysis is done by company to increase their manufacturing efficiency. In cost

analysis interconnection of numerous costs and volume of production is evaluated critically.

ITW is using cost analysis to minimise the per unit cost.

Cost-Volume Profit: CVP analysis is used by ITW Construction Products to determine the way

in which volume of production and costs affects organisation's net profit and operational income.

It provide help in optimising price of products to achieve competitive targets.

Flexible budgeting: It is budgeting techniques in which a budget is prepared by accountants and

managers that is flexible and adjustable with changes in level of production and activities. It is

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

used by ITW Construction Products to evaluate performance of company at different production

level in all aspect.

Cost Variances: It is simple costing term cost variance implies to gap between actual incurred

expenses or cost and expected costs. In ITW Construction Products, cost variances are analysed

by company to allocate any areas of manufacturing that require improvement.

Marginal Costing: In this method of costing cost are classified and presented as fixed

and variable to calculate cost. In ITW Construction these method is used to prepare cost sheet.

Here all fixed costs are classified as time or period cost regardless their nature.

Absorption Costing: It is most widely used method of costing in which all production

expense irrespective of their nature (Fixed or variable), is considered as cost of production in

order to calculate net income (Mitchell, and et.al., 2015).

Cost Allocation: Cost allocation implies to process of classification, collecting and

assigning expenses to per unit. Through allocation of costs to each unit, ITW Construction

determine their pricing policies. Following is a brief discussion on types of cost incurred by

company, as follows:

Variable Expenses: These are kind of expenses that increases and decreases as per

change in production level. In Company major variable expenses are material and labour costs.

Fixed Expenses: These are expenses which are considered as period cost. Main feature

of these expense is that such expenses do not change with varies in production, such fixed selling

and distribution expenses.

Semi-variable Expenses: These kind of expenses are classified as both fixed and

variable. Some part of these expenses are fixed and other one is variable.

Normal Costing: It is most common and usual method of costing. Under this method

simply expenses are allocated to cost per unit. In ITW Construction, these method is used to

calculate net income and asses the cost per unit.

Standard Costing: It is an extension of normal costing. Applying this method ITW

Construction compare their actual performance with standard performance. It provides a

systematic and comparative data to evaluate organisation's efficiency.

level in all aspect.

Cost Variances: It is simple costing term cost variance implies to gap between actual incurred

expenses or cost and expected costs. In ITW Construction Products, cost variances are analysed

by company to allocate any areas of manufacturing that require improvement.

Marginal Costing: In this method of costing cost are classified and presented as fixed

and variable to calculate cost. In ITW Construction these method is used to prepare cost sheet.

Here all fixed costs are classified as time or period cost regardless their nature.

Absorption Costing: It is most widely used method of costing in which all production

expense irrespective of their nature (Fixed or variable), is considered as cost of production in

order to calculate net income (Mitchell, and et.al., 2015).

Cost Allocation: Cost allocation implies to process of classification, collecting and

assigning expenses to per unit. Through allocation of costs to each unit, ITW Construction

determine their pricing policies. Following is a brief discussion on types of cost incurred by

company, as follows:

Variable Expenses: These are kind of expenses that increases and decreases as per

change in production level. In Company major variable expenses are material and labour costs.

Fixed Expenses: These are expenses which are considered as period cost. Main feature

of these expense is that such expenses do not change with varies in production, such fixed selling

and distribution expenses.

Semi-variable Expenses: These kind of expenses are classified as both fixed and

variable. Some part of these expenses are fixed and other one is variable.

Normal Costing: It is most common and usual method of costing. Under this method

simply expenses are allocated to cost per unit. In ITW Construction, these method is used to

calculate net income and asses the cost per unit.

Standard Costing: It is an extension of normal costing. Applying this method ITW

Construction compare their actual performance with standard performance. It provides a

systematic and comparative data to evaluate organisation's efficiency.

Activity-Based Costing: In this method organisation like ITW Construction make a

detailed classification of different costs and allocate them to particular activities and functions. It

help to increase efficiency of different activities in order to attain predetermined goals.

Inventory Costs: Inventory costs are expenses incurred by business entity to store,

manage and procure different kind of inventory. ITW Construction being a manufacturing

company incurs inventory costs such as Cost of storage, handling costs, logistic cost, loading and

unloading expenses etc.

Advantages of minimising inventory costs to an organisation: inventory cost is a vital

factors that assist in calculating gross and net profit. In manufacturing and construction

companies. In ITW Construction, inventory costs are controlled by production managers to

increase overall profitability. Reduction in inventory costs help company to reduce price of

products and increase per unit profit percentage.

