Comprehensive Management Accounting Report: Unicorn Grocery Case Study

VerifiedAdded on 2020/02/05

|18

|5880

|102

Report

AI Summary

This report provides a comprehensive overview of management accounting principles, focusing on their application within the context of Unicorn Grocery, a co-operative grocery store. The report begins with an introduction to management accounting, differentiating it from financial accounting and outlining key areas like performance, risk, and strategic management. It then delves into various management accounting systems, including job costing, inventory management, cost accounting, and price optimization systems. The report further explores different methods used for management accounting reporting, such as job costing reports, performance reports, inventory control reports, variable analysis reports, and budgets. A significant portion of the report is dedicated to the calculation and comparison of marginal and absorption costing methods, highlighting their differences and applications. The report also covers different planning tools for budgetary control and their uses in preparing budgets. Finally, the report discusses the adoption of management accounting systems to solve financial problems and ensure the sustainable success of an organization. The content includes detailed explanations, calculations, and evaluations, making it a valuable resource for understanding and applying management accounting techniques in a practical business setting.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Meaning of management accounting and different types of management accounting

systems...................................................................................................................................3

P2 Different methods that are used for management accounting reporting...........................5

M1 Benefits of management accounting systems.................................................................7

D1 Evaluation of management accounting systems and management accounting reporting 7

TASK 2............................................................................................................................................7

P3 calculation of cost using marginal and absorption costing and explaining the differences

between them..........................................................................................................................7

M2 Application of the range of management accounting techniques..................................11

D2 Interpretation of data for the business activities.............................................................11

TASK 3..........................................................................................................................................12

P4 Different types of planning tools that can be used for budgetary control.......................12

M3 Uses of different planning tools and their application for preparation of budgets........14

P5 Adoption of management accounting systems in order to solve financial problems......14

M4 sustainable success of the organisation by management accounting............................16

D3 use of planning tools for solving financial problems.....................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Meaning of management accounting and different types of management accounting

systems...................................................................................................................................3

P2 Different methods that are used for management accounting reporting...........................5

M1 Benefits of management accounting systems.................................................................7

D1 Evaluation of management accounting systems and management accounting reporting 7

TASK 2............................................................................................................................................7

P3 calculation of cost using marginal and absorption costing and explaining the differences

between them..........................................................................................................................7

M2 Application of the range of management accounting techniques..................................11

D2 Interpretation of data for the business activities.............................................................11

TASK 3..........................................................................................................................................12

P4 Different types of planning tools that can be used for budgetary control.......................12

M3 Uses of different planning tools and their application for preparation of budgets........14

P5 Adoption of management accounting systems in order to solve financial problems......14

M4 sustainable success of the organisation by management accounting............................16

D3 use of planning tools for solving financial problems.....................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

management accounting is the process by which timely and accurate reports are prepared

by the management in relation to statistical and financial data. The information recorded in the

process of management accounting is important for the management as this is used for the

purpose of making important decisions in relation to business (Kaplan and Atkinson, 2015). The

reports prepared in management accounting are required to be made on weekly or monthly basis

and they are only for the internal authorities such as chief executive officer or mangers of

different departments of the company. Unicorn Grocery is the co operative grocery store. It was

established in 1996 and is located in Manchester, England. The main purpose is to provide the

customers with range of fresh, affordable food. In this report, the matters in relation to

management accounting in Unicorn Grocery will be included. The various aspects that will be

discussed in this report will include meaning of management accounting, different types of

management accounting systems, and ways of reporting about management accounting.

TASK 1

P1 Meaning of management accounting and different types of management accounting systems

In order to achieve the goals that are set by Unicorn Grocery, various processes will be

required to be followed which will include measurement, identification, evaluation, interpretation

and communication of the relevant information (Macintosh and Quattrone, 2010). The

information which is obtained and the reports that are made in management accounting are done

for providing the managers of organisation with the relevant information that will help them in

taking the correct decisions for overall benefit of the company. Management accounting is

different from financial accounting as in it various financial aspects like balance sheet, taxation

are dealt with and also the reports of financial data are provided to the external world. There are

three main areas where management accounting extends and those areas are performance

management, risk management and strategic management. There are different types of

management accounting systems which are discussed below:-

1. Job costing system: - In the production process that is undertaken in any company, there

are various activities that are undertaken. In relation to them different types of jobs are

performed in respect of which various costs are incurred. The cost will be made on

cumulative basis and in order to calculate the per unit cost it will be required that all the

management accounting is the process by which timely and accurate reports are prepared

by the management in relation to statistical and financial data. The information recorded in the

process of management accounting is important for the management as this is used for the

purpose of making important decisions in relation to business (Kaplan and Atkinson, 2015). The

reports prepared in management accounting are required to be made on weekly or monthly basis

and they are only for the internal authorities such as chief executive officer or mangers of

different departments of the company. Unicorn Grocery is the co operative grocery store. It was

established in 1996 and is located in Manchester, England. The main purpose is to provide the

customers with range of fresh, affordable food. In this report, the matters in relation to

management accounting in Unicorn Grocery will be included. The various aspects that will be

discussed in this report will include meaning of management accounting, different types of

management accounting systems, and ways of reporting about management accounting.

