Management Accounting Report: Systems, Costs, Budgeting, and Analysis

VerifiedAdded on 2021/02/20

|15

|3931

|34

Report

AI Summary

This report delves into the realm of management accounting, providing a comprehensive analysis of its systems, cost calculation techniques, and budgeting processes within the context of Cambridge Manufacturing Ltd. It explores various management accounting systems such as price optimization, cost accounting, job costing, and inventory management. The report then proceeds to examine different cost calculation techniques, including absorption costing and marginal costing, with practical examples. Furthermore, the report discusses the importance of budgeting for planning and control, and concludes by addressing financial problem identification and the application of appropriate techniques. The report highlights the differences between management and financial accounting and the significance of managerial accounting reports. The report includes calculations and analysis of costs using various methods and techniques, offering a detailed insight into the financial aspects of the business.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and several types of essential systems...........................................1

TASK 2............................................................................................................................................4

Calculate cost using appropriate techniques...........................................................................4

TASK 3...........................................................................................................................................8

Using budgets for planning and control.................................................................................8

TASK 4..........................................................................................................................................10

Identify financial problems and apply appropriate techniques.............................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

Management accounting and several types of essential systems...........................................1

TASK 2............................................................................................................................................4

Calculate cost using appropriate techniques...........................................................................4

TASK 3...........................................................................................................................................8

Using budgets for planning and control.................................................................................8

TASK 4..........................................................................................................................................10

Identify financial problems and apply appropriate techniques.............................................10

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

INTRODUCTION

Management accounting is a set of skills that perform the various accounting information

in such a way that it can assist the management for a better understanding of accounts to prepare

and formulate the policies and decisions for the organisation (DRURY, 2013). It is mainly

followed by the internal team of an enterprises and this is only thing which makes it different

from financial accounting. To better understand the topic of relevant topic taken Cambridge

manufacturing Ltd, it provides weight loss supplements and produced a range of specialist

dietary products and offers nutritional assurance with conventional foo for more gradual weight

loss and weight management. The entire report presents the understanding about management

accounting system as well as reports of particular accounting period of time. Report also focus

on cost techniques which can use to calculate of net profit. Additionally, several planning tools

and accounting tools are applied by business to face off different types of financial problems.

TASK 1

Management accounting and several types of essential systems

Management accounting is the process to prepare different types reports regarding to

internal activities then present in front of top management. In present time every organisation

want to maintain and control their internal system in effective manner so they can apply

management accounting system.

Management accounting system and their types

Management accounting system is procedure to collect, analyse, measure and

determinant meaningful financial information then record in right accounts. These systems can

apply according to situation and help to increase productivity as well as profitability of

Cambridge manufacturing Ltd. There are defined essential system of management accounting

that are discussed underneath:

Price optimisation system- This system mainly based on customer perception and pricing

structure of the company. Every manufacturing company wants to increase their sale so they will

conduct research regarding to their product. It is a mathematical analysis that consist of financial

information of their products and set price of different items as per the analysis and customer

perception. In Cambridge manufacturing Ltd, apply price optimisation system to set best prices

of different supplements and attract much more customers (Herbert and Seal, 2012).

1

Management accounting is a set of skills that perform the various accounting information

in such a way that it can assist the management for a better understanding of accounts to prepare

and formulate the policies and decisions for the organisation (DRURY, 2013). It is mainly

followed by the internal team of an enterprises and this is only thing which makes it different

from financial accounting. To better understand the topic of relevant topic taken Cambridge

manufacturing Ltd, it provides weight loss supplements and produced a range of specialist

dietary products and offers nutritional assurance with conventional foo for more gradual weight

loss and weight management. The entire report presents the understanding about management

accounting system as well as reports of particular accounting period of time. Report also focus

on cost techniques which can use to calculate of net profit. Additionally, several planning tools

and accounting tools are applied by business to face off different types of financial problems.

TASK 1

Management accounting and several types of essential systems

Management accounting is the process to prepare different types reports regarding to

internal activities then present in front of top management. In present time every organisation

want to maintain and control their internal system in effective manner so they can apply

management accounting system.

Management accounting system and their types

Management accounting system is procedure to collect, analyse, measure and

determinant meaningful financial information then record in right accounts. These systems can

apply according to situation and help to increase productivity as well as profitability of

Cambridge manufacturing Ltd. There are defined essential system of management accounting

that are discussed underneath:

Price optimisation system- This system mainly based on customer perception and pricing

structure of the company. Every manufacturing company wants to increase their sale so they will

conduct research regarding to their product. It is a mathematical analysis that consist of financial

information of their products and set price of different items as per the analysis and customer

perception. In Cambridge manufacturing Ltd, apply price optimisation system to set best prices

of different supplements and attract much more customers (Herbert and Seal, 2012).

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting System – It is a set of framework which can use by companies to

evaluate the cost of their products in the context to analysis of stock, profitability as well as cost

control. It can examine past, present and future data to provide the basis for managerial decision

making. A cost accounting system has been recorded all data in simple way and the purpose to

fix sale price to acquire small part of mission. In Cambridge manufacturing Ltd help to

investigate process of producing at different level and detail information like raw material, work

in progress and finished goods.

