Management Accounting Report: Financial Performance of Oshodi PLC

VerifiedAdded on 2021/02/21

|19

|6000

|37

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its significance and application within Oshodi PLC. It begins by defining management accounting and its role in financial decision-making, contrasting it with financial accounting. The report then explores various management accounting systems such as job costing, inventory management, and cost accounting, evaluating their benefits and uses. It details different reporting methods, including budget reports, performance reports, and accounts receivable reports. The analysis extends to the preparation of income statements using both marginal and absorption costing methods. The report evaluates the benefits and limitations of planning tools for budgetary control and analyzes the application of different budgets. Finally, it compares management accounting tools to solve financial problems within an organization. The report highlights the importance of integrating management accounting systems and reporting for effective financial management. This assignment is published on Desklib, a platform providing AI-based study tools for students.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Describing management accounting and the significance of its systems..............................1

P2. Explaining various methods that are been used for the purpose of reporting.......................2

M1. Evaluation of the MA systems through its uses and the application....................................3

D1. Evaluating systems and the reporting of the management accounting with their

integration....................................................................................................................................4

LO 2.................................................................................................................................................4

P 3 Preparation of income statement by marginal and absorption cost.......................................4

LO3..................................................................................................................................................8

P4. Evaluating benefits and the limitation of the various kinds of the planning tools that are

been used for the budgetary control.............................................................................................8

M3&D3. Analysing the uses and the application of the different budgets................................10

....................................................................................................................................................10

LO 4 ..............................................................................................................................................11

P 5 Comparison of management accounting tools to solve the financial problems..................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Describing management accounting and the significance of its systems..............................1

P2. Explaining various methods that are been used for the purpose of reporting.......................2

M1. Evaluation of the MA systems through its uses and the application....................................3

D1. Evaluating systems and the reporting of the management accounting with their

integration....................................................................................................................................4

LO 2.................................................................................................................................................4

P 3 Preparation of income statement by marginal and absorption cost.......................................4

LO3..................................................................................................................................................8

P4. Evaluating benefits and the limitation of the various kinds of the planning tools that are

been used for the budgetary control.............................................................................................8

M3&D3. Analysing the uses and the application of the different budgets................................10

....................................................................................................................................................10

LO 4 ..............................................................................................................................................11

P 5 Comparison of management accounting tools to solve the financial problems..................11

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Management accounting is the process of analysing the business performance by

evaluating the cost and operation of the company. The cost and operation analysis help the

organisation to prepare the internal report to evaluate their market share and growth in compare

to their competitor and provide detail information to the internal and external shareholders. MA

is used to provide the critical information about the company. Oshodi PLC company is a

manufacturing company which use the management accounting system to prepare the annual

report by getting information from various sources. The report highlights the requirement of MA

system in company to get financial and non financial information. Different management

accounting system such as cost accounting, financial accounting, inventory management

accounting, job costing etc. help to analyse the different factors of accounting system and take

effective and efficient decision. It explains the different methods of MA reporting like budget

report, sales report, purchase report, account receivable aging report to record the information for

the future needs. It also demonstrates the use of marginal and absorption costing method to

prepare the income statement of Oshodi PLC company. The report also highlights the advantages

and disadvantages of planning tools and the use of different MA tools to resolve the financial

problem in the organization.

LO1.

P1. Describing management accounting and the significance of its systems.

MA refers to the process that facilitates the financial information and the resources to

managers of Oshodi Plc in making suitable decisions (Bogsnes, 2016). It involves preparing of

the management accounts and the reports for the purpose of providing an accurate statistical and

the financial information to the users. Management accounting is entirely different from financial

accounting as follows-

Management accounting Financial accounting

It is mainly used by the internal stakeholders

that is employees, managers and the owners.

This accounting is been used by both internal

and the external users that includes

shareholders, managers, lenders, employees

etc.

The main purpose of the MA is to helps

Oshodi Plc in controlling, decision-making

and planning.

Its objective is to record for the financial

performance and position of an entity for a

particular period at the end of the accounting

year.

1

Management accounting is the process of analysing the business performance by

evaluating the cost and operation of the company. The cost and operation analysis help the

organisation to prepare the internal report to evaluate their market share and growth in compare

to their competitor and provide detail information to the internal and external shareholders. MA

is used to provide the critical information about the company. Oshodi PLC company is a

manufacturing company which use the management accounting system to prepare the annual

report by getting information from various sources. The report highlights the requirement of MA

system in company to get financial and non financial information. Different management

accounting system such as cost accounting, financial accounting, inventory management

accounting, job costing etc. help to analyse the different factors of accounting system and take

effective and efficient decision. It explains the different methods of MA reporting like budget

report, sales report, purchase report, account receivable aging report to record the information for

the future needs. It also demonstrates the use of marginal and absorption costing method to

prepare the income statement of Oshodi PLC company. The report also highlights the advantages

and disadvantages of planning tools and the use of different MA tools to resolve the financial

problem in the organization.

LO1.

P1. Describing management accounting and the significance of its systems.

MA refers to the process that facilitates the financial information and the resources to

managers of Oshodi Plc in making suitable decisions (Bogsnes, 2016). It involves preparing of

the management accounts and the reports for the purpose of providing an accurate statistical and

the financial information to the users. Management accounting is entirely different from financial

accounting as follows-

Management accounting Financial accounting

It is mainly used by the internal stakeholders

that is employees, managers and the owners.

This accounting is been used by both internal

and the external users that includes

shareholders, managers, lenders, employees

etc.

The main purpose of the MA is to helps

Oshodi Plc in controlling, decision-making

and planning.