TASK 1

P1 Meaning of management accounting and different types of management accounting systems

In order to achieve the goals that are set by Unicorn Grocery, various processes will be

required to be followed which will include measurement, identification, evaluation, interpretation

and communication of the relevant information (Macintosh and Quattrone, 2010). The

information which is obtained and the reports that are made in management accounting are done

for providing the managers of organisation with the relevant information that will help them in

taking the correct decisions for overall benefit of the company. Management accounting is

different from financial accounting as in it various financial aspects like balance sheet, taxation

are dealt with and also the reports of financial data are provided to the external world. There are

three main areas where management accounting extends and those areas are performance

management, risk management and strategic management. There are different types of

management accounting systems which are discussed below:-

1. Job costing system: - In the production process that is undertaken in any company, there

are various activities that are undertaken. In relation to them different types of jobs are

performed in respect of which various costs are incurred. The cost will be made on

cumulative basis and in order to calculate the per unit cost it will be required that all the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expenditure that have been made will have to be added. After that the total that will be

arrived will be needed to be divided by the total number of unite that are produced by

which per unit cost of the product will be ascertained.

2. Inventory management system: - In the manufacturing process, inventory is the most

important aspect that is required to be taken into consideration. There are various things

that should be controlled in this such as the quantity of stock that should be maintained

and the ordering time and level. It will be identified that how much inventory is needed

and at what time. On the basis of this orders will be placed. By this the problem of

shortage and surplus stock will be solved and there will be cost saving that will be

achieved.

3. Cost accounting system: - Perpetual accounting system will be used in the process of

recording. In the conduction of this system, five parts are present that are required to be

done in order to complete the whole process. At first the input that is required in the

manufacturing process will be required to be measured. Then the inventory that is used

will be valued by using various methods such activity based costing. All the cost that are

incurred will be accumulated in the next part of the system. After that all the assumptions

in relation to the cash flow will be made like which system to use in respect of inventory

that is FIFO or weighted average. At last all the capabilities will be recorded by using

perpetual or periodic methods.

4. Price optimisation system: - This system covers the price related aspect in which the

most profitable price will be fixed. After the cost will be ascertained, it will be required

that on the basis of that such price will be decided by which company will be able to

maximise its profit level together with the maintenance of demand. This is needed as the

relation between price and demand is inverse which means that with increase in price,

demand will be reduced and vice versa. So it will be required that appropriate method is

used in deciding price by which both company and customers will be benefited.

P2 Different methods that are used for management accounting reporting

There are various methods that can be used for the purpose of management accounting

reporting. Some of them are discussed below:-

1. Job costing report :- in case of management accounting by taking into consideration all

the cost in relation to various aspects such as production cost, overhead cost, labour cost

arrived will be needed to be divided by the total number of unite that are produced by

which per unit cost of the product will be ascertained.

2. Inventory management system: - In the manufacturing process, inventory is the most

important aspect that is required to be taken into consideration. There are various things

that should be controlled in this such as the quantity of stock that should be maintained

and the ordering time and level. It will be identified that how much inventory is needed

and at what time. On the basis of this orders will be placed. By this the problem of

shortage and surplus stock will be solved and there will be cost saving that will be

achieved.

3. Cost accounting system: - Perpetual accounting system will be used in the process of

recording. In the conduction of this system, five parts are present that are required to be

done in order to complete the whole process. At first the input that is required in the

manufacturing process will be required to be measured. Then the inventory that is used

will be valued by using various methods such activity based costing. All the cost that are

incurred will be accumulated in the next part of the system. After that all the assumptions

in relation to the cash flow will be made like which system to use in respect of inventory

that is FIFO or weighted average. At last all the capabilities will be recorded by using

perpetual or periodic methods.

4. Price optimisation system: - This system covers the price related aspect in which the

most profitable price will be fixed. After the cost will be ascertained, it will be required

that on the basis of that such price will be decided by which company will be able to

maximise its profit level together with the maintenance of demand. This is needed as the

relation between price and demand is inverse which means that with increase in price,

demand will be reduced and vice versa. So it will be required that appropriate method is

used in deciding price by which both company and customers will be benefited.

P2 Different methods that are used for management accounting reporting

There are various methods that can be used for the purpose of management accounting

reporting. Some of them are discussed below:-

1. Job costing report :- in case of management accounting by taking into consideration all

the cost in relation to various aspects such as production cost, overhead cost, labour cost

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and other costs, the cost of the product that is made is calculated (Albelda, 2011). This is

done by ascertaining the total cost that has been incurred and the number of goods that

are manufactured and after that they are required to be divided by which the cost in

association with the production of single product will be calculated. Then the cost report

will be prepared which will include all the information collected. With the help of this

report managers will be able to plan and control the profits being made as they will be

able to compare the cost of the product with its selling price.

2. Performance Reports: - With the help of budgets it will be possible for the managers to

compare the actual amount of incomes and expenses with that of the budgeted amounts.