Job costing system – A job costing system is the process of collecting information which

is connected to cost of production as well as service job. These type information need to submit

in the contract where costs are reimbursed. Most of the companies used particular system to

provide facility of customization of products & services to their customers. In the context to

Cambridge manufacturing Ltd, the system is useful to determine information and examine

accuracy to able to quote price that can allow for a reasonable profit (Kaplan and Atkinson,

2015).

Inventory management system – This system is track the record of inventory and

analysis each level manufacturing. The particular system mainly consider for manufacturing

company where consist of raw material, finished goods in warehouse, stock dispatched to

delivery to merchant or customers. In Cambridge manufacturing Ltd manufacturing company

apply the system to use material in appropriate way and try to reduce wastages. The system

based of three methods which are

LIFO – According to this method inventory come in last that will sale out first.

FIFO – In this method first in first out of stock and company apply this method to

generate profit.

AVOC – There are material used on Average cost.

Difference between management accounting and financial accounting

Basis Management accounting Financial accounting

Meaning It is the process of internal system

and provide data to managers to take

decision and prepare plan and

strategies.

It is an accounting system which

can focus on develop of financial

statement in order to provide

financial information to outsider of

2

evaluate the cost of their products in the context to analysis of stock, profitability as well as cost

control. It can examine past, present and future data to provide the basis for managerial decision

making. A cost accounting system has been recorded all data in simple way and the purpose to

fix sale price to acquire small part of mission. In Cambridge manufacturing Ltd help to

investigate process of producing at different level and detail information like raw material, work

in progress and finished goods.

Job costing system – A job costing system is the process of collecting information which

is connected to cost of production as well as service job. These type information need to submit

in the contract where costs are reimbursed. Most of the companies used particular system to

provide facility of customization of products & services to their customers. In the context to

Cambridge manufacturing Ltd, the system is useful to determine information and examine

accuracy to able to quote price that can allow for a reasonable profit (Kaplan and Atkinson,

2015).

Inventory management system – This system is track the record of inventory and

analysis each level manufacturing. The particular system mainly consider for manufacturing

company where consist of raw material, finished goods in warehouse, stock dispatched to

delivery to merchant or customers. In Cambridge manufacturing Ltd manufacturing company

apply the system to use material in appropriate way and try to reduce wastages. The system

based of three methods which are

LIFO – According to this method inventory come in last that will sale out first.

FIFO – In this method first in first out of stock and company apply this method to

generate profit.

AVOC – There are material used on Average cost.