Inventory Valuation Methods: There are different approaches are used by managers to

value inventories. But most acceptable and commonly applied methods are LIFO, FIFO and

Average cost. Following are explanation of these methods, as follows:

LIFO Method of inventory: This method is emphasises on presumption for valuation of stock

that last purchased inventory is sold at first place.

FIFO Method of inventory: This method emphasises upon assumption for valuation of stock that

first purchased stock is sold at first place (Bromiley and et.al, 2015).

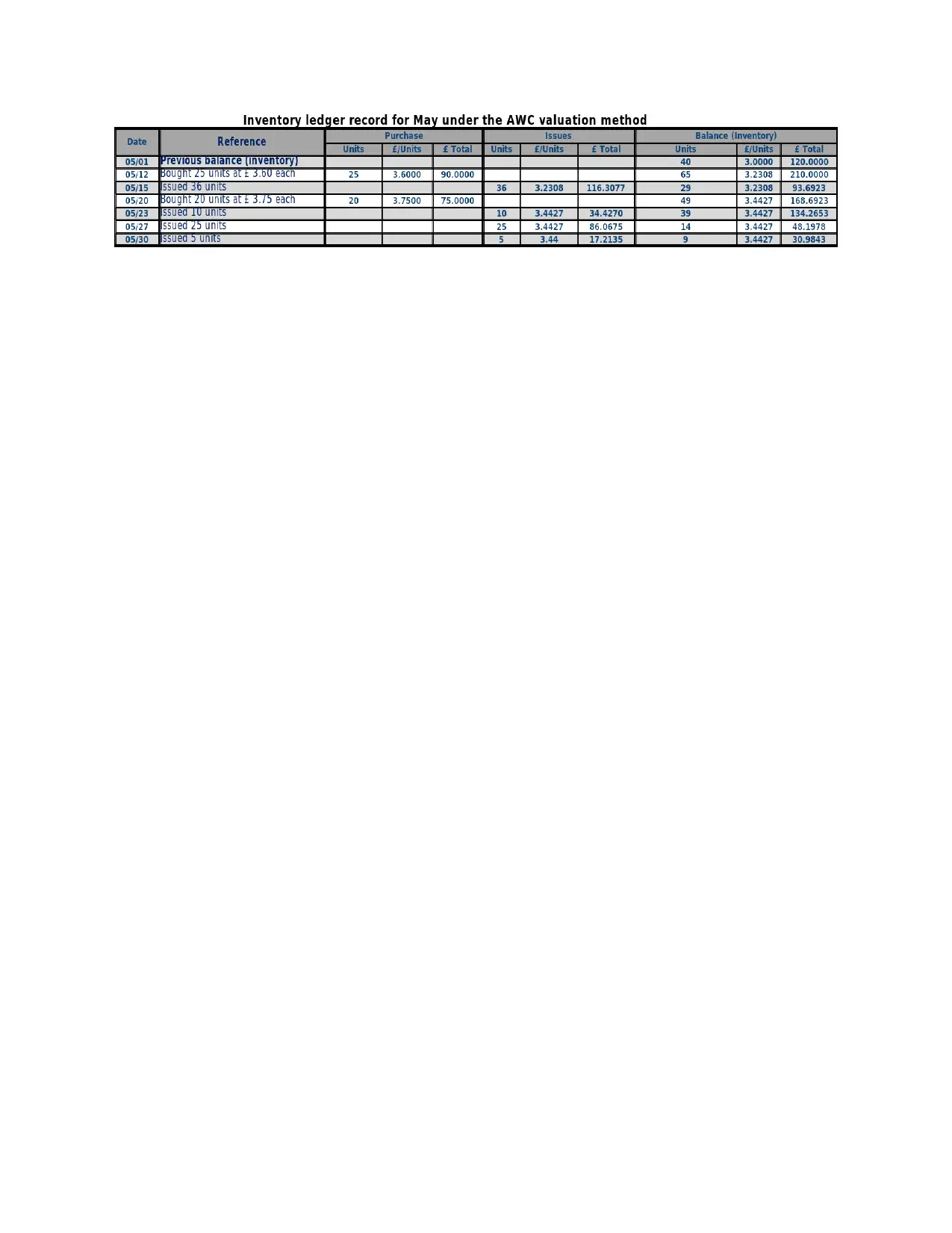

Average Cost Method: Under this method average cost of inventories is calculated and applied to

value inventories.

Overheads Costs: These are expenses incurred by business enterprise excluding

production and manufacturing costs or cost which are incurred directly for the purpose of

production of products. In ITW Construction overhead expenses are selling expenses, salaries

expenses, administration expenses etc.