By doing so they will be able to determine the variances that are present between both the

figures (Ajibolade, Arowomole and Ojikutu, 2010). While preparing new budgets all

these variances will be required to be analysed. Then the performance report will be

prepared taking into consideration all the information regarding these figures. With the

help of these reports managers will be able to evaluate the performance and also will be

able to plan in relation to the future production or any other aspect. Measures can be

taken to improve the performance in order to remove the limitations that are found in the

current position and all this can be achieved by studying these performance reports

properly.

3. Inventory control reports :- in these reports various aspects in relation to inventory will

be included. It will be analysed that what kind of the inventory is used and whether there

is any wastage that is taking place in this respect and if it is than the reason in this regard

is required to be ascertained (Arroyo, 2012). It will be ascertained that at what level the

inventory is required to be maintained or controlled so that Unicorn Grocery will be able

to reduce the cost and thereby increasing the profit level.

4. Variable analysis reports: - this is another type of report that will be required to be

prepared under the management accounting. In this report the variable aspects in relation

to the product will be required to be considered. Variable costs are those costs which

change with even a change of single unit in the production which means that if the

production of the goods will increase that the cost will increase and with decrease in

production the cost will also reduce. These costs will be required to be analysed as they

will affect the profits of the company to a large extent. Information regarding all these

done by ascertaining the total cost that has been incurred and the number of goods that

are manufactured and after that they are required to be divided by which the cost in

association with the production of single product will be calculated. Then the cost report

will be prepared which will include all the information collected. With the help of this

report managers will be able to plan and control the profits being made as they will be

able to compare the cost of the product with its selling price.

2. Performance Reports: - With the help of budgets it will be possible for the managers to

compare the actual amount of incomes and expenses with that of the budgeted amounts.

By doing so they will be able to determine the variances that are present between both the

figures (Ajibolade, Arowomole and Ojikutu, 2010). While preparing new budgets all

these variances will be required to be analysed. Then the performance report will be

prepared taking into consideration all the information regarding these figures. With the

help of these reports managers will be able to evaluate the performance and also will be

able to plan in relation to the future production or any other aspect. Measures can be

taken to improve the performance in order to remove the limitations that are found in the

current position and all this can be achieved by studying these performance reports

properly.

3. Inventory control reports :- in these reports various aspects in relation to inventory will

be included. It will be analysed that what kind of the inventory is used and whether there

is any wastage that is taking place in this respect and if it is than the reason in this regard

is required to be ascertained (Arroyo, 2012). It will be ascertained that at what level the

inventory is required to be maintained or controlled so that Unicorn Grocery will be able

to reduce the cost and thereby increasing the profit level.

4. Variable analysis reports: - this is another type of report that will be required to be

prepared under the management accounting. In this report the variable aspects in relation

to the product will be required to be considered. Variable costs are those costs which

change with even a change of single unit in the production which means that if the

production of the goods will increase that the cost will increase and with decrease in

production the cost will also reduce. These costs will be required to be analysed as they

will affect the profits of the company to a large extent. Information regarding all these

factors will be required to be mentioned in the variable analysis report that will be

prepared. Due to these factors the profits of the company will be directly affected so it is

very important for Unicorn Grocery to compulsorily take them into consideration.

5. Budgets :- Among many elements that are included in management accounting, budget

preparation is one of the most important aspect. In the preparation of budgets the Unicorn

Grocery will have to use the past years budgets and on the basis of the information

presented in them new budgets will be prepared by taking into consideration the future

projections also along with the past data (Hiebl, 2014). Budget will specify the targets

and objectives that are required to be achieved by the company and the expenses and

incomes are also mentioned in the budget. The company will try to maintain the

expenditures on the basis of the budgeted figures while performing its functions in

relation to the attainment of its objectives. The managers of the company will try to find

out the various alternatives in relation to reduction of the cost along with the increase in

the income so that they can maintain the limits that are listed in the budgets and can prove

themselves.

M1 Benefits of management accounting systems

There are various benefits of management accounting systems which are as follows :

decision making : with the help of management accounting systems that are applied an

organisation will be able make appropriate decisions and also they can evaluate the

outcomes in order to find out the shortcomings that are present in the business.

Reduction of expenditure : by following various management accounting systems an

organisation will be able to know about the actions in respect of which expenses are

required to be incurred and by this the expenditure on unwanted activities can be

ignored.

D1 Evaluation of management accounting systems and management accounting reporting

Unicorn grocery will use the accounting systems and than will evaluate them to find out

various thing which it will incorporate in its report which will be helpful for the management to

correct them. While evaluation it will be able to know the deviations of the actuals from the pre

defined objectives. The reasons for such deviations will be identified and then the various

accounting systems will be used to take the corrective actions. By doing so the effectiveness and

efficiency of the business will be improved.

prepared. Due to these factors the profits of the company will be directly affected so it is

very important for Unicorn Grocery to compulsorily take them into consideration.