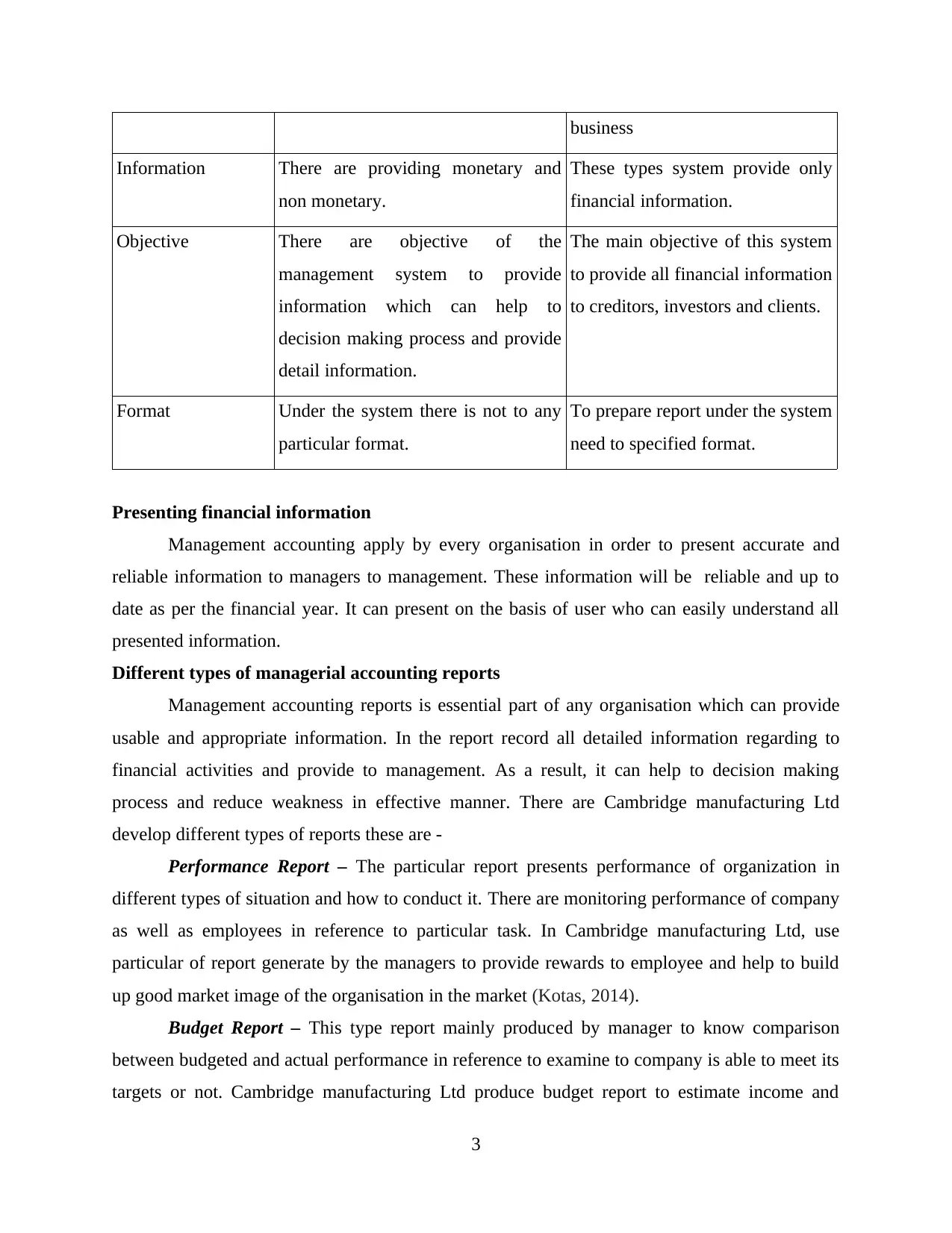

Difference between management accounting and financial accounting

Basis Management accounting Financial accounting

Meaning It is the process of internal system

and provide data to managers to take

decision and prepare plan and

strategies.

It is an accounting system which

can focus on develop of financial

statement in order to provide

financial information to outsider of

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

business

Information There are providing monetary and

non monetary.

These types system provide only

financial information.

Objective There are objective of the

management system to provide

information which can help to

decision making process and provide

detail information.

The main objective of this system

to provide all financial information

to creditors, investors and clients.

Format Under the system there is not to any

particular format.

To prepare report under the system

need to specified format.

Presenting financial information

Management accounting apply by every organisation in order to present accurate and

reliable information to managers to management. These information will be reliable and up to

date as per the financial year. It can present on the basis of user who can easily understand all

presented information.

Different types of managerial accounting reports

Management accounting reports is essential part of any organisation which can provide

usable and appropriate information. In the report record all detailed information regarding to

financial activities and provide to management. As a result, it can help to decision making

process and reduce weakness in effective manner. There are Cambridge manufacturing Ltd

develop different types of reports these are -

Performance Report – The particular report presents performance of organization in

different types of situation and how to conduct it. There are monitoring performance of company

as well as employees in reference to particular task. In Cambridge manufacturing Ltd, use

particular of report generate by the managers to provide rewards to employee and help to build

up good market image of the organisation in the market (Kotas, 2014).

Budget Report – This type report mainly produced by manager to know comparison

between budgeted and actual performance in reference to examine to company is able to meet its

targets or not. Cambridge manufacturing Ltd produce budget report to estimate income and

3

Information There are providing monetary and

non monetary.

These types system provide only

financial information.

Objective There are objective of the

management system to provide

information which can help to

decision making process and provide

detail information.

The main objective of this system

to provide all financial information

to creditors, investors and clients.

Format Under the system there is not to any

particular format.

To prepare report under the system

need to specified format.

Presenting financial information

Management accounting apply by every organisation in order to present accurate and

reliable information to managers to management. These information will be reliable and up to

date as per the financial year. It can present on the basis of user who can easily understand all

presented information.

Different types of managerial accounting reports

Management accounting reports is essential part of any organisation which can provide

usable and appropriate information. In the report record all detailed information regarding to

financial activities and provide to management. As a result, it can help to decision making

process and reduce weakness in effective manner. There are Cambridge manufacturing Ltd

develop different types of reports these are -

Performance Report – The particular report presents performance of organization in

different types of situation and how to conduct it. There are monitoring performance of company

as well as employees in reference to particular task. In Cambridge manufacturing Ltd, use

particular of report generate by the managers to provide rewards to employee and help to build

up good market image of the organisation in the market (Kotas, 2014).

Budget Report – This type report mainly produced by manager to know comparison

between budgeted and actual performance in reference to examine to company is able to meet its

targets or not. Cambridge manufacturing Ltd produce budget report to estimate income and

3

expenses of a company and make assure about the operational and executional activities which

are presented on the base of estimation.

Inventory management Report – These type of reports mainly produced by

manufacturing company in order to track the record of producing process. In Cambridge

manufacturing Ltd, it is prepared to know how to company use different types of raw material at

each level and know wastage inventory. It can help to deduct quantity of wastages and utilises

resources in effective way.

TASK 2

Calculate cost using appropriate techniques

Cost – The particular term directly connect to the business and present the amount of

money which is received and paid by company to conduct different types of transactions. In the

manufacturing company to produce goods and services record on the basis of cost. There are

including all necessary cost which can get assets in lace and ready to use. There are discussed

various types of cost -

Direct & Indirect Cost – Direct cost are those cost which are connected to product and

amount of expenses to easily attributable of the product. These types of cost are

appointed for the commodity on purpose and effect relationship. While indirect cost are

connected to product but amount of expenses is not track-able in an economically

feasible manner.

Fixed and Variable cost – Fixed cost is that cost which can not change after the changes

in proportion to the change in result like monthly salary cost of a supervisor. On the other

side variable cost is changing in proportion to the change in aspects like direct labour cost

(Lukka and Vinnari, 2014).