Its objective is to record for the financial

performance and position of an entity for a

particular period at the end of the accounting

year.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The nature of MA is counted as financial as

well as non-financial because it records for

both monetary and non-monetary information.

It involves mainly the information that are

financial in nature.

Essentials of MA systems-

Job costing system- It refers to the system that accumulates and assigns the production

cost in relation to an individual output or the unit. It is the costing system that is been used at the

time when several items are been produced that are different and has significant cost (Boyabatlı,

Leng and Toktay, 2015). This system plays a crucial role for Oshodi Plc in developing the

information relating to identifying the accuracy of an estimating system of an organization,

which helps in fixing the price that allows for generating larger profits.

Inventory management system- This system of MA makes supervision of the non-

capitalized assets and the inventory items. It is the system helps in the tracking the flow of the

items from the manufacturer to the warehouses and to the POS that is point of selling (Craig and

et.al., 2018). It is been counted as the most significant system for Oshodi Plc as it helps in

maintaining the adequate record of the inventory and in controlling the handling cost attached to

the goods.

Cost accounting system- This MA system referred as the method in which the

production activities are been recoded as per the system of perpetual inventory. This system is

been designed and essential for Oshodi Plc in tracking the cost involved in the manufacturing its

article. It helps the organization in assessing the present and the prospective cost that is and will

be incurred in the process of producing the product.

Price optimization system- It is the mathematical tool that analyse the response of the

customers at various price levels of product (King and Clarkson, 2015). It is the most vital

strategy that has been used by the Oshodi Plc in order to arrive at the setting up the most suitable

price within the defined level of profitability and in developing an understanding regarding

sensitivity of the existing clients in relation to the changes in the price of the product.

P2. Explaining various methods that are been used for the purpose of reporting.

Managerial reporting refers to the formulation of the reports that focuses on the inside

information that is been received through the use of financial accounting. MA reports are been

formulated for regulating, decision-making, planning and in measuring the performance. There

are large number of the reports that is been prepared by the management are as follows-

2

well as non-financial because it records for

both monetary and non-monetary information.

It involves mainly the information that are

financial in nature.

Essentials of MA systems-

Job costing system- It refers to the system that accumulates and assigns the production

cost in relation to an individual output or the unit. It is the costing system that is been used at the

time when several items are been produced that are different and has significant cost (Boyabatlı,

Leng and Toktay, 2015). This system plays a crucial role for Oshodi Plc in developing the

information relating to identifying the accuracy of an estimating system of an organization,

which helps in fixing the price that allows for generating larger profits.

Inventory management system- This system of MA makes supervision of the non-

capitalized assets and the inventory items. It is the system helps in the tracking the flow of the

items from the manufacturer to the warehouses and to the POS that is point of selling (Craig and

et.al., 2018). It is been counted as the most significant system for Oshodi Plc as it helps in

maintaining the adequate record of the inventory and in controlling the handling cost attached to

the goods.

Cost accounting system- This MA system referred as the method in which the

production activities are been recoded as per the system of perpetual inventory. This system is

been designed and essential for Oshodi Plc in tracking the cost involved in the manufacturing its

article. It helps the organization in assessing the present and the prospective cost that is and will

be incurred in the process of producing the product.

Price optimization system- It is the mathematical tool that analyse the response of the

customers at various price levels of product (King and Clarkson, 2015). It is the most vital

strategy that has been used by the Oshodi Plc in order to arrive at the setting up the most suitable

price within the defined level of profitability and in developing an understanding regarding

sensitivity of the existing clients in relation to the changes in the price of the product.

P2. Explaining various methods that are been used for the purpose of reporting.

Managerial reporting refers to the formulation of the reports that focuses on the inside

information that is been received through the use of financial accounting. MA reports are been

formulated for regulating, decision-making, planning and in measuring the performance. There

are large number of the reports that is been prepared by the management are as follows-

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budget report- It refers to the report that includes detailed analysis of the budgeted

revenues, expenses and the income for Oshodi Plc that is to be achieved by performing the task

effectively and efficiently (Lees, Malik and Williams, 2019). This report plays a critical role in

guiding the managers for offering better incentives to the employees, renegotiating the terms and

cutting the cost as it lists down all the assumptions regarding the sources of the expenditure and

the earnings of the company.

Performance report- This MA report is been created by the managers of Oshodi Plc for

measuring performance of the entire company and the employees at the end of the period. This

report is been used by the managers for making the important strategic decisions in relation to

the future of an entity (Maas, Schaltegger and Crutzen, 2016). It helps in depicting the under-

performers within the company so that corrective measures can be taken by the managers like

training them to perform better in towards achievement of the mission.

Accounts receivable reports- This report is framed for recording the remaining balances

that JoJo Fruit comapny has to recover. It assists the managers in determining defaulters and in

finding the issues within the collection process of the company. It provides for tightening the

credit policies of the company in case there are large number of defaulters present because cash

flow is considered as the critical aspect for operating the business smoothly.

Other reports- It refers to the reports that includes other major management reports that

are very essential such as information reports, competitor’s analysis and the project reports. Such

reports are been prepared internally or outsourced from the professionals (Mirgorodskaya and

et.al., 2017). The most suitable action course is dependent on the capabilities in handling the

requirements of the firm.

Thus, for reaching towards the major decisions, managers must have to access to these

authentic and the credible reports.

M1. Evaluation of the MA systems through its uses and the application.

Management accounting systems benefits

Job costing : It helps the Oshodi PLC company to evaluate the qualitative and

quantitative data to take the effective and efficient decisions. It helps to analyse the different

organisational activity and measure their cost and performance of each job to take the decision of

improvement (Iacob and Constantin, 2015).