5. Budgets :- Among many elements that are included in management accounting, budget

preparation is one of the most important aspect. In the preparation of budgets the Unicorn

Grocery will have to use the past years budgets and on the basis of the information

presented in them new budgets will be prepared by taking into consideration the future

projections also along with the past data (Hiebl, 2014). Budget will specify the targets

and objectives that are required to be achieved by the company and the expenses and

incomes are also mentioned in the budget. The company will try to maintain the

expenditures on the basis of the budgeted figures while performing its functions in

relation to the attainment of its objectives. The managers of the company will try to find

out the various alternatives in relation to reduction of the cost along with the increase in

the income so that they can maintain the limits that are listed in the budgets and can prove

themselves.

M1 Benefits of management accounting systems

There are various benefits of management accounting systems which are as follows :

decision making : with the help of management accounting systems that are applied an

organisation will be able make appropriate decisions and also they can evaluate the

outcomes in order to find out the shortcomings that are present in the business.

Reduction of expenditure : by following various management accounting systems an

organisation will be able to know about the actions in respect of which expenses are

required to be incurred and by this the expenditure on unwanted activities can be

ignored.

D1 Evaluation of management accounting systems and management accounting reporting

Unicorn grocery will use the accounting systems and than will evaluate them to find out

various thing which it will incorporate in its report which will be helpful for the management to

correct them. While evaluation it will be able to know the deviations of the actuals from the pre

defined objectives. The reasons for such deviations will be identified and then the various

accounting systems will be used to take the corrective actions. By doing so the effectiveness and

efficiency of the business will be improved.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3 calculation of cost using marginal and absorption costing and explaining the differences

between them

Marginal Costing :- In case of marginal costing variable costs are taken into

consideration so in this the change in the total cost of the product with the change of one unit of

the product will also be reflected. The marginal cost in relation to any product will be calculated

by taking into consideration the total of the direct labour cost, direct material cost and other

direct and variable expenses (Setthasakko, 2010). As there is direct relationship between the

variable cost and the production so the total variable cost will increase with the increase in

production of the product. In this form of costing the fixed cost is written off from the

contribution that will be obtained after deduction of total variable cost from the selling price of

the product.

Absorption costing :- in this form of costing the total cost of the product will be

calculated by taking into account all the costs that are incurred in the preparation of the final

product (Quinn, 2011). The cost will include direct material cost, direct labour cost, and in this

both the variable and fixed overheads will be included. Due to the this fact absorption costing

can also be called as full costing. After the collection of all the cost they will be required to be

allocated among different products that are manufactured. In case of absorption costing, for the

purpose of allocation of the cost in order to do the valuation of inventory activity based costing

can be used. The process of absorption costing will include performance of various steps. The

first step in this process will be the assignment of the cost that are incurred to the cost pools, then

the activity measure that is to be used or the allocation of the cost will have to be determined

along with the amount of usage and lastly the cost will be assigned on the basis of the usage

measures.