Production and non production cost – The production cost mainly focused on the

manufacturing of commodities such as labour cost while non production cost are

concentrate on other cost of the business such as administrative cost.

Absorption Costing – The particular method consider as managerial accounting cost

method where all expenses mainly related to manufacturing for specific products. The particular

method includes both type costs direct and indirect to analysis of cost of production. For

4

are presented on the base of estimation.

Inventory management Report – These type of reports mainly produced by

manufacturing company in order to track the record of producing process. In Cambridge

manufacturing Ltd, it is prepared to know how to company use different types of raw material at

each level and know wastage inventory. It can help to deduct quantity of wastages and utilises

resources in effective way.

TASK 2

Calculate cost using appropriate techniques

Cost – The particular term directly connect to the business and present the amount of

money which is received and paid by company to conduct different types of transactions. In the

manufacturing company to produce goods and services record on the basis of cost. There are

including all necessary cost which can get assets in lace and ready to use. There are discussed

various types of cost -

Direct & Indirect Cost – Direct cost are those cost which are connected to product and

amount of expenses to easily attributable of the product. These types of cost are

appointed for the commodity on purpose and effect relationship. While indirect cost are

connected to product but amount of expenses is not track-able in an economically

feasible manner.

Fixed and Variable cost – Fixed cost is that cost which can not change after the changes

in proportion to the change in result like monthly salary cost of a supervisor. On the other

side variable cost is changing in proportion to the change in aspects like direct labour cost

(Lukka and Vinnari, 2014).

Production and non production cost – The production cost mainly focused on the

manufacturing of commodities such as labour cost while non production cost are

concentrate on other cost of the business such as administrative cost.

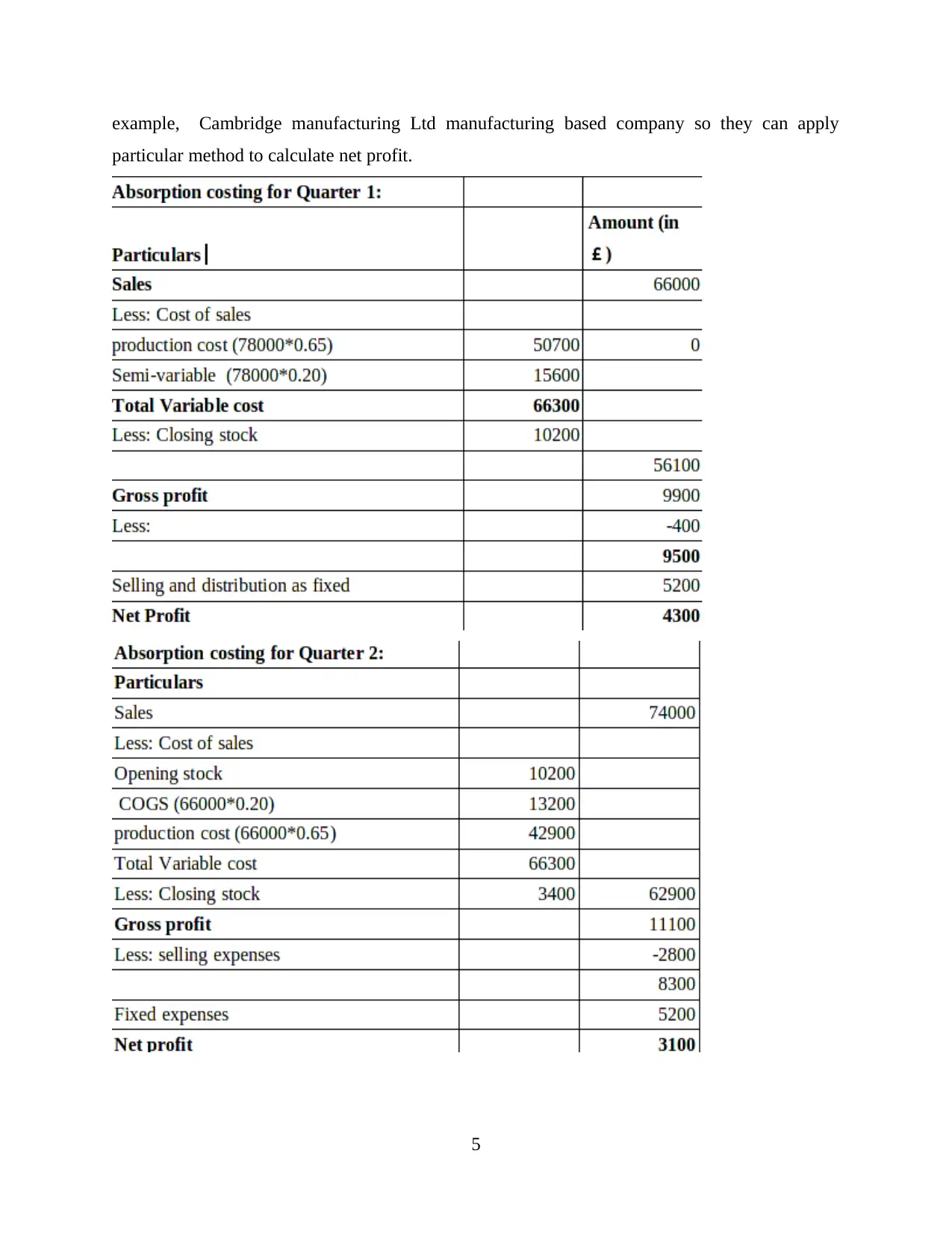

Absorption Costing – The particular method consider as managerial accounting cost

method where all expenses mainly related to manufacturing for specific products. The particular

method includes both type costs direct and indirect to analysis of cost of production. For

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

example, Cambridge manufacturing Ltd manufacturing based company so they can apply

particular method to calculate net profit.