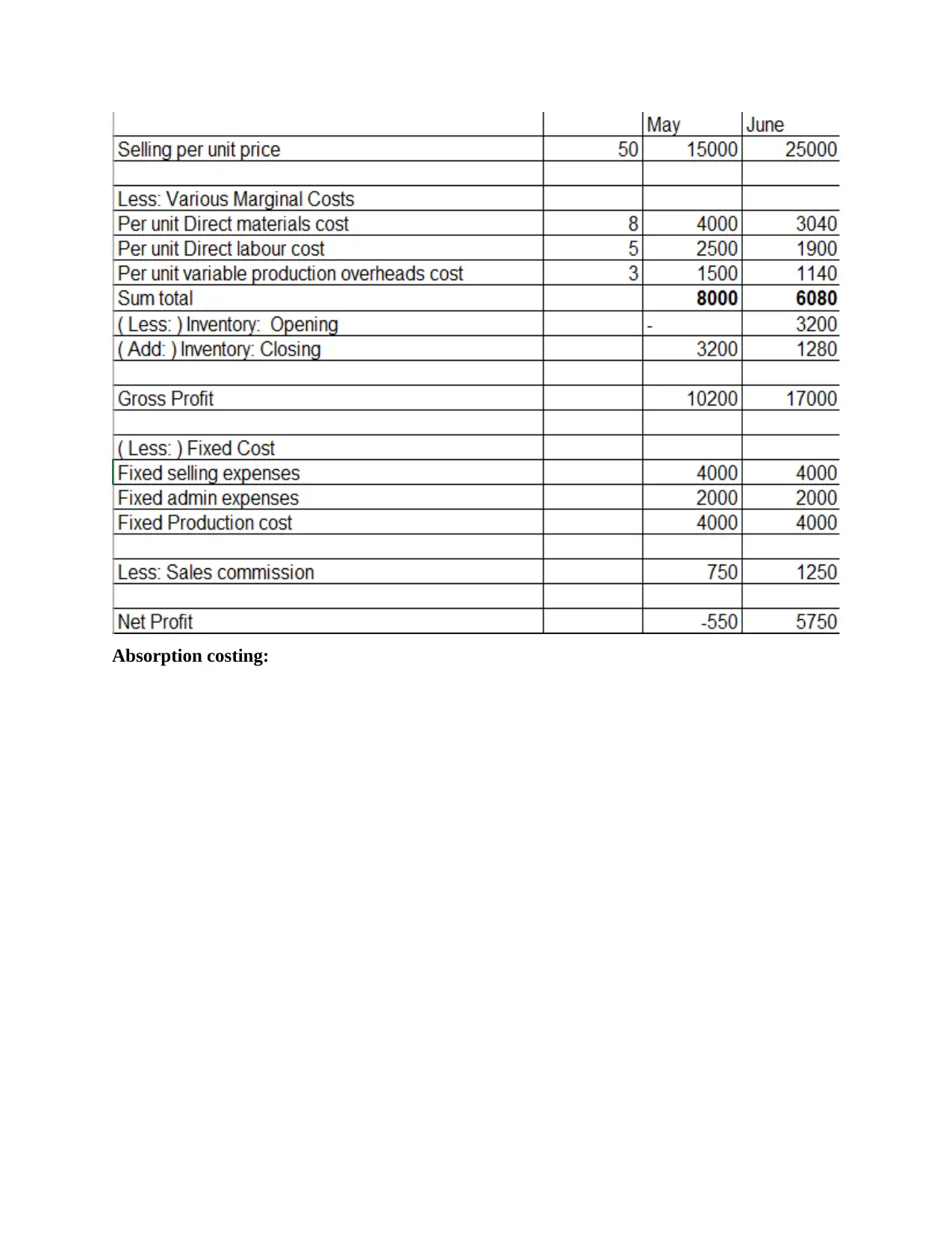

Marginal costing:

detailed classification of different costs and allocate them to particular activities and functions. It

help to increase efficiency of different activities in order to attain predetermined goals.

Inventory Costs: Inventory costs are expenses incurred by business entity to store,

manage and procure different kind of inventory. ITW Construction being a manufacturing

company incurs inventory costs such as Cost of storage, handling costs, logistic cost, loading and

unloading expenses etc.

Advantages of minimising inventory costs to an organisation: inventory cost is a vital

factors that assist in calculating gross and net profit. In manufacturing and construction

companies. In ITW Construction, inventory costs are controlled by production managers to

increase overall profitability. Reduction in inventory costs help company to reduce price of

products and increase per unit profit percentage.