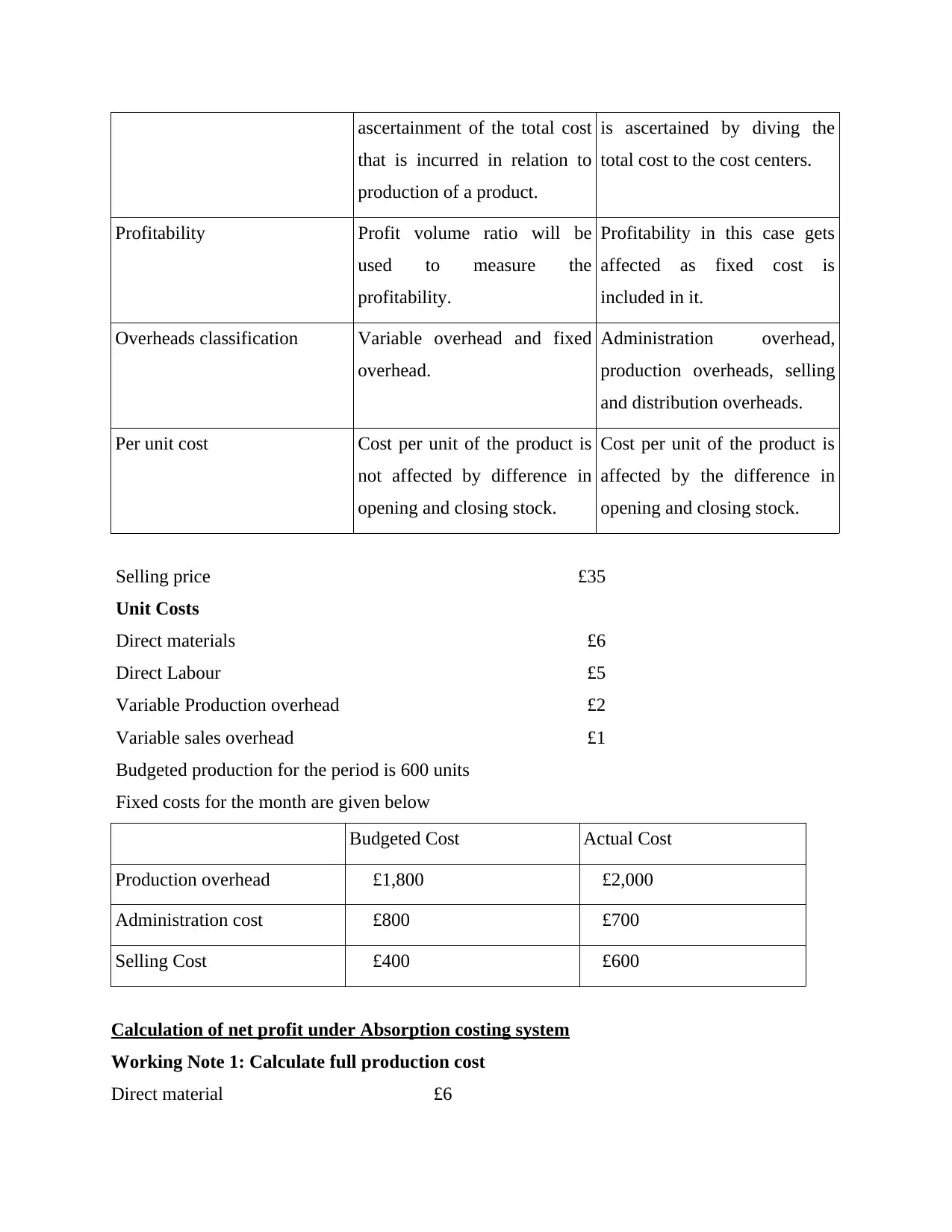

Marginal costing and absorption costing are different from each other in various aspects and the

same are described in the comparison table given below :

BASIS MARGINAL COSTING ABSORPTION COSTING

Meaning A decision making technique

that is used for the purpose of

The process in which the total

cost of production of a product

P3 calculation of cost using marginal and absorption costing and explaining the differences

between them

Marginal Costing :- In case of marginal costing variable costs are taken into

consideration so in this the change in the total cost of the product with the change of one unit of

the product will also be reflected. The marginal cost in relation to any product will be calculated

by taking into consideration the total of the direct labour cost, direct material cost and other

direct and variable expenses (Setthasakko, 2010). As there is direct relationship between the

variable cost and the production so the total variable cost will increase with the increase in

production of the product. In this form of costing the fixed cost is written off from the

contribution that will be obtained after deduction of total variable cost from the selling price of

the product.

Absorption costing :- in this form of costing the total cost of the product will be

calculated by taking into account all the costs that are incurred in the preparation of the final

product (Quinn, 2011). The cost will include direct material cost, direct labour cost, and in this

both the variable and fixed overheads will be included. Due to the this fact absorption costing

can also be called as full costing. After the collection of all the cost they will be required to be

allocated among different products that are manufactured. In case of absorption costing, for the

purpose of allocation of the cost in order to do the valuation of inventory activity based costing

can be used. The process of absorption costing will include performance of various steps. The

first step in this process will be the assignment of the cost that are incurred to the cost pools, then

the activity measure that is to be used or the allocation of the cost will have to be determined

along with the amount of usage and lastly the cost will be assigned on the basis of the usage

measures.

Marginal costing and absorption costing are different from each other in various aspects and the

same are described in the comparison table given below :

BASIS MARGINAL COSTING ABSORPTION COSTING

Meaning A decision making technique

that is used for the purpose of

The process in which the total

cost of production of a product

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ascertainment of the total cost

that is incurred in relation to

production of a product.

is ascertained by diving the

total cost to the cost centers.

Profitability Profit volume ratio will be

used to measure the

profitability.

Profitability in this case gets

affected as fixed cost is

included in it.

Overheads classification Variable overhead and fixed

overhead.

Administration overhead,

production overheads, selling

and distribution overheads.

Per unit cost Cost per unit of the product is

not affected by difference in

opening and closing stock.

Cost per unit of the product is

affected by the difference in

opening and closing stock.

Selling price £35

Unit Costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Cost Actual Cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling Cost £400 £600