5

particular method to calculate net profit.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

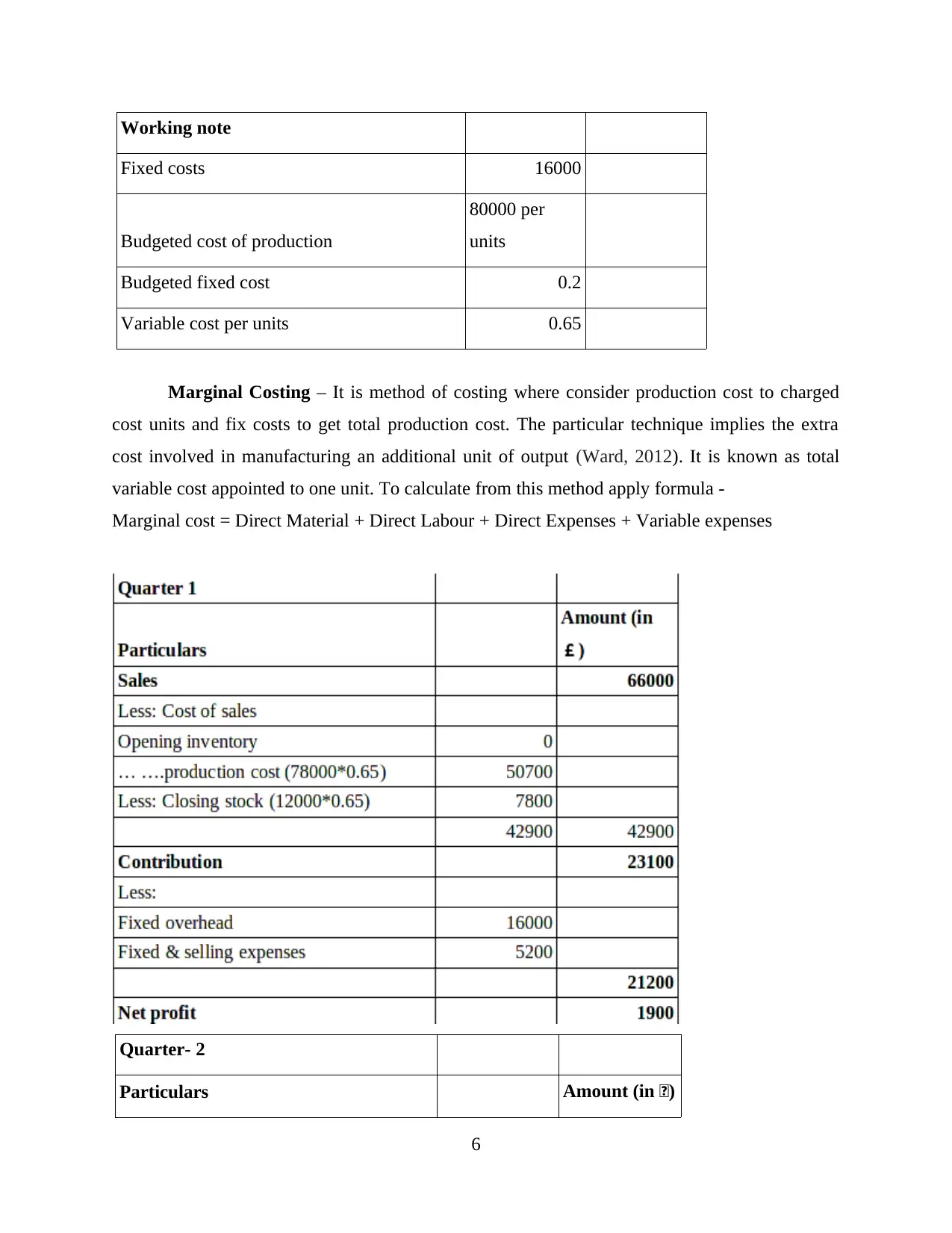

Working note

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Marginal Costing – It is method of costing where consider production cost to charged

cost units and fix costs to get total production cost. The particular technique implies the extra

cost involved in manufacturing an additional unit of output (Ward, 2012). It is known as total

variable cost appointed to one unit. To calculate from this method apply formula -

Marginal cost = Direct Material + Direct Labour + Direct Expenses + Variable expenses

Quarter- 2

Particulars Amount (in £)