3

revenues, expenses and the income for Oshodi Plc that is to be achieved by performing the task

effectively and efficiently (Lees, Malik and Williams, 2019). This report plays a critical role in

guiding the managers for offering better incentives to the employees, renegotiating the terms and

cutting the cost as it lists down all the assumptions regarding the sources of the expenditure and

the earnings of the company.

Performance report- This MA report is been created by the managers of Oshodi Plc for

measuring performance of the entire company and the employees at the end of the period. This

report is been used by the managers for making the important strategic decisions in relation to

the future of an entity (Maas, Schaltegger and Crutzen, 2016). It helps in depicting the under-

performers within the company so that corrective measures can be taken by the managers like

training them to perform better in towards achievement of the mission.

Accounts receivable reports- This report is framed for recording the remaining balances

that JoJo Fruit comapny has to recover. It assists the managers in determining defaulters and in

finding the issues within the collection process of the company. It provides for tightening the

credit policies of the company in case there are large number of defaulters present because cash

flow is considered as the critical aspect for operating the business smoothly.

Other reports- It refers to the reports that includes other major management reports that

are very essential such as information reports, competitor’s analysis and the project reports. Such

reports are been prepared internally or outsourced from the professionals (Mirgorodskaya and

et.al., 2017). The most suitable action course is dependent on the capabilities in handling the

requirements of the firm.

Thus, for reaching towards the major decisions, managers must have to access to these

authentic and the credible reports.

M1. Evaluation of the MA systems through its uses and the application.

Management accounting systems benefits

Job costing : It helps the Oshodi PLC company to evaluate the qualitative and

quantitative data to take the effective and efficient decisions. It helps to analyse the different

organisational activity and measure their cost and performance of each job to take the decision of

improvement (Iacob and Constantin, 2015).

3

Price optimization system: It is a continuous and ongoing process which help the

company to plan the different activities and associated cost to achieve the aim on time by

estimating the price of each activity. The preparation of proper plan regarding setting price of

each activity help the company to attract customer by identifying their need and demands

(Abdallah, 2017). Oshodi PLC company use price optimisation system to prepare plan for

increasing the profit and sales in the market by analysing the behaviour of customer regarding

the price.

Inventory management system: It helps the company to manage the inventory level in

the organisation order the quantity when they required the material. Oshodi PLC company use

the inventory management tool to identify and address the cost of maintenance of inventory level

(Bendell and et.al., 2017). It is used to report the information and help managers & employee's

to take major decision regarding the company performance in market.

Cost accounting : cost accounting system help the company to estimate the cost of each

and every activity & identify the measure to minimize their cost for the effective and efficient

results. It helps the company to measure the performance in the market via comparing

performance through the different accounting tools such as balance scorecard, benchmarking,

key performance indicator etc.

D1. Evaluating systems and the reporting of the management accounting with their integration.

Management accounting reporting and the systems are highly integrated as effective

preparation of the reports is based on the systems like inventory management system helps in the

framing of the accounts receivable reports and the budget report so that accurate measures can be

taken with appropriate estimations. Oshodi Plc can make use of the cost accounting report in

order to manage its cost system effectively and efficiently which in turn helps the firm in keeping

the control over the cost so that higher profitability could be gained.

LO 2

P 3 Preparation of income statement by marginal and absorption cost

Marginal cost : Marginal cost refers the cost incurred in one additional unit of production. It

helps to identify the optimal level of production for the company. In marginal cost method fixed

cost of the company can be considered as the accounting period cost and variable cost is taken as

product cost.

4

company to plan the different activities and associated cost to achieve the aim on time by

estimating the price of each activity. The preparation of proper plan regarding setting price of

each activity help the company to attract customer by identifying their need and demands

(Abdallah, 2017). Oshodi PLC company use price optimisation system to prepare plan for

increasing the profit and sales in the market by analysing the behaviour of customer regarding

the price.

Inventory management system: It helps the company to manage the inventory level in

the organisation order the quantity when they required the material. Oshodi PLC company use

the inventory management tool to identify and address the cost of maintenance of inventory level

(Bendell and et.al., 2017). It is used to report the information and help managers & employee's

to take major decision regarding the company performance in market.

Cost accounting : cost accounting system help the company to estimate the cost of each

and every activity & identify the measure to minimize their cost for the effective and efficient

results. It helps the company to measure the performance in the market via comparing

performance through the different accounting tools such as balance scorecard, benchmarking,

key performance indicator etc.

D1. Evaluating systems and the reporting of the management accounting with their integration.

Management accounting reporting and the systems are highly integrated as effective

preparation of the reports is based on the systems like inventory management system helps in the

framing of the accounts receivable reports and the budget report so that accurate measures can be

taken with appropriate estimations. Oshodi Plc can make use of the cost accounting report in

order to manage its cost system effectively and efficiently which in turn helps the firm in keeping

the control over the cost so that higher profitability could be gained.