Calculation of net profit under Absorption costing system

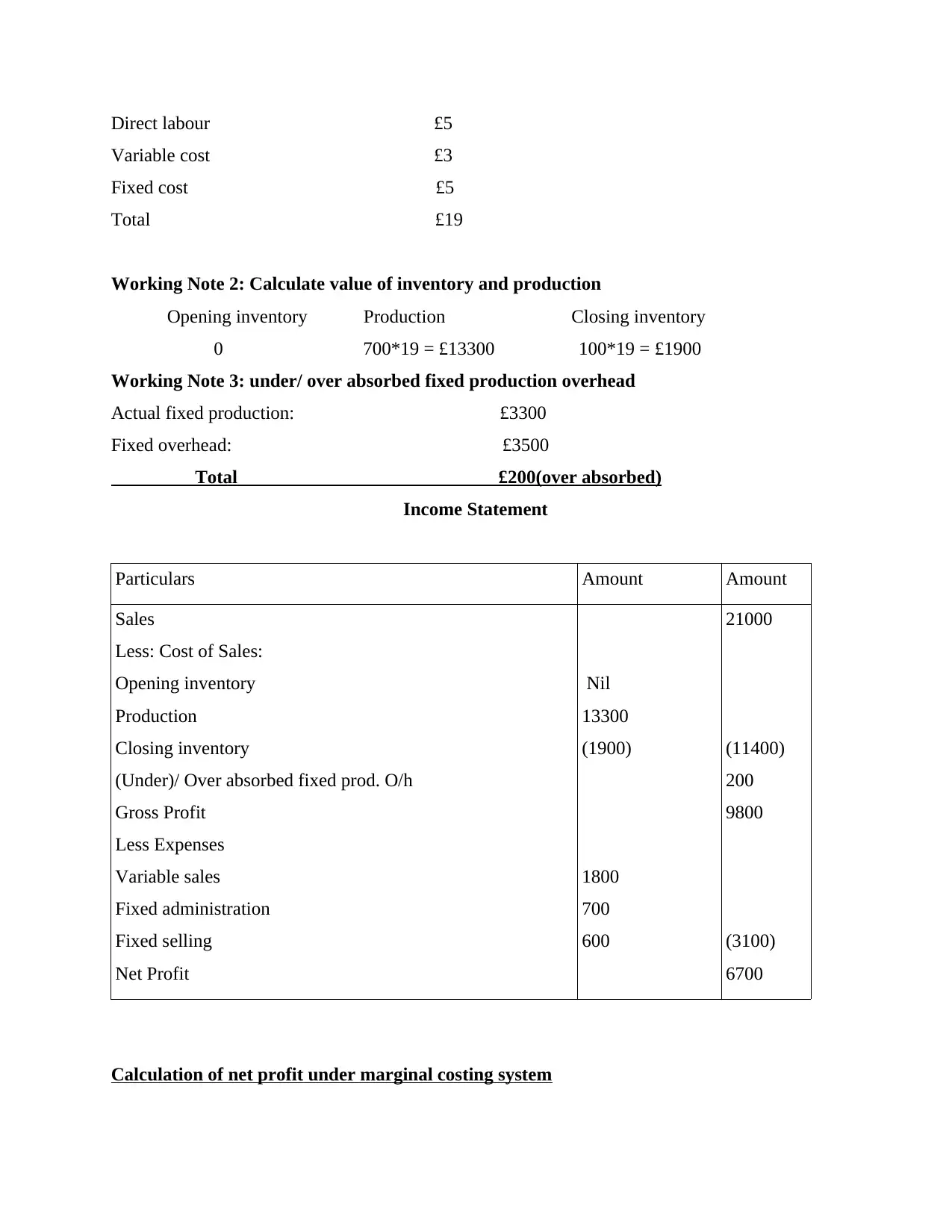

Working Note 1: Calculate full production cost

Direct material £6

that is incurred in relation to

production of a product.

is ascertained by diving the

total cost to the cost centers.

Profitability Profit volume ratio will be

used to measure the

profitability.

Profitability in this case gets

affected as fixed cost is

included in it.

Overheads classification Variable overhead and fixed

overhead.

Administration overhead,

production overheads, selling

and distribution overheads.

Per unit cost Cost per unit of the product is

not affected by difference in

opening and closing stock.

Cost per unit of the product is

affected by the difference in

opening and closing stock.

Selling price £35

Unit Costs

Direct materials £6

Direct Labour £5

Variable Production overhead £2

Variable sales overhead £1

Budgeted production for the period is 600 units

Fixed costs for the month are given below

Budgeted Cost Actual Cost

Production overhead £1,800 £2,000

Administration cost £800 £700

Selling Cost £400 £600

Calculation of net profit under Absorption costing system

Working Note 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Income Statement