6

Fixed costs 16000

Budgeted cost of production

80000 per

units

Budgeted fixed cost 0.2

Variable cost per units 0.65

Marginal Costing – It is method of costing where consider production cost to charged

cost units and fix costs to get total production cost. The particular technique implies the extra

cost involved in manufacturing an additional unit of output (Ward, 2012). It is known as total

variable cost appointed to one unit. To calculate from this method apply formula -

Marginal cost = Direct Material + Direct Labour + Direct Expenses + Variable expenses

Quarter- 2

Particulars Amount (in £)

6

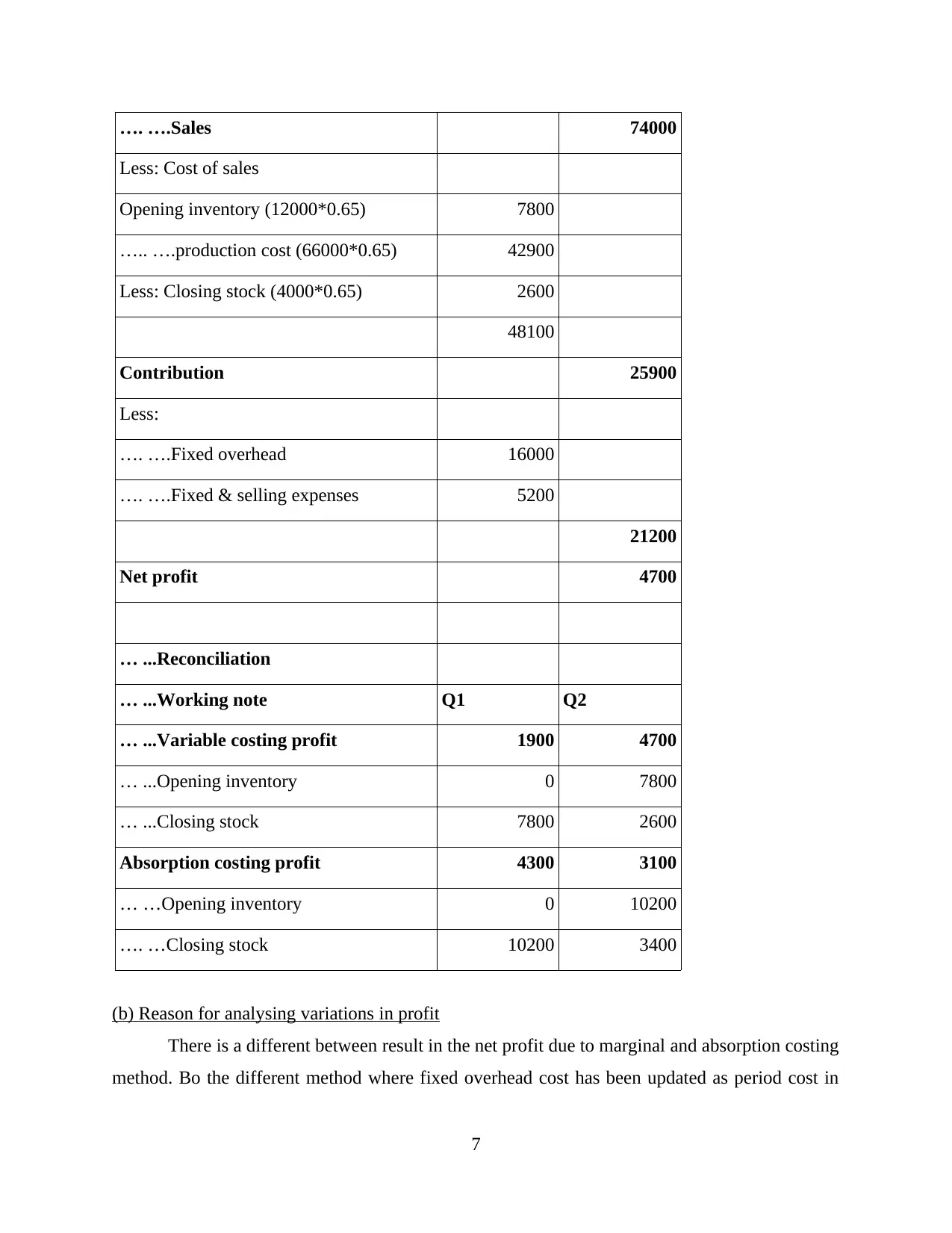

…. ….Sales 74000

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

Net profit 4700

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

(b) Reason for analysing variations in profit

There is a different between result in the net profit due to marginal and absorption costing

method. Bo the different method where fixed overhead cost has been updated as period cost in

7

Less: Cost of sales

Opening inventory (12000*0.65) 7800

….. ….production cost (66000*0.65) 42900

Less: Closing stock (4000*0.65) 2600

48100

Contribution 25900

Less:

…. ….Fixed overhead 16000

…. ….Fixed & selling expenses 5200

21200

Net profit 4700

… ...Reconciliation

… ...Working note Q1 Q2

… ...Variable costing profit 1900 4700

… ...Opening inventory 0 7800

… ...Closing stock 7800 2600

Absorption costing profit 4300 3100

… …Opening inventory 0 10200

…. …Closing stock 10200 3400

(b) Reason for analysing variations in profit

There is a different between result in the net profit due to marginal and absorption costing

method. Bo the different method where fixed overhead cost has been updated as period cost in

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

marginal costing method. On the other side in absorption method whether fixed or variable is

categorised as cost of production (Maas, Schaltegger and Crutzen, 2016).