LO 2

P 3 Preparation of income statement by marginal and absorption cost

Marginal cost : Marginal cost refers the cost incurred in one additional unit of production. It

helps to identify the optimal level of production for the company. In marginal cost method fixed

cost of the company can be considered as the accounting period cost and variable cost is taken as

product cost.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

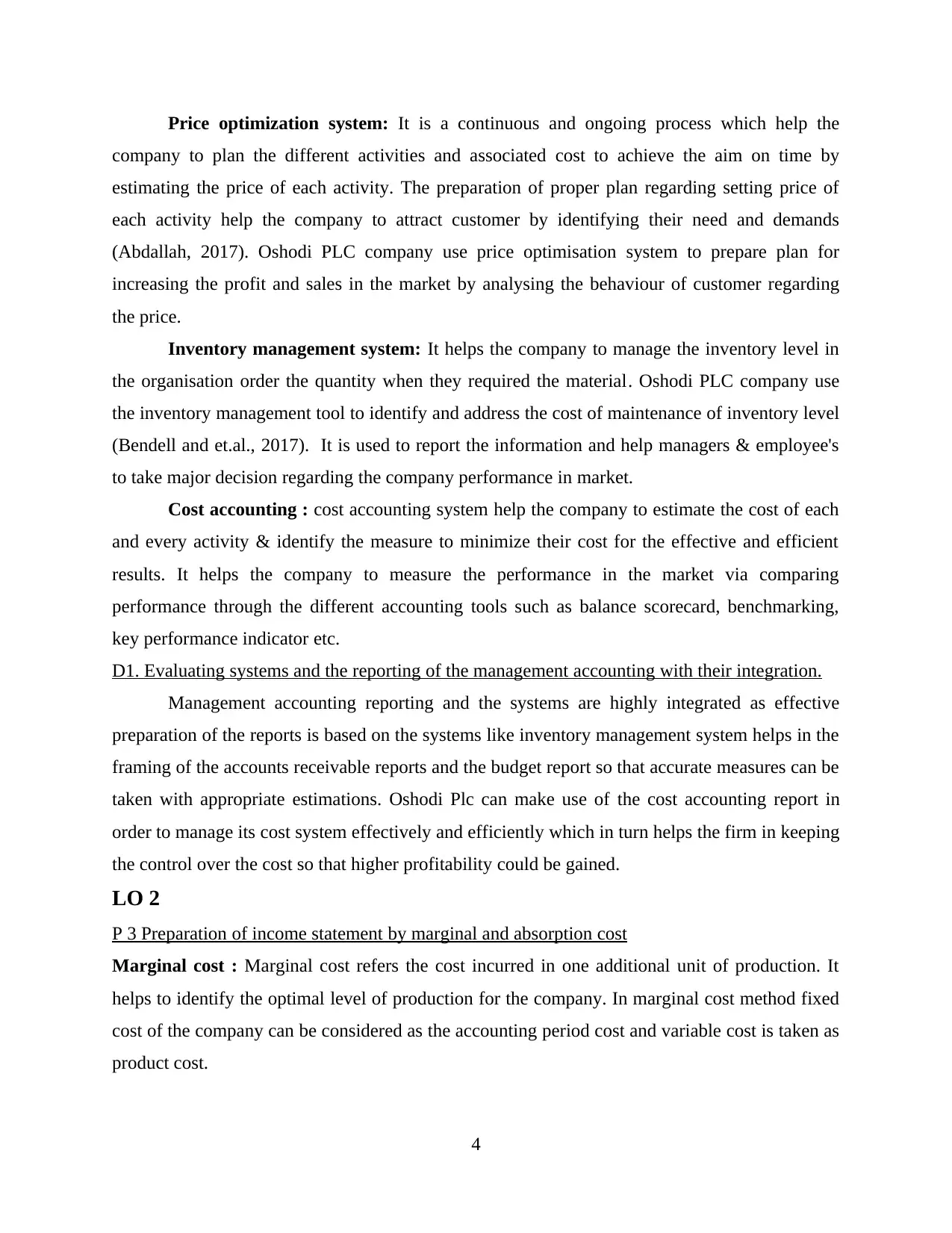

Under marginal costing

Cost per unit

Direct material 18

Direct labour 4

Variable O/H 3

Marginal cost/ unit 25

SP 50

Less : Marginal

cost/unit -25

Less : variable selling

price -5.00

Contribution per unit 20.00

Total production cost = direct material + direct labour = variable overhead

contribution = selling price – (marginal cost per unit + variable selling cost)

Absorption cost : It refers to the method used for calculating the cost associate with the

production activity. It refers to charge all overhead cost in the period when expenses incurred. It

includes the various factors such as direct material, variable manufacturing overhead, direct

labour and fixed manufacturing overhead. It is required by the company for income tax reporting

and financial reporting. It considered both the variable and fixed cost as the product cost.

Per unit cost by absorption cost method

particulars Amount Cost / unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production

overhead 99000/11000 9

Total production cost

variable cost 25

Fixed cost 9

Total 34

Total production cost = variable cost + fixed cost

5

Cost per unit

Direct material 18

Direct labour 4

Variable O/H 3

Marginal cost/ unit 25

SP 50

Less : Marginal

cost/unit -25

Less : variable selling

price -5.00

Contribution per unit 20.00

Total production cost = direct material + direct labour = variable overhead

contribution = selling price – (marginal cost per unit + variable selling cost)

Absorption cost : It refers to the method used for calculating the cost associate with the

production activity. It refers to charge all overhead cost in the period when expenses incurred. It

includes the various factors such as direct material, variable manufacturing overhead, direct

labour and fixed manufacturing overhead. It is required by the company for income tax reporting

and financial reporting. It considered both the variable and fixed cost as the product cost.