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

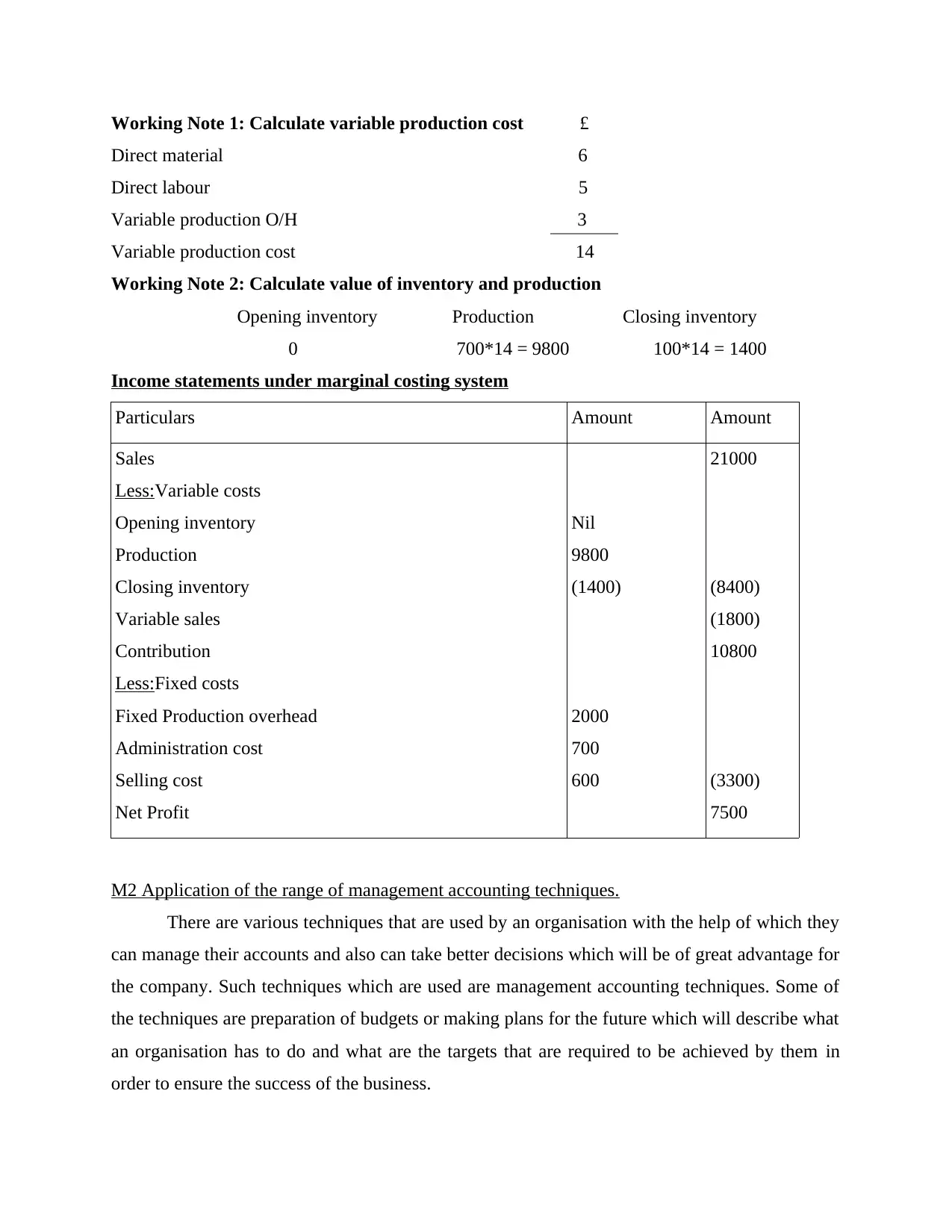

Calculation of net profit under marginal costing system

Variable cost £3

Fixed cost £5

Total £19

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*19 = £1900

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £3300

Fixed overhead: £3500

Total £200(over absorbed)

Income Statement

Particulars Amount Amount

Sales

Less: Cost of Sales:

Opening inventory

Production

Closing inventory

(Under)/ Over absorbed fixed prod. O/h

Gross Profit

Less Expenses

Variable sales

Fixed administration

Fixed selling

Net Profit

Nil

13300

(1900)

1800

700

600

21000

(11400)

200

9800

(3100)

6700

Calculation of net profit under marginal costing system

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Working Note 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Income statements under marginal costing system

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

M2 Application of the range of management accounting techniques.

There are various techniques that are used by an organisation with the help of which they

can manage their accounts and also can take better decisions which will be of great advantage for

the company. Such techniques which are used are management accounting techniques. Some of

the techniques are preparation of budgets or making plans for the future which will describe what

an organisation has to do and what are the targets that are required to be achieved by them in

order to ensure the success of the business.

Direct material 6

Direct labour 5

Variable production O/H 3

Variable production cost 14

Working Note 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Income statements under marginal costing system

Particulars Amount Amount

Sales

Less:Variable costs

Opening inventory

Production

Closing inventory

Variable sales

Contribution

Less:Fixed costs

Fixed Production overhead

Administration cost

Selling cost

Net Profit

Nil

9800

(1400)

2000

700

600

21000

(8400)

(1800)

10800

(3300)

7500

M2 Application of the range of management accounting techniques.

There are various techniques that are used by an organisation with the help of which they

can manage their accounts and also can take better decisions which will be of great advantage for

the company. Such techniques which are used are management accounting techniques. Some of

the techniques are preparation of budgets or making plans for the future which will describe what

an organisation has to do and what are the targets that are required to be achieved by them in

order to ensure the success of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2 Interpretation of data for the business activities.

Absorption costing and marginal costing are two techniques by which the cost of the

product can be calculated. It can be interpreted that the major difference between both the

methods is in relation to the allocation of the fixed overheads. In case of absorption costing profit

is calculated after the allocation of the whole fixed expenses whereas in marginal costing the

fixed expenses are not considered while calculation of the contribution. And due to this factor the

profits in both the cases are different like in the above mentioned problem the profit in case of

absorption costing is 6700 while in case of marginal costing is 7500 and the difference is due to

the allocation of fixed expenses.