Inventory Valuation Methods: There are different approaches are used by managers to

value inventories. But most acceptable and commonly applied methods are LIFO, FIFO and

Average cost. Following are explanation of these methods, as follows:

LIFO Method of inventory: This method is emphasises on presumption for valuation of stock

that last purchased inventory is sold at first place.

FIFO Method of inventory: This method emphasises upon assumption for valuation of stock that

first purchased stock is sold at first place (Bromiley and et.al, 2015).

Average Cost Method: Under this method average cost of inventories is calculated and applied to

value inventories.

Overheads Costs: These are expenses incurred by business enterprise excluding

production and manufacturing costs or cost which are incurred directly for the purpose of

production of products. In ITW Construction overhead expenses are selling expenses, salaries

expenses, administration expenses etc.

Marginal costing:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

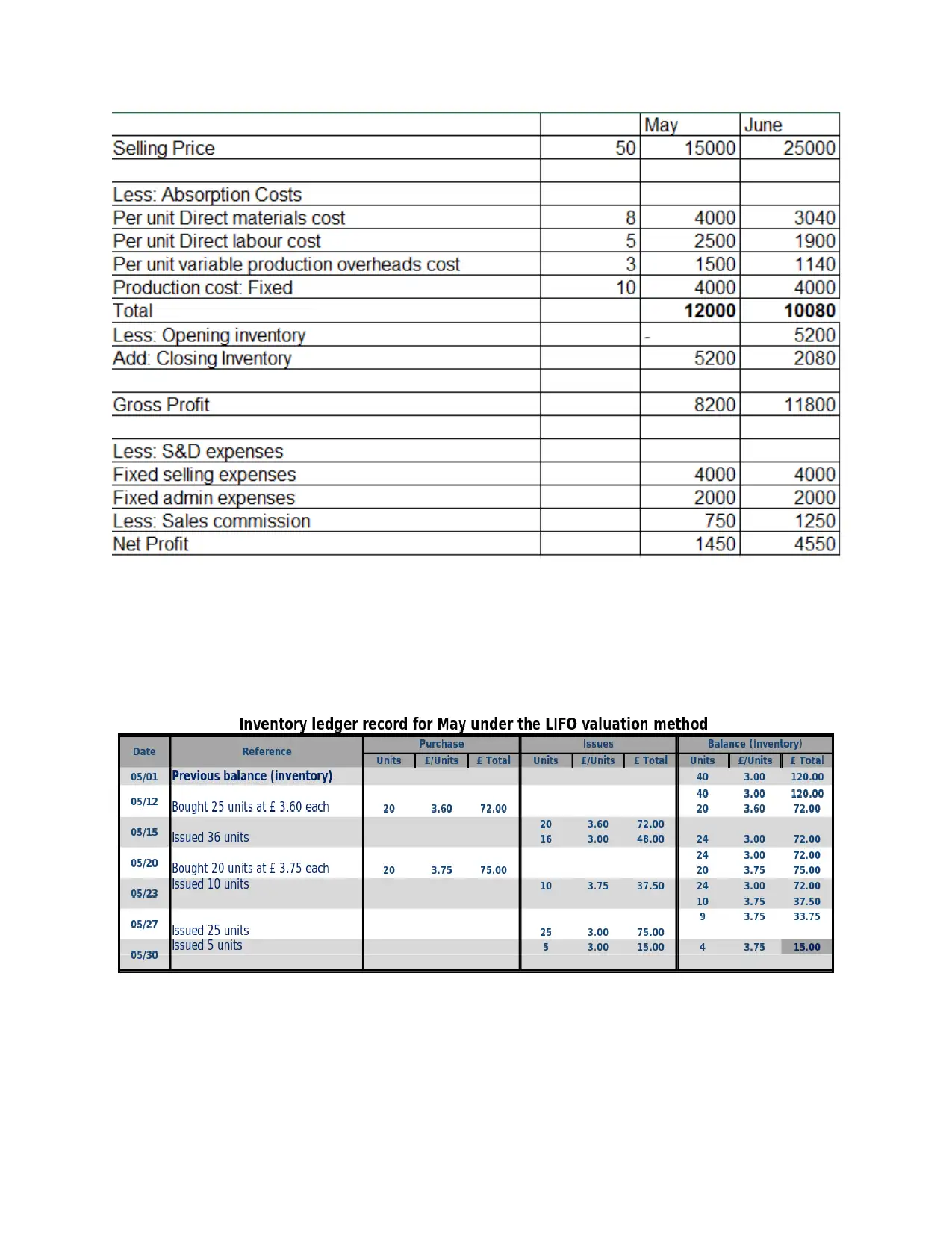

Absorption costing:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.