Per unit cost by absorption cost method

particulars Amount Cost / unit

Normal level of

production 11000

Fixed overhead cost 99000

Fixed production

overhead 99000/11000 9

Total production cost

variable cost 25

Fixed cost 9

Total 34

Total production cost = variable cost + fixed cost

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Preparation of income statement using absorption cost method

6

6

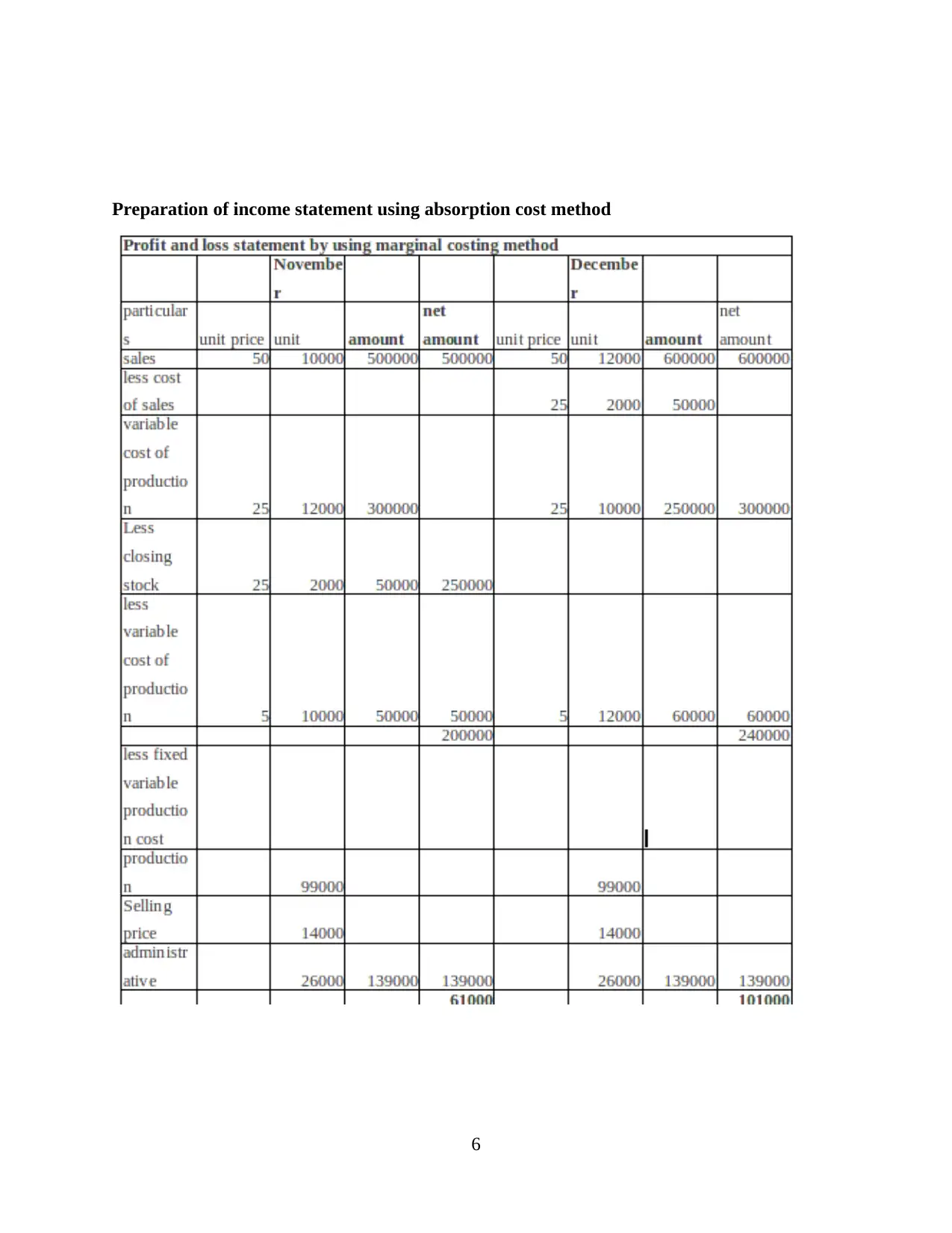

Preparation of income statement by using absorption cost method

Income statement using Absorption costing

November December

Units Amount Amount Units Amount Amount

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 34 2000 68000

Variable cost of production @

34 12000 408000 10000 340000

Less: Closing stock @ 34 2000 68000

340000 408000

Gross profit 160000 192000

Adjustment for over / under

absorption of overheads 9000 9000

169000 183000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 79000 83000

Calculation of over and under absorption for November and December month

Months Production unit O/H unit Total overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Interpretation: It can be concluded from the above table that by using marginal cost

method company able to generate £61000 in November month and £101000 in December month

while using the absorption cost method company generate £79000 in November month and

£83000 in December month. The absorption cost method is the best method to prepare the

income statements because it considered all production cost while marginal cost only considered

the cost which was incurred at the time of production. Absorption method provide more accurate

and reliable result to the company in compare to the marginal cost method.

7

Income statement using Absorption costing

November December

Units Amount Amount Units Amount Amount

Sales @ 50 10000 500000 12000 600000

Less: Cost of sales

Opening stock @ 34 2000 68000

Variable cost of production @

34 12000 408000 10000 340000

Less: Closing stock @ 34 2000 68000

340000 408000

Gross profit 160000 192000

Adjustment for over / under

absorption of overheads 9000 9000

169000 183000

Fixed overheads:

Variable selling overhead 50000 60000

Fixed selling overhead 14000 14000

Fixed Administration overhead 26000 90000 26000 100000

Net profit 79000 83000

Calculation of over and under absorption for November and December month

Months Production unit O/H unit Total overhead O/H incurred

Over/ under

absorption

November 12000 9 108000 99000 9000

December 10000 9 90000 99000 -9000

Interpretation: It can be concluded from the above table that by using marginal cost

method company able to generate £61000 in November month and £101000 in December month

while using the absorption cost method company generate £79000 in November month and

£83000 in December month. The absorption cost method is the best method to prepare the

income statements because it considered all production cost while marginal cost only considered

the cost which was incurred at the time of production. Absorption method provide more accurate

and reliable result to the company in compare to the marginal cost method.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