TASK 3

Using budgets for planning and control

Preparing a budget - Budgeting is a process that defines estimate figure of future

income and expenditure over a specific time of period. Budget is Financial statement or

estimation of revenue and expenses that can be made by a person, a business, a government or

an organisation. Financial department prepares the sheet to assists the department's head in

formulation of budget estimate. Manager discuss the plan for proposed level of activity. Top

management can work with the planned budget according to budget's financial circumstance and

prepare the estimate of forthcoming year. The complete budget are present by managers with the

approval of executive officers. Nero Ltd is used the same process to figure out the proposed

budget. They sets the expenditure level of all the products for every department. The estimate

figure are allocated to their target capital which are available for the project.

Operational budget:

It is a detailed prediction of all estimated income and expenses based on forecasted sales

revenue for a specific time of period. An operational budget is helps the Nero Ltd in the terms

for planning the day to day activities so they always know the working areas.

Advantages - Its advantages are to Nero Ltd to manage the current indirect expenses

which are paid on daily or monthly basis such as office rent, salaries, wages etc. This

budget helps for evaluating the current actual expenses and past expenses too. So they

can found the variation in the expenditure (Tucker and Lowe, 2014).

Disadvantages - It may have some disadvantages first it cover, it is time consuming

concepts especially for the poor organised company. There are not easily predetermined

of accurate data.

Master Budget:

It is a functional budget prepared by particular division of an organisation. Master budget

is sum of the all division's budget. It may includes income statement, balance sheet, cash flow

statement, fund flow statement of an organisation. Nero Ltd can prepare particular budget to

examine capital investment and manufacturing levels (Otley and Emmanuel, 2013) .

8

categorised as cost of production (Maas, Schaltegger and Crutzen, 2016).

TASK 3

Using budgets for planning and control

Preparing a budget - Budgeting is a process that defines estimate figure of future

income and expenditure over a specific time of period. Budget is Financial statement or

estimation of revenue and expenses that can be made by a person, a business, a government or

an organisation. Financial department prepares the sheet to assists the department's head in

formulation of budget estimate. Manager discuss the plan for proposed level of activity. Top

management can work with the planned budget according to budget's financial circumstance and

prepare the estimate of forthcoming year. The complete budget are present by managers with the

approval of executive officers. Nero Ltd is used the same process to figure out the proposed

budget. They sets the expenditure level of all the products for every department. The estimate

figure are allocated to their target capital which are available for the project.

Operational budget:

It is a detailed prediction of all estimated income and expenses based on forecasted sales

revenue for a specific time of period. An operational budget is helps the Nero Ltd in the terms

for planning the day to day activities so they always know the working areas.

Advantages - Its advantages are to Nero Ltd to manage the current indirect expenses

which are paid on daily or monthly basis such as office rent, salaries, wages etc. This

budget helps for evaluating the current actual expenses and past expenses too. So they

can found the variation in the expenditure (Tucker and Lowe, 2014).

Disadvantages - It may have some disadvantages first it cover, it is time consuming

concepts especially for the poor organised company. There are not easily predetermined

of accurate data.

Master Budget:

It is a functional budget prepared by particular division of an organisation. Master budget

is sum of the all division's budget. It may includes income statement, balance sheet, cash flow

statement, fund flow statement of an organisation. Nero Ltd can prepare particular budget to

examine capital investment and manufacturing levels (Otley and Emmanuel, 2013) .

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Advantage - Advantages of this budget are well planning of every division 's function. It

is summery of all branches which is overviewed by the management. This budget help to

determines the long term goals of company.

Disadvantage - Master budget is an extravagant or big budgeted business strategy for

future sales, level of production, future expenses, capital investments. Disadvantage of

this budget are divisional staff are forced to achieve the target in spite of having practical

knowledge of the same task.

Zero based budget

Zero Based Budgeting is the process starts with the postulating that all the department

budget are zero. Nero Ltd's Manager are required to build the budget from ground up level

explaining every penny they want to spend. This is the process to creating budget from null

without using the prior budget or spending figure.

Advantages - Zero-based budgeting is a budgeting method that allocates the resource

based on efficiency and requirement rather than on budget history. It improves the

organisation performance and operating efficiency by examining future expenditures.

Disadvantage - To implicating a zero based budget require special training to personal

that is time consuming and costly. It may harm the brand image of Nero Ltd as it is

require new estimated data.

Pricing Strategies – In the business context, several types of pricing policies can help to

business in order to analysis of cost as well as expenditure where consist of various activities of

business. The Nero Ltd selecting two pricing policies to provide help to cover the cost of

product. The pricing strategy set of the company after analysing of market activities, there is

required to awareness of competitors. After collect information need to set prices f their products

in effective manners. As a result it can help to compete with their competitors and generate much

more profit.

Cost plus Pricing – It is considered to be most essential approach which is used by Nero

Ltd in order to fix cost of goods sold. In this method consist of overhead cost and

material to selling stocks.