TASK 3

P4 Different types of planning tools that can be used for budgetary control

The process by which the budgets are prepared in respect of the future times and after

preparation they are compared with the actual performance. By doing the comparison differences

between budgeted figures and actual figures are found and this process is known as budgetary

control (Hülle, Kaspar and Möller, 2011). With the help of the variances that are found,

management will be able to analyse them and take the corrective measures in order to remove the

differences that are found. The main objective of using budgetary control are that it defines that

is required to be done in order to achieve the objectives that have been set by Unicorn Grocery.

With thee help of it the coordination among various departments can be established and also with

the help of it profits of the company will be increased by the process of elimination of wastes.

Advantages of Budgetary control :-

unicorn grocery will be able to increase the profits by using budgetary control as it will

specify the goals and objectives that are required to be achieved.

With the help of it Unicorn grocery will be able to establish better coordination among

different departments.

Targets are fixed by the budgets and than various departments are required to work

effectively in order to achieve those targets.

Absorption costing and marginal costing are two techniques by which the cost of the

product can be calculated. It can be interpreted that the major difference between both the

methods is in relation to the allocation of the fixed overheads. In case of absorption costing profit

is calculated after the allocation of the whole fixed expenses whereas in marginal costing the

fixed expenses are not considered while calculation of the contribution. And due to this factor the

profits in both the cases are different like in the above mentioned problem the profit in case of

absorption costing is 6700 while in case of marginal costing is 7500 and the difference is due to

the allocation of fixed expenses.

TASK 3

P4 Different types of planning tools that can be used for budgetary control

The process by which the budgets are prepared in respect of the future times and after

preparation they are compared with the actual performance. By doing the comparison differences

between budgeted figures and actual figures are found and this process is known as budgetary

control (Hülle, Kaspar and Möller, 2011). With the help of the variances that are found,

management will be able to analyse them and take the corrective measures in order to remove the

differences that are found. The main objective of using budgetary control are that it defines that

is required to be done in order to achieve the objectives that have been set by Unicorn Grocery.

With thee help of it the coordination among various departments can be established and also with

the help of it profits of the company will be increased by the process of elimination of wastes.

Advantages of Budgetary control :-

unicorn grocery will be able to increase the profits by using budgetary control as it will

specify the goals and objectives that are required to be achieved.

With the help of it Unicorn grocery will be able to establish better coordination among

different departments.

Targets are fixed by the budgets and than various departments are required to work

effectively in order to achieve those targets.

Centralised control is established with the decentralised actions by using budgetary

control.

Disadvantages of budgetary control :-

Preparation of the accurate budgets is different under the changing environment.

Heavy expenditure is required to be incurred for the preparation of budgets and it is not

possible for the small businesses.

In case the management is not supportive than it will lead to the failure of the budgetary

control.

Different types of budgets :-

1. zero based budgeting :- In management accounting zero based budgeting is a approach

in which budget is prepared with the zero base (Salehi, Rostami and Mogadam, 2010). It

can be said that in zero based budgeting for the determination of expenses of new period

the actual expenses that will be incurred will have to be taken into consideration and no

reference to the past expenses will be provided. Justification in regards to all the activities

will be required to be provided and it will be explained that how much income will be

generated with respect to each cost.

Advantages of zero based budgeting :-

Efficiency : as in this historical data is not taken into consideration rather the actual

figures are considered so the allocation of the resources is more efficient.

Accuracy : I this reliance is not placed on the old figures. In fact the different

departments check each and every aspect of the cash flow and with the help of it cost of

operations is calculated.

Coordination : with the help of it the coordination and communication among all the

departments is increased which helps in motivating employees.

Disadvantages of zero based budgeting :-

as the budget is required to be made from the beginning it will require that large number

of employees should be there so it means will result in high manpower requirement.

This budgeting technique will lead to more time consumption of unicorn grocery as in

this new data is to be made every year.

control.

Disadvantages of budgetary control :-

Preparation of the accurate budgets is different under the changing environment.

Heavy expenditure is required to be incurred for the preparation of budgets and it is not

possible for the small businesses.

In case the management is not supportive than it will lead to the failure of the budgetary

control.

Different types of budgets :-

1. zero based budgeting :- In management accounting zero based budgeting is a approach

in which budget is prepared with the zero base (Salehi, Rostami and Mogadam, 2010). It

can be said that in zero based budgeting for the determination of expenses of new period

the actual expenses that will be incurred will have to be taken into consideration and no

reference to the past expenses will be provided. Justification in regards to all the activities

will be required to be provided and it will be explained that how much income will be

generated with respect to each cost.

Advantages of zero based budgeting :-

Efficiency : as in this historical data is not taken into consideration rather the actual

figures are considered so the allocation of the resources is more efficient.

Accuracy : I this reliance is not placed on the old figures. In fact the different

departments check each and every aspect of the cash flow and with the help of it cost of

operations is calculated.

Coordination : with the help of it the coordination and communication among all the

departments is increased which helps in motivating employees.

Disadvantages of zero based budgeting :-

as the budget is required to be made from the beginning it will require that large number

of employees should be there so it means will result in high manpower requirement.

This budgeting technique will lead to more time consumption of unicorn grocery as in

this new data is to be made every year.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.