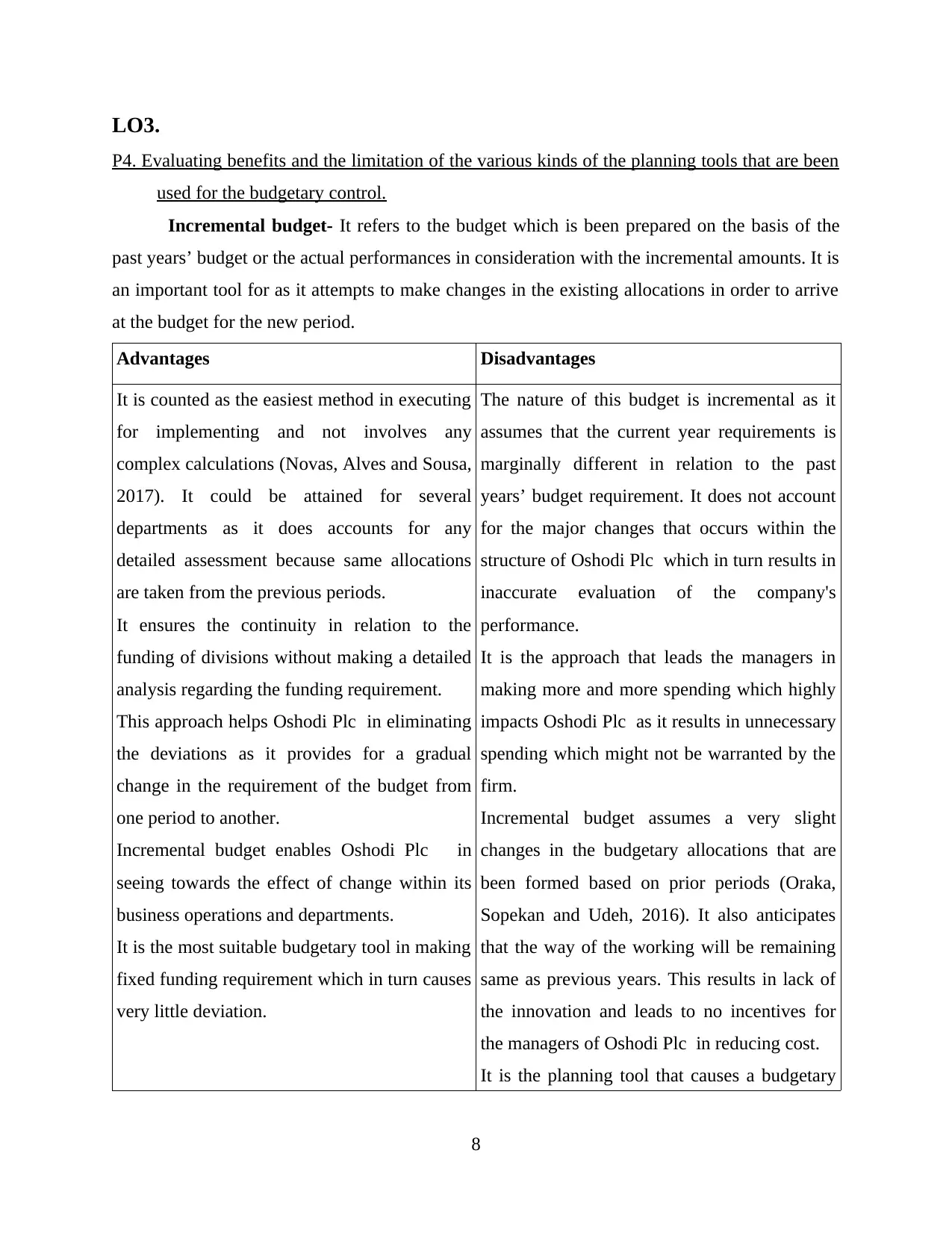

LO3.

P4. Evaluating benefits and the limitation of the various kinds of the planning tools that are been

used for the budgetary control.

Incremental budget- It refers to the budget which is been prepared on the basis of the

past years’ budget or the actual performances in consideration with the incremental amounts. It is

an important tool for as it attempts to make changes in the existing allocations in order to arrive

at the budget for the new period.

Advantages Disadvantages

It is counted as the easiest method in executing

for implementing and not involves any

complex calculations (Novas, Alves and Sousa,

2017). It could be attained for several

departments as it does accounts for any

detailed assessment because same allocations

are taken from the previous periods.

It ensures the continuity in relation to the

funding of divisions without making a detailed

analysis regarding the funding requirement.

This approach helps Oshodi Plc in eliminating

the deviations as it provides for a gradual

change in the requirement of the budget from

one period to another.

Incremental budget enables Oshodi Plc in

seeing towards the effect of change within its

business operations and departments.

It is the most suitable budgetary tool in making

fixed funding requirement which in turn causes

very little deviation.

The nature of this budget is incremental as it

assumes that the current year requirements is

marginally different in relation to the past

years’ budget requirement. It does not account

for the major changes that occurs within the

structure of Oshodi Plc which in turn results in

inaccurate evaluation of the company's

performance.

It is the approach that leads the managers in

making more and more spending which highly

impacts Oshodi Plc as it results in unnecessary

spending which might not be warranted by the

firm.

Incremental budget assumes a very slight

changes in the budgetary allocations that are

been formed based on prior periods (Oraka,

Sopekan and Udeh, 2016). It also anticipates

that the way of the working will be remaining

same as previous years. This results in lack of

the innovation and leads to no incentives for

the managers of Oshodi Plc in reducing cost.

It is the planning tool that causes a budgetary

8

P4. Evaluating benefits and the limitation of the various kinds of the planning tools that are been

used for the budgetary control.