Full costing pricing – It will include as practices of cost of a product which is determined

from as firms on the basis of their direct cost as per units.

9

is summery of all branches which is overviewed by the management. This budget help to

determines the long term goals of company.

Disadvantage - Master budget is an extravagant or big budgeted business strategy for

future sales, level of production, future expenses, capital investments. Disadvantage of

this budget are divisional staff are forced to achieve the target in spite of having practical

knowledge of the same task.

Zero based budget

Zero Based Budgeting is the process starts with the postulating that all the department

budget are zero. Nero Ltd's Manager are required to build the budget from ground up level

explaining every penny they want to spend. This is the process to creating budget from null

without using the prior budget or spending figure.

Advantages - Zero-based budgeting is a budgeting method that allocates the resource

based on efficiency and requirement rather than on budget history. It improves the

organisation performance and operating efficiency by examining future expenditures.

Disadvantage - To implicating a zero based budget require special training to personal

that is time consuming and costly. It may harm the brand image of Nero Ltd as it is

require new estimated data.

Pricing Strategies – In the business context, several types of pricing policies can help to

business in order to analysis of cost as well as expenditure where consist of various activities of

business. The Nero Ltd selecting two pricing policies to provide help to cover the cost of

product. The pricing strategy set of the company after analysing of market activities, there is

required to awareness of competitors. After collect information need to set prices f their products

in effective manners. As a result it can help to compete with their competitors and generate much

more profit.

Cost plus Pricing – It is considered to be most essential approach which is used by Nero

Ltd in order to fix cost of goods sold. In this method consist of overhead cost and

material to selling stocks.

Full costing pricing – It will include as practices of cost of a product which is determined

from as firms on the basis of their direct cost as per units.

9

TASK 4

Identify financial problems and apply appropriate techniques

In present time every organisation face different type of financial problem which can

become reason of stress. There is need to manage money in proper way and have appropriate

monetary resources to execute business activities and operations. Currently Cambridge

manufacturing Ltd is dealing with some of them. As a result, it can affect to company's

productivity and also profitability. All the money related problems of the company as follows - Late Payments by clients – Many time clients who can purchase commodities on credit

and take late payments which is become reason of financial issues. As a result it can

affect to efficient of business so it is essential to tighten the credit policy so that

outstanding money can be achieved by the entity on time (Renz, 2016).

Improper money management system – To conduct business activities it is required to

manage money in proper way but Nero Ltd can not manage as per the accounting

principles. To solve particular problem need to recruited hired skilled workers who have

knowledge of accounting and understand every situation easily.

The manager of Cambridge manufacturing Ltd are applied particular techniques to

recognise financial problem. These are as follows:

Benchmarking – The particular technique applied by company to achieve minimum

expected result. It is mainly applied to compare policies and practices of company with another

company to evaluate financial issues. Benchmarking can be used to identify problem of improper

money managements and late payments by customers through compare strategies of the

company with others. When company compare performance of Cambridge manufacturing

strategies and performance with another company that time get that selected company can not

proper manage of money transaction as a result it can affect to profitability.

KPI – The key performance indicator can be used by company to determine financial and

non financial information. As a result it can help to analysis of success and failure of the

processes that will be adopted by company. In Cambridge manufacturing Ltd use particular

technique to identify problem of improper money management system. It can assist to manager

how to determine unexpected expenditure that may take place in future (Sánchez-Rodríguez,

and Spraakman, 2012). Through this tool company can analysis financial and non financial

10

Identify financial problems and apply appropriate techniques

In present time every organisation face different type of financial problem which can

become reason of stress. There is need to manage money in proper way and have appropriate

monetary resources to execute business activities and operations. Currently Cambridge

manufacturing Ltd is dealing with some of them. As a result, it can affect to company's

productivity and also profitability. All the money related problems of the company as follows - Late Payments by clients – Many time clients who can purchase commodities on credit

and take late payments which is become reason of financial issues. As a result it can

affect to efficient of business so it is essential to tighten the credit policy so that

outstanding money can be achieved by the entity on time (Renz, 2016).

Improper money management system – To conduct business activities it is required to

manage money in proper way but Nero Ltd can not manage as per the accounting

principles. To solve particular problem need to recruited hired skilled workers who have

knowledge of accounting and understand every situation easily.

The manager of Cambridge manufacturing Ltd are applied particular techniques to

recognise financial problem. These are as follows:

Benchmarking – The particular technique applied by company to achieve minimum

expected result. It is mainly applied to compare policies and practices of company with another

company to evaluate financial issues. Benchmarking can be used to identify problem of improper

money managements and late payments by customers through compare strategies of the

company with others. When company compare performance of Cambridge manufacturing

strategies and performance with another company that time get that selected company can not

proper manage of money transaction as a result it can affect to profitability.

KPI – The key performance indicator can be used by company to determine financial and

non financial information. As a result it can help to analysis of success and failure of the

processes that will be adopted by company. In Cambridge manufacturing Ltd use particular

technique to identify problem of improper money management system. It can assist to manager

how to determine unexpected expenditure that may take place in future (Sánchez-Rodríguez,

and Spraakman, 2012). Through this tool company can analysis financial and non financial

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.