Incremental budget- It refers to the budget which is been prepared on the basis of the

past years’ budget or the actual performances in consideration with the incremental amounts. It is

an important tool for as it attempts to make changes in the existing allocations in order to arrive

at the budget for the new period.

Advantages Disadvantages

It is counted as the easiest method in executing

for implementing and not involves any

complex calculations (Novas, Alves and Sousa,

2017). It could be attained for several

departments as it does accounts for any

detailed assessment because same allocations

are taken from the previous periods.

It ensures the continuity in relation to the

funding of divisions without making a detailed

analysis regarding the funding requirement.

This approach helps Oshodi Plc in eliminating

the deviations as it provides for a gradual

change in the requirement of the budget from

one period to another.

Incremental budget enables Oshodi Plc in

seeing towards the effect of change within its

business operations and departments.

It is the most suitable budgetary tool in making

fixed funding requirement which in turn causes

very little deviation.

The nature of this budget is incremental as it

assumes that the current year requirements is

marginally different in relation to the past

years’ budget requirement. It does not account

for the major changes that occurs within the

structure of Oshodi Plc which in turn results in

inaccurate evaluation of the company's

performance.

It is the approach that leads the managers in

making more and more spending which highly

impacts Oshodi Plc as it results in unnecessary

spending which might not be warranted by the

firm.

Incremental budget assumes a very slight

changes in the budgetary allocations that are

been formed based on prior periods (Oraka,

Sopekan and Udeh, 2016). It also anticipates

that the way of the working will be remaining

same as previous years. This results in lack of

the innovation and leads to no incentives for

the managers of Oshodi Plc in reducing cost.

It is the planning tool that causes a budgetary

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

slack in within the management of Oshodi Plc

where the managers build lower growth in the

revenues and the higher growth in the expenses

in order to attain favourable variances.

Cash budget- It refers to the assumptions that are made in relation to the cash outflows

and the inflows for the business over the particular time period. This budget is been used for

assessing that Oshodi Plc is having sufficient cash for operating its business.

Advantages Disadvantages

It is the planning tool that helps the company

in determining the accurate cash balances in

order to fulfil the routine obligations (Surianti

and Dalimunthe, 2015). It shows that the firm

is maintaining the minimum liquidity and the

requirement of the cash balances that are

provisioned by the banks and internal

regulations are been maintained.

Cash budget also helps Oshodi Plc in

determining the cash needed in making the

operational activity more and more productive.

It assists an enterprise in maintaining its

liquidity position as it provides the detailed

analysis regarding the cash receipt and the

expenditures.

It helps in identifying the cash amount that is

been required for fulfilling the short term and

the immediate obligations without making use

of any credit lines or the overdraft protection.

This budget can cause distortions as the cash

inflows does not equate to the profits. Cash

inflows that are resulting from the fines,

security deposits, selling of the capital assets or

any other activity.

It is the budget that are very much susceptible

to the manipulation as it restricts the cash flow

for a particular period and in inflating the cash

flow for next period. Under this budget, in case

the operations of the company are experiencing

the loss, postponing the payouts may show the

positive value of the cash flow.

The major limitation of this budget is that it is

based on the estimates (Wildavsky, 2017).

Revenues and the expenses for the future

period are estimated which could be wrong in

case of the uncertain or the changing

conditions.

9

where the managers build lower growth in the

revenues and the higher growth in the expenses

in order to attain favourable variances.

Cash budget- It refers to the assumptions that are made in relation to the cash outflows

and the inflows for the business over the particular time period. This budget is been used for

assessing that Oshodi Plc is having sufficient cash for operating its business.

Advantages Disadvantages

It is the planning tool that helps the company

in determining the accurate cash balances in

order to fulfil the routine obligations (Surianti

and Dalimunthe, 2015). It shows that the firm

is maintaining the minimum liquidity and the

requirement of the cash balances that are

provisioned by the banks and internal

regulations are been maintained.

Cash budget also helps Oshodi Plc in

determining the cash needed in making the

operational activity more and more productive.

It assists an enterprise in maintaining its

liquidity position as it provides the detailed

analysis regarding the cash receipt and the

expenditures.

It helps in identifying the cash amount that is

been required for fulfilling the short term and

the immediate obligations without making use

of any credit lines or the overdraft protection.

This budget can cause distortions as the cash

inflows does not equate to the profits. Cash

inflows that are resulting from the fines,

security deposits, selling of the capital assets or

any other activity.

It is the budget that are very much susceptible

to the manipulation as it restricts the cash flow

for a particular period and in inflating the cash

flow for next period. Under this budget, in case

the operations of the company are experiencing

the loss, postponing the payouts may show the

positive value of the cash flow.

The major limitation of this budget is that it is

based on the estimates (Wildavsky, 2017).

Revenues and the expenses for the future

period are estimated which could be wrong in

case of the uncertain or the changing

conditions.

9

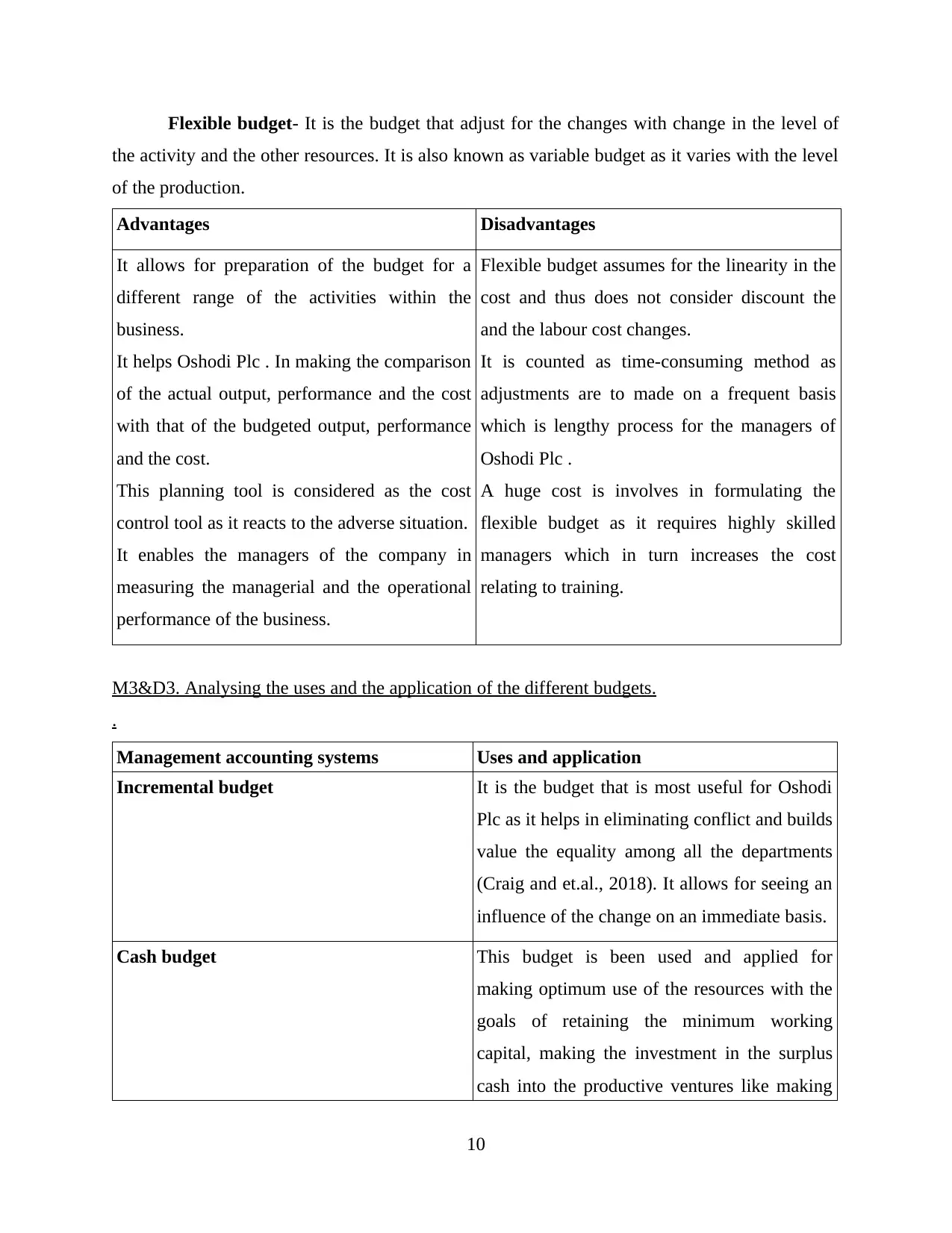

Flexible budget- It is the budget that adjust for the changes with change in the level of

the activity and the other resources. It is also known as variable budget as it varies with the level

of the production.

Advantages Disadvantages

It allows for preparation of the budget for a

different range of the activities within the

business.

It helps Oshodi Plc . In making the comparison

of the actual output, performance and the cost

with that of the budgeted output, performance

and the cost.

This planning tool is considered as the cost

control tool as it reacts to the adverse situation.

It enables the managers of the company in

measuring the managerial and the operational

performance of the business.

Flexible budget assumes for the linearity in the

cost and thus does not consider discount the

and the labour cost changes.

It is counted as time-consuming method as

adjustments are to made on a frequent basis

which is lengthy process for the managers of

Oshodi Plc .

A huge cost is involves in formulating the

flexible budget as it requires highly skilled

managers which in turn increases the cost

relating to training.

M3&D3. Analysing the uses and the application of the different budgets.

.

Management accounting systems Uses and application

Incremental budget It is the budget that is most useful for Oshodi

Plc as it helps in eliminating conflict and builds

value the equality among all the departments

(Craig and et.al., 2018). It allows for seeing an

influence of the change on an immediate basis.

Cash budget This budget is been used and applied for

making optimum use of the resources with the

goals of retaining the minimum working

capital, making the investment in the surplus

cash into the productive ventures like making

10

the activity and the other resources. It is also known as variable budget as it varies with the level

of the production.

Advantages Disadvantages

It allows for preparation of the budget for a

different range of the activities within the

business.

It helps Oshodi Plc . In making the comparison

of the actual output, performance and the cost

with that of the budgeted output, performance

and the cost.

This planning tool is considered as the cost

control tool as it reacts to the adverse situation.

It enables the managers of the company in

measuring the managerial and the operational

performance of the business.

Flexible budget assumes for the linearity in the

cost and thus does not consider discount the

and the labour cost changes.

It is counted as time-consuming method as

adjustments are to made on a frequent basis

which is lengthy process for the managers of

Oshodi Plc .

A huge cost is involves in formulating the

flexible budget as it requires highly skilled

managers which in turn increases the cost

relating to training.

M3&D3. Analysing the uses and the application of the different budgets.

.

Management accounting systems Uses and application

Incremental budget It is the budget that is most useful for Oshodi

Plc as it helps in eliminating conflict and builds

value the equality among all the departments

(Craig and et.al., 2018). It allows for seeing an

influence of the change on an immediate basis.

Cash budget This budget is been used and applied for

making optimum use of the resources with the

goals of retaining the minimum working

capital, making the investment in the surplus

cash into the productive ventures like making

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.